Lecture 5 - Financial Planning and Forecasting

Strategy

A company’s strategy consists of the competitive moves, internal operating approaches, and action plans devised by management to produce successful performance.

Strategy is management’s “game plan” for running the business.

Managers need strategies to guide HOW the organization’s business will be conducted and HOW performance targets will be achieved.

2

Strategic Planning

Strategic planning is a systematic process through which an organization agrees on and builds commitment among key stakeholders to priorities that are essential to its mission and are responsive to the environment.

Strategic Planning guides the acquisition and allocation of resources to achieve these priorities.

3

Strategic Planning versus Operational Planning

Strategic Planning

– formulation–What, where–ends–vision–effectiveness– risk

Operational Planning

– implementation

–how

–means

–plans

–efficiency

–control

4

Financial Planning and Pro Forma Statements

Financial plans evaluate the economics behind the strategy and operations. They consist of six steps:

1. Project financial statements to analyze the effects of the operating plan on projected profits and financial ratios.

2. Determine the funds needed to support the plan.

3. Forecast funds availability.

4. Establish and maintain a system of controls to govern the allocation and use of funds within the firm.

5. Develop procedures for adjusting the basic plan if the economic forecasts upon which the plan was based do not materialize

6. Establish a performance-based management compensation system.

5

Steps in Financial Forecasting

Forecast sales

Project the assets needed to support sales

Project internally generated funds

Project outside funds needed

Decide how to raise funds

See effects of plan on ratios and stock price

6

Sales Forecast

Sales forecasts are usually based on the analysis of historic data.

An accurate sale forecast is critical to the firm’s profitability:

Under-optimistic

Too much inventoryand/or fixed assets

•Low turnover ratio•High cost of depreciation and storage•Write-offs of obsolete inventory

•Low profit•Low rate of return on equity•Low free cash flow•Depressed stock price

Over-optimistic

•Company will fail to meet demand•Market share will be lost

Sales Forecast

7

8

Sales Forecast

The Percent of Sales Method

This is the most common method, which begins with the sales forecast expressed as an annual growth rate in dollar sale revenue.

Many items on the balance sheet and income statement are assumed to change proportionally with sales.

9

Step 1 - Analyze the Historical Ratios

*Spontaneous generated funds - increase spontaneously with sales

**

10

Step 2 – Forecast the Income Statement

11

How to Forecast Interest Expense

Interest expense is actually based on the daily balance of debt during the year.

There are three ways to approximate interest expense. Base it on:

Debt at end of year

Debt at beginning of year

Average of beginning and ending debt

More…

12

Basing Interest Expense on Debt at End of Year

Will over-estimate interest expense if debt is added throughout the year instead of all on January 1.

Causes circularity called financial feedback: more debt causes more interest, which reduces net income, which reduces retained earnings, which causes more debt, etc.

Basing Interest Expense on Debt at Beginning of Year

Will under-estimate interest expense if debt is added throughout the year instead of all on December 31.

But doesn’t cause problem of circularity.

13

A Solution that Balances Accuracy and Complexity

Base interest expense on beginning debt, but use a slightly higher interest rate.

Easy to implement

Reasonably accurate

Basing Interest Expense on Average of Beginning and Ending Debt

Will accurately estimate the interest payments if debt is added smoothly throughout the year.

But has problem of circularity.

14

15

Step 3 – Forecast the Balance Sheet

15

16

Step 4 – Raising the Additional Funds Needed

17

2009 Balance Sheet(Millions of $)

Cash & sec. $ 10 Accts. pay. &accruals $ 200

Accounts rec. 375 Notes payable 110Inventories 615 Total CL $ 310 Total CA $ 1000 L-T debt 754

Common +pr stk 170Net fixedassets

Retainedearnings 766

Total assets $2,000 Total Liabilities $2,000

1000

18

2009 Income Statement (Millions of $)

Sales $3,000.00Less: COGS (87.2%) 2616.00 Dep costs 100.00 EBIT $ 283.80Interest 88.00 EBT $ 195.80Taxes (40%) +pr.div 82.30Net income $ 113.50

Dividends (Com+Pr $57.50Add’n to RE $56.00

AFN (Additional Funds Needed):Key Assumptions

Operating at full capacity in 2009.

Each type of asset grows proportionally with sales.

Payables and accruals grow proportionally with sales.

2009 profit margin ($113.5/$3,000 = 3.80%) and retention ratio (56/114) = .49 will be maintained.

Sales are expected to increase by $300 million.

19

20

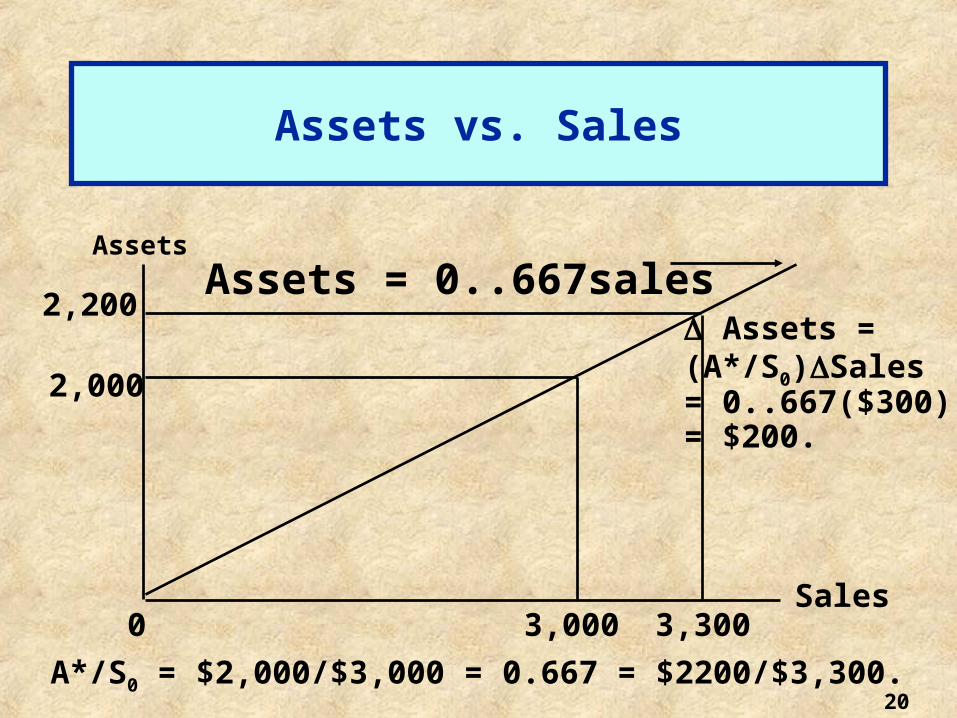

Assets

Sales0

2,000

3,000

2,200

3,300

A*/S0 = $2,000/$3,000 = 0.667 = $2200/$3,300.

Assets =(A*/S0)Sales= 0..667($300)= $200.

Assets = 0..667sales

Assets vs. Sales

Definitions of Variables in AFN

A*/S0: assets required to support sales; called capital intensity ratio.

∆S: increase in sales.

L*/S0: spontaneous liabilities ratio

M: profit margin (Net income/sales)

RR: retention ratio; percent of net income not paid as dividend.

21

If assets increase by $200 million, what is the AFN?

AFN = (A*/S0)∆S - (L*/S0)∆S - M(S1)(RR)

AFN = ($2,000/$3,000)($300) (0.667) x $300

- ($200/$3,000)($300) (0.067) x ($300)

- 0.0380($3,300)(0.49) = $118 million

AFN = $118 million.

22

How Would Increases in Various Items Affect the AFN?

Higher sales:

Increases asset requirements, increases AFN.

Higher dividend payout ratio:

Reduces funds available internally, increases AFN.

Higher profit margin:

Increases funds available internally, decreases AFN.

Higher capital intensity ratio, A*/S0:

Increases asset requirements, increases AFN.

Pay suppliers sooner:

Decreases spontaneous liabilities, increases AFN.

23

Implications of AFN

If AFN is positive, then you must secure additional financing.

If AFN is negative, then you have more financing than is needed.

Pay off debt.

Buy back stock.

Buy short-term investments.

24

What if Balance Sheet Ratios are Subject to Change

We have so far assumed that ratios of both assets and liabilities to sales are constant over time

Sometimes this assumption is incorrect.

25

26

Ass

ets

Sales0

1,1001,000

2,000 2,500

Declining A/S Ratio

$1,000/$2,000 = 0.5; $1,100/$2,500 = 0.44. Declining ratio shows economies of scale. Going from S = $0 to S = $2,000 requires $1,000 of assets. Next $500 of sales requires only $100 of assets.

BaseStock

Economies of Scale

27

Ass

ets

Sales

1,000 2,000500A/S changes if assets are lumpy. Generally will have excess capacity, but eventually a small S leads to a large A.

500

1,000

1,500

Lumpy Assets – Buying Discrete Units

28

What if 2009 fixed assets had been operated at 96% of capacity:

Capacity sales =Actual sales

% of capacity

= = $3,125.$3,000

0.96

Thus, if sales increase to $3,300 fixed assets would only have to increase to 3,300 x .32 = $1,056

Target Fixed Assets/Sales = = = 32%Actual Fixed Asset $1,000 Full Capacity Sales $3,125

Summary: How different factors affect the AFN forecast.

Excess capacity: lowers AFN.

Economies of scale: leads to less-than-proportional asset increases.

Lumpy assets: leads to large periodic AFN requirements, recurring excess capacity.

29

30

Recommended