4-1

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Management Accounting Lecture 10 (Chapter 4)

Systems Design: Process Costing

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Todays’ Lecture

n System Design – Process Costing

n Review of Process Costing versus Job-Order Costing

n When should Process Costing be Used?

n How is it Used?

n Journal entries

n Calculating balances by the Weighted Average Cost method

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Product Costing

n Product Costing is the mapping and allocating of costs to a specific product

n Its purpose is to provide executives with critical information including: n How to minimize costs n How to price a product competitively and profitably

n There are two main methodologies of Product Costing 1. Job-Order Costing – each job is different 2. Process Costing – many of the same products

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Job Order Costing

n Job-Order Costing is the costing methodology applied in companies in the following circumstances: n Produce many different products or packages n Manufacture to order so each job is different

n Examples would be: n SNC (engineering and construction) n Airbus (aircraft) n Other?

n In these cases, a company needs to know, often on an order by order basis, what are the costs associated with fulfilling the order

n Cost records for each job will be required to support decision making and billing of the customer

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Process Costing

n Process Costing is the costing methodology applied in companies in the following circumstances: n Produce many units of a single product n Each unit is substantially similar to other units

n Examples would be: n Lenovo (PC manufacturing) n Frito lay (Snacks and beverages) n Others?

n That each of these products are substantially the same, managers are able to apply the same average cost to each unit

n Cost records for each job will be required to support decision making and billing of the customer

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Similarities & Differences Between Job-Order and Process Costing

n Similarities n Both are Product Costing systems assigning material, labour

and overhead to products n Both systems use the same manufacturing accounts n The flow of costs are very similar in both systems

n Differences n Process Costing is used for single products which run

continuously (versus differing products/packages) n Process Costing tracks cost by department (versus by job) n Tracks unit cost by department (versus by job sheet)

4-2

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

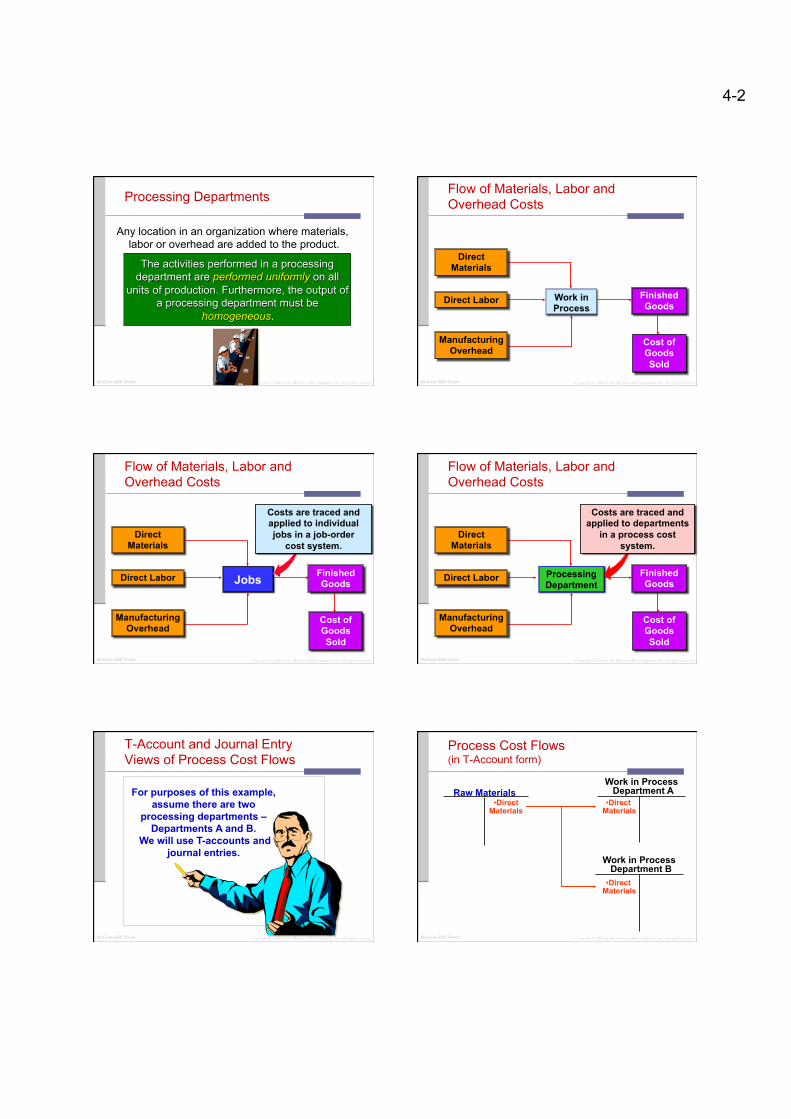

Processing Departments

Any location in an organization where materials, labor or overhead are added to the product.

The activities performed in a processing department are performed uniformly on all

units of production. Furthermore, the output of a processing department must be

homogeneous.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Finished Goods

Cost of Goods Sold

Work in Process

Direct Materials

Direct Labor

ManufacturingOverhead

Flow of Materials, Labor and Overhead Costs

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Finished Goods

Cost of Goods Sold

Direct Labor

ManufacturingOverhead

Jobs

Costs are traced and applied to individual jobs in a job-order

cost system. Direct

Materials

Flow of Materials, Labor and Overhead Costs

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Finished Goods

Cost of Goods Sold

Direct Labor

ManufacturingOverhead

Processing Department

Costs are traced and applied to departments

in a process cost system.

Direct Materials

Flow of Materials, Labor and Overhead Costs

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

For purposes of this example, assume there are two

processing departments – Departments A and B.

We will use T-accounts and journal entries.

T-Account and Journal Entry Views of Process Cost Flows

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Raw Materials

Work in Process Department B

Work in Process Department A

• Direct Materials

• Direct Materials

• Direct Materials

Process Cost Flows (in T-Account form)

4-3

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

GENERAL JOURNAL Page 4

Date DescriptionPost. Ref. Debit Credit

Work in Process - Department A XXXXXWork in Process - Department B XXXXX

Raw Materials XXXXXTo record the use of direct material.

Process Cost Flows (in journal entry form)

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Work in Process Department B

Work in Process Department A Salaries and

Wages Payable

• Direct Materials

• Direct Materials

• Direct Labor

• Direct Labor • Direct

Labor

Process Cost Flows (in T-Account form)

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

GENERAL JOURNAL Page 4

Date DescriptionPost. Ref. Debit Credit

Work in Process - Department A XXXXXWork in Process - Department B XXXXX

Salaries and Wages Payable XXXXXTo record direct labor costs.

Process Cost Flows (in journal entry form)

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Work in Process Department B

Work in Process Department A

Manufacturing Overhead

• Overhead Applied to

Work in Process

• Applied Overhead

• Applied Overhead

• Direct Labor

• Direct Materials

• Direct Labor

• Direct Materials

• Actual Overhead

Process Cost Flows (in T-Account form)

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

GENERAL JOURNAL Page 4

Date DescriptionPost. Ref. Debit Credit

Work in Process - Department A XXXXXWork in Process - Department B XXXXX

Manufacturing Overhead XXXXXTo apply overhead to departments.

Process Cost Flows (in journal entry form)

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Work in Process Department B

Work in Process Department A

• Direct Materials

• Direct Labor

• Applied Overhead

• Direct Materials

• Direct Labor

• Applied Overhead

Transferred to Dept. B

• Transferred from Dept. A

Process Cost Flows (in T-Account form)

4-4

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

GENERAL JOURNAL Page 4

Date DescriptionPost. Ref. Debit Credit

Work in Process - Department B XXXXXWork in Process - Department A XXXXX

To record the transfer of goods fromDepartment A to Department B.

Process Cost Flows (in journal entry form)

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Finished Goods Work in Process Department B

• Cost of Goods

Manufactured

• Direct Materials

• Direct Labor

• Applied Overhead

• Transferred from Dept. A

• Cost of Goods

Manufactured

Process Cost Flows (in T-Account form)

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

GENERAL JOURNAL Page 4

Date DescriptionPost. Ref. Debit Credit

Finished Goods XXXXXWork in Process - Department B XXXXX

To record the completion of goodsand their transfer from Department Bto finished goods inventory.

Process Cost Flows (in journal entry form)

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Finished Goods

Cost of Goods Sold

Work in Process Department B

• Cost of Goods

Manufactured

• Direct Materials

• Direct Labor

• Applied Overhead

• Transferred from Dept. A

• Cost of Goods

Sold

• Cost of Goods

Sold

• Cost of Goods

Manufactured

Process Cost Flows (in T-Account form)

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

GENERAL JOURNAL Page 4

Date DescriptionPost. Ref. Debit Credit

Cost of Goods Sold XXXXXFinished Goods XXXXX

To record cost of goods sold.

Process Cost Flows (in journal entry form)

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Equivalent Units of Production

Equivalent units are the product of the number of partially completed units and the percentage

of completion of those units.

We need to calculate equivalent units because a department usually has some partially completed

units in its beginning and ending inventory.

4-5

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Two half completed products are equivalent to one completed product.

So, 10,000 units 70% complete are equivalent to 7,000 complete units.

+ = 1

Equivalent Units – The Basic Idea

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Calculating Equivalent Units

Equivalent units can be calculated two ways:

�The First-In, First-Out Method – FIFO is covered in the appendix to this chapter.

�The Weighted-Average Method – This method will be covered in the main portion of the chapter.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

The weighted-average method . . . • Makes no distinction between work done in prior or current periods. • Blends together units and costs from prior and current periods.

Characteristics of the Weighted Average Method

The equivalent units of production for a department are the number of units transferred to the next department (or finished goods) plus the equivalent units in the department’s ending

work in process inventory. McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Direct labor costs may be small

in comparison to other product

costs in process costing systems.

Direct Materials

Type of Product Cost

Dol

lar A

mou

nt

Direct Labor

Conversion

Treatment of Direct Labor

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Type of Product Cost

Dol

lar A

mou

nt Conversion

Direct labor and manufacturing overhead may be combined into one product cost called conversion.

Direct Materials

Treatment of Direct Labor

Direct labor costs may be small

in comparison to other product

costs in process costing systems.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Weighted-Average Example

Percent CompletedShaping and Milling Department Units Materials ConversionBeginning work in process 200 55% 30%

Units started into production in May 5,000

Units completed during May and 4,800 100% 100% transferred to the next department

Ending working process 400 40% 25%

Double Diamond Skis reported the following activity in Shaping and Milling Department

for the month of May:

4-6

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Weighted-Average Example

The first step in calculating the equivalent units is to identify the units completed and transferred

out of the Department in May (4,800 units).

Materials Conversion

Units completed and transferred to the next department 4,800 4,800

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Weighted-Average Example

Materials Conversion

Units completed and transferred to the next department 4,800 4,800 Work in process, June 30:

400 units × 40% 160

Equivalent units of Production in during the month of May 4,960

The second step is to identify the equivalent units of production in ending work in process with respect to

materials for the month (160 units) and add this to the 4,800 units from step one.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Weighted-Average Example

Materials Conversion

Units completed and transferred to the next department 4,800 4,800 Work in process, June 30:

400 units × 40% 160 400 units × 25% 100

Equivalent units of Production in during the month of May 4,960 4,900

The third step is to identify the equivalent units of production in ending work in process with respect to conversion for the month (100 units) and add this to

the 4,800 units from step one.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Weighted-Average Example

Equivalent units of production always equals: Units completed and transferred + Equivalent units remaining in work in process

Materials Conversion

Units completed and transferred to the next department 4,800 4,800 Work in process, June 30:

400 units × 40% 160 400 units × 25% 100

Equivalent units of Production in during the month of May 4,960 4,900

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Weighted-Average Example

Beginning Work in Process

200 Units 55% Complete

Ending Work in Process

400 Units 40% Complete

5,000 Units Started

4,800 Units Started and Completed

Materials

4,800 Units Completed 160 Equivalent Units 400 × 40%

4,960 Equivalent units of production

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

5,000 Units Started

4,800 Units Completed

4,800 Units Started and Completed

100 Equivalent Units 400 × 25%

4,900 Equivalent units of production

Beginning Work in Process

200 Units 30% Complete

Ending Work in Process

400 Units 25% Complete

Conversion

Weighted-Average Example

4-7

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

The following table includes some additional facts for Double Diamond Skis’ Shaping and Milling Department for May.

Computing Cost Per Equivalent Unit

Beginning work in process: 200 units

Materials: 55% complete $ 9,600 Conversion: 30% complete 5,575

Production started during May 5,000 units Production completed during May 4,800 units Costs added to production in May

Materials cost $ 368,600 Conversion cost 350,900

Ending work in process 400 units Materials: 40% complete Conversion: 25% complete

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Compute and Apply Costs

The formula for computing the cost per equivalent unit is :

Cost per equivalent

unit =

Cost of beginning work in process

inventory Cost added during

the period

Equivalent units of production

+

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Compute and Apply Costs

TotalCost Materials Conversion

Cost to be accounted for: Work in process, May 1 15,175$ 9,600$ 5,575$ Costs added in the Shipping and Milling Department 719,500 368,600 350,900 Total cost 734,675$ 378,200$ 356,475$

Equivalent units 4,960 4,900 Cost per equivalent unit

Here is a schedule with the cost and equivalent unit information.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

TotalCost Materials Conversion

Cost to be accounted for: Work in process, May 1 15,175$ 9,600$ 5,575$ Costs added in the Shipping and Milling Department 719,500 368,600 350,900 Total cost 734,675$ 378,200$ 356,475$

Equivalent units 4,960 4,900 Cost per equivalent unit 76.25$ 72.75$ Total cost per equivalent unit = $76.25 + $72.75 = $149.00

Compute and Apply Costs

$378,200 ÷ 4,960 units = $76.25

Here is a schedule with the cost and equivalent unit information.

$356,475 ÷ 4,900 units = $72.75

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Computing the Cost of Ending Work in Process Inventory

Materials Conversion TotalEnding work in process inventory: Equivalent units of production 160 100

Cost of ending work in process inventory -$ -$ -$

Units completed and transferred out: Units transferred to the next department 4,800 4,800 Cost per equivalent unit 76.25$ 72.75$ Cost of units transferred out 366,000$ 349,200$ 715,200$

Shaping and Milling DepartmentCost of Ending Work in Process Inventory and the Units Transferred Out

Step 1: Record the equivalent units of production in ending work in process inventory.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Materials Conversion TotalEnding work in process inventory: Equivalent units of production 160 100 Cost per equivalent unit 76.25$ 72.75$ Cost of ending work in process inventory 12,200$ 7,275$ 19,475$

Units completed and transferred out: Units transferred to the next department 4,800 4,800 Cost per equivalent unit 76.25$ 72.75$ Cost of units transferred out 366,000$ 349,200$ 715,200$

Shaping and Milling DepartmentCost of Ending Work in Process Inventory and the Units Transferred Out

Computing the Cost of Ending Work in Process Inventory

Step 2: Record the cost per equivalent unit.

4-8

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Materials Conversion TotalEnding work in process inventory: Equivalent units of production 160 100 Cost per equivalent unit 76.25$ 72.75$ Cost of ending work in process inventory 12,200$ 7,275$ 19,475$

Units completed and transferred out: Units transferred to the next department 4,800 4,800 Cost per equivalent unit 76.25$ 72.75$ Cost of units transferred out 366,000$ 349,200$ 715,200$

Shaping and Milling DepartmentCost of Ending Work in Process Inventory and the Units Transferred Out

Computing the Cost of Ending Work in Process Inventory

Step 3: Compute the cost of ending work in process inventory.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Computing the Cost of Units Transferred Out

Materials Conversion TotalEnding work in process inventory: Equivalent units of production 160 100 Cost per equivalent unit 76.25$ 72.75$ Cost of ending work in process inventory 12,200$ 7,275$ 19,475$

Units completed and transferred out: Units transferred to the next department 4,800 4,800 Cost per equivalent unit 76.25$ 72.75$ Cost of units transferred out 366,000$ 349,200$ 715,200$

Shaping and Milling DepartmentCost of Ending Work in Porcess Inventory and the Units Transferred Out

Step 1: Record the units transferred out to the next department.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Materials Conversion TotalEnding work in process inventory: Equivalent units of production 160 100 Cost per equivalent unit 76.25$ 72.75$ Cost of ending work in process inventory 12,200$ 7,275$ 19,475$

Units completed and transferred out: Units transferred to the next department 4,800 4,800 Cost per equivalent unit 76.25$ 72.75$ Cost of units transferred out 366,000$ 349,200$ 715,200$

Shaping and Milling DepartmentCost of Ending Work in Porcess Inventory and the Units Transferred Out

Computing the Cost of Units Transferred Out

Step 2: Record the cost per equivalent unit.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Materials Conversion TotalEnding work in process inventory: Equivalent units of production 160 100 Cost per equivalent unit 76.25$ 72.75$ Cost of ending work in process inventory 12,200$ 7,275$ 19,475$

Units completed and transferred out: Units transferred to the next department 4,800 4,800 Cost per equivalent unit 76.25$ 72.75$ Cost of units transferred out 366,000$ 349,200$ 715,200$

Shaping and Milling DepartmentCost of Ending Work in Process Inventory and the Units Transferred Out

Computing the Cost of Units Transferred Out

Step 3: Compute the cost of units transferred out.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Reconciling Costs

Step 1: Compute the costs to be accounted for by adding the cost of beginning work in process and the production costs added in May.

Costs to be accounted for: Cost of beginning work in process inventory 15,175$ Costs added to production during the period 719,500 Total cost to be accounted for 734,675$

Shaping and Milling DepartmentCost Reconciliation

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Costs to be accounted for: Cost of beginning work in process inventory 15,175$ Costs added to production during the period 719,500 Total cost to be accounted for 734,675$

Cost accounted for as follows: Cost of ending work in process inventory 19,475$ Cost of units transferred out 715,200 Total cost accounted for 734,675$

Shaping and Milling DepartmentCost Reconciliation

Reconciling Costs

Step 2: Compute the costs to accounted for by adding the cost of ending work in process and the cost of units transferred out in May.

4-9

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

FIFO vs. Weighted-Average Method

The FIFO method (generally considered more accurate than the weighted-average method) differs

from the weighted-average method in two ways:

1. The computation of equivalent units.

2. The way in which the costs of beginning inventory are treated.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

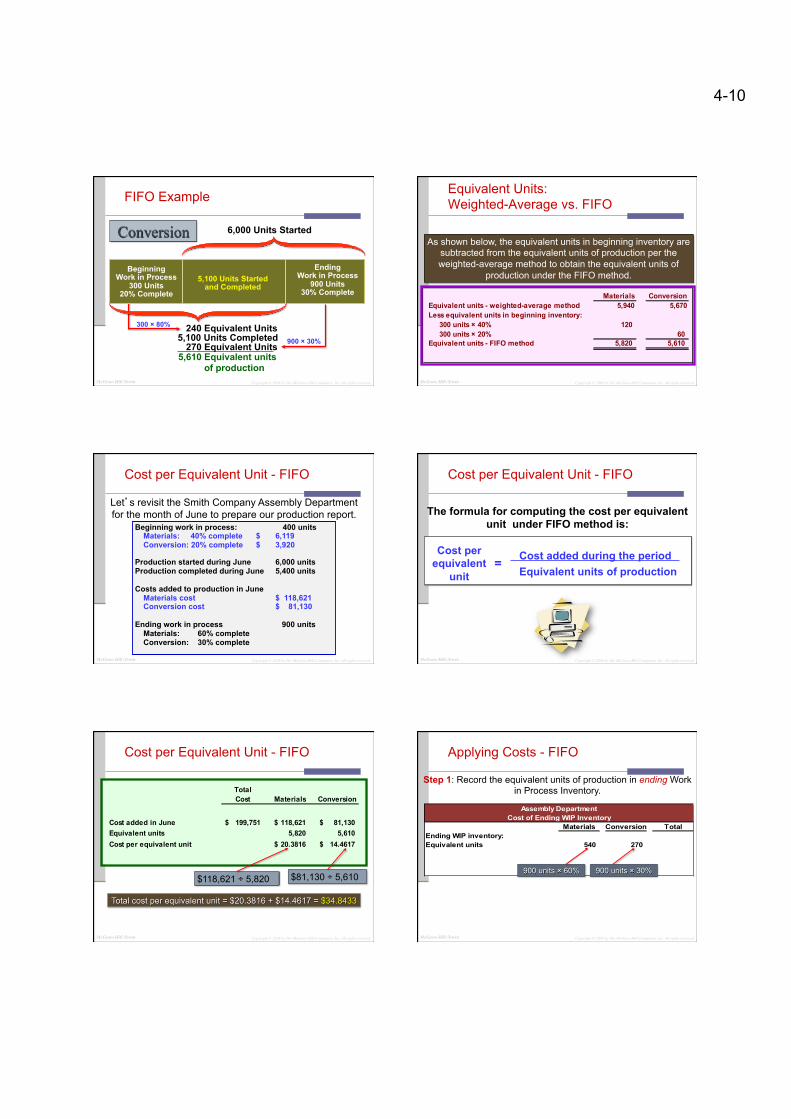

Equivalent Units – FIFO Method

Let’s revisit the Smith Company example. Here is information concerning the Assembly Department

for the month of June.

Percent CompletedUnits Materials Conversion

Work in process, June 1 300 40% 20%

Units started into production in June 6,000

Units completed and transferred out 5,400 of Department A during June

Work in process, June 30 900 60% 30%

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Equivalent Units – FIFO Method

Step 1: Determine equivalent units needed to complete beginning Work in Process Inventory.

Materials Conversion

To complete beginning Work in Process: Materials: 300 units × (100% - 40%) 180 Conversion: 300 units × (100% - 20%) 240

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Equivalent Units – FIFO Method

Step 2: Determine units started and completed during the period.

Materials Conversion

To complete beginning Work in Process: Materials: 300 units × (100% - 40%) 180 Conversion: 300 units × (100% - 20%) 240

Units started and completed during June 5,100 5,100

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Equivalent Units – FIFO Method

Step 3: Add the equivalent units in ending Work in Process Inventory.

Materials Conversion

To complete beginning Work in Process: Materials: 300 units × (100% - 40%) 180 Conversion: 300 units × (100% - 20%) 240

Units started and completed during June 5,100 5,100 Ending Work in Process Materials: 900 units × 60% complete 540 Conversion: 900 units × 30% complete 270

Equivalent units of production 5,820 5,610

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Beginning Work in Process

300 Units 40% Complete

Ending Work in Process

900 Units 60% Complete

6,000 Units Started

5,100 Units Started and Completed

FIFO Example

Materials

900 × 60% 5,100 Units Completed 540 Equivalent Units 5,820 Equivalent units of production

180 Equivalent Units 300 × 60%

4-10

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Beginning Work in Process

300 Units 20% Complete

Ending Work in Process

900 Units 30% Complete

6,000 Units Started

5,100 Units Started and Completed

FIFO Example

Conversion

5,100 Units Completed 270 Equivalent Units 900 × 30%

5,610 Equivalent units of production

240 Equivalent Units 300 × 80%

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Equivalent Units: Weighted-Average vs. FIFO

Materials ConversionEquivalent units - weighted-average method 5,940 5,670Less equivalent units in beginning inventory: 300 units × 40% 120 300 units × 20% 60 Equivalent units - FIFO method 5,820 5,610

As shown below, the equivalent units in beginning inventory are subtracted from the equivalent units of production per the weighted-average method to obtain the equivalent units of

production under the FIFO method.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Beginning work in process: 400 units Materials: 40% complete $ 6,119 Conversion: 20% complete $ 3,920

Production started during June 6,000 units Production completed during June 5,400 units Costs added to production in June

Materials cost $ 118,621 Conversion cost $ 81,130

Ending work in process 900 units Materials: 60% complete Conversion: 30% complete

Cost per Equivalent Unit - FIFO

Let’s revisit the Smith Company Assembly Department for the month of June to prepare our production report.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Cost per Equivalent Unit - FIFO

The formula for computing the cost per equivalent unit under FIFO method is:

Cost per equivalent

unit = Cost added during the period

Equivalent units of production

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Cost per Equivalent Unit - FIFO

TotalCost Materials Conversion

Cost added in June 199,751$ 118,621$ 81,130$ Equivalent units 5,820 5,610 Cost per equivalent unit 20.3816$ 14.4617$

Total cost per equivalent unit = $20.3816 + $14.4617 = $34.8433

$118,621 ÷ 5,820 $81,130 ÷ 5,610

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Materials Conversion TotalEnding WIP inventory:Equivalent units 540 270

Assembly DepartmentCost of Ending WIP Inventory

Applying Costs - FIFO

Step 1: Record the equivalent units of production in ending Work in Process Inventory.

900 units × 60% 900 units × 30%

4-11

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Applying Costs - FIFO

Step 2: Record the cost per equivalent unit.

Materials Conversion TotalEnding WIP inventory:Equivalent units 540 270 Cost per equivalent unit 20.3816$ 14.4617$

Assembly DepartmentCost of Ending WIP Inventory

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Materials Conversion TotalEnding WIP inventory:Equivalent units 540 270 Cost per equivalent unit 20.3816$ 14.4617$ Cost of Ending WIP inventory 11,006$ 3,905$ 14,911$

Assembly DepartmentCost of Ending WIP Inventory

Applying Costs - FIFO

Step 3: Compute the cost of ending Work in Process Inventory.

540 × $20.3816 270 × $14.4617

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Cost of Units Transferred Out

Step 1: Record the cost in beginning Work in Process Inventory.

Materials Conversion TotalCost of Units Transferred Out: Cost in beginning WIP inventory 6,119$ 3,920$ 10,039$ Cost to complete beginning WIP Equivalent units to complete 180 240 Cost per equivalent unit 20.3816$ 14.4617$ Cost to complete beginning WIP 3,669$ 3,471$ 7,140 Cost of units started and completed: Units started and completed 5,100 5,100 Cost per equivalent unit 20.3816$ 14.4617$ Cost of units started and completed 103,946$ 73,755$ 177,701 Cost of Units Transferred Out 194,880$

Assembly DepartmentCost of Units Transferred Out in June

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Cost of Units Transferred Out

Step 2: Compute the cost to complete the units in beginning Work in Process Inventory.

Materials Conversion TotalCost of Units Transferred Out: Cost in beginning WIP inventory 6,119$ 3,920$ 10,039$ Cost to complete beginning WIP Equivalent units to complete 180 240 Cost per equivalent unit 20.3816$ 14.4617$ Cost to complete beginning WIP 3,669$ 3,471$ 7,140 Cost of units started and completed: Units started and completed 5,100 5,100 Cost per equivalent unit 20.3816$ 14.4617$ Cost of units started and completed 103,946$ 73,755$ 177,701 Cost of Units Transferred Out 194,880$

Assembly DepartmentCost of Units Transferred Out in June

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Cost of Units Transferred Out

Step 3: Compute the cost of units started and completed this period.

Materials Conversion TotalCost of Units Transferred Out: Cost in beginning WIP inventory 6,119$ 3,920$ 10,039$ Cost to complete beginning WIP Equivalent units to complete 180 240 Cost per equivalent unit 20.3816$ 14.4617$ Cost to complete beginning WIP 3,669$ 3,471$ 7,140 Cost of units started and completed: Units started and completed 5,100 5,100 Cost per equivalent unit 20.3816$ 14.4617$ Cost of units started and completed 103,946$ 73,755$ 177,701 Cost of Units Transferred Out 194,880$

Assembly DepartmentCost of Units Transferred Out in June

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Cost of Units Transferred Out

Step 4: Compute the total cost of units transferred out.

Materials Conversion TotalCost of Units Transferred Out: Cost in beginning WIP inventory 6,119$ 3,920$ 10,039$ Cost to complete beginning WIP Equivalent units to complete 180 240 Cost per equivalent unit 20.3816$ 14.4617$ Cost to complete beginning WIP 3,669$ 3,471$ 7,140 Cost of units started and completed: Units started and completed 5,100 5,100 Cost per equivalent unit 20.3816$ 14.4617$ Cost of units started and completed 103,946$ 73,755$ 177,701 Cost of Units Transferred Out 194,880$

Assembly DepartmentCost of Units Transferred Out in June

4-12

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Reconciling Costs

Costs to be accounted for: Cost of beginning Work in Process Inventory 10,039$ Costs added to production during the period 199,751 Total cost to be accounted for 209,790$

Cost accounted for as follows: Cost of ending Work in Process Inventory 14,911$ Cost of units transferred out 194,880 Total cost accounted for* 209,791$

Assembly DepartmentCost Reconciliation for June

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Reconciling Costs

Costs to be accounted for: Cost of beginning Work in Process Inventory 10,039$ Costs added to production during the period 199,751 Total cost to be accounted for 209,790$

Cost accounted for as follows: Cost of ending Work in Process Inventory 14,911$ Cost of units transferred out 194,880 Total cost accounted for* 209,791$

Assembly DepartmentCost Reconciliation for June

* $1 rounding error.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

A Comparison of Costing Methods

In a lean production environment, FIFO and weighted-average methods yield similar

unit costs.

When considering cost control, FIFO is superior to weighted-average because it

does not mix costs of the current period with costs of the prior period.

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Review

n System Design – Process Costing – FIFO Inventory Method

n What is FIFO?

n FIFO versus Average Cost method

n When should FIFO be used?

n Journal entries

n Calculating balances by the FIFO Cost method

McGraw-Hill /Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Tutorial

n Review of today’s lecture n Review Problem

n 4-2 n 4-5

Recommended