Investor PresentationMarch 2019

2

Certain matters contained in this Presentation include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of theSecurities Exchange Act of 1934, as amended. We make these forward-looking statements in reliance on the safe harbor protections provided under the Private Securities LitigationReform Act of 1995.

All statements, other than statements of historical fact, included in this presentation including the prospects of our industry, our anticipated financial performance, our anticipated annual dividend growth rate, management's plans and objectives for future operations, planned capital expenditures, business prospects, outcome of regulatory proceedings, market conditions, and other matters, may constitute forward-looking statements. Although we believe that the expectations reflected in these forward-looking statements are reasonable, we cannot assure you that these expectations will prove to be correct. These forward-looking statements are subject to certain known and unknown risks and uncertainties, as well as assumptions that could cause actual results to differ materially from those reflected in these forward-looking statements. Factors that might cause actual results to differ include, but are not limited to, our ability to generate sufficient cash flow from operations to enable us to pay our debt obligations and our current and expected dividends or to fund our other liquidity needs; any sustained reduction in demand for, or supply of, the petroleum products we gather, transport, process, market and store; the effect of our debt level on our future financial and operating flexibility, including our ability to obtain additional capital on terms that are favorable to us; our ability to access the debt and equity markets, which will depend on general market conditions and the credit ratings for our debt obligations and equity; the loss of, or a material nonpayment or nonperformance by, any of our key customers; the amount of cash distributions, capital requirements and performance of our investments and joint ventures; the consequences of any divestitures of non-strategic operating assets or divestitures of interests in some of our operating assets through partnerships and/or join ventures; the failure to realize the anticipated benefits of our acquisition of Meritage Midstream ULC and its midstream infrastructure assets through our joint venture SemCAMS Midstream ULC; the amount of collateral required to be posted from time to time in our commodity purchase, sale or derivative transactions; the impact of operational and developmental hazards and unforeseen interruptions; our ability to obtain new sources of supply of petroleum products; competition from other midstream energy companies; our ability to comply with the covenants contained in our credit agreements, continuing covenant agreement, and the indentures governing our notes, including requirements under our credit agreements and continuing covenant agreement to maintain certain financial ratios; our ability to renew or replace expiring storage, transportation and related contracts; the overall forward markets for crude oil, natural gas and natural gas liquids; the possibility that the construction or acquisition of new assets may not result in the corresponding anticipated revenue increases; any future impairment of goodwill resulting from the loss of customers or business; changes in currency exchange rates; weather and other natural phenomena, including climate conditions; a cyber attack involving our information systems and related infrastructure, or that of our business associates; the risks and uncertainties of doing business outside of the U.S., including political and economic instability and changes in local governmental laws, regulations and policies; costs of, or changes in, laws and regulations and our failure to comply with new or existing laws or regulations, particularly with regard to taxes, safety and protection of the environment; the possibility that our hedging activities may result in losses or may have a negative impact on our financial results; general economic, market and business conditions; as well as other risk factors discussed from time to time in our each of our documents and reports filed with the SEC.

Readers are cautioned not to place undue reliance on any forward-looking statements contained in this press release, which reflect management’s opinions only as of the date hereof. Except as required by law, we undertake no obligation to revise or publicly release the results of any revision to any forward-looking statements.

We use our Investor Relations website and social media outlets as channels of distribution of material company information. Such information is routinely posted and accessible on our Investor Relations website at ir.semgroupcorp.com. We are present on Twitter and LinkedIn: SemGroup Twitter and LinkedIn

Forward-Looking Information

3

SemGroupTransformed Portfolio Provides Strategic Platform

2016 - 2018

Simplify | Transform

2019 & Beyond

Execute | Strengthen | Deliver

• Rolled up Rose Rock Midstream MLP

• Sold non-core assets

• Acquired Gulf Coast platform

• Announced Canadian growth projects

• Deployed strategies to optimize existing assets

• Improved quality of cash flows

• Focused efforts to strengthen balance sheet

• Complete key projects

• Successfully renew contracts

• Focus on cost savings

• Continue deleveraging efforts

• Capital efficient growth around existing platforms

• Focus on project returns

• Unlock synergies in Canada and connect MidCon to Gulf Coast

Completed In Focus

4

• Capture EBITDA growth from organic projects• Evaluate partner funding for new growth projects• Consider additional JVs and asset sales• Opportunistically seek other sources of cost-effective capital

Continue Deleveraging Efforts

• Expand SemCAMS Midstream JV Footprint• Montney liquids takeaway via proposed Montney-to-Market (M2M) Pipeline• Connect Mid-Con & Gulf Coast assets via proposed Gladiator Pipeline• Maximize export opportunities at HFOTCO to meet growing demand

• Expand Canadian system connectivity and capacity◦ Pipestone Pipeline, Patterson Creek Expansion, Smoke Lake Plant

• Conversion of White Cliffs pipe to NGL service• Increase HFOTCO connectivity via Moore Road pipeline

• Execute contract renewals across portfolio• Integrate Meritage and SemCAMS assets• Enhance HFOTCO pipeline connectivity

Capture Growth Opportunities

Complete Key Growth Projects

Commercialization &Asset Optimization

SemGroup 2019 Strategic Goals and PrioritiesBALANCE prudent capital management with CAPTURING strategic growth opportunities

5

SemCAMS Midstream Competitive Advantages

Experienced and reliable

operator

Stable cash flows supported by credit-worthy

customers

Irreplicable sour gas processing

andacid gas transfer

solution

Takeaway optionality

via pipeline, truck & rail

Facility interconnections

provideoperational flexibility & optimization

Asset footprint in prolific

Montney and Duvernay

plays

Montney and Duvernay Focused Midstream Company

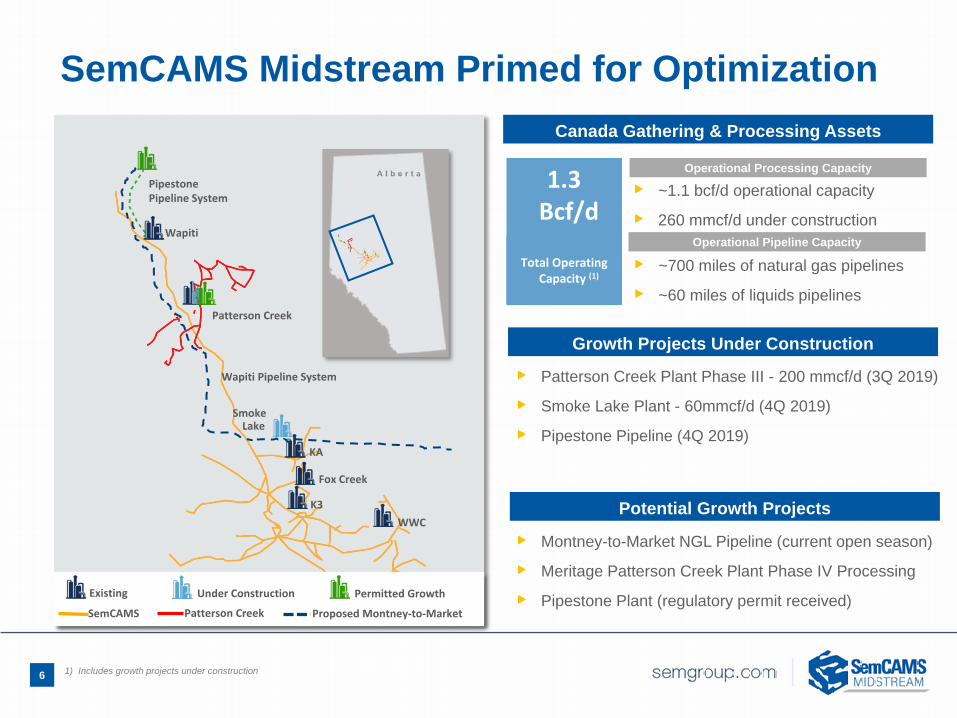

SemCAMS Midstream Primed for Optimization

1) Includes growth projects under construction

▶ ~1.1 bcf/d operational capacity

▶ 260 mmcf/d under construction

Growth Projects Under Construction

Canada Gathering & Processing Assets

1.3 Bcf/d

Total Operating Capacity (1)

Potential Growth Projects

Operational Processing Capacity

Operational Pipeline Capacity

▶ ~700 miles of natural gas pipelines

▶ ~60 miles of liquids pipelines

▶ Patterson Creek Plant Phase III - 200 mmcf/d (3Q 2019)

▶ Smoke Lake Plant - 60mmcf/d (4Q 2019)

▶ Pipestone Pipeline (4Q 2019)

▶ Montney-to-Market NGL Pipeline (current open season)

▶ Meritage Patterson Creek Plant Phase IV Processing

▶ Pipestone Plant (regulatory permit received)

Wapiti

PipestonePipeline System

Patterson Creek

Smoke Lake

KA

Fox Creek

K3WWC

Wapiti Pipeline System

Existing Under Construction

Patterson CreekSemCAMS

Permitted Growth

Proposed Montney-to-Market

6

▶ Assets located in prolific liquids-rich Montney play

• Situated in the Gold Creek and Karr regions

• Basin is top quartile with highly competitive well economics

• Producer IRR’s ~30% - 50% on C$50 Ed Par oil / C$2 AECO

• Significant stacked resource potential

▶ Acreage Dedication & MVCs provide cash flow stability

• 400,000 acres dedicated

• MVCs constitute ~31% of 2018E revenue

▶ Existing 195 mmcf/d processing capacity to double

• Phase III Expansion under construction (estimated completion 3Q 2019)

• Expansion adds 200 mmcf/d capacity

▶ Producer development plans to support future growth

▶ Service offerings continue to expand as producers accelerate development

• Emulsion handling / central delivery batteries business rapidly growing in Western Canada

▶ Largest producers are private equity sponsored E&P’s highly incentivized to continue delineation of acreage and enhance value

Patterson Creek Overview Patterson Creek Footprint

Patterson Creek OverviewGas Processing Capacity

Existing: 195 mmcf/dUnder Construction: 200 mmcf/d ~3Q 2019

Miles of Pipelines

101 miles of gas gathering pipelines; 38 miles of oil gathering pipelines; 18 miles of emulsion and gas lift pipelines

InterconnectsResidue Gas: TCPL and AllianceRaw Gas: CNRLLiquids: Pembina Peace Pipeline

Recently Acquired Patterson Creek System

Patterson Creek Assets

7

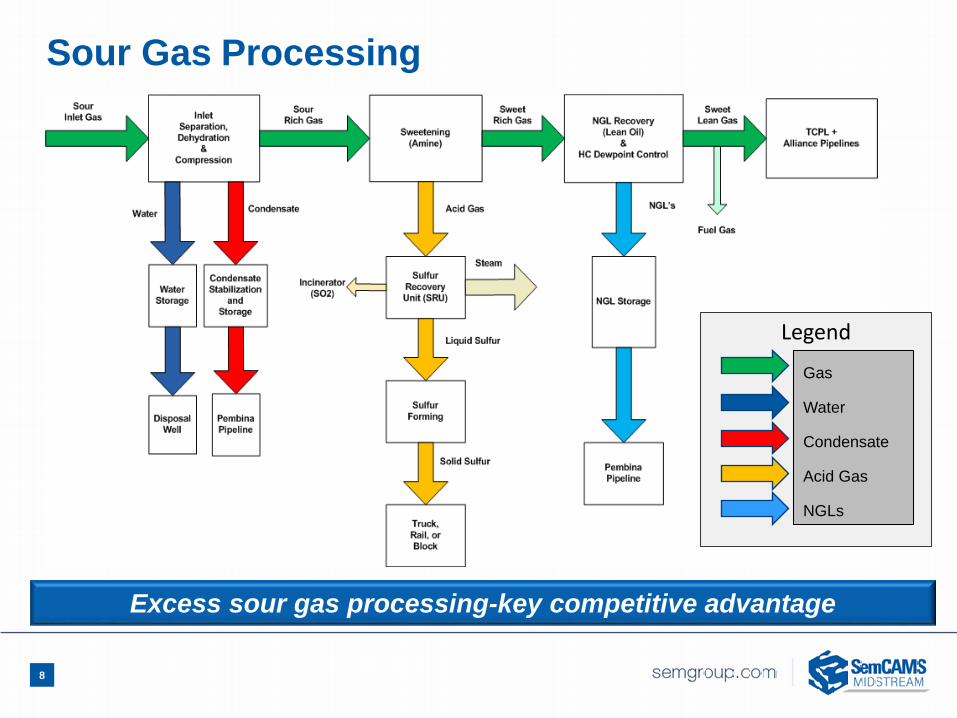

Legend

Sour Gas Processing

Gas

Water

Condensate

Acid Gas

NGLs

Excess sour gas processing-key competitive advantage

8

99% 97% 99% 100%92%

97% 95%100% 100%

96%100% 99%

0%10%20%30%40%50%60%70%80%90%

100%

2007

T

2008

2009

T

2010

2011

2012

T

2013

T

2014

2015

2016

2017

T

2018

T YT

D

1) Includes KA and K3 plants; excludes planned outages (plant turnarounds)2) SemCAMS volumes include total processed volumes - K3, KA and West Fox Creek facilities3) Scheduled plant turnaround at KA4) Scheduled plant turnaround at K3

SemCAMS Midstream PerformancePlant Reliability (1) Average Processing Volume (2) (mmcf/d)

(4)

Customers

(3)

T = Turnaround Years

Historical reliability of >98%, excluding planned outages

9

Canadian Condensate Market Overview

Source: RBC Capital Markets, Government Data

“Western Canada willlikely remain shortcondensate for theforeseeable futuresupporting itspremium vs. Edmonton condensate and rough parity withWTI (C$)” - RBC

Oil sands diluent demand, combined with short fall in local condensate supply will continue to drive production growth

“Condensate demandin western Canada isexpected to outstripdomestic supply, withimports bridging the gap and rail playinga bigger role.” - RBC

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.820

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

1420

1520

1620

1720

1820

1920

2020

21

MM

Bpd

Forecast

CondensateDemand

ImpliedCondensate

Imports

CondensateProduction

Premium Condensate Market Supply and Demand

10

2017 Demand Forecast (Current)2016 Demand Forecast

2017 Supply Forecast (Current)2016 Supply Forecast

96

32 30 2211 17 18 11 12 8 8 8 10 5 7 5 5

15

61

19 1720

23 7 310 3 6 4 4 1

5 1

16

0

20

40

60

80

100

120

140

160

180

2017 2018 YTD

▶ Montney production continues to grow, deep inventory of potential new build infrastructure projects across the fairway

▶ SemCAMS’ liquids processing and sour plant experience are clear competitive advantages as Montney operators continue to be focused on liquids-rich opportunities

▶ Producers have increasingly encountered sour gas in new emerging areas

11

Montney, Significant Development Potential

Cenovus Pipestone Montney acreage recently acquired by NuVista

Wapiti Pipestone Montney Mineral Rights

Source: GeoScout

2017–18 Wapiti/Montney Drilling Activity by Producer

SemCAMS Montney Customers

▶ SemCAMS’ existing area infrastructure, technical expertise, and operational track record are competitive advantages as operators look for long-term gathering and processing solutions

▶ Operators are increasingly encountering sour production in the Duvernay and estimate that as much as 25% of Duvernay could be sour

▶ Major Duvernay producers in the Kaybob area continue to flow sour production to our KA facility

▶ Smoke Lake plant under construction located north of KA to process incremental sour gas production

Footprint in the Core of the Duvernay

26

Duvernay Mineral Rights

Source: GeoScout.

2017–18 Duvernay Drilling Activity by Producer

32

16 156

44

8

15

17 17

10

22

15 1

0

10

20

30

40

50

60

70

Chevron Encana Murphy Paramount Shell XTO Energy Other

2017 2018 YTD

12

2019 Operational Guidance AssumptionsGuidance Capacity Notes

Canada: SemCAMS Midstream JVK3, KA & West Fox Creek Plants (mmcf/d) 390 - 410 695 Legacy volumes

Wapiti Plant (mmcf/d) (3) 100 - 110 200 Volumes ramp - Exit 4Q19 >150 mmcf/d

Smoke Lake Plant (mmcf/d) 25 60 First volumes Nov 2019 at ~25 mmcf/d

Patterson Creek Plant (mmcf/d) 140 - 150 195 Volumes ramp - Exit 4Q19 ~160 mmcf/d; capacity 395 mmcf/d

Key Growth Projects Expected Completion

Estimated 2019 Capex Total Spend (1) EBITDA Multiple (2)

Canada: SemCAMS Midstream JVWapiti Plant (3) In service Jan 2019 $46 $250 ~7x

Patterson Creek Plant Phase III 3Q 2019 $100 $210 (4) ~5-8x

Smoke Lake Plant 4Q 2019 $30 $50 ~6x

Pipestone Pipeline 4Q 2019 $24 $40 ~7x

1) Total project spend reflects 100% basis for SemCAMS Midstream JV 2) Assumes developed multiple target3) Wapiti plant volumes ramp through 2020, estimated utilization of 75% by year-end 2019 and full capacity by mid-year 20204) Includes USD $110 million of 2018 capex spent prior to close

2019 Operational Guidance & Key Growth Projects

13

$/USD

Recommended