Week Ending 29th November 2015

1

NEFS Research Division Presents:

The Weekly Market

Wrap-Up

NEFS Market Wrap-Up

2

Contents Macro Review 3 United Kingdom

United States Eurozone

Australia & New Zealand Canada

Japan

Emerging Markets

10

India China Africa

Russia and Eastern Europe Latin America

South East Asia Middle East

Equities

17

Financials Oil & Gas

Retail Technology

Pharmaceuticals Industrials & Basic Materials

Commodities

Energy Precious Metals

Agriculturals

23

Currencies 26

EUR, USD, GBP AUD, JPY & Other Asian

Week Ending 29th November 2015

3

THE WEEK IN BRIEF

Thanksgiving and

Black Friday

Thanksgiving was celebrated in the US on

Thursday, and with consumers flocking to the

shops over the four-day celebration, retail sales

are expected to receive a boost. The holiday

has had an impact on energy prices, with

increased demand for gasoline and natural gas

causing what most expect to be a short term

recovery in prices. Meanwhile, Black Friday has

also helped retail sales, with many benefiting

from bargains both in store an online: Amazon

has reported record one-day sales in the UK,

while popular card game, Cards Against

Humanity, having great success in selling

absolutely nothing for $5, making $71,000!

Unemployment

falls in Japan

Japanese unemployment, now at 3.1%, hit a

twenty year low in October, coming in

considerably better than forecasts. Meanwhile

inflation, excluding oil costs, showed a 1.2%

annual increase. The news comes as a

confidence boost for Prime Minister Abe’s

government, and makes the potential for

quantitative easing much less likely than it

appeared last week.

Autumn Statement

spells out new cuts

This week George Osborne announced a

number of changes to government spending,

with major cuts to the budgets for Transport,

Business, Environment, Energy, and Culture

and Media, while spending on the NHS,

Education, International Aid and policing have

been maintained. The cuts come as the

chancellor hopes to cut the deficit, which has

repeatedly missed targets set by the

conservative government. However, following

the severe pressure on Osborne over his

planned tax credit cuts, in this week’s statement

the chancellor decided to scrap the proposed

changes completely. This means that the

government will almost certainly miss its target

for the level of welfare spending, for this, and

most likely for the next, fiscal year. With the UK

economy continuing to take time to recover, it

seems fair to expect the government to

continue to miss targets for the coming years,

heaping yet more pressure on Osborne to make

further cuts. It is clear that the government will

have to substantially increase tax revenue or

reduce government spending, or both, if it

wants to achieve a £10 billion budget surplus,

as targeted by the chancellor.

Jack Millar

NEFS Market Wrap-Up

4

MACRO REVIEW

United Kingdom

This week’s headline regards the release of the

Autumn Statement and Spending Review by

the Chancellor. The Autumn Statement is an

annual update on the government’s plan on

spending and taxation based on the economic

projections provided by the Office for Budget

Responsibility (OBR). The spending review

sets out the government’s spending plan for the

rest of this parliament, including spending on

infrastructure and governmental departments.

The key point is how the planned £20 billion of

cuts are distributed across government

departments. These cuts are necessary in

order to achieve the Chancellor’s promise of

eliminating the public sector deficit by 2020,

however the NHS, education and international

aid are protected from cuts. Also, due to

security concerns following the Paris attacks,

the police budget will not be reduced. The

summary of the main spending cuts include

Transport (-37%), Business (-17%),

Environment (-15%), Energy (-22%) Culture

and Media (-22%). Importantly the Chancellor

has scrapped his planned reduction in tax

credits following its defeat in the House of Lords

and the backlash from the public. The cuts

follow this government’s ongoing favour of

austerity to balance the books. All in all these

cuts are aimed to improve public finances and

achieve the Chancellor’s target of a budget

surplus of £10 billion by 2020. However, the

chart below illustrates that the Chancellor is

relying more on increasing tax receipts and

welfare cuts than cuts in public spending.

In other news, revisions by the Office of

National Statistics show that a widening trade

gap has had a record negative effect on third

quarter growth. While growth remained

unchanged at 0.5%, net trade knocked 1.5% of

main growth rate, with a 0.9% increase in

exports overshadowed by a 5.5% decrease in

imports, the most since records began in 1997.

This further highlights the imbalance in the

economy, and the UK’s reliance on domestic

consumption. Fortunately domestic spending is

experiencing robust growth due to zero inflation

and rising real wages. While this provides a

positive short term outlook it does highlight

inherent weaknesses in the UK economy and

competitiveness abroad.

Matteo Graziosi

Week Ending 29th November 2015

5

United States

It’s the annual Thanksgiving holiday this

weekend in the US. About 138.5 million

Americans will throng to the shops over the

four-day weekend (including online shoppers)

to take advantage of heavily discounted

consumer goods. Robust growth in the US

economy, especially on the consumer side,

should be reflected in sales figures.

The preliminary release of the real GDP growth

rate from the Bureau of Economic Analysis beat

forecasts of 2.0% to reach an annualised rate

of 2.1% for the third quarter. This was higher

than the initial estimated growth of 1.5% made

in the previous month. This GDP figure is the

second of three for the quarter, with the final

release in December when more information

can be incorporated. It is worth noting that it is

the first release, advance GDP growth data,

which has the biggest impact. Revisions for

third-quarter GDP resulted from the smaller

than previously estimated decrease in private

inventory investment.

Continuing on from strong macroeconomic

data, the US Census Bureau released data

showing durable goods orders rose by 3.0%

month-on-month, almost double forecasts of

1.6%. This is significantly higher than last

month’s decline of 0.8%. Durable goods orders

represent the total value of new purchase

orders placed with manufacturers for durable

goods (hard goods that have a life expectancy

of more than three years). It is a leading

indicator of production as rising purchase

orders signal that manufacturers will increase

activity as they work to fill the orders. Core

durable goods orders rose in line with forecasts

by 0.5% month-on-month. This is higher than

last month’s decline of 0.1%, shown in the

graph below. Orders for aircraft are volatile and

can severely distort the underlying trend and as

such are removed for core data. The core data

is therefore thought to be a better gauge of

purchase order trends. The aforementioned

strength in the US economy may be driving

companies to invest more in new equipment

following years of underinvestment due to

economic uncertainty.

Encouraging economic signs point towards an

interest rate rise in December to avoid potential

above-target inflation problems. Positive results

from next week’s data releases on the

unemployment rate, average hourly earnings

and non-farm payrolls should all but confirm the

imminent rate hike in December that the

markets have been predicting.

Sai Ming Liew

NEFS Market Wrap-Up

6

Eurozone

Consumer confidence in the EU has increased

from the revised figure of -7.5 last month to -5.9

for November, which measures the amount of

optimism consumers have about the economy.

This is shown on the graph of EU consumer

confidence below. Conversely, this increase in

consumer confidence in the Euro Area was

offset by a decline in EU business confidence.

The European commission announced this

week that the Business Climate Indicator, which

measures the level of confidence of the

businesses located in the Eurozone, fell from

0.44 in October to 0.36 in November 2015.

While it was expected that business confidence

would rise in November to 0.45, this was not the

case. The European commission advised that

these figures were collected prior to the Paris

attacks this month - it is expected that the

attacks will greatly reduce consumer and

business confidence within France and the

Euro area as a whole.

The largest increases in economic sentiment

about businesses were in services, which rose

from 12.3 in October to 12.8 in November, and

the construction sector, which increased from -

20.7 to -17.8 this month. German consumer

confidence declined for the sixth month in a row

from 9.4 to 9.3, which is the lowest figure

recorded since February 2015, but it still

managed to stay above the expectations of the

market. The cause for this fall in German

consumer confidence is mainly due to worries

about the German unemployment figures due

to be released, which are predicted to rise.

In other news, the European Commission this

week has advised the Eurozone, particularly

Germany and the Netherlands, to invest more

money in order to help increase the GDP

growth and the inflation rate in the Eurozone.

Both indicators have been disappointing over

the last few months, with negative inflation

being present alongside low GDP growth

figures. These two countries were singled out

due to the large current account surpluses they

possess: it is believed that, because they both

have a surpluses, they have the finance to

invest more. For example, in 2014 Germany

had a current account surplus as a percentage

of GDP of 7.8% - the commission rates a

surplus larger than 7% as excessive. The

European Commission stated that economies

such as Germany and the Netherlands need to

rebalance their economies away from their

reliance on exports. They believe that they

should invest more and encourage consumer

spending.

Kelly Wiles

Week Ending 29th November 2015

7

Australia & New

Zealand

This week we learned that Australia’s Private

Capital Expenditure depreciated significantly to

-9.2%, down from -4.0% in the previous quarter.

This came as a shock for forecasters who

predicted a -2.3% change. The Australian

Bureau of Statistics announced that total new

private capital expenditure had fallen to AUD

31.4 billion. The data pointed out that

investment in buildings and structures fell by

9.8% (at AUD 19.8 billion), while spending on

equipment, plant and machinery was down by

8.2% (at AUD 11.5 billion).

Capex (the money invested by a company to

upgrade or purchase physical, non-consumable

assets such as properties) is expected to be

21% lower in 2015-16 than it was in 2014-15.

Senior economist at RBC capital markets Su-

Lin Ong pointed out there’s “weakness across

the board, in services and capex”, as spending

on production plants haven’t changed a great

deal. As a result, such depreciations in

spending on key equipment may cause

downward expectations on growth figures, as

less capital expenditure may inhibit growth.

However, the downward pressure on Capex is

also believed to have been contributed to by the

sharp reductions in mining investment, as many

projects are reaching completion and therefore

recent investment has been low in the industry.

The Capex indicator is particularly useful as it is

helping to show how well the Australian

economy is transitioning from a mining to non-

mining economy.

Meanwhile, New Zealand’s trade balance came

in with promising prospects. Improving from the

NZD 1140 million deficit in September, the

trade balance came in at NZD -963 million in

October, as shown in the graph below. The

trade balance during this period tends to be its

lowest around this time of year.

A decline in imports by 2.2% was led by

reductions in petrol, avgas (aviation gasoline),

and capital goods. There were fewer large

plane imports during October, a potential

contributor to the decline. However, exports

also fell by 4.5%, owing to reductions in dairy

imports such as milk powder, butter and

cheese. Despite the reduction in the deficit for

the October months, compared to last year, the

deficit had widened slightly, up from -892

million.

China has been a key player in this. China’s

demand for dairy products spurred the changed

in dairy exports. The amount of milk powder

exported to China fell by 65%, but still remains

the most-exported commodity.

Meera Jadeja

NEFS Market Wrap-Up

8

Canada

“Going forward, the risks to the Canadian

outlook remain tilted to the downside” according

to Bill Morneau, Canada’s new Finance

Minister, who spoke at a press conference, also

noting that other G-20 countries face similar

conditions. According to the Bank of Canada

(BoC), real GDP is expected to grow by 2% in

2016, and 2.5% in 2017. The central bank’s

view is that slow growth in Canada is due to

weaknesses in the global economy. Reiterating

this in a presentation this week, Lynn Patterson,

the BoC’s Deputy Governor, stated that the

forecast increase in growth is likely to be due to

increases in non-energy exports and

investment. The chart below shows the

forecasted takeover of energy exports by non-

energy and non-commodity exports.

Weakness in the global economy is particularly

significant for Canada, as Canada is reliant on

trade in two senses: firstly, commodity exports,

of which prices are largely driven by growth in

China, and secondly, exports to the US. The

recovery of oil prices is expected to be slow,

with forecasts estimating that it is unlikely that

prices will reach USD 60 per barrel even by

2018. Last week, the Canadian Dollar fell below

USD 0.75 on the same day that the price of

crude oil dropped below USD 40 per barrel.

A report by CIBC World Markets has

highlighted that in order to stimulate growth

over the next decade, Canada will need to

produce high-value products and improve skills,

thereby diversifying its economy. Improving

skills is particularly important, as highlighted in

a report by Capital Economics that the number

of high-paying jobs in Canada has been

declining for the first time since the 2008

financial crisis. Unemployment has been high in

energy-reliant provinces such as Alberta and

recent employment creation has mostly been in

temporary or part-time work.

There may be some good news however.

Increasing speculation that the US Federal

Reserve will raise interest rates soon is a sign

of an improving US economy, and as Canada’s

biggest trading partner, US growth should help

Canadian exports. Next week the Bank of

Canada’s Governing Council will meet to

decide whether to change the current interest

rate of 0.5%. Low interest rates alongside a

weak Canadian dollar are helping to keep

growth going at the moment, however this is yet

to spur the much-needed surge in private

investment.

Shamima Manzoor

Week Ending 29th November 2015

9

Japan

The latest unemployment rate for October,

released on Thursday, indicates that the labour

market remains tighter than ever, at 3.1%.

Below the 3.4% previously forecast, this is the

lowest jobless rate Japan has seen since July

of 1995, as shown on the graph below. The

strength of Japanese manufacturing has been

at the forefront of this. The preliminary

Purchasing Managers’ Index (PMI) reading of

52.8 indicates an expansion of the sector at its

fastest pace in over 18 months, boosting

employment. In theory, a buoyant labour

market would lead firms to increase wages for

workers but Japanese firms remain cautious in

the midst of the slowing emerging markets and

weak export growth.

Japan’s lacklustre wage growth has become

very visible in the latest household spending

figures. Falling by 2.4% compared to last year,

weak household expenditure in an economy

with 1.24 applicants for every job, is a clear sign

that it is domestic consumption is a significant

drag for growth and the reflation of the

economy. On Wednesday Prime Minister

Shinzo Abe called for a 3% increase to the

minimum wage, which he hopes will increase

wage growth, stimulate consumer spending

and create inflation.

Inflation data released this week, as measured

by the core CPI, shows a 0.1% reduction of the

price level annually. However, an alternative

indicator of inflation released by the Bank of

Japan, which strips out the effect of lower oil

costs, shows a 1.2% increase in the price level.

In addition to the optimism expressed by the

Bank in recent months, this gives further

indication that the BoJ is unlikely to change their

monetary policy in the short-term, as their

measure supports an improving underlying

inflation trend since 2013. A recent poll by

Reuters shows that economists are split on

whether more quantitative easing will follow at

the start of next year.

On Friday PM Abe called on his Cabinet to

compile a budget for additional fiscal spending.

The extra budget for April 2016 will aim to tackle

the effects of both the declining population and

the impact of trade diversion on sectors

affected by the Trans-Pacific Partnership free

trade agreement.

No longer considering deflation as a top priority,

the Japanese government seems be focused

on the wider revitalisation of the economy.

Given the diminishing returns of QE this could

mean a permanent shift toward fiscal policy and

structural reforms.

Loy Chen

NEFS Market Wrap-Up

10

EMERGING MARKETS

China

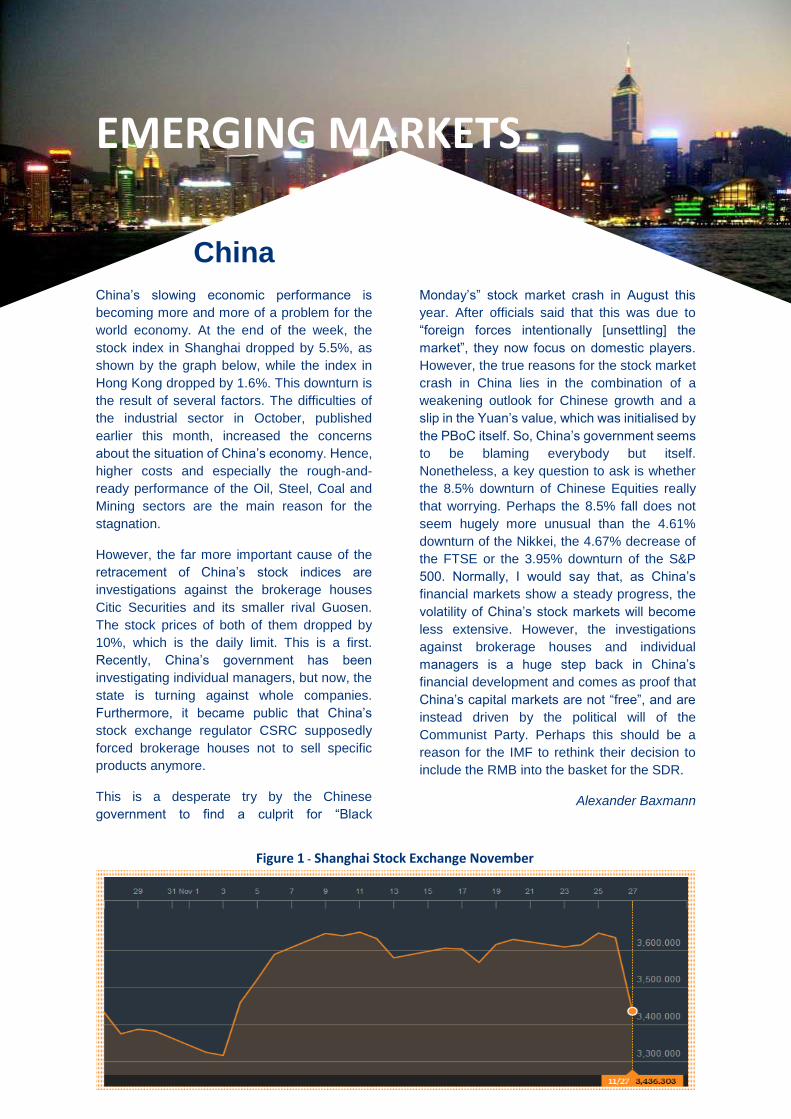

China’s slowing economic performance is

becoming more and more of a problem for the

world economy. At the end of the week, the

stock index in Shanghai dropped by 5.5%, as

shown by the graph below, while the index in

Hong Kong dropped by 1.6%. This downturn is

the result of several factors. The difficulties of

the industrial sector in October, published

earlier this month, increased the concerns

about the situation of China’s economy. Hence,

higher costs and especially the rough-and-

ready performance of the Oil, Steel, Coal and

Mining sectors are the main reason for the

stagnation.

However, the far more important cause of the

retracement of China’s stock indices are

investigations against the brokerage houses

Citic Securities and its smaller rival Guosen.

The stock prices of both of them dropped by

10%, which is the daily limit. This is a first.

Recently, China’s government has been

investigating individual managers, but now, the

state is turning against whole companies.

Furthermore, it became public that China’s

stock exchange regulator CSRC supposedly

forced brokerage houses not to sell specific

products anymore.

This is a desperate try by the Chinese

government to find a culprit for “Black

Monday’s” stock market crash in August this

year. After officials said that this was due to

“foreign forces intentionally [unsettling] the

market”, they now focus on domestic players.

However, the true reasons for the stock market

crash in China lies in the combination of a

weakening outlook for Chinese growth and a

slip in the Yuan’s value, which was initialised by

the PBoC itself. So, China’s government seems

to be blaming everybody but itself.

Nonetheless, a key question to ask is whether

the 8.5% downturn of Chinese Equities really

that worrying. Perhaps the 8.5% fall does not

seem hugely more unusual than the 4.61%

downturn of the Nikkei, the 4.67% decrease of

the FTSE or the 3.95% downturn of the S&P

500. Normally, I would say that, as China’s

financial markets show a steady progress, the

volatility of China’s stock markets will become

less extensive. However, the investigations

against brokerage houses and individual

managers is a huge step back in China’s

financial development and comes as proof that

China’s capital markets are not “free”, and are

instead driven by the political will of the

Communist Party. Perhaps this should be a

reason for the IMF to rethink their decision to

include the RMB into the basket for the SDR.

Alexander Baxmann

Figure 1 - Shanghai Stock Exchange November

Week Ending 29th November 2015

11

India

Prime Minister Modi was once again on his

travels this week, gracing Singapore with his

presence in light of fifty years of relations

between the two countries. During his visit Modi

stressed the importance of making

improvements to India’s business environment

for foreign investors via a number of different

reforms. However, a report released this week

by Moody’s, a global ratings agency,

encouraged the government to push more

aggressively for domestic economic reforms,

warning that a loss of momentum as a result of

delays could hamper investment amid weak

global growth.

Since Modi took office 18 months ago, he has

been on a mission to improve the country’s

economy, as well as create a business friendly

economic climate. It would be unfair to say that

he has not succeeded in doing so, relaxing

foreign direct investment (FDI) norms in 15

sectors and seeing a 40% increase in FDI since

he was elected. However, attention must now

shift to domestic reform, which has been a

cause for frustration for the government all

year. The report released by Moody’s said “The

Modi administration so far this year has been

unable to enact legislation on key reforms,

including a unified goods and services tax

(GST) and the Land Acquisition Bill.”

Implementing GST is crucial for India, not just

to garner higher taxes, but also to restore its

brand amid losing investor sentiment owing to

slacking reforms. By triggering higher

consumption through a unified tax system, India

will also see industrial investments rise in order

to meet demand. Some economists estimate

that the combination of these two components

could promote a 1.5 to 2% increase in GDP

growth, but only timely implementation of the

bill will allow it to become a reality.

The loss of momentum as a result of delays

referred to by Moody’s can in part be seen in

the results of a recent survey of 400 businesses

taken by the MNI Indicators Business

Sentiment index. Not even Diwali could boost

business sentiment, as it dropped from 62.3%

to 60.9% in October. This is about 12% down

from a year earlier, as the graph shows, and is

at the lowest level since February 2014.

Talking about reforms has proven effective to a

certain extent, but now is the time to implement

them on a vast scale. Whilst Modi has no issue

selling reforms to the rest of the world,

persuading Parliament to adopt them is

something he is yet to master.

Homairah Ginwalla

NEFS Market Wrap-Up

12

Africa

In a controversial turn of events, South Africa

has decided to lift its 2009 domestic rhino horn

trade ban. Many South African rhino breeders

argue that, since the ban, costs to protect herds

from poachers have increased massively,

hence destroying all profits and leading many to

sell their rhinos at huge costs. Those in favour

of lifting the ban argue that local rhino

businesses and their workers will be protected,

thus helping the economy. Moreover there is

evidence to suggest that the recent surge is

rhino poaching is directly related to the ban,

with the ban having created an underground

market with augmented prices and therefore

increased poacher incentives. From 2005 to

2009, 36 rhinos were killed on average per

year, whereas in 2014 alone, 1,215 rhinos were

killed. It is hoped that, by removing the ban,

prices will fall and poaching will decrease. This

will also be achieved through selling the vast

government stockpile of obtained rhino horns.

Finally, if the trade is legalised, the authorities

will be able to monitor poaching and ensure it is

carried out to legal standards. As a result, it is

hoped that legalisation will instead act to protect

rhino numbers.

In Rwanda, an 8.5 megawatt solar-power plant

has been completed in under a year,

consequently deeming it Africa’s fastest solar-

power project. It is clear evidence of Rwanda’s

successful economic growth, in being able to

quickly raise funds for projects. The $23.7m

solar field is 20% more efficient than normal, by

using computers that allow the panels to follow

the sun’s path. The construction of the plant

provided 350 local jobs and currently powers

over 15,000 homes in a 9km radius, increasing

Rwanda’s generating capacity by 6%. In

Rwanda’s rapidly expanding economy, as

shown in the graph below, increasing civilian

access to power and investment in

infrastructure is considered crucial for further

expansion. Politicians hope that by storing the

energy and selling it to other countries, as seen

already with Oslo, it will further boost the

economy and kick-start the creation of other

solar-power plants, to meet global

consumption. This will utilise a valuable African

asset - solar-power. However, critics argue that

the energy will eventually end up going only to

rich Western economies, and not to African

civilians. Furthermore, if more solar-power

plants are created, this will take up valuable

land needed to grow crops.

Charlotte Alder

Week Ending 29th November 2015

13

Russia and Eastern

Europe

Less of a focus on Russia this week and more

on Eastern Europe as a whole, after the

controversy surrounding the Turkish downing of

a Russian jet.

The Russian reaction to the downing of a

military jet allegedly over Turkish airspace has

dominated news this week, highlighting the

current worldwide political tension permeating

our households. Unsurprisingly, this event is

likely to carry with it substantial economic

effects. The Russian Prime Minister,

Medvedev, announced that Russia would be

imposing sanctions aimed at thwarting Turkey’s

economy. Supported by Putin, the sanctions

will target trade, tourism and joint investment

projects between the two countries in response

to what Russia is calling, “an act of aggression”.

The announced plans include bans on Turkish

business in Russia, a halt on the construction of

a sub-Black Sea natural gas pipeline and the

removal of Russian funds in the building of a

nuclear power station in Turkey. These seem

harsh and one might expect the Turkish to

respond apologetically, however the retort has

been one of defiance, with Mr Erdogan,

President of Turkey, claiming that Turkey can

find help elsewhere.

Russia and Turkey have engaged in $28 billion

worth of trade with each other from January to

September of this year. Consequently, the

economic ailments that these sanctions will

carry are bound to have an effect on the Turkish

economy. Erdogan had planned to triple trade

volumes to $100 billion by 2020 – an unlikely

reality, it would now seem. In addition, Russia

had been instrumental to Turkey’s economic

growth in her provision of numerous investment

opportunities, all of which were burgeoning, and

now at risk. It is estimated that Turkey could

lose $12 billion from the sanctions. To underline

the severity of this loss, we must realise that it

would amount to 2.6% of annual GDP.

Putin has advised Russians in Turkey to leave,

and for those planning a trip to change their

schedules. For those who do not take heed of

his warnings, he has tightened control on the

Russia-Turkey border, making it extremely

difficult for exchange of persons across. This is

of great significance when we consider that

Russians account for one tenth of tourism in

Turkey (worth $2.7 billion). Tourism revenues

(shown in the graph below) are likely to

substantially decrease.

The measures seem harsh but defiant, and

Turkey’s resilience is inspiring. One might note,

however, that the current economic climate

cannot afford to have two major economies

going head to head.

Tom Dooner

NEFS Market Wrap-Up

14

Latin America

Luis Diaz, head of the Democratic Action party

in the town of Altagracia de Orituco in central

Venezuela, was shot while he was meeting with

locals on Wednesday. Opposition leaders

blamed militias supporting the governing United

Socialist Party of Venezuela (PSUV). Yet the

current President Nicolas Maduro has so far

made no public comment.

Democratic Action is part of the opposition

Democratic Unity coalition about to contest a

December 6 election for a new National

Assembly in Venezuela. So this controversy

comes at a time when tensions are running high

- polls show the coalition has a good chance of

wresting the legislature from the ruling

socialists for the first time in 16 years.

Support for the Socialist Party is dwindling, as

poor economic policy and increasing homicide

rates (see graph featured at bottom of page)

have led to increased poverty and public unrest.

At first Maduro used the country’s vast oil funds

to provide public services and subsidised fuel,

which helped him to gain the public’s support.

However, economic mishandling has made

society poorer, widening the gap between the

rich and the poor, causing many to be driven

towards crime. At the institutional level, the

police force is underfunded and suffers from

high levels of corruption. Furthermore the

judicial system is poor and again shrouded in

corruption, there aren’t as many courts and

judges as there should be and the correct

decisions are not being made. As a result,

violent crime reigns. For example, look at

Caracas, the capital of Venezuela - it has a

homicide rate of 82 per 100,000, more than ten

times the global average.

Venezuela continually tries to shift blame to

neighbouring Colombia - one can only assume

that the reason behind Maduro’s activity is to

boost patriotic sentiment in order to increase

confidence in his party. However, for the

emerging economy to truly prosper, it must

address its current issues at the core through

economic reforms instead of turning to others

for an excuse. Furthermore, with an annual

GDP growth rate of -4% and the last recorded

inflationary figure at 68.5%, whichever party

wins the election has major economic and

crime issues to solve.

This also comes at a time when in his first press

conference as Argentinean President last

Monday, the centre-right Mr Macri said that he

would seek Venezuela’s suspension from

regional Mercosur trade bloc over rights abuses

committed by President Maduro’s

administration.

Max Brewer

Week Ending 29th November 2015

15

South East Asia

Amando Tetangco, the current governor of the

Philippine Central Bank for the past 11 years,

has been criticised for his inattention to detail

and devotion to a particular hobby - video

games. However, whether down to a

combination of skilful economic analysis and

common sense, or just luck, Tetangco

continues to take a prudent approach which has

led to the emergence of Philippines as South

East Asia’s fifth largest economy.

Tetango has recently announced that the

macroeconomic policies and structural reforms

in the Philippines are carefully considered and

approached cautiously. Perhaps Tetango’s

greatest achievement is his implementation of

sensible policies with huge long-term benefits,

whilst working with two governments over the

past 11 years. He states that this approach will

not change even when there will be a change in

government next year.

In the past 5 years, Aquino’s reign has seen

spending on education and infrastructure

double, whilst healthcare tripled, surpassing

competing Asian countries such as Singapore

and Malaysia. This highlights the Philippines’

commitment to its young population, with the

expected population to reach 140 million in the

next thirty years which shows that country has

the potential for its services sector to expand

massively. Additionally, the construction sector

has also picked up, due increases in

government spending on infrastructure - more

jobs will lead to further rises in consumer

spending.

However, it seems that the Philippines still has

a long way to go, as it has been revealed that

the poor infrastructure cost to the economy is

$60 million a day, which will certainly deter

multinational companies from outsourcing to

the Philippines: poor roads and airport

developments will lead to high costs, impacting

on profits. Moreover, an average journey on the

road takes around 45 minutes due to the heavy

congestion which creates further problems,

particularly if the Philippines want to compete

with the world’s fastest growing foreign direct

investment location, Vietnam.

Overall, the real question is whether the

Philippines can continue to take this long-term

approach, which has seen annual GDP exceed

China’s in recent cases, or whether the next

year’s new government will make radical

changes (that Tetangco will certainly not be

content with). Whatever happens, it is clear the

Philippines do not want to return back to the

dark days when it was branded ‘the sick man of

Asia’ by many economists, riddled with

corruption and bureaucracy.

Alex Lam

NEFS Market Wrap-Up

16

Middle East

A week after the prediction of an 8% growth rate

by the Iranian Central Bank governor in 5 years’

time, many claim the view to be unrealistic,

given the 2% current annual GDP growth in

Iran. Growth is expected to stall again, thanks

to low oil prices and rising unemployment. The

unemployment rate is moving in the wrong

direction, rising to 10.9% in the last quarter, and

is expected to maintain the upward trend in

2016.

Iran's Statistics Centre has announced the

inflation rate in Iran's urban areas for this month

to be 13.1%, 0.2% less than the preceding

month. The centre said that the consumer price

index (CPI) in Iran's urban areas is 0.7% more

than in the previous month. Scrutinising the

different sectors, the index for foods, drinks and

tobacco products has shown an increase of

0.3% compared to the month before, and a

growth of 7.9% when compared to the same

time last year - the index for services and non-

edible goods hit 209.7. According to the revised

estimates of Trading Economics, the inflation

rate in Iran is forecasted to be near 14% in the

last quarter of 2015 before it falls, and then

fluctuates between 9% and 10% in 2016.

Meanwhile, this week Dubai was confirmed to

host the world expo 2020, thus entering the

phase of increased activity. There has been an

upward revision of the growth forecasts of the

country: GDP Growth Rate in the UAE is

expected to be 3.88% by the end of this quarter,

while by 2020, the UAE GDP Growth Rate is

projected to trend around 4.94%. This growth is

expected to come along with an improvement in

infrastructure and a fall in the unemployment

rates. In the next few years, 275,000 jobs are

estimated to be created in and around the

region to service the Expo, across sectors.

Overall the positive halo effect of the Expo 2020

Dubai will leave behind a strong transformative

social and economic legacy across the region.

However, there is a growing fear of the debt led

growth of the economy whose reduced prices

of Oil and diesel are now taking a huge toll on

government revenues. The Country has

witnessed a 2% increase in the Debt to GDP

ratio in the last quarter of 2015. This trend could

hamper the long run growth prospects of the

economy.

Sreya Ram

Week Ending 29th November 2015

17

EQUITIES

Financials

This week in the financial industry saw four

senior partners of KMPG arrested in their

Belfast office after allegedly evading tax. This

was a blow for the company’s reputation in

Northern Ireland after they supposedly moved

from Dublin so the staff could “better perform

day-to-day tasks”. Elsewhere, Spanish BBVA

has bought a 30% stake in the British

challenger bank, Atom. BBVA believe there is a

gap in the market for a bank with few legacy

cost structures or systems to grow. The market

reacted well to the news with BBVA’s share

price increasing 3.2% this week.

Brazil’s biggest investment bank, BTG Pactual,

showed this week how an unpredictable shock

can cause a large shift in the market. The

bank’s chief executive and multibillionaire,

André Esteves was arrested in connection with

a corruption scandal involving Brazilian oil firm,

Petrobras. There were large negative reactions

as Mr Esteves has been the mastermind behind

the success of the bank and has a 20% share

in the business, thus there is mass uncertainty

surrounding the future of the bank. Rating

agencies, Fitch and Moody’s have suggested

they may have to downgrade the credit rating of

the bank, even in light of the interim CEO

announcing the bank will be increasing liquidity

in order to reduce the risk. The markets have

reacted badly, with the share price falling 40%

on Wednesday, as shown by the graph below.

German insurance giant and asset manager,

Allianz, has announced it will be launching a

joint venture with the Chinese search engine

group, Baidu, and investment group, Hillhouse

Capital. This is the company’s attempt to

expand in the Chinese market, as demand for

insurance in China continues to grow at a

considerable rate. The move is also intended to

help Allianz achieve their target of 13% return

on equity by 2018 whilst boosting revenues to

€6.5bn. In my opinion, this is a logical idea as it

will enable Allinaz to grab a share of the

Chinese market, however, whilst the Chinese

economy is still unstable following the stock

market crash this summer, the move could

prove costly.

Sam Ewing

NEFS Market Wrap-Up

18

Oil and Gas

This week, oil futures (CLF6: NYMEX) further

dropped 2.7% to $41.89 pressured by a strong

dollar and concerns over excessive global

supply. This triggered a selloff in energy US

stocks on Friday’s short session: Southern

Energy Company (SWN: NYSE) fell by 7.22%,

making it the biggest decliner among the S&P

500 stocks, while Consol Energy Inc. (CNX:

NYSE) followed closely with a decline of 6.5%.

On Wednesday, billionaire financier Andrè

Esteves was arrested under a new set of

investigation into a vast bribes-for contracts

scheme at Petrobras (PETR4: SAO). The

allegations are that former executives

conspired with construction bosses, black

market money dealers and politicians to extract

an estimated R$6bn through fraudulent

contracts. Petroleo Brasileiro SA Petrobras is

Brazil’s state-run oil giant, and with its discovery

of giant offshore oil reserves in 2007, has

transformed into one of the world’s most

promising oil companies and a symbol of a

resurgent Brazil, raising $70bn in its share

sales in 2010, one of the biggest in history.

Overall, the negative implications for the

financial sector of any association with the

Petrobras scandal were immediate, moving

Brazil’s economy on its track to one of its worst

recession since the Great Depression. The

graph below showcases the plummeting of

Petrobras’ share price since Wednesday, from

$5.58 to $4.94, an 11.5% decrease so far.

Meanwhile, the two former heads of BP and

Royal Dutch Shell, Europe’s two largest oil

companies, have argued that the two groups

failed to act fast enough to respond to the

implications of climate change for their

businesses. Their professed concern is not

matching the sweeping actions needed to

address the problem, and the consequences of

it are likely to be reflected in the stock market in

future weeks. Due to the ongoing

investigations, Petrobras was obliged to

announce that it would have to delay the

publication of its third quarter results, which will

likely have an enormous impact on the value of

the company. Morgan Stanley, for instance,

estimates the company’s assets to be slashed

by $8.1bn, while UBS put the damage estimate

to something between $10bn and $15bn.

Andrea Di Francia

Week Ending 29th November 2015

19

Retail

Analysts’ forecasts pertaining to retail equities

were this week dominated by “Black Friday”,

the ubiquitous lowering of prices for retail goods

to consumers, now commonplace for large

retail chains. Black Friday, when viewed simply

as a day of increased retail spending from

consumers, will ultimately have a tangible,

albeit small, impact on the year results of

retailers. However, Black Friday results could

potentially be viewed as an indication of holiday

season performance for retailers, and thus

could potentially have a significant impact on

retailers and their behaviour. As such, strong

sales could improve a retailer’s share price, and

weak sales could have an adverse impact.

This theory, however, disregards the plethora of

convoluted metrics which impact a retailer’s

share price and overall performance, and

overestimates the importance of Black Friday

when viewed from a stock or sector analyst’s

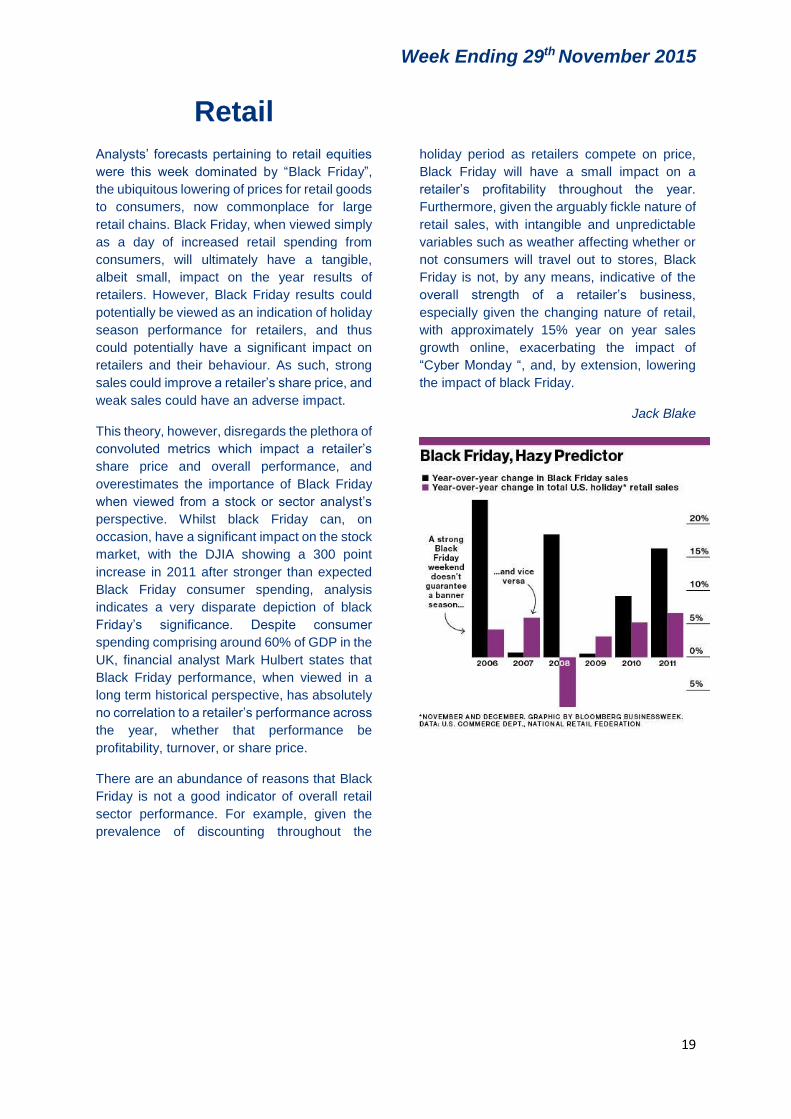

perspective. Whilst black Friday can, on

occasion, have a significant impact on the stock

market, with the DJIA showing a 300 point

increase in 2011 after stronger than expected

Black Friday consumer spending, analysis

indicates a very disparate depiction of black

Friday’s significance. Despite consumer

spending comprising around 60% of GDP in the

UK, financial analyst Mark Hulbert states that

Black Friday performance, when viewed in a

long term historical perspective, has absolutely

no correlation to a retailer’s performance across

the year, whether that performance be

profitability, turnover, or share price.

There are an abundance of reasons that Black

Friday is not a good indicator of overall retail

sector performance. For example, given the

prevalence of discounting throughout the

holiday period as retailers compete on price,

Black Friday will have a small impact on a

retailer’s profitability throughout the year.

Furthermore, given the arguably fickle nature of

retail sales, with intangible and unpredictable

variables such as weather affecting whether or

not consumers will travel out to stores, Black

Friday is not, by any means, indicative of the

overall strength of a retailer’s business,

especially given the changing nature of retail,

with approximately 15% year on year sales

growth online, exacerbating the impact of

“Cyber Monday “, and, by extension, lowering

the impact of black Friday.

Jack Blake

NEFS Market Wrap-Up

20

Technology

Reviewing the Technology industry this week,

we see some variation in performance levels,

with Intel Corporation perceiving a rise in share

prices by 4.1% to $34.56, whilst Hewlett-

Packard experienced a fall from $14.28 to

$12.56. This 12% drop, combined with what

has been a poor annual performance, with a

sharp yearly decline of 26.01% in share prices,

could prove disastrous for the American-based

Information Technology Company and the

confidence of its shareholders.

After reporting on the huge boost in share

prices last week, a further increase has been

spectated by Infineon Technology over this

week. The German semiconductor company

announced its recent expected fourth-quarter

income figures, with a net value predicted at

€322 million – an 80% rise on last year’s value.

Such excellent news saw Infineon’s share price

soar 15% higher on the Thursday. This success

comes down to numerous factors, with one

being the €131 million tax fillip, and another

being its €3 billion acquisition of International

Rectifier last year. This California-based

corporation operated at a greater margin than

Infineon itself, boosting the overall group’s

margin and performance. Infineon has

maintained this success throughout the year,

with share prices being up 16.9% to €13.48

from €11.20, demonstrated by the graph below

– excellent news for shareholders, with huge

prospects for further successful investments.

Reflecting upon last week’s news regarding

Google Plus, the huge tech-firm is now

revealing its plans to instigate app streaming

into its devices. Google plans to remove

barriers surrounding apps, allowing for a more

integrated service between its apps and the

World Wide Web, which in turn allows for easier

access to information from all devices. Google

went ahead with an app-streaming experiment

recently, testing the outcome of such a change,

and it was proven that such a movement would

indeed open up the possibilities of Google’s

search business, enhancing the digital world.

But this service comes at the cost of shifting

how Google’s services interact with information,

and the technological changes required may

result in the loss of consumer-valuable

features. Despite this ambitious

announcement, share prices fell from a weekly

high of $782.90 to $770 - though only a minor

drop.

These two firms continually progress their

respective equities, whilst consistently boosting

their own market capitalisation, resulting in

quality satisfaction from their shareholders with

future expectations at the highest; making

these shares definitely worth an investment.

Daniel Land

Infineon’s share prices this week

Week Ending 29th November 2015

21

Pharmaceuticals

Pharmaceuticals have remained relatively

stable this week amidst the announcement of a

historically large acquisition taking place within

the sector. The NASDAQ Biotechnology Index

rose by 1.92% and the FTSE 350

Pharmaceuticals & Biotechnology Index rose a

mere 0.13% over the course of the week.

Marking the biggest healthcare deal in history,

among an active year of mergers and

acquisitions, Pfizer announced a $160bn

takeover of Dublin-based Allergan last Monday

which (if finalised) will create the world's largest

pharmaceuticals group. Despite paying a

premium for the stock, which had a market

capitalisation of only $123bn ahead of the deal

confirmation, Pfizer's share had risen 1.1% over

the course of the week as hopeful analysts such

as Cowen & company and SunTrust upgraded

the stock due to the deal making strategic

sense. Although analysts fear that Pfizer has

undervalued its synergy cost budget (estimated

to cost $2bn) since it is likely to face significant

difficulties, they cite the increase in US to Ex-

US sales mix, from 44:56 percent to 61:39

percent as an optimistic re-enforcement that the

new firm will have considerable pricing power.

Yet, the deal is still to be completed. It is now

seeking approval from Washington - political

power plays will be an important factor. This

deal finally enables Pfizer to move its domicile

to a lower tax jurisdiction in Ireland which is

expected to cut its tax rate by roughly 7%. This

activity, which has been replicated across other

Big Pharma, confirms the importance of clever

accounting over research triumphs, as Pfizer's

clever accountant-turned-CEO Ian Read, who

strongly pushes for shareholder value, has

increased Pfizer 's share price by almost double

since his appointment.

In other news, Turing Pharmaceuticals, one of

the main reported companies accused of drug

price hikes (Daraprim increased by 5,455%),

has abandoned its price cut promise. Despite

not being a publicly traded company, this

highlights the industry’s reliance on high prices.

Yet, its competitor, Imprimis Pharmaceuticals,

which responded by offering alternative

compounded substitutes, has reported strong

earnings growth by undercutting price hikes.

Rating increases have helped its share price to

rocket by 28% in the past week as seen below.

Along with the fact that the promise of resulting

R&D growth from mergers rarely materialises,

continual market density and thus competition

shrinkage due to recent M&A is likely to

disadvantage patients in the long run. Perhaps

Pharmaceutical companies will soon feel a

wrath from the market for morphing into

marketing rather than research enterprises in

the long run, or maybe this is just becoming an

inevitable trend.

Sam Hillman

NEFS Market Wrap-Up

22

Industrials & Basic

Materials

China, the fastest growing economy in the last

decade, has seen its industrial production grow

5.6% year-on-year. This is the slowest pace

since April 2015, as a result of lower capacity

utilization in the industrial sector with weak

demand from local and foreign consumers.

The slowdown in the Chinese Industrials and

Manufacturing sector is prevalent where China

has repeatedly lowered its growth forecast over

the years.

China metal producers are finally feeling the

heat where they have requested for the

Chinese authorities to purchase surplus metal

reserves to ease pressure in the market. The

state-controlled metals industry body, China

Nonferrous Metals Industry Association,

proposed on Monday that the government

scoop up aluminium, nickel and minor metals

including cobalt and indium. The Association

had suggested that state buys 900,000 tonnes

of aluminium, 30,000 tonnes of refined nickel,

40 tonnes of indium, and 400,000 tonnes of

zinc.

While it is unclear if the authorities will agree to

the proposal, the approach underlines the

extent to which smelters in the world’s top

producer and consumer are suffering from

prices at or near multi-year lows. This also

wouldn’t be the first time something like this has

taken place - back in 2009, the authorities

purchased up to 700,000 tonnes of copper to

arrest sliding copper prices. At that time, copper

was trading at USD3000/tonne and with the

State Reserve Bureau’s help, copper prices

stabilised, and many believe that this was the

key factor in helping push prices up to

USD10000/tonne by 2011.

The direction of the State Reserve Bureau is

still unclear, as China has not been able to

consume as much metals as they produce

amidst the slowing economic growth in the

country. Metal prices are arguably in worse

shape today than in 2009. Aluminium is down

by almost 30% the past year. Nickel is at 12-

year lows, falling to USD8145/tonne this week.

The last time it dropped below this level was in

2003. Hence, it would be a large bill to foot

should the SRB step in to stabilise the market.

The share price of Aluminium Corp. of China

Limited has declined by 27.05% since March

2015 and has also underperformed the S&P500

by a whopping 27.28%. The negative earnings

of the company alongside the oversupply in the

industry will prove to be challenging times

ahead for the company.

Erwin Low

Week Ending 29th November 2015

23

COMMODITIES

Precious Metals

This week we have seen the precious metals

sector prices continue to waiver around

historically low levels. Gold prices dropped by

13USD to 1072USD/oz., flirting with its lowest

level since February 2010 on the strength of the

US Dollar. The other metals prices have also

remained low over the week. Prices are stuck in

their worse rout since July as the Federal

Reserve officials continue to raise the

expectations of an interest rate hike in

December.

The Gold prices this week have been pushed

down further from 1085.67.24 USD/oz. to

1072.10 USD/oz, as shown on the chart below.

This came after the dollar index, which

measures the currency against a basket of its

peers, was up 0.2% to 99.79%, leaving it less

than 1% below the 12-year high touched in

March. The prospects of a stronger dollar and a

deepened expectation of an interest rate

increase have sent investors fleeing from Gold

as prices of Gold continue to tumble. As I

mentioned last week, the higher the interest

rate, the lower the appeal for Gold as they lose

out to competitive assets that pay interest or

dividends such as bonds.

Silver has also continued to stay low, hovering

just above the 14USD/oz. mark, almost

reaching its lowest levels since 2009. Silver is

still considered as one of the most volatile

metals and its fluctuations tend to be large, and

follow similar trends as Gold. The strengthening

of the dollar has remained a negative on

precious metals prices as both industrial and

investor demand remain poor.

Platinum on the other hand, has a positive

outlook as analysts view it as an oversold metal.

As the prices of Platinum have hovered around

the 845USD to 850USD mark and because of

the Volkswagen scandal, prices of Platinum

have become very attractive. There would be a

substitution effect as Platinum would see

demand rise for industrial uses such as the

gasoline car market.

In other news, Palladium prices have continued

to linger around the 545USD to 550USD mark

this week as the overall outlook for Palladium

looks grim. Palladium is widely used in

production of catalytic converters for gasoline

engines.

With the strong US economic outlook, it must

be imminent that the Fed will eventually raise

the interest rates. Higher rates would mean an

increased probability of a slower growth and a

stronger US dollar coupled with a weak global

economy would be a negative for the overall

Precious Metals prices.

Samuel Tan

Gold Price

Trend

NEFS Market Wrap-Up

24

Energy

It’s been an eventful week in the energy market,

as many commodities make a strong

resurgence. Labelled as a market reaction to

the shooting down of a Russian jet by Turkish

forces, WTI and Brent Crude Oil have risen

4.0% and 1.6% respectively, while the biggest

mover came in the form of Gasoline which rose

dramatically climbing 8.5% for the week.

Oil prices climbed from Tuesday as fears of a

supply disruption after the Turkish military shot

down a Russian jet fighter along the Syrian

border. Many are therefore worried that supply

coming from Russia and the Middle East into

Europe will be halted as tensions rise between

the two nations. Although there appears to be

no clear signal of intent for war by either side,

President Putin has called the incident “a stab

in the back”. While this had a hand in the surge

in Gasoline prices, the main reason for the

increase in prices seems to stem from limited

supplies in North-eastern America ahead of

Thanksgiving, which took place on Thursday,

one of the biggest holidays of the year in the

US.

In other energy news, Natural Gas made a

surprising recovery after its heavy losses in the

previous week. Despite the US Energy

Information Administration (EIA) reporting that

US natural gas stocks increased by 9 billion

cubic feet for the week ending November 20,

prices rose 7.4% over the past seven days.

With supply increasing, the price increase can

therefore only be explained by an even greater

increase in demand. Forecasts for colder

temperatures over the coming days, released

on Monday and Wednesday, is the reason for

the demand increase according to energy-

advisory firm Gelber & Associates, stating that

“Domestic [US] weather models are calling for

a cold front to sweep through the country in the

next two days.” The graph below shows this

market reaction clearly, with a large surge on

Wednesday off the back of both the continuing

cold in the coming days and the Thanksgiving

holiday on Thursday, with many families in the

US traditionally eating (and thus heating) their

homes.

For the future, one would imagine gas prices to

fall once all the Thanksgiving festivities end. In

regards to the Oil price, the jury is still out; what

takes place between Russia and Turkey over

the coming weeks will play a role in the direction

of prices.

Harry Butterworth

Week Ending 29th November 2015

25

Agriculturals

Monday signified a turning point in the price of

cotton. While the production of cotton has

declined appreciably over the last year due to

decreased demand, the main driving force in

shifting prices back upwards is the decline in

high-quality supply.

During the period from 20th October to 20th

November, the price fell from 64.25 USD/lb to

60.05 USD/lb (a fall of 6.54%). The graph below

shows the price of cotton hitting a low point at

the end of last week, before rising 3.21% by

Wednesday, 25th November.

Pakistan, the 4th largest cotton supplier in the

world, concluded that these changes were a

consequence of heavy flooding and the

consequent harm caused by pests. The

projected amount of cotton to be produced in

2015/2016 cycle was 2325 million kilograms.

However at the moment, due to very late

sowing, the expected estimated output might be

as low as 1705 million kilograms, equivalent to

a 26.7% decline. The US Department of

Agriculture seems to be more optimistic,

forecasting a smaller drop in production – by

17%. Furthermore, the weather and pests

contributed to drastically lowered quality of the

cotton produced. It is believed that only around

40% will be of quality considered as high. Up

until mid-November, demand remained low as

the traders expected a higher supply. As this

prediction was not the case, traders rushed to

obtain more good-quality cotton..

The government of Zimbabwe has already

decided to introduce support to farmers and

initiatives for greater production. The

government is planning to spend $26 million on

distribution of necessities (such as seeds and

fertilisers) to farmers. AGRITEX, the national

agricultural extension service, is responsible for

the identification of affected farmers and

ensuring the support packages are distributed.

With regard to other commodities, soybean

prices began to pick up since 13th November

and rose from 855.25 USD/bu to 876.75

USD/bu by 27th November. Analysts concluded

that this outcome might have been influenced

by the Thanksgiving celebrations; traders

assumingly were more willing to complete

purchases beforehand. The sudden increase in

price might be well overestimated and shortly

return to the previous trend next week. Similar

comments were attributed to increased cotton

demand. According to Jordan Lea, co-owner of

Eastern Trading Company, closing a position

and having a 4-day weekend could have been

an additional short-term factor in price

fluctuations.

Goda Paulauskaite

NEFS Market Wrap-Up

26

CURRENCIES

Major Currencies

The euro remained near seven month lows

against the dollar after closing under 1.07 for

the sixth straight session. The dollar ended the

week with a three day winning streak against

the euro, having closed higher in five of the last

six trading sessions. The pair wavered between

1.0596 and 1.0683 before settling 1.0596, down

0.15% on Friday’s session.

EUR/USD gained support at 1.0591, the low

from November 23rd and was met with

resistance at 1.1096, the low from October 28th.

The euro could fall even further later next week

if the ECB's Governing Council institutes further

easing measures to stimulate the economy and

bolster inflation at its meeting in Frankfurt. Over

the last few weeks, ECB president Mario Draghi

has sent strong indications that the central bank

could increase the scope of its comprehensive

EUR 60 billion a month quantitative easing

program at the meeting. On Wednesday,

Reuters reported that the ECB could also

impose a two-tiered penalty next week for

banks that leave deposits at its facility. The

ECB's benchmark refinancing rate is at a record

low of 0.05%, while rates at the deposit facility

are already in negative territory at -0.20%.

Less than two weeks later, the Federal Open

Market Committee is expected to raise its

benchmark Federal Funds Rate for the first time

in more than nine years. The rate, which banks

charge on interbank overnight loans at the Fed,

has remained at a near-zero level since

December, 2008. The potential for sharp

divergence between monetary policies in the

US and the Eurozone has sent the dollar

soaring, as foreign investors look to pile into the

greenback in order to capitalise on

higher yields.

With volatility on the rise and many key events

ahead, the market is about to start, what could

be a historic December. After six months of

closing between 1.09 and 1.12, the pair broke

decisively to the downside and is about to post

the lowest monthly close since 2002. A

combination of more easing by the ECB and a

strong US jobs report could send EUR/USD

below 2015 lows located at 1.0460 and would

open the doors for a decline toward parity. The

pressure on EUR/USD could continue until after

the Fed’s decision when the pair could start to

stabilise.

Adam Nelson

Week Ending 29th November 2015

27

Minor Currencies

The Swiss Franc has been weakening long

term; the trend began in mid-October when

Mario Draghi committed the ECB to considering

further QE at their next monetary policy meeting

in December. This does not explicitly affect the

Franc, but because the EU is Switzerland’s

largest trading partner, the Swiss National bank

will need to take action to weaken their currency

to keep their exports competitive. This caused

the USD/CHF to rise significantly in mid-

October and break through the 0.980

resistance level, which had previously been

proven strong when the pair bounced off the

price multiple times in August and September.

Once the price was broken, a trend began

(highlighted in the graph below) averaging an

increase of 13 pips per day. This uptrend made

surprisingly swift work of the 1.000 price, which

one would have thought would have produced

substantial psychological resistance. Prices for

this pair haven’t reached this range in over 5

years, and so there is some uncertainty among

currency traders as what positions they should

be taking or where the significant price levels

will be. However, given the imminent rate hike

from the Fed, and with the Swiss National Bank

giving further considerations to actions they can

take to weaken the Franc, we can expect the

trend in USD/CHF to continue into the

foreseeable future.

The Australian dollar had an up and down week

against its US counterpart. The currency briefly

broke its October high but unfortunately for the

Aussie the gains were lost later on, ending the

week roughly even. However, against the Euro

and Pound Sterling the Aussie pushed forward.

General feeling around the Reserve Bank of

Australia has been negative in recent weeks,

but better than expected unemployment data

has meant odds of further RBA rates cuts have

lengthened. The ECB’s and the BoE’s recent

dovish behaviour has made speculators prefer

Aussie dollar in trading, gaining 0.5% against

GBP and 0.4% against EUR this week. The

coming week could bring some change in

sentiment around the Aussie dollar, if figures for

trade balance and quarterly growth are different

to forecasts.

Will Norcliffe-Brown

USD/CHF 1 day candlestick (Source: OANDA)

NEFS Market Wrap-Up

28

The Research Division was formed in early 2011 and is a part of the Nottingham Economics and Finance Society (NEFS, formerly known as NFS and UNIS). It consists of teams of analysts closely monitoring particular markets and providing insights into their developments, digested in our NEFS Weekly Market Wrap-Up. The goal of the division is both the development of the analysts’ writing skills and market knowledge, as well as providing NEFS members with quality analysis, keeping them up to date with the most important financial news. We would appreciate any feedback you may have as we strive to grow the quality and usefulness of weekly market wrap-ups.

For any queries, please contact Josh Martin at [email protected]. Sincerely Yours, Josh Martin, Director of the Nottingham Economics & Finance Society Research Division

This Publication has been prepared solely for informational purposes, and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security, product,

service or investment. The opinions expressed in this Publication do not constitute investment advice and independent advice should be sought where appropriate.

Whilst reasonable effort has been made to ensure the accuracy of the information contained in this Publication, this cannot be guaranteed and neither NEFS nor any

other related entity shall have any liability to any person or entity which relies on the information contained in this Publication, including incidental or consequential

damages arising from errors or omissions. Any such reliance is solely at the user’s risk.

As featured on:

Sponsors: Platinum: Gold:

About the Research Division The Research Division was formed in early 2011 and is a part of the Nottingham Economics and Finance Society (NEFS, formerly known as NFS and UNIS). It consists of teams of analysts closely monitoring particular markets and providing insights into their developments, digested in our NEFS Weekly Market Wrap-Up. The goal of the division is both the development of the analysts’ writing skills and market knowledge, as well as providing NEFS members with quality analysis, keeping them up to date with the most important financial news. We would appreciate any feedback you may have as we strive to grow the quality and usefulness of weekly market wrap-ups. For any queries, please contact Jack Millar at [email protected] Sincerely Yours, Jack Millar, Director of the Nottingham Economics & Finance Society Research Division

Recommended