INVESTOR PRESENTATIONSeptember 2016

Parsley Energy Overview

Market Snapshot

Premier Acreage Position(2)

NYSE Symbol: PEMarket Cap: $7,088 MM(1)

Net Debt: $691 MM(2)

Enterprise Value: $7,779 MMShare Count: 207 MM(3)

Midland Basin Net Leasehold Acreage: 90,306(2)

Delaware Basin Net Leasehold Acreage: 42,485(2)

2Q16 Production: 35.7 MBoe/d

(1) Based on 8/30/2016 closing price; (2) As of end 2Q16 pro forma for closing of S. Delaware minerals acquisition on 7/14/2016 and acquisition and equity and debt offerings closed 8/19/2016;(3) As of end of 2Q16 pro forma for equity offering closed 8/19/2016

Leading growth profile

Robust returns

Strategic acquirer

Strong financial position

Abundant upside

2Q16 Highlights

Net production up 23% Q/Q and 60% Y/Y

Net oil production up 25% Q/Q and 82% Y/Y

Adjusted EBITDAX up 48% Q/Q and 52% Y/Y

D&C costs down 8% Q/Q and 26% Y/Y

LOE per Boe down 17% Q/Q and 52% Y/Y

Cash G&A per Boe down 32% Q/Q and 28% Y/Y

Investment Summary

2

9.2

14.015.3

18.218.9

22.2 21.6

25.2

29.1

35.7

0

5

10

15

20

25

30

35

40

0

2

4

6

8

10

12

14

16

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

Net Production (M

Boe/d)Ri

g Co

unt

Horizontal Rigs Vertical Rigs Quarterly Net Production (MBoe/d)

Ongoing Production Momentum

Updated 2016E Production (36.0-38.0 MBoe/d)

In August, raised midpoint of full-year 2016 production guidance by 4,000 Boe/d

New guidance implies 68% year-over-year production growth at the midpoint, with oil production up 90% year-over-year

16% compound quarterly production growth rate over nine quarters as a public company(1)

Previous 2016E Production (31.5-34.5 MBoe/d)

(1) Parsley completed its initial public offering on May 29, 2014 3

Operating Cost Compression

Operating Costs ($/Boe)

$9.12 $7.63$5.57 $5.25 $4.37

$5.91$6.86

$4.41 $6.25$4.28

$2.68$1.75

$1.90$1.58

$1.97

$17.71$16.24

$11.88$13.08

$10.62

2Q15 3Q15 4Q15 1Q16 2Q16

LOE Cash G&A Production & Ad Valorem Taxes

LOE per Boe down for 5 consecutive quarters

Cash G&A per Boe down 32% quarter-over-quarter

Lowered 2016 LOE and cash G&A guidance ranges in August

$5.50 - $6.50

$4.50 – $5.25

2016E(Previous)

2016E(Updated)

$4.75 - $5.75

$4.50 - $5.00

2016E(Previous)

2016E(Updated)

Updated Unit Cost Guidance ($/Boe)

LOE Cash G&A

-40% Y/Y

4

$6.5$6.0

$5.5 $5.2$4.8

2Q15 3Q15 4Q15 1Q16 2Q16

8,000

10,000

12,000

14,000

16,000

18,000

20,0000 5 10 15 20 25 30

Mea

sure

d D

epth

(ft

)

Drilling Days

1st Well 2nd Well 3rd Well

Favorable Development Cost Trends

Continuing to drive down Midland Basin D&C costs

Substantial portion of cost savings attributable to streamlined drilling and completion processes

Southern Delaware Drilling & Completions Costs ($MM)(1)

Midland Basin Drilling & Completion Costs ($MM)(1)

Southern Delaware Cost Compression

Drilling Time Reduction Rapid rate of change in

S. Delaware well costs

Cycle times compressing

Expect convergence toward Midland D&C costs

(1) Normalized for 7,000’ completed lateral

$8.0

$5.7

1st Well Current Costs

5

Glasscock County Acquisition Overview

$400 MM acquisition includes:

9,140 mostly contiguous net leasehold acres in Glasscock County

240 gross horizontal drilling locations in primary target intervals (Lower Spraberry, Wolfcamp A, and Wolfcamp B), with average lateral length of ~7,500’

Mineral and overriding royalty interests translating to ~5% average increase in net revenue interest (“NRI”)

Estimated net production of 270 Boe/d at acquisition announcement on August 15, 2016

5 saltwater disposal wells

Scheduled to close on or before Oct 4, 2016

6

Illustrative Net Present Value Uplift(2)

Glasscock Acquisition Detail – Royalty Interests(1)

Illustrative Rate of Return Uplift(2) Mineral and overriding royalty interests increase NRI by approximately 5% on average

Higher NRI translates to higher returns and NPV

At strip prices: ROR increases by ~10% NPV increases by ~$0.8 MM

0%

20%

40%

60%

80%

100%

120%

140%

$40 $45 $50 $55 $60

ROR

(%)

Oil Price

$0

$2

$4

$6

$8

$10

$40 $45 $50 $55 $60

NPV

($M

M)

Oil Price

Strip Prices

Strip Prices

(1) Assumptions relating to well results and costs are not to be representative of the results we will achieve and may differ materially therefrom; (2) NYMEX WTI and Henry Hub strip prices as of 7/21/2016; NGL price: 40% of WTI; $3/Mcf gas for flat pricing scenarios; Based on the Company’s 1 MMBoe EUR type curve for 7,000’ completed lateral; $4.8MM D&C; 90% WI (reflecting average acquired WI); NRI’s shown are 8/8th’s; $7,500/month fixed LOE; $2.00/BO variable LOE; Estimated ROR and NPV are pre-tax and unhedged 7

Glasscock Acquisition - Favorable Geologic Attributes

Acquired Acreage

Wolfcamp Drill Depth Wolfcamp Thickness Geothermal Gradient

Acquired acreage has comparable depth, thickness, and thermal maturity to Parsley’s high-quality Upton and Reagan core acreage

Degrees Fahrenheit per 1000’ Depth

Drill Depth Sweet Spot

Temperature Sweet Spot

Thickness Sweet Spot

Degrees Fahrenheit per 1,000’ Depth

8

Compelling Acquisitions Year-to-Date

Net LeaseholdAcreage

Net RoyaltyAcreage

Estimated Acquired Production (Boe/d)(2)

Purchase Price ($MM)

Midland Basin 23,953 516 ~2,400 $774

Southern Delaware 17,726 4,847 ~1,480 $440

TOTAL 41,679 5,363 ~3,880 $1,214

9

Acquired ~42,000 net leasehold acres in 1H16 for ~$17,000 per acre(1)

Also acquired more than 5,000 net royalty acres

Large, distributed acreage position supports future growth potential

Year-to-Date Acquisition Summary

(1) Adjusted for estimated PDP value but not for acquired wells in various stages of drilling and completion; (2) Estimated production at time of purchase agreement

Mineral and Surface Rights Enhance Asset Value

Mineral rights acquisition closed in July 2016

Average NRI increases from 75% to 92.5% on affected acreage

Running one rig for one year, higher NRI adds ~400 MBoe and ~$16 MM cash flow(1)

with no additional cost

(1) Cash flow estimate based on NYMEX WTI and Henry Hub strip prices as of 7/21/2016 using NSAI-estimated average EUR for potential horizontal wells on Parsley acreage in S. Del. Basin

Acquired surface rights on ~24,000 acres

Estimate savings of at least $200 M per well on water sourcing and disposal

Additional savings on pads, batteries, roads, rights-of-way, and other surface damages

10

0

25

50

75

100

125

150

30 60 90 120

Cum

ulat

ive

Prod

ucti

on (

MBo

e)(1

)

Days of ProductionTrees Ranch Wells Ranger C4-7-4309H

Favorable Initial Results on Acquired Reeves County Acreage

First Parsley-completed well on recently acquired acreage in Reeves County on pace with strong Trees Ranch wells at the 60-day mark

Strong offset Wolfcamp A wells suggest abundant resource potential on and around acquired acreage

Southern Delaware Well Results

Strong Wolfcamp A Offsets in Reeves County(2)

Well Name Operator Peak Month IP (Boe/d) (3)

Lateral Length

1 Caribou 10-1H Patriot 1,433 4,787’

2 W State 1202H Concho 1,835 5,990’

3 W State 1204H Concho 1,925 5,730’

4 Whiskey River0927-7-1H Jagged Peak 1,381 9,663’

12

3

4

11(1) Normalized to 7,000’ completed lateral and for downtime of 24 hours or more; (2) Production results for selected wells not intended to be representative of potential production from wells we intend to drill in target acreage or of any particular location in such acreage; (3) Source: IHS or company data

Wolfcamp NPV(1)

0%

20%

40%

60%

80%

100%

120%

140%

$40 $45 $50 $55 $60

Rate

of

Retu

rn (

%)

Oil Price

$0

$2

$4

$6

$8

$10

$12

$14

$16

$40 $45 $50 $55 $60

NPV

($M

M)

Oil Price

Attractive Well Economics across Acreage Portfolio

Wolfcamp Returns(1)

(1) NYMEX WTI and Henry Hub strip prices as of 7/21/2016; NGL price: 40% of WTI; $3/Mcf gas for flat pricing scenarios; Midland Basin: based on 1 MMBoe EUR type curve for 7,000’ completed lateral; $4.8MM D&C; 100% WI, 75% NRI; $7,500/month fixed LOE; $2.00/BO variable LOE; Southern Delaware: based on NSAI ~880 MBoe EUR type curve for 7,000’ completed lateral; $5.7MM D&C; 100% WI; $7,500/month fixed LOE; $2.00/BO variable LOE; Estimated ROR and NPV are pre-tax and unhedged

Strip Prices

Strip Prices

First-rate productivity and low costs yield attractive economics in both the Midland and Southern Delaware Basins

Mineral rights produce significant uplift in already compelling returns and NPV

12

Significant Inventory Upside

Parsley well data, petrophysical analysis, and offset results point to four promising target intervals

94% average working interest across Southern Delaware acreage

Close to 500 gross horizontal locations on high-NRI minerals acreage

Significant upside to existing 1,100+ Midland Basin Wolfcamp A and B horizontal locations with Upper Wolfcamp B target and downspacingpotential

Potential increase from 16 to 45 wells per section in the Wolfcamp A and B alone

~850 feet of Wolfcamp A and B combined gross thickness is thickest in Midland Basin core trend area; accommodates ~300’ vertical spacing between landing zones

Midland Basin Wolfcamp A/B Inventory Upside

2nd Bone Spring

Stacked Pay Potential in the Southern Delaware Basin

Wolfcamp A

UpperWolfcamp B

LowerWolfcamp B

Appr

ox.

600

ft

Current Inventory Spacing 660’

Downspaced 330’A-UB-LB

Stack Test (3Q16)

UB-LB Stack & Downspace Test

(2017)

1-Mile Gun Barrel

A-UB-LBStack & Stagger

Test (4Q16)Current InventoryInventory Upside

3rd Bone Spring

Wolfcamp(2 Flow Units)

Gross / NetHz Locations

Assumed Wells per Section

Average Lateral Length

140 / 132 4 7,160’

140 / 132 4 7,160’

550 / 517 8(per flow unit)

7,190’

830 / 781

Note: Spacing tests will be on different leases

13

$475

$550

$400

0

200

400

600

2016 2017 2018 2019 2020 2021 2022 2023 2024

($M

M)

Borrowing Base Senior Notes

Liquidity Summary ($MM) First lien borrowing base availability $475 Cash on hand $259Total liquidity $734

$734 MM of liquidity

Fully undrawn borrowing base of $475 MM

Favorable maturity schedule, with earliest notes maturity in 2022

Strong Financial Position

Favorable Debt Maturity Schedule

Note: All data as of end 2Q16 pro forma for closing of S. Delaware minerals acquisition on 7/14/2016, for acquisition announced 8/15/16 and for equity ($271MM net proceeds) and debt ($200MM net proceeds) offerings closed 8/19/16 14

Substantial Hedge Position

Well-hedged for next several quarters

Structure of oil hedges retains full upside exposure to higher oil prices

(1) When NYMEX price is above put price, Parsley receives the NYMEX price. When NYMEX price is between the put price and the short put price, Parsley receives the put price. When NYMEX price is below the short put price, Parsley receives the NYMEX price plus the difference between the short put price and the put price; (2) Premium realizations represent net premiums collected (from rolled down positions) or paid (including deferred premiums), which are recognized as income or loss in the period of settlement; (3) Functions similarly to put spreads except that when index price is at or above the call price, Parsley receives the call price

$0

$15

$30

$45

$60

$75

0

5

10

15

20

25

3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18

WTI ($/Bbl)M

Bbls

/d

MBbls/d Hedged Weighted Average Long Put Price

2018

3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18

OIL:

Put Spreads (MBbls/d)(1) 21.8 23.5 20.5 20.2 16.1 16.1 4.2

Put Price ($/Bbl) $45.17 $45.03 $45.88 $45.88 $52.85 $52.85 $52.50

Short Put Price ($/Bbl) $32.87 $32.78 $34.14 $34.14 $41.46 $41.46 $40.00

Premium Realization ($ MM)(2) 5.2 5.6 (4.9) (4.9) (7.2) (7.2) (2.9)

M id-Cush Basis Swaps (MBbls/d) 8.2 8.2 11.3 11.3 12.2 12.2 -

Swap Price ($/Bbl) ($0.87) ($0.87) ($1.00) ($1.00) ($1.05) ($1.05) -

NATURAL GAS:(3)

Three Way Collars (MMBtu/d) - - 15.8 15.7 15.5 15.5 -

Call Price ($/MMBtu) - - $4.02 $4.02 $4.02 $4.02 -

Put Price ($/MMBtu) - - $2.75 $2.75 $2.75 $2.75 -

Short Put Price ($/MMBtu) - - $2.36 $2.36 $2.36 $2.36 -

2016 2017

15

2016 Guidance

Capital Expenditures ($MM)

Unit Costs

LOE ($/Boe) $5.50 - $6.50 $4.50 - $5.25

Cash G&A ($/Boe) $4.75 - $5.75 $4.50 - $5.00

Production & Ad Valorem Taxes (% of Revenue)

6.5% - 7.5% 6.5% - 7.5%

Capital Program

Drilling & Completion ($MM) $355 - $395 $395 - $435

Infrastructure & Other ($MM) $55 - $65 $65 - $75

Total Development Expenditures ($MM) $410 - $460 $460 - $510

Activity

Gross Horizontal Completions

Midland BasinDelaware Basin

Average Lateral Length

65 – 75

60 – 685 – 7

~7,000’

80 – 90

75 - 835 - 7

~7,000’

Gross Vertical Completions

Average Working Interest

3 – 6

85 – 95%

3 – 6

85 – 95%

Production

Production (MBoe/d)

% Oil

Previous

31.5 – 34.5

65 – 70%

Updated 8/3/2016

36.0 – 38.0

65 – 70%

Gross Horizontal Completions

$410 - $460$460 - $510

2016E (Previous) 2016E (Updated)

65 - 75

80 - 90

2016E (Previous) 2016E (Updated)

21% Increase at Midpoints

11% Increase at Midpoints

Completing 15 more horizontal wells on just $50 MM capex increase(1)

(1) Based on the mid-point of guidance range16

4

5

6

7

8

9

10

11

12

2016 2017 2018

Hor

izon

tal R

ig C

ount

+1 Rig / Year +2 Rigs / Year +3 Rigs / Year

Positioned for Leading Production Growth

60%

(1) 2016 production based on midpoint of guidance range

Parsley has sufficient inventory depth, acreage footprint, and operational capacity to increase rig count

High average working interest and net revenue interest translate to strong production contribution per rig

30%

Potential 2016-2018 Production CAG

R(1)

2016-2018 Production CAGR Sensitivity

17

$734 MM of liquidity(3)

Net Debt / Annualized Adjusted EBITDAX of 2.1x(3,4)

Substantial hedge position in place

Investment Highlights

(1) See slide 12 for associated assumptions; (2) Adjusted for estimated PDP value but not for acquired wells in various stages of drilling and completion; (3) As of end 2Q16 pro forma for closing of S. Delaware minerals acquisition on 7/14/2016 and acquisition and equity and debt offerings closed 8/19/2016; (4) Net leverage ratio based on annualized adjusted 2Q16 EBITDAX

Expect 68% year-over-year production growth based on midpoint of 2016 guidance

16% compound quarterly production growth rate over nine quarters as a public company

Wolfcamp wells generate ROR of ~60%-90% and NPV of ~$7 MM-$12 MM at strip prices(1)

Growing horizontal production base drives higher oil percentage and lower operating costs per Boe

Acquired ~42,000 net leasehold acres in 1H16 for ~$17,000 per acre(2)

Acquired mineral rights in S. Delaware Basin boost Parsley’s average NRI to 92.5% on affected acreage

Ongoing delineation of multiple target formations in the Midland Basin

Scratching the surface of significant resource potential in the Southern Delaware BasinAbundant Upside

Strategic Acquirer

Leading Growth Profile

World-class Returns

Strong Financial Position

18

Investment Highlights

APPENDIX

19

Glasscock Acquisition Detail - Leasehold

11,672 gross (9,140 net) leasehold acres in Glasscock County

Estimated current net production of 270 Boe/d from 67 vertical wells

Mostly contiguous acreage accommodates long-lateral development

High average working interest of 92% on identified drilling locations

99% held by production

Existing facilities and infrastructure facilitate ongoing development

Significant Inventory Additions(1)

432 gross (397 net) horizontal drilling locations

215 net locations in priority target intervals (Lower Spraberry, Wolfcamp A, and Wolfcamp B), with average lateral length of 7,500’

182 net locations in secondary target intervals (Middle Spraberry, Wolfcamp C, and Cline), with average lateral length of 6,950’

Approximately 90% of locations in Core area

Target Interval Gross / NetHz Locations

Average Lateral Length

Middle Spraberry 80 / 72 7,500’

Lower Spraberry 80 / 72 7,500’

Wolfcamp A 80 / 72 7,500’

Wolfcamp B 80 / 72 7,500’

Wolfcamp C 56 / 55 6,600’

Cline 56 / 55 6,600’

432 / 397

GLASSCOCK

MIDLAND

(1) Based on internal estimates assuming 660’ between-well spacing in each target interval20

Glasscock Acquisition - Strong Offset Results(1)

Parsley’s Dwight Gooden 6-7-01AH, completed in the Wolfcamp A, is outpacing the Company’s 1 MMBoe type curve by 10% after almost 90 days of production, with an 82% oil-cut

Encouraging results from other operators in the Lower Spraberry, Wolfcamp A, and Wolfcamp B intervals

Strong Offset Wells Near Acquisition Acreage

0

40

80

120

30 60 90 120

Cum

ulat

ive

Prod

ucti

on (

MBo

e)(2

)

Days of Production

Dwight Gooden 6-7-01AH

First Parsley Horizontal Well in Glasscock

Well Name Bench Operator Peak Month IP (Boe/d) (3)

Lateral Length

1 Dwight Gooden6-7-01AH WC A Parsley 1,161(4) 5,890’

2 Saxon B-1101WA WC A Diamondback 1,173 7,229’

3 Saxon B-1101WB WC B Diamondback 1,118 7,651’

4 Saxon A-1101LS L Spraberry Diamondback 1,086 7,279’

5 Riley B 1807-1WA WC A Diamondback 1,233 7,173’

6 Calverley 1H WC A RSP Permian 1,757(4) 9,968’

7 Calverley 2H WC B RSP Permian 1,877(4) 9,830’

8 Woody 4-1H WC A RSP Permian 946(4) 4,954’

9 Woody 4-2H WC B RSP Permian 1,027(4) 4,954’

(1) Production results for selected wells not intended to be representative of potential production from wells we intend to drill in target acreage or of any particular location in such acreage; (2) Normalized to 7,000’ completed lateral and for downtime of 24 hours or more; (3) Source: IHS or operator presentations; 2-stream; (4) Peak 30-day 3-stream

2,3,4

5

8,9

1

6,7

GLASSCOCK

MIDLAND

21

Glasscock Acquisition - Ample Thickness Across Acreage

A

A’

Middle Spraberry

Lower Spraberry

Wolfcamp A

Wolfcamp B

Wolfcamp C

Cline

A A’

6,500’

7,500’

8,500’

9,500’

TVD

Favorable log characteristics from areas with strong offset wells correlate to acquired acreage

GLASSCOCK

MIDLAND

22

+$0

+$1

+$2

+$3

+$4

+$5

+$6

+0%

+2%

+4%

+6%

+8%

+10%

+12%

+0% +5% +10% +15%

Increase in Project NPV

($MM

)

Incr

ease

in P

roje

ct R

ate

of R

etur

n

Increase in Well Performance

Pads Support Improved Costs and Productivity

Cost and Efficiencies

Estimate $1 MM savings for three-well pad versus three single wells

2-day reduction in spud-to-spud time versus single wells

33% increase in frac stages per day versus single wells

173

205

150

160

170

180

190

200

210

Single Wells Pad Wells

IP30

per

1,0

00’

(Boe

/d)

Estimated Project Economics: 3-Well Pad vs. 3 Single Wells(1)

(1) Assumes $1 MM capital savings vs. single wells plus 10% reduction in LOE for three years due to centralized compression

Pad Productivity Case Study: Upton Core Wolfcamp A

IP30 on Upton Core Wolfcamp A pad wells up 18% versus analogous single wells

Wolfcamp A wells completed in tandem with Wolfcamp B wells set two new company records:

Hirsch E 4201H: 284 Boe/d per 1,000’ IP30

Atkins 14-11-4202H: ~130,000 Boe 90-day cumulative production

Zipper frac induced stress shadowing enhancing well productivity

Upton Core Wolfcamp A Wells

+18%

23

Prepared for Southern Delaware Rig Ramp

Marketing

Ample options for immediate gas and oil takeaway with nearby WahaGas Hub and high-capacity oil transmission lines

Infrastructure

Potential water supply and disposal in place with buildout ongoing

Existing processing and transmission infrastructure provides electricity hubs from which to build out power grid

Surface Ownership

Estimate at least $200 M per-well savings on water sourcing and disposal

Additional savings on pads, batteries, roads, rights-of-way, and other surface damages

24

60 MMcf/d Gas Plant 200 MMcf/d Gas Plant 150 MBo/d Oil Transfer Line

60 MMcf/d Gas Plant(expected by YE16)

120 MMcf/d Gas Plant(Waha Hub)

160 MBo/d Oil Transfer Line

Selected Operating Data

(1) One Boe is equal to six Mcf of natural gas or one Bbl of oil or NGLs based on an approximate energy equivalency. This is an energy content correlation and does not reflect a value or price relationship between the commodities; (2) Average prices shown in the table include transportation and gathering costs and reflect prices both before and after the effects of the Company’s realized commodity hedging transactions. The Company’s calculation of such effects includes both realized gains and losses on cash settlements for commodity derivative transactions and premiums paid or received on options that settled during the period

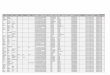

Parsley Energy, Inc.Selected Operating Data

(Unaudited)Three Months Ended

June 30, March 31, June 30,2016 2016 2015

Net production volumes:Oil (MBbls) 2,157 1,731 1,183Natural gas (MMcf) 3,154 2,944 2,698NGLs (MBbls) 566 425 392Total (Mboe)(1) 3,249 2,647 2,025Average net daily production (Boe/d) 35,703 29,088 22,249

Average sales prices(2): Oil, without realized derivatives (per Bbl) $42.25 $30.06 $53.61Oil, with realized derivatives (per Bbl) 47.49 46.73 60.78Natural gas, without realized derivatives (per Mcf) 1.85 1.88 2.48Natural gas, with realized derivatives (per Mcf) 1.85 1.88 2.65NGLs (per Bbl) 16.51 11.04 19.76Total, without realized derivatives (per Boe) $32.72 $23.52 $38.45Total, with realized derivatives (per Boe) $36.20 $34.42 $42.86

Average costs (per Boe):Lease operating expenses $4.37 $5.25 $9.12Production and ad valorem taxes $1.97 $1.58 $2.68Depreciation, depletion and amortization $17.23 $18.66 $21.93General and administrative expenses (including stock-based compensation) $5.33 $7.29 $6.95General and administrative expenses (cash based) $4.28 $6.25 $5.91

25

Adjusted EBITDAX

Note: Certain reclassifications to prior period amounts have been made to conform with current presentation

2016 2015 2016 2015

Adjusted EBITDAX reconciliation to net loss:Net loss attributable to Parsley Energy, Inc. stockholders (21,377)$ (19,129)$ (40,731)$ (36,153)$ Net loss attributable to noncontrolling interests (6,111) (7,051) (12,448) (13,585) Depreciation, depletion and amortization 55,988 44,407 105,372 81,788 Exploration costs 8,978 1,515 9,666 4,734 Acquisition costs 486 — 486 — Loss (gain) on sale of property 469 (1,031) 119 (1,031) Accretion of asset retirement obligations 215 221 385 470 Stock based compensation 3,391 2,112 6,150 3,753 Interest expense, net 12,199 11,099 23,393 22,940 Income tax benefit (10,918) (10,216) (20,486) (15,690) Rig termination costs — 3,870 — 8,970 Derivative loss 27,304 17,733 25,216 10,591 Net settlements on derivative instruments 747 8,071 19,187 21,267 Net premium realization on options that settled during the period 10,551 2,181 20,965 2,045 Adjusted EBITDAX 81,922$ 53,782$ 137,274$ 90,099$

Three Months Ended June 30, Six Months Ended June 30,

Parsley Energy, Inc.Adjusted EBITDAX

(Unaudited, in thousands)

26

Forward Looking Statements and Cautionary StatementsForward-Looking StatementsThe information in this presentation includes “forward-looking statements” that are made pursuant to the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995. All statements,other than statements of historical fact included in this presentation, regarding our strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects, plans andobjectives of management are forward-looking statements. When used in this presentation, the words “could,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project” and similar expressionsare intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. These forward-looking statements are based on Parsley Energy, Inc.’s(“Parsley Energy,” “Parsley,” or the “Company”) current expectations and assumptions about future events and are based on currently available information as to the outcome and timing of futureevents. We caution you that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond our control, incident tothe exploration for and development, production, gathering and sale of oil and natural gas. These risks include, but are not limited to, commodity price volatility, inflation, lack of availability of drillingand production equipment and services, environmental risks, drilling and other operating risks, regulatory changes, the uncertainty inherent in estimating reserves and in projecting future rates ofproduction, the production potential of our undeveloped acreage, cash flow and access to capital, the timing of development expenditures and the risk factors discussed in or referenced in our filingswith the United States Securities and Exchange Commission (“SEC”), including our Annual Report on Form 10-K and our subsequent Quarterly Reports on Form 10-Q and Current Reports on Form 8-K.

You are cautioned not to place undue reliance on any forward-looking statements, which speak only as of the date of this presentation. Except as otherwise required by applicable law, we disclaim anyduty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this presentation.

Our production forecasts and expectations for future periods are dependent upon many assumptions, including estimates of production decline rates from existing wells and the undertaking and outcomeof future drilling activity, which may be affected by significant commodity price declines or cost increases.

Reconciliation of Non-GAAP Financial MeasuresAdjusted EBITDAX and adjusted net income or loss are financial measures that are not presented in accordance with generally accepted accounting principles in the United States (“GAAP”).Reconciliations of these non-GAAP financial measures can be found in our Annual Report on Form 10-K and in the appendix to this presentation.

Industry and Market DataThis presentation has been prepared by Parsley and includes market data and other statistical information from third-party sources, including independent industry publications, government publicationsor other published independent sources. Although Parsley believes these third-party sources are reliable as of their respective dates, Parsley has not independently verified the accuracy or completenessof this information. Some data are also based on the Parsley’s good faith estimates, which are derived from its review of internal sources as well as the third-party sources described above.

Oil & Gas ReservesThis presentation provides disclosure of Parsley’s proved reserves, which are those quantities of oil and gas, which, by analysis of geoscience and engineering data, can be estimated with reasonablecertainty to be economically producible—from a given date forward, from known reservoirs, and under existing economic conditions (using unweighted average 12-month first day of the month prices),operating methods, and government regulations—prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless ofwhether deterministic or probabilistic methods are used for the estimation.

In this presentation, proved reserves attributable to Parsley as of 12/31/15 are estimated utilizing SEC reserve recognition standards and pricing assumptions based on SEC pricing of $46.79 / Bbl crude,$2.501 / MMBtu gas, and adjusted realized pricing of $46.54 / Bbl crude, $16.42 / Bbl NGL, and $2.531 / Mcf residue gas. References to our estimated proved reserves as of 12/31/15 are derived fromour proved reserve report prepared by Netherland, Sewell & Associates, Inc. (“NSAI”).

We may use the term “expected ultimate recoveries” (“EURs”) or other descriptions of volumes of reserves, which terms include quantities of oil and gas that may not meet the SEC’s definitions ofproved, probable and possible reserves, and which the SEC's guidelines strictly prohibit Parsley from including in filings with the SEC. Unless otherwise stated in this presentation, such estimates havebeen prepared internally by our engineers and management without review by independent engineers. These estimates are by their nature more speculative than estimates of proved, probable andpossible reserves and accordingly are subject to substantially greater risk of being actually realized, particularly in areas or zones where there has been limited or no drilling history. We include theseestimates to demonstrate what we believe to be the potential for future drilling and production by the Company. Actual locations drilled and quantities that may be ultimately recovered from ourproperties will differ substantially. In addition, we have made no commitment to drill all of the drilling locations. Ultimate recoveries will be dependent upon numerous factors including actualencountered geological conditions, the impact of future oil and gas pricing, exploration and development costs, and our future drilling decisions and budgets based upon our future evaluation of risk,returns and the availability of capital and, in many areas, the outcome of negotiation of drilling arrangements with holders of adjacent or fractional interest leases. Our estimates may changesignificantly as development of our properties provides additional data and therefore actual quantities that may ultimately be recovered will likely differ from these estimates. Our related expectationsfor future periods are dependent upon many assumptions, including estimates of production decline rates from existing wells, the undertaking and outcome of future drilling activity and activity that maybe affected by significant commodity price declines or drilling cost increases.

Unless otherwise noted, Net Present Value (“NPV”) estimates are before taxes and assume the Company generated EUR and decline curve estimates based on Company drilling and completion costestimates that do not include facilities, land, seismic, general and administrative (“G&A”) or other corporate level costs.

Recommended