BUSINESS

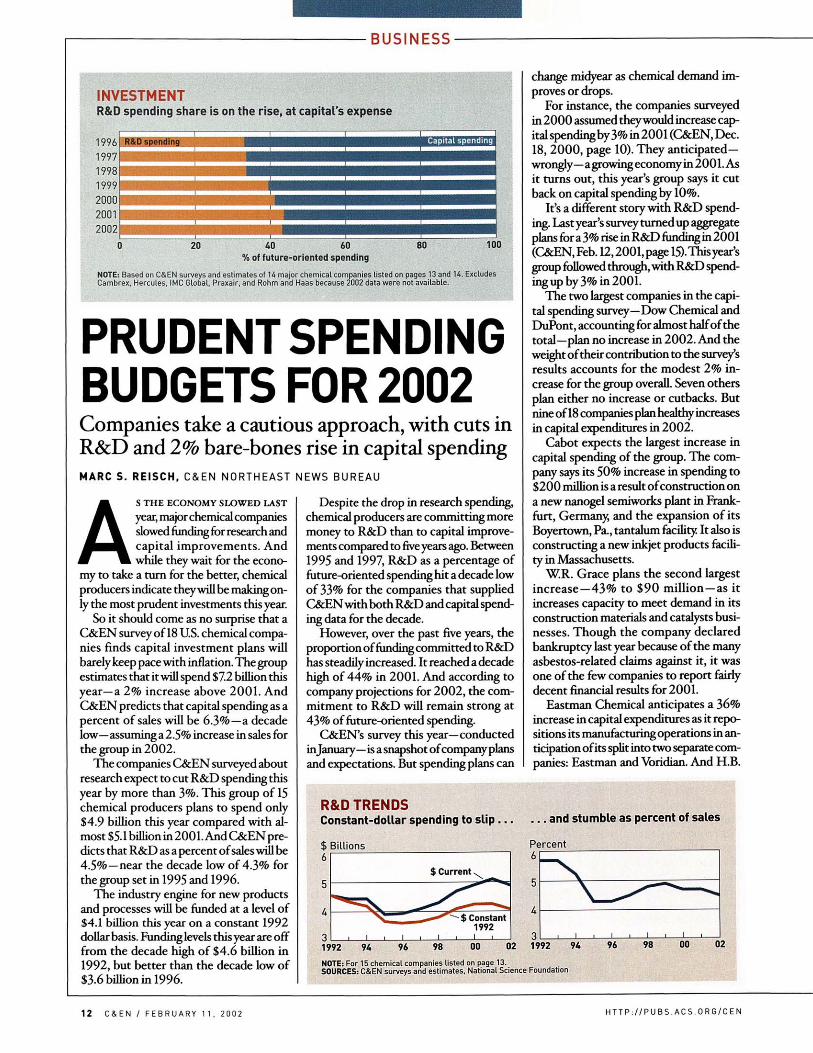

INVESTMENT R&D spending share is on the rise, at capital's expense

1996 1997 1998 1999 2000 2001 2002

) spending Capital spending

20 40 60 % of future-oriented spending

80 100

NOTE: Based on C&EN surveys and estimates of U major chemical companies listed on pages 13 and 14. Excludes Cambrex, Hercules, IMC Global, Praxair, and Rohm and Haas because 2002 data were not available.

PRUDENT SPENDING BUDGETS FOR 2002 Companies take a cautious approach, with cuts in R&D and 2% bare-bones rise in capital spending MARC S. REISCH, C&EN NORTHEAST NEWS BUREAU

AS THE ECONOMY SLOWED LAST

year, major chemical companies slowed funding for research and capital improvements. And while they wait for the econo

my to take a turn for the better, chemical producers indicate they will be making only the most prudent investments this year.

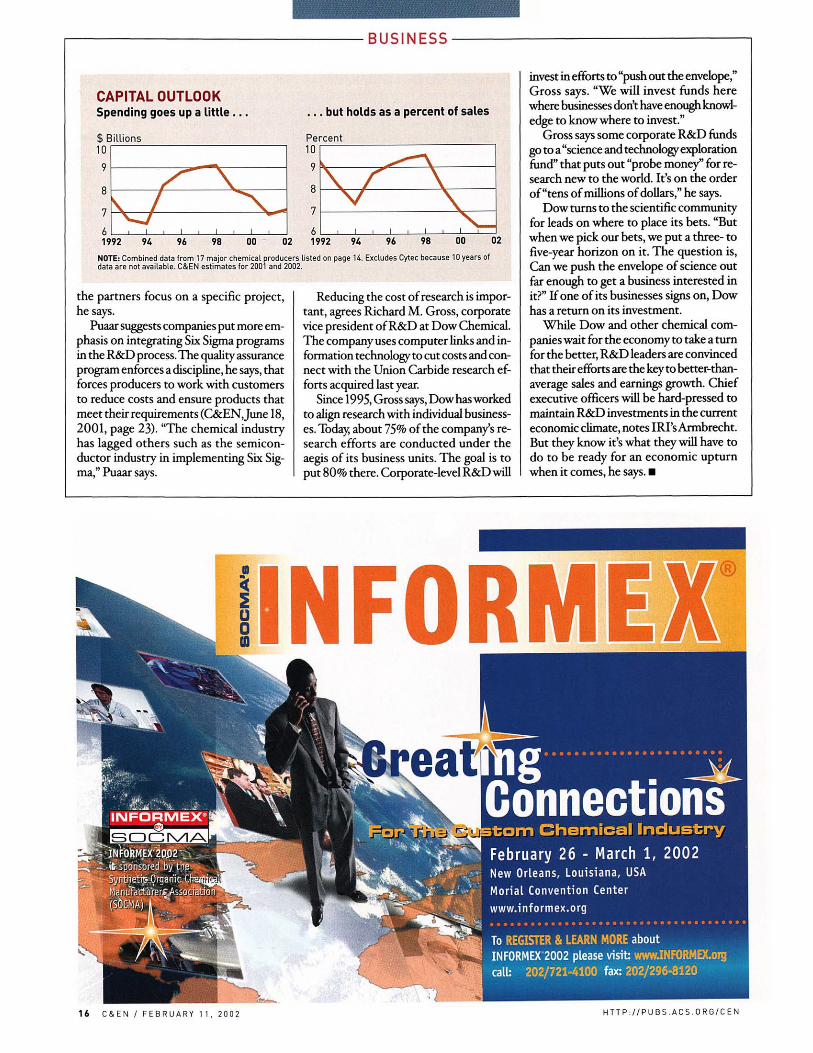

So it should come as no surprise that a C&EN survey of 18 U.S. chemical companies finds capital investment plans will barely keep pace with inflation. The group estimates that it will spend $7.2 billion this year—a 2% increase above 2001. And C&EN predicts that capital spending as a percent of sales will be 6.3%—a decade low—assuming a 2.5% increase in sales for the group in 2002.

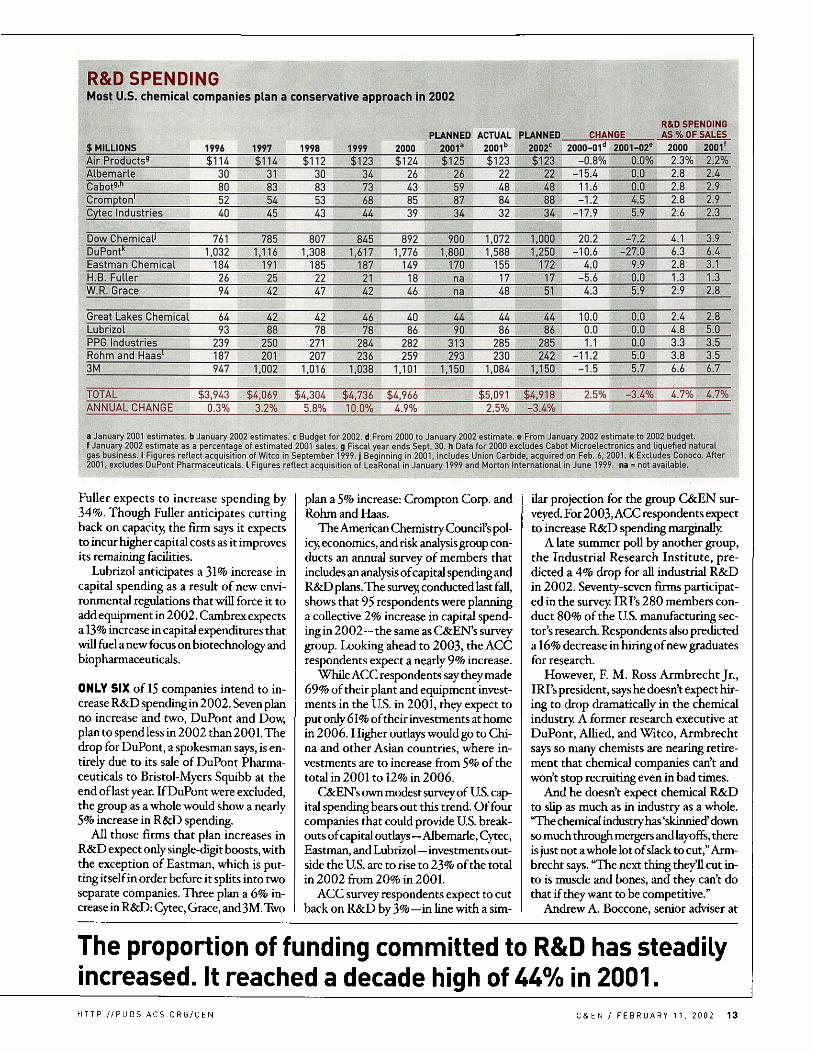

The companies C&EN surveyed about research expect to cut R&D spending this year by more than 3%. This group of 15 chemical producers plans to spend only $4.9 billion this year compared with almost $5.1billionin2001. AndC&EN predicts that R&D as a percent of sales will be 4.5%—near the decade low of 4.3% for the group set in 1995 and 1996.

The industry engine for new products and processes will be funded at a level of $4.1 billion this year on a constant 1992 dollar basis. Funding levels this year are off from the decade high of $4.6 billion in 1992, but better than the decade low of $3.6 billion in 1996.

Despite the drop in research spending, chemical producers are committing more money to R&D than to capital improvements compared to five years ago. Between 1995 and 1997, R&D as a percentage of future-oriented spending hit a decade low of 33% for the companies that supplied C&EN with both R&D and capital spending data for the decade.

However, over the past five years, the proportion of funding committed to R&D has steadily increased. It reached a decade high of 44% in 2001. And according to company projections for 2002, the commitment to R&D will remain strong at 43% of future-oriented spending.

C&EN's survey this year—conducted injanuary—is a snapshot of company plans and expectations. But spending plans can

R&D TRENDS Constant-dollar spending to sl ip. . .

$ Billions

change midyear as chemical demand improves or drops.

For instance, the companies surveyed in 2000 assumed they would increase capital spending by 3% in 2001 (C&EN, Dec. 18, 2000, page 10). They anticipated-wrongjy—a growing economy in 2001. As it turns out, this year's group says it cut back on capital spending by 10%.

It's a different story with R&D spending. Last year's survey turned up aggregate plans for a3% rise inR&D fundingin2001 (C&EN, Feb. 12,2001, page 15). This year's group followed through, with R&D spending up by 3% in 2001.

The two largest companies in the capital spending survey—Dow Chemical and DuPont, accounting for almost half of the total—plan no increase in 2002. And the weight of their contribution to the survey's results accounts for the modest 2% increase for the group overall. Seven others plan either no increase or cutbacks. But nine of 18 companies plan healthy increases in capital expenditures in 2002.

Cabot expects the largest increase in capital spending of the group. The company says its 50% increase in spending to $200 million is a result of construction on a new nanogel semiworks plant in Frankfurt, Germany, and the expansion of its Boyertown, Pa., tantalum facility It also is constructing a new inkjet products facility in Massachusetts.

W.R. Grace plans the second largest increase—43% to $90 million—as it increases capacity to meet demand in its construction materials and catalysts businesses. Though the company declared bankruptcy last year because of the many asbestos-related claims against it, it was one of the few companies to report fairly decent financial results for 2001.

Eastman Chemical anticipates a 36% increase in capital expenditures as it repositions its manufacturing operations in anticipation of its split into two separate companies: Eastman and Voridian. And H.B.

. . . and stumble as percent of sales

Percent

1992 M

NOTE: For 15 chemical companies listed on page 13. SOURCES: C&EN surveys and estimates, National Science Foundation

12 C&EN / FEBRUARY 1 1 . 2002 H T T P : / / P U B S . A C S . O R G / C E N

R&D SPENDING Most U.S. chemical companies plan a conservative approach in 2002

PLANNED ACTUAL $ MILLIONS 1996 1997 1998 1999 2000 2001a 200Γ

PLANNED. 2002c 2000-01

CHANGE R&D SPENDING AS % OF SALES

2001-02e 2000 2001 Air Products9

Albemarle Cabot»·11

Crompton1

Cytec Industries

$1U 30 80 52 40

$114 31 83, 54 45

$112 30 83 53 43

$123 34 73 68 44

$124 26 43 85 39

$125 26 59 87 34

$123 22 48 84 32

$123 22 48 88 34

-0 .8% -15.4

11.6 -1.2

-17.9

0.0% 0.0 0.0 4.5 5.9

2.3% 2.8 2.8 2.8 2.6

2.2% 2.4 2.9 2.9 2.3

Dow ChemicalJ

DuPontk

Eastman Chemical H.B. Fuller W.R. Grace

761 1,032

184 26 94

785 1,116

191 25 42

807 1,308

185 22 47

845 1,617

187 21 42

892 1,776

149 18 46

900 1,800

170 na na

1,072 1,588

155 17 48

1,000 1,250

172 17 51

20.2 -10.6

4.0 -5.6 4.3

-7.2 -27.0

9.9 0.0 5.9

4.1 6.3 2.8 1.3 2.9

3.9 6.4 3.1 1.3 2.8

Great Lakes Chemical Lubrizol PPG Industries Rohm and Haas1

3M

64 93

239 187 947

42 88

250 201

1,002

42 78

271 207

1,016

46 78

284 236

1,038

40 86

282 259

1,101

44 90

313 293

1,150

44 86

285 230

1,084

44 86

285 242

1,150

10.0 0.0 1.1

-11.2 -1.5

0.0 0.0 0.0 5.0 5.7

2.4 4.8 3.3 3.8 6.6

2.8 5.0 3.5 3.5 6.7

TOTAL ANNUAL CHANGE

$3,943 0.3%

$4,069 3.2%

$4,304 5.8%

$4,736 10.0%

$4,966 4.9%

$5,091 2.5%

$4,918 -3.4%

2.5% -3.4% 4.7% 4.7%

a January 2001 estimates, b January 2002 estimates, c Budget for 2002. d From 2000 to January 2002 estimate, e From January 2002 estimate to 2002 budget. f January 2002 estimate as a percentage of estimated 2001 sales, g Fiscal year ends Sept. 30. h Data for 2000 excludes Cabot Microelectronics and liquefied natural gas business, i Figures reflect acquisition of Witco in September 1999. j Beginning in 2001, includes Union Carbide, acquired on Feb. 6, 2001. k Excludes Conoco. After 2001, excludes DuPont Pharmaceuticals. I Figures reflect acquisition of LeaRonal in January 1999 and Morton International in June 1999. na = not available.

Fuller expects to increase spending by 34%. Though Fuller anticipates cutting back on capacity, the firm says it expects to incur higher capital costs as it improves its remaining facilities.

Lubrizol anticipates a 31% increase in capital spending as a result of new environmental regulations that will force it to add equipment in 2002. Cambrex expects a 13% increase in capital expenditures that will fuel a new focus on biotechnology and biopharmaceuticals.

ONLY SIX of 15 companies intend to increase R&D spending in 2002. Seven plan no increase and two, DuPont and Dow, plan to spend less in 2002 than 2001. The drop for DuPont, a spokesman says, is entirely due to its sale of DuPont Pharmaceuticals to Bristol-Myers Squibb at the end of last year. If DuPont were excluded, the group as a whole would show a nearly 5% increase in R&D spending.

All those firms that plan increases in R&D expect only single-digit boosts, with the exception of Eastman, which is putting itself in order before it splits into two separate companies. Three plan a 6% increase in R&D: Cytec, Grace, and 3M. Two

plan a 5% increase: Crompton Corp. and Rohm and Haas.

The American Chemistry Council's policy, economics, and risk analysis group conducts an annual survey of members that includes an analysis of capital spending and R&D plans. The survey conducted last fall, shows that 95 respondents were planning a collective 2% increase in capital spending in 2002—the same as C&EN's survey group. Looking ahead to 2003, the ACC respondents expect a nearly 9% increase.

While ACC respondents say they made 69% of their plant and equipment investments in the U.S. in 2001, they expect to put only 61% of their investments at home in 2006. Higher outlays would go to China and other Asian countries, where investments are to increase from 5% of the total in 2001 to 12% in 2006.

C&EN's own modest survey of U.S. capital spending bears out this trend. Of four companies that could provide U.S. breakouts of capital outlays—Albemarle, Cytec, Eastman, and Lubrizol—investments outside the U.S. are to rise to 23% of the total in 2002 from 20% in 2001.

ACC survey respondents expect to cut back on R&D by 3%—in line with a sim

ilar projection for the group C&EN surveyed. For 2003, ACC respondents expect to increase R&D spending marginally

A late summer poll by another group, the Industrial Research Institute, predicted a 4% drop for all industrial R&D in 2002. Seventy-seven firms participated in the survey IRI's 280 members conduct 80% of the U.S. manufacturing sector's research. Respondents also predicted a 16% decrease in hiring of new graduates for research.

However, F. M. Ross Armbrecht Jr., IRI's president, says he doesn't expect hiring to drop dramatically in the chemical industry A former research executive at DuPont, Allied, and Witco, Armbrecht says so many chemists are nearing retirement that chemical companies can't and won't stop recruiting even in bad times.

And he doesn't expect chemical R&D to slip as much as in industry as a whole. <The chemical industry has 'skinnied' down so much through mergers and layoffs, there is just not a whole lot of slack to cut," Armbrecht says. "The next thing they'll cut into is muscle and bones, and they can't do that if they want to be competitive."

Andrew A. Boccone, senior adviser at

The proportion of funding committed to R&D has steadily increased. It reached a decade high of 44% in 2001. H T T P : / / P U B S . A C S . O R G / C E N C & E N / F E B R U A R Y 1 1 , 2 0 0 2 1 3

BUSINESS

management consulting firm Kline & Co., agrees. The chemical industry keeps expecting to grow through acquisition, he said in a recent speech, but the universe of companies to acquire is shrinking and the markets it serves are maturing. If the specialty chemical industry, in particular, is to grow, it needs a resurgence in innovative thinking, Boccone says.

One way to think differently is to adopt "stretch goals," suggests Krishna Narayan, a partner in the chemical industry practice of Chicago-based consultants Diamond-Cluster International. "Find a customer

who is not satisfied and asks you to stretch your current capabilities to meet their needs," he suggests.

Such a customer advances R&D and helps a company become more competitive. And working with this type of customer benefits all of a company's customers. "It changes the way a company does business and makes its products more competitive," Narayan says.

Chemical companies have to "return to their roots, and take advantage of new biological routes to compounds that can support the notion of sustainable develop

ment," says Calvin B. Cobb, a vice president and chemical industry leader at management consulting firm Cap Gemini Ernst & %ung. And companies have to take advantage of advances in molecular engineering through adoption of nano-technology and other materials science breakthroughs.

"GLOBALIZATION and cost reduction have run their course," suggests Cobb, immediate past-president of the American Institute of Chemical Engineers. "WeVe got to go back to basics. I'd argue now is the time to increase R&D."

But Cobb realizes that R&D is "difficult to manage and success rates are low. Throwing money into research may not be the answer, particularly if your batting average is low" He suggests that more companies adopt the stage-gate process. "It's widely accepted, but not universally"

Rohm and Haas uses the stage-gate process to periodically measure the ultimate value of a research project against the time, effort, and money that goes into it. At various stages, a research team makes an assessment of a project and decides whether or not to continue. "We also look at the natural evolution of a business," says David C. Bonner, global technology director at Rohm and Haas's polymer technology center. "We don't want to get into

GLOBAL INVESTMENT Survey of major U.S. chemical firms finds capital spending to rise 2% in 2002

PUNNED ACTUAL PLANNED. CHANGE $ MILLIONS Air Products1

Albemarle Cabot1·» Cambrex Cromptonh

Cytec

1996 $951

90 209 32 39 73

1997 $870

85 163 36 50 91

1998 $771

71 187 43 67

104

1999 $889

78 166 31

132 77

2000 $768

52 137 39

155 77

2001a

na 60 na 40

175 80

2001b

$708 50

133 40

135 64

2002c

$708 55

200 45

115 74

2000-01d

-7.8% -3.8 -2.9 2.6

-12.9 -16.9

2001-02e

0.0% 10.0 50.4 12.5

-14.8 15.6

Dow Chemical' DuPontJ

Eastman Chemical H.B. Fuller W.R. Grace Great Lakes

1,3a 1,701

789 90

457 237

1,198 2,129

749 69

259 133

1,546 2,240

500 62

101 161

1,412 2,055

292 56 83

119

1,349 1,925

226 49 65

157

1,500 2,000

300 na na na

1,600 1,600

215 32 63

160

1,600 1,600

292 43 90 95

18.6 -16.9 -4.9

-34.7 -3.1

1.9

0.0 0.0

35.8 34.4 42.9

-40.6

Hercules IMC Global Lubrizol PPG Industries Praxair 3M

120 173 94

489 893

1,109

119 244 101 466 902

1,406

157 368 93

487 781

1,430

196 248 65

490 653

1,039

187 118 86

561 704

1,115

na 180 90

450 650

1,000

66 125 65

301 650

1,000

60 140 85

300 650

1,000

-64.7 5.9

-24.4 -46.3 -7.7

-10.3

-9.1 12.0 30.8 -0.3 0.0 0.0

TOTAL ANNUAL CHANGE

$8,890 7.2%

$9,070 2.0%

$9,169 1.1%

$8,081 -11.9%

$7,770 -3.8%

$6,994 -10.0%

$7,152 2.3%

-10.0% —

2.3% —

a December 2000 estimates, b January 2002 estimates, c Budget for 2002. d From 2000 to January 2002 estimate, e From January 2002 estimate to 2002 budget. f Fiscal year ends Sept. 30. g Data for 2000 excludes Cabot Microelectronics and liquefied natural gas business, h Figures reflect acquisition of Witco in September 1999. i Beginning in 2001, includes Union Carbide, acquired on Feb. 6, 2001. j Excludes Conoco. After 2001, excludes DuPont Pharmaceuticals, na = not available.

14 C&EN / FEBRUARY 1 1 , 2002 HTTP://PUBS. ACS.ORG/CEN

DOMESTIC INVESTMENT U.S. capital spending slips in 2002

2001 a 2002b

Albemarle Cytec Eastman Lubrizol

$50 64 215 65

$45 42 185 45

$55 74 292 85

$50 44 235 60

TOTAL $394 $317 $506 $389 a January 2002 estimates, b Budget for 2002.

it too early since we can waste a lot of time waiting for it to mature."

"If we think [a project] will take a long time to grow, we might partner with a university," Bonner says. That is what Rohm and Haas is doing with a proprietary nan-otechnology capability that is "so novel we don't fully understand it." If it gains momentum, "we would put more resources into the project" and bring it back to Rohm and Haas.

Cabot also has a mechanism to expand its market opportunities. The company successfully used the stage-gate process to grow and then spin off Cabot Microelectronics—a company that is now a leader in supplying semiconductor wafer polishing compounds. It hopes to repeat that success with other businesses. To begin, "we survey markets Cabot is not serving and explore leading-edge trends," says Dan Gilliland, Cabot vice president of business development.

"We talk to innovators in a field and learn from them about what we can do," he says. "We try to envision the next step in the technology And then we see if we can bring technology competencies we have to a new development."

NOT ALL NEW developments are breakthroughs, and many are extensions of existing lines of business. The trend has been to put the bulk of research under the direction of business units, Bonner says. "Where there were only strong ties before, the links are integral now to more rapidly bring new products to market." But for "front end" research, a company needs a separate administrative unit with "a mission to create new technology platforms to feed into its business strategy." Rohm and Haas calls the effort "targeted fundamental development."

Rohm and Haas has two such innovation centers now: one for polymers and the other for electronic materials. Though the centers concentrate on areas of interest to the firm's business units and keep a sharp eye out to identify opportunities for new

businesses, they also scan for the most innovative practices, such as the use of high-throughput screening to develop new catalysts and polymers.

The company expects to set up a different kind of innovation center later in the year that is likely to involve universities and other companies. The objective, Bonner says, would be to develop technology that promotes sustainable development. "Sustainable development has not been technology based. We'd like to inject that."

Bonner envisions the new center including economic and technology groups at universities to find ways to drive policy and technology in tandem.

To make decisions that advance technology as well as the bottom line, Sal Puaar, product and process leader at management consulting firm Celerant, also recommends multiparty efforts. R&D in joint ventures with those that possess complementary technology and with suppliers can be beneficial to all involved if

Get It AH with HPFC from Biotage

As a chemist today, you face ever-increasing demands to produce more compounds, at higher purity, and — if you're lucky — in larger quantities.

Fortunately, Biotage has the answer: HPFC. Our Horizon™ High Performance FLASH Chromatography system simplifies the purification of a wide range of organic compounds using a variety of chromatographic media.

New compression and sampling technologies reduce sample prep time and accommodate sample sizes up to 20 grams. Plus an intuitive user interface makes purification easy, fast, and flexible,, saving you valuable time.

Accelerate your discoveries today by visiting www.biotage.com, or just call 800-446-4752.

ζ A Dyax Corp. Company

P.O. Box 8006 · Charlottesville, VA 22906 U.S.A. Phone 800-446-4752 · Fax 434-979-4743 E-mail [email protected] · Web www.

The Dyax logo is a registered trademark of Dyax Corp. HPFC and Horizon are trademarks of Biotage, Inc., A Dyax Corp. Company.

H T T P : / / P U B S . A C S . O R G / C E N C&EN / FEBRUARY 1 1. 2002 15

You Want

Higher Purity

Greater Speed

Larger Scale

BUSINESS

CAPITAL OUTLOOK Spending goes up a little . . .

$ Billions 10 9

8

7 6

^V i ^ . j * " " -

ι Ι ι I

. . . but holds as a percent of sales

Percent 10

7 6

^ ^-^Λ \ / Λ v \ i l

1992 94 96 98 00 02 1992 96 96 98 00 02 NOTE: Combined data from 17 major chemical producers listed on page U. Excludes Cytec because 10 years of data are not available. C&EN estimates for 2001 and 2002.

the partners focus on a specific project, he says.

Puaar suggests companies put more emphasis on integrating Six Sigma programs in the R&D process. The quality assurance program enforces a discipline, he says, that forces producers to work with customers to reduce costs and ensure products that meet their requirements (C&EN, June 18, 2001, page 23). "The chemical industry has lagged others such as the semiconductor industry in implementing Six Sigma," Puaar says.

Reducing the cost of research is important, agrees Richard M. Gross, corporate vice president of R&D at Dow Chemical. The company uses computer links and information technology to cut costs and connect with the Union Carbide research efforts acquired last year.

Since 1995, Gross says, Dow has worked to align research with individual businesses. Today, about 75% of the company's research efforts are conducted under the aegis of its business units. The goal is to put 80% there. Corporate-level R&D will

invest in efforts to "push out the envelope," Gross says. "We will invest funds here where businesses don't have enough knowledge to know where to invest."

Gross says some corporate R&D funds go to a "science and technology exploration fund" that puts out "probe money" for research new to the world. It's on the order of "tens of millions of dollars," he says.

Dow turns to the scientific community for leads on where to place its bets. "But when we pick our bets, we put a three- to five-year horizon on it. The question is, Can we push the envelope of science out far enough to get a business interested in it?" If one of its businesses signs on, Dow has a return on its investment.

While Dow and other chemical companies wait for the economy to take a turn for the better, R&D leaders are convinced that their efforts are the key to better-than-average sales and earnings growth. Chief executive officers will be hard-pressed to maintain R&D investments in the current economic climate, notes IRI's Armbrecht. But they know it's what they will have to do to be ready for an economic upturn when it comes, he says. •

INFORMEX .

16 C&EN / FEBRUARY 1 1 , 2002

To REGISTER & LEARN MORE about INF0RMEX 2002 please visit: www.INFORMEX.org call: 202/721-4100 fax: 202/296-8120

H T T P : / / P U B S . A C S . O R G / C E N

RreatiTra JNFORMEX'2002 te sponsored by the Synthetic Organic Cheiijjg ManuTacVurerÇ-Associatior ÎSÔCMAÏ l

S O C M / a ijid-i=iùi=»:<

February 26 - March 1, 2002 New Orleans, Louisiana, USA

Morial Convention Center

www.informex.org

Connections Far'TftelESIBstom Chemical Indus t ry

Recommended