13 – 15 March 2017

Merrill Lynch Conference

Merrill Lynch Conference

2

44%

56%

Revenue (R66.5bn)

55%

45%

Operating profit (R4.1bn)

Group revenue and operating profit split – September 2016

Automotive and Logistics Equipment and Handling

Equipment southern Africa

Divisional overview

4

Merrill Lynch Conference

Order book of R1.7bn at end Jan 2017 (Sept 2016: R1.3bn)

Increase in mining and contract mining activity as commodity prices continue to improve

DRC: Major mining customer has indicated intent to resume mobilising a portion of mining fleet

Aftermarket activity remains resilient

Stronger Rand impacting Dollar translation

Equipment southern Africa – operational update

0 1 000 2 000

SouthernAfrica

Order book (Rm)

Jan 2017 Sept 2016

5

Merrill Lynch Conference

Southern Africa sales history

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Rbn

Equipment sales Product support

30%

28%

34%

46%

36%

33%

41%46%

50%

56%

6

Merrill Lynch Conference

31%

56%

8%5%

2016

39%

50%

6%5%

2015

Southern Africa revenue profile by line of business – September

New equipment Product support Used equipment Rental

7

Merrill Lynch Conference

29%

52%

15%

4%

2016

40%

43%

13%

4%

2015

Southern Africa new equipment sales by industry – September

Mining Construction Power Contract mining

8

Merrill Lynch Conference

Upswing in coal and iron ore prices signalling positive global mining recovery

Improved oil price sustainable due to OPEC production cuts

Recent jump in Cu prices buoyed by production reaching plateau

Commodity price movement

Source: Global Economic Monitor (GEM) Commodities

Copper, Coal & Iron ore Platinum & Copper

-

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

-

20

40

60

80

100

120

140

160

2 013 2 014 2 015 2 016 2017M01

Coal Crude oil Iron ore Platinum Copper

USD

9

Merrill Lynch Conference

Commodity mix - mining unit sales by commodity - 2012 - 2016

COALGlencore

South 32

Exxaro

Vale

COPPER

Mopani Copper

Vedanta

Barrick

Palabora Copper

DML

FQM

DIAMONDSDeBeers

Debswana

Namdeb

Petra

Catoca

GOLD B2Gold Gold One

IRON ORESishen

KolomelaKhumani

MANGANESE South 32

PLATINUMPGM

Anglo PlatinumImpala

URANIUM Rossing Uranium Swakop Uranium

ZINCSkorpion

Rosh Pinah

Coal25%

Contractors12%

Copper13%

Diamonds13%

Gold4%

Iron Ore5%

Manganese2%

Other7%

Platinum2%

Rental14%

Uranium1%Zinc2%

10

Merrill Lynch Conference

Surface mining project outlook

Coal PGM / Zinc / Manganese Diamonds Uranium

Coal of Africa – Makhado (2018)

South 32 – Wwk (2017)

Sekoko – Waterberg (2017)

ResGen – Boikarabelo (2018-2019)

Glencore – Zonnebloem (2018)

Glencore - Makoupan Project (2017)

Vale – Moatize Expansion (2017/18)

ICVL – Minas Benga (2017)

Chitotolo / Catoca (2017) - CompleteDebswana – Orapa Cut 3 (2020)

Valencia (Norasa) – (2020)

Debswana – Jwaneng Cut 9 (2019)

Transhex – Namakwa Diamonds (2018)

Tshipi Borwa (2019)

Vedanta Gamsberg (2017) Exxaro – Belfast Project (2019)Foskor (2017) – Complete

Glencore-Shanduka (2017) - Complete

Avel Moolmans – Sishen - (2017)

Iron Ore

11

Merrill Lynch Conference

Underground mining project outlook

Hernic Ferrochrome (2019)

DRC

ANGOLA

NAMIBIA

BOTSWANA

ZAMBIA

ZIMBABWE

MALAWI

MOZAMBIQUE

SOUTH

AFRICA

LESOTHO

Assmang Black Rock (2017-2019)

Venetia Underground Mine

(2020 – 2021)

Platreef Project (2019-2021)

Coal PGM /Zinc/ Manganese Copper Chrome

Kgalagadi Project (2017 - 2020)PGM Maseve (2017 - 2018)

Sasol Longwall (2020)

Palabora Copper (2017 - 2021)Glencore Mopani (2017 - 2020)

Konkola Copper mines (2017 - 2020)

B2Gold Wolfshag (2019 - 2020)

Gold Diamonds

12

Merrill Lynch Conference

Significant rise in the number of enquiries

from contract miners

May signal an increase in mining activities

in the near future

Orders received

WBHO (R45m): A total of 6 units, mainly

construction type of equipment. (6x140k, 4x

336D2L, 2x CS533E, 1x CS78B, 2x232D)

Andru Mining: 20x OHT (10x 777’s and 10x

773’s)

Foskor: 4x 789’s. We have managed to

place equipment in this mine where it was

previously only competitor equipment. This is

a significant milestone.

Exxaro: 8x 777 OHT (2 in Grootegeluk and 6

in Leewpan mine)

South Africa - significant orders received

Cat CS533E Vibratory Soil Compactor & Motor Graders

Off Highway Trucks (OHT’s) for Andru Mining & Exxaro

13

Merrill Lynch Conference

More positive outlook for 2017 than prior year

Glencore indicated that they going to invest further in their

operations in DRC

Increase shareholding in Katanga Mining

Katanga ore leach processing plant to be completed in

second half of 2017

Increase in on site presence at Katanga mining by

approximately 120 people by end of 2017

Large increase in component replacement expected in the

following 18 months

Joint Venture will benefit from:

Cost restructuring that took place in 2016

Increased customer base

DRC update

Equipment Russia

Divisional overview

15

Merrill Lynch Conference

Order book of $56.2m at end January 2017 (September 2016: $21.1m)

Commodity prices, specifically coal, showing signs of recovery – increase in tender activity

Inflationary pressure on operating costs due to strengthening rouble

Capitalise on mining greenfield opportunities driven by improvement in commodities

Protect and grow aftermarket revenues through technology and customer fit solutions

Stronger Rand impacting Dollar translation

Equipment Russia – operational update

0 20 40 60

Russia

Order book ($m)

Jan 2017 Sept 2016

Merrill Lynch Conference

16

0

100

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

$m

Equipment sales Product support

Russia sales history

24%

25%

29%

36%

28%

27%33%

46%

61%

51%

Merrill Lynch Conference

17

43%

51%

1% 4%

2016

34%

61%

1% 4%

2015

Russia revenue profile by line of business – September

New equipment Product support Used equipment Rental

Merrill Lynch Conference

18

68%

7%

8%

4%

13%

2016

59%10%

18%

5%

8%

2015

Russia new equipment sales by industry – September

Mining Construction Power Oil and gas Other

19

Merrill Lynch Conference

Norilsk Nickel

2xR1600 4xR1600 6xR1700

1xR1300

1xPM102

$2.3m $2.7m $5.2m

Polyus

34x793 / 2x785 / 6x777 / 4x773

$117m prime + $24m aftersales (2018)

Sovrudnik

1xM16

$0.9m

RUSAL

4x777G 2x777G

$3.4m $1.7m

AS Siyaniye (Kupol)

2x745 2x745

$0.9m $0.9m

ZDK Pavlik

2x777D

1x16M3

$2.7m

GV Gold Ugakhan

1x6018 1xD9R

5x777G 1xD6R

$8.7m

Bystrinsky

4x789D 8x789D

$9.3m $18.6m

Muna

37 units

$47m (2018)

Delivered

Firm Orders

Greenfields / Major Projects

Current mining opportunities

Gross

1xD6R 1x725C

1xTH514

1x950GC

1xD6R

$0.3m $1.2m

Kekura

37 units

$21m (2018)

Vasilievsky Rudnik

2xD6R 12x773E

2xD9R

$1.8m $7.5m

20

Merrill Lynch Conference

Bystrinsky greenfield success

Prime Product

Contract signed in December 2016 for 12 CAT

789D mining trucks:

• Delivery in 2017

• 4 units shipped in January 2017

• Deal Value: $28m

• Future prospects for up to 20 more CAT 789D’s

Additional equipment under negotiation:

• 2 CAT 6030 FS

• 2 CAT 992K

• 1 CAT 16M

Site service agreement – under negotiation

Parts – on site parts warehouse

Service - 24 hours a day, 7 days a week

Project Manager appointed

Health monitoring and oil sampling

Concentrator complex

Mine workshop

21

Merrill Lynch Conference

Polyus package deal success

Mining Truck order:

Confirmation letter received from Polyus in Feb 2017:

• 34 CAT 793D’s - 2018 delivery

• 6 CAT 777G’s - 2017 delivery

• 2 CAT 785C’s - 2018 delivery

• 4 CAT 773E’s - 2017 delivery

• Total Deal Value: $141m of the following:

o Parts and tooling: $24m

o Machines: $117m

Future prospects:

Up to 15 more CAT 785D’s in 2018-2020

Training and Support Deliverables:

Parts – on site parts warehouse

24 Major components valued at $3.7m

Immersive Simulator

Preventative maintenance bay for 2 trucks

Equipment Iberia

Divisional overview

23

Merrill Lynch Conference

Spanish economic growth driven by buoyant tourism sector, but is not translating into

increased activity in the segments served

Machine industry in Spain shows growth but concentrated in small equipment

Power systems co-generation repowering opportunity in medium term

Marine and Digital capabilities development remains key driver for future growth

Order book growth driven by new machines orders

Focus on cost management and improved efficiencies

Equipment Iberia – operational update

0 20 40

Iberia

Order book (€m)

Jan-17 Sep-16

Merrill Lynch Conference

24

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

€m

Equipment sales Product support

Iberia sales history

30%

30%

34%

40%37%

33% 35%

41% 44% 44%

Merrill Lynch Conference

25

41%

44%

12%

3%

2016

37%

44%

16%

3%

2015

Iberia revenue by line of business – September

New equipment Product support Used equipment Rental

Merrill Lynch Conference

26

4%

44%

52%

2016

2%

46%

52%

2015

Iberia new equipment sales by industry – September

Mining ConstructionPower

Handling

Divisional overview

Merrill Lynch Conference

28

Agreement to dispose of Handling and Agriculture SA assets into 50/50 JV with BayWa at NAV

Trading as BHBW (Pty) Ltd with effect from 1 March 2017 following approval by competition

authorities

Will continue as the exclusive southern African dealer of Hyster and UTILEV lift trucks and

warehousing equipment.

Will continue as the exclusive southern Africa dealer of AGCO products, Massey Ferguson and

Challenger

Extended offering in the agriculture value chain is planned

R297m net proceeds received end February 2017

Joint venture to be equity accounted from 1 March 2017

Handling - Operational update

Automotive

Divisional overview

Merrill Lynch Conference

30

Record result in a challenging trading environment

Revenue R31.4bn (2015: R28.7bn) – up 9.5%

Operating profit R1 654m (2015: R1 529m) – up 8.2%

Operating margin for the year maintained at 5.3%

Strong used vehicle profit contribution

Automotive - operational update

0 100 200 300 400 500 600 700

Car Rental

Avis Fleet

Motor Trading

Sept 2016 Sept 2015

Margin

+14%

-2.1%

+15%

9.0%

9.1%

15.4%

17.0%

2.6%

2.4%

Operating profit (Rm)

Merrill Lynch Conference

31

Well balanced Automotive portfolio provides resilience

Revenue CAGR of 11% delivers operating profit CAGR of 16%

Inter-business unit synergies continue to deliver value

Targeted capital allocation supports value creation

Recently acquired businesses performing in line with expectation

Integrated business model delivers value

0

300

600

900

1200

1500

1800

2011 2012 2013 2014 2015 2016

Rm Operating profit by BU

Car Rental Motor Trading Avis Fleet

0

300

600

900

1200

1500

1800

2011 2012 2013 2014 2015 2016

RmOperating profit

Operating profit 1H Operating profit 2H

Merrill Lynch Conference

32

Sustained growth in rental days

Pleasing revenue per day increase

Fleet utilisation maintained at 75%

Strong used vehicle profit contribution

Customer satisfaction remains above 90%

Maintain market leadership

Car Rental

Car Rental YTD Jan’17 FY’16

Rental days +4.2% +3.8%

Rental revenue per day +2.4% +5.4%

Merrill Lynch Conference

33

Avis Fleet YTD Jan’17 FY’16

Finance fleet +1.0% -2.4%

Under maintenance -3.8% -2.3%

FY’16 financed fleet negatively impacted by Lesotho

contract

Return to finance fleet growth in 2017

Customer retention rates remain high

Net reduction in OEM maintenance plans due to lower new

vehicle sales

Reduced fleet terminations impact used contribution in

FY’16

Positive start to this year with strong contribution from used

Economic environment impact certain African countries

Avis Fleet

Merrill Lynch Conference

34

Motor Trading YTD Jan’17 FY’16

New unit sales -10% -6.4%

Parts revenue +10% +13%

Service hours +6.0% +0.6%

Focused dealership footprint – “Fewer, Bigger, Better”

Strategy continues

New vehicle market remains under pressure

Recent acquisitions support result:

Two Mercedes-Benz dealerships (1 Mar 2016)

Majority share in SMD (1 May 2016)

Positive contribution from aftermarket revenues

Maintained market share

Motor Trading

Merrill Lynch Conference

35

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Total South African Vehicle Market

Passenger LCV M&HCV

Motor Retail

Forecasts and information by Dr. Neal Bruton

Total market forecast for

2017 calendar year:

Growth of 2.5% - 3.5%

Merrill Lynch Conference

36

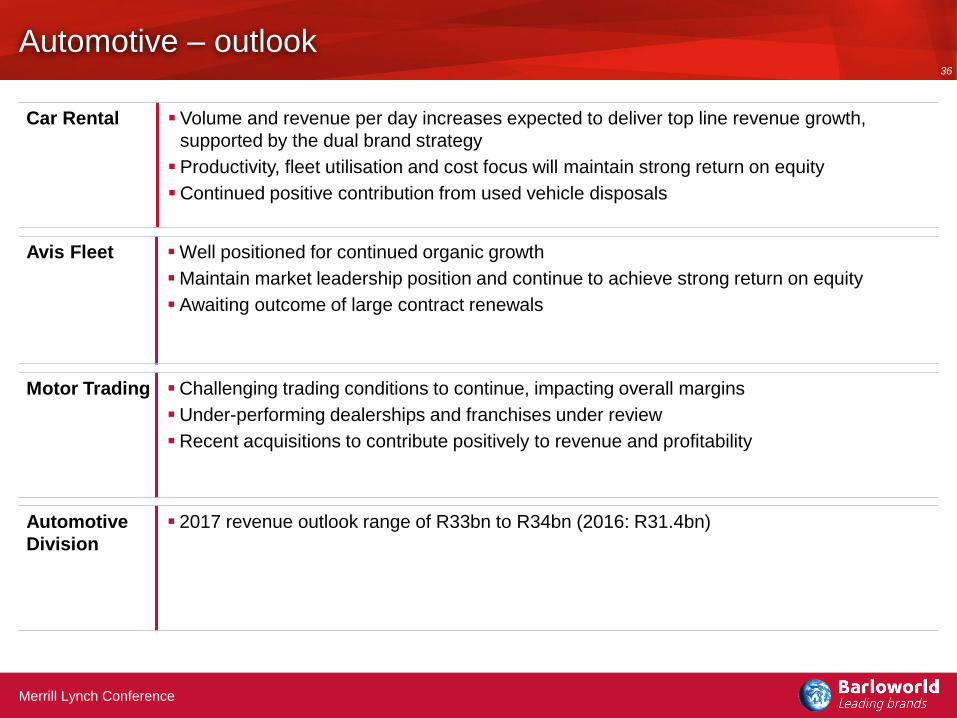

Automotive – outlook

Car Rental Volume and revenue per day increases expected to deliver top line revenue growth,

supported by the dual brand strategy

Productivity, fleet utilisation and cost focus will maintain strong return on equity

Continued positive contribution from used vehicle disposals

Motor Trading Challenging trading conditions to continue, impacting overall margins

Under-performing dealerships and franchises under review

Recent acquisitions to contribute positively to revenue and profitability

Avis Fleet Well positioned for continued organic growth

Maintain market leadership position and continue to achieve strong return on equity

Awaiting outcome of large contract renewals

Automotive

Division

2017 revenue outlook range of R33bn to R34bn (2016: R31.4bn)

Logistics

Divisional overview

Merrill Lynch Conference

38

Trading ahead of last year

Benefit from full financial impact of new contracts and acquisitions

Leveraging investments in Smartmatta, KLL Group and Aspen acquisitions

Diversifying and extending service offerings

Logistics - operational update

Merrill Lynch Conference

39

Diverse blue chip customer base

13 – 15 March 2016

Merrill Lynch Conference

Recommended