Selling South Africa in the UK

Bashni MuthayaSATTIC, 2 September 2012

Slide no. 2 © South African Tourism 2012

Agenda

• Megatrends affecting Western Europe

• UK – an important source market

• Trends affecting the UK trade

• How to close the deal

Slide no. 3 © South African Tourism 2012

Megatrends affecting Western Europe

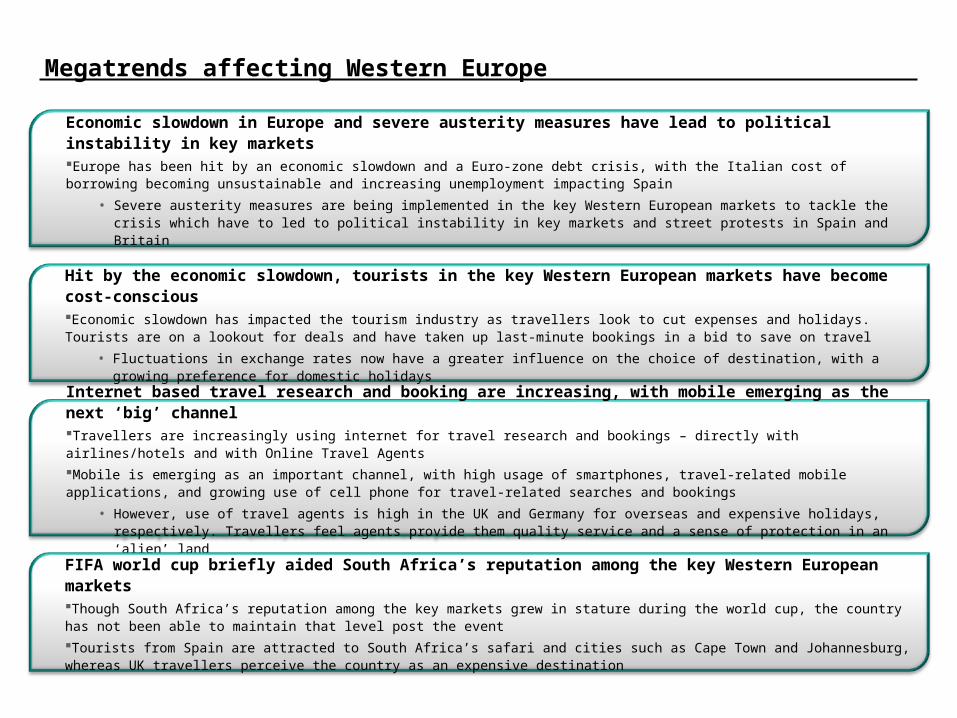

Economic slowdown in Europe and severe austerity measures have lead to political instability in key marketsEurope has been hit by an economic slowdown and a Euro-zone debt crisis, with the Italian cost of borrowing becoming unsustainable and increasing unemployment impacting Spain

• Severe austerity measures are being implemented in the key Western European markets to tackle the crisis which have to led to political instability in key markets and street protests in Spain and Britain

Internet based travel research and booking are increasing, with mobile emerging as the next ‘big’ channelTravellers are increasingly using internet for travel research and bookings – directly with airlines/hotels and with Online Travel Agents

Mobile is emerging as an important channel, with high usage of smartphones, travel-related mobile applications, and growing use of cell phone for travel-related searches and bookings

• However, use of travel agents is high in the UK and Germany for overseas and expensive holidays, respectively. Travellers feel agents provide them quality service and a sense of protection in an ‘alien’ land

Hit by the economic slowdown, tourists in the key Western European markets have become cost-consciousEconomic slowdown has impacted the tourism industry as travellers look to cut expenses and holidays. Tourists are on a lookout for deals and have taken up last-minute bookings in a bid to save on travel

• Fluctuations in exchange rates now have a greater influence on the choice of destination, with a growing preference for domestic holidays

FIFA world cup briefly aided South Africa’s reputation among the key Western European marketsThough South Africa’s reputation among the key markets grew in stature during the world cup, the country has not been able to maintain that level post the event

Tourists from Spain are attracted to South Africa’s safari and cities such as Cape Town and Johannesburg, whereas UK travellers perceive the country as an expensive destination

Slide no. 4 © South African Tourism 2012

EUROPE

The UK is the largest source market for South Africa from Europe. Despite the economic slowdown, the UK travellers’ spend per day in SA has increased since 2008

Note: 1Total Direct Foreign Expenditure, excluding CapexSource: ‘Tourism Flows Outbound in the United Kingdom’, Euromonitor International, Jun 2011; SAT Departure Survey, 2003-2010; Grail Research Analysis of focus group discussions in the UK

Why is the UK Market Important?

Travel is an Integral part of the UK travellers’ lives...

...And despite the economic slowdown, the UK travellers have increased their spending in South

Africa The UK is South Africa’s largest source market from Europe, in terms

of number of travellers

• While outbound travel from the UK declined by 7.8% between 2008-11, arrivals to SA declined by only 1.7% in the same period

• Despite the economic slowdown, the UK travellers’ spend (TFDS1) per day in South Africa grew at CAGR 3.8% between 2008–11

Travel forms an integral part of the UK travellers’ lives. A significant percentage of the population travels for leisure, annually

• After a decline of 14.3% in spending by the UK travellers on international travel in 2009 over 2008, the spending grew by 7.6% in 2009–10, to ~GBP 33.7Bn

• Outbound travel from the UK is forecast to grow by 1.5% p.a. from 2011 to 2016

SOUTH AFRICA

UNITED KINGDO

M

Largest source market from

Europe

Slide no. 5 © South African Tourism 2012

Who are the key UK Traveller Segments?

Key traveller segments from the UK are NSSAs and Wanderlusters, who have extensive international travel experience and seek variety at destinations

Next Stop South Africa (NSSA)

The British NSSA are wealthier, experienced international travellers, with annual household income above GBP 44,000. They are aged between 41 and 65, and do not have any dependant children

NSSAs typically look for natural beauty and authentic cultural experiences. They prefer independent or small group travel, and look for luxury and comfort as part of their experience. They thoroughly research the destination and plan out their holidays, before reaching the destination

Wanderluster

The British Wanderluster segment is made up of younger persons between the ages of 25 and 40, who do not have children. They have considerable travel experience, and have an annual household income above GBP 40,000

Wanderlusters’ desired experiences centre around nature, culture, and adventure. While the economic slowdown has forced Wanderlusters to spend in a targeted manner, they have preferred not to cut spending in travel, as travel forms an integral part of their lives. They have instead reduced their expenditure elsewhere

Source: Grail Research Analysis of focus group discussions in the UK

Slide no. 6 © South African Tourism 2012

UK Strategic Objectives 12/13 Business plan:

Consumer: Enthuse considerers to plan to visit SA now by credibly showcasing SA as an exciting and relaxing holiday that they can afford

Trade: Partner UK TO’s and TA’s to better promote SA as an escape which meets the needs for excitement and relaxation of the UK traveller, by packaging a larger variety of products and experiences and delivering innovative pricing into the market thus improving short term desire to travel to SA

Slide no. 7 © South African Tourism 2012

The British believe in their RIGHT to travel to escape the demands of modern life.

They want to visit iconic sites and also be INSPIRED by special experiences that are unique to them.

They want learn about the LOCAL CULTURE and people at tourist destinations.

Experiences of OTHER PEOPLE, particularly other Brits and the information they ‘discover’ will INSPIRE them to make their travel choices.

They need confirmation that their visit will be a UNIQUE EXPERIENCE exclusive to them alone.

WHO?…..INSIGHT - The UK Consumer

Slide no. 8 © South African Tourism 2012

Source: Grail Research Analysis of focus group discussions in the UK

The UK Travellers’ Travel Planning Process

It all starts with inspiration for the UK travellers. They have a list of destinations in their mind and they aim to shortlist countries to visit from this list

• The list is developed by listening to experiences of other people, reading/ watching things about tourist destination, and ‘iconic’ or ‘unknown/ less-developed’ status of the destinations

The UK travellers then take several factors into consideration for short-listing the destination to visit

• They thoroughly research on parameters such as travel cost, climatic conditions at a destination, and the security situation at the destination, to short-list the destination to visit

The UK travellers then determine the best time to travel to a destination, based on the availability and price of flights and hotel bookings, and seasons/ weather conditions at the destination

The UK travellers refer to multiple information sources for planning their travel, such as travel guides and the Internet

The UK travellers then move on to booking their travel. They conduct extensive research to determine the best bargain deal/ offer for them, along with the most reliable channel for booking

• They prefer booking through a travel agent when travelling to a lesser-known/ unsafe destination, or while planning a complex itinerary

Once a travel destination has been short-listed from the inspiration list, the British extensively research the destination, to plan and book their travel

Slide no. 9 © South African Tourism 2012

The UK Travellers’ Perceptions about South Africa

Source: Grail Research Analysis of focus group discussions in the UK

Seeing the photographs of fellow British travellers/ hearing their experiences about South Africa inspires the British to travel to the country

They believe that if they have a local contact, with whom they can roam around in the country, or if they take a packaged tour, they will be safer when visiting the country

The British have a limited awareness about the variety of experiences on offer in South Africa

• They primarily associate South Africa with crime/ apartheid, wine, wildlife, and Cape Town

• They relate safari/ wildlife more to Kenya than South Africa

The British feel South Africa is unsafe and an ‘unofficial apartheid’ is still prevalent in the country

• They feel that South Africa’s rich and poor are still divided along racial lines

The British believe that crime in South Africa is violent and barbaric. They know that South Africans live in gated communities, and therefore the British feel that their freedom will be curbed when visiting the country

The British feel that South Africans living in the UK are unfriendly, arrogant, and outspoken

Slide no. 10 © South African Tourism 2012

10

Key Messages

Slide no. 11 © South African Tourism 2012

Channel Key Trends in the UK Travel Market

Competitive landscapeCompetitive landscape

Negative Impact of the Global SlowdownNegative Impact of the Global Slowdown

Change in Consumer DemandsChange in Consumer Demands

Increased Role of the InternetIncreased Role of the Internet

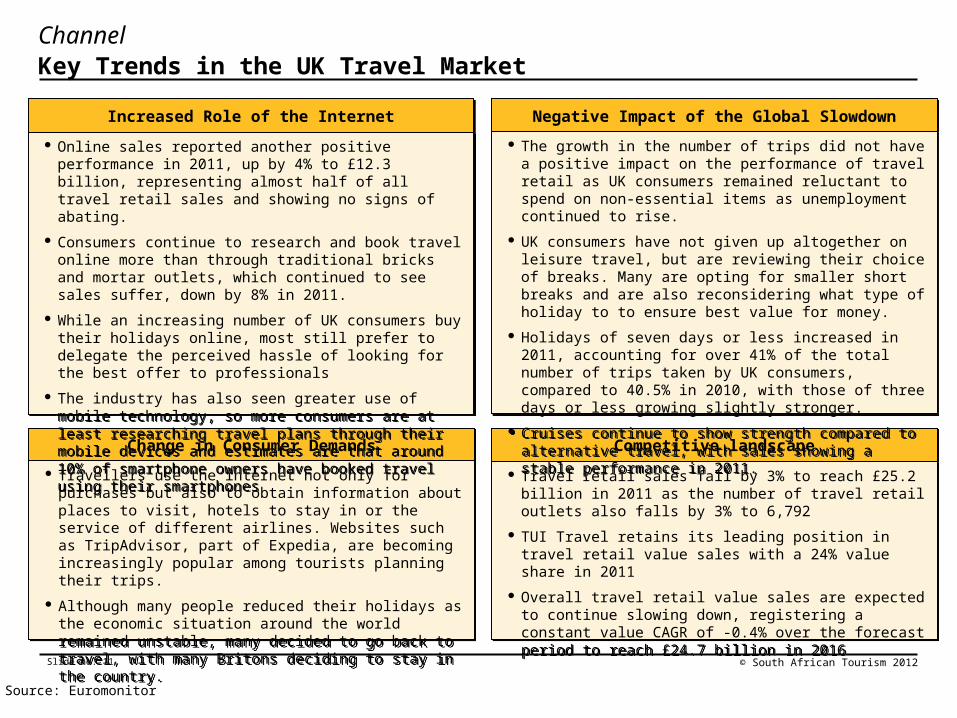

Travel retail sales fall by 3% to reach £25.2 billion in 2011 as the number of travel retail outlets also falls by 3% to 6,792

TUI Travel retains its leading position in travel retail value sales with a 24% value share in 2011

Overall travel retail value sales are expected to continue slowing down, registering a constant value CAGR of -0.4% over the forecast period to reach £24.7 billion in 2016

Travel retail sales fall by 3% to reach £25.2 billion in 2011 as the number of travel retail outlets also falls by 3% to 6,792

TUI Travel retains its leading position in travel retail value sales with a 24% value share in 2011

Overall travel retail value sales are expected to continue slowing down, registering a constant value CAGR of -0.4% over the forecast period to reach £24.7 billion in 2016

The growth in the number of trips did not have a positive impact on the performance of travel retail as UK consumers remained reluctant to spend on non-essential items as unemployment continued to rise.

UK consumers have not given up altogether on leisure travel, but are reviewing their choice of breaks. Many are opting for smaller short breaks and are also reconsidering what type of holiday to to ensure best value for money.

Holidays of seven days or less increased in 2011, accounting for over 41% of the total number of trips taken by UK consumers, compared to 40.5% in 2010, with those of three days or less growing slightly stronger.

Cruises continue to show strength compared to alternative travel, with sales showing a stable performance in 2011.

The growth in the number of trips did not have a positive impact on the performance of travel retail as UK consumers remained reluctant to spend on non-essential items as unemployment continued to rise.

UK consumers have not given up altogether on leisure travel, but are reviewing their choice of breaks. Many are opting for smaller short breaks and are also reconsidering what type of holiday to to ensure best value for money.

Holidays of seven days or less increased in 2011, accounting for over 41% of the total number of trips taken by UK consumers, compared to 40.5% in 2010, with those of three days or less growing slightly stronger.

Cruises continue to show strength compared to alternative travel, with sales showing a stable performance in 2011.

Travellers use the internet not only for purchases but also to obtain information about places to visit, hotels to stay in or the service of different airlines. Websites such as TripAdvisor, part of Expedia, are becoming increasingly popular among tourists planning their trips.

Although many people reduced their holidays as the economic situation around the world remained unstable, many decided to go back to travel, with many Britons deciding to stay in the country.

Travellers use the internet not only for purchases but also to obtain information about places to visit, hotels to stay in or the service of different airlines. Websites such as TripAdvisor, part of Expedia, are becoming increasingly popular among tourists planning their trips.

Although many people reduced their holidays as the economic situation around the world remained unstable, many decided to go back to travel, with many Britons deciding to stay in the country.

Online sales reported another positive performance in 2011, up by 4% to £12.3 billion, representing almost half of all travel retail sales and showing no signs of abating.

Consumers continue to research and book travel online more than through traditional bricks and mortar outlets, which continued to see sales suffer, down by 8% in 2011.

While an increasing number of UK consumers buy their holidays online, most still prefer to delegate the perceived hassle of looking for the best offer to professionals

The industry has also seen greater use of mobile technology, so more consumers are at least researching travel plans through their mobile devices and estimates are that around 10% of smartphone owners have booked travel using their smartphones

Online sales reported another positive performance in 2011, up by 4% to £12.3 billion, representing almost half of all travel retail sales and showing no signs of abating.

Consumers continue to research and book travel online more than through traditional bricks and mortar outlets, which continued to see sales suffer, down by 8% in 2011.

While an increasing number of UK consumers buy their holidays online, most still prefer to delegate the perceived hassle of looking for the best offer to professionals

The industry has also seen greater use of mobile technology, so more consumers are at least researching travel plans through their mobile devices and estimates are that around 10% of smartphone owners have booked travel using their smartphones

Source: Euromonitor

Slide no. 12 © South African Tourism 2012

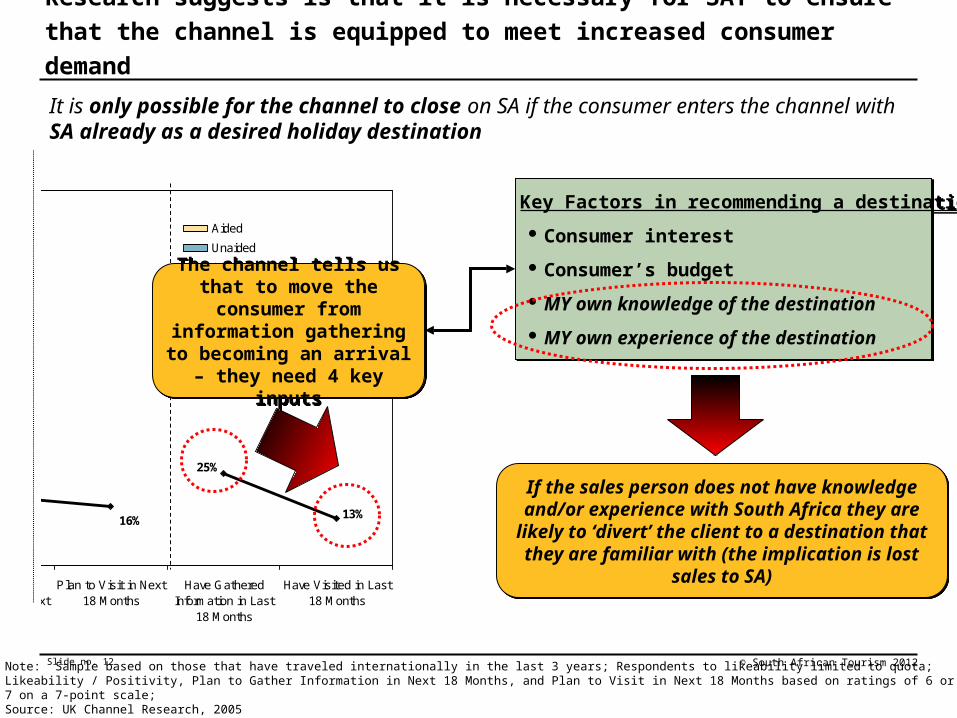

16%

25%

13%

0%

25%

50%

75%

100%

Total Awareness Likeability /Positivity

Consideration Plan to GatherInformation in Next

18 Months

Plan to Visit in Next18 Months

Have GatheredInformation in Last

18 Months

Have Visited in Last18 Months

Aided

Unaided

South Africa

Note: Sample based on those that have traveled internationally in the last 3 years; Respondents to likeability limited to quota; Likeability / Positivity, Plan to Gather Information in Next 18 Months, and Plan to Visit in Next 18 Months based on ratings of 6 or 7 on a 7-point scale; Source: UK Channel Research, 2005

Research suggests is that it is necessary for SAT to ensure that the channel is equipped to meet increased consumer demand

It is only possible for the channel to close on SA if the consumer enters the channel with SA already as a desired holiday destination

Key Factors in recommending a destination:

Consumer interest

Consumer’s budget

MY own knowledge of the destination

MY own experience of the destination

Key Factors in recommending a destination:

Consumer interest

Consumer’s budget

MY own knowledge of the destination

MY own experience of the destination

If the sales person does not have knowledge and/or experience with

South Africa they are likely to ‘divert’ the client to a destination that they are

familiar with (the implication is lost sales to SA)

If the sales person does not have knowledge and/or experience with

South Africa they are likely to ‘divert’ the client to a destination that they are

familiar with (the implication is lost sales to SA)

The channel tells us that to move the consumer from

information gathering to becoming an arrival

– they need 4 key inputs

The channel tells us that to move the consumer from

information gathering to becoming an arrival

– they need 4 key inputs

Slide no. 13 © South African Tourism 2012

1.6

1.6

1.7

1.7

1.8

1.8

1.9

2.2

2.3

2.4

2.5

2.6

1 2 3 4

In addition to being equipped, the channel also needs to be able to offer the right product; price is a major product barrier

Please Indicate the Degree to Which You Feel That Each of the Following is a Barrier For You Selling South Africa More Often

Flights to the destination are too expensive

I do not feel the destination is safe

High capacity utilization on the flights

Packages to the destination are too expensive

I do not feel familiar with the destination

Destination does not represent good value for money

Lack of easy access to information on activities and / or hotels

Consumers are not interested in visiting the destination

There are not enough / type of tour packages offered

Flight schedules to the destination are not convenient

Destination does not offer comparable cultural experience

Destination does not offer as many interesting activities

Price is a recurring theme in the U.K.

Ave = 2.0

Note: 1=Not a barrier, 5=Significant barrierSource: U.K. Channel Research (2005)

Minimum Service Level

Minimum Service Level

Intermediate

Service Level

Intermediate

Service Level

Advanced Service Level

Advanced Service Level

Customized Bi-Annual Consumer Newsletter

Access to Work-shops

Prioritized Access to Printed Collateral

Access to Trade-Only Call-Centre

Reactive Access to Collateral

Access to Trade-Only Internet Site

Monthly Trade Newsletter

ImportantImportant PriorityPriority

JMAs

‘Fam’-trips

Preferential Call-Centre Access / Trade Mgr Access

Support In-house Educational / Training

Programs

Co-Sponsorship of Pages in Brochures

Chain TAs

and

Conglomerat

esIndependent

and Affi

liate

d

TAs Pure P

lay

TOsTOs w

ith a

Retail A

gent

StandardStandard

SAT evaluates ROI on investing in brochures vs other media

Channel Wish List:

Services desired by channel

Legend

Services SAT provides to the channel

For the U.K. market, the types of channel players have been prioritized and allocated to a particular service model

How are we doing?

• Trade trained: 2008 = 1,925 2009 = 2,085 2010 = 1,926 2011 = 1,729

• JMAs signed to date: 14

Thank you

Recommended