1

1. COVID-19 pandemic has reshaped enterprises' priority to adopt new agile business model. We highlight that >70% of enterprises are at early stage of digital adoption.

2. New age/digital services, which comprise of Cloud, Data, Experience and Cyber, are expected to clock 16.5% CAGR and reach US$900bn (67% of total spend) by FY25E.

3. Top-4 Indian IT firms (TCS, Infosys, Wipro and HCLT) are expected to witness strong revenue acceleration driven by higher demand and pay-off from investments in new-age technologies and talent base (reskilling of workforce, innovation centres, digital labs and capability-focused acquisitions).

4. Additionally, the Indian IT companies are likely to benefit from potential captive monetization efforts and vendor consolidation efforts by the global enterprises in the medium-term.

5. Whilst the Biden administration has dovish tone on immigration, we expect localization trend to continue.

6. Resilient operating model (low capex and high variable cost structure) and double-digit revenue growth visibility over FY21E-FY24E deserves premium valuation over broader market.

We Initiate Coverage on Top-4 IT Names with BUY

f TCS: We believe stock deserves multiple rerating on the back of strong double-digit revenue

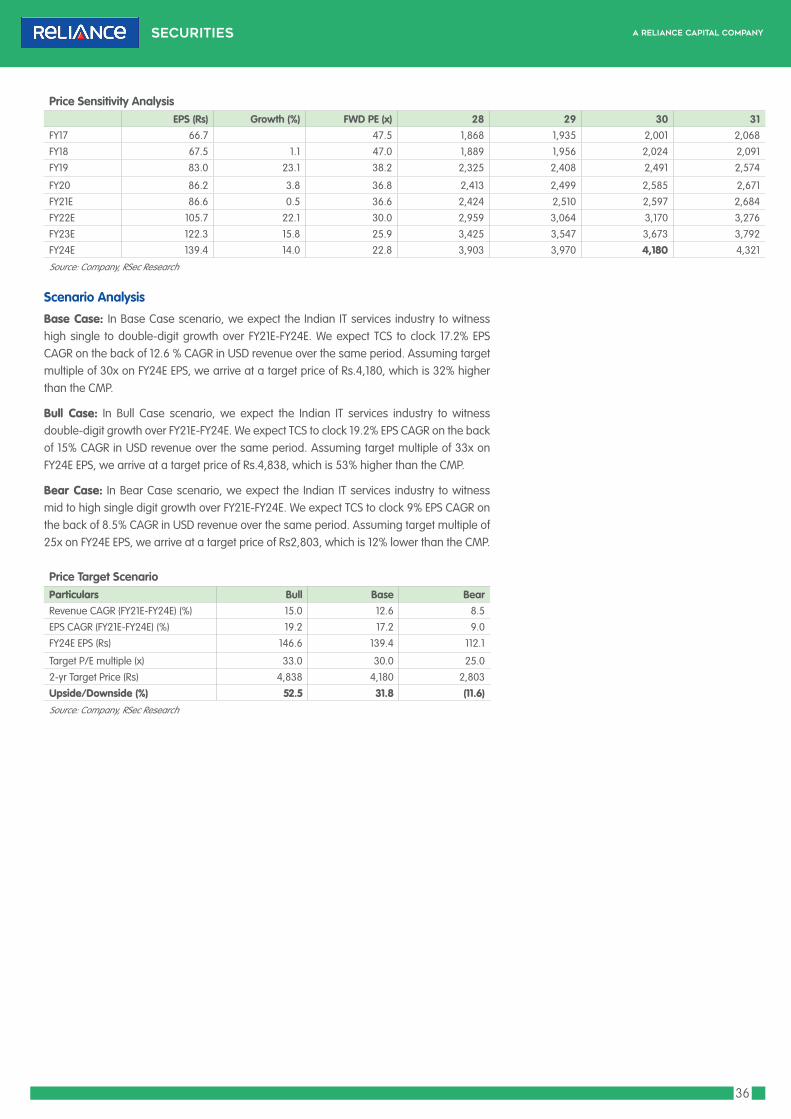

CAGR of 12.6%, expanding EBIT margin and industry leading return ratios (FY24E). We initiate coverage on TCS with BUY and a 2-Year Target Price of Rs4,180 (valuing the stock at 30x PE on FY24E EPS), which implies 32% upside from the current level.

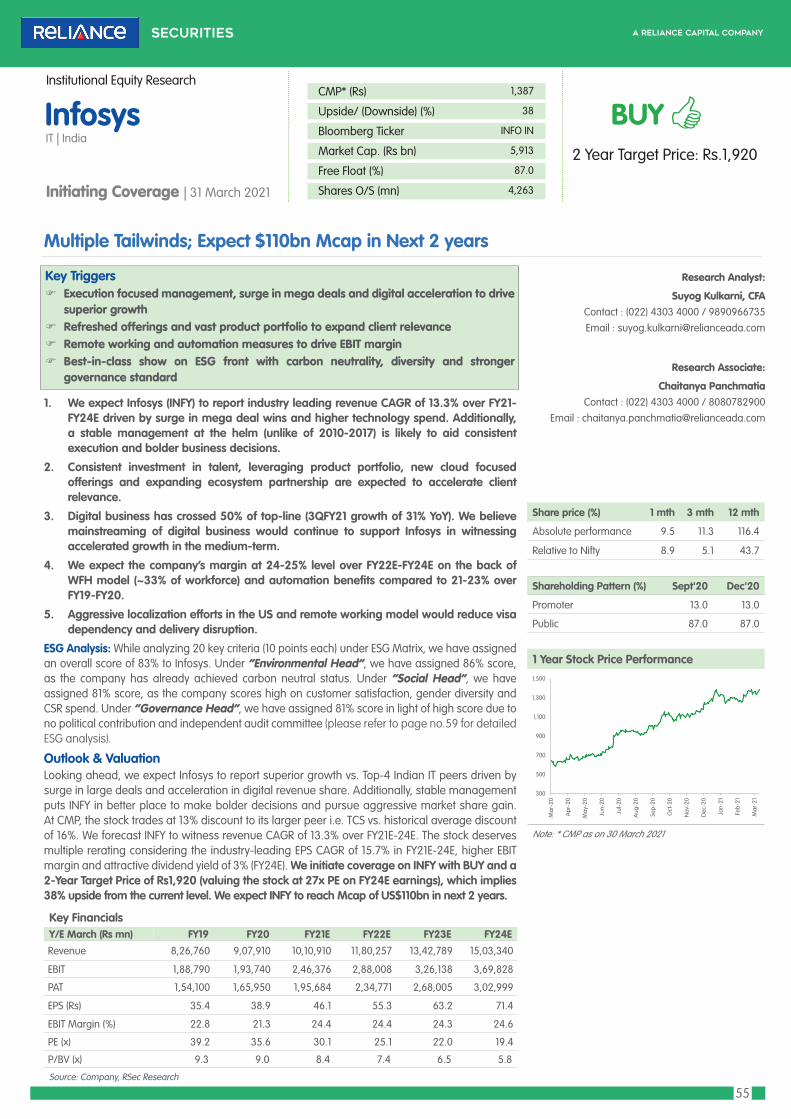

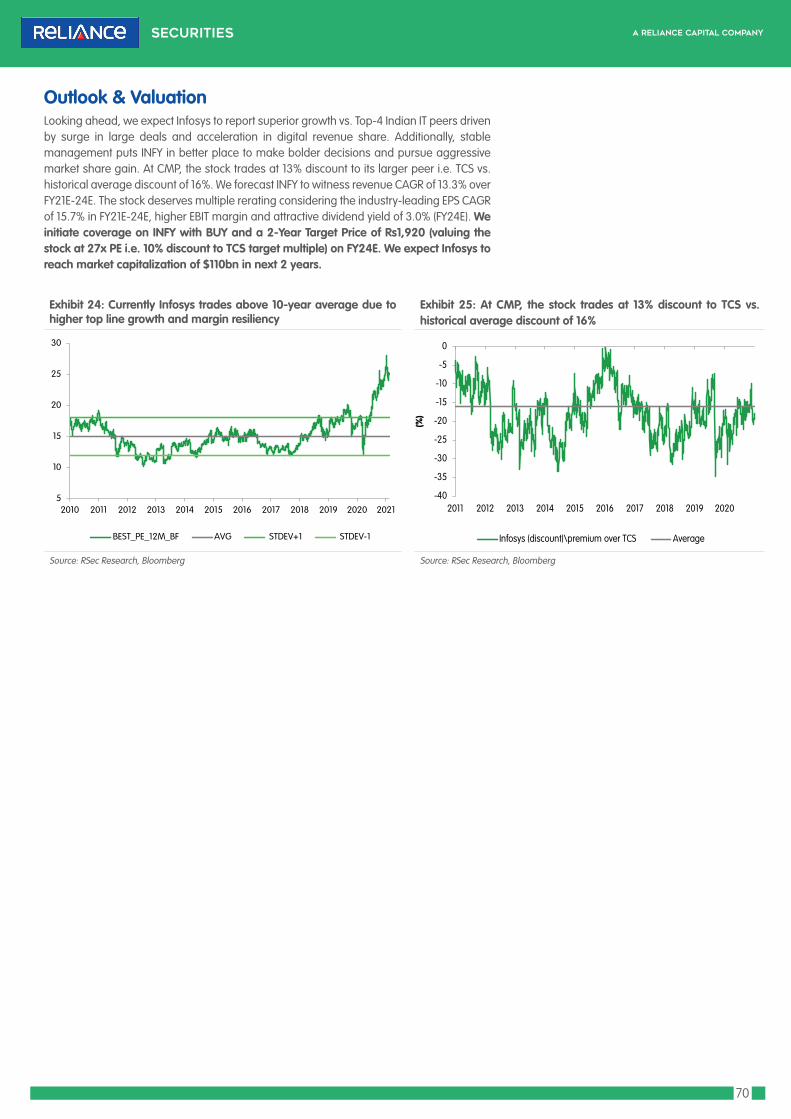

f Infosys: We forecast INFY to witness revenue CAGR of 13.3% over FY21E-24E. The stock

deserves multiple rerating considering the industry-leading EPS CAGR of 15.7% over

FY21E-24E, higher EBIT margin and attractive dividend yield of 3.1% (FY24E). We initiate coverage on INFY with BUY and a 2-Year Target Price of Rs1,920 (valuing the stock at 27x PE on FY24E EPS), which implies 38% upside from the current level.

f HCLT: We forecast HCLT to witness revenue CAGR of 11.7% over FY21E-24E Currently, the

stock trades at 15x of FY24E EPS, which is 37% discount to larger peers i.e. Infosys and TCS.

We initiate coverage on HCLT with BUY and a 2-Year Target Price of Rs1,320 (valuing the stock at 20x PE of FY24E EPS), which implies 33% upside from the current level.

f Wipro: We forecast Wipro to witness revenue CAGR of 13.3% including Capco acquisition.

At CMP, the stock trades at 16.3x on FY24 EPS, which is 25% discount to average of larger

peers i.e. Infosys and TCS. We initiate coverage on Wipro with BUY and a 2-Year Target Price of Rs565 (valuing the stock at 22x PE on FY24E EPS), which implies 35% upside from the current level.

Coverage Summary

Company Rating CMP (Rs)

2 Yr TP (Rs)

Upside (%)

TCS BUY 3,172 4,180 32

Infosys BUY 1,387 1,920 38

HCLT BUY 995 1,320 33

Wipro BUY 420 565 35

Price Performance

Mkt. Cap. Absolute Performance

Company (Rs bn) 1 M 3 M 12 M

TCS 11,905 8.5 9.0 73.7

Infosys 5,913 9.5 11.3 116.4

HCLT 2,700 7.0 5.9 128.2

Wipro 2,396 1.4 9.4 113.2

Key Sectoral Tailwinds:Around 70% of enterprises are at early stage of digital adoption – huge opportunity

Digital services are likely to clock 15-20% CAGR in the medium-term led by Cloud adoption

Potential acquisition opportunities of captive units and vendor consolidation to help the IT players in gaining market share

Strong medium-term growth visibility, resilient business model and consistent cash return policy warrant premium valuation

Top-4 Indian IT names are expected to witness 32-38% upside from the current level

Click Image for Video Presentation

India IT Services - Well-placed to Witness Multi-Year Growth Acceleration

Initiating Coverage | 31 March 2021Institutional Equity Research

Research Analyst:

Suyog Kulkarni, CFAContact : (022) 41681371 / 9890966735

Email : [email protected]

Research Associate:

Chaitanya PanchamatiaContact : (022) 41681371 / 8080782900

Email : [email protected]

We have made changes to our Recommendation and Target Price. Please refer to Page no. 118 at the end of the report.

Source: RSec Research; Note: CMP as on 30 March 2021

Source: RSec Research; Note: CMP as on 30 March 2021

2

Table of Contents

Content Page No.

Sector At a Glance 1-30

f (I)ndia (T)omorrow – A Bird's Eye View of Indian IT Industry........................................................... 3

f Sector At a Glance - Key Charts........................................................................................................... 4

f Key Sectoral Dynamics – At a Glance................................................................................................. 6

• Pandemic-led Accelerated Adoption of Technology..................................................................................... 6• Digital IT Services Expected to Clock 15-20% CAGR over FY20-25E............................................................. 10• Top-4 IT Names Score Well on Digital Capabilities....................................................................................... 11• Potential Acquisition Opportunities of Captive Units/ Vendor Consolidation to Increase Market

Share......................... 13

• Analysis of Key US Clients Suggests Revenue Share Opportunities........................................................... 15• Dovish Tone of New US Administration on Immigration - Worst is Over.................................................... 18

f Nifty IT Trades at 1-25% Discount to Nifty/NASDAQ;............................................................................... 23

f Channel Check Takeaways................................................................................................................................ 28

f Investment Decision Matrix (IDM)................................................................................................................... 29

f Environmental, Social & Governance Matrix (ESGM)............................................................................... 30

Company Section 33-118

TCS 34-54

Infosys 55-74

HCL Technologies 75-96

Wipro 97-118

3

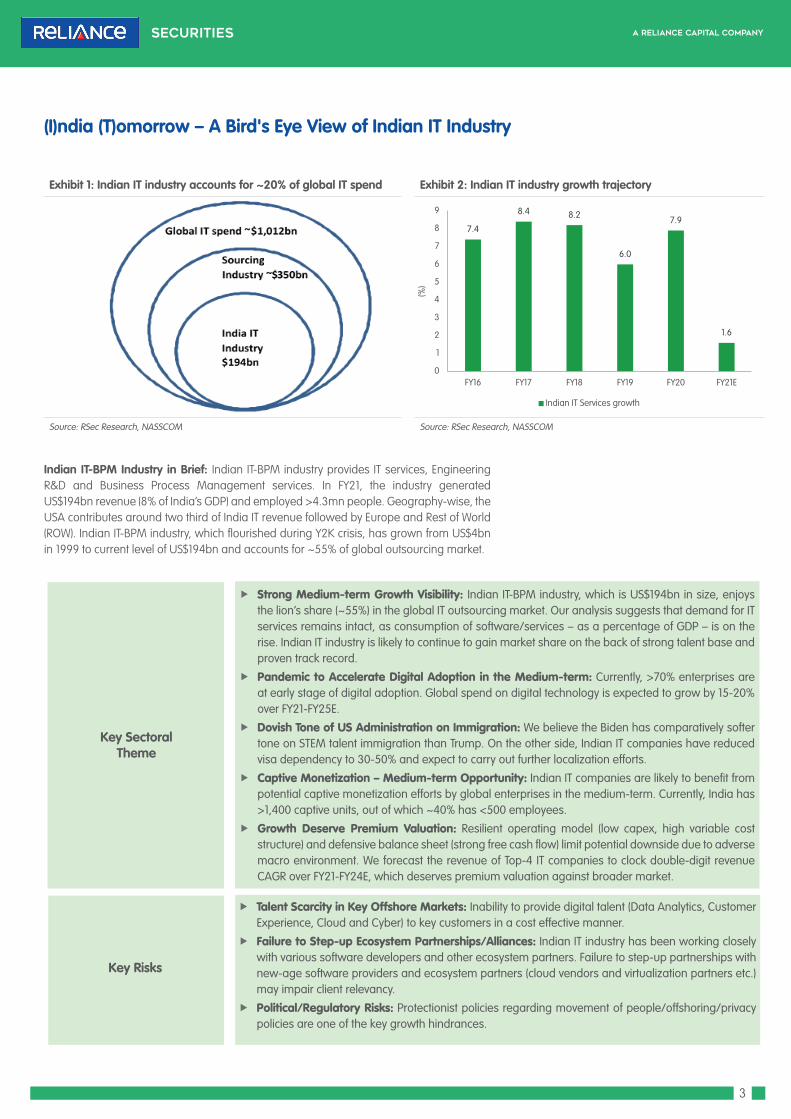

(I)ndia (T)omorrow – A Bird's Eye View of Indian IT Industry

Exhibit 1: Indian IT industry accounts for ~20% of global IT spend Exhibit 2: Indian IT industry growth trajectory

Source: RSec Research, NASSCOM Source: RSec Research, NASSCOM

Indian IT-BPM Industry in Brief: Indian IT-BPM industry provides IT services, Engineering R&D and Business Process Management services. In FY21, the industry generated US$194bn revenue (8% of India’s GDP) and employed >4.3mn people. Geography-wise, the USA contributes around two third of India IT revenue followed by Europe and Rest of World (ROW). Indian IT-BPM industry, which flourished during Y2K crisis, has grown from US$4bn in 1999 to current level of US$194bn and accounts for ~55% of global outsourcing market.

Key Sectoral Theme

f Strong Medium-term Growth Visibility: Indian IT-BPM industry, which is US$194bn in size, enjoys the lion’s share (~55%) in the global IT outsourcing market. Our analysis suggests that demand for IT services remains intact, as consumption of software/services – as a percentage of GDP – is on the rise. Indian IT industry is likely to continue to gain market share on the back of strong talent base and proven track record.

f Pandemic to Accelerate Digital Adoption in the Medium-term: Currently, >70% enterprises are at early stage of digital adoption. Global spend on digital technology is expected to grow by 15-20% over FY21-FY25E.

f Dovish Tone of US Administration on Immigration: We believe the Biden has comparatively softer tone on STEM talent immigration than Trump. On the other side, Indian IT companies have reduced visa dependency to 30-50% and expect to carry out further localization efforts.

f Captive Monetization – Medium-term Opportunity: Indian IT companies are likely to benefit from potential captive monetization efforts by global enterprises in the medium-term. Currently, India has >1,400 captive units, out of which ~40% has <500 employees.

f Growth Deserve Premium Valuation: Resilient operating model (low capex, high variable cost structure) and defensive balance sheet (strong free cash flow) limit potential downside due to adverse macro environment. We forecast the revenue of Top-4 IT companies to clock double-digit revenue CAGR over FY21-FY24E, which deserves premium valuation against broader market.

f Talent Scarcity in Key Offshore Markets: Inability to provide digital talent (Data Analytics, Customer Experience, Cloud and Cyber) to key customers in a cost effective manner.

f Failure to Step-up Ecosystem Partnerships/Alliances: Indian IT industry has been working closely with various software developers and other ecosystem partners. Failure to step-up partnerships with new-age software providers and ecosystem partners (cloud vendors and virtualization partners etc.) may impair client relevancy.

f Political/Regulatory Risks: Protectionist policies regarding movement of people/offshoring/privacy policies are one of the key growth hindrances.

Key Risks

7.4

8.4 8.2

6.0

7.9

1.6

0

1

2

3

4

5

6

7

8

9

FY16 FY17 FY18 FY19 FY20 FY21E

(%)

Indian IT Services growth

4

Sector At a Glance - Key Charts

Exhibit 3: Digital adoption by the enterprises Exhibit 4: Industry experts expect medium term technology uptrend

Source: IT Consultant, RSec Reserach Source: RSec Research, Gartner

Exhibit 5: Digital IT Services Expected to clock 15%-20% CAGR over FY20-FY25E

Source: Wipro

Exhibit 6: Top-40 IT Firms Contribute Only 45% to Global IT Services Industry

Exhibit 7: According to Survey, Financial Stability of IT vendor Remains a Primary Concern of 2021 vs. 2020

Source: RSec Research, Bloomberg Source: RSec Research, Everest Survey

0

5

10

15

20

25

30

35

40

45

50

Early stage Intermediate stage Advanced stage Developed

(%)

Enterprise Digital adoption

53

38

3026 26

14

84

0

10

20

30

40

50

60

Serviceproviderfinancialstability

Serviceprovider

perfomance

Availability ofservice

provider fornew/niche

nees

Cybersecuritythreats

Impact ofservice

providerslong termWFH plan

Lack ofinnovation

from serviceprovider

Decrease inprovider

productivity

Serviceprovider

fraud

(%)

Despite changes there remains concerns such as provider financial stability and performance in 2021

38 39 40 40 40 41

3 4 4 4 4 4

58 58 56 56 56 55

0

20

40

60

80

100

120

58 58 56 56 56 55

(%)

Top 36 global IT names Top 4 Indian IT names Other

3.6

5.0 5.5 5.5 5.4

-2.7

6.0 6.3

8.3 9.1

-4

-2

0

2

4

6

8

10

2020 2021E 2022E 2023E 2024E

(%)

IT Services growth forecast at Jan'20 IT Services growth forecast at Jan'21

5

Exhibit 8: TCS Reported Book to Bill Ratio of 1.4x during 9MFY21 Exhibit 9: Industry experts expect medium term technology uptrend

Source: Company, RSec Research Source: Company, RSec Research

Exhibit 12: Top-4 IT names deserve multiple re-rating, as IT industry is embracing more consumer industry like features

Exhibit 13: US bond yields remain well below historical average

Source: RSec Research, Bloomberg Source: RSec Research, Bloomberg

Exhibit 10: Currently, Nifty IT 12M forward PE trades at 1% discount to Nifty vs. historical peak premium of 40-60%

Exhibit 11: However, NASDAQ (US Technology Index) 12M forward PE trades at 45% premium to S&P500

Source: Rsec Research, Bloomberg Source: Rsec Research, Bloomberg

-30

-20

-10

0

10

20

30

40

50

60

70

01-

07

07-

07

01-

08

07-

08

01-

09

07-

09

01-

10

07-

10

01-

11

07-

11

01-

12

07-

12

01-

13

07-

13

01-

14

07-

14

01-

15

07-

15

01-

16

07-

16

01-

17

07-

17

01-

18

07-

18

01-

19

07-

19

01-

20

07-

20

01-

21

(%)

Nifty IT vs Nifty premium/(discount) Last 10 Yr Average Last 5 Yr Average

0

10

20

30

40

50

60

70

800

1-0

7

08

-07

03

-08

10-0

8

05

-09

12-0

9

07-

10

02

-11

09

-11

04

-12

11-1

2

06

-13

01-

14

08

-14

03

-15

10-1

5

05

-16

12-1

6

07-

17

02

-18

09

-18

04

-19

11-1

9

06

-20

01-

21

(%)

NASDAQ vs S&P premium/(discount) Last 10 Yr Average Last 5 Yr Average

HULGilletteBritania

Nestle

Asian Paints

EPAM

Colgate

TCSInfosysWiproHCLT

8

18

28

38

48

58

68

78

0 5 10 15 20 25 30

FY24

PE

(x)

FY21-FY24E EPS CAGR (%)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

10 year US bond Yield 5 year average 10 year average

(%)

6

Key Sectoral Dynamics – At a GlanceWe are optimistic on the IT Services industry on the back of the following indicators:

f Pandemic-led Accelerated Adoption of Technology

f Digital IT Services Expected to Clock 15-20% CAGR over FY20-25E

f Top Four IT Names Score Well on Digital Capabilities

f Potential Acquisition Opportunities of Captive Units/ Vendor Consolidation to Increase Market Share

f Dovish Tone of New US Administration on Immigration - Worst is Over

I. Pandemic-led Accelerated Adoption of TechnologyIn Jul’20, we highlighted that the levers of medium-term technology demand remained intact, as the demand of IT services/software depends on two factors: (1) level of economic activity; and (2) pace of innovation/introduction of new technology/business model changes. In the early period of the pandemic, though the level of economic activity remained subdued, there was a higher propensity among the enterprises to adopt newer business models and digital technologies. In the medium-term technology landscape, digital technologies (Cloud, Data, Customer Experience and DevOps) were already present but pandemic proved to be a material stimulant in driving the enterprises to adopt agile digital operating model globally. While the digital adoption journey of the enterprises was in much calibrated manner, the pandemic has warranted business case of faster adoption of new age technologies. The pandemic highlighted the downsides of carrying a technology debt and the need for greater resilience, which resulted in accelerated initiative. The enterprises, which were already ahead in digital transformation journey, have managed to respond to pandemic-led challenges better than their peers.

Since our report (July 20, 2020), NIFTY IT has gained 68% and outperformed the broader market by 15%. Going forward, we highlight that the enterprises have committed for medium-term technology transformation programme and we expect accelerated timelines and faster digital transformation for global enterprises. Large Indian IT names are likely to be the key beneficiary of enterprise-wide adoption of new age technology. We forecast USD revenue CAGR of 12.6%/13.3%/13.3%/11.7% for TCS/Infosys/Wipro/HCLT over FY21-24E.

A. Pandemic Reshaped Enterprise Priority to Adopting New Business Model: During the COVID-19 outbreak, few companies managed to grow and gain market share despite immense pressure on both demand and supply front. Additionally, the pandemic accelerated already growing importance of agile operating model, as the customer reach has become much more digital and personalized. The enterprises are in the midst of adopting newer business model, which are based on hyper personalization of consumer needs, user-based pricing, asset sharing model, collaborative workforce and creating agile/scalable operating model.

Exhibit 14: Adaption of new business models remains top enterprise priority

2021 Rank 1 2 3 4 5

Enterprise Priorities Adapting to new business model

Slowdown in decision making

Price/cost pressure Recovery from the Pandemic

Talent/skills shortage

Source: Everest

7

B. Accelerated Digital Timelines & Increased Focus on Digital: The enterprises have stepped up efforts on IT modernization to cope up with new business model and bring in efficiency with cost take out deals. According to Mackenzie’s survey, 60% enterprises – which have witnessed organic growth in last 3 Years – are likely to accelerate their technology up-gradation timeline to maintain their competitive growth leadership. Interestingly, 50% enterprises, which have reported lower decline, increased their focus on digital and large change in technology direction. Enterprise IT transformation remains priority for the leaders (to maintain competitive advantage) as well as for the laggards (for efficiency, growth and survival).

Exhibit 15: Enterprises with strong organic growth in last three years have accelerated transformation timelines

Source: IT Consultant

Exhibit 16: Over 50% of enterprises with declining organic growth have increased focus on digital initiatives

Source: IT Consultant

C. Digital Transformation Still at Nascent Stage: Digital adoption by global enterprises is still at inception stage. According to a survey, >70% of enterprises are in the early stage (early stage experiment and small pilots) and intermediate stage (developing foundations and building operations at scale) in term of digital maturity. The enterprises in technology and retail vertical are comparatively in advanced stage compared to financial and healthcare sector in terms of digital maturity. The current digital transformation priorities reflect the current state of capabilities, impact of COVID-19, management motivations and budget constraints. The current digital transformation priorities are: (1) modernizing IT infrastructure to increase agility, flexibility and security; (2) need to rapidly change and adopt; and (3) organizing customer data, analytics and insight across organization. The top priority for technology investments are: (1) Cybersecurity; (2) Cloud; (3) ML/AI; (4) IoT; and (5) 5G roll-out.

61.0

4.0

24.0

2.0

9.0

0

10

20

30

40

50

60

70

Acceleratedtimeline

Deceleratedtimeline

Increased focuson digital

Large change indirection

Don't know

(%)

Revenue increased by >25%

23.0

13.0

45.0

8.011.0

0

5

10

15

20

25

30

35

40

45

50

Acceleratedtimeline

Deceleratedtimeline

Increased focus ondigital

Large change indirection

Don't know

(%)

Revenue decreased by >25%

8

Exhibit 17: Digital adoption by the enterprises Exhibit 18: Healthcare and Banking industry names lead in early stage transformation adopters

Source: IT Consultant, RSec Research Source: IT Consultant, RSec Research

Exhibit 19: According to IT consultant, maintaining infrastructure operational and agility is the top priority of global enterprises

Source: IT Consultant, RSec Research

Exhibit 20: Key priorities remain Cybersecurity, Cloud, AI, IoT & 5G

Source: IT Consultant, RSec Research

0

5

10

15

20

25

30

35

40

45

50

Early stage Intermediate stage Advanced stage Developed

(%)

Enterprise Digital adoption

28

32

23

20

38

50

40

52

16

12

18

20

18

6

19

8

0 10 20 30 40 50 60 70 80 90 100

Banking/Finance

Healthcare

Retail

Technology

(%)

Early stage Intermediate stage Advanced stage Developed

16

18

19

21

22

22

23

27

30

37

46

0 10 20 30 40 50

Training executives and other leaders

support and security for remote employees

Reinventing workplace to support distributed employee

Improving employee experience (EX) including remote work options

Training and/or hiring employees with digital skill sets

Conducting research to understand customer needs and customer journey

Integrating all customer touchpoints to create a better customer experience

Accelerating innovation through formal programs, internal and external

Organizing customer data, insights and analytics across the organization

Improving operational agility and updating policies and processes to more rapidly adapt to change

Maintain IT infrastructure to increase agility, flexibility, manageability and security

(%)

6

8

8

8

9

10

14

15

16

17

17

17

18

20

23

24

25

27

31

36

42

44

0 5 10 15 20 25 30 35 40 45 50

Drones

Quantum Computing

Autonomous vehicles/ robotics

Wearables

3D Printing/additive manufacturing

Edge Computing

Blockchain

Augmented Reality(AR)/Virtual Reality(VR)

DevOps

Cross functional colloborational platforms

Mobile solutions

Tele-conferencing/video Conferencing

Social Media

eCommerce Platforms

Data Science

Conventional technologies

Real time analytics and reporting

5G

Internet of things (IoT)

Machine learning (ML), Artificial Intelligence(AI)

Cloud

Cybersecurity

(%)

9

D. IT Vendors to Benefit from Medium-term Demand Acceleration from CY21E Onwards: The industry consultants expect that the IT vendors would benefit from the medium-term acceleration in demand from CY21 onwards. Outlook on enterprise spending on IT services has improved by 80-180bps range to 6%/6.3%/8.3% for CY21E/CY22E/CY23E (vs. earlier expectation of 5%/5.5%/5.5%). We also highlight that the historical US software spending, as a percentage of GDP, has been rising consistently. Additionally, global software spends are also likely to go up, going forward. This trend is also likely to accelerate further, which would aid the global software adoption to grow in the range of 8.8-13% over CY21-CY24E. We expect digital adoption to drive demand for software and new age IT services in the medium-term.

Exhibit 21: Industry experts expect medium term technology uptrend Exhibit 22: Software spending is also on the rise

Source: RSec Research, Gartner Source: RSec Research

Exhibit 23: Software investments, as percentage of GDP, are on consistent rise

Source: Federal Reserve Economic Data

11.7

-2.4

8.810.2

12.913.7

-4

-2

0

2

4

6

8

10

12

14

16

2019 2020 2021E 2022E 2023E 2024E

(%)

Software Growth forecast

0.0

0.5

1.0

1.5

2.0

2.5

1959

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

(%)

US Software investments as % of GDP

3.6

5.0 5.5 5.5 5.4

-2.7

6.0 6.3

8.3 9.1

-4

-2

0

2

4

6

8

10

2020 2021E 2022E 2023E 2024E

(%)

IT Services growth forecast at Jan'20 IT Services growth forecast at Jan'21

10

II. Digital IT Services Expected to Clock 15-20% CAGR over FY20-25EGlobal IT spend is likely to clock 7% CAGR over FY21-FY25E. While the traditional components (52%) of spend (on-premise data center and non DevOP ADMs) are expected to witness a negative CAGR of 5%, digital components are expected to register 15-20% CAGR over FY21-FY25E. Digital IT services primary comprise of Cloud hosting, Cloud migration, DevOps, Consulting, transformation projects and IoT. New growth areas i.e. 5G, robotics and block chain are likely to witness 30% CAGR over the same period. The key differentiators for digital solutions are: transformation DNA, industry-specific solutions, automation capabilities and availability of digital talent. Digital component likely to become the core component (67%) of IT services budget in FY25E.

Exhibit 24: Digital IT Services are expected to clock 15%-20% CAGR over FY20-FY25E

Source: Wipro

A. Commentary of Large Financial Institutions Seems Promising: Compilation of commentary from large financial intuitions suggest that technology spending is likely to remain the core of business transformation. Historically, the banks were averse to move their workloads on public cloud due to privacy and other regulatory concerns. But recent commentary suggests accelerated efforts in adopting hybrid Cloud model. Additionally, the banks have strengthened their efforts on data analytics front. Geography-wise, the US banks spend ~40-50% of total technology budget on new-age services, whereas the European banks spend ~25-30% of total budget in new areas. We highlight that the European banks must increase their spend on technology budgets to compete against US Fintech peers.

11

Exhibit 25: Global Banks Remain Committed to Modernize Their IT Ecosystem

Banks Comments

JP Morgan f Bank has built many data centers which work efficiently and bank is also planning move stuff to public cloud. Company is refactoring applications working on data, AI to get there. In every meeting we are talking about data, AI and cloud and what we are moving on cloud.

f AI is being used in asset wealth management, CIB, in trading, in Commercial Banking prospecting and it’s literally the tip of the iceberg.

f Whatever we say today, 10 years from now, it will be probably 50 times more than we are doing today and the banks would spend anything to get it done faster.

BofA f Bank is investing $3.5bn in technology next year which includes expansion of new financial centers. Currently, 69% of bank's consumers and wealth management households are digitally active.

US Bancorp f The company has planned to step up investments in digital channels

Citi f During CY20, expenses being up by 2% to 3%. Most of that is likely to be driven by the-the transformation spend

Barclays f Every year, bank invests over £250mn in technology change projects, and we invest as much, if not more, in technology than the world’s leading tech companies. Annual Technology budget was $3.5bn in 2020.

Deutsche Bank f Bank wanted to become a technology company and digital leader, with plans to spend €13bn on IT through 2022

Source: RSec Research

Exhibit 26: US Banks spend ~48% of Technology Budget on New Areas

Source: RSec Research; Statista

III. Top-4 IT Names Score Well on Digital CapabilitiesThe Indian IT companies have stepped up efforts on digital technologies (Cloud, AI, Cybersecurity, DevOps and experience) in last few years driven by: (1) reskilling majority of workforce with new-age technology; (2) co-operation with the universities and setting up innovation centers; (3) injecting digital experts in deal executions and also refreshing deal offerings to provide integrated deals; and (4) stepping up partnerships with the Cloud hyperscalers and US software names. Currently, digital business accounts for >40% of topline, which we expect to grow in high double-digit. Indian large cap IT names have formed separate units to focus on Cloud migration, Cloud native applications and ancillary services. Cloud, as an infrastructure service, has grown in the excess of 30% in last few quarters, as accelerated Cloud adoption continues to benefit the IT services firm as ecosystem partners.

25 26 27 2830

3337

4044

48

1315

1719

2124

2729

3133

0

10

20

30

40

50

60

2013 2014 2015 2016 2017 2018 2019 2020 2021E 2022E

(%)

North America Europe

12

Exhibit 27: Digital is Becoming New Core for Indian IT Names with Revenue Exposure in the Range of 40-50%

Company name Digital as % of revenues

Comments

Accenture 70 (Aug’20)

f It announced the formation of Accenture Cloud First with US$3bn investment over three years to help the clients across industries rapidly. Accenture Cloud First is a new multi-service group of 70,000 cloud professionals. This new group integrates the company’s wide-ranging cloud expertise, including cloud migration, infrastructure and application services and ecosystem partnerships; deep industry and cross-industry insights, data and applied Intelligence capabilities

TCS ~40-50 f The company has also made Cloud as a strategic priority. TCS cloud consulting unit will look at cross

functional and hybrid cloud business opportunities, where the company will apply its contextual knowledge

Infosys 50 f It launched Cobalt-dedicated cloud unit, which has >15,000 cloud assets and >200 micro verticals

solutions. Infosys acquired few cloud based companies i.e. Simplus, Guidevision & Blue Acron

Wipro 41+ f It is working on Cloud related reskilling initiatives. The company is investing in vertical led offerings,

cloud studios and lab to accelerate growth

HCLT 40+

f It launched a new IP to accelerate deployment of SAP environments on Google Cloud Platform. HCLT also became the only certified SAP competency partner for four hyperscalers i.e. Google Cloud, AWS, Azure and IBM. HCL is also now a Microsoft Cloud Adoption Framework Enterprise Scale Certified Partner. HCLT also expanded collaboration with AWS by joining the ISV workload migration programme. On IBM Cloud, it had set up partnership 2 year ago on hybrid cloud; recently, it expanded this partnership to include IBM public cloud with focus on certain regulated industries.

LTI 44.4 f Targets US$1bn revenue form cloud business in next 3 years. It has set independent cloud unit for each

hyperscaler. LTI has aligned teams with focus on both verticals and service lines.

Mphasis 53.8

f “Our hunting teams have also been realigned to focus on high-growth verticals and on a cloud partner-driven go-to-market strategy. We have seen a 3x increase in our cloud pipeline in the last one year. A 300% jump in the cloud pipeline is attributable primarily to the massively increased adoption and consumption. The company does fair bit of work with both AWS and Azure, and that's what is driving that growth in both pipeline and in the actual TCV”

Source: RSec Research

A. Public Cloud Adoption is Growing High Double-digit: Public cloud companies -Infrastructure as a Service (IaaS) has been growing at ~30%. Amazon Web Services enjoys the lion’s share in the ecosystem with 49% market share. Google Cloud and Microsoft Azure are other large players, who are seeing strong growth. Every dollar spent on Cloud leads to additional US$3 spend on ecosystem.

B. Top-4 IT Names have Strong Relationship with Cloud Platform Providers: Large Indian IT firms were one of the early collaborators with Cloud platform providers. Top-4 IT firms have dedicated teams for each Cloud providers with industry-specific professionals. According to IT consultant Everest, Top-4 Indian IT firms have leadership position with all 3 Cloud platform providers. According to Flexera 2020 state of Cloud survey, 93% enterprises have multi-cloud strategy, while 87% enterprises have a hybrid Cloud strategy. Additionally, 59% enterprises expect Cloud usage to exceed prior year plans due to COVID-19. The organizations expect Cloud spend to increase by 47% in CY21E.

Exhibit 28: Top-4 IT Names Enjoy Strong Ecosystem Relationship with Large Cloud Hyperscalers

Accenture TCS Infosys Cognizant Capgemini Wipro HCLT TechM LTI Mphasis Mindtree

Cloud

System Integrator Capabilities on Google Cloud Platform

Leader Leader Leader Contender Contender Leader Leader Contender

System Integrator Capabilities on Microsoft Azure

Leader Leader Leader Leader Leader Leader Leader Contender Contender Contender Contender

System Integrator Capabilities on Amazon WEB Services.

Leader Leader Leader Leader Leader Leader Leader Contender Contender Contender

Source: RSec Research, Everest

13

IV. Potential Acquisition Opportunities of Captive Units/Vendor Consolidation to Increase Market ShareThe IT services industry is fragmented with the Top-40 names contributing only 45% to total market. Enterprises have large internal tech teams and have also set up multiple offshore units. Additionally, the large enterprises generally deploy multiple vendors across different technology sub-verticals and different geographies. We expect the Indian IT names to witness accelerated market share gain driven by: (1) consistent stable performance in pandemic period and in the aftermath; (2) monetization of captive/internal IT teams - cost take out, variable cost operating model; and (3) consolidation of distributed vendors ecosystem - flight to safety/quality. Historically, Indian IT industry has been consistently gaining market share, which currently stands at 19.4% compared to 9.7% in 2010. Recent surge in large employee rebadging IT deals by TCS, Infosys and Wipro are expected to accelerate this trend further, going forward.

Exhibit 29: Top-40 IT Firms Contribute Only 45% to Global IT Services Industry

Exhibit 30: Indian IT Industry Contributes 19.2% to Global IT Spend

Source: RSec Research, Bloomberg Source: Rsec Research, Nasscom

A. Expect Vendor Consolidation Likely to be Medium-term Tend: There is large scope for the IT sector vendor ecosystem, as there are multiple small technology and geography specific midsize IT vendors. The mid-cap IT firms in general work with few large clients and have high client concentration. They enjoy niche specialization but lack scale and full stack capabilities in some cases to win large size deals. In FY20, L&T acquired Indian IT mid-cap firm Mindtree to get access of capabilities in Technology and Travel & Hospitality vertical. L&T already owns 2 IT and ER&D firms i.e. L&T Infotech and L&T Technology. During last year, Baring Private Equity acquired Virtusa for $2bn. Currently, Baring operates 3 IT firms i.e. Virtusa, Coforge and Hexaware (unlisted). Recently, a large European IT service provider also unsuccessfully attempted to merge with DXC technology. We expect consolidation among IT vendors is likely to be medium-term trend, which will enhance scale and gain market share.

Exhibit 31: Key acquisitions in IT industry

Date Acquirer Type Target Consideration Ownership

Jan-19 Capgemini IT company Altran Eur 3.6bn 100%

Apr-19 Baring Private Equity Asia PE player NIIT Technology $709mn 56% (30% from promoter and 26% from open offer)

Mar-19 L&T Conglomerate Mindtree $1550mn 66.3% (20.3% from promoter, 15% from market, 31% open offer)

Jan-19 DXC IT company Luxoft $2bn 100%

Jul-19 Atos IT company Syntel $3.4bn 100%

Apr-17 DXC IT company Merger of Computer Science Corporation and HPE Enterprise segment

$26bn Merger

Apr-16 Blackstone PE player Mphasis $825mn-$1100mn 60%

Mar-16 Virtusa IT company Polaris $166mn 52%

Source: RSec Research

38 39 40 40 40 41

3 4 4 4 4 4

58 58 56 56 56 55

0

10

20

30

40

50

60

70

80

90

100

2014 2015 2016 2017 2018 2019

(%)

Top 36 global IT names Top 4 India IT Other

2.5

19.2

0

5

10

15

20

25

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

E

(%)

India IT share in Global IT Spend

14

B. Large Indian IT Names to Benefit from Flight to Safety: According to survey conducted by IT services consultant Everest, ~74% enterprises were satisfied with their service providers during COVID-19 shutdown. The primary concern of the enterprises (~53% of respondents) for 2021 is financial stability of service providers vs. niche capability few years back. This suggests that the large Indian IT names backed by strong profitability and net cash balance sheet are likely to be the primary beneficiaries of latest change in enterprise preferences.

Exhibit 32: 74% of Enterprises Satisfied With Their IT Vendors During Pandemic

Exhibit 33: Financial Stability of IT vendor Remains a Primary Concern

Source: RSec Research, Everest Source: RSec Research, Everest

C. Employee Rebadging & Cost Takeout Deals Likely to be Medium-term Trend: We expect trend of large transformation and cost takeout deals to continue in the medium-term driven by: (1) efficiency pressure on enterprises due to COVID-19; (2) better resiliency by IT vendors vs. internal IT/captive teams; and (3) need for integrated transformation approach. There are 1,400 captive units in India, out of which 40% units have <500 employees. Additionally, a glimpse at vendor ecosystem suggests possibility of further vendor consolidation. We believe Top-4 IT names will remain the key beneficiary of monetization of captive unit and Internal IT team. These deals are often large and come with 5-7-year contract duration, which we believe provide strong revenue visibility over the medium-term.

Exhibit 35: TCS reported Book to Bill Ratio of 1.4x during 9MFY21 Exhibit 36: Infosys also reported strong acceleration in large deal orders

Source: RSec Research Source: RSec Research

Exhibit 34: Key Large Deal Wins

Deal Name Size Description

TCS Acquires Postbank Systems Annual run rate of Eur260mn

Driving technology led transformation of bank; ~1,500 employees added

Infosys Daimler Deal US$3.2bn Migration to Hybrid Cloud and Infrastructure Overhaul

Infosys Rolls Royce Deal Not Available Engineering and R&D services

Infosys Transamerica Deal Not Available Enhance digital capabilities

Wipro Metro Deal US$700mn Complete technology, engineering and solutions transformation; ~1,300 employees added

3638

18

4 4

0

5

10

15

20

25

30

35

40

Highly Satisfied ModeratelySatisfied

Neutral ModeratelyDissatisfied

HighlyDissatisfied

(%)

Average Satisfaction with service providers during COVID-19 shutdown

53

38

3026 26

14

84

0

10

20

30

40

50

60

Serviceproviderfinancialstability

Serviceprovider

perfomance

Availability ofservice

provider fornew/niche

nees

Cybersecuritythreats

Impact ofservice

providerslong termWFH plan

Lack ofinnovation

from serviceprovider

Decrease inprovider

productivity

Serviceprovider

fraud(%

)

Despite changes there remains concerns such as provider financial stability and performance in 2021

15

Exhibit 37: TCS' Top 20 US Clients

Client Key Competition

Financial Services f Infosys, LTI, Wipro, Iris Software, Virtusa, NTT data Services, Accenture, Mitchell/Martin, Capgemini, Maveric, Incandescent Tech, Synechron Inc, Oracle Financial Services, E&Y, Photon

Technology f Infosys, Wipro, Quest Global, Cognizant, Deloitte, Red Oak Technologies, DGN Technologies, Antra, Bridgenexus, Compunnel Software, Mastech, Mythri

Retail f KFORCE, Mindtree, Atos, Cognizant, Adecco, Deloitte, Mastech, Ocher Technology, Ugam Solutions

Pharma retail f Cognizant, Photon, GlobalLogic, Accenture, Mastech Digital, Persistent, Populus Group, Multivision, I3 Infotek, E&Y, federal Soft Systems

Financial Services f HCLT, Wipro, IBM, Mastech Digital, Compunnel Software Group, Daman, Populus Group, Inherent Technologies

Financial Services f Atos, Cognizant, KFORCE, Compunnel Software Group, NTT Data, Tech Aspect, Deloitte, Wipro, Capgemini

Healthcare f Cognizant, Headstrong LLC, Randstad, Mastech, Genpact, Computer Software Group, Deloitte, Genpact, Nemo IT, Xsell Resources, Comtek, Kforece, Zensar

Entertainment f Cognizant, Infosys, Mastech Digital, Accenture, MARLABS, Xavient, Wipro, Tata Elexi, E&Y, Virtusa

Financial Services f CSC Covansys Corporation, Cognizant, Accenture, Infostrech, ProKarma, DXC Technology, Perficient, Mastech, Compunnel Software Group, Deloitte, SRS Consulting

Technology f Infosys, SRS Consulting, LTI, Wipro, Zensar, Tech Mahindra, Accenture, Persistent, HCLT, Cognizant, Randstad Technology, Urpan Technology, Capgemini, Enquero, Onstak

Financial Services f Atos, Cognizant, Infosys, Intraedge, IBM, Mastech, Impetus, Deloitte, Humac, M3BI, Virtusa, Computer Software Group, Mindtree

Diversified f Genpact, Tech Mahindra, Capgemini, Accenture, E&Y, Quest Global Services, Hexaware, Headstrong

Financial Services f Mastech, Virtusa, Accenture, Cognizant, E&Y, Randstad, Indotronix, Quiddity Infotech

Financial Services f CGI Technologies, Cognizant, Accenture, Mastech, Randstad, Deloitte, Compunnel Software, EPAM, Mastech, Virtusa, Bradford

Retail f Wipro, Larsen & Toubro Infotech, Cognizant, IBM, Deloitte, HCLT, Capgemini, Accenture, L&T Technology Services, I3 Infotech, Microexcel, BirlaSoft, TechMahindra

Financial Services f HTC Global Services, Capgemini, Accenture, IBM, NTT Data, ARV Systems, Savy Info Systems, Majesco, Global Data

Professional Services f ValuLabs, Infocepts, Maantic, Wave Solutions, Asta CRS

Financial Services f Infosys, Headstrong, Capgemini, Tech mahindra, Synechron, Capgemini, E&Y, Genpact, Deloitte, Virtusa, Mastech Digital

Financial Services f Randstad, Synechron, Diversant, Data INC, Infosys, Mitchell/Martin Collabera, Accenture, Deloitte, E&Y, Genesis Corp

Pharmaceutical f Infosys, Deloitte, Informatica, L&T Technology, Mastech, Deloitte, HCLT, Headstrong, Capgemini, Synechron

Source: RSec Research, Department of Labour (US); Note: Grey highlight denotes common Top-20 client accounts for Top-4 IT names

D. Analysis of Key US Clients Suggests Revenue Share Opportunities: We have analyzed Labour Condition Applications (LCAs) of Top-4 IT names for FY20 (Oct’19-Sept’20), which suggests that the Top-20 US clients list is diversified, and it largely comprises of financial services, retail, technology, automobiles and healthcare firms. We have also analyzed key competitors in large accounts. The key conclusions of our analysis are given in the following:

1. There are multiple common client accounts for Top-4 IT names in top-20 US client accounts list.

2. Accenture, Cognizant and Capgemini remains key global IT competitors. Additionally, Mid cap IT names such as Mphasis and Mindtree has made stronger inroads into the client IT ecosystem.

3. We also highlight HR firms such as Randstad and KFORCE have a decent workshare in the key accounts. We believe this rise was driven by protective visa regime in the US. We expect the large Indian IT firms to benefit from comparatively softer tone on immigration front by the Biden Administration.

4. While the IT vendor ecosystem is dominated by larger vendors (4-6 large vendors), there are multiple medium and small unlisted IT vendors as well (5-20 vendors). Thus, we see a huge scope for vendor consolidation in Top-20 US accounts, going forward.

16

Exhibit 38: Infosys' Top 20 US Clients

Industry Peers

Technology f TCS, Wipro, Quest Global, Cognizant, Deloitte, Red Oak Technologies, DGN Technologies, Antra, Bridgenexus, Compunnel Software, Mastech, Mythri

Retail f Cognizant, TCS, Headstrong LLC, Randstad, Mastech, Genpact, Computer Software Group, deloitte, Genpact, Nemo IT, Xsell Resources, Comtek, Kforece, Zensar

Financial Services f Kforce, Luxoft, Globallogic, Prophesy, Accenture, Sierra Computer, V Soft Consulting

Utility f TCS, HCLT, E&Y, Bridgewater Consulting, Brillio, Anira Software, Cognizant

Financial Services f Atos, Cognizant, TCS, Intraedge, IBM, Mastech, Impetus, Deloitte, Humac, M3BI, Virtusa, Computer Software Group, Mindtree

Financial Services f TCS, LTI, Wipro, Iris Software, Virtusa, NTT data Services, Accenture, Mitchell/Martin, Capgemini, Maveric, Incandescent Tech, Synechron Inc, Oracle Financial Services, E&Y, Photon

Financial Services f IBM, Cognizant,Deloitte, Accenture, V3Tech Solutions, Computer Software Group

Technology f TCS, SRS Consulting, LTI, Wipro, Zensar, Tech Mahindra, Accenture, Persistent, HCLT, Cognizant, Randstad Technology, Urpan Technology, Capgemini, Enquero, Onstak

Financial Services f Wipro, Mphasis, Mastech, Compunnel Software Group, Randstad Tech, Comtek, Dots Technology, HCLT, Persistent, Eureka, M2 Source

Financial Services f Computer Software Group, Atos, Accenture, VASS, Vizplum, Clearlite, Digital Scripts, ERP Analysts, Federal Soft, Horizon Advanced Systems, IBM, Lorhan Corp, LynxTech Group, Morlogic, Quadratic Systems

Financial Services f NTT data, Randstad, Cognizant, Compunnel Software, Persistent, Diversant, Mastech, Mphasis, HCLT, Birlasoft, Deloitte, Synechron Inc

Telecom f Deloitte, Cognizant, Mastech, Kforce, Brillio, TCS, Agreeya,Techno-Comps, Marbles, GlobalLogic, Infinite Computer Solutions, HCL America, Randstad Tech, Virtusa

Energy f Wipro, HCLT, NITCO, Coglomerate IT Services, E&Y, Genuine IT

Financial Services f KFORCE, Compunnel Software, Mastech, Randstad, HCLT, Adroit, Digipulse, Anjus, Technosoft, TCS, Capgemini

Automobile f CSC Covansys, Congnizant, TCS, Deloitte, Hitachi Vantara, HCLT, Hexaware, Hinduja Tech, KFORCE, Mindtree, Photon, Cognizant, Mastech, Photon

Financial Services f CSC, Vertiv, LTI, Accenture, Deloitte, Mastech, EvonSys, Cognizant, Compunnel, EATEAM

Healthcare f Infinite Computer Solutions, Cognizant, TEKNEST, Altek, Cognizant, Concret, Dataquest, Devcare, grrenbyte, Oberon, Orgspire

Retail f KFORCE, Wipro, Cognizant, Populus, Centizen, Cloudwick, E&Y, Mastech, TCS, Centizen, Invincible Tech, Mavensoft

Services f TCS, KFORCE, Randstad, Mercury, Advanced technology Consulting, AMITI, C Vision, Dexperts, Emaestro, Nemo IT, Smart Scope Technologies, 3A Soft

Healthcare f Cognizant, Tech Mahindra, Speciality Resources, Deloitte, Virtusa, Computech

Source: RSec Research, Department of Labour (US); Note: Grey highlight denotes common Top-20 client accounts for Top-4 IT names

17

Exhibit 39: Wipro's Top 20 US Clients

Clients Key Competition

Technology f TCS, Infosys, Quest Global, Cognizant, Deloitte, Red Oak Technologies, DGN Technologies, Antra, Bridgenexus,Compunnel Software, Mastech, Mythri

Financial Services f Infosys, Mphasis, Mastech, Compunnel Software Group, Randstad Tech, Comtek, Dots Technology, HCLT, Persistent, Eureka, M2 Source

Financial Services f Cognizant, Compunnel Software Group, Mastech Digital, Deloitte, Vak IT, Federal Soft Systems, Accenture

Financial Services f TCS, LTI, Infosys, Iris Software, Virtusa, NTT data Services, Accenture, Mitchell/Martin, Capgemini, Maveric, Incandescent Tech, Synechron Inc, Oracle Financial Services, E&Y, Photon

Logistics f Atos, Mphasis, HCLT, Deloitte, Sai Technology, KFORCE, Compunnel Software Group, Infogain, Vidorra

Financial Services f Atos, Maxima Consulting, Oracle Financial Services, Cognizant, TCS, Mastech Digital, IBM, Hexaware

Technology f TCS, SRS Consulting, LTI, Infosys, Zensar, Tech Mahindra, Accenture, Persistent, HCLT, Cognizant,Randstand Technology, Urpan Technology, Capgemini, Enquero, Onstak

Retail/Pharma f CGI Technologies, Cognizant, TCS, Accenture, Mastech, Randstad, Deloitte, Compunnel Software, EPAM, Mastech, Virtusa, Bradford

Technology f Deloitee, KFORCE, Mphasis, TCS, Infosys, Inspirisys, Accenture, Capgemini, Quest Global, Unique Key Resources, Adecco, System Soft Technologies, Softcom, ITC Infotech

Professional Services f Accenture, TCS, Randstad, Titan Data Group, Javen Technology, Mastech, Techvision, Javen Technology

Technology f HCLT, Zen3 Infosolutions, Infosys, Couloir, TCS, Cirquetech, Brillio, KFORCE, Accenture, Aricent Tech, Cognizant, Isite Technology, Lasai Technolgogies

Retail f KFORCE, Infosys, Cognizant, Populus, Centizen, Cloudwick, E&Y, Mastech, TCS, Centizen, Invincible Tech, Mavensoft

Financial Services f CSC, TechM, Compunnel Software Group, Mastech, Altimetrik, EPAM, High Quartile, KFORCE, EPAM, Cognizant

Automobile f L&T Infotech, L&T Technology, CSC Covansys, Delta Computer Consulting, Accenture, IBM, Mastech Digital, HCLT, Altair, Product design, Infosys, Cognizant

Financial Services f Capgemini, KFORCE, Cognizant, TCS, Xavient Digital, E&Y, CGI Technology, Conch Technology

Financial Services f Cognizant, Infosys, TCS, Hexaware, Mastech, Americcloud Solutions, Oracle Financial Services Software, Atos, Synopsis, E&Y, Compunnel Software Group, Virtusa, Innovative Consulting

Energy f Infosys, HCLT, NITCO, Conglomerate IT Services, E&Y, Genuine IT

Retail/Consumer Goods f TCS, Larsen & Toubro Infotech, Cognizant, IBM, deloitte, HCLT, Capgemini, Accenture, L&T Technology Services, I3 Infotech, Microexcel, BirlaSoft, TechMahindra

Financial Services f TCS, Cognizant, KFORCE, Mastech Digital, Federal Soft Systems, 8K Miles Health Cloud

Energy f L&T Infotech, Tech Mahindra, Accenture, L&T Technology Services, Compunnel Software Group, EPAM

Financial Services Cognizant, Accenture, Lucent Systems, TCS, IGate Solutions

Source: RSec Research, Department of Labour (US) ; Note: Grey highlight denotes common Top-20 client accounts for Top-4 IT names

18

Exhibit 40: HCLT's Top 20 US Clients

Clients Key Competition

Financial Services f KFORCE, TCS, Wipro, IBM, Mastech Digital, Compunnel Software Group, Daman, Populus Group, Inherent technologies

Pharmaceutical f Cognizant, Accenture, E&Y, deloitte, CGI Technologies, LS Solutions, Infosys, United Pharma Technology, White Collar Technologies, Mastech Digital, Compunnel Software Group

Technology f ETOUCH Systems, Deloitte, Accenture, HCLT, Tech Mahindra, EPAM, Infosys, IBM, Global Logic, KFORCE, TCS

Communication f Capgemini, HCLT, Infosys, Telecom Technology, Pro Karma, UST Global, Tech Democracy, Wipro, Accenture, NTT data, TCS, Amdocs, Compunnel Software Group

Industrial f Infosys, TCS, Accenture, Fujitsu America, Cyient, E&Y, Ruleware, Tech Mahindra, App Soft, TechMagix, Dotcom team

Logistics f Atos, Mphasis, Wipro, Deloitte, Sai Technology, KFORCE, Compunnel Software Group, Infogain, Vidorra

Beverage f E&Y, DEXTEROUSUSA, Altran, Anveta

Media & Entertainment f Accenture, Birlasoft, Cognizant, Capgemini, E&Y, Ciber, Info Services, Deloitte, Genpact, Globant, Affine, Everest

Industrial f L&T Technology Services, Quest Global, Einfochips, Compunnel Software Group, Cyient, Anventa, Blucapsoft, Caltek Solutions, Computer Professionals

Financial Services f Infosys, DXC, Luxoft, Accenture, TCS, Cira Infotech, Ikcon Technologies, Oracle Financial Services, Alttech, Ariston, Inficare

Healthcare f Capgemini, E&Y, Deloitee, Wipro, Horkus Solutions, Katalyst Helthcares

Finance f Capgemini, Incandescent Technologies

Healthcare f Capgemini, Indus USA, Cognizant, Geometric, I3 Infotech, Ilink Systems, Systechcorp

Technology f Zen3 Infosolutions, Infosys, Couloir, TCS, Wipro, Cirquetech, Brillio, KFORCE, Accenture, Aricent Tech, Cognizant, Isite Technology, Lasai Technologies

Healthcare f Cognizant, Capgemini, HCLT, IBM, I3 Infotek, The Fountain Group

Financial Services f TCS, Mphasis, Cognizant, Capgemini, E&Y, Accenture

Financial Services f Infosys, TCS, Hexaware, Cognizant, Photon, Procal Technologies

Technology f Infosys, Aricent, UST Global, Deloitte, L&T Technology, Cerium Systems, TCS, Wipro

Financial Services f Mastech Digital, TCS, Cognizant, I-Link Solutions, ASTA CRS, Astir IT Solutions, Compunnel Software Group, Iris Software

Financial Services f Infosys, Wipro, Deloitte, EPAM, Mastech, Cognizant, Softcom Systems, Cyberthink, Compunnel Software Group, Capgemini

Source for all : RSec Research, Department of Labour (US); Note: Grey highlight denotes common Top-20 client accounts for Top-4 IT names

V. Dovish Tone of New US Administration on Immigration - The Worst is OverWe highlight that the new US president has comparatively softer tone on immigration. President Biden has put most of hard Trump era rules on review. New administration has tabled ‘US Citizenship Act 2021’ in the both House and Senate, which proposes to (1) increase country quota of green card from 7% to 20%; and (2) issue H-4 work visas to spouses and children. Notably, any substantial easing of laws is not possible given divided house and senate.

Our View: The Indian IT companies are likely to continue the localization efforts (most of them have already in the range of 50-70%) to reduce medium-term visa dependency. On the other hand, the US technology unemployment remains substantially below its national average, which underscores the United States’ dependency on high skilled technology talent from abroad. While localization remains key part of Top-4 Indian IT companies, incremental spending is likely to be lower than past 2-3 years. Though the new US administration mulls easing STEM visa restrictions, we expect prevailing wage rate to go up.

19

Exhibit 41: New US President has comparatively softer tone on immigration

Topics Proposals

Naturalization of green card Restore and defend the naturalization process for green card holders. The Biden Administration will streamline and improve the naturalization process to make it more accessible to qualified green card holders. Biden will restore faith in the citizenship process by removing roadblocks to naturalization and obtaining the right to vote, addressing the application backlog by prioritizing the adjudication workstream and ensuring applications are processed quickly, and rejecting the imposition of unreasonable fees.

Reform temporary visa system

Biden will work with the Congress to reform temporary visas to establish a wage-based allocation process and establish enforcement mechanisms to ensure they are aligned with the labour market and not used to undermine wages. Then, Biden will support expanding the number of high-skilled visas and eliminating the limits on employment-based visas by country, which create long backlogs.

New Visa Categories Creating a new visa category to allow cities and counties to petition for higher levels of immigrants to support their growth. Biden will support a programme to allow any county/municipal executive of a large or midsize county/city to petition for additional immigrant visas to support the region’s economic development strategy, provided the employers in those regions certify there are available jobs and that there are no workers to fill them. Holders of these visas would be required to work and reside in the city/county that petitioned for them and would be subject to the same certification protections as other employment-based immigrants.

Rights of Immigrant workers Biden will work with Congress to ensure that the employers are not taking advantage of immigrant workers and that the US citizen workers are not being undercut by the employers. Biden will also work to ensure that the employers have the right tools to certify their workers’ employment status and will restore focus on abusive employers instead of on the vulnerable workers.

Source: President Biden’s Website, RSec Research

US Tech Services Unemployment Rate Remains Low vs. Elevated National Average: COVID-19 outbreak led to sharp slump in economic activities worldwide. In just few months, the US employment rate soared to 14.8% from 3.8% in Feb’20. According to Computing Technology Industry Association (CompTIA), unemployment rate for technology occupants remains low at 2.3%% in comparison to elevated national average (6.3%). Interestingly, the technology companies reduced their workforce in May’20, but non-tech employers across the US increased hiring of technology professionals. According to CompTIA, during past three years, tech services and custom software sector accounted for >75% of job gains in the tech industry. Talent demand in the field of IT infrastructure modernization, systems, data and cyber security is likely to remain robust.

Exhibit 42: US Technology unemployment remains low against national average

Source: CompTIA, Department of Labour, US

Exhibit 43: Indian IT names have more than 50% local staff in US office

Company Localization in US (%)

TCS >50

Infosys 61

Wipro 70

HCLT 68

Mindtree ~50

Source: Rsec Research

0

2

4

6

8

10

12

14

16

1-20

19

3-20

19

5-20

19

7-20

19

9-20

19

11-2

019

1-20

20

3-20

20

5-20

20

7-20

20

9-20

20

11-2

020

1-20

21

(%)

US Tech Unemployement US Unemployment

20

Expect Strong Profitability to Continue over FY21E-FY24EA. EBIT Margin Likely to Remain Elevated: During last three quarters, the Top-4 IT names have consistently exceeded street consensus driven by work from home operating model, lower travel and facility cost, controlled hiring with accelerated utilization. We expect the Top-4 IT names to report 50-310bps margin expansion in FY21E. Going ahead, while we forecast margin deceleration from the record 3QFY21 levels, profitability levels are likely to remain elevated vs. FY17-FY20 levels driven by: (1) improved operating leverage with accelerated double-digit topline; (2) rising share of high-margin digital services, which will constitute >50% of revenues; (3) hybrid working model, which is likely to stay with ambitious medium-term work from home plans by large IT names; and (4) automation and efficiency gains. There are clear margin headwinds i.e. (1) step-up in hiring and lower utilization from current peak levels; (2) resumption of partial travel and facility cost from 2HCY21; and (3) rise in attrition levels to pre-pandemic levels. Additionally, we expect the Top-4 IT names to consistently invest in talent, capabilities and sales and marketing teams to improve market positioning, as the demand environment continues to remain buoyant.

B. Flexible Hybrid Work Model Likely to be Future of Work: Multiple large US technology firms have committed permanent work from home for select roles and planning to move on to hybrid working model. Non-technologies companies from India and across globe are also planning to move some roles to remote working. Infosys and TCS have also set medium-term targets for flexible hybrid model. TCS has announced 25x25 work model, under which the company expects only 25% of employees need to work from office. Infosys too plans permanent work from home for 33-50% of workforce.

Additionally, according to PwC’s US Remote Work Survey – Jan 21, remote work has been an overwhelming success for both employees and employers. The shift in positive attitudes toward remote work is evident: 83% of employers now say the shift to remote work has been successful for their company, compared to 73% in June 2020 survey. This suggests increasing adoption of hybrid work model amongst the global enterprises.

Our View: We expect flexible hybrid work model to lead to lower facility and travel cost. Additionally, hybrid working model is likely to be preferred working model for the employees as well as the employers. Additionally, we expect hybrid working options to make Indian IT companies more attractive for innovation culture and talent retention.

Exhibit 44: Expect strong EBIT margin levels to continue (%)

Companies FY20 FY21E FY22E FY23E FY24E

TCS 24.6 25.1 25.8 26.1 26.1

Infosys 21.3 24.4 24.4 24.3 24.6

HCL Tech 19.6 21.2 20.4 20.2 20.2

Wipro 17.1 19.6 17.8 18.5 19.0

Source: RSec Research

Exhibit 45: Recurring PAT margin (%)

Companies FY20 FY21E FY22E FY23E FY24E

TCS 20.6 19.8 20.9 21.5 21.8

Infosys 18.3 19.4 19.9 20.0 20.2

HCL Tech 15.7 17.4 16.5 16.5 16.7

Wipro 15.9 17.1 15.4 15.9 16.4

Source: RSec Research

21

Exhibit 46: Employers Survey on Work from Home and Hybrid model Exhibit 47: Employees Survey on Work from Home and Hybrid model

Source: PwC’s US Remote Work Survey – Jan 21 Source: PwC’s US Remote Work Survey – Jan 21

Exhibit 48: Indian IT Names Plan for Medium Term Hybrid Delivery Model

Company Work from Home Plan

Infosys f Company plans permanent work from home for 33-50% of workforceTCS f Announced the 25x25 work model, through which only 25% of its employees will need to work from office by

2025Wipro f ~98% of employees are working from home. According to website, the company believes that with newer

advents in technology, it will only see the WFH population getting more empowered and robust.HCLT f Majority of employees are working from home with improved efficiency.Source: Rsec Research

C. High-margin Digital Biz & Automation Benefit to Aid on Cost Front: Digital business enjoys attractive pricing versus legacy business. Infosys management has highlighted that the IT services in digital space command pricing premium against legacy services. HCLT has also highlighted that gross profit from Mode 2 business are higher. We expect the IT services names to enjoy margin tailwind, as digital revenue share becomes dominant part of their total revenue. Additionally, they have also stepped up efforts on automation efforts with improved process and introduction of bots. During last three years, Infosys has repurposed >20,000 employees driven by automation efforts, which led to ~100-150bps annualized cost saving.

D. Depreciating INR – A Consistent Medium-term Tailwind: In last decade, INR depreciated against the USD by almost 50%. The INR depreciation was consistent in each year except for 2017. The Indian IT services companies bill their revenues predominantly in USD and majority cost centers are in INR. Amongst the Top-4 Indian IT names, Infosys and TCS have comparatively higher hedging in upcoming couple of quarters and they have higher sensitivity towards USD-INR movement. In general, 1% changes in USD-INR leads to 20-30bps impact on EBIT margin. On EPS front, 1% change in USD-INR leads to 1-1.5% change in earnings. We believe the IT companies are likely to enjoy consistent medium-term tailwind from INR depreciation.

Exhibit 49: INR Witnessed Consistent Depreciation against USD

Source: RSec Research

Exhibit 50: EBIT margin sensitivity for 1% USD INR Change (bps)

TCS 25-30

Infosys 25-30

Wipro 20-30

HCLT 20-30

Source: RSec Research

18.2

3.6

12.8

2.2

4.72.7

-6.0

8.9

2.5 2.5

-10

-5

0

5

10

15

20

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

(%)

Depreciation in INR

83%

11%

6%

Employers Opinions

Successful Mixed Results Unsuccessful

71%

23%

6%

Employees Opinions

Successful Mixed Results Unsuccessful

22

Accelerated Inorganic Acquisitions by Infosys & WiproHistorically, Accenture and Cognizant have put higher stress on inorganic capability building. Accenture has spent US$1.6bn on M&As in FY20. Accenture has closed >30 acquisitions in the areas of Cloud, data/AI, experience and cyber in CY20. As the technology adoption by global enterprise is on rise, we believe there is inherent limitation in developing capability with internal resources. Recently, Infosys and Wipro have stepped up capability-based acquisitions with focus on Cloud, Experience and partnership SaaS providers. Recently, Wipro acquired Capco, a financial services, which focused on consulting and IT services for $1.4bn. Infosys also spent ~$800mn on acquisitions and joint ventures during CY20. We expect the Indian IT firms need to accelerate inorganic capability building in line with global peers.

Exhibit 51: Indian IT names lag behind US peers on inorganic capability building

Source: RSec Research

23

Nifty IT Trades at 1-25% Discount to Nifty/NASDAQ; Growth Deserves Further ReratingCurrently, Nifty 1-year forward PE multiple stands at 27x, which is 1% discount to the broader market. Additionally, Nifty IT is trading at 25% discount to NASDAQ, which witnessed substantial multiple rerating (~45% premium) compared to S&P-500 owing to disruption by large technology firms. Further, Nifty IT traded at 10-30% premium over broader market during FY10-FY14 when IT names were reporting double digit growth. Looking ahead, we expect Nifty IT to trade at premium to broader index driven by: (1) double-digit revenue growth expectation over FY21E-FY24E and medium-term growth resiliency due to increasing technology adoption; (2) increasing collaboration with large hypersclaers and SaaS companies; and (3) peer set companies (with ~15% revenue growth) are trading at higher multiple.

Exhibit 52: Currently, Nifty IT 12M forward PE trades at 1% discount to Nifty vs. historical peak premium of 40-60%

Source: RSec Research, Bloomberg

Exhibit 53: However, NASDAQ (US Technology Index) 12M forward PE trades at 45% premium to S&P500

Source: RSec Research, Bloomberg

A. IT Industry Embraces Features of Consumer Industry, which Deserves Multiple Re-Rating: We believe the IT industry is embracing more consumer industry like features i.e. growth resiliency, consistency in business cycle, stable EBIT margin and strong cash flow conversation. Currently, Nifty Consumer index trades at 100% premium to Nifty IT and Nifty. We expect Nifty IT to deserve premium multiple on the back of strong EPS expectation over FY21E-FY24E.

-30

-20

-10

0

10

20

30

40

50

60

70

01-0

7

07-0

7

01-0

8

07-0

8

01-0

9

07-0

9

01-10

07-1

0

01-11

07-1

1

01-12

07-1

2

01-13

07-1

3

01-14

07-1

4

01-15

07-1

5

01-16

07-1

6

01-17

07-1

7

01-18

07-1

8

01-19

07-1

9

01-2

0

07-2

0

01-2

1

(%)

Nifty IT vs Nifty premium/(discount) Last 10 Yr Average Last 5 Yr Average

0

10

20

30

40

50

60

70

80

01-0

7

08-0

7

03-0

8

10-0

8

05-0

9

12-0

9

07-10

02-11

09-11

04-12 11-12

06-13

01-14

08-14

03-15

10-15

05-16

12-16

07-17

02-18

09-18

04-19 11-19

06-2

0

01-2

1

(%)

NASDAQ vs S&P premium/(discount) Last 10 Yr Average Last 5 Yr Average

24

0

20

40

60

80

100

120

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar

-17

Jun-

17

Sep-

17

Dec

-17

Mar

-18

Jun-

18

Sep-

18

Dec

-18

Mar

-19

Jun-

19

Sep-

19

Dec

-19

Mar

-20

Jun-

20

Sep-

20

Dec

-20

Nifty Consumer Index- 1 YR FWD Nifty 50 1 YR FWD

B. Low Discount Rate & Attractive Dividend Yield to Support Valuation: Additionally, one more variable, which we believe supports premium valuation is low US interest yield rate. The US Fed remains committed to keep the rates at low levels. Additionally, the Indian IT names have consistent cash return policies and dividend yield that generally remains at 3-4%, which make IT sector much more attractive.

Exhibit 56 : US bond yields remains well below historical average Exhibit 57: Top-4 India IT names - dividend yield

Source: RSec Research, Bloomberg Source: RSec Research

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

10 year US bond Yield 5 year average 10 year average

Exhibit 54: Nifty Consumer Index 12 Month FWD PE enjoys considerable premium over broad based index due to growth resiliency and consistency across business cycle

Exhibit 55: Top-4 IT names deserve multiple re-rating as IT industry embracing more consumer industry like features

Source: RSec Research, Bloomberg Source: RSec Research, Bloomberg

C. Indian IT Names Lead in Brand Value Perception: According Brand Finance, brand value of the Indian companies has increased considerably in 2021. Leading the pack in Top-10 was Infosys followed by HCL Technologies. Accenture retained the title of world’s most valuable and trusted IT brand. TCS gained 11% in brand value, while IBM lost 24%. With 19% gain in brand value, Infosys entered the Big 4 of IT services club globally and the fastest growing brand in the Top-10.

According to Brand Finance, the COVID-19 pandemic has transformed the IT services landscape, accelerating change across the sectors by 3-5 years. Those brands, which were able and ready to quickly shift from purely operating as service providers to consulting and transformation partners have been reaping the benefits in the face of adversity. The large contract wins for IT services brands in Europe in the last year mark the beginning of a trend, which we expect to continue, going forward. Our analysis suggests that the strongest brands will capture the lion’s share of this expected growth. Higher brand value suggests improving market perception for the top IT names, which should reflect in higher market share, improved customer/employee satisfaction and higher valuation multiple, going forward.

HULGilletteBritania

Nestle

Asian Paints

EPAM

Colgate

TCSInfosysWiproHCLT

8

18

28

38

48

58

68

78

0 5 10 15 20 25 30

FY24

PE (x

)

FY21-FY24E EPS CAGR (%)

2.93.1

3.4

1.9

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

TCS Infosys HCL Tech Wipro

(%)(%

)

25

Exhibit 58: Top-4 Indian IT names lead in brand value perception

Ranking 2021

Ranking 2020

Name Brand Value 2021($mn)

Brand Value 2020 ($mn)

% YoY

change

1 1 Accenture 26,028 25,294 2.9

2 2 IBM (IT Services) 16,057 21,188 (24.2)

3 3 TCS 14,924 13,499 10.6

4 5 Infosys 8,402 7,087 18.6

5 4 Cognizant 8,032 8,573 (6.3)

6 6 Capgemini 6,750 6,630 1.8

7 9 HCL 5,524 4,889 13.0

8 8 Ntt Data 5,081 5,058 0.5

9 10 Wipro 4,301 4,324 (0.5)

10 11 Samsung SDS 3,693 3,695 (0.1)

Source: Brand Finance, RSec Research

Revenues INR mn

RSec Consensus Delta (%)

FY22E FY23E FY24E FY22E FY23E FY24E FY22E FY23E FY24E

TCS 18,94,520 21,35,089 23,99,003 18,67,834 20,84,489 23,65,068 1.4 2.4 1.4

Infosys 11,80,257 13,42,789 15,03,340 11,56,773 12,99,278 14,36,436 2.0 3.3 4.7

HCLT 8,58,313 9,67,190 10,79,027 8,51,335 9,44,333 10,53,899 0.8 2.4 2.4

Wipro 7,22,507 8,10,897 8,89,804 7,01,154 7,68,187 8,29,642 3.0 5.6 7.3

EBIT margin (%)

RSec Consensus Delta (bp)

FY22E FY23E FY24E FY22E FY23E FY24E FY22E FY23E FY24E

TCS 25.8 26.1 26.1 26.2 26.4 26.4 (46) (25) (22)

Infosys 24.4 24.3 24.6 24.0 24.1 24.1 39 17 48

HCLT 20.4 20.2 20.2 21.3 21.2 21.2 (86) (104) (104)

Wipro 17.8 18.5 19.0 18.4 18.6 18.6 (69) (8) 42

Exhibit 59: RSec vs. Consensus

EPS (Rs)

RSec Consensus Delta (%)

FY22E FY23E FY24E FY22E FY23E FY24E FY22E FY23E FY24E

TCS 105.7 122.3 139.4 105.8 118.0 136.2 (0.1) 3.7 2.3

Infosys 55.3 63.2 71.4 52.8 59.6 64.5 4.8 5.9 10.8

HCLT 52.3 58.8 66.3 53.1 59.2 65.1 (1.6) (0.6) 1.9

Wipro 19.5 22.6 25.8 20.3 22.5 24.5 (3.9) 0.7 5.2

Source: RSec Research

26

Exhibit 60: IT Services Comparison Sheet

Revenue Growth (US$) (%) EBIT margin (%) PE (x) RoE (%)

Stocks Price (Rs/US$)

Mcap US$bn

FY22E FY23E FY24E FY22E FY23E FY24E FY22E FY23E FY24E FY22E FY23E FY24E

TCS 3,172 157.3 15.8 11.2 10.9 25.8 26.1 26.1 30.0 25.9 22.8 45.8 44.1 41.8

Infosys 1,387 77.7 17.4 12.3 10.5 24.4 24.3 24.6 25.1 22.0 19.4 31.5 31.7 31.5

HCLT 995 36.1 14.0 11.2 10.1 20.4 20.2 20.2 19.0 16.9 15.0 22.5 22.3 22.1

Wipro 420 32.4 17.7 11.0 8.5 17.8 18.5 19.0 21.5 18.6 16.3 14.2 14.6 15.7

Tech Mahindra# 1,016 13.1 11.3 9.7 8.4 13.7 15.0 15.0 18.8 15.7 12.8 18.4 19.6 20.3

Average of Top-5 Indian IT names

15.2 11.1 9.7 20.4 20.8 21.0 29.3 25.5 22.3 26.5 26.5 26.3

Accenture* 280 186.0 7.7 7.1 7.5 15.2 15.4 15.4 29.8 27.0 25.1 29.7 29.1 30.8

Cognizant* 78 42.1 6.7 5.6 6.8 14.5 15.3 15.3 21.4 19.6 17.8 14.8 17.3 16.7

EPAM* 388 21.8 24.8 22.6 27.7 17.4 17.7 19.4 52.4 42.0 33.5 19.4 20.2 20.2

Average of US based IT names

13.1 11.8 14.0 15.7 16.1 16.7 34.5 29.6 25.5 21.3 22.2 22.6

Global IT Average 14.4 11.3 11.3 18.6 19.1 19.4 31.3 27.0 23.5 24.5 24.9 24.9Source: RSec Research; Note: # In case of Tech Mahindra, we have used consensus estimates for FY24E; *Bloomberg consensus estimates over FY22-FY24E

27

Exhibit 62: Comparative Analysis - HCLT & Wipro

HCLT Wipro

Financials (Rs Mn) FY20 FY21E FY22E FY23E FY24E FY20 FY21E FY22E FY23E FY24E

Revenues 7,06,780 7,54,112 8,58,313 9,67,190 10,79,027 6,10,232 6,12,005 7,22,507 8,10,897 8,89,804EBIT 1,38,530 1,59,546 1,75,096 1,95,372 2,17,964 1,05,031 1,14,753 1,28,303 1,49,929 1,69,018

Adj PAT 1,11,080 1,32,066 1,41,520 1,59,182 1,79,645 96,985 98,776 1,11,273 1,28,879 1,46,794

Growth (%)

Revenues 15.1 2.4 14.0 11.2 10.1 4.2 0.3 18.1 12.2 9.7EBIT 17.2 15.2 9.7 11.6 11.6 2.5 9.3 11.8 16.9 12.7Adj PAT 11.5 18.9 7.2 12.5 12.9 5.8 1.8 12.7 15.8 13.9

Margin (%)

EBIT 19.6 21.2 20.4 20.2 20.2 17.2 18.8 17.8 18.5 19.0Adj PAT 15.7 17.5 16.5 16.5 16.6 15.9 16.1 15.4 15.9 16.5Per Share (RS)

EPS 41.0 48.7 52.4 58.9 66.4 16.5 18.3 19.5 22.6 25.7DPS 5.0 20.0 24.0 28.0 32.0 1.0 2.0 4.0 6.0 8.0Book value 180.8 218.1 246.0 280.3 318.4 95.4 113.9 129.4 146.0 163.7Valuation (x)

P/E 24.3 20.5 19.0 16.9 15.0 25.4 22.9 21.5 18.6 16.3EV/EBIT 16.7 14.1 13.0 12.0 11.0 20.7 18.7 16.6 14.8 13.8P/BV 5.5 4.6 4.0 3.6 3.1 4.4 3.7 3.2 2.9 2.6Div Yield (%) 0.5 2.0 2.4 2.8 3.2 0.2 0.5 1.0 1.4 1.9Return Ratio (%)

RoCE (%) 22.0 22.4 20.9 20.9 20.9 17.3 16.0 15.0 15.4 15.6RoE (%) 24.1 24.3 22.5 22.3 22.1 16.1 15.1 14.2 14.6 15.7Source: Company, RSec Research

Exhibit 61: Comparative Analysis - TCS & Infosys

TCS Infosys

Financials (Rs Mn) FY20 FY21E FY22E FY23E FY24E FY20 FY21E FY22E FY23E FY24E

Revenues 15,69,490 16,41,676 18,94,520 21,35,089 23,99,003 9,07,910 10,10,910 11,80,257 13,42,789 15,03,340EBIT 3,85,800 4,11,870 4,88,192 5,57,668 6,27,250 1,93,740 2,46,376 2,88,008 3,26,138 3,69,828

Adj PAT 3,23,400 3,24,888 3,96,566 4,59,051 5,23,166 1,65,950 1,95,684 2,34,771 2,68,005 3,02,999

Growth (%)

Revenues 5.4 0.4 15.8 11.2 10.9 8.3 6.3 17.4 12.3 10.5EBIT 3.0 6.8 18.5 14.2 12.5 2.6 27.2 16.9 13.2 13.4Adj PAT 2.8 0.5 22.1 15.8 14.0 7.7 17.9 20.0 14.2 13.1

Margin (%)

EBIT 24.6 25.1 25.8 26.1 26.1 21.3 24.4 24.4 24.3 24.6Adj PAT 20.6 19.8 20.9 21.5 21.8 18.3 19.4 19.9 20.0 20.2Per Share (RS)

EPS 61.4 66.7 67.5 83.0 86.2 39.0 46.1 55.3 63.2 71.4DPS 73.0 58.0 65.0 70.0 80.0 17.5 30.0 33.0 38.0 42.0Book value 219.7 204.7 244.5 295.8 354.0 150.4 160.1 181.9 206.4 235.1Valuation (x)

P/E 36.8 36.6 30.0 25.9 22.8 35.6 30.1 25.1 22.0 19.4EV/EBIT 29.3 27.0 23.3 20.8 18.7 27.9 22.1 19.4 17.5 15.8P/BV 13.7 15.1 12.6 10.5 8.7 9.0 8.4 7.4 6.5 5.8Div Yield (%) 2.3 1.8 2.0 2.2 2.5 1.3 2.2 2.4 2.7 3.0Return Ratio (%)

RoCE (%) 38.3 40.8 46.8 44.9 42.5 23.0 23.0 23.0 23.0 23.0RoE (%) 36.6 39.2 45.8 44.1 41.8 25.4 28.9 31.5 31.7 31.5Source: Company, RSec Research

28

Channel Check Takeaways f COVID-19 pandemic has accelerated the demand for transformation services. The

enterprises, which have invested in IT ecosystem ahead of others, have performed better than others during the pandemic period. Amid multiple technology disruptions, adoption of new business model remains the primary objective of global enterprises.

f The enterprises are moving from current 20% share of Cloud to 80%. According to multiple industry experts, Cloud opportunity varies between US$500mn-1bn. IT services companies have set up their dedicated team with individual Cloud platforms.