3I INFOTECH LTD, VASHI

RETAIL BANKING INDUSTRY

- Now and Future Trends

MayurSN

5/11/2015

The document exhibits the present status of retail banking industry in India and the future potential in Mobile Banking.

MayurSN

Retail Banking Industry – Now and Future

Pag

e1

CONTENTS INTRODUCTION: ........................................................................................................................................ 2

OVERALL CUSTOMER EXPERIENCE STAGNATED, BUT EXTREME ENDS OF POSITIVE AND NEGATIVE

EXPERIENCES INCREASED .......................................................................................................................... 2

GROWTH OF LOW COST CHANNELS FAILS TO DISPLACE BRANCH USAGE ............................................... 3

UNPRECEDENTED ADVANCEMENT IN REACH ........................................................................................... 4

FUNDAMENTAL SHIFT IN NATURE AND INTENSITY OF COMPETITION: WAR FOR TRANSACTIONS ......... 5

INDIA’S DIGITAL STATISTICS – 2015 .......................................................................................................... 7

RETAIL BANKING INDUSTRY TRENDS ........................................................................................................ 9

Customers Redefine the Rules of the Game ......................................................................................... 9

INDIAN RETAIL BANKING IN FUTURE ...................................................................................................... 10

THE TOP 10 RETAIL BANKING TRENDS AND PREDICTIONS FOR 2015 ARE: ............................................ 11

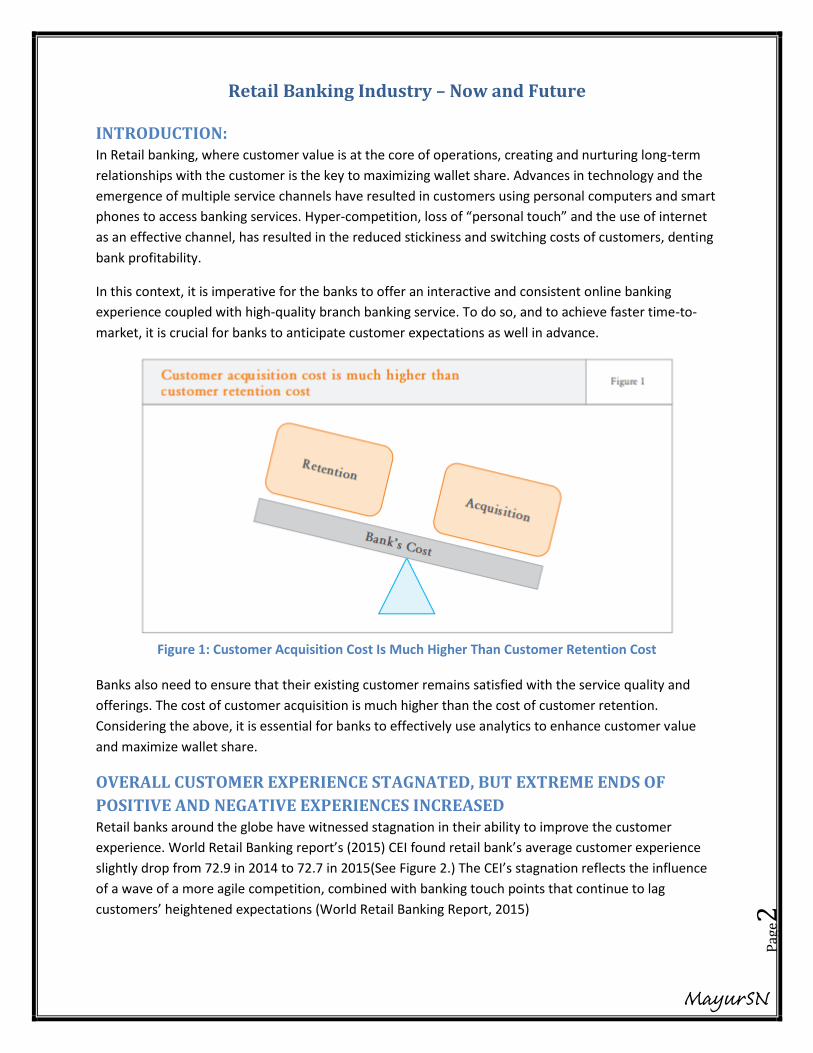

Figure 1: Customer Acquisition Cost Is Much Higher Than Customer Retention Cost ................................. 2

Figure 2: Customer Experience Index (CEI), by Country 2015 ...................................................................... 3

Figure 3: Customers Using Channels at least weekly (%), 2014-2015 .......................................................... 4

Figure 4: Different Digital India – Smart Phones to become Primary Banking Channel in 5 Years. ............. 5

Figure 5: Growth in Digital Transactions Followed by ATM/CDM ................................................................ 6

Figure 6: Competition in Transaction is expected to rise dramatically ........................................................ 7

Figure 7: Distribution of Mobile Users in India ............................................................................................. 7

Figure 8: Number of Internet Users in India (2013 to 2018e) ...................................................................... 8

Figure 9: Mobile Banking Users Statistics ..................................................................................................... 8

Figure 10: From “Bell Curve” to “Well Curve” – Customer Demand is Polarizing ........................................ 9

MayurSN

Retail Banking Industry – Now and Future

Pag

e2

INTRODUCTION: In Retail banking, where customer value is at the core of operations, creating and nurturing long-term

relationships with the customer is the key to maximizing wallet share. Advances in technology and the

emergence of multiple service channels have resulted in customers using personal computers and smart

phones to access banking services. Hyper-competition, loss of “personal touch” and the use of internet

as an effective channel, has resulted in the reduced stickiness and switching costs of customers, denting

bank profitability.

In this context, it is imperative for the banks to offer an interactive and consistent online banking

experience coupled with high-quality branch banking service. To do so, and to achieve faster time-to-

market, it is crucial for banks to anticipate customer expectations as well in advance.

Banks also need to ensure that their existing customer remains satisfied with the service quality and

offerings. The cost of customer acquisition is much higher than the cost of customer retention.

Considering the above, it is essential for banks to effectively use analytics to enhance customer value

and maximize wallet share.

OVERALL CUSTOMER EXPERIENCE STAGNATED, BUT EXTREME ENDS OF

POSITIVE AND NEGATIVE EXPERIENCES INCREASED Retail banks around the globe have witnessed stagnation in their ability to improve the customer

experience. World Retail Banking report’s (2015) CEI found retail bank’s average customer experience

slightly drop from 72.9 in 2014 to 72.7 in 2015(See Figure 2.) The CEI’s stagnation reflects the influence

of a wave of a more agile competition, combined with banking touch points that continue to lag

customers’ heightened expectations (World Retail Banking Report, 2015)

Figure 1: Customer Acquisition Cost Is Much Higher Than Customer Retention Cost

MayurSN

Retail Banking Industry – Now and Future

Pag

e3

GROWTH OF LOW COST CHANNELS FAILS TO DISPLACE BRANCH USAGE The internet has quickly become the most-favored channel by customers in all regions. Already high

levels of Internet usage rose further throughout the last year, resulting in all the regions having at or

close to two-thirds of their customer accessing banking websites at least weekly. Across most region,

mobile usage is at or close to one-third of customers accessing it at least weekly.

While customers have quickly adapted to the idea of tapping into the internet and/or mobile devices to

check their balances, in customer view, the branch remains the last resort to handle practically any

other type of matter. Even when it comes to simple products like current accounts and credit cards,

research found customers still overwhelmingly conduct the application process in the branch versus via

the Internet or mobile.

Figure 2: Customer Experience Index (CEI), by Country 2015

MayurSN

Retail Banking Industry – Now and Future

Pag

e4

Figure 3: Customers Using Channels at least weekly (%), 2014-2015

UNPRECEDENTED ADVANCEMENT IN REACH

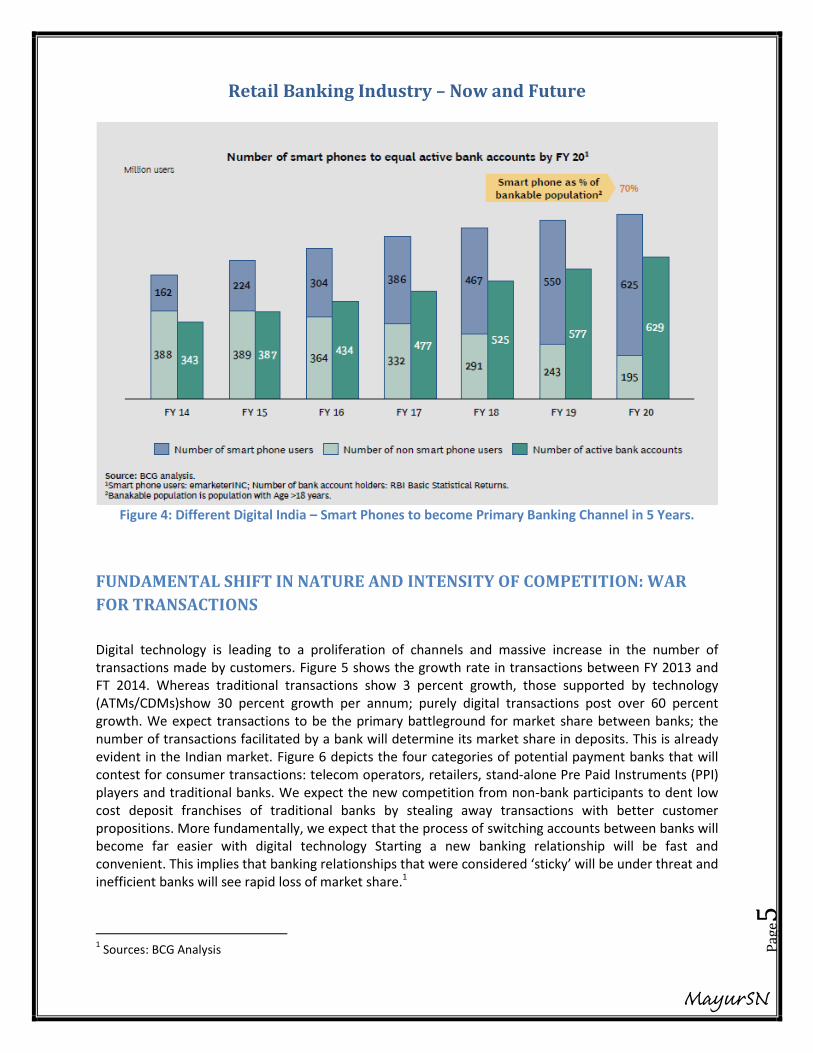

The digital revolution is upon us in its full glory. Technology is advancing by the day. Affordable smartphones and high bandwidth access will reach an unprecedented number of Indian consumers in the coming years. The Indian Government’s ambitious vision for a digital India emboldens us to predict that within the next five years we will see a new, digitally savvy Indian consumer emerging across urban as well as rural markets. As depicted in figure 4, by 2020 we expect the number of smart phone users to equal the number of active bank accounts in the country, and cover 70-80 percent of the eligible population. It is possible to envisage that almost all eligible customers will be on-boarded onto the mobile phone-based digital payment and savings platform in next five years. A similar revolution is conceivable on the lending side. The phenomenal impact of the information bureau on the retail lending business in India is evident in the continuously declining NPA ratio of retail lending for banks. Extension of the information bureau to cover a larger population will lead to a majority of Indian people who are self-employed, or employed in the unorganized sector, to have credit history and eligibility for credit from the banking sector. Incorporation of telecom and electricity bill payment records into the credit information bureau can unleash this enormous potential to extend the penetration of banking in India.

MayurSN

Retail Banking Industry – Now and Future

Pag

e5

Figure 4: Different Digital India – Smart Phones to become Primary Banking Channel in 5 Years.

FUNDAMENTAL SHIFT IN NATURE AND INTENSITY OF COMPETITION: WAR

FOR TRANSACTIONS

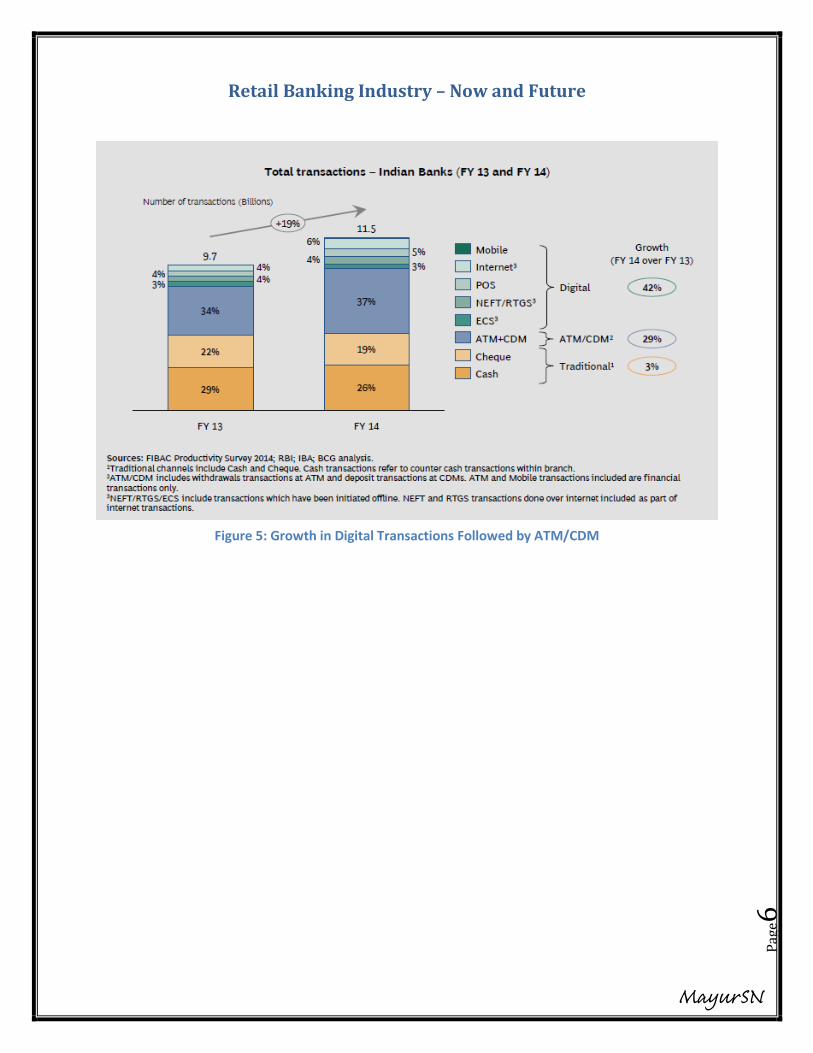

Digital technology is leading to a proliferation of channels and massive increase in the number of transactions made by customers. Figure 5 shows the growth rate in transactions between FY 2013 and FT 2014. Whereas traditional transactions show 3 percent growth, those supported by technology (ATMs/CDMs)show 30 percent growth per annum; purely digital transactions post over 60 percent growth. We expect transactions to be the primary battleground for market share between banks; the number of transactions facilitated by a bank will determine its market share in deposits. This is already evident in the Indian market. Figure 6 depicts the four categories of potential payment banks that will contest for consumer transactions: telecom operators, retailers, stand-alone Pre Paid Instruments (PPI) players and traditional banks. We expect the new competition from non-bank participants to dent low cost deposit franchises of traditional banks by stealing away transactions with better customer propositions. More fundamentally, we expect that the process of switching accounts between banks will become far easier with digital technology Starting a new banking relationship will be fast and convenient. This implies that banking relationships that were considered ‘sticky’ will be under threat and inefficient banks will see rapid loss of market share.1

1 Sources: BCG Analysis

MayurSN

Retail Banking Industry – Now and Future

Pag

e6

Figure 5: Growth in Digital Transactions Followed by ATM/CDM

MayurSN

Retail Banking Industry – Now and Future

Pag

e7

Figure 6: Competition in Transaction is expected to rise dramatically

INDIA’S DIGITAL STATISTICS – 2015 2

Figure 7: Distribution of Mobile Users in India

2 Sources: www.wearesocial.com

MayurSN

Retail Banking Industry – Now and Future

Pag

e8

Figure 8: Number of Internet Users in India (2013 to 2018e)

Figure 9: Mobile Banking Users Statistics

MayurSN

Retail Banking Industry – Now and Future

Pag

e9

RETAIL BANKING INDUSTRY TRENDS

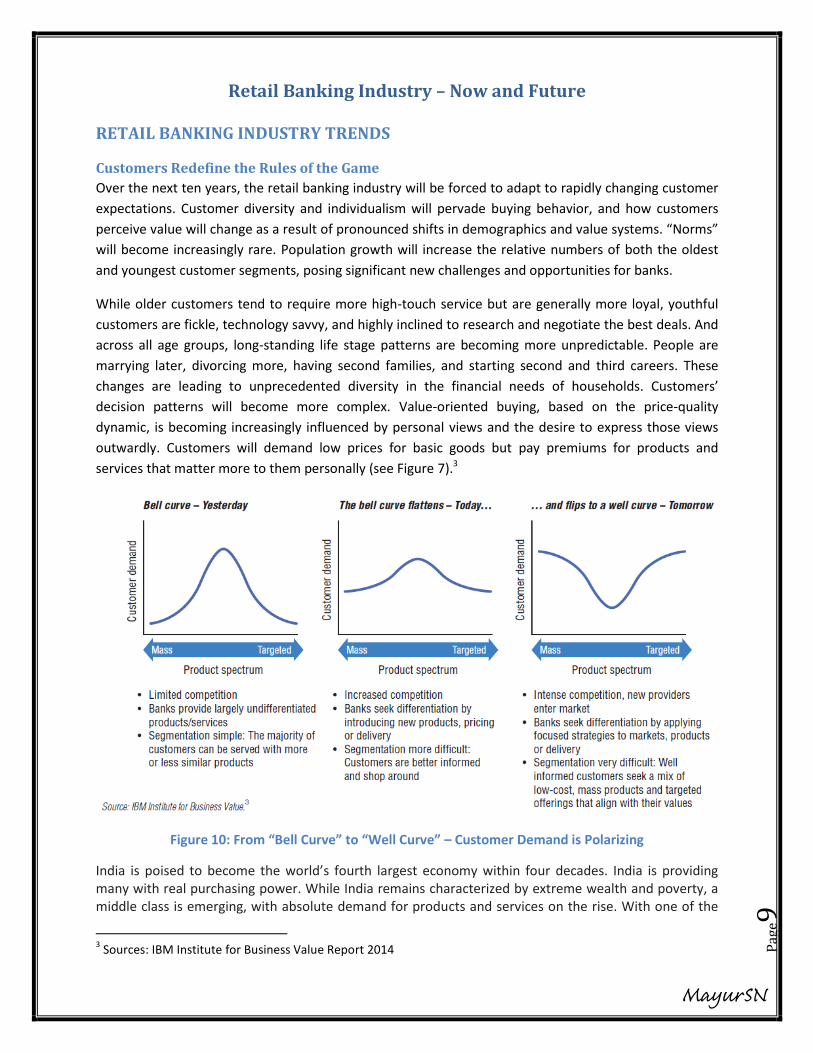

Customers Redefine the Rules of the Game

Over the next ten years, the retail banking industry will be forced to adapt to rapidly changing customer

expectations. Customer diversity and individualism will pervade buying behavior, and how customers

perceive value will change as a result of pronounced shifts in demographics and value systems. “Norms”

will become increasingly rare. Population growth will increase the relative numbers of both the oldest

and youngest customer segments, posing significant new challenges and opportunities for banks.

While older customers tend to require more high-touch service but are generally more loyal, youthful

customers are fickle, technology savvy, and highly inclined to research and negotiate the best deals. And

across all age groups, long-standing life stage patterns are becoming more unpredictable. People are

marrying later, divorcing more, having second families, and starting second and third careers. These

changes are leading to unprecedented diversity in the financial needs of households. Customers’

decision patterns will become more complex. Value-oriented buying, based on the price-quality

dynamic, is becoming increasingly influenced by personal views and the desire to express those views

outwardly. Customers will demand low prices for basic goods but pay premiums for products and

services that matter more to them personally (see Figure 7).3

Figure 10: From “Bell Curve” to “Well Curve” – Customer Demand is Polarizing

India is poised to become the world’s fourth largest economy within four decades. India is providing many with real purchasing power. While India remains characterized by extreme wealth and poverty, a middle class is emerging, with absolute demand for products and services on the rise. With one of the

3 Sources: IBM Institute for Business Value Report 2014

MayurSN

Retail Banking Industry – Now and Future

Pag

e10

most under penetrated retail lending markets in Asia Pacific, India offers great potential for the future of banking.

Industry executives’ estimate that India’s retail lending has grown by 30 percent a year in the past few years, and mortgages, which make up half the total, have been rising at an even brisker pace.

According to a study sponsored by Visa International, the number of credit and debit cards grew at an annual rate of 55 percent in the seven years to 2004. Indian citizens now hold 44 million cards, 14 million of which are credit cards.

INDIAN RETAIL BANKING IN FUTURE

Is expected to grow exponentially supported by technology intensive processes and customer friendly models with focus on convenience and cost effectiveness. A report titled Indian Banking 2020: Making Decade’s Promise come True brought out by the Boston Consulting Group in 2010 had identified ten broad trends for the Indian banking. These and a few other areas which should receive the attention of banks seeking opportunities for sustainable growth are summarized below:-

Retail banking will be immensely benefited from the Indian demographic dividend. It is important to note that the middle class population is expected to touch 200 million by 2020 and 475 million by 2027. This would imply mortgages would grow fast and likely to cross `40 trillion by 2020;

Another segment that will provide huge opportunities will be the financing of affordable housing for growing ‘low’ & ‘middle’ class;

Rapid accumulation of wealth in rich households will drive wealth management to 10X size;

“The Next Billion” consumer segment will emerge as the largest in terms of numbers and will accentuate the demand for low cost banking solutions and innovative operating models, throwing up a big market of small customers;

Branches and ATMs will need to grow 2X and 5X respectively to serve the huge addition to bankable population. Low cost branch network with smaller sized branches will be adopted;

Mobile banking will come of age with widespread access to internet on mobile reaping the benefit of the high mobile density in the country;

Banks will have to adopt CRM and data warehousing in a major way to reduce customer acquisition costs and improve risk management. Banks will have to understand and adopt new technologies like, cloud computing and invest significantly in analytics based on big data;

Margins will see downward pressure both in retail and corporate banking, spurring banks to generate more fees and improve operating efficiency;

Although banks will continue to focus on domestic business, given the rising trend of globalization, cross-border banking business will need more attention. As per a recent World Bank report, India retained its topmost position with US$ 70 billion in remittances in 2013 followed by China (US$ 60 billion), the Philippines (US$ 25 billion), Mexico (US$ 22 billion), Nigeria (US$ 21 billion), Egypt (US$

17 billion), Pakistan (US$ 15 billion) and Bangladesh (US$ 14 billion). 4 (Shri Harun R Khan, June 2014)

4 (Shri Harun R Khan, June 2014)

MayurSN

Retail Banking Industry – Now and Future

Pag

e11

THE TOP 10 RETAIL BANKING TRENDS AND PREDICTIONS FOR 2015 ARE: 1. Using Customer Analytics to Drive Contextual Experiences

2. Expedited Deployment of Digital Delivery

3. Mobile-First Design

4. Increasing Digital and Social Selling

5. Mass Market Acceptance of Mobile Payments

6. Focus on Security and Authentication 7. Industry Consolidation

8. Enhanced Customer Incentivisation

9. Investment in Innovation, Incubation and Uncommon Alliances

10. Increased Impact of Digital Disruptors5

5 Sources: http://thefinancialbrand.com/46189/2015-top-banking-trends-predictions-forecast-digital-disruption/

MayurSN

Retail Banking Industry – Now and Future

Pag

e12

BIBLIOGRAPHY (2015). World Retail Banking Report. Capgemini & EFMA.

Shri Harun R Khan, D. G. (June 2014). Banks in India: Challenges & Opportunities. BFSI Conference 2014

organized by SBICap Securities. Mumbai: www.rbi.org.in.

SOURCES: http://thefinancialbrand.com/46189/2015-top-banking-trends-predictions-forecast-digital-

disruption/

(Shri Harun R Khan, June 2014)

IBM Institute for Business Value Repot 2014

BCG Analysis

MayurSN

Recommended