Presented by:

Ivonne Bachar, CPPM CF

Director, Property Mgmt. Office

Stanford University

Event:

NCURA – Regions VI and VII

Denver, CO

April 4-6, 2011

Page 1

A Property Management Primer

Key Elements Affecting Equipment in Research

Today’s Focal Points

Page 2

Property Life Cycles – A Birds Eye Look Key Terms Regulatory Context Pre-Award Post Award Close-outs and Audits

Discussion Encouraged!

Page 3

Terms & Concepts

TitlePropertyEquipmentExempt EquipmentMaterial SuppliesScreeningCAPGFP/GFM

AccountabilityAccountabilityStewardshipStewardship

CapitalCapitalDepreciationDepreciation

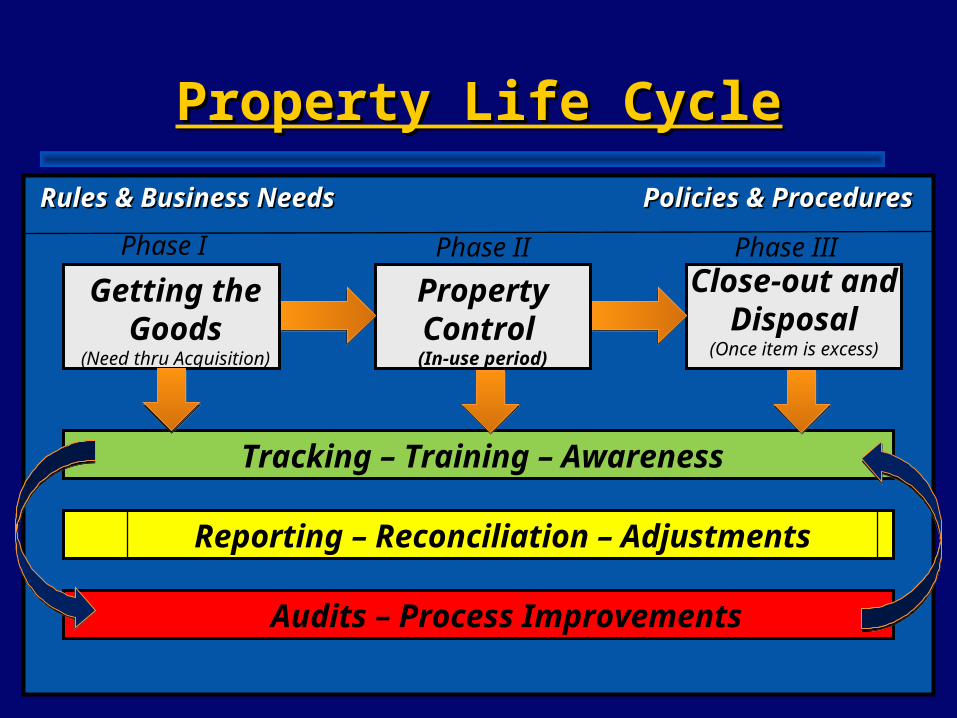

Property Life CycleProperty Life Cycle

Rules & Business NeedsRules & Business Needs Policies & ProceduresPolicies & Procedures

Getting theGoods

(Need thru Acquisition)

Phase I Phase II Phase III

PropertyControl

(In-use period)

Close-out andDisposal

(Once item is excess)

Tracking – Training – Awareness

Reporting – Reconciliation – Adjustments

Audits – Process Improvements

Page 5

“Regulatory” Context

Office of Management & Budget (OMB) Circulars Federal Acquisition Regulations (FAR)

Agency-Specific Supplements State Regulations Accounting Standards (GASB, GAAP, FASB) IRS Guidelines Export Controls Other associated regulations (e.g. EPA) Data Security VCSs and ILPs Agreement-specific Terms & Conditions

6

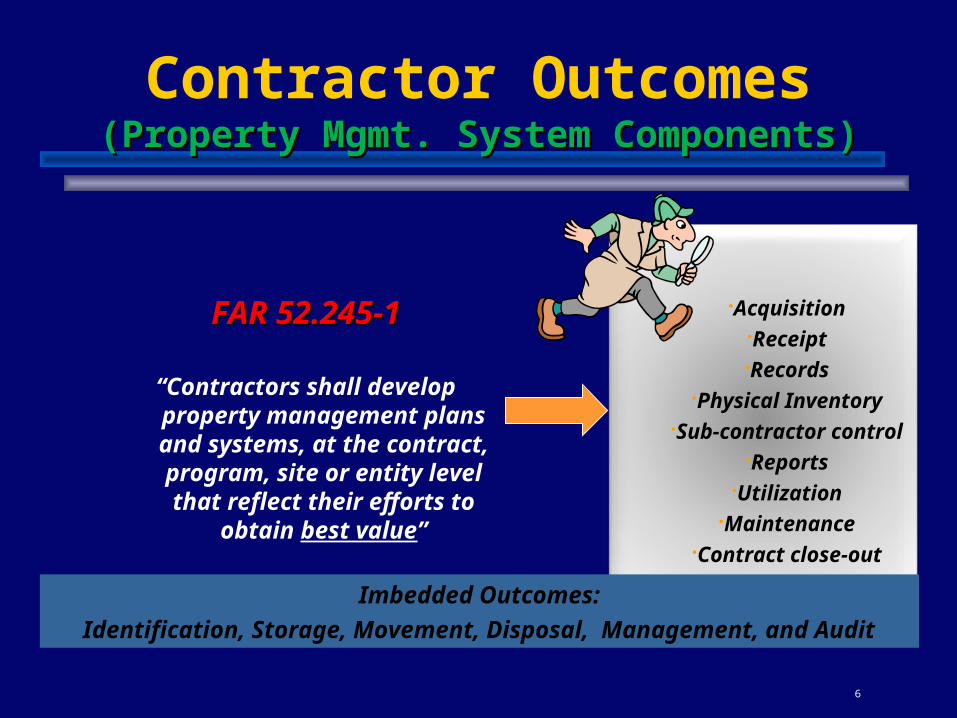

Contractor Outcomes(Property Mgmt. System Components)(Property Mgmt. System Components)

AcquisitionReceipt

RecordsPhysical Inventory

Sub-contractor controlReports

UtilizationMaintenance

Contract close-out

FAR 52.245-1FAR 52.245-1

“Contractors shall develop property management plans and systems, at the contract, program, site or entity level that reflect their efforts to

obtain best value”

Imbedded Outcomes:

Identification, Storage, Movement, Disposal, Management, and Audit

Page 7

Regulatory Requirements(Grants)

Code of Federal Regulation / OMB CircularsCode of Federal Regulation / OMB Circulars2 CFR 220 ( OMB A-21)

Cost Principles for Educational Institutions

2 CFR 215 (OMB A-110) Uniform Administrative Requirements for Grants and Cooperative

Agreements with Institutions of Higher Education, Hospitals, and other Non-Profit Organizations

A-87 Cost Principles for State, Local, and Indian Tribal Governments

A-123 Management’s Responsibility for Internal Control

A-133 Audits of Institutions of Higher Education & Other Non-Profit

Institutions

Page 8

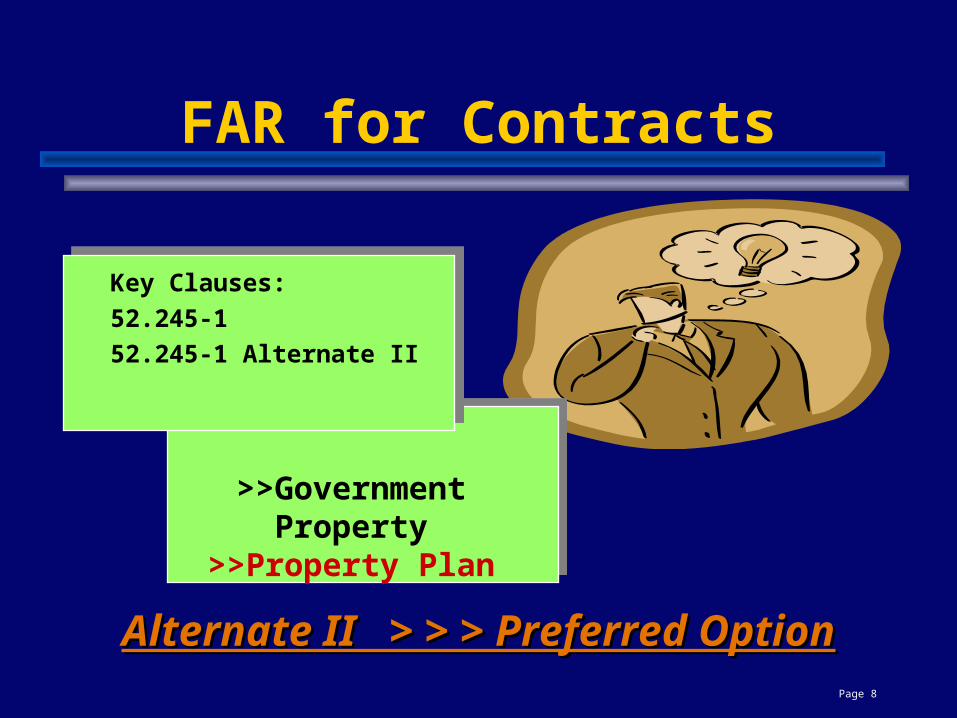

FAR for Contracts

Key Clauses:

52.245-1

52.245-1 Alternate II

Alternate II > > > Preferred OptionAlternate II > > > Preferred Option

>>Government Property>>Property Plan

Page 9

52.245-1, Alternate II52.245-1, Alternate II

Gives title to recipient for equipment under $5,000, provided that the recipient obtained CO’s approval before each acquisition.

Gives title to recipient for equipment $5,000 or greater, with CO’s permission. (Note: Sponsor holds title during life of contract)

Applies only to Contractor Acquired Property

Beware of Tax Implications

Pre-Award

Support SOW Property Plan for contract proposals Budget justifications Identify methods of acquisition Clearly define

FabricationsDeliverables

Acceptance and delivery criteria Negotiate appropriate clause

Page 10

Page 11

Acquisition

Approved budget vs. authority to purchase Approvals & Screening Financial & Reporting Categorization Explicit listing of GFP needed Import & Export End of period purchases

Methods of Acquisition and Lifecycle Methods of Acquisition and Lifecycle ChangesChanges

Sponsor Furnished

Or Loaned

University (Contractor)

Acquired

• Purchases

• FabricationsFabrications

Donation

• Incoming Transfers

• Title Transfers

If Sponsor Title

Considered GFP

Lease

Rent

Equipment Title – GrantsEquipment Title – Grants

Sponsored Sponsored GRANTGRANT University

TitlePurchasesTaxable

Notes: In some cases granting agency may impose future use restrictions on equipment In rare cases when equipment is furnished on a grant or if specified in the terms of the

grant, it is treated as sponsor owned. Some Federal Sponsors retain right to title, and may opt to reclaim to non-exempt property

(OMB Circulars)

Equipment Title – ContractsEquipment Title – Contracts

FederalFederalSponsored CONTRACTSponsored CONTRACT

FAR 52.245-1 (Alt. II)

FAR 52.245-1 or per T&C

<$5K University TitleF&A (aka IDC) Applies

Sponsor TitleNon-Taxable

No F&A (aka IDC)

Notes: Equipment furnished by Sponsor, remains sponsor-owned Non-Federal, Sponsor-Owned equipment may be taxable (e.g. State of California) May request title transfer to Sponsor-owned property upon completion of award

$5K> Sponsor TitleNo F&A (aka IDC)

(FAR Clause)

Page 15

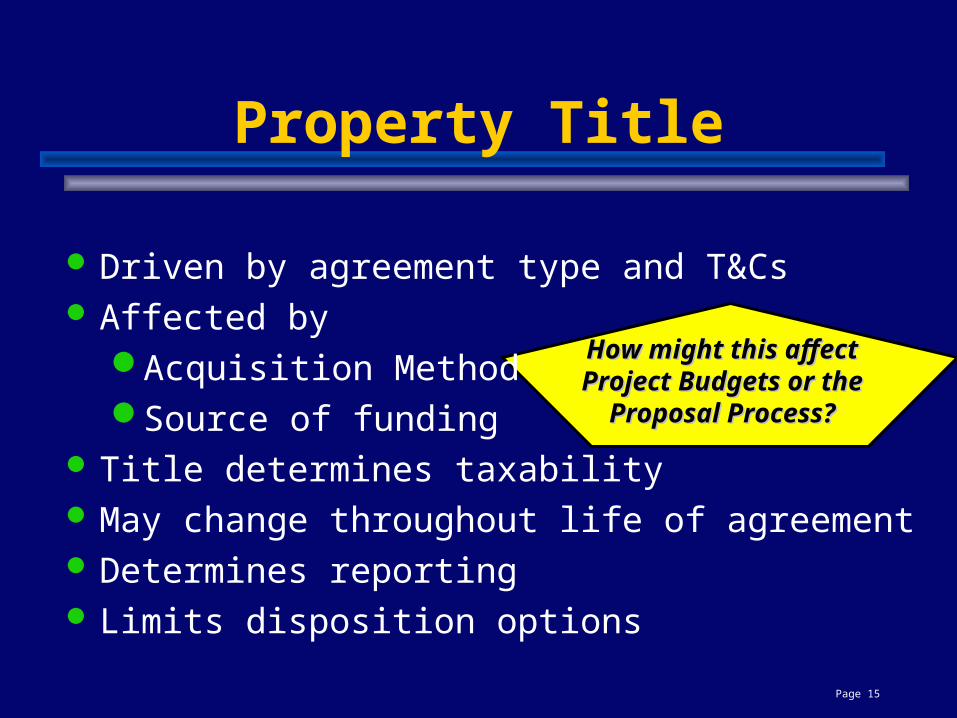

Property Title

Driven by agreement type and T&Cs Affected by

Acquisition MethodSource of funding

Title determines taxability May change throughout life of agreement Determines reporting Limits disposition options

How might this affectHow might this affectProject Budgets or theProject Budgets or the

Proposal Process?Proposal Process?

Page 16

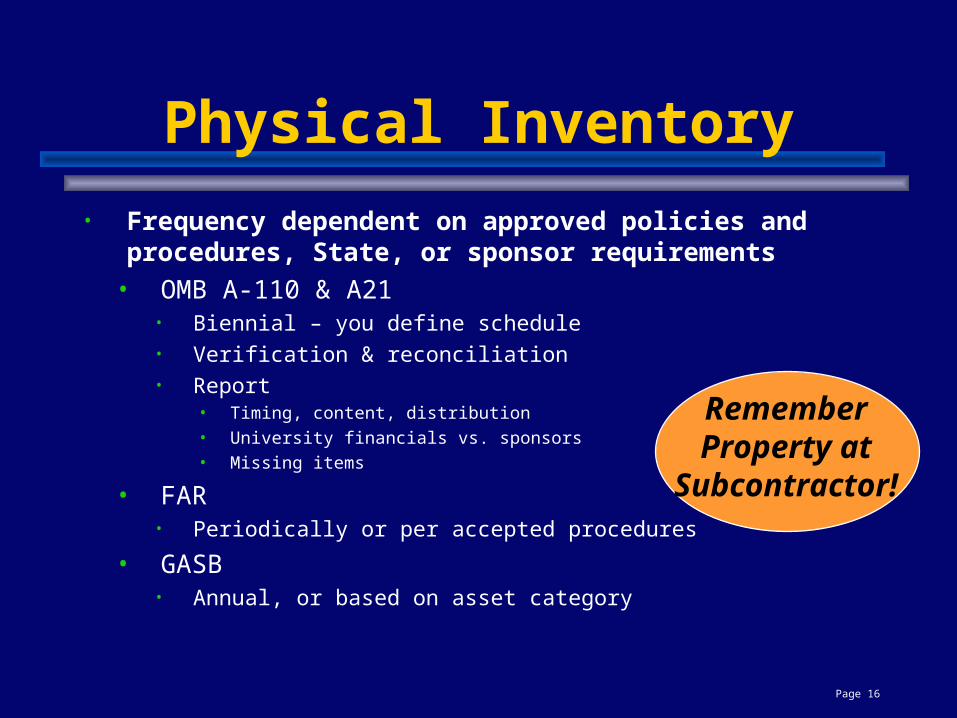

Physical Inventory

• Frequency dependent on approved policies and procedures, State, or sponsor requirements

• OMB A-110 & A21• Biennial – you define schedule• Verification & reconciliation• Report

• Timing, content, distribution• University financials vs. sponsors• Missing items

• FAR• Periodically or per accepted procedures

• GASB• Annual, or based on asset category

Remember Property at

Subcontractor!

Transfers(Incoming or Outgoing)(Incoming or Outgoing)

Define items involved Award type & status Funding Source Method of acquisition Current title Retention requirements Cost or no-cost? Approvals Import-Export Issues

“It Depends” starts here...

Page 18

Subcontracting

Ensure your flow down addresses AT LEAST:AT LEAST:Confirm recipient’s property systemAcquisition and TitleIdentification and RecordsPhysical inventoryReports, including LDDTUseDispositionRisk and LiabilityStewardship responsibilities

Page 19

SubcontractsTitle Issues, cont.

The Prime needs to be careful not to give the sub greater title rights than the prime has been given; consider:

What type of instrument is the Prime?Is the sub an eligible recipient?Is the sub doing research or other professional services?Are there restrictions on the prime’s clear title?How is GP affected?At what point is title granted to sub?

Page 20

Reports

Agency Specific Management and Self Assessment Internal Audit Interim

Financial and/or Accountability Physical Inventory Loss, Damage, Destruction, Theft Corrective Action Final Closeout

Include Sub-award infoInclude Sub-award info

Other “Hot Spots” International and Collaborative Agreements Self-Assessments Import - Export controls Fabrications Journal Transfers P-Card Purchases Indirect Cost implications Multi-disciplinary projects Multi-source funding Data Security

Page 21

It’s about integration

Page 22

Rules andRequirements Orgs, Policies,

Procedures,People

Assets and TechInfrastructure Property

ProfessionalSkills

Page 23

Questions???Questions???

Thank you for being here today!!!

Concerns???Concerns???

Recommended