LNG in JapanLNG in JapanChallenges of Tokyo Gas Challenges of Tokyo Gas

in the Current Turbulent Marketin the Current Turbulent Market

2

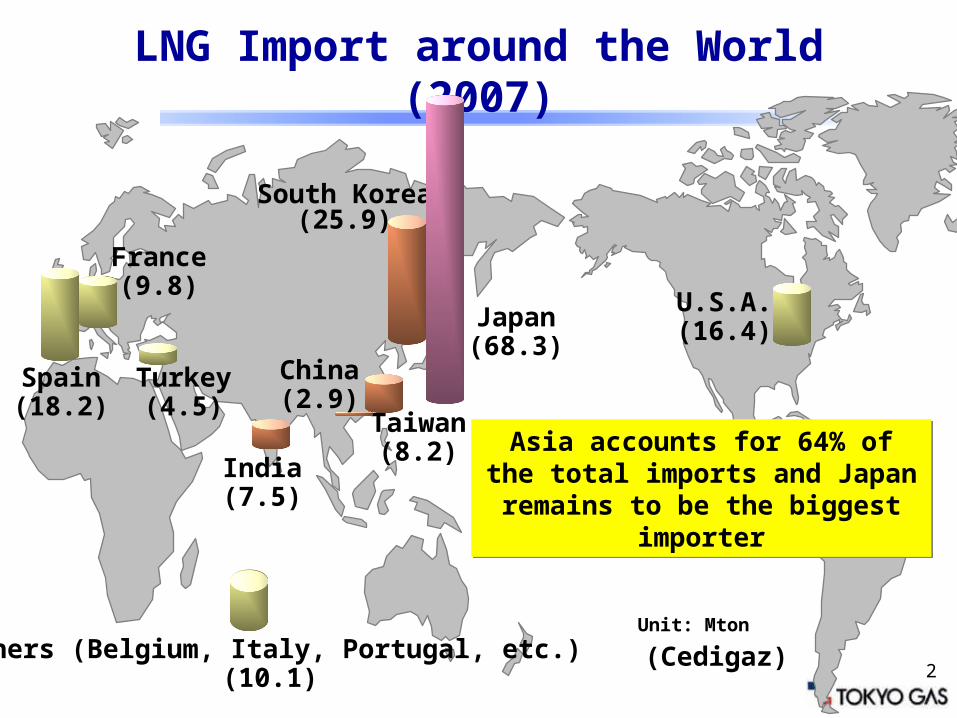

LNG Import around the World (2007)

South Korea(25.9)

Taiwan(8.2)

India(7.5)

U.S.A.(16.4)

Spain(18.2)

France(9.8)

Turkey(4.5)

Others (Belgium, Italy, Portugal, etc.)(10.1)

(Cedigaz)Unit: Mton

China(2.9)

Asia accounts for 64% of the total imports and Japan remains to be

the biggest importer

Asia accounts for 64% of the total imports and Japan remains to be

the biggest importer

Japan(68.3)

3

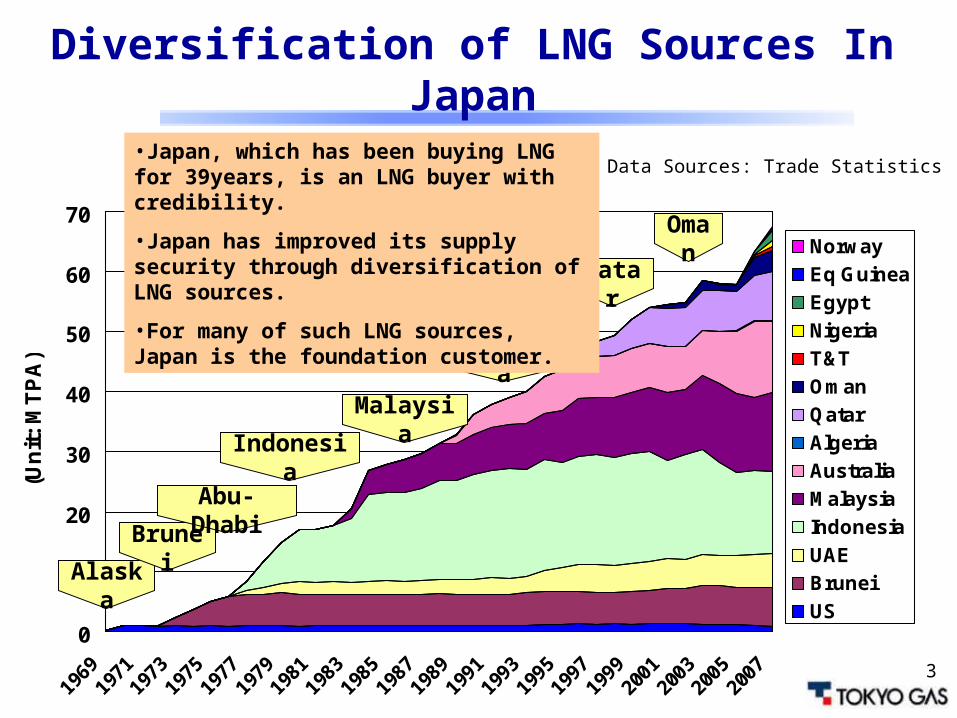

Diversification of LNG Sources In Japan

0

10

20

30

40

50

60

70

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

(Un

it:

MT

PA

)

Norway

Eq Guinea

Egypt

Nigeria

T&T

Oman

Qatar

Algeria

Australia

Malaysia

Indonesia

UAE

Brunei

US

Alaska

Brunei

Abu-Dhabi

Indonesia

Malaysia

Australia

Oman

Data Sources: Trade Statistics

Qatar

•Japan, which has been buying LNG for 39years, is an LNG buyer with credibility.

•Japan has improved its supply security through diversification of LNG sources.

•For many of such LNG sources, Japan is the foundation customer.

4

Primary Energy Consumption Comparison of the world (2007)

Source:BP Statistical Review of World Energy June 2008

The share of natural gas consumption is still smaller in comparison to other countries.

44% 46%

20%32% 28%

51%40%

32%

18%

36%

16% 14%

3%

9%7%

47%

22% 35%55% 24%

24% 25%

70%

51%56%

31% 18%16%

29%

12%14% 1% 1% 4% 1%

9%6% 6%

4% 0%6% 7% 5% 6% 6% 5% 6%

1%

1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Japan

S.Kore

a

China

Indi

a

E.Asi

a

M.E

ast

Amer

ica

Europe

Soviet

Total

HydroNuclearCoalGasOil

Former

Union

5

Unit:MTPA

based on “Natural gas market in Asia-Pacific and Atlantic 2008, IEEJ”

0

10

20

30

40

50

60

70

80

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Contract Demand (Low case) Demand (High Case)

LNG Supply-Demand Projection in Japan

38MTPA of LNG

Japan, with scarcity in natural resource, will continue to increase LNG import to meet the increase in gas demand and to renew existing contracts.

60

2

4

6

8

10

12

14

16

18

20

22

96 97 98 99 00 01 02 03 04 05 06 07 080

20

40

60

80

100

120

140

LNG(J apan)

Crude Oil(J CC)

($/mmbtu)($/bbl)

Movement in Crude Oil and LNG Prices

Asian LNG Prices have been stable in the past, but in the future … ?

•Recent rapid rise in crude oil has impacted LNG price discussion

•Recent rapid rise in crude oil has impacted LNG price discussion

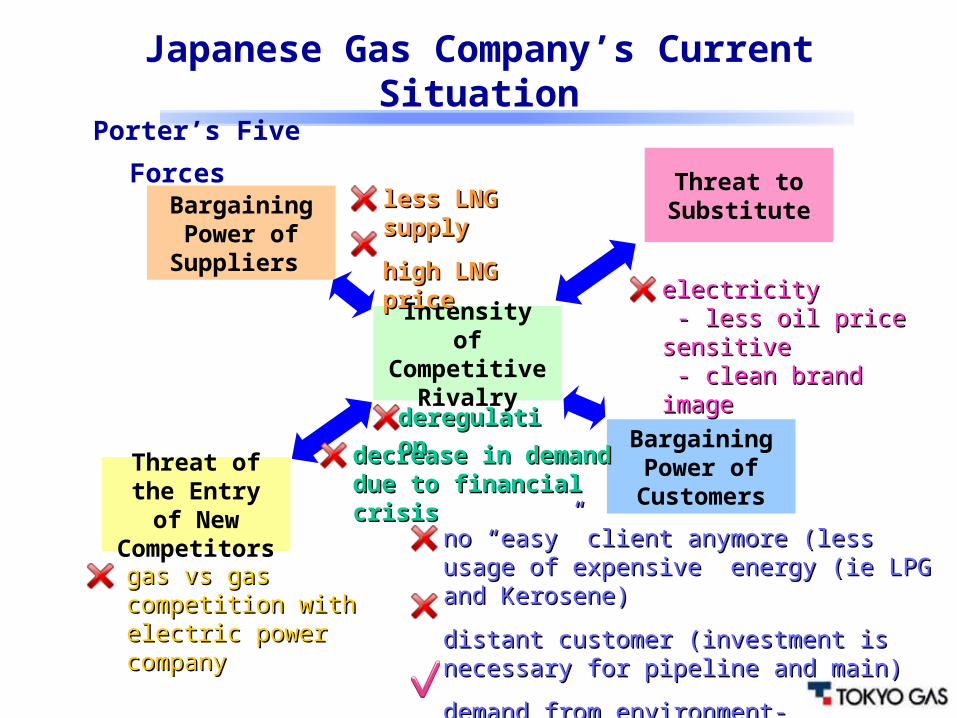

Japanese Gas Company’s Current Situation

Bargaining Power of

Suppliers

Intensity of Competitive

Rivalry

Bargaining Power of

Customers

Threat to Substitute

Threat of the Entry of New Competitors

Porter’s Five Forces less LNG supplyless LNG supply

high LNG pricehigh LNG price

gas vs gas competition gas vs gas competition with electric power with electric power companycompany

deregulationderegulation

decrease in demand decrease in demand due to financial crisisdue to financial crisis

electricity electricity - less oil price sensitive - less oil price sensitive - clean brand image - clean brand image

no “easy” client anymore (less usage of no “easy” client anymore (less usage of expensive energy (ie LPG and Kerosene) expensive energy (ie LPG and Kerosene)

distant customer (investment is necessary for distant customer (investment is necessary for pipeline and main)pipeline and main)

demand from environment-friendlinessdemand from environment-friendliness

Japanese Gas Company’s Current Situation

Bargaining Power of

Suppliers

Intensity of Competitive

Rivalry

Bargaining Power of

Customers

Threat to Substitute

Threat of the Entry of new Competitors

less supplyless supply

high LNG price ~oil high LNG price ~oil parityparity

no “easy” client anymore (less usage of no “easy” client anymore (less usage of expensive energy (ie LPG and Kerosene) expensive energy (ie LPG and Kerosene)

distant customer (investment is necessary for distant customer (investment is necessary for pipeline and main)pipeline and main)

demand from environment-friendlinessdemand from environment-friendliness

electricity (less oil price electricity (less oil price sensitive)sensitive)

clean brand image for clean brand image for electricity electricity

gas vs gas gas vs gas competition with competition with electric companyelectric company

deregulationderegulation

decrease in demand decrease in demand due to financial due to financial crisiscrisis

Porter’s Five Forces

Sustainable Japanese gas market need to Sustainable Japanese gas market need to be supported by:be supported by:

1.1. LNG price that can support LNG Buyer’s LNG price that can support LNG Buyer’s long term investment and growthlong term investment and growth

2. LNG price with less sensitive to oil price 2. LNG price with less sensitive to oil price fluctuation (gentler slope)fluctuation (gentler slope)

3.3. separation of long-term and spot LNG separation of long-term and spot LNG pricingpricing

Sustainable Japanese gas market need to Sustainable Japanese gas market need to be supported by:be supported by:

1.1. LNG price that can support LNG Buyer’s LNG price that can support LNG Buyer’s long term investment and growthlong term investment and growth

2. LNG price with less sensitive to oil price 2. LNG price with less sensitive to oil price fluctuation (gentler slope)fluctuation (gentler slope)

3.3. separation of long-term and spot LNG separation of long-term and spot LNG pricingpricing

9Asia-PacificAsia-PacificEurasiaEurasiaMiddle-EastMiddle-East

AtlanticAtlanticAtlanticAtlanticExisting Flow

New Flow

Regional Aspects of Gas Prices

•Although globalization has emerged in a portion of shorter-term trades, the bulk of LNG trades remain to be regional long-term contracts.

•Downstream gas market still carry strong regional characteristics around the world.

Oil ProductsOil Products Henry HubHenry HubJCCJCC

10

LNG Market Trend in Asia

China•A large number of domestic pipe line projects exist.•The difference between domestic market prices and LNG prices cannot be covered by subsidies.

•Will end users not be able to pay high prices?•Although numerous plans exist for the LNG terminal construction, will those be realized?

•Will return to the coal-based energy policy occur?

India•With the development of domestic gas fields in Dhirubhai and Deen Dayal on the East Coast in place, is large amount of LNG is required?

Rise of LNG prices

11

Strong Points of Japan as an LNG Buyer

Japan will continue to be the Foundation Customer for New LNG Projects.

By launching new LNG projects with Japanese buyers as the Foundation Buyers, new LNG projects can further expand its business

to other new markets and new fields.

Japan will continue to be the Foundation Customer for New LNG Projects.

By launching new LNG projects with Japanese buyers as the Foundation Buyers, new LNG projects can further expand its business

to other new markets and new fields.

•39 years history Stable Buyer•Has actual market Strong demand base•Substantial facilities can absorb demand growth•Financial support for natural resources advantages in terms and conditions

•39 years history Stable Buyer•Has actual market Strong demand base•Substantial facilities can absorb demand growth•Financial support for natural resources advantages in terms and conditions

Especially natural gas demand for gas companies will dramatically increase if the LNG price satisfies conditions for sustainable growth in downstream gas market. Win/Win situation for both LNG Buyers and the Sellers.

12

Area 03-13

NORTHERN TERRITORYWESTERN

AUSTRALIA

50

KILOMETRES

A U S T R A L I A

0 100

JPDA

Area 03-12

250km

500km

Melville Is.

EAST TIMOR

DARWIN

Suai

Dili

BAYU-UNDAN

ConocoPhillips (US) 57.15% (Operator)Santos (Au) 11.39%INPEX (JPN) 11.27%Eni (Italy) 10.99%TEPCO/Tokyo GasTEPCO/Tokyo Gas 9.20% 9.20% (TE:TG= 2 : 1)(TE:TG= 2 : 1)

ResourcesNatural Gas 3.4TCF(100bcm)LPG Condensate 400mil. bbl

LPG/Condensate (FSO)

Submarine PL (500km)

Darwin LNG (1 train)Darwin LNG (1 train)

[Total Cost USD 3.5bil]

LNG Sale and Purchase (SPA)Seller: Darwin LNGBuyer:Buyer: TEPCO, Tokyo GasTEPCO, Tokyo GasVolume: 3mtpa

(TE 2mtpa, TG 1mtpa)Period: Jan. 2006~ (17years)Shipping: FOB

Topics2004: Condensate LPG2006: LNG

Upstream by Tokyo Gas

13

New Upstream ParticipationPluto and Gorgon

Project Outline

Pluto Gorgon

EquityHolder

Woodside 100%Chevron 50%Shell 25%ExxonMobil 25%

Reserve 4.5~5tcf 40tcf

Plant Capacity

4.3mtpa 15mtpa

Plant Location

Barrup LNG Park Barrow Island

Project Start 2010 -

TG Contract (LNG & Upstream)

Pluto Gorgon

<Contracted> <HOA>

Seller Woodside Chevron

ACQ 1.5~1.75mtpa 1.2mtpa

Duration 15 + 5years 25 years

TransportFOB (incl. some ExShip)

FOB

Equity 5% TBD

Gorgon LNG

14

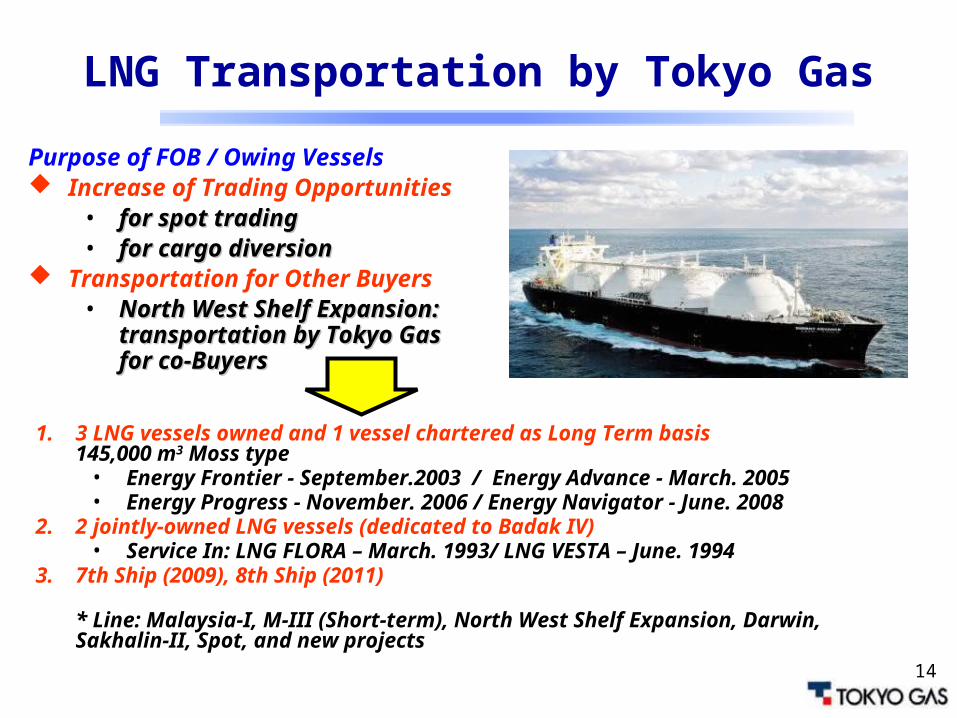

Purpose of FOB / Owing Vessels Increase of Trading Opportunities

• for spot tradingfor spot trading• for cargo diversionfor cargo diversion

Transportation for Other Buyers• North West Shelf Expansion:North West Shelf Expansion:

transportation by Tokyo Gastransportation by Tokyo Gasfor co-Buyersfor co-Buyers

LNG Transportation by Tokyo Gas

1. 3 LNG vessels owned and 1 vessel chartered as Long Term basis 145,000 m3 Moss type

• Energy Frontier - September.2003 / Energy Advance - March. 2005• Energy Progress - November. 2006 / Energy Navigator - June. 2008

2. 2 jointly-owned LNG vessels (dedicated to Badak IV)• Service In: LNG FLORA – March. 1993/ LNG VESTA – June. 1994

3. 7th Ship (2009), 8th Ship (2011)

* Line: Malaysia-I, M-III (Short-term), North West Shelf Expansion, Darwin, Sakhalin-II, Spot, and new projects

15

Thank you very much!!

Recommended