1

Options

2

OptionsFinancial Options

• There are Options and Options

- Financial options

- Real options

3

OptionsFinancial Options

• A financial option gives its owner the right (but not the obligation)

to purchase or sell an asset at a fixed price at some future date.

• Puts

• Calls

• Strike price/Exercise price

• American/European

4

Table 20.1 Option Quotes for Amazon.com Stock

5

OptionsFinancial Options

Option Pricing• Binomial - Two state single period - Law of one price - Replicating portfolio Call option, SP 50, No dividend, Stock will either rise by 10 or fall by 10 Risk free rate is 6%

6

OptionsFinancial Options/Pricing

Stock Bond Call

60 1.06 max (60-50,0) = 10

0 1

Stock 50 Bond 1 40 1.06 max (40 -50,0) = 0

60 = up and 40 = down S = Share price and t = number of shares and B = investment in the bond. SP = 50

7

OptionsFinancial Options/Pricing

• Value of portfolio containing the stock and the bond must = the value of the portfolio in each state.

• 60St + 1.06B = 10• 40St + 1.06B = 0• So St = .5• And B = - 18.8679• 60 x .5 - 1.06 x 18.8679 = 10• 40 x .5 – 1.06 x 18.8679 = 0

8

OptionsFinancial Options/Pricing

• Generalising we get

• St = Cu – Cd and B = Cd – Sdt

Su – Sd 1+rf

This gives us the replicable portfolio

The Call option price then follows

C = St + B or 50x.5 – 18.8679(1) = 6.13

9

OptionsFinancial Options/Pricing

• But what about multi period models?

• Strike price of 50, Rf = 6%

0 1 2 Periods

50

30

40

60

40

20

10

OptionsFinancial Options/Pricing

• We start at the end and work back

1 2

50

60

40

Max(60 -50,0) = 10

Max 40 -50,0) = 0

This is the same as before therefore St = .5 and B = -18. 87 and the call value at time 1 is 6.13

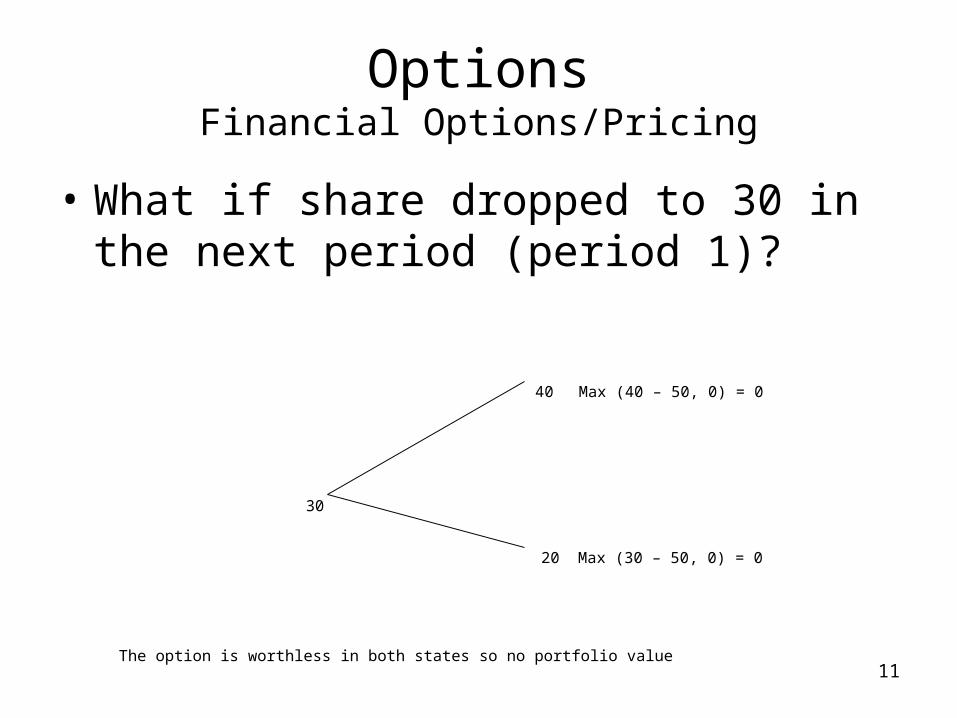

11

OptionsFinancial Options/Pricing

• What if share dropped to 30 in the next period (period 1)?

30

40 Max (40 – 50, 0) = 0

20 Max (30 – 50, 0) = 0

The option is worthless in both states so no portfolio value

12

OptionsFinancial Options/Pricing

• Now move back a period

0 1

40

Stock Call

50 6.13

30 0

Now work out replicating portfolio at time 0

St = Cu – Cd = 6.13 – 0 = 0.3065

Su – Sd 50 – 30

B = Cd – Sdt = 0 - 30(0.3065) = - 8.67

1 + rf 1.06

13

OptionsFinancial Options/Pricing

• So the Call value at Time 0 is

• C = St + B = 40(0.3065) +(-) 8.67 = 3.59

14

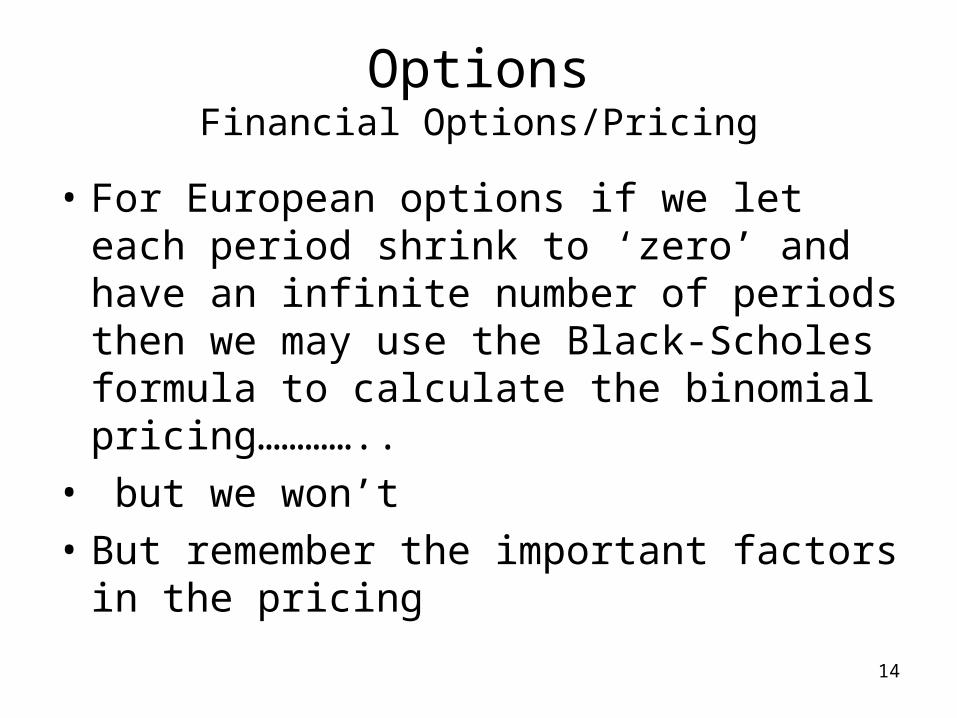

OptionsFinancial Options/Pricing

• For European options if we let each period shrink to ‘zero’ and have an infinite number of periods then we may use the Black-Scholes formula to calculate the binomial pricing…………..

• but we won’t

• But remember the important factors in the pricing

15

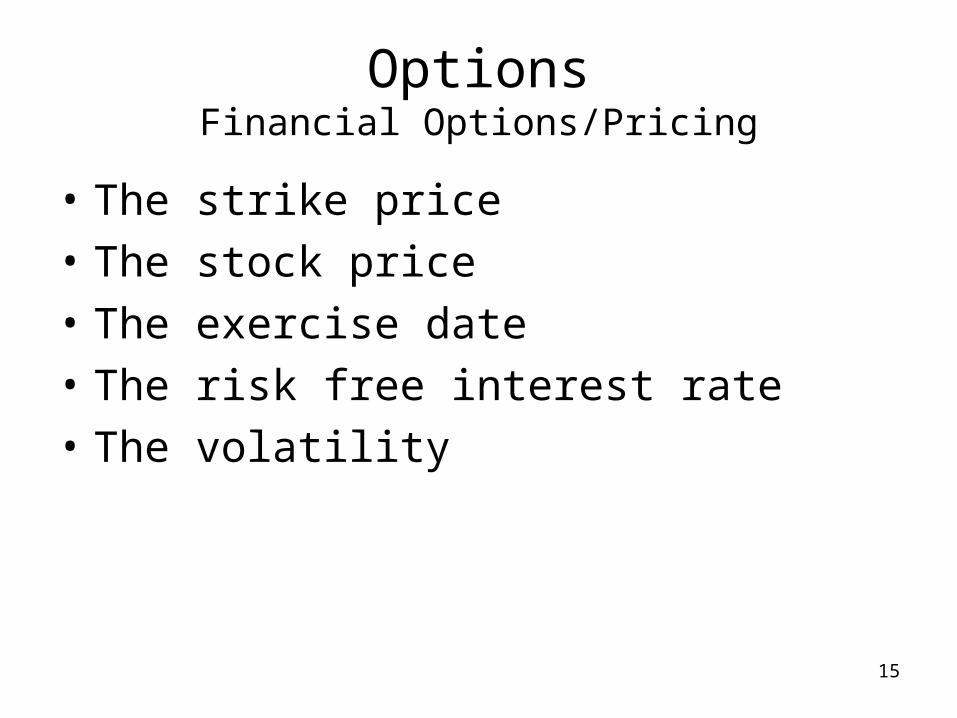

OptionsFinancial Options/Pricing

• The strike price

• The stock price

• The exercise date

• The risk free interest rate

• The volatility

16

OptionsReal Options

• And there are Real Options

The right to take a particular business decision e.g. a capital investment decision.

Main distinction is that the asset is normally not traded

17

OptionsReal Options

• Until now we have considered a stream of cash flows during the project, starting from today, to determine the NPV

• But what about alternatives such as delaying the start or abandoning the project after a while?

18

OptionsReal Options

• To analyse the alternatives we need Decision Trees

A graphical representation of future decisions and uncertainty resolution (B & DeM)

19

OptionsReal Options

• Meet (re meet) Megan

• Goes to markets

• Sells, average profit 1,100

• Costs of Booth 500, in advance

Go to meet

Stay at home

profit

1,100 – 500 = 600

0

20

OptionsReal Options

• Now add some uncertainty

• If it rains (25% chance) she will make a loss = -100

• If it is sunny her profit is higher = 1,500

21

OptionsReal Options

Go to meet

sunshine 75%

1,500

Stay at home

Rain 25% - 100

Decision node

Information node

0

- 500

22

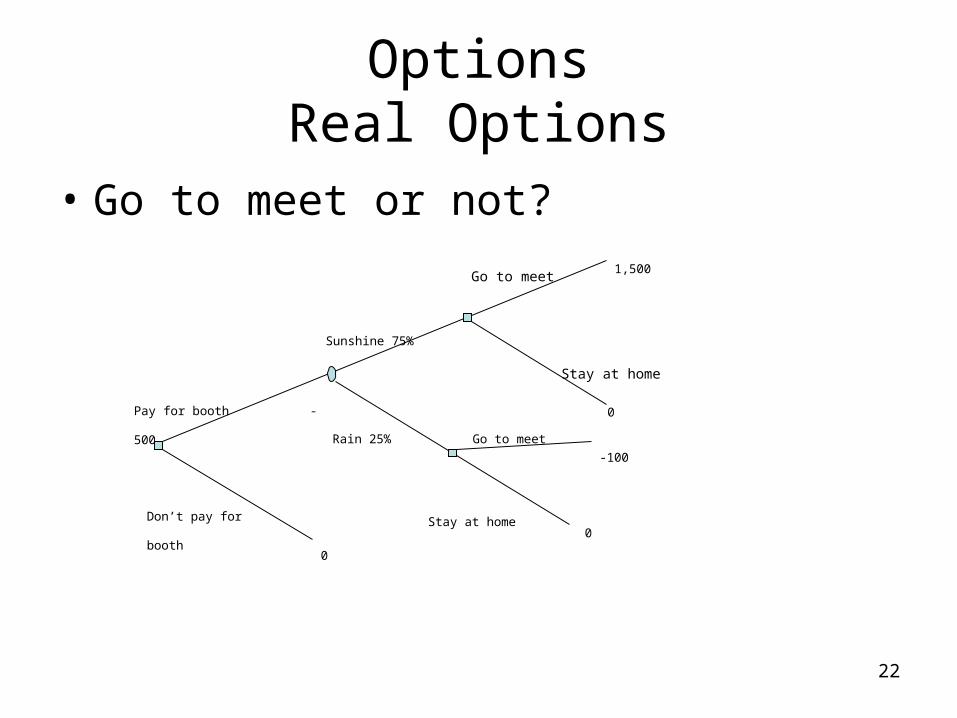

OptionsReal Options

• Go to meet or not?

Don’t pay for booth

Pay for booth - 500

Sunshine 75%

Rain 25% Go to meet

Stay at home

Stay at home

Go to meet1,500

0

-100

0

0

23

OptionsReal Options

• So what is the ‘value’ of this real option to Megan?

Expected profit without choice i.e. go to meet regardless

= 1,500 x .75 +-100 x .25 = 1,100

Expected profit with choice

= 1,500 x .75 = 1,125

So choice/option worth 25

24

OptionsReal Options

• Should Megan pay for the booth?

Expected profit will be 1125 -500 = 625

So Yes

25

OptionsReal Options

• When else may they be used?- Option to delay Invest now only where NPV is

substantially greater than zero But What are costs of delay? What is volatility? What are costs of investment?

26

OptionsReal Options

• Option to Grow

• Option to Expand

• Option to Abandon

• Option to Prepay

Recommended