8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 1/26

TERM PAPER OF

BASIC OF PERSONAL

FINANCE

(OE175)

TOPIC: - HEALTH INSURANCE

SUBMITTED TO;-

MS. JASPREET KAUR

SUBMITTED BY : -

PRITI SINGH

REG.NO. 3440070133

B.TECH –BIOTECH (MBA)

ROLL NO. OE17511

ACKNOWLEDGEMENT

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 2/26

I , priti hereby take the advantage to thank my teacher, Ms. JASPREET KAUR

for assigning me such a wonderful topic for my term paper& extending meconsistent help, support & guiding throughout the project.

Also, I will like to thank my friends for aiding me with the requisite materials &

information for my project.

My immeasurable gratitude to my roommates & my parents cannot be expressed

in words for the support they have provided.

PRITI SINGH

TABLE OF CONTENT

INTRODUCTION…………………..3

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 3/26

HISTROY…………………………..3-4

WORKING…………………………4-5

POLICES…………………………..5-7

COMPANIES...…………........................7-24

• ICICI LOMARD

• BAJAJ ALLIANZ LIFE INSURANCE

• THE NEW INDIA ASSURANCE COMPANY LIMITED

• NEW INDIA INSURANCE LTD

NEW POLICY………………………24-26

CONCULSION……………………….26

REFRENCES…………………………27

INTRODUCTION

Health insurance like other forms of insurance is a form of collectivism by means of which

people collectively pool their risk, in this case the risk of incurring medical expenses. The

collective is usually publicly owned or else is organized on a non-profit basis for the members of

the pool, though in some countries health insurance pools may also be managed by for-profit

companies. It is sometimes used more broadly to include insurance covering disability or long-

term nursing or custodial care needs. It may be provided through a government-sponsored social

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 4/26

insurance program, or from private insurance companies. It may be purchased on a group basis

(e.g., by a firm to cover its employees) or purchased by an individual. In each case, the covered

groups or individuals pay premiums or taxes to help protect themselves from unexpected

healthcare expenses. Similar benefits paying for medical expenses may also be provided through

social welfare programs funded by the government.

By estimating the overall risk of healthcare expenses, a routine finance structure (such as a

monthly premium or annual tax) can be developed, ensuring that money is available to pay for

the healthcare benefits specified in the insurance agreement. The benefit is administered by a

central organization such as a government agency, private business, or not-for-profit entity.

HISTORY AND EVOLUTION

The concept of health insurance was proposed in 1694 by Hugh the Elder Chamberlen from the

Peter Chamberlen family. In the late 19th century, "accident insurance" began to be available,

which operated much like modern disability insurance. This payment model continued until the

start of the 20th century in some jurisdictions (like California), where all laws regulating health

insurance actually referred to disability insurance.

Accident insurance was first offered in the United States by the Franklin Health Assurance

Company of Massachusetts. This firm, founded in 1850, offered insurance against injuries

arising from railroad and steamboat accidents. Sixty organizations were offering accident

insurance in the U.S. by 1866, but the industry consolidated rapidly soon thereafter. While there

were earlier experiments, the origins of sickness coverage in the U.S. effectively date from

1890. The first employer-sponsored group disability policy was issued in 1911.

Before the development of medical expense insurance, patients were expected to pay all other

health care costs out of their own pockets, under what is known as the fee-for-service business

model. During the middle to late 20th century, traditional disability insurance evolved into

modern health insurance programs. Today, most comprehensive private health insurance

programs cover the cost of routine, preventive, and emergency health care procedures, and most

prescription drugs, but this is not always the case.

Hospital and medical expense policies were introduced during the first half of the 20th century.

During the 1920s, individual hospitals began offering services to individuals on a pre-paid basis,

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 5/26

eventually leading to the development of Blue Cross organizations. The predecessors of today's

Health Maintenance Organizations (HMOs) originated beginning in 1929, through the 1930s

and on during World War II.

WORKING

A health insurance policy is a contract between an insurance company and an individual or his

sponsor (e.g. an employer). The contract can be renewable annually or monthly. The type and

amount of health care costs that will be covered by the health insurance company are specified

in advance, in the member contract or "Evidence of Coverage" booklet. The individual insured

person's obligations may take several forms:-

• PREMIUM: The amount the policy-holder or his sponsor (e.g. an employer) pays to the

health plan each month to purchase health coverage.

• DEDUCTIBLE: The amount that the insured must pay out-of-pocket before the health

insurer pays its share. For example, a policy-holder might have to pay a $500 deductible per

year, before any of their health care is covered by the health insurer. It may take several doctor's

visits or prescription refills before the insured person reaches the deductible and the insurance

company starts to pay for care.

• CO-PAYMENT: The amount that the insured person must pay out of pocket before thehealth insurer pays for a particular visit or service. For example, an insured person might pay a

$45 co-payment for a doctor's visit, or to obtain a prescription. A co-payment must be paid each

time a particular service is obtained.

• COINSURANCE: Instead of, or in addition to, paying a fixed amount up front (a co-

payment), the co-insurance is a percentage of the total cost that insured person may also pay. For

example, the member might have to pay 20% of the cost of a surgery over and above a co-

payment, while the insurance company pays the other 80%. If there is an upper limit on

coinsurance, the policy-holder could end up owing very little, or a great deal, depending on the

actual costs of the services they obtain.

• EXCLUSIONS: Not all services are covered. The insured person is generally expected

to pay the full cost of non-covered services out of their own pocket.

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 6/26

• COVERAGE LIMITS: Some health insurance policies only pay for health care up to a

certain dollar amount. The insured person may be expected to pay any charges in excess of the

health plan's maximum payment for a specific service. In addition, some insurance company

schemes have annual or lifetime coverage maximums. In these cases, the health plan will stop

payment when they reach the benefit maximum, and the policy-holder must pay all remaining

costs.

• OUT-OF-POCKET MAXIMUMS: Similar to coverage limits, except that in this case,

the insured person's payment obligation ends when they reach the out-of-pocket maximum, and

the health company pays all further covered costs. Out-of-pocket maximums can be limited to a

specific benefit category (such as prescription drugs) or can apply to all coverage provided

during a specific benefit year.

• CAPITATION: An amount paid by an insurer to a health care provider, for which the

provider agrees to treat all members of the insurer..

• PRIOR AUTHORIZATION: A certification or authorization that an insurer provides

prior to medical service occurring. Obtaining an authorization means that the insurer is obligated

to pay for the service, assuming it matches what was authorized. Many smaller, routine services

do not require authorization.

TYPES OF HEALTH POLICY

1. GROUP HEALTH INSURANCE POLICY is an insurance cover applied for by the

employer, with Insurance Company. The employer would usually have to pay only a part

of the premium (unlike earlier when 100% employee benefits were prevalent) of the

group medical insurance policy.

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 7/26

2. SMALL AND LARGE BUSINESS GROUP HEALTH INSURANCE QUOTES,

and, as an Employer, What are the Benefits of Providing Group Medical Insurance

Policies:

• It is a well known fact that an employee values a group health insurance cover and its

benefits. It is viewed by the employee as the second best thing next to monetary

compensation, and gives the employer the added advantage of being able to employ and

retain the best in the business.

• Additionally, a group health insurance policy also offers your employees and yourself a

special bonanza in the form of tax incentives. For instance, as an employer you could

reduce payroll taxes, by offering your employees group health insurance as part of a

whole compensation package, thereby deducting 100% of the premiums that you would

have had to pay on a qualifying group health insurance plan..

1. BASIC HEALTH INSURANCE QUOTE

The Basic Health Insurance Plan was specially designed to function as an inexpensive (limited

benefit) alternative to the major group health insurance covers which are very expensive. This

can be comprised of an "any size group" and its outstanding features include:

• Hospitalisation and surgery benefits

• Medical Emergency Room benefits

• An option of either a single cover or a family coverage

• Visits/Consultations at a doctor's office of your choice

• Affordability

• Accessibility-to qualify for this Plan, there is no necessity to undergo physical exams,

and neither are medical questions asked as a pre-qualifier. For those members who are

eligible; this medical insurance cover is "guaranteed issue."

1. TYPES OF GROUP HEALTH INSURANCE PLANS

Group Health Insurance Plans are broadly split into indemnity plans (traditional indemnity plan,

an FFS or Fee for Service Plan, and more prevalent in the east coast) and managed care plans

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 8/26

(very popular in western USA), both different from each other in approach.The outstanding

differences between the indemnity and managed care plans are in sectors concerning:

• Out -of-pocket expenses for covered medical services,

• Choice of medical providers and hospitals, and

• How medical bills are paid.

In an indemnity plan, you will have a wider choice of hospitals and medical/healthcare providers

(this includes specialists like a cardiologist).In a managed care plan, you will incur less

paperwork and out-of-pocket expenses.

1. FEE FOR SERVICE PLAN

In these plans, the insured patient is examined by a doctor chosen by him, and the medical professional receives a fee for each service given to the insured patient. The fee- for -service

health insurance claim is filed either by the patient or the medical provider.

COMPANIES

ICIC LOMBARD

ICICI Lombard General Insurance Company Limited is a 74:26 joint venture between ICICI

Bank Limited , India's second largest bank with $79 billion in assets and Fairfax Financial

Holdings Limited, a Canada based $26 billion diversified financial services company engaged in

general insurance, reinsurance, insurance claims management and investment management.

ICICI Lombard is the largest private sector general insurance company in India with a Gross

Written Premium (GWP) of Rs. 3345 million for the year ended March 31, 2008.

ICICI Lombard General Insurance has been conferred the 'Customer and Brand Loyalty award

in the 'Insurance Sector - Non-Life' at the 2nd Loyalty awards, 2009. It was awarded the

‘General Insurance Company of the Year’ at the 11th Asia Insurance Industry Awards. The

company also won the 'NDTV Profit Business Leadership Award 2007' and was adjudged as the

most Customer Responsive Company in the Insurance category at the Economic Times Avaya

Global Connect Customer Responsiveness Award 2006. It has the Gold Shield for "Excellence

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 9/26

in Financial Reporting" by the ICAI (Institute of Chartered Accountants of India) for the year

ended March 31, 2006.

Advantages

• A single premium health policy that covers hospitalisation expenses of entire family.

• Cashless Hospitalisation at 3500+ network hospitals.

• Income Tax Benefits on premiums paid under Section 80 D** of Income Tax Act,

1961.

• Medical Insurance for Sum Insured of Rs. 2 lacs, 3 lacs or 4 lacs

• No medical check up to the age of 55.

• Also covers hospitalization activities arising out of terrorist activities

PRODUCTS

1. HEALTH PLUS ADVANTAGE

This is a very good and beneficial plan introduce by the ICICI Lombard with floter facility. A

person can save tax as well as get tax benefit against their investment.

Advantage:-

1. FLOATER COVER :- Anyone out of the 2 adults insured can avail of either covers

under Health Advantage Plus; Floater provides a common cover for both members

.

2.NO MEDICAL

CHECK - UP

No health check-up up to the age of 55 years (age as on last

birthday)

3.CASHLESS

HOSPITALIZATION Simply use our 'Health Advantage Plus' ID card at

any of the empanelled 3500+ hospitals and avail of

cashless service, a boon for those times when you

need finance the most. This benefit is only for

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 10/26

hospitalisation claims.

4.MAXIMUMTAX

BENEFIT You can avail a full utilisation of tax benefit on up to

Rs. 15,000/- (Rs. 20,000 for Senior Citizens) as

premium paid under Section 80D of the Income Tax

Act,1961. This will save up to Rs. 4635/- ^ in your

tax liability in one years.

For the first time in India,a person can avail of an insurance cover for orthopedic, maternity,

dental, pharmacy, general practitioner and other medical expenses incurred up to the sum

insured on OPD basis.• The following OPD expenses are covered:

RooM

• Boarding Expenses as charged by the Hospital

• Nursing Expenses

• Expenses related to Dental Treatment

Surgeon, Anaesthetist, Medical Practitioner, Consultants, Specialist Fees

Anaesthesia, Blood, Oxygen, Operation Theatre Charges, Surgical Consumables,

Medicines and Drugs, Diagnostic Materials and X-ray, Dialysis, Chemotherapy,Radiotherapy, Cost of Pacemaker, Cost of Artificial Limbs External Medical Aids,

Dental treatment charges, Ambulance charges

.

DISADVANTAGES

• We can lodge a claim only once during the Period of Insurance, i.e. 90 days after

commencement of policy and up to 30 days after expiry of the Period of Insurance.

• Any illness / disease / injury pre-existing disease before the inception of the policy.

1. INDIVIDU AL PERSONAL ACCIDENT INSURANCE

It is the insurance plan introduce by the ICICI Lombard to ensure personal safety for us.

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 11/26

Individual Personal Accident Insurance Policy provides immediate coverage on policy

issuance. This policy covers you against Accidental Death & Permanent Total Disablement

(PTD) on account of an accident. Customised coverage that offers choices in sum insured.

The insurance cover is available in options of Rs. 3 Lakhs, 5 Lakhs, 10 Lakhs or 20 Lakhs.

The Policy Covers:- Individual Personal Accident Insurance pays our nominee the sum

insured chosen, in case an accident occurs during the policy period resulting in the insured's:

• Death

Permanent Total Disability - Individual Personal Accident Insurance pays compensation

against the permanent and total loss of limbs, sight etc., (including on account of terrorism or

acts of terrorism) due to an accident.

A person can get the following during period of insurance.

Loss of use/Actual loss by

physical separation of

Percentage of Capital Sum

Insured*

Sight of both eyes 100%

Both hands 100%

Both feet 100%

One hand and one foot 100%

One eye and one hand or one

foot

100%

Sight of one eye 50%

One hand or one foot 50%

ADVANTAGES

• Covers against Accidental Death - Permanent Total Disablement (PTD) on account of an

accident.

• Immediate cover on policy issuance

• Choose among Sum insured options of Rs. 3, 5, 10 and 20 Lakhs

• Covers claims arising out of Terrorism or acts of Terrorism

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 12/26

• No health check-up required for policy issuance

• Renewable till the age of 70 years

Easy Claim Process with minimal documentation

DISADVANTAGE

The Company shall not be liable under this policy for:

• Death, injury or disablement of Insured Person;

(a) whilst engaging in aviation or ballooning, or whilst mounting into, or

dismounting from or travelling in any balloon or aircraft other than as a passenger

(fare-paying or otherwise) in any duly licensed standard type of aircraft anywhere

in the world.

(b) directly or indirectly caused by venereal disease or insanity;

(c) arising or resulting from the Insured committing any breach of the law with

criminal intent.

.

BAJAJ ALLIANZ LIFE INSURANCE

Bajaj Allianz General Insurance Company Limited or Bajaj Allianz Insurance is a joint

venture between two of the most reputed names in the world of insurance - Bajaj Finserv

Limited and Allianz SE. Both of the names are known for their strength, expertise and

stability in the insurance sector. While Bajaj Finserv Limited holds the 74% of the paid

up capital of Rs. 110 crore, Allianz SE holds the remaining 26%. It can be added here

that Bajaj Finserv Limited has very recently demerged from Bajaj Auto Limited.

Bajaj Allianz Insurance started its journey on May 2, 2001 when it received the

certificate of Registration from Insurance Regulatory and Development Authority

(IRDA) for conducting General Insurance business in India including Health Insurance.

As on the end of March 2009, the income of Bajaj Allianz Insurance went up to Rs. 2,866

crore with a growth of 11% over the previous year. It also registered a net profit of Rs. 95

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 13/26

crore, highest by any private insurer, in the last financial year.

PRODUCTS

1. HEALTH GUARD POLICY

It covers expenses arise during the period of illines of insured person.

Advantage

Health Guard policy takes care of your hospitalization expenses & also offers a

wide coverage of pre & post hospitalization expenses.

Room rent limit General 'No Limit'

Room rent limit ICU 'No Limit';

Medical OT charges 'No Limit'

Doctor fee limit: 'No Limit'

The member has cashless facility at over 2400 hospitals across India

The member can opt for hospitals besides the empanelled ones, in which the

expenses incurred by him shall be reimbursed within 14 working days from

submission of all documents.

Pre and post - hospitalization expenses covers relevant medical expenses incurred

60 days prior to and 90 days after hospitalization.

Cumulative bonus of 5 % is added to your sum assured for every claim free year.

Family discount of 10 % is applicable.

Covers ambulance charges in an emergency subject to limit of Rs. 1000 /-

No tests required up to 45 years up to SI 10 lacs*

10% co- payment applicable if treatment taken in non-network hospitals. Waiver

of co-payment is available on payment of additional premium

Pre-existing diseases covered after 4 years continuous renewal with Bajaj Allianz

Family discount of 10% is applicable

DISADVANTAGE

• No floater facility.

• No Expenses related to Dental Treatment is available.

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 14/26

• NON allopathic tereatment is not incurred inthis policy and no pregenancy related

decisive is covered.

• Pre illness expenses covered after four year of successful completiton of policy.

The period is too long.

1. SILVER HEALTH POLICY

It is a policy introduced by the bajaj alliance for the people of age year of mor than46

years.

As the age of an individual increases the health care costs increase & become a burden on

the individual. The senior citizens have to pay out the hard earned savings to meet the

expenses. Bajaj Allianz’s Silver Health plan is exclusively designed for the senior

citizens, which covers medical expenses incurred during hospitalization period so this is

a very good policy introduced by the bajaj.

ADVANTAGE

This policy is very good for the senior citizen because the medical treatment is expensive

for the people for this age group.

• Pre-existing diseases covered from the second year of the policy.

• A flat benefit of 3% of admissible hospitalization expenses are paid towards pre

& post hospitalization expenses.

• Cashless facility : With Silver Health plan, the member has access to cashless

facility at various network of over 2400 hospitals across India (subject to exclusions and

conditions)

• If admission in non-network hospitals the expenses incurred would be reimbursed

within 14 days from the submission of all documents.

• 20% of co-payment of the admissible claim to be paid by the member if treatment

is taken in a hospital other than a network hospital.

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 15/26

• Waiver of co-payment is available on payment of additional premium.

Cumulative bonus of 5 % added to your sum assured for every claim free year.

• Health Check up at the end of continuous four claim free years.

• Family discount of 5 % is applicable.

Income tax benefit on the premium paid as per section 80-D of the Income Tax Act as

per existing IT law.

• Cumulative bonus of 5 % added to your sum assured for every claim free year.

• Health Check up at the end of continuous four claim free years.

• Income tax benefit on the premium paid as per section 80-D of the Income TaxAct as per existing IT law.

DISADVANTAGE

Pre existing desises are not covered before two years of policy taken.

• 20% of co-payment of the admissible claim to be paid by the member if treatment

is taken in a hospital other than a network hospital.

• No allopathic treatment is not included.

• No dental treatment charges are included.

• No floater facility is available.

NEW INDIA ASSURANCE COMPANY LIMITED

There are two types of health policies being offered by The New India Assurance

Company Ltd for the year 2009-10 as follows:-

1. UNIVERSAL HEALTH INSURANCE SCHEME

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 16/26

2. JAN AROGYA BIMA POLICY

1. UNIVERSAL HEALTH INSURANCE SCHEME - SALIENT

FEATURES

Medical Reimbursement

The policy provides reimbursement of hospitalization expenses upto Rs.30,000/- to an

individual /family, subject to the following sub-limits:-

A. (i) Room, Boarding expenses upto Rs.150/- per day

(ii) If admitted in ICU upto Rs.300/- per day

B. Surgeon, Anesthetist, Consultant, specialists fees, Nursing expenses upto

Rs.4,500/- per illness/ injury

C. Anesthesia, Blood, Oxygen, OT charges, Medicines, Diagnostic material & X-Ray,

Dialysis, Radiotherapy, Chemotherapy, Cost of pacemaker, Artificial limb, etc

upto Rs. 4,500/- per illness/ injury

D. Total expenses incurred for any one illness upto Rs. 15,000/-

Personal Accident Cover

Coverage for Death of the Earning Head of the family (as named in the schedule) due to

accident: Rs. 25,000/-.

Disability Cover

If the earning head of the family is hospitalized due to an accident / illness a

compensation of Rs.50/- per day will be paid per day of hospitalization up to a maximum

of 15 days after a waiting period of 3 days.

For purpose of this POLICY HOSPITAL means:

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 17/26

• Any Hospital/ Nursing home registered with the local authorities and under the

supervision of a registered and qualified Medical practitioner.

• Hospital/ Nursing Home run by Government.

• Enlisted hospitals run by NGOS / Trusts / selected private hospitals with fixed schedule

of CHARGES.

• It should have minimum 15 beds (10 in case of class 'C' cities having a population lest

than 5 lakhs) with fully equipped OT, fully qualified nursing staff round the clock and

fully qualified doctor should be in charge round the clock.

• Hospitalization should be for a minimum period of 24 hrs. However this time limit is

not applied to some specific treatments and also where due to technological advancement

hospitalization for 24 hrs may not be required.

OTHERS FEATURES

• Any One Illness - Will be deemed to mean continuous period of illness and it includes

relapse within 60 days from the date of last consultation with the hospital.

• Age Limitations - This Policy covers people between the age of 3 months to 70 years.

• Family - Means earning head, spouse and up to maximum of three dependent children.

Dependent parents can also be included.

• Floater Basis - The benefit of family will operate on floater basis i.e. the total

reimbursement of Rs.30,000/- can be availed of individually or collectively by members

of the family.

Premium

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 18/26

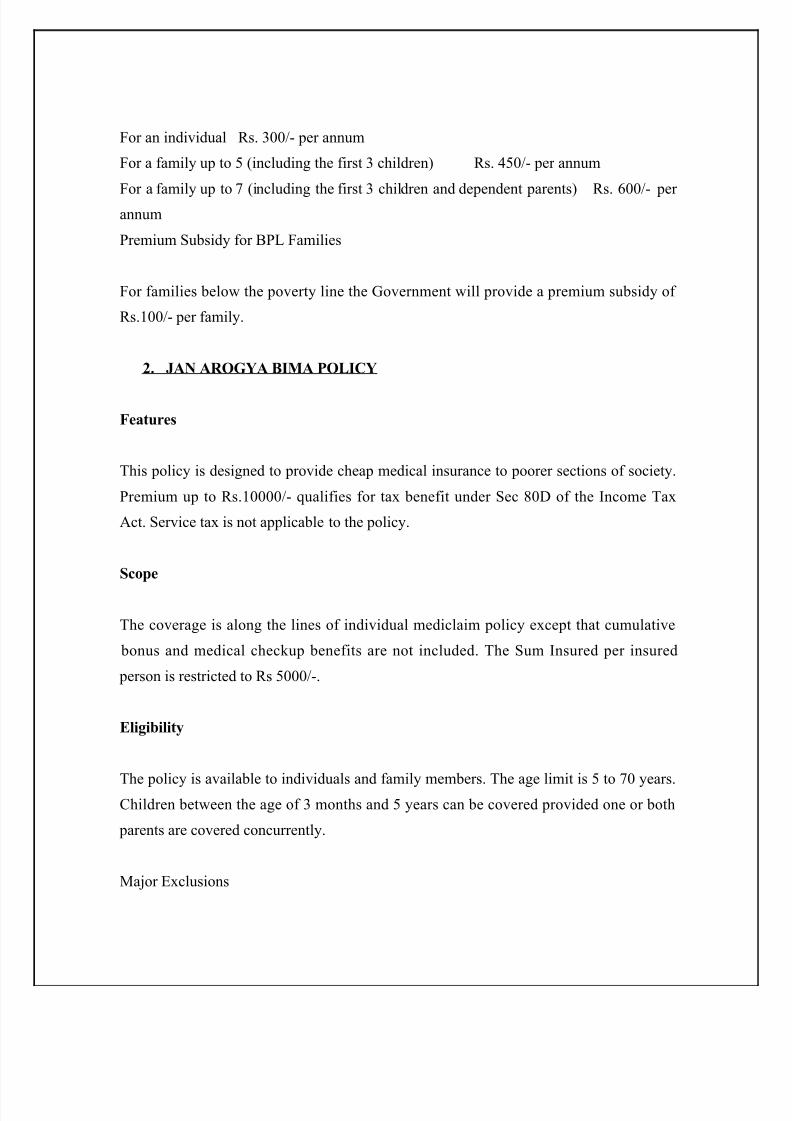

For an individual Rs. 300/- per annum

For a family up to 5 (including the first 3 children) Rs. 450/- per annum

For a family up to 7 (including the first 3 children and dependent parents) Rs. 600/- per annum

Premium Subsidy for BPL Families

For families below the poverty line the Government will provide a premium subsidy of

Rs.100/- per family.

2. JAN AROGYA BIMA POLICY

Features

This policy is designed to provide cheap medical insurance to poorer sections of society.

Premium up to Rs.10000/- qualifies for tax benefit under Sec 80D of the Income Tax

Act. Service tax is not applicable to the policy.

Scope

The coverage is along the lines of individual mediclaim policy except that cumulative

bonus and medical checkup benefits are not included. The Sum Insured per insured

person is restricted to Rs 5000/-.

Eligibility

The policy is available to individuals and family members. The age limit is 5 to 70 years.Children between the age of 3 months and 5 years can be covered provided one or both

parents are covered concurrently.

Major Exclusions

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 19/26

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 20/26

Financial Institutions, Automobile Manufacturers, NGOs and State Governments for

marketing of its Insurance services.

POLICIES OFFERED:

• Personal Line Insurance – insurance of person and property would include

Personal Accident, Mediclaim, Critical Illness, Amartya Siksha Yojana , Motor

Policy - Two Wheelers, Householders Policy, Niwas Yojana , Personal Liability,

Professional Indemnity for a Doctor / Lawyer and others.

• Rural Line Insurance – insurance policies devised for the rural people and weaker

section of urban society like Cattle / Livestock Insurance, Brackish Water Prawn

Insurance, Sericulture Insurance, Horticulture/Plantation Insurance, Kisan

Agriculture Pumpset Insurance and others.

• Industrial Line Insurance – these insurances covers various risks faced by the

industry and are of two types, Project Insurance like Erection All Risk Insurance

and Contractor's All Risk Insurance and Operational Insurance like Fire policy,

Machinery Insurance policy, Electronic Equipment Insurance policy and

Consequential Loss (Fire) policy.

Commercial Line Insurance – the company offers different options to protect thecommercial organizations against the loss of or damage to property and liability arising

out of an action or inaction in the course of the commercial activity

Top of Form

http://w w w .medi National Insuranc National Insuranc This article gives National Insuranc

Bottom of Form

Features of Products and Services

Family Floater Health Insurance Policy wherein entire family will be covered under

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 21/26

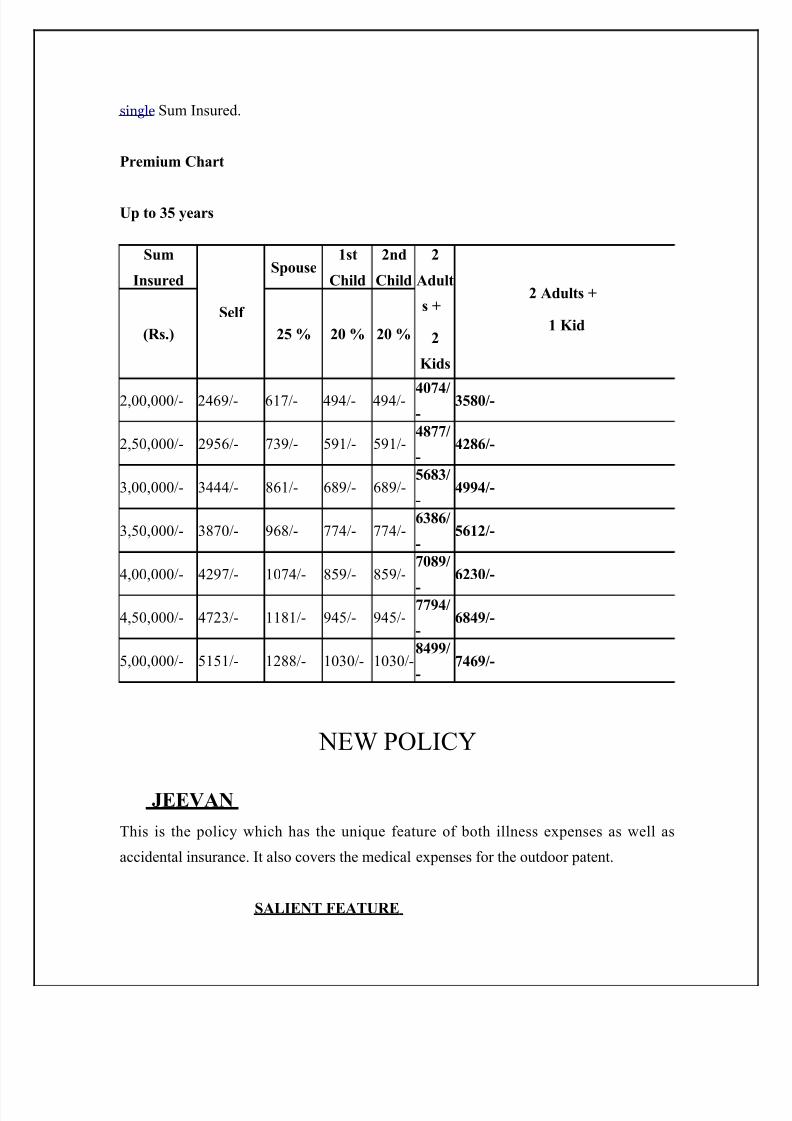

single Sum Insured.

Premium Chart

Up to 35 years

Sum

Insured

Self

Spouse1st

Child

2nd

Child

2

Adult

s +

2

Kids

2 Adults +

1 Kid(Rs.) 25 % 20 % 20 %

2,00,000/- 2469/- 617/- 494/- 494/- 4074/-

3580/-

2,50,000/- 2956/- 739/- 591/- 591/-4877/

-4286/-

3,00,000/- 3444/- 861/- 689/- 689/-5683/

-4994/-

3,50,000/- 3870/- 968/- 774/- 774/-6386/

-5612/-

4,00,000/- 4297/- 1074/- 859/- 859/-7089/

-

6230/-

4,50,000/- 4723/- 1181/- 945/- 945/-7794/

-6849/-

5,00,000/- 5151/- 1288/- 1030/- 1030/-8499/

-7469/-

NEW POLICY

JEEVAN

This is the policy which has the unique feature of both illness expenses as well as

accidental insurance. It also covers the medical expenses for the outdoor patent.

SALIENT FEATURE

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 22/26

The policy is available in two forms.

Only illness Expenses is Paid by the company.

Illness as well as Accidental claim is covered by the company.

If a person is taken only illness policy then they have to payRs.1200 as a premum per month.

BENEFIT

Person can get medical expenses with room charges as well as ambulance charges.It cover pre illness desires like castrates, dental etc.

NO critical pre illness desires is covered under this policy.

Only 50% medical expenses is bear by the company.

Only one time expenses is covered by the company for the pre illness diseases.

Pregnancy related diseases are fully covered by the Company.

Floater facility is available for the family of four people i.e. husband, wife and two

spouse.

If insured person cannot avail the facility of insurance then 5% of the total amount is paid

to the concerned person after 7 year of successful completion of policy.

If person continue the policy for 20 years then he can get 3% of total premium amount

after 20 years. For the person of age more than 55 years and up to 70 years can get the

medical checkup expenses once in a year.

Policy Covers:- Covers medical expenses incurred as an inpatient during hospitalization

for more than 24 hours, including room charges, doctor’s / surgeon’s fee, medicines,

diagnostic tests, etc 30 days pre-hospitalization

• 60 days post-hospitalization

• Pre-existing diseases shall be covered after 2 years of continuous renewal with the

company

• Coverage against Swine Flu / H1N1 influenza in case of hospitalisation~

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 23/26

• Following technologically advanced treatments that do not need 24-hour

hospitalization* but are covered under this policy are::

○ Cataract

○ Dilatation and curettage

○ Cardiac Catheterization

○ Lithotripsy (Kidney Stone removal)

○ Chemotherapy

○ Tonsillectomy

○ Radiotherapy

○ Eye Surgery

FEATURES

PREMIUM is paid monthly for Rs.1800. Person who takes this policy can avail the

benefit of accidental claim also.

ACCIDENTAL CLAIM COVERS:-

Loss of use/Actual loss by

physical separation of

Percentage of Capital Sum

Insured*

Sight of both eyes 100%

Both hands 100%

Both feet 100%

One hand and one foot 100%

One eye and one hand or one

foot

100%

Sight of one eye 50%

One hand or one foot 50%

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 24/26

ILLNESS CLAIM COVERS:- Covers medical expenses incurred as an inpatient during

hospitalization for more than 24 hours, including room charges, doctor’s / surgeon’s fee,

medicines, diagnostic tests, etc 30 days pre-hospitalization

• 60 days post-hospitalization

• Pre-existing diseases shall be covered after 2 years of continuous renewal with the

company

• Coverage against Swine Flu / H1N1 influenza in case of hospitalization~

• Following technologically advanced treatments that do not need 24-hour

HOSPITALIZATION* but are covered under this policy are::

○ Cataract

○ Dilatation and curettage

○ Cardiac Catheterization

○ Lithotripsy (Kidney Stone removal)

○ Chemotherapy

○ Tonsillectomy

○

Radiotherapy

○ Eye Surgery

BENEFIT

Person can get medical expenses with room charges as well as ambulance charges.

It covers pre illness disease like castrates, dental etc.

NO critical pre illness disease is covered under this policy.

Only 50% medical expenses is bear by the company.

Only one time expenses is covered by the company for the pre illness diseasePregnancy related disease is fully covered by the Company.

Floater facility is available for the family of four people i.e. husband, wife and two

spouse.

If insured person cannot avail the facility of insurance then 5% of the total amount is paid

to the concerned person after 7 year of successful completion of policy.

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 25/26

If person continued the policy for 20 years then he can get 3% of total premium amount

after 20 years.

For the person of age more than 55 years and up to 70 years can get the medical checkup

expenses once in a year.

Note:- No Medical Checkup required for the age of up to 55 years.

CONCLUSION

Health systems are complex and fluid entities working at multiple levels; there are no

simple solutions. For the development of equitable and effective health systems,

researchers need to embrace two inter-linked challenges. Firstly, in a context where the

links between poverty, marginalization and (ill) health are so compelling, there is an

urgent need to mainstream an equity or pro-poor approach throughout the research cycle.

In operational research, pro-poor indicators are essential to ensure that equity

considerations do not evaporate, but are central to analysis, dissemination and scale-up.

Secondly researchers need to build partnerships on many fronts: multi-disciplinary

partnerships to ensure that their research does justice to the holistic and complex nature

of health systems; partnerships for capacity building to promote demand, delivery and

uptake of research; and partnerships with the broader research, policy and practice

constituency, from communities to service providers to policy makers, to ensure the

timeliness and relevance of the research agenda and a receptive research-policy-practice

interface. There is no magic formula for these partnerships, as they will need to reflect

different, often fast-moving, institutional contexts, the interplay between vertical and

horizontal approaches to health in specific countries, and particular research foci. The

levels of engagement demanded by these partnerships will take time, energy, skills and

resources. "Methods for partnership development" is a new component for the evolving

health systems research paradigm. We need a global research culture that values andfunds these new levels of engagement from multiple sources including governments,

foundations, and charities.

8/6/2019 Term Parer of Finance

http://slidepdf.com/reader/full/term-parer-of-finance 26/26

REFERENCES

• http://www.nia25.com/

• http://en.wikipedia.org/wiki/ICICI_Lombard

• http://www.icicilombard.com/app/ilom-en/default.aspx

• http://www.icicilombard.com/app/ilom-en/personalproducts/Health/Health-

Advantage.aspx

• http://www.bajajallianzlife.co.in/

• http://www.bajajallianzlife.co.in/category-detail.asp?id=8

• www.newindia.co.in

• http://www.health-policy-systems.com/content/7/1/26

• http://www.medindia.net/patients/insurance/national-insurance-company-

limited-parivar.

• http://www.medindia.net/patients/insurance/national-insurance-company-limited-star-

national-swasthya-bima.htm

http://www.insureurhealth.com/health-insurance-articles/health-insurance-types.htm

Recommended