Embed Size (px)

Citation preview

A Holistic Approach to Counterparty Credit Risk Management

November 2014

Speakers » Mehna Raissi is a Director in Product Management in the

Enterprise Risk Solutions group with Moody’s Analytics and has been with the firm for nearly six years. She manages the single obligor credit risk products suite which include RiskCalc™, CMM ™ (Commercial Mortgage Metrics) and LossCalc™. Mehna is responsible for the management and product innovation of these premier credit risk management tools. Mehna completed her Bachelors in Managerial Economics from University of California, Davis, and her MBA from University of San Francisco.

» Cristina Pieretti is a Senior Director in the Content group at Moody's Analytics based in New York and has been with the firm for six years. In her current role, she is responsible for the product management of CreditEdge ®. Prior to joining Moody’s Analytics, Cristina spent more than ten years in banking where she participated in multiple transactions in Latin America. Cristina holds an engineering degree and an MBA. She is also a CFA Charterholder.

Agenda Topics

Identifying credit risk challenges

Determining credit worthiness and implementing limits management

Applying early warning techniques and setting monitoring triggers

Importance of Credit Risk Management and Challenges

Counterparty Risk

Trading Risk

Buyer Risk

Vendor Risk

Risk-based Pricing

Benchmark

Limit

Setting

What and where are the risks?

Bad Debt

Miscalculation of capital reserves

Disruption to supply chain

Unforeseen

Challenges in C&I Risk Management

Data Quality & Availability

What is the data quality?

Standardized Processes

Ongoing Monitoring

Other Risk Drivers

Credit Risk Models

• Limited up to date data and ongoing availability

• Data captured at origination may not be complete for ongoing data analysis

• Data management is important for historical and forward looking analysis

• Storing data in a single system of record for consistency

• Improving operational controls by standardizing credit policies

• Setting up workflow processes to ensure systematic loan origination processes

• Improve credit origination decisions with accurate and predictive risk models

• Leveraging risk models for capital allocation and reserve setting

• Stress testing models that leverages baseline borrower risk

• Early warning indictor of risk deteriorations

• Dashboard reports showing borrower risk migration

• Setting limits based on risk levels

• Understand unexpected shifts that provide additional transparency

• Incorporate qualitative factors for a comprehensive analysis

How to minimize errors?

What are the most effective credit risk

tools?

How to manage counter-party risk?

What other factors should be taken into

consideration?

Determining Creditworthiness

How to address your credit and counterparty risk

Evaluate potential customer

Set credit limits and terms

Monitor exposures

Determine credit score

Perform sector analysis

Your process…

Choose counterparties with

credit quality

Your objectives…

Accurate and consistent pricing of

credit risk

Focus on riskiest exposures

Avoid overexposure to a sector Early warning

Your requirements…

High quality data Industry peer insight Standardized/ consistent process

Accurate models Transparent scoring

Effective monitoring system

Interpreting risk diagnostics that drive business decisions

» 1-Year and 5-Year EDF™ (Expected Default Frequency) credit measures and Implied Ratings

» Percentiles show the proportion of statements in the development sample that have lower (better) EDFs

» Mappings to Organizational Ratings

» Term structure outputs over five years providing short-term and long-term views

Relative Contributions provides risk driver insight

10

Ratio drivers point out many weaknesses firms financials

Compare a borrower against a peer group for additional transparency

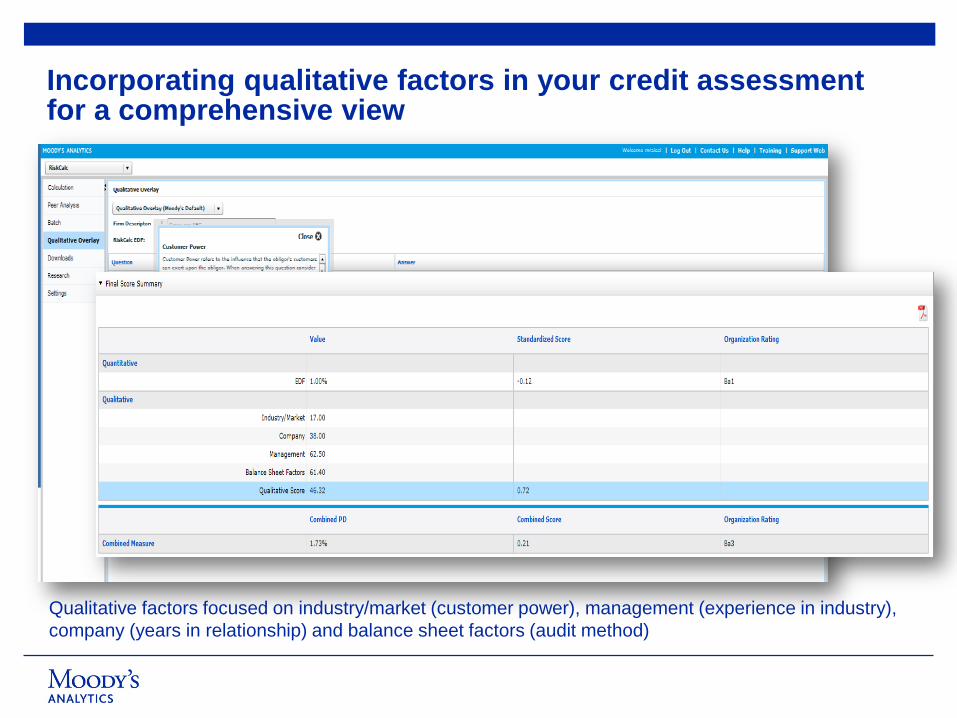

Incorporating qualitative factors in your credit assessment for a comprehensive view

Qualitative factors focused on industry/market (customer power), management (experience in industry), company (years in relationship) and balance sheet factors (audit method)

Setting limits that help manage business goals

» Pre-qualification module to streamline business operations

» Setting limits to manage concentration goals by Industry

» Risk based pricing to ensure systematic framework for tying risk to interest rates

Zero Limits Low Limits Medium Limits High Limits

0.02%

35.00%

0.50%

10.00%

2.00%

5.00%

1.00%

0.20%

EDF

0.05%

0.10%

Exposure

Early warning techniques and monitoring triggers

Can we detect potential defaulters early enough? One-Year Expected Default Frequency (EDF™) Measures

Best practices - Taking a closer look at monitoring credit risk and early warning

Default probabilities are ideal metrics for early warning

Expected Default Frequency (EDF) measures have the advantages of being:

» Point-in-time

» High frequency

» Granular

» Unbiased

» Global coverage

Best practices - Monitoring credit risk and early warning

EDF Level

EDF Change

Relative EDF Level

EDF Relative Change

Monitoring & Early Warning

Toolkit

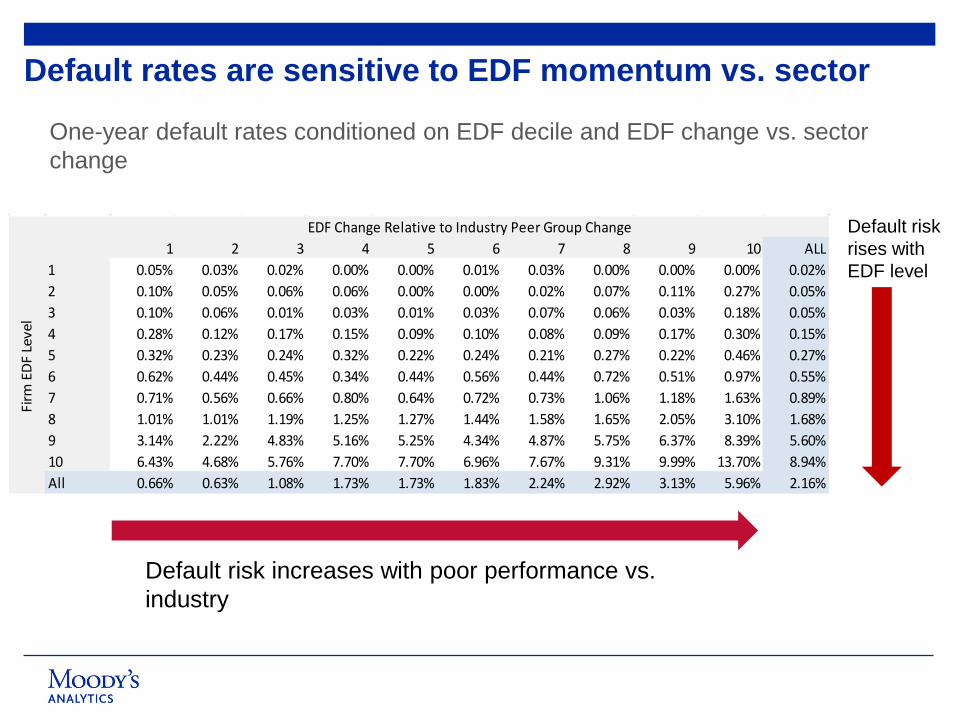

Companies that underperform their industry sectors historically experience much higher default risk

Historical Default Rates for Firms Whose EDFs Underperform their Sectors are Significantly Higher

Negative EDF momentum signals higher default risk One-year default rates conditioned on EDF momentum

Default rates are sensitive to EDF momentum vs. sector

One-year default rates conditioned on EDF decile and EDF change vs. sector change

1 2 3 4 5 6 7 8 9 10 ALL1 0.05% 0.03% 0.02% 0.00% 0.00% 0.01% 0.03% 0.00% 0.00% 0.00% 0.02%2 0.10% 0.05% 0.06% 0.06% 0.00% 0.00% 0.02% 0.07% 0.11% 0.27% 0.05%3 0.10% 0.06% 0.01% 0.03% 0.01% 0.03% 0.07% 0.06% 0.03% 0.18% 0.05%4 0.28% 0.12% 0.17% 0.15% 0.09% 0.10% 0.08% 0.09% 0.17% 0.30% 0.15%5 0.32% 0.23% 0.24% 0.32% 0.22% 0.24% 0.21% 0.27% 0.22% 0.46% 0.27%6 0.62% 0.44% 0.45% 0.34% 0.44% 0.56% 0.44% 0.72% 0.51% 0.97% 0.55%7 0.71% 0.56% 0.66% 0.80% 0.64% 0.72% 0.73% 1.06% 1.18% 1.63% 0.89%8 1.01% 1.01% 1.19% 1.25% 1.27% 1.44% 1.58% 1.65% 2.05% 3.10% 1.68%9 3.14% 2.22% 4.83% 5.16% 5.25% 4.34% 4.87% 5.75% 6.37% 8.39% 5.60%10 6.43% 4.68% 5.76% 7.70% 7.70% 6.96% 7.67% 9.31% 9.99% 13.70% 8.94%All 0.66% 0.63% 1.08% 1.73% 1.73% 1.83% 2.24% 2.92% 3.13% 5.96% 2.16%

Firm

EDF

Leve

l

EDF Change Relative to Industry Peer Group Change

Default risk increases with poor performance vs. industry

Default risk rises with EDF level

Monitoring the EDF Level Sears Holdings Corp.’s EDF measure has signaled heightened risk of default over the past year

Sears Holdings’ One-Year Expected Default Probability

Relative EDF level Sears Holdings Corp.’s default probability is among the highest in its industry sector

One-Year Expected Default Probability for Sears Holdings and its Industry Sector

90th Percentile

Relative EDF level Sears Holdings Corp.’s default probability is among the highest in its industry sector

One-Year Expected Default Probability for Sears Holdings and its Individual Peers

Set Alerts to Monitor PD Level, PD Change and Relative Performance

Best Practices - Risk Monitoring Template

EDF level

EDF change

Current Percentile

Rank Momentum

Putting It All Together

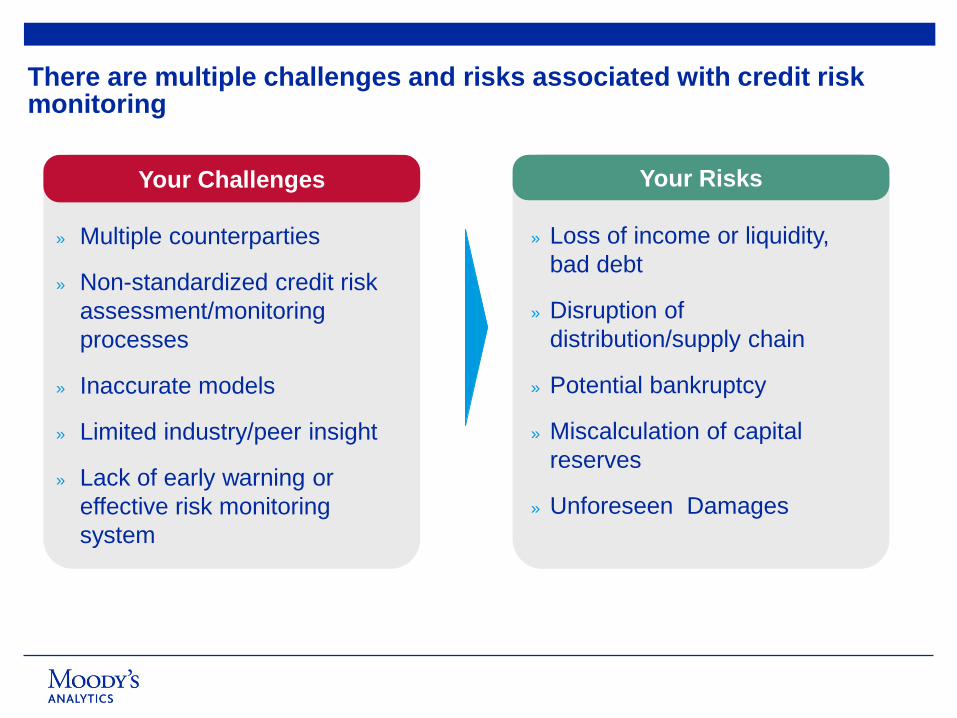

There are multiple challenges and risks associated with credit risk monitoring

Your Challenges

» Multiple counterparties

» Non-standardized credit risk assessment/monitoring processes

» Inaccurate models

» Limited industry/peer insight

» Lack of early warning or effective risk monitoring system

» Loss of income or liquidity, bad debt

» Disruption of distribution/supply chain

» Potential bankruptcy

» Miscalculation of capital reserves

» Unforeseen Damages

Your Risks

An Effective Credit Risk Monitoring System can be leveraged in several ways

Adherence to Accounting rules

» Calculate amortization schedules and credit reserves » Estimate credit impairments (OTTI) for investment

portfolios

» Accurately and consistently price credit risk » Avoid overexposures to a single client, industry or

region

Risk-Based Pricing & Limit Tracking

» Focus on riskiest exposures » Early detection of deterioration in the credit risk

of a counterparty

Credit Risk Monitoring & Early Warning

Downstream & Upstream Credit Risk

» Qualify new customers » Choose vendors and suppliers with high credit

quality

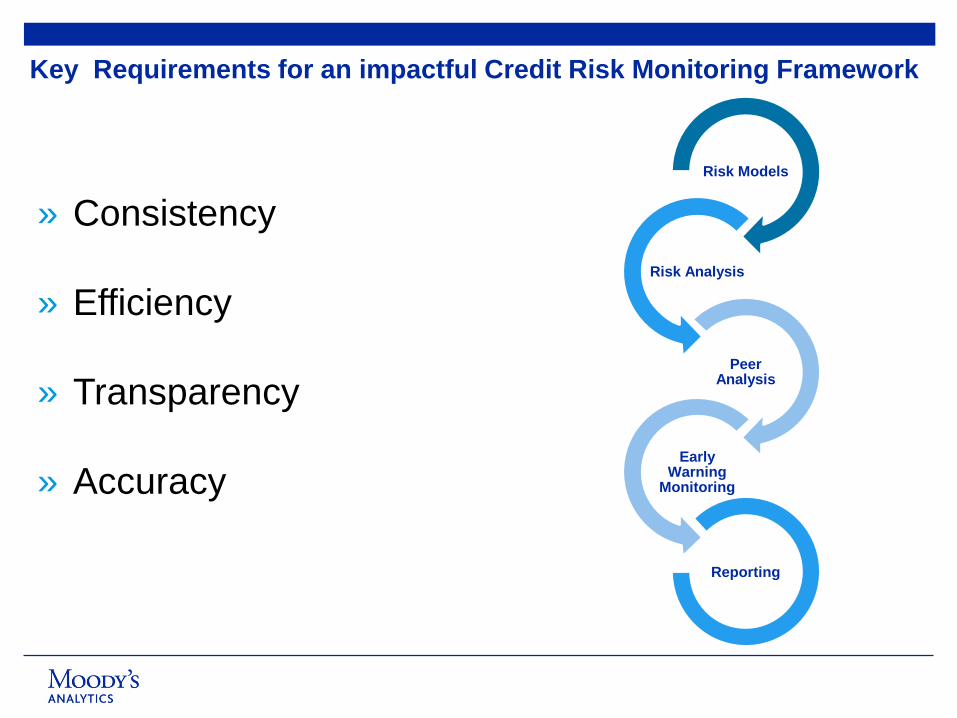

Key Requirements for an impactful Credit Risk Monitoring Framework

» Consistency

» Efficiency

» Transparency

» Accuracy

Risk Models

Risk Analysis

Peer Analysis

Early Warning

Monitoring

Reporting

Monitoring and early warning playbook summary Our research suggests a general approach to effective early warning using EDF measures:

EDF Level

EDF Change

Relative EDF Level

EDF Relative Change

Monitoring & Early Warning

Toolkit

Questions?