The great and challenging solar opportunity in India

Our “New Energy Team” combines comprehensive data with deep insights and customized analysis

Since 2008, BRIDGE TO INDIA has been driving change in the Indian solar market through excellence in analysis and communication and is widely recognized as a leading consulting company in this area

Our strengths:

A 360 degree view of the market dynamics

An unrivalled network of

industry stakeholders

A cross-functional team with skills in engineering,

finance, business management and

economics

2 © BRIDGE TO INDIA

Business strategy

Regulatory and policy advice

Market analysis

Due diligence and valuation

Debt and equity fund raising

Business match-making

Market trend projections

Thought leadership reports

Online content

3 © BRIDGE TO INDIA

In renewables, storage and power grids, we have worked with many of the leading stakeholders in India

Powered by BRIDGE TO INDIA

India’s leading online solar marketplace for installers and consumers

Source: Bridge To India analysis

Where India stands on solar today 1

The fundamental drivers of solar 2

The current opportunities 3

Source: Bridge To India analysis

Where India stands on solar today 1

India’s total installed solar capacity in 2015 is 3 GW

Source: BRIDGE TO INDIA database

© BRIDGE TO INDIA

8 © BRIDGE TO INDIA

Will India become one of the largest solar markets in the world? Three different perspectives…

• Compare: Germany 38 GW • € 100+ billion opportunity • 40 GW for distributed solar • 10-‐15 GW under dev. • But: no master plan

• Compare: Germany 3 GW p.a. • < 1% of power generaGon • 95% uGlity scale • Good: ecosystem in place

What are the alterna6ves? • Coal: infra, polluGon • Gas: imports • Large hydro: democracy • Nuclear: underperformer • Underdevelopment?

The Vision

The new Indian government wants to make it a 100 GW

market by 2020

Today, it is only a 1-‐2 GW per year

market

The Reality

The Need

India needs huge amounts of power but has few opGons

9 © BRIDGE TO INDIA

But will it be a design market?...

• Distributed generaGon • Consumer soluGons • Govt. only a facilitator

(through failings, market seWng)

• Slower iniGal growth, more sustainable long-‐term growth

• Market driver: policy (not subsidy)

• Entry point: Grid-‐level soluGon

• Size: UGlity-‐scale generaGon • Project types: Government

tenders, solar parks, GW-‐scale solar projects

• Companies: Established/large-‐scale players

• Success factors: Large project management and finance

• Challenge: Grid management

10 © BRIDGE TO INDIA

… or a default market?

• Market driver: Reacts to a need

• Entry point: Consumer soluGons

• Size/project types: Distributed generaGon

• Govt. role: only a facilitator (through failings, power price seWng)

• Companies: Room for new entrants, business models, technologies

• Success factors: consumer access

• Challenge: Consumer awareness

Source: Bridge To India analysis

The fundamental drivers of solar 2

Bottom line: India needs much, much more electricity

11920

6697

3493 2621 2438

1578 672

0

2000

4000

6000

8000

10000

12000

14000

Very low per capita power consumption

U.S.

Germ

any

China

Iran

Brazil

Mexico

India

Source: World Bank, Bridge To India analysis

And: 400 million people in India are without access to grid electricity

Frequent grid outages

21-30 hours/ week

<5 hours/ week

6-10 hours/ week

11-20 hours/ week

>30 hours/ week

© BRIDGE TO INDIA

kWh

1 2

3

In a “Development” scenario, India needs to increase power supply by a factor of 5

© BRIDGE TO INDIA

1,050

4,978

India’s projected energy generation (TWh/year)

+7% pa

2012 2035 (est)

Scenario “Development” • Average growth of 8% p.a.

over next 20 years • IndustrializaGon (higher

energy intensity of GDP) • Efficiency gains in

generaGon, transmission and distribuGon

• Closing of electricity gap (10%+)

• ElectrificaGon for all (400m) • Historical growth at 7% p.a. • Per person power

consumpGon would be ca. 3,000 kWh p.a. – comparable to current global average

Source: Bridge To India analysis

India’s future power mix: a “coal” vs. a “solar” scenario

“Coal-‐heavy” scenario • Ca. 600 GW new coal fired power plants by

2035 • Total lifeGme emissions of 80 GtCO2 = 8% of

global, historic carbon budget • Large fresh water polluGon (India’s coal has

high ash content) • Air polluGon (India already has 13 of the 20

most polluted ciGes) • Environmental destrucGon due to open cast

mining • Infrastructure bomlenecks: railways (already

used 50% of Indian railway cap.), ports • Import of coal (and gas) – energy security and

current account deficit • Coal price rising? (India’s demand will impact

global prices, future carbon prices)

“Solar-‐heavy” scenario • Ca. 1,600 GW of solar Gll 2035 (and 100 GW

of coal) • Solar would contribute around 60% of power • Annual growth solar rate of 35% (18 GW in

five years as compared to govt. goal of 100 GW)

• At current cell efficiencies, would require ca. 0.8% of India’s land mass or 8% of its waste land

• Would require large investments into balancing, storage, grid infrastructure, demand management

• Would lead to a massive reducGon in the cost of solar (and storage) due to scale

Source: BRIDGE TO INDIA analysis

Source: Bridge To India analysis

The current opportunities 3

More and more international players are investing into the utility-scale Indian solar market

© BRIDGE TO INDIA

International utilities (Equity IRR: 13-15%)

PE backed IPPs (Equity IRR: 18-20%)

International developers (Equity IRR: 15-17%)

Others

Indian corporates (Equity IRR: 20% plus)

Welspun

NTPC

Azure

Hin Clean

SunEdison

Acme (EDF)

Mahindra Sunborne

Essel

Solairedirect

Renew

First Solar

Hero

Today Waaree

Focal

0

50

100

150

200

250

300

350

400

0 50 100 150 200 250 300 350 400

Cap

acity

und

er d

evel

opm

ent M

W

Capacity installed MW

Return expectations for investors

Source: BRIDGE TO INDIA analysis

26.2

7.4

0.75 0.62

Area required per MW (in acre)

Solar parks could make life much easier for investors (land, evacuation) 25 solar parks with an aggregate capacity of 20 GW under development

© BRIDGE TO INDIA

Wind Solar Thermal Nuclear

Source: Spectrum land use report, BRIDGE TO INDIA analysis

Rising tariffs are driving a business case for distributed, private PPA solar models

Cumulative DISCOM deficit of USD 50 billion!

+ 20% Maharashtra

+ 15 - 31% Tamil Nadu

+ 12% Delhi

+ 90% Greater Noida

+ 30 - 50% Bihar

Recent proposed tariff hikes

0

2

4

6

8

10

MH

-MS

ED

CL

KA

-BE

SC

OM

TN-

TAN

GE

DC

O

Del

hi

UP

Har

yana

INR

/ kW

h

Industrial tariffs - Base Energy Charges (2007-2014)

+ 18% Rajasthan

© BRIDGE TO INDIA

Source: BRIDGE TO INDIA analysis

0

2

4

6

8

10

12

Mah

aras

htra

Tam

il N

adu

Kar

nata

ka

Del

hi

Odi

sha

And

hra

Pra

desh

Tela

ngan

a

Utta

r Pra

desh

Wes

t Ben

gal

Raj

asth

an

Pun

jab

Ker

ala

Bih

ar

Har

yana

Him

acha

l

Ass

am

Jhar

khan

d

Mad

hya

Guj

arat

Utta

rakh

and

Chh

attis

garh

INR

/ kW

h Rooftop solar is already financially attractive for commercial consumers across many states…

Viability of rooftop solar for commercial customers

Cost of Solar

Cost of Solar with AD

Solar PV system viable Viable with AD Not viable

Commercial HT tariff

© BRIDGE TO INDIA

Source: BRIDGE TO INDIA analysis

Source: BRIDGE TO INDIA analysis

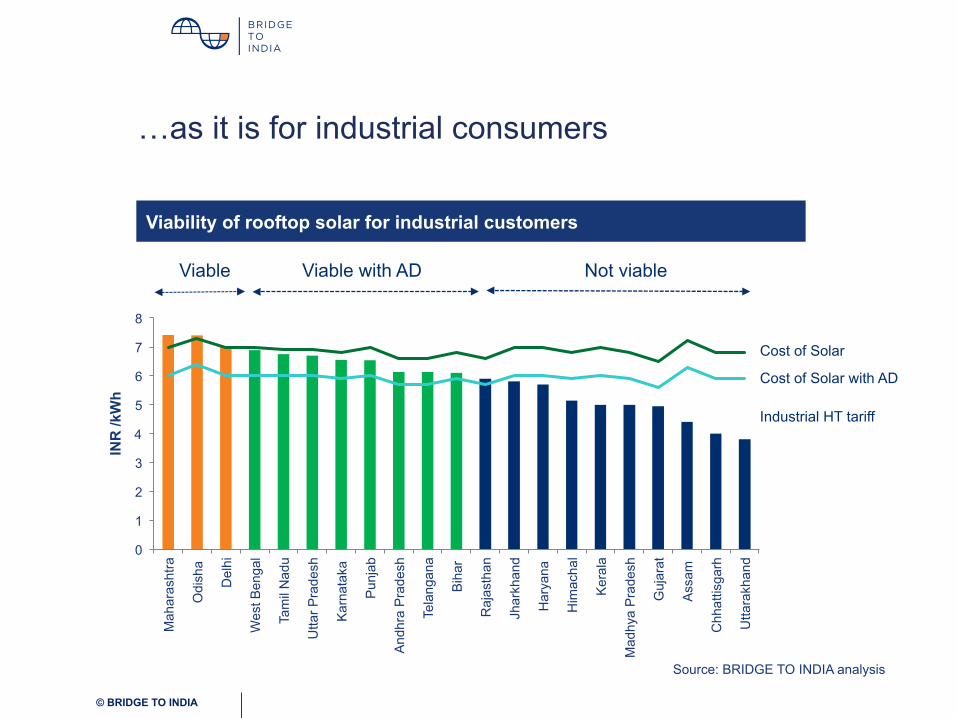

…as it is for industrial consumers

Viability of rooftop solar for industrial customers

Cost of Solar

Cost of Solar with AD

Viable Viable with AD Not viable

Industrial HT tariff

0

1

2

3

4

5

6

7

8

Mah

aras

htra

Odi

sha

Del

hi

Wes

t Ben

gal

Tam

il N

adu

Utta

r Pra

desh

Kar

nata

ka

Pun

jab

And

hra

Pra

desh

Tela

ngan

a

Bih

ar

Raj

asth

an

Jhar

khan

d

Har

yana

Him

acha

l

Ker

ala

Mad

hya

Pra

desh

Guj

arat

Ass

am

Chh

attis

garh

Utta

rakh

and

INR

/kW

h

© BRIDGE TO INDIA

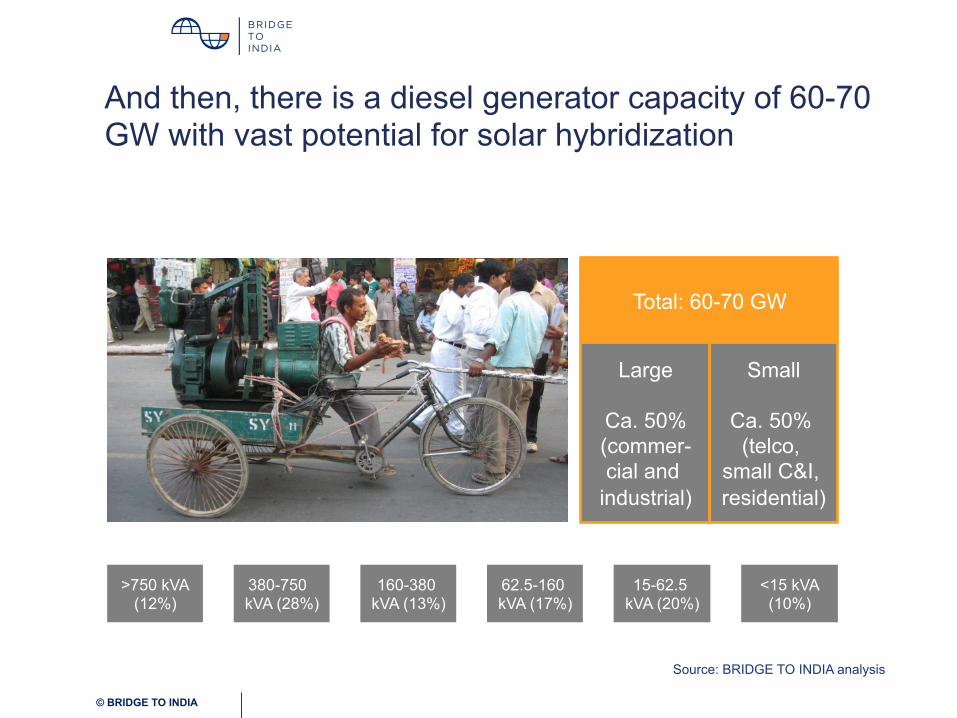

And then, there is a diesel generator capacity of 60-70 GW with vast potential for solar hybridization

Total: 60-70 GW

Small

Ca. 50% (telco,

small C&I, residential)

>750 kVA (12%)

380-750 kVA (28%)

160-380 kVA (13%)

<15 kVA (10%)

15-62.5 kVA (20%)

62.5-160 kVA (17%)

© BRIDGE TO INDIA

Large

Ca. 50% (commer-cial and

industrial)

Source: BRIDGE TO INDIA analysis

So what can European companies do in India?

© BRIDGE TO INDIA

Picture: The Economist

Sell “intelligent” grid related know-how?

Invest in projects? (new risk profile?)

Sell “intelligent” consumer power technologies?

Invest in startups?

… and more. (Remember: it’s a long term game)

© BRIDGE TO INDIA

www.bridgetoindia.com www.bridgetoindia.com/blog www.facebook.com/bridgetoindia LinkedIn group –’ India Solar Future’ www.twitter.com/bridgetoindia

Tank you!

[email protected] +91-124-420-4003

Recommended