EASTERN EUROPE &

How to best approach this market

Samuel Vetrak, CEOStudentMarketing Ltd

May 2nd, 2011

---------------------------------------------------------------------With special attention to K-12 sector

How to best approach Eastern Europe

Knowing trends helps you identify opportunities,

design thorough strategy and compete successfully.

Good marketing decisions guided by market research

lead to 25% - 50% increase in revenues within 3 years.

Sources: D.Smith , J.H. Fletcher: The Art & Science of Interpreting Market Research Evidence

Research and development:

Outline

K-12 global student mobility

Eastern Europe

Agent market

How to best approach this market

How to best approach Eastern Europe

Definition of K-12

Is a designation for the sum of primary and secondary education. Internationally, it is often

understood as educational travel. The expression K-12 is a shortening of Kindergarten

through 12th grade (16-19 years old). It is often used in USA, Canada and Australia.

Statistically, K-12 global international student mobility is measured on secondary level only

or data for primary level are not measured separately.

Source: Macmillan Dictionary, CAPS-I, Australian Human Rights Commission, Whatis.com

K-12 global student mobility

23%

58%

71%

22%

32%

29%

31%

10 YTD Increase in % of change

2000 2001 2002 2003 2004 2005 2006 2007 2008 200980

90

100

110

120

130

140

150

160

170

180

K12

Language Travel

Study Abroad

Work Experience

Adventure Travel

Other - Group

Other - FIT

Percentage of change in the youth travel sectors

Sources: UNESCO, LTM, OECD, CAPS-I, CSIET, Citizenship and immigration Canada, Ministry of Education NZ, British Boarding Schools, Australian Education International

K-12 global student mobility

K-12 sector has not been affected by ecomonic downturn as much as some other sectors.

Numbers of international K-12 students in last 10 years

Sources: UNESCO, LTM, OECD, CAPS-I, CSIET, Citizenship and immigration Canada, Ministry of Education NZ, British Boarding Schools, Australian Education International

K-12 global student mobility

K-12 sector is globally increasing its numbers with 35% 10YTD growth.

2000 2001 2002 2003 2004 2005 2006 2007 2008 200980000

85000

90000

95000

100000

105000

110000

115000

120000

83096

88407

97518

103885

10037397928

103629

110615

114408112298

Sources: UNESCO, LTM, OECD, CAPS-I, CSIET, Citizenship and immigration Canada, Ministry of Education NZ, British Boarding Schools, Australian Education International & extrapolated data

2009USA 25%

Australia 24,5%UK 19%

Canada 16%New Zealand 15%

2008USA 25%

Australia 24%UK 18%

Canada 17%New Zealand 14,5%

Numbers of international K-12 students by receiving destinations

K-12 global student mobility

Total number of international K-12 students is estimated to be above 120,000.

USA

Australia

United Kingdom

Canada

New Zealand

0 5000 10000 15000 20000 25000 30000

27924

27506

21533

18319

17016

29004

28313

20545

19910

166362008

2009

Market shares in K-12*

Canada is one of the strongest K-12 destinations, but its market share is decreasing (1.9% in 3 years).

K-12 global student mobility

Sources: UNESCO, LTM, OECD, CAPS-I, CSIET, Citizenship and immigration Canada, Ministry of Education NZ, British Boarding Schools, Australian Education International & extrapolated data

* Calculated from total number of major international K-12 destinations where data available (2009).

USA Australia United Kingdom Canada New Zealand0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

24.8% 24.5%

19.2%

16.3%15.2%

Number of total students in 2010 was 9,0% higher than in 2005, 12,6% higher than in 2003.

Source: Statistics on Semester and Year Programs, The Council on Standards for International Educational Travel

2004 2005 2006 2007 2008 2009 201024000

25000

26000

27000

28000

29000

30000

23.5%

24.0%

24.5%

25.0%

25.5%

26.0%

26.5%

27.0%

27.5%

26201

25815

27972

28268

29004

2792428142

26.1%

26.4%

27.0%

25.6%

25.3%

24.8%

Total USAGlobal share

K-12 global student mobility

Numbers and market shares of USA

Sources: Australian Education International

Number of total students in 2009 was 9,6% higher than in 2005.

2002 2003 2004 2005 2006 2007 2008 200920000

21000

22000

23000

24000

25000

26000

27000

28000

29000

22.0%

23.0%

24.0%

25.0%

26.0%

27.0%

28.0%

23224

2694727312

2509524471

26782

28313

27506

23.8%

26.0%

27.2%

25.6%

23.6%

24.2%

24.7%24.5%

Total studentsGlobal share

K-12 global student mobility

Numbers and market shares of Australia

Numbers and market shares of UK

Sources: Independent Schools Council, British Boarding Schools Workshop

Number of total students in 2010 was 18,1% higher than in 2005, and 37,4% higher than in 2000.

2002 2003 2004 2005 2006 2007 2008 200910000

12000

14000

16000

18000

20000

22000

24000

14.5%

15.0%

15.5%

16.0%

16.5%

17.0%

17.5%

18.0%

18.5%

19.0%

19.5%

18139

1803016460

1822618378

20852 20545

2153318.6%

17.4%

16.4%

18.6%

17.7%

18.8%

17.9%

19.0%

Total studentsGlobal share

K-12 global student mobility

Sources: Ministry of Education of New Zealand

Number of total students in 2010 was 52,1% higher than in 2005, and 19,5% higher than in 2002.

2002 2003 2004 2005 2006 2007 2008 2009 201010000

11000

12000

13000

14000

15000

16000

17000

18000

19000

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

18.0%

15259

17448

14477

11984

13933

15207

1663617016

18228

15.6%

16.8%

14.4%

12.2%

13.4%13.7%

14.5%

15.2%

Total students NZGlobal share

K-12 global student mobility

Numbers and market shares of New Zealand

Source: Citizenship and Immigration Canada, CAPS-I & extrapolated data

Number of total sutdents in 2009 was 8,9% higher than in 2005, and 5,5% higher than in 2000.

2002 2003 2004 2005 2006 2007 2008 200910000

12000

14000

16000

18000

20000

22000

15.0%

15.5%

16.0%

16.5%

17.0%

17.5%

18.0%

18.5%

17366

15941

15923 16808

1887519506

19910

18319

17.8%

15.4%

15.8%

17.2%

18.2%

17.6%17.4%

16.3%

Total studentsGlobal share

K-12 global student mobility

Numbers and market shares of Canada

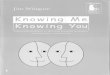

K-12 mobility and market shares in last 10 years

Sources: UNESCO, LTM, OECD, CAPS-I, CSIET, Citizenship and immigration Canada, Ministry of Education NZ, British Boarding Schools, Australian Education International

K-12 global student mobility

K-12 sector is globally increasing its numbers, whereas Canada‘s market share is decreasing.

Overall revenues generated internationally in K-12 sector are estimated to be cca 1.5 bn.

2001 2002 2003 2004 2005 2006 2007 2008 20090

20000

40000

60000

80000

100000

120000

140000

New Zealand

Canada

UK

Australia

USA

TOP Sending countries:

China, South Korea, Taiwan,

Hong Kong, Germany

Eastern Europe is already sending more K-12 students than Latin America.

Sources: UNESCO, LTM, OECD, CAPS-I, CSIET, Citizenship and immigration Canada, Ministry of Education NZ, British Boarding Schools, Australian Education International & extrapolated data

International K-12 students by sending regions

K-12 global student mobility

33%

26%

22%

8%

6%

2% 2% 1% 1%South and Central Asia

South East Asia

Western Europe

Eastern Europe

Central and South America

Sub-Saharan Africa

North America

North Africa and the Middle East

Australia and Oceania

Conclusions

•K-12 represents cca 120.000 students & 1.5 bn (18.319 & 300m in Canada)

•K-12 sector is growing more steadily than other sectors

•Canada is not gaining as much as some other destination

•Canada’s market share is actually descreasing (1.9% in 3 years)

•Eastern Europe is already sending more K-12 students than Latin America

K-12 global student mobility

Eastern Europe

• Multinational diversified region

• Economically growing market

• Interest in English learning

• Increasing demand for education abroad

• Sending more K-12 students than Latin America

• Price sensitive

• Demand for USA/North America

• Agents are predominant booking channel

Eastern Europe

Market features

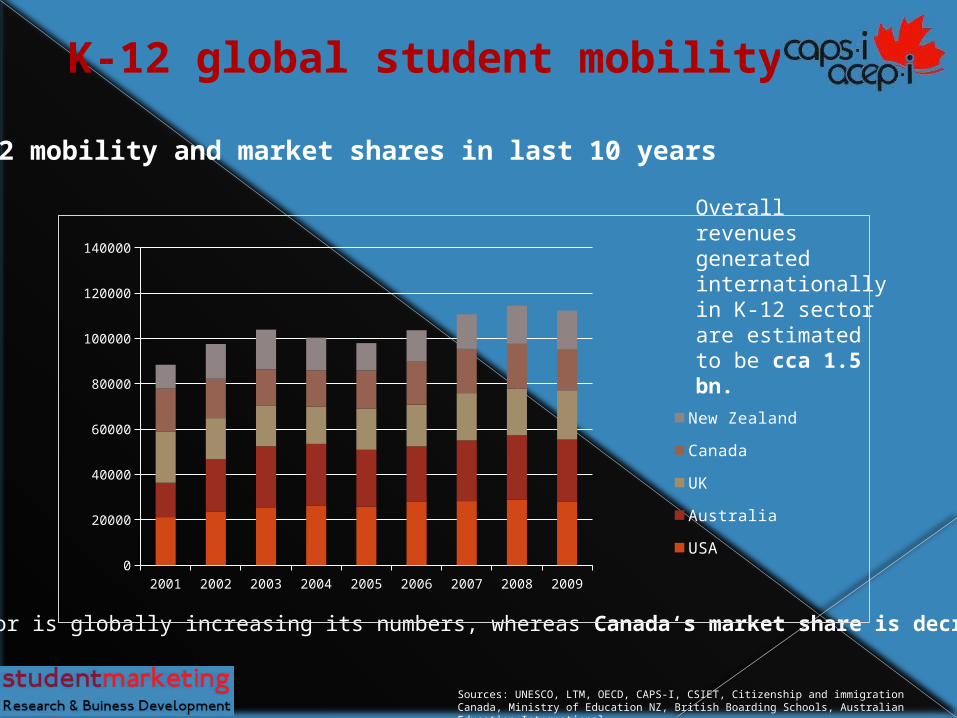

Poland, Czech Republic, Hungary, Slovakia, Belarus, Russia, Ukraine, Estonia, Latvia, Lithuania, Croatia, Slovenia, Albania, Serbia, Bosnia a Herzegovina, Montenegro, Macedonia, Romania, Bulgaria, Romania, Georgia, Armenia, Azerbaijan, Kazakhstan , Kyrgyzstan, Turkey, Tajikistan,

Armenia, Moldova, Turkmenistan, Uzbekistan

Eastern Europe

450m population29 countries18 languages6% K-12 market share770.000 int students

2.600 stu agencies228 K-12 agencies

Portugal

Greece

Italy

Sweden

Spain

France

Netherlands

Belgium

Finland

Austria

Germany

Norway

Swizerland

0 200 400 600 800 1000 1200 1400 1600 1800 2000

Eastern Europe Western Europe

Sources: Laborstats – ILO, 2010

TurkmenistanUzbekistan

UkraineBulgaria

KazakhstanRussia

RomaniaLatvia

HungaryTurkey

SlovakiaPoland

Czech RepublicCroatia

Slovenia

0 200 400 600 800 1000 1200 1400 1600 1800

Eastern Europe

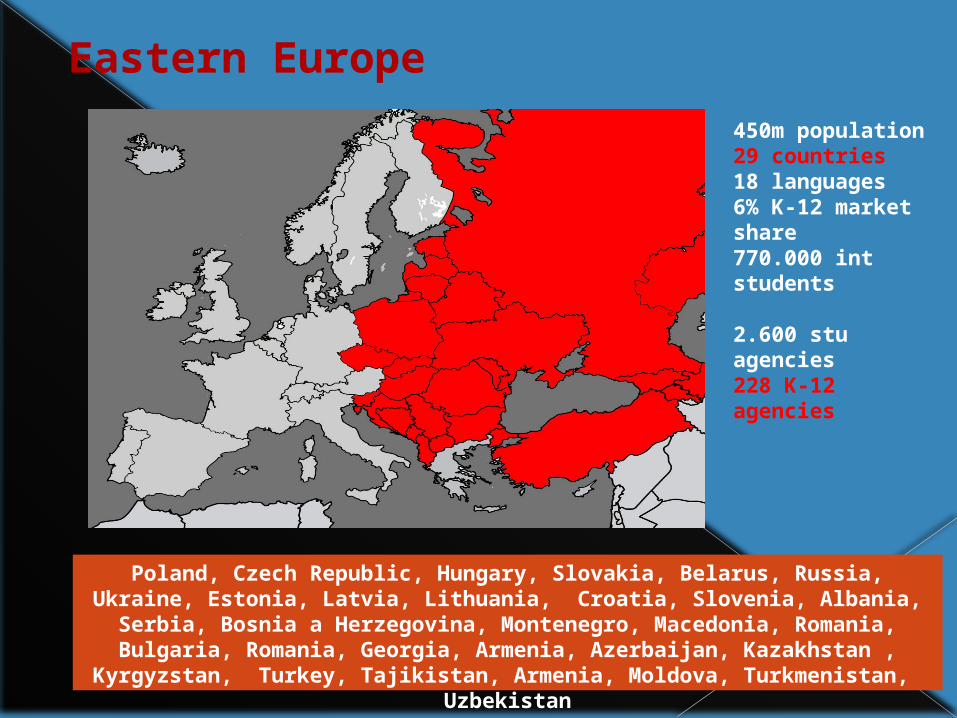

Purchasing power (K-12 Index) – sending countries

Similar to BigMac Index: number of working days one has to work for average wage to buy High School in Canada. The lower the column is, the stronger the buying power is.

Sources: Labostats - ILO

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 20100

100

200

300

400

500

600

700

800

683

618 610 604

549502

479436 417

366340 330

99 96 92 88 85 82 79 76 73 70 67 65

EE TOTALWE TOTAL

Purchasing power doubles in Eastern Europe, Eastern European can afford twice more than in 2000.

Purchasing power (K-12 Index)

Eastern Europe

TOP 100 Most expensive cities in the world (Economist Intelligence Unit)

Source: Economist

4. London (UK)

.....

18. Sydney (Australia)

24. Melbourne (Australia)

28. New York (USA)

29. Manchester (UK)

34. Vancouver

36. Chicago (USA)

36. Montreal

39. Los Angeles (USA)

40. Perth (Australia)

41. Brisbane (Australia)

41. San Francisco (USA)

43. Toronto

44. Washington (USA)

Canadian destinations are more affordable than competitive destinations.

Eastern Europe

Eastern Europe

Market demand for education abroad

Market demand for education abroad is increasing in Eastern Europe, the region is becoming extremely important in the global student market and offers unique opportunity in upcoming years.

2000 20080

20000

40000

60000

80000

100000

120000

140000

160000

91000

146000

Language Travel

2004 2008270000

280000

290000

300000

310000

320000

330000

340000

350000

298000

350000Higher Education

2003 20090

1000

2000

3000

4000

5000

6000

7000

3104

6418

K-12

Eastern Europe

Demand for English in Europe (incl. Eastern Europe)

Eastern European countries increase their English knowledge faster then some in Western Europe.

ColombiaChina

Venezu

elaJap

an

Turke

y

Bulgaria

Hungary

Czech Rep

ublic Italy

Taiw

anSp

ain

Poland

Romania

Portuga

l

France

Lithuan

ia

Slova

kiaRussi

a

Argentina

Latvia

South Korea

Greece

Estonia

Croati

a

Austria

German

y

Slove

nia

Luxe

mbourg

Belgium

Finlan

d

Denmark

Malta

Netherl

ands

Swed

en0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

The increase is within young generation, their need and learn English more than their parents.

Eastern Europe is already sending more K-12 students than Latin America.

Sources: UNESCO, LTM, OECD, CAPS-I, CSIET, Citizenship and immigration Canada, Ministry of Education NZ, British Boarding Schools, Australian Education International & extrapolated data

International K-12 students by sending regions

33%

26%

22%

8%

6%

2% 2% 1% 1% South and Central Asia

South East Asia

Western Europe

Eastern Europe

Central and South America

Sub-Saharan Africa

North America

North Africa and the Middle East

Australia and Oceania

Eastern Europe

Australia

New Zealand

Canada

Ireland

France UK

USA

BelgiumBrazil

South Afric

a

Germany

Argentina0

5000

10000

15000

20000

25000

1430

5

1300

7

8614

1109

8

8364

1083

3

6592 75

21

7641

7152

3736

2105

1

1943

1

1685

9

1611

6

1559

4

1356

5

1369

0

1187

5

8243

8285

7667

Semester Year Abroad

(in CAD; ECB April 20th 2011)

Source: StudentMarketing 2011

Average prices in Eastern Europe (K-12 receiving destinations)

Eastern Europe

Price is an important factor for parents when making purchasing decisions.

Source: StudentMarketing 2011. On the basis of the offer of Eastern European agents. The prices are in average. They may vary due accommodation type (homestay/residence) and the school type (private/public).

(in CAD)

Australia Canada France USA UK SA

Semester (tuition, room, board) 14305 8614 8364 5829 10833 7641

Year (tuition, room, board) 21051 16859 15594 13690 13565 8243

Flight tickets (roundtrip) 1850 1122 227 924 269 1110

Visa fee 555 125 0-138 0 - 134 0 - 120 61

TOTAL 23456 18106 15821 14614 13834 9414

Average prices in Eastern Europe (K-12 receiving destinations)

Eastern Europe

Source: StudentMarketing 2011

Average prices in Europe (High School in Canada)

Eastern Europe

Western Europe Eastern Europe

Semester Public 13889 8042

YearPublic 21423 16552

Private 29255 23523

(in CAD)

Eastern Europe is still more price sensitive region than Western Europe (across sectors).

USA43%

Australi

a5%

UK44%

Canada9%

TOP K-12 destinations in Eastern Europe

Source: StudentMarketing 2011

Eastern Europe

Eastern Europeans are traditionally interested in USA, USA as K-12 however sometimes does not meet the demand from Eastern Europe.

Importance of agents

"Parents of prospective students often require the services of an agent to ensure they get exactly

what they are looking for. “In some of these countries,” asserts Declan Millar at High Schools

International, which places students in high schools in Ireland, the UK, Australia, the USA and

Canada, “clients do not have the expertise or experience to make good informed choices and

depend on agencies for this and for visa guidance. They also depend on local agents for

progression guidance to universities.”

Eastern Europe

Importance of agents

•Eastern Europe has similar booking habits to other markets

•Almost all K-12 bookings come from agents (industry experience, no data available)

•Trend similar to other junior levels in educational sectors (language, jugendreisen, etc.)

•Parents need agents due trust, orientation, paperwork, problemsolving, etc.

•Online shopping is not increasing in educational travel ama in other sectors

•Online presence however is important (cca 60-80% check before visiting stone office)

Eastern Europe

Conclusions

•Eastern Europe represents 29 countries (nationality mix)

•Eastern Europeans have now 2 times stronger purchasing power than in 2000

•Eastern Europe is growing and already sending more K-12 students than Latin America

•Canadian schools could gain from limited supply in USA

•Canadian schools could benefit from sensitive price strategy

•Canadian schools should approach agents as the most important channel

Eastern Europe

There are 29 countries and 2600 youth and student travel agents.

Agent market is maturing, but there are still mostly small agencies.

Average sending numbers per agent is 258.

Schools need to be prepared to work with several agencies in region.

To maintain effort and overheads, educators need to be selective what agents to work with.

Features of agents or how to qualify agencies:

- Age / Experience- Portfolio- Offices / Counsellors- Sending numbers- Price levels- Workshop attendance- Credentials / Association membership

Source: StudentMarketing 2011

Agents in Eastern Europe

Source: StudentMarketing 2011

Agents in Eastern Europe

Profile of agents by experience/age

Agent market is maturing, not so many new agencies, market is taken by old agencies who have made to buid their market position. These agencies are the best targets to make representatives.

1 to 5 5 to 10 10 to 15 15 to 20 20 to 30 30 to 40 40 to 50 50+0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

12.0%

24.5%25.7%

24.5%

9.6%

0.9% 0.6%1.8%

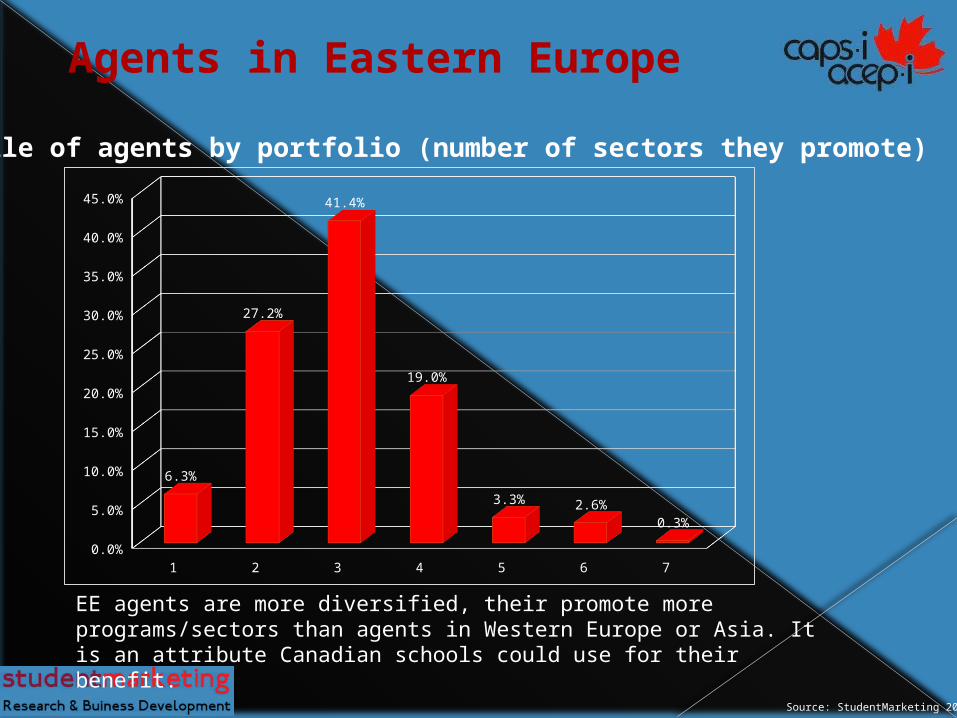

Profile of agents by portfolio (number of sectors they promote)

Source: StudentMarketing 2011

Agents in Eastern Europe

EE agents are more diversified, their promote more programs/sectors than agents in Western Europe or Asia. It is an attribute Canadian schools could use for their benefit.

1 2 3 4 5 6 70.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

6.3%

27.2%

41.4%

19.0%

3.3% 2.6%0.3%

Profile of agents by number of inter/national offices

Source: StudentMarketing 2011

Agents in Eastern Europe

EE agencies are usually small operations and have no more then 1 office. Canadian schools need to be prepared to work with several representatives in order to cover the region or countries like Russia.

1 2-3 4-5 1-5 6-10 11-15 15-20 20 +0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

57.2%

12.8%

4.2%

74.2%

3.7%1.2% 0.7% 1.1%

7.7%

2.2% 0.7%

10.5%

1.9% 0.3% 0.4% 0.8%

National offices

International Offices

1-10 10-50 50-100 100-200 200 and more0

5

10

15

20

25

30

35

40

31%

39%

9%13%

9%

Profile of agents by number of students administered by one employee

Source: StudentMarketing 2011

Most EE agents have qualified and sufficient personel to provide high level of consultancy and customer service the parents and youngsters require.

Agents in Eastern Europe

1-10 10-50 50-100 100-200 200 and more0%

5%

10%

15%

20%

25%

30%

35%

40%

6%

12%

28%

39%

15%

Profile of agents by number of students administered by one office

Source: StudentMarketing 2011

Agents in Eastern Europe

Most EE agents still offer in person customer service in their offices, it is also one of the reasons why the market is broken down to many small agencies.

Profile of agents by sending numbers

Even though Eastern Europe as a region represents a significant sending region, most agents in Eastern Europe do not send high number of international students.

Source: StudentMarketing 2011

Agents in Eastern Europe

1-10 10-100 100-500 500-1000 1000 and more0

5

10

15

20

25

30

35

40

45

50

1.9

21.7

41

13.5

21.9

4.4

22.1

36.8

16.2

20.6

6.9

46.8

34.8

6.64.8

Western Europe

Germany

Eastern Europe

Profile of agents by price levels

There are various financialmethods in between educational institution and educational agency:

- Gross prices/Commission- Gross prices/Agency Fee- Net Prices - other

Eastern Europe is still very price sensitive and most agents need to adjust the price (only 25% of agencies promote they products for an average price).

below average over0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%38.2%

25.5%

36.4%

Source: StudentMarketing 2011

Agents in Eastern Europe

Source: StudentMarketing 2011

K-12 agents who have attended educational b2b workshops in the past 3 years.

Profile of agents by workshop attendance

Attended workshop

44%

Did not at-tend56%

Agents in Eastern Europe

There are dozens of b2b workshop opportunities in Educational Travel:

ALPHE UKStudyWorldWYSTCALPHE RussiaICEF BerlinBBSWICEF MoscowALPHE Istanbul....

Regarding agent attendance, workshops are one of the best occasions where CAPS-i or individual Canadian schools could build their profile and get new agent partners.

Source: StudentMarketing 2011

21%

79%

Member Not a member

Profile of agents by association membership

Agents in Eastern Europe

There are 110 agent associations worldwide, and dozens in Eastern Europe, that track quality of agencies:

•AREA•TEAG•UED

etc.

For CAPS-i or individual Canadian schools, agent associations represent a unique opportunity to increase their profile and open leads to new agent partners.

K-12 agents who are members of association.

BEST agents in Eastern Europe

Using previous understanding and profiling agents, identification of the most suitable quality agencies can be done as mentioned herein (sample picture only).

Source: StudentMarketing 2011

Agents in Eastern Europe

Conclusions

•Agent market is maturing, but still many small agencies in region

•2.600 agencies in 29 countries

•Educators need to be selective what agents to work with

•There are up to 20 criteria educators can consider

•228 K-12 agents and 800 edu agents (LT & HiEd) in Eastern Europe

•Selective approach enables educators to establish agent relationships effectively

Agents in Eastern Europe

Approach

•Educational value – emphasize academic value in comparison to other destinations

•Translations – to ease understanding for ultimate decision makers/parents

•Competitive price – individually by market

•Focus on agents – agents are predominant channel

•Be selective what agents to work with (out of 2.600)

•Individual educator: attend workshops; followed by sales trips

•Association: Branding at associations, workshops, trade mission; followed by FAM trip

How to best approach Eastern Europe

Source: StudentMarketing 2011

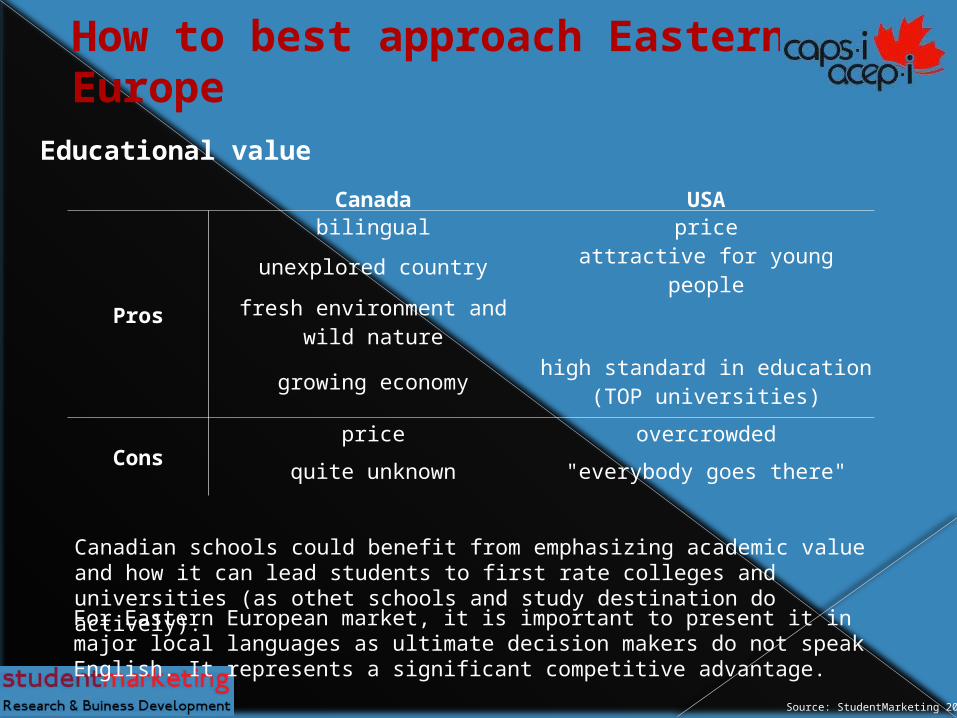

Canadian schools could benefit from emphasizing academic value and how it can lead students to first rate colleges and universities (as othet schools and study destination do actively).

Educational value

Canada USA

Pros

bilingual price

unexplored country attractive for young people

fresh environment and wild nature

growing economy high standard in education (TOP universities)

Consprice overcrowded

quite unknown "everybody goes there"

How to best approach Eastern Europe

For Eastern European market, it is important to present it in major local languages as ultimate decision makers do not speak English. It represents a significant competitive advantage.

(in CAD)

Competitive price

Source: StudentMarketing 2011, Caps-I

Canada USA Difference USA

Semester (tuition, room, board incl.) 8614 6592 - 2022 ↓23,5%

Year (tuition, room, board incl.) 16859 13690 - 3169 ↓18,8%

Tuition only 8219 8530 311 ↑3,8%

Homestay only (year) 8640 5160 3480 ↓40,3%

Flight tickets (roundtrip) 1122 924 - 198 ↓17,6%

Visa fee 125 0 / 134 - 125

How to best approach Eastern Europe

Should it be within possibility, competitve pricing and interactive pricing approach are relevant.

57,4% of High School agents do not promote Canada and represent an opportunity for Canadian schools to have fast approach to experienced agencies with existing outreach.

UK USA Canada Germany France Australia Ireland New Zealand Malta South Africa0

20

40

60

80

100

120

140 130 127

97

79

67 6661

4837

15

Potential agent partners

Source: StudentMarketing 2011

How to best approach Eastern Europe

K-12 agents by destinations

K-12 Agents by sectors

91% out of 2600 agents in Eastern Europe do not promote High School programs. Agents promoting Language and Higher Education represent an opportunity for Canadian schools.

0

10

20

30

40

50

60

70

80

90

9

87

5853

5

15

6

Source: StudentMarketing 2011

How to best approach Eastern Europe

Potential agent partners

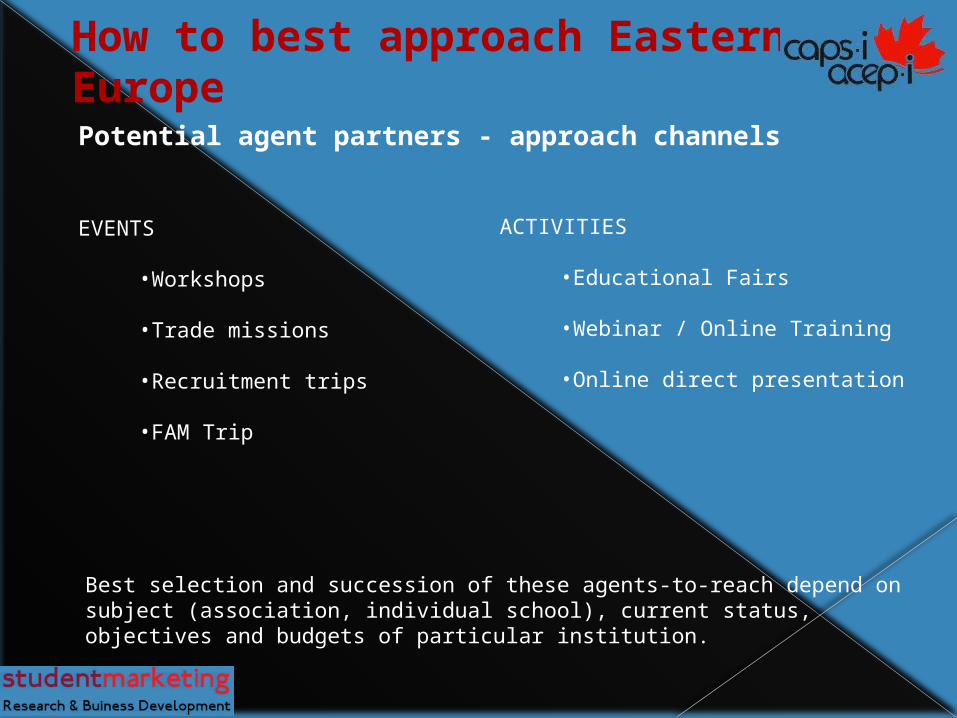

Potential agent partners - approach channels

EVENTS

•Workshops

•Trade missions

•Recruitment trips

•FAM Trip

How to best approach Eastern Europe

ACTIVITIES

•Educational Fairs

•Webinar / Online Training

•Online direct presentation

Best selection and succession of these agents-to-reach depend on subject (association, individual school), current status, objectives and budgets of particular institution.

educational provider located in Canada language, work and study,

internship, career college 10 years in industry total 6.000+ students

Goal: indentification of agents and market opportunities in EE (done in 2007) Result: 35% increase in 2008, 48% increase in 2009

2005 2006 2007 2008 2009 2010

How to best approach Eastern Europe

CASE STUDY

General Conclusions

•K-12 represents cca 120.000 students & $1.5 bn (18.319 & $300m in Canada)

•K-12 sector is growing, but Canada is not gaining as other destinations

•Eastern Europe is a growing region

•Multinational population with increasing demand for education abroad

•Academic value is not well known and needs to be promoted more

•Agents represent predominant recruitment channel in this segment and region

•Regarding number of agencies, selective approach but in person b2b meetings are needed

How to best approach Eastern Europe

EASTERN EUROPE &

How to best approach this market

-------------------------------------------------------Thank you!

Samuel Vetrak, CEOStudentMarketing Ltd

student-market.comMay 2nd, 2011

Recommended