Metropolitan Chicago Industrial Market Report | Year End 2006

Chicago | Year End 2006 Market Report

We are pleased to present NAI Hiffman’s Year-End 2006 Market Report, an analysis of the Metropolitan Chi-cago offi ce and industrial markets. Our goal is to provide a unique perspective on the area’s vibrant commer-cial real estate market from the largest full-service, privately-owned real estate service fi rm in the Midwest. This report is a result of collaboration between NAI Hiffman agents in each of the various submarkets, along with our unparalleled research group which analyzes data from a wide variety of sources.

In 2006, the downtown offi ce market showed steady improvement over the year as new construction de-liveries slowed and fi nally paused. Anchors for these new buildings are still in the process of relocating. Vacancy rates therefore will continue to fl uctuate in the near term until the dust settles. The next round of construction delivery is still several years off which should give the market time to fi ll several holes. In the suburbs, most markets continue to recover. While fl uctuations are to be expected going forward, multiple tenants are looking for large blocks of space in most areas. Signifi cant new construction is limited to the Central North and East-West Corridor markets. Further developement will wait on suitable anchor tenants before breaking ground.

The Chicago industrial market continues to reign as one of the most dominant in the nation. Retail distribu-tion and logistics companies comprised most of the larger transactions announced during 2006. Retail giant Wal-Mart occupied two buildings at CenterPoint’s Intermodal Center in Elwood, IL, a combined 3.4 million square feet. The industrial market grew by 13.6 million square feet, bringing the total market Metropolitan Area inventory to more than one billion square feet. Investors in industrial real estate remain bullish. Year-to-date sales transactions were more than $1.58 billion representing more than 166 properties, with most of the gain attributed to warehouse and distribution properties.

NAI Hiffman is one of Chicago’s largest and most active commercial real estate fi rms and is the Chicago area representative for NAI Global, the industry’s largest managed network of global real estate service providers, comprised of over 3,500 professionals in 300 markets in 40 countries.

With both city and suburban offices, NAI Hiffman is in the market daily, insuring the most current, com-prehensive market knowledge for clients such as Wm. Wrigley Jr. Company, Cornerstone Realty Advisors, PacTrust, UBS, The St Paul, WorldCom and the United States Postal Service. Give us the opportunity to earn your trust, and we will deliver for you.

Sincerely,

Michael J. FlynnOffi ce Brokerage

John F. CashIndustrial Brokerage

Ryan MurphyRetail Brokerage

Chad M. FirselInvestment Services

Table of Contents

Local Economy ........................................1Industrial Overview ..................................2Industrial Market Statistics .....................3 Industrial Markets Lake County ......................................4 O’Hare ................................................5 Central DuPage .................................6 I-88 Corridor ......................................7 I-55 Corridor ......................................8 I-80 East & West ................................9 Industrial Market Map .....................10Investment .............................................11

The data compiled in the Chicago Office Market Report is the legal property of NAI Hiffman. Reproduction or dissemination of the information contained herein is strictly prohibited without the expressed written consent of NAI Hiffman. This report contains information, including information available to the public, which has been relied upon by NAI Hiffman on the assumption that it is accurate and complete without independent verification by NAI Hiffman. NAI Hiffman accepts no responsibility if this should prove to be inaccurate or incomplete. No warranty or representation, express or implied, is made by NAI Hiffman as to the accuracy or completeness of the information contained herein, and same is submitted subject to errors, omissions, and changes in market conditions.

NAI Hiffman Year End 2006 Market Report

year at this time. This compares to a national average of 4.5%, down from 5.0% last year at this time. The top sec-tors in 2006 have once again been professional services, education and healthcare, and leisure and hospitality, all of which showed gains in employment. Losers for the year include durable goods manufacturing, telecommunications,

Local Economy | Year End 2006

Unemploymentin percentseasonally adjustedthru November 2006

4.0

5.0

6.0

7.0

8.0

20052004200320022001

U.S.Metro Chicago

2006

Chicago, the third largest metropolitan area in the U.S. after New York and Los Angeles, is the most influential economic region between the East and West Coasts. Situated at the geographical heart of the nation, Chicago’s locational advantages have fostered its development into an inter-national center for banking, securities, high technology, air transportation, business services, wholesale and retail trade and manufacturing. In addition, Chicago is one of the principal trading centers for commodities, financial and derivative futures products. In 2006 Site Selection magazine once again named Chicago the number one destination for new or expanded corporate facilities projects in the nation, a position the city has held in four of the last five years.

Chicago has a higher rate of employment in management, business and finance, and office and administrative job growth than the nation. Likewise it also has higher rates of production and transportation and material moving occu-pations. This indicates both an “office economy” as well as a “production” and “distribution” economy. With one of the most diversified economies of any region in the coun-try, Chicago is less vulnerable to fluctuations in individual industries than most other large urban areas. The Chicago region’s considerable economic diversity is reflected in the ten largest publicly traded companies headquartered here ranked by market capitalization: Abbott Laboratories, Boeing, Kraft Foods, McDonald’s Corp., Motorola, Walgreen Co., Exelon Corp., The Allstate Corp., Caterpillar and Baxter International.

During 2006 the Chicago economy continued to gather steam with unemployment dropping rapidly throughout the year. The Chicago metropolitan area recorded its lowest unemployment rate for November on record this year with a seasonally adjusted figure of 3.9%, falling from 5.6% last

StatisticsPopulation ............................................................ 8,619,935

Population Change 2000-2006 (est.) .......................... +4.2%

Households .......................................................... 3,016,690

Median Household Income (est.) .............................. $58,038

2004 Gross Metro Product ($ billion) .......................... $392.6

Labor Force .......................................................... 4,077,500

Jobs Created Nov. ‘05 - Nov. ‘06 .............................. 42,000

Unemployment Rate (SA) .............................................. 3.9%

US Unemployment Rate (SA) ........................................ 4.5%

Data as of Nov.. 2006 unless noted otherwise. Data from Bureau of Labor Statistics, SiteRight, U.S. Council of Mayors, IL Dept. of Employment Security

and federal government employment. The Chicago area economy gained 42,000 jobs during the 12 months ending in November, the most recent period for which statistics are available, according to the U.S. Bureau of Labor Statistics.

In 2007, Metro Chicago growth should continue, but at a slower pace than 2006. Job growth is expected to be 0.53% in 2007, less than half the 1.1% growth rate for the 12 months that ended in November, according to the Regional Economics Application Laboratory (REAL) at the University of Illinois at Urbana-Champaign.

Employment declines are expected in manufacturing and information services, according to REAL. Hospitality and leisure services will lead the gainers. However, even the strongest sector of the local economy, professional and business services firms, is in for a slowdown, projected by economy.com to expand 2.7%, barely half the 4.5% increase registered in 2006. Growth in this sector will come from accounting and consulting firms. Bankruptcy filings, income restatements and stepped up compliance practices mandated by Sarbanes-Oxley all feed the industry.

Home sales in the metropolitan region are expected to rise about 15 percent in 2007 after falling 20 percent in 2006. Permits for home construction are projected to drop 18 percent, after falling 1.6% in 2006, according to Moody’s economy.com. They rose 18 percent in 2005.

Bureau of Labor Statistics, Illinois Department of Employment Security

1

2

Industrial Market | Year End 2006

MARKET OVERVIEWThe Chicago industrial market continues to reign as one of the most dominant in the nation. Retail distribution and lo-gistics companies comprised most of the larger transactions announced during 2006. Retail giant Wal-Mart occupied two buildings at CenterPoint’s Intermodal Center in Elwood, IL, a combined 3.4 million square feet. The industrial market grew by 13.6 million square feet, bringing the total market Metro-politan Area inventory to more than one billion square feet. Investors in industrial real estate remain bullish. Year-to-date sales transactions were more than $1.59 billion consisting of more than 166 properties, with most of the gain attributed to warehouse and distribution product. The year ended on positive absorption with an 11.00% availability rate, down from 11.65% at year end 2005.

With its central location for national transportation, the Chi-cago region will continue to dominate the Midwest expand-ing into areas beyond the traditional metropolitan borders. Mature communities like those of O’Hare and the Near West suburbs are rapidly undergoing industrial redevelopment.

Demand for new product combined with land scarcity has resulted in an active teardown and redevelopment market. New industrial development continues unabated in 2006 along the I-55, I-57, I-88 and I-80 corridors. Leasing activ-ity and user demand are anticipated to improve this quarter with retailers and logistics companies continuing to drive much of the distribution activity. The outlook for 2007 is sus-tained growth propelled by continued strong infl ow of equity into the industrial market.

Sales of suburban industrial buildings, 100,000 sf and greater, totaled approximately $341.6 million at the end of the fourth quarter. Notable suburban sales during the fourth quarter included 10 buildings purchased by ProLogis total-ing $144.9 million ($53 psf) and two buildings purchased

Address Size (sf) Price (mil) Price psf Buyer Seller

1000 Veterans Pky., Bolingbrook 405,000 $23.6 $58 ML Realty Partners ProLogis175 Ambassador Dr., Naperville 331,000 20.8 63 -- Wrightwood Capital1290 Remington Blvd., Bolingbrook 315,000 18.3 58 ProLogis ML Realty Partners315 Kirk Rd., St. Charles 309,000 14.4 47 Inland Real Estate Bradley Associates505 Crossroads Pky., Bolingbrook 291,000 16.9 58 ProLogis ML Realty Partners9625 55th St., Kenosha, WI 175,052 13.5 77 Inland Real Estate Bradley Associates2019 Corporate Ln., Naperville 123,475 10.2 82 TIAA Prairie Point Bldg., IV LLC

Major 4th Quarter Industrial Sales Transactions

2006 Industrial SalesBuyer - Seller Profilein $ million

preliminary330.4

Private -National

Private -Local

REITInstitu-tion

Foreign

391.5250.4250.8

103.9

Other

BuyerSeller

270.0

769.3

302.2138.7

0.0

216.5151.6

by Inland Real Estate Group totaling $27.9 million ($58 psf) from Bradley Associates and CenterPoints’ three building $68 million ($66 psf) purchase in Bolingbrook from various sellers. One-off transactions included developer Panattoni Developments’ $8.2 millon ($64 psf) sale to LIT Industrial.

Industrial Submarket Availabilityin percent

LakeI-88CDPI-55O’Hare

9.8011.01

13.87

8.74 8.65

I-80WI-80E

13.73

17.76

3

NAI Hiffman Year End 2006 Market Report

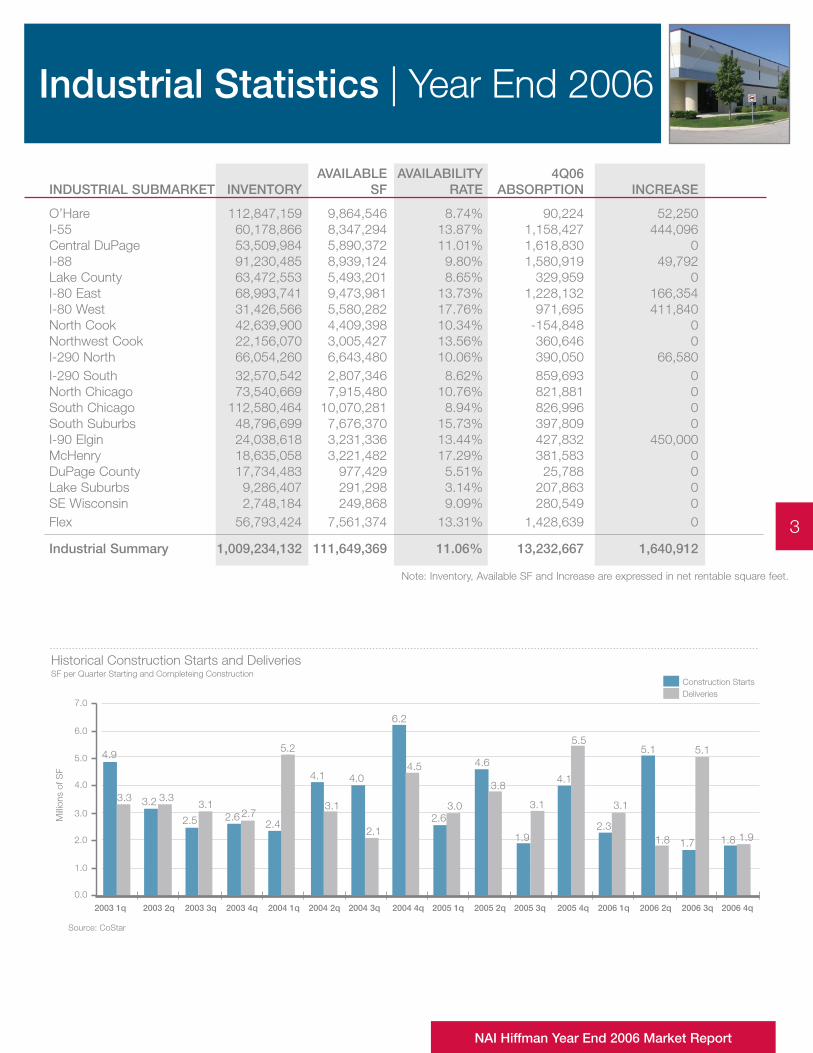

Historical Construction Starts and DeliveriesSF per Quarter Starting and Completeing Construction

Construction StartsDeliveries

4.9

3.3 3.2 3.3

2.5

3.12.6 2.7

5.2

4.1

3.1

4.0

2.1

6.2

4.5

2.63.0

4.6

3.8

1.9

3.1

4.1

5.5

2.3

3.1

5.1

1.8 1.7

5.1

1.8 1.92.4

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0.02003 1q 2003 2q 2003 3q 2003 4q 2004 1q 2004 2q 2004 3q 2004 4q 2005 1q 2005 2q 2005 3q 2005 4q 2006 1q 2006 2q 2006 3q 2006 4q

Source: CoStar

Milli

ons

of S

F

AVAILABLE AVAILABILITY 4Q06 INDUSTRIAL SUBMARKET INVENTORY SF RATE ABSORPTION INCREASE

O’Hare 112,847,159 9,864,546 8.74% 90,224 52,250 I-55 60,178,866 8,347,294 13.87% 1,158,427 444,096 Central DuPage 53,509,984 5,890,372 11.01% 1,618,830 0 I-88 91,230,485 8,939,124 9.80% 1,580,919 49,792 Lake County 63,472,553 5,493,201 8.65% 329,959 0 I-80 East 68,993,741 9,473,981 13.73% 1,228,132 166,354 I-80 West 31,426,566 5,580,282 17.76% 971,695 411,840 North Cook 42,639,900 4,409,398 10.34% -154,848 0 Northwest Cook 22,156,070 3,005,427 13.56% 360,646 0 I-290 North 66,054,260 6,643,480 10.06% 390,050 66,580 I-290 South 32,570,542 2,807,346 8.62% 859,693 0 North Chicago 73,540,669 7,915,480 10.76% 821,881 0 South Chicago 112,580,464 10,070,281 8.94% 826,996 0 South Suburbs 48,796,699 7,676,370 15.73% 397,809 0 I-90 Elgin 24,038,618 3,231,336 13.44% 427,832 450,000 McHenry 18,635,058 3,221,482 17.29% 381,583 0 DuPage County 17,734,483 977,429 5.51% 25,788 0 Lake Suburbs 9,286,407 291,298 3.14% 207,863 0 SE Wisconsin 2,748,184 249,868 9.09% 280,549 0 Flex 56,793,424 7,561,374 13.31% 1,428,639 0

Industrial Summary 1,009,234,132 111,649,369 11.06% 13,232,667 1,640,912

Industrial Statistics | Year End 2006

Note: Inventory, Available SF and Increase are expressed in net rentable square feet.

Lake County Absorptionin 100,000 sf

7.66

6.075.81

4.033.30

4Q063Q062Q061Q064Q05

7.968.888.9410.08

8.65

Lake County Availabilityin percent

4Q063Q062Q061Q064Q05

Industrial | Lake County

Major Lake County Lease Transactions

Major Lake County Sale Transactions

Tenant Address Size (sf)

Focus Products Group 9501 80th Ave., Pleasant Prairie, WI 100,000Anatol Equipment 801 Technology Way, Libertyville, IL 25,211RJ Furniture 3807 Hawthorne Ct., Waukegan, IL 14,473

Address Size (sf) Price (mil) Price psf Buyer Seller

9625 55th St., Kenosha, WI 175,052 $13.50 $77 Inland Real Estate Group Bradley Associates3731 Sunset Ave., Waukegan, IL 130,000 8.30 64 LIT Industries Panattoni Development

StatisticsMarket Size (sf) ................................................... 63,472,553

Overall Vacant space (sf) ....................................... 5,493,201

Overall Vacancy .......................................................... 8.65%

4Q06 Absorption (sf) ................................................ 329,959

YTD Absorption (sf) ............................................... 2,284,125

Net Rental Rate ............................................... $3.50 - $5.75

Under Construction ............................................................ 0

MARKET OVERVIEWFourth quarter market activity in the northern suburbs was highlighted by the absorption of one of the market’s largest buildings at Lakeview X in Kenosha, WI by Uline. A 600,000-sf build-to-suit distribution center purchased from McShane/Metlife was recently announced by Medline Industries, a lo-cal manufacturer of medical supplies. The property is to be built in the new Liberty Point Business Center in Libertyville. Other signifi cant transactions include Johnson Diversey, Inc.’s recent 10-year, build-to-suit lease of 551,000 sf with Liberty Property Trust for a distribution center scheduled to open in the fall of 2007 in Stutevant, WI.

A growing inventory of speculative facilities in the Lake Coun-ty cities of Gurnee and Waukegan is taking place between 60,000 and 130,000 sf. In particular, developer Panattoni is bullish on this submarket and is delivering institutional qual-ity, high-cube space in Gurnee and at Oak Grove Business Center in Waukegan.

This is an extension of previous success they have enjoyed at the Amhurst Lake Business Park, also in Waukegan.

4

NAI Hiffman Year End 2006 Market Report

5

Industrial | O’Hare

O’Hare Absorptionin 100,000 sf

3.56

4Q063Q062Q061Q064Q05

9.97

6.87

0.55 0.90

9.14 8.82 8.7410.74 10.02

O’Hare Overall Availabilityin percent

4Q063Q062Q061Q064Q05

Major O’Hare Market Lease Transactions

Major O’Hare Market Sale Transactions

Tenant Address Size (sf)

Coaster Company of America 255 Wille Road, Des Plaines, IL 253,410Symons Concrete Forms 2400 Arthur Avenue, Elk Grove Village, IL 230,766W. E. Roe Industries 2200 Mount Prospect Road, Des Plaines, IL 73,286Target Logistics 123 Sivert Court, Bensenville, IL 49,875Associated Global Systems 2001 Estes Avenue, Elk Grove Village, IL 42,080

Address Size (sf) Price (mil) Price psf Buyer Seller

2299 Busse Rd., Elk Grove Village, IL 316,000 $12.50 $40 ProLogis John B. Sanfilippo & Sons1001 Busse Rd., Elk Grove Village, IL 265,000 $8.14 $31 ProLogis Rollex Corporation1501 Nicholas Blvd., Elk Grove Village, IL 225,000 $9.60 $43 ProLogis Rollex Corporation

StatisticsMarket Size (sf) ................................................. 112,847,159

Overall Vacant space (sf) ....................................... 9,864,546

Overall Vacancy .......................................................... 8.74%

4Q06 Absorption (sf) .................................................. 90,224

YTD Absorption (sf) ............................................... 2,130,011

Net Rental Rate ............................................... $3.00 - $8.50

Under Construction ................................................... 52,250

MARKET OVERVIEWThe price of land in the O’Hare market has increased rapidly in the past few years. Developers are now paying 80% more for land than they were in 2003. The reason for this is that many institutional real estate owners are buying land on speculation. The belief is that companies that need to be as close as possible to the airport, such as freight forwarders, will be willing to pay a higher lease rate to be operating in a state-of-the-art distribution facility close to O’Hare. A state-of-the-art facility constitutes a minimum of 28-ft. clear ceilings, an increased number of exterior truck docks (1 dock per 3,200 sf) and increased parking ratios for employees as well as trailer staging areas.

The Eagle Logistics facility at 1717 Busse Road is an example of an institutional owner tearing down an existing outdated facility and building a modern distribution facility for a freight forwarder. This was the fi rst major industrial build-to-suit development in the O’Hare market that started this new trend of tearing down existing buildings.

Rental rates for new Class A facilities range from $6.50 psf to $8.50 psf on a net rental basis. Class B facilities that offer 20-ft. clear ceiling heights lease for $3.75 to $4.50 psf on a net rental basis and buildings offering ceiling heights under 20 feet lease for $3.00 to $3.75 psf net.

6

Industrial | Central DuPage

Central DuPage Absorptionin 100,000 sf

5.84

4Q063Q062Q061Q064Q05

9.658.12

1.06

16.18

Central DuPage Availabilityin percent

4Q063Q062Q061Q064Q05

12.8313.7215.03

14.0811.01

Major Central DuPage Market Lease Transactions

Major Central DuPage Market Sale Transactions

Tenant Address Size (sf)

Lagasse, Inc. 230 E. Lies Rd., Carol Stream, IL 150,796United Stationers 898 Carol Ct., Carol Stream 139,444Weyehaeuser Corporation 300 S. Mitchell Ct., Addison, IL 135,579Ingram Micro, Inc. 284-314 E. Lies Rd., Carol Stream, IL 60,238

Address Size (sf) Price (mil) Price psf Buyer Seller

545-565 Fullerton Ave., Carol Stream, IL 101,336 $8.85 $87 Colony Capital Wrightwood Capital

MARKET OVERVIEWThe Central DuPage market has matured in recent years after several decades of strong growth. Few large land sites remain available for development. This has caused the value of the remaining vacant land sites to rise to between $8.00 and $13.00 per square foot. While land is scarce, users continue to migrate to Central DuPage from Cook County and the surrounding area, attracted by newer product and lower tax rates. Central DuPage is also considered a more centrally located market for distribution companies seeking to serve the metropolitan Chicagoland area.

This year, market absorption has been strong, and avail-ability is at a relatively low 11.01%. Owner occupants have seen an increase in property values over the past few years and tenants have seen rental rates stabilize to between $3.75 and $4.75 per square foot net, depending on the size of the space and level of improvements.

The downward trend of the availability rate combined with the scarcity of available land for development should keep rental rates stable for the foreseeable future.

StatisticsMarket Size (sf) ................................................... 53,509,984

Overall Vacant space (sf) ....................................... 5,890,372

Overall Vacancy ........................................................ 11.01%

4Q06 Absorption (sf) ............................................. 1,618,830

YTD Absorption (sf) ............................................... 3,980,098

Net Rental Rate ............................................... $3.95 - $6.25

Under Construction ............................................................ 0

Pictured above: Carol Point, Carol Stream, where United Stationers leased 139,444 sf.

NAI Hiffman Year End 2006 Market Report

7

Industrial | I-88 Corridor

I-88 Corridor Absorptionin 100,000 sf

5.395.03

2.52

9.96

15.19

4Q063Q062Q061Q064Q05

Major I-88 Corridor Lease Transactions

Major I-88 Corridor Sale Transactions

Tenant Address Size (sf)

WOW Logistics 2540 Prospect Blvd., Aurora 344,681Postal Logistics 2380 Diehl Rd., Aurora 76,120Strata-Tac 1055-1071 Kingsland Dr., Batavia 19,267

Address Size (sf) Price (mil) Price psf Buyer Seller

175 Ambassador Dr., Naperville, IL 331,000 $20.80 $63 - Wrightwood Capital315 Kirk Rd., St. Charles, IL 309,000 $14.40 $47 Inland Real Estate Group Bradley Associates

Italics denotes NAI Hiffman transactions

10.169.238.619.34 9.80

I-88 Corridor Availabilityin percent

4Q063Q062Q061Q064Q05

StatisticsMarket Size (sf) ................................................... 91,230,485

Overall Vacant space (sf) ....................................... 8,939,124

Overall Vacancy .......................................................... 9.80%

4Q06 Absorption (sf) ............................................. 1,580,919

YTD Absorption (sf) ............................................... 2,869,470

Net Rental Rate ............................................... $2.50 - $6.50

Under Construction ................................................... 49,792

MARKET OVERVIEWThroughout 2006, the I-88 Corridor has continued to see steady demand in all size ranges. As a result, several devel-opers have taken new land positions in the Corridor to meet that demand. For example, IDI has introduced Prairie Point West, a 72-acre industrial development located on the south side of I-88 on Molitor Road just west of Eola. They are plan-ning several speculative buildings in the 300,000-400,000 sf range. Also, Duke recently acquired the remaining industrial land in the Butterfi eld Business Park from the Levy Organi-zation. The developer is planning to build several big box industrial buildings either on a build-to-suit and speculative basis.

The lack of available land in feeder markets, such as Cen-tral DuPage, will continue to cause demand to shift towards the I-88 Corridor, particularly for companies who value quick highway access.

The most recent sizable transaction in the I-88 Corridor was a long term lease for 350,000 sf completed at Space Cen-ter’s building located at 2540 Prospect Drive. WOW Logis-tics relocated from a smaller space in Naperville to take over this entire building.

Pictured above: 2540 Prospect Blvd., Aurora, where WOW Logistics leased 344,681 sf this quarter.

8

Industrial | I-55 Corridor

I-55 Absorptionin 100,000 sf

6.35

4Q063Q062Q061Q064Q05

13.57

4.80

1.45

18.88

11.58

I-55 Corridor Availabilityin percent

4Q063Q062Q061Q064Q05

15.8015.0115.7816.8313.87

Major I-55 Corridor Lease Transactions

Major I-55 Corridor Sale Transactions

Tenant Address Size (sf)

Best Buy 2601 Internationale Centre, Woodridge, IL 365,000New Breed Logistics 1170 W. Remington Blvd., Romeoville, IL 86,696Powers Retail Services 375 W. Frontage Rd., Bolingbrook, IL 67,000Blue Package Delivery 1186-1192 Arbor Dr., Romeoville, IL 45,230

Address Size (sf) Price (mil) Price psf Buyer Seller

1000 Veterans Pky., Bolingbrook, IL 315,000 $18.30 $58 ProLogis ML Realty Partners1290 Remington Blvd., Bolingbrook, IL 315,000 $18.30 $58 ProLogis ML Realty Partners505 Crossroads Pky., Bolingbrook, IL 200,000 $11.60 $58 ProLogis ML Realty Partners

Italics denotes NAI Hiffman transactions

StatisticsMarket Size (sf) ................................................... 60,178,866

Overall Vacant space (sf) ....................................... 8,347,294

Overall Vacancy ........................................................ 13.87%

4Q06 Absorption (sf) ............................................. 1,158,427

YTD Absorption (sf) ............................................... 3,779,815

Net Rental Rate ............................................... $2.75 - $7.50

Under Construction ................................................. 444,096

MARKET OVERVIEWThe I-55 Corridor remains the most active and sought after market for industrial development throughout the Chicagoland area, despite a vacancy rate of approximately 13%, down from 16% a year ago. Year-to-date absorption for the Corridor will end similar to last year with approximately four million sf absorbed within the market.

Developers continue to complete speculative projects along I-55. During the year, approximately 4 million sf of new projects were brought on line. More are planned or under construction with delivery scheduled for mid 2007.

Leasing activity within the Corridor was strong in 2006 with notable deals such as Sears – 814,848 sf, Kimberly Clark – 805,912 sf, Levy Home Entertainment – 426,203 sf and Broder Bros. – 425,000 sf, to name a few.

Effective rental rates on 300,000 sf properties and greater range between $2.50 NNN to $2.95 NNN. Rates are expected to remain fl at in the fi rst half of the year with continued optimism that rental growth will start to occur as

the abundance of supply within the submarket continues to be absorbed. Free rent is also prevalent.

Despite the fl at rent growth, the barriers to entry within the market remain very challenging with virtually every piece of developable ground being developer controlled. It is predicted I-55 will remain the most active market in 2007 and absorption will continue to improve.

Pictured above: 1186-1192 Arbor Dr., Romeoville, where Blue Package Delivery leased 45,230 sf.

NAI Hiffman Year End 2006 Market Report

9

Industrial | I-80 East & West

I-80 East & I-80 West Absorptionin 100,000 sf

0.40

0.65

0.890.75

0.97

4Q063Q062Q061Q064Q05

I-80 WestI-80 East

1.14

0.600.58

1.57

1.23

I-80 East & I-80 West Availabilityin percent

15.73

4Q063Q062Q061Q064Q05

16.5717.3516.09

I-80 WestI-80 East

14.3314.0613.6614.37

17.76

13.73

Major I-80 East/I-80 West New DevelopmentsAddress Size (sf) Developer Status

CenterPoint Intermodal Center, Elwood, IL 1,200,000 CenterPoint Properties Under ConstructionAMB Minooka Distribution Center, Minooka, IL 1,000,595 AMB Corporation Planned Spring 2007Minooka Ridge Business Park, Minooka, IL 861,438 OPUS Under ConstructionProLogis Park 80, Bldg., 1, Morris, IL 806,400 ProLogis CompletedCommerce Center at University Park, Univeristy Park, IL 700,000 Clayco CompletedJoliet Crossings, Joliet, IL 575,024 TCB Under ConstructionCherry Hill Business Park IV, New Lenox, IL 522,250 Northern CompletedLogistiCenter at Sauk Village, Sauk Village, IL 258,950 DP Partners Under Construction

Recent construction deliveries include the completion of 806,400 sf building in Morris, IL by developer ProLogis and an 861,438 sf spec building expandable to 1 million sf by Opus North. Absorption for the quarter remains positive with rents averaging $2.50 - $3.00 net for units over 250,000 sf and $3.00 net and up for units under 250,000 sf.

I-80 EASTDuring fourth quarter the availability rate decreased slightly from 14.33% to 13.73% on positive absorption of 1,228,132 sf, with a leasing volume of 567,898 sf noted this quarter.In the corridor, the City of Mokena approved plans for TCB Development Company to develop 250 acres into a busi-ness park. A mix of build-to-suit, speculative industrial and other commercial development is planned. Low interest rates, the abundance of available land, and the close prox-imity to major transportation arteries in the area continue to attract big box distribution users. Rents are currently $2.50 - $3.00 net for units over 250,000 sf and $3.00 net and up for units under 250,000 sf.

I-80 WESTWith abundant land available for development, exceptional transportation links, and low taxes, the I-80 West is a mar-ket undergoing tremendous growth. During the fourth quar-ter, availability increased to 17.76% from 15.73% at the end of third quarter.

Statistics I-80 East I-80 West

Market Size (sf) ..................... 68,993,741 ........... 31,426,566

Overall Vacant space (sf) ......... 9,473,981 ............. 5,580,282

Overall Vacancy .......................... 13.73% ................. 17.76%

4Q06 Absorption (sf) ............... 1,228,132 ................ 971,695

YTD Absorption (sf) ................. 3,549,530 ............. 2,909,108

Net Rental Rate ................. $2.00 - $4.25 ........ $2.75 - $4.50

Under Construction ................... 166,354 ................ 411,840

10

Industrial | Submarket Map

KANE CO.KENDALL CO.

ELG

IN-O'HARE EXPWY.

5594

57

90

9094

55

9094

94

190

294

90

290

294

290

290

80

80

88

355

94

90

53

Lake Michigan

Evanston

Northbrook

Deerfiield

Waukegan

NapervilleAurora

Elgin Schaumburg

OakBrook

Joliet

Bolingbrook

RomeovilleTinleyPark

OrlandPark

St. Charles

CrystalLake

Des Plaines

BuffaloGrove

LakeForest

Libertyville

CHICAGOMIDWAYAIRPORT

Chicago

ILLIN

OIS

INDI

ANA

COOK CO.WILL CO.

COOK CO.DUPAGE CO.

LAKE CO.COOK CO.

KANE

CO.

DUPA

GE C

O.

MCHENRY CO.KANE CO.

MCHE

NRY C

O.LA

KE C

O.

WISCONSINILLINOIS

KEND

ALL C

O.W

ILL C

O. DUPAGE CO.COOK CO.

Lombard

Carol Stream

ChicagoHeights

Hoffman Estates

RollingMeadows

Rosemont

Niles

ArlingtonHeights

OakbrookTerrace

OakPark

Lisle

Warrenville

Gurnee

OakLawn

La Grange

Woodridge

DownersGrove

GlenEllyn

Mundelein

Palatine

McHenry

PalosHeightsLemont

Frankfort

Harvey

BedfordPark

MelrosePark

Elk Grove

Addison

Glenview

Lincolnshire

Cicero

HighlandPark

Skokie

Lake Zurich

Woodstock

KENDALL CO.GRUNDY CO.

LASA

LLE C

O.KE

NDAL

L CO.

DEKA

LB C

O.KA

NE C

O.

UniversityPark

Munster

Scherervil

Cedar Lake

ChicagoHts.

Minooka

NewLenox

Mokena

Morris

Newmark

YorkvilleSandwich

Sugar Grove

Sycamore

Elburn

Batavia

Marengo

Lake inthe Hills

Harvard

Hebron

Walworth

SpringGrove

RoundLake

TwinLakes

West to Rochelle I-88

I-55

I-80

Central DuPage

NorthwestCook North Cook

I-290North

O'Hare

Lake County/Southern WI

GarEast

Chicago

Hammond

De Kalb

BOON

E CO.

MCHE

NRY C

O.

11

NAI Hiffman Year End 2006 Market Report

Investment | Year End 2006

2006 Downtown Office SalesBuyer - Seller Profilein $ million

preliminary533.9

Private -National

Private -Local

REITInstitu-tion

Foreign

198.0

432.0298.0

0.0

Other

BuyerSeller

4,620.3

331.9

1,221.4

287.0

940.0

313.0

2,989.0

2006 Suburban Office SalesBuyer - Seller Profilein $ million

preliminary515.4

Private -National

Private -Local

REITInstitu-tion

Foreign

226.2155.3

0.0 26.9

Other

BuyerSeller

732.0

303.8

524.2398.7

0.0 29.8

381.3

DOWNTOWN OFFICEInvestors continue to be attracted to high-quality well-leased properties. Preliminary numbers for CBD sales show an increase from $4.28 billion (ave. sale price of $208 psf) in 2005 to $6.10 billion ($223 psf) in 2006. Five properties this year either closed or are under contract for over $300 per square foot, and one, One South Dearborn, broke the $400 per square foot barrier.

Local and national private capital bought almost 90% of all properties downtown by dollar volume while selling almost 58%. Other major sellers included foreign capital and REITS, who remain unable to make today’s pricing/returns accretive to their FFO (EPS equivalent). German investors led foreign sellers due to liquidity issues. Institutional capital was also a net seller in 2006.

SUBURBAN OFFICEMuch like the downtown market, private capital, both local and national, drove acquisition activity in the suburbs this year. REITs and institutional capital were net sellers in 2006. Foreign capital was limited to the sale/lease-back of Computer Associates East-West Corridor campus. Preliminary numbers for multi-story sales show an increase from $1.70 billion (ave. sale price of $141 psf) in 2005 to $1.95 billion ($154 psf) in 2006.

INDUSTRIALSales of suburban industrial buildings, 100,000 sf and great-er, totaled $1.58 billion, up from $1.38 billion in 2005. Net buyers included foreign, institution, REIT and private nation-al investors. Others and private local investors were net sellers. Active investors included AMB, Bradley Associates, Cabot Properties, CenterPoint Properties, Cobalt Capital Partners, Colony Realty Partners, First Industrial, IDI, Inland, KTR Capital Partners, Liberty Property Trust, ML Realty, Rose Group, RREEF Funds, TA Realty Associates and Welsh Investments Company. Notable transactions includ-ed CenterPoint Properties’ multi-transaction, $156.6 million 13-property sale ($49 psf) to Australia-based James Fielding Funds; The Rose Group’s 1.1 million SF flex portfolio sale to Colony Realty Partners for $108 million ($98 psf); ProLogis’ 10-building $144.9 million ($52 psf) acquisition from ML Realty; and Inland Realty’s three-building single-tenant portfolio for $27.9 million ($58 psf) acquisition from Bradley Associates. Notable one off transactions included Panattoni Developments’ $8.2 million ($64 psf) sale to LIT Industrial, AMB Fund’s $12.8 million ($42 psf) sale to WCZ, LLC and

TIAA’s (Teachers Insurance & Annunity Associations’) $10.1 million ($82 psf) sale to Prairie Point Building IV, LLC.

Cap rates are expected to stabilize with minimal upward pressure due to the unprecedented levels of liquidity. Event risk could impact cap rates in the short term.

2006 Industrial SalesBuyer - Seller Profilein $ million

preliminary330.4

Private -National

Private -Local

REITInstitu-tion

Foreign

391.5250.4250.8

103.9

Other

BuyerSeller

270.0

769.3

302.2138.7

0.0

216.5151.6

NAI Global

Committed to Chicago. Connected to the world.

NAI Hiffman is the Chicago area representative of NAI Global. NAI Global has the deepest roots in com-mercial real estate. But what makes us different is the way we bring together the people and resources we have around the world to deliver results for our clients. As the world’s only managed network of com-mercial real estate fi rms, we work together to help our clients strategically optimize their assets. Our clients come to us for our deep local knowledge. They build their businesses on the power of our global managed network.

Build on the power of our network.™

NAI Hiffman

NAI Hiffman is the largest full service, privately-owned commercial real estate brokerage and management company in the Chicago region. With over 200 brokers and employees, NAI Hiffman is dedicated to providing our clients with the most compre-hensive real estate services with the highest level of professionalism and integrity.

NAI Hiffman delivers world-class, results-oriented, offi ce, industrial, retail and investment brokerage and management services including:

NAI Hiffman is the Chicago regional representative of NAI Global, the world’s leading managed network of commercial real es-tate fi rms spanning the globe. As the world’s only managed network of commercial real estate fi rms, NAI works together to help our clients strategically optimize their assets. Our clients come to us for our deep local knowledge. They build their business on the power of our global managed network. With over 300 offi ces in more than 40 countries, NAI is connected to the world.

Acquisition & Dispositions Leasing & Subleasing Tenant Representation Property Management

Sale/Leaseback Build-to-Suit Investment Services Site Selection

Due Diligence Market Research Consulting & Strategic Planning Receivership & REO Disposition

One Oakbrook TerraceSuite 600Oakbrook Terrace, IL 60181tel 630-932-1234fax 630-932-7258

One South Wacker DriveSuite 1990Chicago, IL 60606tel 312-327-6900fax 312-923-8023

www.hiffman.com

Recommended

![[K] NAI OXI](https://img.dokumen.tips/doc/110x75/568c4ac21a28ab491699760c/k-nai-oxi.jpg)