May 24, 2018

ICICI Securities Ltd | Retail Equity Research

Result Update

Healthy EBITDA/t despite input pressure…

Ramco reported a mixed set of Q4FY18 numbers. Revenues increased

22.3% YoY to | 1,254.8 crore (vs. I-direct estimate of | 1,206.5 crore) led

by 20.2% YoY increase in volumes to 2.7 MT (vs. I-direct estimate of 2.6

MT) due to higher sales in eastern region. Further, realisation increased

1.8% YoY to | 4,586 (vs. I-direct estimate of | 4,710)

EBITDA/t declined 16.4% YoY to | 995/t (vs. I-direct estimate of

| 1,098/t) mainly led by 30.7% YoY increase in power cost/t and 12.6%

YoY increase in freight cost/t

The company has reduced its debt by | 310 crore and recommended a

dividend of | 3/share in FY18. The company plans to add 1.5 MT clinker

capacity at Andhra Pradesh for | 680 crore. This expansion is in addition

to 3 MT capacity expansion announced by the company previously

Operating markets key beneficiary of increased infra spends…

The pick-up in road tendering activity, improved sand availability in the

company’s operating markets and healthy demand from government’s low

cost housing programme are expected to be key drivers of cement demand.

As a result, we expect demand (15 MT) to outpace supply (7 MT) positively

impacting utilisation levels. Consequently, we expect Ramco’s operating

markets to register growth of 7-8% over the next three to four years.

Capacity expansion to further drive growth…

The company has over the years penetrated the West Bengal and Odisha

market. Ramco is planning to further penetrate in the east through capacity

expansion. Of the 4.5 MT capacity expansion planned by the company, 2 MT

will be in the east (1 MT each in West Bengal, Odisha) while 2.5 MT will be

set up in the south (in Andhra Pradesh). The capacity expansion in the east

will enable the company to remove capacity constraint and also increase its

market share. Apart from expansion in the east, the capacity expansion in AP

(south) will enable it to tap the growing opportunity of this market (that is

expected to grow at 14% CAGR in the next two to three years).

Healthy cash flow generation to keep balance sheet light!

During the downturn in the south in FY10-15, efficient management of cash

flows has enabled the company to reduce debt-equity from 1.6x to 1.0x in

FY15 and further to 0.3x in FY18. Going forward, we believe the company’s

robust cash flow generation (~| 2,500 crore in FY18-20E) will not only

enable to fund its capex through internal accruals but also maintain its debt-

equity at 0.3x.

Better sand availability, improving margins key positives; maintain BUY

Better sand availability in Tamil Nadu, one of the key markets of Ramco

Cement (~60% of capacity share), is expected to be a key contributor to

volume growth in coming years. This coupled with higher penetration in the

eastern markets will give a tailwind to overall volume growth. Apart from

higher penetration in the east, we expect the southern region to witness an

upturn mainly led by higher government spending on low cost housing,

irrigation and other infra projects. Considering this, coupled with capacity

expansion we expect revenues to grow at a CAGR of 14.1% in FY18-20E. In

addition, we expect the EBITDA margin to improve from FY18 onwards

mainly led by stabilisation of power costs and improvement in freight costs.

Considering the capacity expansion, better leverage (D/E: 0.3x) and cost

efficiency, Ramco is currently trading at attractive valuations. Hence, we

maintain our BUY rating on the stock with an SOTP based target price of

| 930 (i.e. 15x FY20E EV/EBITDA).

Ramco Cements (RAMCEM) | 795

Rating matrix

Rating : Buy

Target : | 930

Target Period : 9-12 months

Potential Upside : 17%

What’s changed?

Target Price

EPS FY19E

EPS FY20E

Rating

Changed from | 822 to | 930

Changed from | 30.1 to | 29.1

Unchanged

Changed from | 37.3 to | 35.0

Quarterly performance

Q4FY18 Q4FY17 YoY (%) Q3FY18 QoQ (%)

Revenue 1,254.8 1,026.2 22.3 1,056.4 18.8

EBITDA 272.2 270.8 0.5 235.3 15.7

EBITDA (%) 21.7 26.4 -470 bps 22.3 -58 bps

PAT 108.6 134.5 -19.2 122.7 -11.5

Key financials

FY17 FY18 FY19E FY20E

Net Sales 3949.5 4406.4 4983.2 5734.0

EBITDA 1176.4 1099.4 1333.2 1587.2

Net Profit 649.3 555.7 684.5 825.1

EPS (|) 27.3 23.5 29.1 35.0

Valuation summary

(x) FY17 FY18 FY19E FY20E

P/E 29.0 33.7 27.3 22.6

Target P/E 34.1 39.6 32.0 26.5

EV/EBITDA 17.1 18.0 15.2 12.7

EV/Tonne (US$) 203.5 200.3 192.6 159.8

P/BV 5.0 4.6 4.1 3.6

RoNW (%) 17.4 13.7 15.2 16.1

RoCE (%) 12.7 10.4 11.5 12.2

Stock data

Particulars Amount (| crore)

Market Capitalisation 18855.7

Total Debt (FY18) 1113.2

Cash (FY18) 146.8

EV 19822.1

52 week H/L (|) 879/649

Equity Capital 23.6

Face Value (|) 1.0

Price performance

1M 3M 6M 12M

ACC -12.7 -16.7 -22.0 -17.7

UltraTech Cement -3.3 -7.4 -9.6 -11.1

Ramco Cement 1.9 16.3 15.9 20.4

Research Analyst

Rashesh Shah

Devang Bhatt

ICICI Securities Ltd | Retail Equity Research Page 2

Variance analysis

Q4FY18 Q4FY18E Q4FY17 YoY (%) Q3FY18 QoQ (%) Comments

Net Sales 1,254.8 1,206.5 1,026.2 22.3 1,056.4 18.8 20.2% YoY growth in volumes led to a rise in revenues during the quarter

Other income 19.0 5.8 6.5 193.8 5.2 268.4

Raw Material Expenses 168.4 157.3 123.6 36.3 143.3 17.6

Employee Expenses 73.8 73.2 67.3 9.7 75.9 -2.8

Power and fuel 217.6 197.5 138.5 57.1 170.8 27.4

Higher pet coke prices and exhaustion of low cost pet coke inventory led to

increase in power and fuel cost

Freight 354.1 329.6 261.6 35.3 284.0 24.7 The rise in freight cost was mainly due to increase in diesel prices

Others 168.7 167.7 164.4 2.6 147.1 14.7

EBITDA 272.2 281.3 270.8 0.5 235.3 15.7

EBITDA Margin (%) 21.7 23.3 26.4 -470 bps 22.3 -58 bps The fall in EBITDA margins was mainly due to increase in operating expenses

Interest 10.5 29.6 20.1 -48.0 16.0 -34.7

Depreciation 75.4 69.9 85.4 -11.6 73.0 3.4

PBT 205.3 187.6 171.8 19.5 151.5 35.6

Total Tax 96.7 46.9 37.3 159.1 28.7 236.9

Reported PAT 108.6 140.7 134.5 -19.2 122.7 -11.5

Adjusted PAT 108.6 140.7 134.5 -19.2 122.7 -11.5 Higher tax expanses and lower operating margins led to decline in PAT

Key Metrics

Volume (MT) 2.74 2.56 2.28 20.2 2.27 20.3

Higher sales in the east and improving demand in Tamil Nadu led to increase in

volumes in the quarter

Realisation (|) 4,586 4,710 4,507 1.8 4,645 -1.3 Prices remained stable in south

EBITDA per Tonne (|) 995 1,098 1,189 -16.4 1,035 -3.9 The fall in EBITDA/t was mainly led by higher power & fuel cost

Source: Company, ICICI Direct Research

Change in estimates

(| Crore) Old New % Change Old New % Change Comments

Revenue 4,878.4 4,983.2 2.1 5,610.6 5,734.0 2.2

We expect revenues to increase at a CAGR of 14.1% over FY18-

20E mainly led by capacity expansion and increased penetration in

the east

EBITDA 1,326.4 1,333.2 0.5 1,557.9 1,587.2 1.9

EBITDA Margin (%) 27.2 26.8 -44 bps 27.8 27.7 -9 bps We expect EBITDA margin to improve led by cost efficiency

PAT 709.4 684.5 -3.5 878.0 825.1 -6.0

EPS (|) 30.1 29.1 -3.5 37.3 35.0 -6.1

FY19E FY20E

Source: Company, ICICI Direct Research

Assumptions

Comments

FY16 FY17 FY18 FY19E FY20E FY19E FY20E

Volume (MT) 7.2 8.3 9.3 10.3 11.6 10.1 11.3

Better sand availability in Tamil Nadu and higher government

spend to drive volumes over the next three years

Realisation (|) 4,940 4,731 4,732 4,824 4,934 4,847 4,955

EBITDA per Tonne (|) 1,482 1,409 1,181 1,291 1,366 1,318 1,376

We expect company to register EBITDA/t of above | 1300 in

FY20E

EarlierCurrent

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 3

Company Analysis

Operating markets key beneficiary of increased infra spends…

The pick-up in road tendering activity, improved sand availability in the

company’s operating markets and healthy demand from the government’s

low cost housing programme are expected to be key drivers of cement

demand. In addition, we expect an improvement in pricing to continue in the

company’s key markets led by pick up in demand. Consequently, we expect

Ramco to register revenue growth of 14.1% over FY18-20E.

Cement demand in south to outpace capacity expansion…

New capacity expansion in the southern region in FY14-18 slowed down to

10 MT vs. about 27 MT in the preceding four years. Going forward, we

expect capacity expansion to further slow down to ~7 MT in FY18-20E.

Hence, supply pressure from new players/capacity should remain low.

Further, with an improvement in demand led by infra projects and individual

house builders, we expect demand (15 MT) to outpace supply (7 MT)

positively impacting utilisation levels. We expect utilisation to improve from

57% in FY18 to 63% in FY20E thereby positively impacting margins levels.

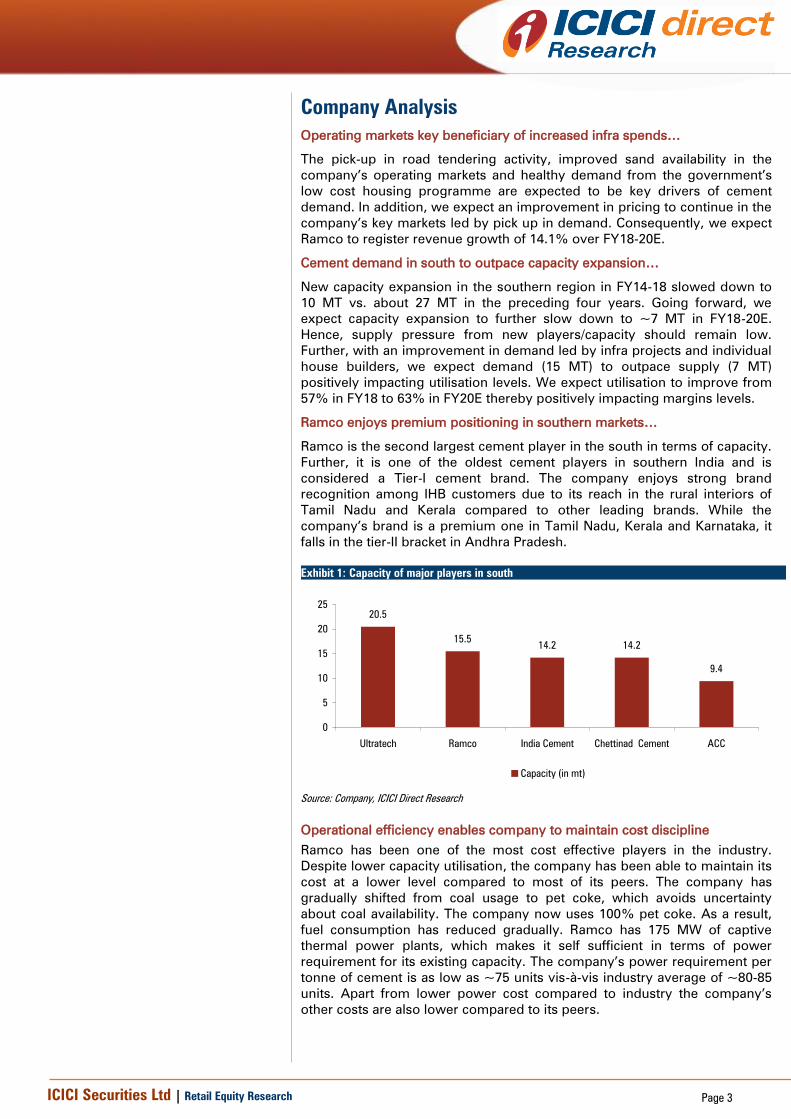

Ramco enjoys premium positioning in southern markets…

Ramco is the second largest cement player in the south in terms of capacity.

Further, it is one of the oldest cement players in southern India and is

considered a Tier-I cement brand. The company enjoys strong brand

recognition among IHB customers due to its reach in the rural interiors of

Tamil Nadu and Kerala compared to other leading brands. While the

company’s brand is a premium one in Tamil Nadu, Kerala and Karnataka, it

falls in the tier-II bracket in Andhra Pradesh.

Exhibit 1: Capacity of major players in south

20.5

15.514.2 14.2

9.4

0

5

10

15

20

25

Ultratech Ramco India Cement Chettinad Cement ACC

Capacity (in mt)

Source: Company, ICICI Direct Research

Operational efficiency enables company to maintain cost discipline

Ramco has been one of the most cost effective players in the industry.

Despite lower capacity utilisation, the company has been able to maintain its

cost at a lower level compared to most of its peers. The company has

gradually shifted from coal usage to pet coke, which avoids uncertainty

about coal availability. The company now uses 100% pet coke. As a result,

fuel consumption has reduced gradually. Ramco has 175 MW of captive

thermal power plants, which makes it self sufficient in terms of power

requirement for its existing capacity. The company’s power requirement per

tonne of cement is as low as ~75 units vis-à-vis industry average of ~80-85

units. Apart from lower power cost compared to industry the company’s

other costs are also lower compared to its peers.

ICICI Securities Ltd | Retail Equity Research Page 4

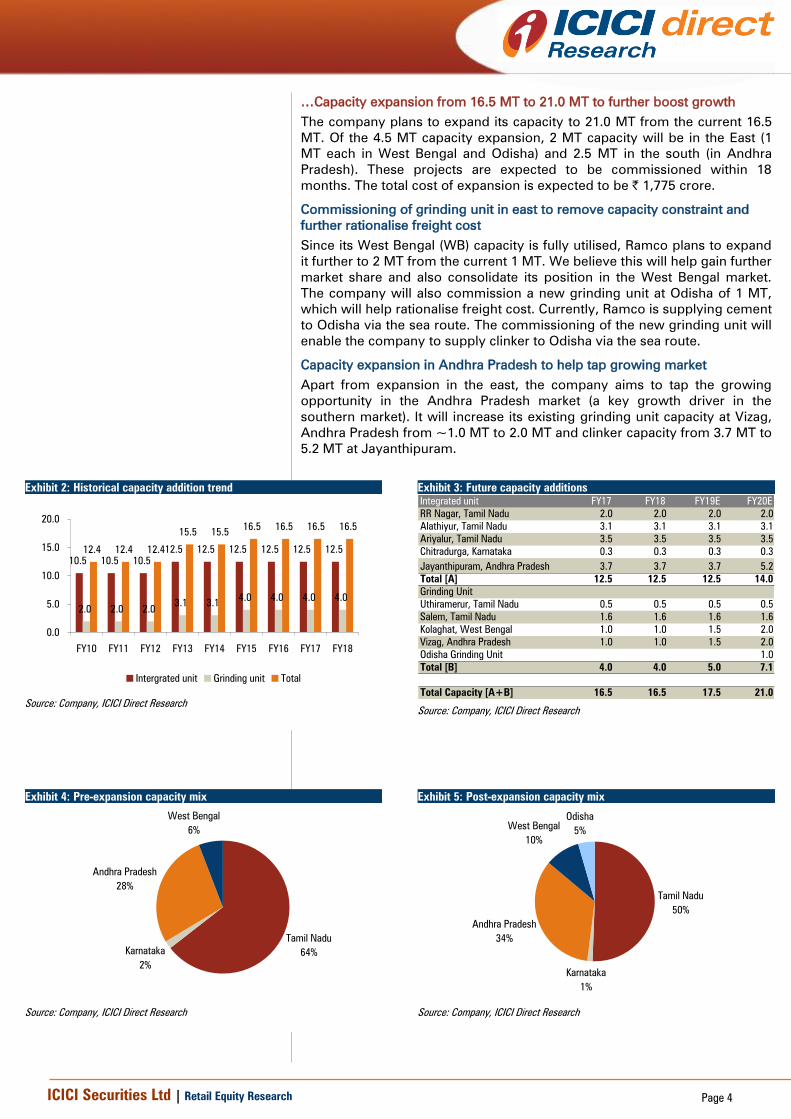

…Capacity expansion from 16.5 MT to 21.0 MT to further boost growth

The company plans to expand its capacity to 21.0 MT from the current 16.5

MT. Of the 4.5 MT capacity expansion, 2 MT capacity will be in the East (1

MT each in West Bengal and Odisha) and 2.5 MT in the south (in Andhra

Pradesh). These projects are expected to be commissioned within 18

months. The total cost of expansion is expected to be | 1,775 crore.

Commissioning of grinding unit in east to remove capacity constraint and

further rationalise freight cost

Since its West Bengal (WB) capacity is fully utilised, Ramco plans to expand

it further to 2 MT from the current 1 MT. We believe this will help gain further

market share and also consolidate its position in the West Bengal market.

The company will also commission a new grinding unit at Odisha of 1 MT,

which will help rationalise freight cost. Currently, Ramco is supplying cement

to Odisha via the sea route. The commissioning of the new grinding unit will

enable the company to supply clinker to Odisha via the sea route.

Capacity expansion in Andhra Pradesh to help tap growing market

Apart from expansion in the east, the company aims to tap the growing

opportunity in the Andhra Pradesh market (a key growth driver in the

southern market). It will increase its existing grinding unit capacity at Vizag,

Andhra Pradesh from ~1.0 MT to 2.0 MT and clinker capacity from 3.7 MT to

5.2 MT at Jayanthipuram.

Exhibit 2: Historical capacity addition trend

10.5 10.5 10.5

12.5 12.5 12.5 12.5 12.5 12.5

2.0 2.0 2.03.1 3.1

4.0 4.0 4.0 4.0

12.4 12.4 12.4

15.5 15.516.5 16.5 16.5 16.5

0.0

5.0

10.0

15.0

20.0

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Intergrated unit Grinding unit Total

Source: Company, ICICI Direct Research

Exhibit 3: Future capacity additions

Integrated unit FY17 FY18 FY19E FY20E

RR Nagar, Tamil Nadu 2.0 2.0 2.0 2.0

Alathiyur, Tamil Nadu 3.1 3.1 3.1 3.1

Ariyalur, Tamil Nadu 3.5 3.5 3.5 3.5

Chitradurga, Karnataka 0.3 0.3 0.3 0.3

Jayanthipuram, Andhra Pradesh 3.7 3.7 3.7 5.2

Total [A] 12.5 12.5 12.5 14.0

Grinding Unit

Uthiramerur, Tamil Nadu 0.5 0.5 0.5 0.5

Salem, Tamil Nadu 1.6 1.6 1.6 1.6

Kolaghat, West Bengal 1.0 1.0 1.5 2.0

Vizag, Andhra Pradesh 1.0 1.0 1.5 2.0

Odisha Grinding Unit 1.0

Total [B] 4.0 4.0 5.0 7.1

Total Capacity [A+B] 16.5 16.5 17.5 21.0

Source: Company, ICICI Direct Research

Exhibit 4: Pre-expansion capacity mix

Tamil Nadu

64%Karnataka

2%

Andhra Pradesh

28%

West Bengal

6%

Source: Company, ICICI Direct Research

Exhibit 5: Post-expansion capacity mix

Tamil Nadu

50%

Karnataka

1%

Andhra Pradesh

34%

West Bengal

10%

Odisha

5%

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 5

Expect revenue CAGR of 14.1% during FY18-20E

Ramco’s revenues have grown at a modest pace of CAGR 2.4% in FY14-17

mainly due to weak market condition in the south and lower utilisation in the

east. However, in FY17, the revenues increased 10.5% YoY due to a pick-up

in cement demand and increased market share in the eastern region. Going

forward, we expect revenues to increase at a CAGR of 14.1% in FY18-20E

mainly led by capacity expansion, revival in the rural economy and increased

government spending.

Exhibit 6: Revenues to increase at 14.1% CAGR over FY18-20E

3949.5

4406.4

4983.2

5734.0

500.0

1500.0

2500.0

3500.0

4500.0

5500.0

6500.0

FY17 FY18 FY19E FY20E

Source: Company, ICICI Direct Research

Exhibit 7: Capacity details

Particulars Year Cement Capacity

Opening FY18 16.5

Addition Q3FY19 1.0

Addition Q1FY20 2.0

Addition FY20 1.5

Total 21.0

Source: Company, ICICI Direct Research

Exhibit 8: Volume to increase at CAGR of 11.7% over FY18-20E

11.6

10.3

9.3

8.3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

FY17 FY18 FY19E FY20E

Source: Company, ICICI Direct Research

Exhibit 9: Realisation to increase at CAGR of 2.1% over FY18-20E

4934

4824

47324731

4600

4650

4700

4750

4800

4850

4900

4950

FY17 FY18 FY19E FY20E

Source: Company, ICICI Direct Research

Exhibit 10: Volumes in Q4FY18 increase 20% YoY

2.7

2.32.22.22.32.02.02.1

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

Q4FY18

Source: Company, ICICI Direct Research

Exhibit 11: Realisation in Q4FY18 declines 1.8% YoY

4586

4645

4956

4785

4507

4760

5006

4668

4200

4300

4400

4500

4600

4700

4800

4900

5000

5100

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

Q4FY18

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 6

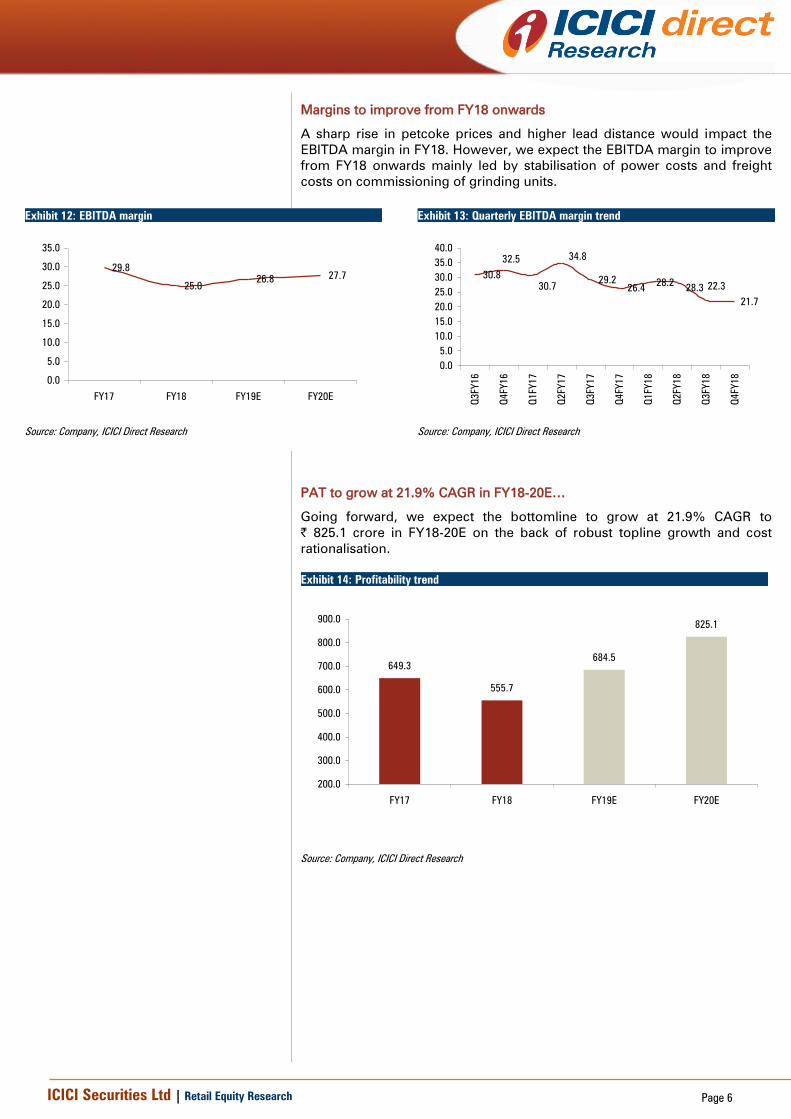

Margins to improve from FY18 onwards

A sharp rise in petcoke prices and higher lead distance would impact the

EBITDA margin in FY18. However, we expect the EBITDA margin to improve

from FY18 onwards mainly led by stabilisation of power costs and freight

costs on commissioning of grinding units.

Exhibit 12: EBITDA margin

29.8

25.026.8

27.7

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

FY17 FY18 FY19E FY20E

Source: Company, ICICI Direct Research

Exhibit 13: Quarterly EBITDA margin trend

30.829.2

26.428.2

21.7

28.3 22.3

34.8

30.7

32.5

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

Q4FY18

Source: Company, ICICI Direct Research

PAT to grow at 21.9% CAGR in FY18-20E…

Going forward, we expect the bottomline to grow at 21.9% CAGR to

| 825.1 crore in FY18-20E on the back of robust topline growth and cost

rationalisation.

Exhibit 14: Profitability trend

649.3

555.7

684.5

825.1

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

FY17 FY18 FY19E FY20E

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 7

Outlook and valuation

Better sand availability in Tamil Nadu, one of the key markets of Ramco

Cement (~60% of capacity share), is expected to be a key contributor to

volume growth in the coming years. This coupled with higher penetration in

the eastern markets will give a tailwind to overall volume growth. Apart from

higher penetration in the east, we expect the southern region to witness an

upturn mainly led by higher government spending on low cost housing,

irrigation and other infra projects. Considering this, coupled with capacity

expansion we expect revenues to grow at a CAGR of 14.1% in FY18-20E. In

addition, we expect the EBITDA margin to improve from FY18 onwards

mainly led by stabilisation of power costs and improvement in freight costs.

Considering the capacity expansion, better leverage (D/E: 0.3x) and cost

efficiency, Ramco is currently trading at attractive valuations. Hence, we

maintain our BUY rating on the stock with an SOTP based target price of

| 930 (i.e. 15x FY20E EV/EBITDA).

Exhibit 15: One year forward EV/tonne

0

1000

2000

3000

4000

5000

May-12

Aug-12

Nov-12

Feb-13

May-13

Aug-13

Nov-13

Feb-14

May-14

Aug-14

Nov-14

Feb-15

May-15

Aug-15

Nov-15

Feb-16

May-16

Aug-16

Nov-16

Feb-17

May-17

Aug-17

Nov-17

Feb-18

May-18

Million $

EV $240 $200 $175 $125 $80

Source: Company, ICICI Direct Research

Exhibit 16: One year forward EV/EBITDA

1000.0

11000.0

21000.0

31000.0

41000.0

May-12

Sep-12

Jan-13

May-13

Sep-13

Jan-14

May-14

Sep-14

Jan-15

May-15

Sep-15

Jan-16

May-16

Sep-16

Jan-17

May-17

Sep-17

Jan-18

May-18

EV 18.0x 15.0x 12.0x 10.0x 8.0x 6.0x

Source: Company, ICICI Direct Research

Exhibit 17: Valuation

Sales Growth EPS Growth EV/Tonne EV/EBITDA RoNW RoCE

(| cr) (%) (|) (%) (US$) (x) (%) (%)

FY16 3,573.26 -2.0 22.8 127.7 210.9 19.5 17.5 12.2

FY17 3,949.54 10.5 27.3 19.8 203.5 17.1 17.4 12.7

FY18 4,406.36 11.6 23.5 -13.9 200.3 18.0 13.7 10.4

FY19E 4,983.21 13.1 29.1 23.7 192.6 15.2 15.2 11.5

FY20E 5,733.99 15.1 35.0 20.6 159.8 12.7 16.1 12.2

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 8

Recommendation history vs. consensus estimate

0

200

400

600

800

1,000

May-

18

Mar-

18

Feb-

18

Dec-

17

Nov-

17

Sep-

17

Jul-

17

Jun-

17

Apr-

17

Mar-

17

Jan-

17

Dec-

16

Oct-

16

Sep-

16

Jul-

16

Jun-

16

Apr-

16

Feb-

16

Jan-

16

Nov-

15

Oct-

15

Aug-

15

Jul-

15

May-

15

(|

)

0.0

20.0

40.0

60.0

80.0

100.0

(%

)

Price Idirect target Consensus Target Mean % Consensus with BUY

Source: Bloomberg, Company, ICICI Direct Research, * Initiated coverage on October 23, 2017

Key events

Date Event

May-09 Ramco sets up 1 MT grinding unit in in Kanchipuram district, Tamil Nadu

May-09 The company sets up 1.6 MT grinding unit in Salem, Tamil Nadu

Feb-10 The company commisions 1 MT grinding unit in Kolaghat, West Bengal

Mar-12 Increased the capacity at Ariyalur, Tamil Nadu by 1.5 MT taking the total capacity of the plant to 3.5 MT

Mar-15 1 MT grinding unit started in Vizag, Andhra Pradesh

Source: Company, ICICI Direct Research

Top 10 Shareholders Shareholding Pattern

Rank Name Latest Filing Date % O/S Position (m) Change (m)

1 Ramco Group 31-Mar-18 34.9 82.2 0.0

2 L&T Investment Management Limited 31-Mar-18 4.4 10.4 1.5

3 Tamil Nadu, State of 31-Mar-18 3.4 8.0 0.0

4 Kotak Mahindra Asset Management Company Ltd. 31-Mar-18 3.2 7.6 0.1

5 SBI Funds Management Pvt. Ltd. 30-Apr-18 2.7 6.4 -0.2

6 Sundaram Asset Management Company Limited 31-Mar-18 2.5 5.8 0.3

7 Aberdeen Asset Management (Asia) Ltd. 31-Mar-18 2.4 5.7 0.0

8 Sri Vishnu Shankar Mill Ltd 31-Mar-18 1.6 3.9 0.0

9 Ramaraju Surgical Cotton Mills, Ltd. 31-Mar-18 1.5 3.6 0.0

10 HDFC Standard Life Insurance Company Limited 31-Mar-18 1.4 3.3 0.1

(in %) Mar-17 Jun-17 Sep-17 Dec-17 Mar-18

Promoter 42.30 42.67 42.75 42.75 42.75

FII 14.52 14.53 14.83 13.89 13.12

DII 18.88 18.48 18.01 19.05 20.35

Others 24.30 24.32 24.41 24.31 23.78

Source: Reuters, ICICI Direct Research

Recent Activity

Investor name Value Shares Investor name Value Shares

L&T Investment Management Limited 16.56 1.49 Axis Asset Management Company Limited -3.92 -0.34

Sundaram Asset Management Company Limited 3.34 0.30 Invesco Hong Kong Limited -3.33 -0.30

Norges Bank Investment Management (NBIM) 3.67 0.30 The New India Assurance Co. Ltd. -2.96 -0.27

HDFC Standard Life Insurance Company Limited 1.64 0.15 Shamyak Investment Pvt. Ltd. -2.78 -0.25

Canara Robeco Asset Management Company Ltd. 1.39 0.13 SBI Funds Management Pvt. Ltd. -2.63 -0.21

Buys Sells

Source: Reuters, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 9

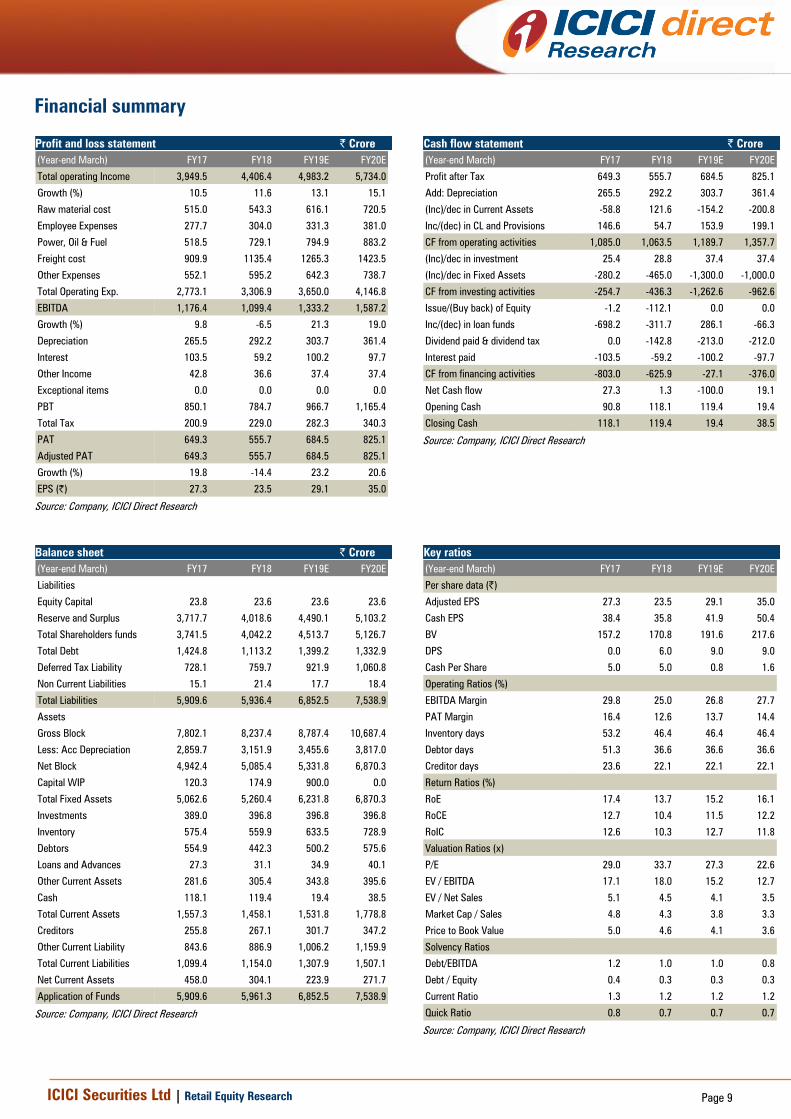

Financial summary

Profit and loss statement | Crore

(Year-end March) FY17 FY18 FY19E FY20E

Total operating Income 3,949.5 4,406.4 4,983.2 5,734.0

Growth (%) 10.5 11.6 13.1 15.1

Raw material cost 515.0 543.3 616.1 720.5

Employee Expenses 277.7 304.0 331.3 381.0

Power, Oil & Fuel 518.5 729.1 794.9 883.2

Freight cost 909.9 1135.4 1265.3 1423.5

Other Expenses 552.1 595.2 642.3 738.7

Total Operating Exp. 2,773.1 3,306.9 3,650.0 4,146.8

EBITDA 1,176.4 1,099.4 1,333.2 1,587.2

Growth (%) 9.8 -6.5 21.3 19.0

Depreciation 265.5 292.2 303.7 361.4

Interest 103.5 59.2 100.2 97.7

Other Income 42.8 36.6 37.4 37.4

Exceptional items 0.0 0.0 0.0 0.0

PBT 850.1 784.7 966.7 1,165.4

Total Tax 200.9 229.0 282.3 340.3

PAT 649.3 555.7 684.5 825.1

Adjusted PAT 649.3 555.7 684.5 825.1

Growth (%) 19.8 -14.4 23.2 20.6

EPS (|) 27.3 23.5 29.1 35.0

Source: Company, ICICI Direct Research

Cash flow statement | Crore

(Year-end March) FY17 FY18 FY19E FY20E

Profit after Tax 649.3 555.7 684.5 825.1

Add: Depreciation 265.5 292.2 303.7 361.4

(Inc)/dec in Current Assets -58.8 121.6 -154.2 -200.8

Inc/(dec) in CL and Provisions 146.6 54.7 153.9 199.1

CF from operating activities 1,085.0 1,063.5 1,189.7 1,357.7

(Inc)/dec in investment 25.4 28.8 37.4 37.4

(Inc)/dec in Fixed Assets -280.2 -465.0 -1,300.0 -1,000.0

CF from investing activities -254.7 -436.3 -1,262.6 -962.6

Issue/(Buy back) of Equity -1.2 -112.1 0.0 0.0

Inc/(dec) in loan funds -698.2 -311.7 286.1 -66.3

Dividend paid & dividend tax 0.0 -142.8 -213.0 -212.0

Interest paid -103.5 -59.2 -100.2 -97.7

CF from financing activities -803.0 -625.9 -27.1 -376.0

Net Cash flow 27.3 1.3 -100.0 19.1

Opening Cash 90.8 118.1 119.4 19.4

Closing Cash 118.1 119.4 19.4 38.5

Source: Company, ICICI Direct Research

Balance sheet | Crore

(Year-end March) FY17 FY18 FY19E FY20E

Liabilities

Equity Capital 23.8 23.6 23.6 23.6

Reserve and Surplus 3,717.7 4,018.6 4,490.1 5,103.2

Total Shareholders funds 3,741.5 4,042.2 4,513.7 5,126.7

Total Debt 1,424.8 1,113.2 1,399.2 1,332.9

Deferred Tax Liability 728.1 759.7 921.9 1,060.8

Non Current Liabilities 15.1 21.4 17.7 18.4

Total Liabilities 5,909.6 5,936.4 6,852.5 7,538.9

Assets

Gross Block 7,802.1 8,237.4 8,787.4 10,687.4

Less: Acc Depreciation 2,859.7 3,151.9 3,455.6 3,817.0

Net Block 4,942.4 5,085.4 5,331.8 6,870.3

Capital WIP 120.3 174.9 900.0 0.0

Total Fixed Assets 5,062.6 5,260.4 6,231.8 6,870.3

Investments 389.0 396.8 396.8 396.8

Inventory 575.4 559.9 633.5 728.9

Debtors 554.9 442.3 500.2 575.6

Loans and Advances 27.3 31.1 34.9 40.1

Other Current Assets 281.6 305.4 343.8 395.6

Cash 118.1 119.4 19.4 38.5

Total Current Assets 1,557.3 1,458.1 1,531.8 1,778.8

Creditors 255.8 267.1 301.7 347.2

Other Current Liability 843.6 886.9 1,006.2 1,159.9

Total Current Liabilities 1,099.4 1,154.0 1,307.9 1,507.1

Net Current Assets 458.0 304.1 223.9 271.7

Application of Funds 5,909.6 5,961.3 6,852.5 7,538.9

Source: Company, ICICI Direct Research

Key ratios

(Year-end March) FY17 FY18 FY19E FY20E

Per share data (|)

Adjusted EPS 27.3 23.5 29.1 35.0

Cash EPS 38.4 35.8 41.9 50.4

BV 157.2 170.8 191.6 217.6

DPS 0.0 6.0 9.0 9.0

Cash Per Share 5.0 5.0 0.8 1.6

Operating Ratios (%)

EBITDA Margin 29.8 25.0 26.8 27.7

PAT Margin 16.4 12.6 13.7 14.4

Inventory days 53.2 46.4 46.4 46.4

Debtor days 51.3 36.6 36.6 36.6

Creditor days 23.6 22.1 22.1 22.1

Return Ratios (%)

RoE 17.4 13.7 15.2 16.1

RoCE 12.7 10.4 11.5 12.2

RoIC 12.6 10.3 12.7 11.8

Valuation Ratios (x)

P/E 29.0 33.7 27.3 22.6

EV / EBITDA 17.1 18.0 15.2 12.7

EV / Net Sales 5.1 4.5 4.1 3.5

Market Cap / Sales 4.8 4.3 3.8 3.3

Price to Book Value 5.0 4.6 4.1 3.6

Solvency Ratios

Debt/EBITDA 1.2 1.0 1.0 0.8

Debt / Equity 0.4 0.3 0.3 0.3

Current Ratio 1.3 1.2 1.2 1.2

Quick Ratio 0.8 0.7 0.7 0.7

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 10

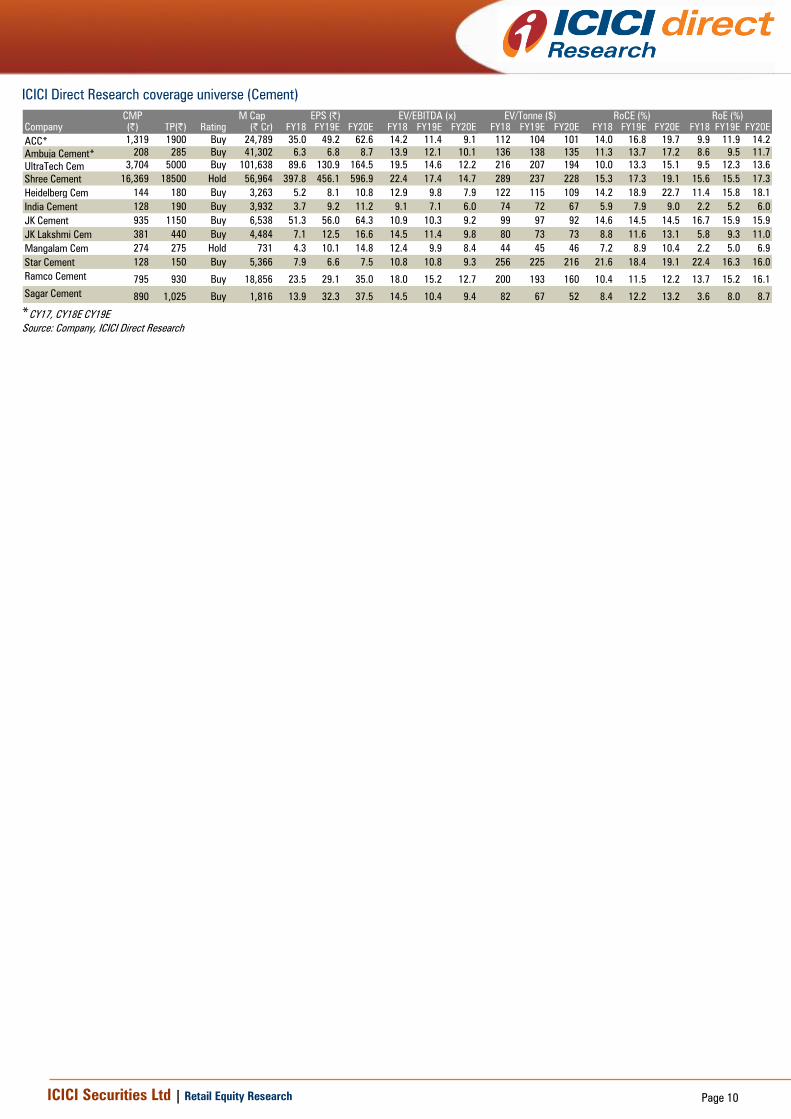

ICICI Direct Research coverage universe (Cement)

CMP M Cap

(|) TP(|) Rating (| Cr) FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E

ACC* 1,319 1900 Buy 24,789 35.0 49.2 62.6 14.2 11.4 9.1 112 104 101 14.0 16.8 19.7 9.9 11.9 14.2

Ambuja Cement* 208 285 Buy 41,302 6.3 6.8 8.7 13.9 12.1 10.1 136 138 135 11.3 13.7 17.2 8.6 9.5 11.7

UltraTech Cem 3,704 5000 Buy 101,638 89.6 130.9 164.5 19.5 14.6 12.2 216 207 194 10.0 13.3 15.1 9.5 12.3 13.6

Shree Cement 16,369 18500 Hold 56,964 397.8 456.1 596.9 22.4 17.4 14.7 289 237 228 15.3 17.3 19.1 15.6 15.5 17.3

Heidelberg Cem 144 180 Buy 3,263 5.2 8.1 10.8 12.9 9.8 7.9 122 115 109 14.2 18.9 22.7 11.4 15.8 18.1

India Cement 128 190 Buy 3,932 3.7 9.2 11.2 9.1 7.1 6.0 74 72 67 5.9 7.9 9.0 2.2 5.2 6.0

JK Cement 935 1150 Buy 6,538 51.3 56.0 64.3 10.9 10.3 9.2 99 97 92 14.6 14.5 14.5 16.7 15.9 15.9

JK Lakshmi Cem 381 440 Buy 4,484 7.1 12.5 16.6 14.5 11.4 9.8 80 73 73 8.8 11.6 13.1 5.8 9.3 11.0

Mangalam Cem 274 275 Hold 731 4.3 10.1 14.8 12.4 9.9 8.4 44 45 46 7.2 8.9 10.4 2.2 5.0 6.9

Star Cement 128 150 Buy 5,366 7.9 6.6 7.5 10.8 10.8 9.3 256 225 216 21.6 18.4 19.1 22.4 16.3 16.0

Ramco Cement795 930 Buy 18,856 23.5 29.1 35.0 18.0 15.2 12.7 200 193 160 10.4 11.5 12.2 13.7 15.2 16.1

Sagar Cement890 1,025 Buy 1,816 13.9 32.3 37.5 14.5 10.4 9.4 82 67 52 8.4 12.2 13.2 3.6 8.0 8.7

RoCE (%) RoE (%)

Company

EV/Tonne ($)EV/EBITDA (x)EPS (|)

*CY17, CY18E CY19E

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 11

RATING RATIONALE

ICICI Direct Research endeavours to provide objective opinions and recommendations. ICICI Direct Research

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and

the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICI Direct Research Desk,

ICICI Securities Limited,

1st

Floor, Akruti Trade Centre,

Road No. 7, MIDC,

Andheri (East)

Mumbai – 400 093

ANALYST CERTIFICATION

We /I, Rashesh Shah CA, Darpan Thakkar MBA research analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our

personal views about any and all of the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or

view(s) in this report. Analysts aren't registered as research analysts by FINRA and might not be an associated person of the ICICI Securities Inc.

Disclosures:

ICICI Securities Limited (ICICI Securities) and its affiliates are a full-service, integrated investment banking, investment management and brokerage and financing group. We along with affi liates are leading

underwriter of securities and participate in virtually all securities trading markets in India. We and our affiliates have investment banking and other business relationship with a significant percentage of

companies covered by our Investment Research Department. Our research professionals provide important input into our investment banking and other business selection processes. ICICI Securities

generally prohibits its analysts, persons reporting to analysts and their dependent family members from maintaining a financial interest in the securities or derivatives of any companies that the analysts

cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on reasonable basis, ICICI Securities, its subsidiaries and associated companies, their directors and

employees (“ICICI Securities and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities

from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities

policies, in circumstances where ICICI Securities is acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return of investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities and affiliates accept no liabilities for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities and its affiliates might have managed or co-managed a public offering for the subject company in the preceding twelve months. ICICI Securities and affiliates might have received

compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of public offerings, corporate finance, investment

banking or other advisory services in a merger or specific transaction. It is confirmed that Rashesh Shah CA, Darpan Thakkar MBA research analysts and the authors of this report have not received any

compensation from the companies mentioned in the report in the preceding twelve months. Our research professionals are paid in part based on the profitability of ICICI Securities, which include earnings

from Investment Banking and other business.

ICICI Securities or its subsidiaries collectively do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the

research report.

It is confirmed that Rashesh Shah CA, Darpan Thakkar MBA research analysts and the authors of this report or any of their family members does not serve as an officer, director or advisory board member

of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. ICICI Securities and affiliates may act upon or make use

of information contained in the report prior to the publication thereof.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.

ICICI Securities Ltd | Retail Equity Research Page 12

ANALYST CERTIFICATION

We /I, Rashesh Shah, CA, and Devang Bhatt, PGDBM Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately

reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this

report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a SEBI registered Research Analyst with SEBI Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Rashesh Shah, CA, and Devang Bhatt, PGDBM Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding

twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Rashesh Shah, CA, and Devang Bhatt, PGDBM Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.

Recommended