8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 1/18

market intelligence

38 . images retail . OCtOBer 2011

market intelligence

OCtOBer 2011 . images retail . 39

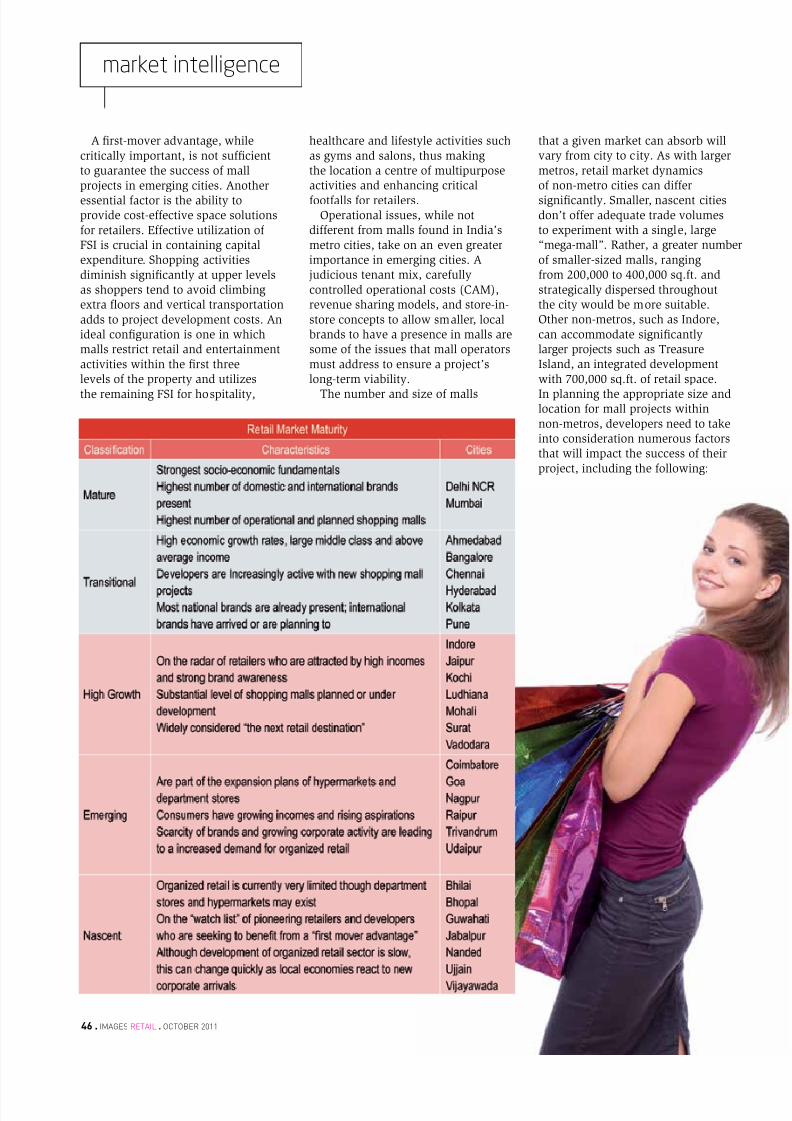

O t Bt Tc20 Idi ti dtitio ot oi

Dfi Cit Ti Jones Lang LaSalle’s city tiering

system is based on the combined

current levels o real estate activity

(supply and demand) in three

key sectors – oces, retail and

hospitality.

• Tier I cities currently comprise

o Delhi, Mumbai and

Bangalore;

• Tier II cities comprise o

Chennai, Hyderabad, Pune and

Kolkata;

• Tier III cities comprise thebalance o the cities in our

analysis.

Cities can move between tiers as

market circumstances change.

Kolkata, or example, moved

rom a Tier III to Tier II city in

2007 to refect increasing levels

o real estate activity. Similarly

in Chennai, real estate activity is

growing so rapidly that the city

may be reclassied as a Tier I city

in the near uture.

InDIa’s CITy TIers

is there lie beyond the metros or indian retailers? actually

there is. here is a look at the most promising emerging retail

destinations o india, rom indore and jaipur to goa and

raipur. excerpts rom a jones lang lasalle meghraj report.

TIER I TIER II TIER III

D el hi C he nn ai L ud hi an a

Mumbai Hyderabad Mohali

B an ga lo re Pu ne J ai pu r

– Kolkata Udaipur

– – Indore

– – Ujjain

– – Bhopal

– – Jabalpur

– – Nagpur

– – Bhilai

– – Raipur

– – Vadodara

– – Surat

– – Nanded

– – Goa

– – Vijayawada

– – Coimbatore

– – Kochi

– – Thiruvana-nthapuram

– – Guwahati

While India is one of the rst

nations to emerge from the global

nancial crisis of 2007, its propertymarket is not emerging without scars.

Across all property asset classes,

none has felt the pain more thanretail. Hardly a week went by in

2008 and early 2009 without some

announcement of retailers scalingback operations, mall projects being

cancelled or shelved, and investors

pulling out of projects.Mid-2009 was a turning point

for the Indian economy. As the

retail sector returned to stability,the condence level of retailers

and investors was renewed. Malldevelopers and operators also tooka wiser approach to new projects in

terms of design, management and

location. Offering quality, well-managed retail space to under-served

markets was a recipe for success that

the wise capitalized on early.

As a new decade begins, India’s

retail sector moves beyond infancy,where organized retail was just

beginning to get a foothold in

major metros, to adolescence whereorganized retail has penetrated deeper

into Indian markets. In order to

understand the opportunities in theretail property market as the Indian

retail sector progresses in its path

of maturity, one needs to go off thepath so often taken by developers,

investors and retailers, both domestic

and foreign. An exploration of markets

off the beaten track will reveal wherethe new geography of opportunity lies

in the Indian retail property market.For the purposes of our analysis,

we have looked beyond India’s top

7 metros to focus on a selection of

20 markets that are in various stagesof retail maturity. We examine the

changing plot of the Indian retail story

and assess the lessons learned and

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 2/18

market intelligence

40 . images retail . OCtOBer 2011

new trends as a result of the global

economic downturn. Our examination

of these 20 markets also goes intocategorizing them into levels of

maturity and places that information

against current rental levels to

assess which ones pose the greatest

opportunities for developers, investors

and occupiers.

The resIlIenCy O COnsumerIsm

As in many nations, retail

consumption in India was severely

impacted as a result of the global

economic downturn. Now that the

nation’s economic recovery is well

under way, it is becoming apparent

that the underlying factors which

propelled India’s high-octane

consumerism in the past remain truetoday:

• Demographics are still favourable

with two-thirds of the nations

population below age 35

• Urbanization is still rapidly

occurring, and at a greater depth

with many Tier III and Tier IV

cities providing concentrations of

retailing potential

• India’s economy seems

unstoppable, suffering only a

slowdown in the rate of growth

during the global economic crisis

while others contracting

Net Domestic Product & Monthly Per Capita Consumption in India

Source: Ministry o Statistics and Programme Implementation, Government o India

*: Non-ood includes clothing & ootware, durable goods, education, uel & light, rent, taxes and misc. goods & services

• India’s middle-class is still growing

as are per capita incomes and the

availability of credit.

• The depth and breadth of

organized retail penetration

beyond India’s major metros is

still continuing into markets which

offer favourable opportunities for

retailers and property developers.The Indian retail market stood at

USD 330 bn in 2007 with little more

than 4 percent of it being attributed

to the organized retail sector. By the

end of 2010 the organized segment

is to grow to 10 percent of total

retail within the country. This rapid

growth of organized retail is partially

attributed to the phenomenal burst

of new shopping malls built over the

last three years, an increasing number

of which are located in the nation’s

smaller, under-served markets.

However, organized retail is also being

driven throughout India by resilient

consumers who are typically young,urbanized and brand-conscious

shoppers with changing preferences

towards consumerism.

reTaIl In nOn-meTrO markeTs

The retailing landscape varies

signicantly across India as markets

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 3/18

market intelligence

44 . images retail . OCtOBer 2011

differ greatly in size, maturity and

purchasing power. Developers and

operators of retail property in smaller

Indian markets need to be cognizant

of the variations that exist between

metros and non-metros as they plan,

build and operate shopping malls.

TypOlOgy anD Orm

The retail activities in India’s smallercities are typically known by their

traditional markets – bazaars and

fairs – which have over eons served

as crossroads for retail and wholesale

trade, barter and entertainment,

much like souks in the Middle

East. Historically, these stretches

of urban patch provided “shopping

entertainment” for traders and

consumers. Indeed, the traditional

markets, which contained the bazaars

and fairs, have played a pivotal role in

the origin and growth of these cities.In present-day emerging cities,

shopping areas display some common

trends that can be discerned and

discretely classied into non-exclusive

categories of CBD-Linked Street,

Arterial Street, Afuent Market

or Landmark Adjacent Market.

Shopping areas in emerging cities

have historically been formed along

important transport corridors or trade

routes. As these cities evolve, new

routes and neighborhoods provide

fertile ground to develop new age,

organized retail destinations. MR-10

in Indore is one such example of a

new transport corridor around which

clusters of new residential and retail

settlements have developed as the

population has grown.

keys TO suCCess: plannIng,

DesIgn, OperaTIng & IrsT-mOver

aDvanTages

The rst shopping centres developed

in India’s emerging cities witnessed

an unprecedented level of interest

from consumers and became the

primary destination for shopping,

eating and entertainment. A lack

of entertainment options and an

inconvenient retail environment

caused by lack of parking, crowdedlanes and uncomfortable weather,

made the rst such developments in

each city very successful. First movers

into cities such as Indore (Treasure

Island, 2005), Surat (Iscon Mall,

2008) and Vadodara (Central Mall,

2008) witnessed healthy footfalls

and sales volumes. These pioneering

developments provided the means

for national and international brands

including Pantaloon, Westside, Levis

Strauss, Big Bazaar, Nike and PVR

to penetrate into India’s untapped

markets.

The TraDITIOnalmarkeTs InCluDIng TheBazaars anD aIrs havehIsTOrICally playeDa pIvOTal rOle In TheOrIgIn anD grOwTh OCITIes aCrOss InDIa.

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 4/18

market intelligence

46 . images retail . OCtOBer 2011

A rst-mover advantage, while

critically important, is not sufcient

to guarantee the success of mall

projects in emerging cities. Another

essential factor is the ability toprovide cost-effective space solutions

for retailers. Effective utilization of

FSI is crucial in containing capital

expenditure. Shopping activities

diminish signicantly at upper levels

as shoppers tend to avoid climbing

extra oors and vertical transportation

adds to project development costs. An

ideal conguration is one in which

malls restrict retail and entertainment

activities within the rst three

levels of the property and utilizes

the remaining FSI for hospitality,

healthcare and lifestyle activities such

as gyms and salons, thus making

the location a centre of multipurpose

activities and enhancing critical

footfalls for retailers.Operational issues, while not

different from malls found in India’s

metro cities, take on an even greater

importance in emerging cities. A

judicious tenant mix, carefully

controlled operational costs (CAM),

revenue sharing models, and store-in-

store concepts to allow smaller, local

brands to have a presence in malls are

some of the issues that mall operators

must address to ensure a project’s

long-term viability.

The number and size of malls

that a given market can absorb will

vary from city to city. As with larger

metros, retail market dynamics

of non-metro cities can differ

signicantly. Smaller, nascent citiesdon’t offer adequate trade volumes

to experiment with a single, large

“mega-mall”. Rather, a greater number

of smaller-sized malls, ranging

from 200,000 to 400,000 sq.ft. and

strategically dispersed throughout

the city would be more suitable.

Other non-metros, such as Indore,

can accommodate signicantly

larger projects such as Treasure

Island, an integrated development

with 700,000 sq.ft. of retail space.

In planning the appropriate size andlocation for mall projects within

non-metros, developers need to take

into consideration numerous factors

that will impact the success of their

project, including the following:

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 5/18

market intelligence

48 . images retail . OCtOBer 2011

• Demographics and income levels

• Connectivity and proximity

to local destinations such as

tourist attractions, education and

health hubs, and commercialdevelopments

• Presence of competing retail

centres and high streets

• Consumer behavior patterns

including share of wallet across

product categories and frequency

of shopping

• Expected geographic growth

patterns of their city

• Changing consumer proles and

increasing levels of afuence.

20 reTaIl DesTInaTIOns TO waTCh

In 2007, Jones Lang LaSalle’s World

Winning Cities Research Programme

published a landmark study on the

Indian retail sector entitled “The

Geography of Opportunity – The

India 50”. In that report, 50 Indian

cities were classied into 5 categories

based upon the socio-economic

fundamentals, retail demand and

retail supply found within those

markets.

As the retail industry in India

matures and looks for new growth

The nexT Three CaTegOrIesO reTaIl ClassIICaTIOn– hIgh grOwTh, emergInganD nasCenT – Is whereThe aCTIOn wIll Be asreTaIlers anD DevelOpersenDeavOur TO Deepen TheIrunDersTanDIng O ThesemarkeTs anD CapITalIzeOn The OppOrTunITIes ThaTThey presenT.

strategies in the wake of the global

economic downturn, we felt a fresh

look at our analysis was appropriate.

While the methodology employed and

factors considered for classicationremained the same in our most recent

analysis, we expanded the set of cities

that we considered.

Our results reveal that the set

of cities in our top two categories,

Mature and Transitional, have not

changed from our original analysis.

Retail in these top eight markets

is fairly well understood and

documented, and these cities no

longer represent the frontier of retail

in India.

Conversely, the next three categoriesof retail classication – High Growth,

Emerging and Nascent – is where

the action will be as retailers and

developers endeavour to deepen their

understanding of these markets and

capitalize on the opportunities that

they present. While a large number of

Tier III cities in India can be placed

in one of these three categories, we

have limited our discussion to 20

markets which we feel best illustratethe characteristics of the category

based upon consumer proles, market

characteristics and developer activity.

hIgh-grOwTh CITIes

InDOre

Indore, the commercial capital of

Madhya Pradesh, is the centre of

business and trading activities in

Central India. While the city is also

known for its textile industry, Indore

is undergoing fast-paced infrastructuredevelopment to match the future

demand from other industrial sectors.

The state and local government

are undertaking several initiatives

to promote Indore as a premier

destination for investment.

Being a historic city, Indore has a

distinct core (old city) with newer

developments spread spatially

around in a concentric manner.

Residential, retail and institutional

areas dominate the city core in which

wholesale markets are prevalent andtraditional high streets dominate the

retail landscape. Khajuri Bazaar and

Kothari Market are located on M.G.

Road, which, along with Jawaharlal

Nehru Road, dened the retail hub

of the city before the emergence of

markets adjacent to Palasia Chauraha

and Bombay Hospital. Presently, a

signicant amount of retail activity is

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 6/18

market intelligence

50 . images retail . OCtOBer 2011

occurring in the central and eastern

parts of the city close to the high-end

residential locations such as Palasia,

Race Course, Saket, Gulmohar as

well as the upcoming locations suchas Vijay Nagar, MR 10 and Indore

Bypass.

A high number of afuent

entrepreneurs who reside in Indore are

driving the demand for local brands

along with national and international

retailers. Older, unorganized high

street markets are slowly giving way

to organized retail with the arrival of

new malls and shopping centres in

the city.

Approximately 1.7 mn sq.ft. of retail

space currently exists in Indore withanother 2.5 mn sq.ft. expected in the

next few years as 3-4 mall projects

have been announced. With several

prominent retailers considering

venture in the city, organized retail

has a bright future in Indore.

JaIpur

Jaipur, the capital of Rajasthan, is

a major international and domestic

tourist destination as part of India’s

Golden Triangle tourism circuit.Proximity to Delhi and Gurgaon is

helping to fuel both tourism and retail

activity in Jaipur. Economic growth,

rising disposable incomes and a

changing socio-economic environment

have led to the expansion of urban

spaces around the city with suburban

and peripheral locations becoming

the focus of development. Arterial

roads, such as M.I. Road and

Sansar Chander Road have becomefully commercialized for retail and

wholesale trade.

Jaipur is the rst city in Rajasthan

to have experienced modern

shopping plazas and multiplexes.

Approximately 10 shopping mall-

cum-multiplexes, totalling 800,000

sq.ft, are operational at various

locations in the city, with another 15

in the developing or planning stages.

Upcoming integrated townships

within Jaipur’s suburbs and along its

growth corridors also have a retailcomponent as a part of their product

mix. Major malls currently operational

in the city include Crystal Court, Mile

Stone, Mall 21, Silver Square, Crystal

Palm, City Flex, MGF Metropolitan

and Silver Square.

Retail spaces have a high rate of

absorption in Jaipur with major

brands and anchors such as Shoppers

Stop, Blackberry, McDonald’s and Big

Bazaar taking up space. There may

be a temporary oversupply condition,

but it is likely to get absorbed by

organized retail spaces offering

JaIpur Is The IrsT CITy InraJasThan TO experIenCemODern shOppIng plazasanD mulTIplexes. arOunD10 shOppIng malls-Cum-mulTIplexes areOperaTIOnal aT varIOuslOCaTIOns

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 7/18

market intelligence

52 . images retail . OCtOBer 2011

unique shopping experiences and

an increasing population as Jaipur

continues to mature as a commercial

destination.

kOChI

Kochi, also known as Cochin, is the

commercial capital of Kerala and

has historically been an important

port city in India. As a major tourist

destination and the gateway to

Kerala’s backwaters, Kochi has

witnessed growth in medical tourism

and eco-tourism, along with a boom

in its local IT/ITES sector, elevating

the city into an important investment

destination in South India.

As with other emerging cities inIndia, retail activity in Kochi has

traditionally been concentrated on a

central high street, with M.G. Road

being the dominant retail corridor of

merchants dealing in gold, textiles

and various other items. Marine

Drive, a more recent retail destination,

is challenging M.G. Road as the

preferred high street in Kochi, as

are the areas of Vytilla Junction,

Palarivattam and Edapally.High street dominance is about

to change in Kochi with a variety of

new retail formats being developed

throughout the city. The North-South

National Highway 47 bypass is being

transformed into a mall corridor.

Presently the city has one functional

mall and six malls are under various

stages of construction including a

1mn sq.ft. project by the Lulu Group.

Other builders such as Prestige

Group, Aerens Group, Abad Builders

and Emkay Group are working on

mall projects that will be of various

kOChI has wITnesseDgrOwTh In meDICalTOurIsm anD eCO-TOurIsm,alOng wITh a BOOm InITs lOCal IT/ITes seCTOr,

elevaTIng The CITy InTOan ImpOrTanT InvesTmenTDesTInaTIOn In sOuTh InDIa.

standards, specialities and use

formats.

luDhIana

Ludhiana, known for its hosieryand sporting goods industries, is

the most populated city of Punjab.

The service sector, which includes

nancial, banking and public services,

also plays an important role in thecity’s economy. Good connectivity

with major cities and an encouraging

business environment has made

the city the favourite investment

destination of the state.

Ferozpur Road is the main growth

corridor for retail and commercial

development in Ludhiana, in addition

to being a well-known, high-end

residential destination. Punjab

Agricultural University, Hotel Majestic

Park Plaza (the only 5-star hotel in the

city) and the Feroze Gandhi Market

(the only organized commercial centre

of Ludhiana) are located along this

major artery.

Over the past couple of years,

Ferozpur Road has witnessed major

developments in the organized retailsector with Ansal Plaza, Flamez

Mall and Westend Mall becoming

operational. This is mainly a result

of its proximity to the city centre and

posh residential colonies, presence of

prominent hotels, and the declining

popularity of Mall Road (the city’s rst

organized retail corridor) among the

retailers and consumers for its scarce

parking facilities.

Arterial development together

with improving infrastructure has

facilitated the growth of the realestate market in Ludhiana. The

entry of established players has

induced competition into the market,

thereby leading to a renewed focuson quality real estate projects.

Numerous national and local

developers including Ansal API, DLF,

MBD Group, Omaxe and Chadha

Group have proposed further retail

developments along Ferozpur Road.

mOhalI

Mohali can be regarded as a planned

extension of the city of Chandigarh.

Residents of this town are compelled

to travel to Chandigarh to shop due

to a shortage of quality local retail

destinations. The main markets of

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 8/18

market intelligence

56 . images retail . OCtOBer 2011

Mohali have been developed as sector

markets, as the cities of Chandigarh

and Mohali are collectively divided

into 74 sectors.

Many of Mohali’s sector marketsare located on a straight road from

Sector 58 to 65. Most of the ground

oor space in this retail corridor has

been occupied by local merchants

including restaurants, grocery shops,

departmental stores, jewellers, white

good showrooms and banks.

The Punjab Urban Planning &

Development Authority (PUDA) is

developing the Sector 70 market

to entice Mohali residents to shop

locally. Underlying factors including

a large segment of population inthe higher socio-economic proles

seeking residential options in the

region, proximity to Chandigarh, and

initiatives taken by the Government of

Punjab to promote industrial and IT/

ITES development are likely to have

a positive impact on Mohali’s retail

development.

Shalimar Mall and Mall Matrix, with

a combined area of 300,000 sq.ft., are

the rst malls proposed in Mohali. Six

additional malls are in various stages

of construction. These projects, along

with others that have been planned,

could add an additional 5.5 mn sq.ft.

of new retail space.

suraT

Surat, renowned for its textilemanufacturing and diamond

cutting/polishing industries, is a

major industrial hub in Gujarat.

Industrialization has not only boosted

the local real-estate market but has

also drawn an inux of migrants

from neighbouring cities. Rising

population and income, along with an

optimistic employment outlook, will

continue to boost retail development

in Surat which is ush with afuent

consumers.

Excellent road connectivity hasencouraged retail mall development in

outlying areas such as Piplod, Vesu,

Varachha Road and near Udhana

Navasi Road. The most preferred retail

destinations in the city are Dumas

Road, Parle Point, Ghoddod Road,

Piplod and Ring Road.

Well-known brands have not only

entered Surat but have also expanded

with multiple outlets in the city.

Surat has several retail investments

from major domestic brands such as

Croma, @ Home, Reliance Fresh, Big

Bazar and Shoppers Stop.

Existing retail space in Surat totals

to approximately 600,000 sq.ft. With

three to four malls in the planning

stage, another 560,000 sq.ft. of new

retail space is expected to enter the

market.

vaDODara

Vadodara lies along Gujarat’s

golden corridor which extends fromAhmedabad to Vapi. The city is one

of India’s foremost industrial centres

with dominant groups of chemicals

and pharmaceuticals manufacturers.

The centre of Vadodara is

dominated by residential, commercial

and institutional districts. Wholesale

markets and high-street retail areas

dominate the retail typology in this

core area of the old city and adjacent

areas. Here, Vadodara’s traditional,

established markets can be found

along the prominent shopping

corridors of Mahatma Gandhi Road

InDusTrIalIsaTIOn InsuraT has nOT OnlyBOOsTeD lOCal realesTaTe markeT BuT hasalsO Drawn mIgranTs

rOm neIghBOurIngCITIes.

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 9/18

market intelligence

58 . images retail . OCtOBer 2011

vaDODara’s emergIngCOmmerCIal anD reTaIlDIsTrICTs are prInCIpallylOCaTeD On The wesTernsIDe O The CITy. rC DuTTrOaD, raCe COurse rOaDanD OlD paDra rOaDhave emergeD as amOusCOmmerCIal DesTInaTIOnswIThIn The CITy.

(Nyay Mandir Gate to Mandavi

Gate), Raopura Road, Rajmahal Road,

Mangal Bazaar and Dandiya Bazaar.

Vadodara’s emerging commercial

and retail districts are principallylocated on the western side of the

city’s railway line. R.C. Dutt Road,

Race Course Road and Old Padra

Road have emerged as the prime

retail and commercial destinations

within the city. A majority of national

and international brands operating

in Vadodara are primarily located

along these roads. The predominant

typology of retail developments found

here are commercial complexes with

retail space on the lower ground and

upper ground oors with ofce spaceabove. Approximately 4.6 mn sq.ft. of

retail space is operational in Vadodara

with another 1 mn sq.ft. of new retail

space expected to enter the market

in the next few years as additional

projects are in various stages of

planning and development.

COImBaTOre

Coimbatore, a key industrial city

in South India, is regarded as the

preferred IT destination in Tamil Nadu

after Chennai. Several private sector

initiatives in the city have contributed

to an increase in real estate activity

in the region. Since commercial

establishments already have theirpresence in the CBD of the city, located

at the high density areas of RS Puram

and Race Course Road, new commercial

locations have been encouraged to set

up along major corridors towards the

outskirts of the city.

Coimbatore has its traditional retail

markets on Oppankara Street and

Cross Cut Road where both wholesale

and retail businesses are conducted.

Other retail markets can be found in

and around the residential locations of

Avinashi Road, Race Course Road and

100 Feet Road.

High streets such as BharathiyarRoad, Avinashi Road, Mettupalayam

Road and Cross Cut Road are currently

the main retail hubs of the city.

Brands including Ford, Nokia, Philips,

Hyundai, Sony, Bajaj,and Hero Honda

presently have their showrooms

scattered across these markets while

the likes of Zodiac, Lee, Nike, Reebok

and United Colors of Benetton are

found in RS Puram.

gOa

The state of Goa, located along India’sWestern coast, is the nation’s foremost

tourist destination. A steady growth

of tourist arrivals, both foreign and

domestic, has resulted in the state

achieving rapid economic growth.

The northern part of the state has

seen greater relative prosperity,

infrastructure development and early

commercialisation. South Goa has

provided the region with a dynamic

hospitality industry including a

number of ve-star deluxe hotels

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 10/18

market intelligence

60 . images retail . OCtOBer 2011

typology found in Goa is high street

shopping with major clusters located

near Main Avenue, Dr. A.B. Road,

18th June Road, and M.G. Road.

Being a tourism hub, theretail markets in Goa are largely

unorganized and are located at the

beach towns of Baga, Candolim and

Calangute, with the latter two having

well-developed high streets that are

home to high-end brands. While mall

developments are yet to come up,

a number of multi-storied shopping

centres are underway in Goa. A

further two retail developments (OsiaMall and Prot Centre) are proposed

in Margao and will total 100,000 sq.ft.

retail space.

nagpur

Nagpur, the largest city in central

India, is also the third most populous

city of Maharashtra. The city’s retail

market has existed in an unorganized

form in areas such as Itwari and

Sitabuldi, and in a semi-organized

form in the western part of the city.

These markets typically developed

near high-end residential settlements

where residents belonging to

Nagpur’s trading class possessed a

high propensity to spend. The city’s

established prime retail areas include

Dharampeth, Ramdaspeth, Gokulpeth,Central Avenue, Gandhibagh, Sadar,

and Sitabuldi, with locales such as

Wardhaman Nagar, Wardha Road, and

Khamla having been identied as high

potential areas.

Six malls are currently operational

in Nagpur. The city’s planning

authority is working with private

developers to ensure balanced retail

development in Nagpur. Large scale

projects such as MIHAN (Multimodal

International Hub Airport at Nagpur),

a proposed IT SEZ, and ButiboriIndustrial Estate have lead to an

increased demand in the residential

sector, which in turn has generated

demand for retail and commercial

spaces in the city. An ongoing IT/

ITES boom has also led to the inux

of young migrants who demand

organized retail outlets and have a

willingness to pay.

The past few years have seen

an emphatic transformation in the

number of retail brands that have

come into Nagpur. Retailing itself hasundergone a considerable shift, and

more can be expected in the near

future as traditional markets slowly

give way to organized retail formats.

The existing 1.5 mn sq.ft. of existing

retail space in Nagpur is expected to

double as three to four malls are beingplanned or developed.

raIpur

Raipur, a major trading and business

hub for the entire Chhattisgarh region,

has a large number of specialized

markets for various commodities. A

majority of these traditional markets

are located in the centre of the city

with newly emerging retail areas along

the Grand Eastern Road (NH-6). The

stretch on NH-6 between Tati Bandh

to Teli Bandha has emerged as the

most active retail destination in the

The exIsTIng 1.5 mn sq.T. O exIsTIng reTaIl spaCe Innagpur Is expeCTeD TO DOuBle as Three TO Our mallsare BeIng planneD Or DevelOpeD

along its coast-line. Panaji, the CBD

of Goa, comprises a signicant part of

Goa’s retail market.

With its year-round ow of

international and domestic tourists,Goa is a small but signicant

retail destination. Retail real estate

development is concentrated along

three of the city’s major arteries: A. B.

Road, M.G. Road and 18th June Road.

International and domestic brands are

located along M.G. Road, while local

retailers are concentrated on 18th

June Road. The predominant retail

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 11/18

market intelligence

62 . images retail . OCtOBer 2011

OrganIzeD reTaIl IswIDespreaD ThrOughOuTuDaIpur wITh Durganursery rOaD, shakTInagar anD suDkhaDIaCIrCle havIng The largesTCOnCenTraTIOn O newenTranTs. a seleCTIOn OTOp BranDs Is presenT InThe CITy

recent years whereas Sharda Chowk

and Jaistambh Chowk are noteworthy

markets in the city centre.

A few small, unorganized shopping

centres have been completed over thepast few years with Raipur getting

its rst shopping mall, City Mall 36,

followed by two or three more in

recent years.

TrIvanDrum

Trivandrum, the capital of Kerala, is

the second largest city in the state and

home to a large population of urban

professionals. Technopark, a 340 acre

IT park located in Trivandrum, is one

of the largest IT parks in India with

150 marquee IT rms and over 20,000employees.

Large-scale employment

opportunities such as this are a major

part of the reason that Trivandrum

witnessed a 42 percent increase in

population during 1991-2001 and

why it is ranked second in the state

of Kerala in terms of market potential

and afuence.

Trivandrum’s central business

district is also the heart of the city’s

traditional retail district with Palayam,

Chala and East Fort being the 3

most prominent markets. M.G. Road

and the area between Pattom and

Kesavadasapuram are the growth

corridors of retail in the city. Kedaram,

Karimpanal Arcade and Attukal

Shopping Complex are some of the

noteworthy shopping destinations

within the city.

The suburbs, which are residential

in nature, currently only haveneighbourhood format retail stores.

While retailers have land banks

in the suburban areas (in close

proximity to Technopark), no major

development has taken place yet to

explore the potential of this area. Only

58,000 sq.ft. of retail space exists in

Trivandrum.

uDaIpur

The lake city of Udaipur is a

popular tourist destination in India.

Historically, retail markets in Udaipur

have been an integral part of the city.

As Udaipur grew beyond the banks

of its lakes, major transportation

arteries developed into retail corridors.

Retail high streets continue to be

xture along Bapu Bazaar, Chetak

Circle, Suraj Pole, Ashwini Bazaar,

Nehru Bazaar, Bada Bazaar, ShastriCircle, Delhi Gate, Sindhi Bazaar,

Town Hall and Chand Pole. These are

complimented by specialized high

streets at Ghantaghar Market Udaipur

(jewellery), Malda Estate (apparel)

and Hathi Pole (antiques).

Organized retail is widespread

throughout Udaipur with Durga

Nursery Road, Shakti Nagar and

Sudkhadia Circle having the largestconcentration of new entrants.

A wide selection of international

and domestic brands is present in

Udaipur across numerous categories

of retail with Nokia, Adidas, John

Players, Levi Strauss and Pizza Hut

already having a presence in the city.

Domestic supermarkets such as Big

Bazaar and Reliance Fresh have also

established themselves in prominent

locations within Udaipur. Movie

theatres, both new (Fun Cinemas) and

reconstructed (Paras Cinema) are also

well represented in the city.

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 12/18

market intelligence

64 . images retail . OCtOBer 2011

t i’

w ’ v . W

z - v ,

w . n

w

v w

v .

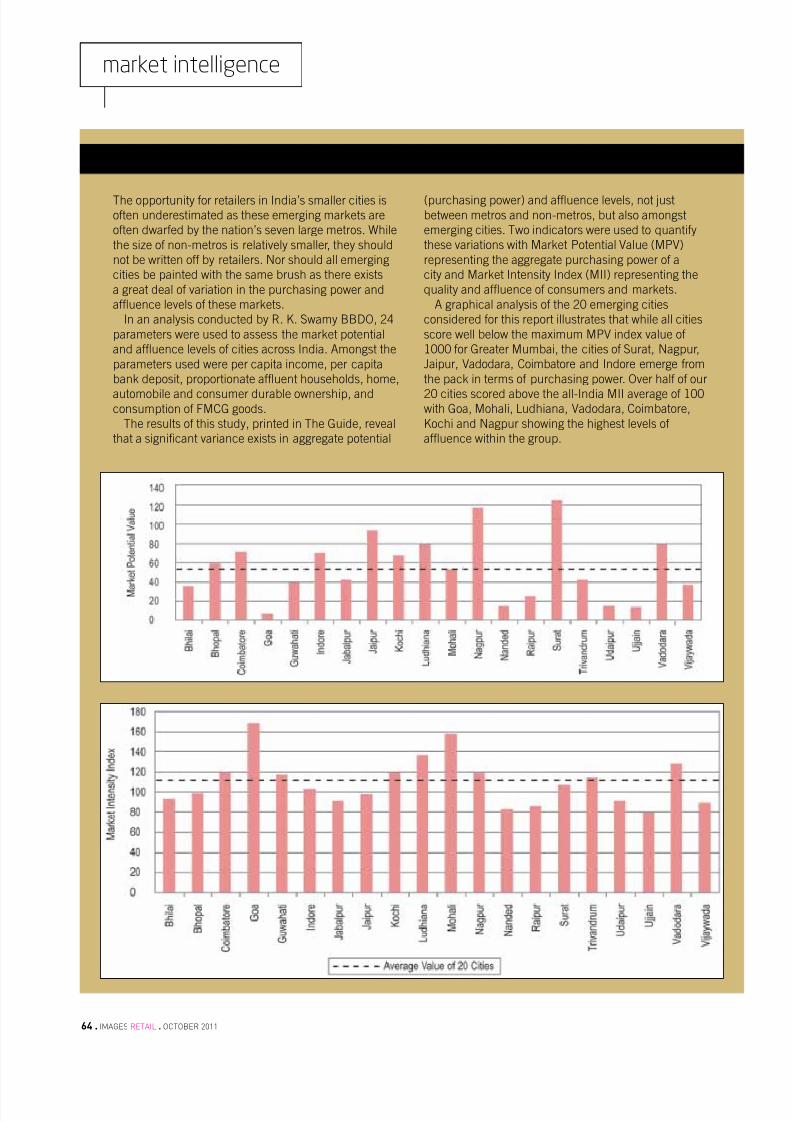

i r. k. sw bbdo, 24

w

v i. a

w ,

, , ,

w, mcg .

t , t g, v

f v

( w) v, w -,

. tw w q

v w m p V (mpV)

w

m i i (mii)

q .

a 20

w

w w mpV v

1000 g m, s, n,

j, V, c i

w. ov

20 v -i mii v 100w g, m, l, V, c,

k n w v

w .

The purChasIng pOwer anD aluenCe O InDIa’s emergIng CITIes

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 13/18

market intelligence

66 . images retail . OCtOBer 2011

nasCenT CITIes

BhIlaI

Bhilai, the second largest city in thestate of Chattisgarh, is known as the

steel capital of India. Home to India’s

largest steel plant, SAIL, Bhilai is one

of the most industrialized sectors of

the state.

The inux of professionals working

at SAIL has added a cosmopolitan

avour to the local culture of the city

and spurred demand for organized

retail. Bhilai is ranked as the top

city of Chhattisgarh state in terms of

market potential and afuency.

NH-6 is the central retail corridorin Bhilai with major developments

located around the main junctions of

the highway. Among the city’s sectoral

markets, the City Centre and Sector-6

markets are the most popular.

The format of retail developments in

Bhilai is mostly high street in nature

with some mixed-use retail-and-ofce

complexes found in projects such as

Chauhan Estate and Dhillon Complex.

A few brands such as Raymond,

Reebok, Titan, Koutons , Gini & Jony

and Peter England can be found in

markets along NH-6 such as Supela

Chowk and Akash Ganga.Retail projects in the upcoming

areas of Bhilai typically do not have

an independent existence but can be

located in the ground and rst oors

of residential apartments. These are

mostly full service departmental

stores. Although there are no

multiplexes in Bhilai, some traditional

cinema halls including Venkatesh,

Maurya and Chandra have upgradedthemselves to cater to the city’s

present needs.

Presently, the city of Bhilai does

not have any shopping mall although

a 690,000 sq.ft. project is being

developed by Entertainment World

Developers.

BhOpal

A few malls are under construction

or planned in prominent areas of

the capital city of Madhya Pradesh.

Various mixed-use commercialcomplexes in the city currently

showcase a few brands. Organized

retail exists to a limited extent in

scattered areas of Bhopal in the form

of some supermarket chains.

The area around Hoshangabad

Road is also fast developing into a

commercial sector. Approximately

240,000 sq.ft. of retail space exists in

Bhopal.

whIle The sIze O nOn-meTrOs Is relaTIvelysmaller, They shOulDnOT Be wrITTen O ByreTaIlers. nOr shOulD allemergIng CITIes Be paInTeDwITh The same Brushas There exIsTs a greaTDeal O varIaTIOn In ThepurChasIng pOwer anDaluenCe levels O ThesemarkeTs.

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 14/18

market intelligence

68 . images retail . OCtOBer 2011

guwahaTI

Guwahati, the capital city of the

state of Assam, is the gateway to

the north-eastern states of India.

The petroleum and tea industriesdominate the Guwahati economy

which is the centre of culture,

politics, and commerce for the entire

region. An inux of migrants over

the past decade has caused the city’s

population to swell by more than 40

percent and provided a boost to the

development of the region.

Retail markets were traditionally

conned to the city centre in

Guwahati with areas such as Pan

Bazaar, Paltan Bazaar and Fancy

Bazaar being the most popularmarkets. Arterial thoroughfares

eventually developed into retail

corridors, with the G.S. Road

becoming the most prominent.

Departmental stores, supermarkets

and large format stand-alone stores

are the most popular retail formats

in Guwahati. With the development

of the shopping malls and plazas,national and international brands

have started to migrate from high

streets into malls.

Big Bazaar (stand-alone), The Hub,

Cube Mall, Dona Planet and Sohum

are some of the existing brands and

organized shopping areas in the city

of Guwahati.

An additional 600,000 sq.ft. of

retail property development has

been proposed for development in

Guwahati, most of it along G.S. Road.

JaBalpur

Jabalpur, with 1.2 million residents,

is one of the wealthier cities in the

state of Madhya Pradesh. It is the

headquarter of many important

Central and State departments which

employ thousands of government

workers. Jabalpur serves as a

distribution centre for a wide variety

of products and natural resources

from all over. Its relative prosperity

has caused it to be ranked third in the

state in terms of market potential andafuence.

Residents of Jabalpur, who have

relatively higher disposable incomes,

are limited to shopping at the

traditional markets of Soni Bazaar,

Madhital and Sadar Market. Treasure

Island (Jabalpur), a 680,000 sq.

ft. retail project, has added a new

dynamic to the local retail landscape.

nanDeD

Nanded, a religious hub to India’s

Sikh community, has one of most

prominent Gurudwaras in the country.

DeparTmenTal sTOres,supermarkeTs anDlarge OrmaT sTanD-alOne sTOres are mOsTpOpular reTaIl OrmaTsIn guwahaTI. wITh TheDevelOpmenT O shOppIngmalls anD plazas, BranDshave sTarTeD TO mIgraTerOm hIgh sTreeTs InTOmalls.

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 15/18

market intelligence

70 . images retail . OCtOBer 2011

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 16/18

market intelligence

72 . images retail . OCtOBer 2011

It draws more than 1 million tourists

annually and is the agricultural,

educational and healthcare hub of the

region.

As a trading and business centre fornearby towns and rural hinterland,

the city of Nanded has well-

established retail markets. Station

Road, Vazirabad, Shivaji Nagar and

Doctors Lane are the prominent retail

and commercial hubs of the city.

vIJayawaDa

Vijayawada, the third largest city

in Andhra Pradesh, is a hub of

commercial activity with a strong

educational infrastructure and ITindustrial base. Retail districts in

Vijayawada have traditionally been

concentrated along Shivalayam Street

and Samarangam Chowk, which form

the older part of the city. Alternative,

modern forms of retail business have

started appearing along Mahatma

Gandhi Road (erstwhile Bandar Road),

Besant Road and, to an extent, along

Karl Marx Road (erstwhile Eluru

Road). Vijayawada’s retail landscape

is expected to undergo furthertransformation as organized retail

projects are already under construction

along Mahatma Gandhi Road, Old

Bus Stand area and Gandhinagar, with

additional projects being proposed,

potentially propelling these areas to the

prime retail districts of the city.

eCOnOmIC aCTIvITy In

uJJaIn Is DrIven By The

agrICulTural InDusTryOr whICh The CITy

serves as a regIOnal

whOlesale markeT. The

CITy reCeIves a large

numBer O TOurIsTs

ThrOughOuT The year.

ThIs Is supplemenTeD By

amOus relIgIOus aIrs

ThaT Draw up TO hal a

mIllIOn pIlgrIms.

uJJaIn

As a city of great cultural and religious

importance, Ujjain receives a large

number of tourists throughout the

year. This is supplemented by famous

religious fairs that draw up to half a

million pilgrims. Economic activity

in Ujjain is driven by the agricultural

industry for which the city serves as a

regional wholesale market.Small, traditional shops dominate

the retail landscape in Ujjain. The

main market area of the city, adjacent

to Free Ganj Tower, is home to

domestic apparel brands such as Peter

England, John Players, Charlie Outlaw

and Raymond.

Gopal Mandir and Satigate are two

other prominent shopping districts

within the city.

Treasure Island (Ujjain), a 400,000

sq.ft. shopping mall on Dhanwantri

Chikisa Kendra, is a star attraction of

the city’s landscape.

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 17/18

market intelligence

74 . images retail . OCtOBer 2011

8/3/2019 Market Intelligence JLLM

http://slidepdf.com/reader/full/market-intelligence-jllm 18/18

market intelligence

The rIghT markeT maynOT Be The OBvIOus Or

sae ChOICe. prOperTyDevelOpers musT lOOkBeyOnD InDIa’s 7 largemeTrOs anD IDenTIylOCaTIOns wITh The rIghTmIx O markeT maTurITy,reTaIl mOmenTum anDspaCe aOrDaBle OrBranDs. unlIke The rIghTmarkeT, The rIghT prOJeCTIs maDe, nOT DIsCOvereD.

OuTlOOk

While the performance of economies around the world

will certainly have an impact on India’s retail sector, the

stable footing it is on as a result of strong underlyingfundamentals in demographics, urbanization and a growing

middle class should provide reason for optimism.

Success is far from guaranteed for retail property

developers, however. For them it is critical to take the

lessons learned from the recent downturn and go forward

with a cunning eye for the right market and the right

project.

The right market may not be the

obvious or safe choice. Property

developers must look beyond India’s

7 large metros and identify locations

with the right mix of market maturity,retail momentum and space affordable

for brands. Finding markets with

sufcient retail potential (purchasing

power) where a rst mover advantage

may yet be realized is a recipe that

has worked well for developers such

as Entertainment World Developers

and may be imitated by others going

forward.

Unlike the right market, the right

project is made, not discovered.

Operators of organized retail need to

be vigilant in containing costs in non-

metro cities by employing innovative

techniques to maximize FSI throughmixed-use projects and keeping a lid

on CAM charges. Tenant mix, an issue

with any shopping mall project, needs

to take into account local preferences

for value versus premium retailers

and brands that represent a good

combination of international, national

and local merchants. Modestly-sized

malls which are strategically located

within a city and compliment, rather

than compete with, existing high

streets are the most likely to achieve

long term prosperity for developers,

operators and retailers.

Recommended