Impact of IFRSs on the Mining Industry

James Saloman, PricewaterhouseCoopers LLPMike Moretto, BC Securities Commission

IFRS for The Mining Industry

Objective

• Provide a high-level awareness of general and key issues

• Focus on junior and mid-size entities

• This isn’t a substitute for reading the standards

2

IFRS for The Mining Industry

Myths and Realities

• Transition will be easy!

• Transition will be difficult!

• This isn’t as challenging as it is for some sectors, e.g. banking, insurance, oil and gas

• IFRS resources are scarce and everyone needs them

• Everyone should have an outside advisor

• The IASB’s Extractive Activities project will affect transition

3

IFRS for The Mining Industry

IFRS 1, First-time Adoption of IFRS• First reporting is in Q1 2011 with a need for

comparative information

• Date of transition is January 1, 2010 for a calendar year company

• General principle is that standards effective at December 31, 2011 have to be applied for all periods presented and retroactively

(continued)

4

IFRS for The Mining Industry

IFRS 1, First-time Adoption of IFRS (continued)

• There is lots of relief from the general principle, e.g. can elect to use fair value as “deemed cost” at date of transition

• The deemed cost election can mitigate issues related to component accounting and impairment

• Reconciliations are required from Canadian GAAP to IFRS

5

IFRS for The Mining Industry

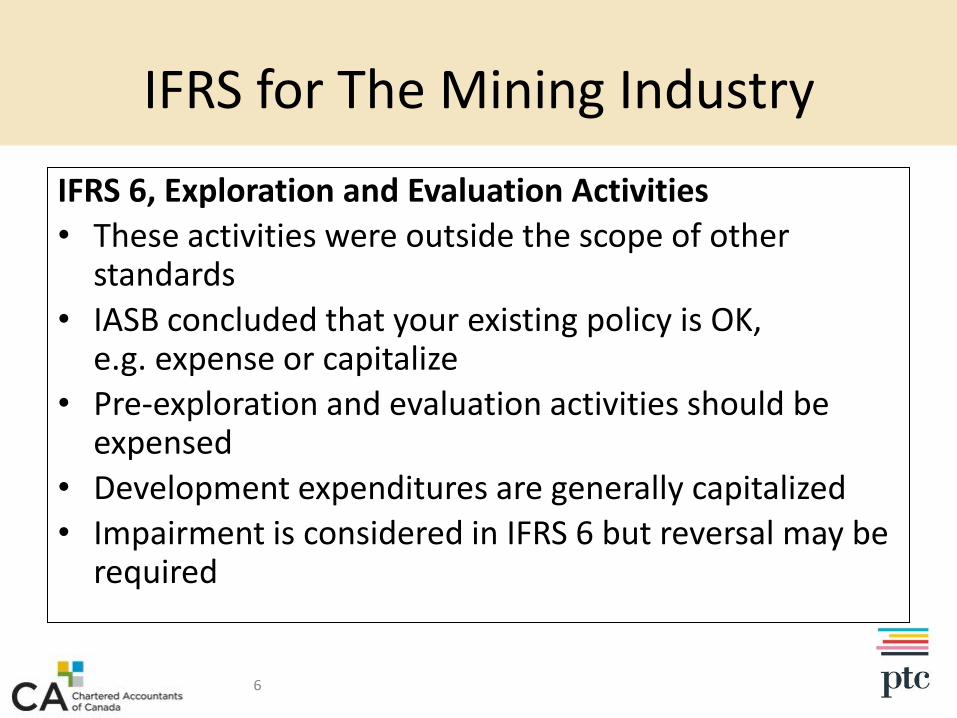

IFRS 6, Exploration and Evaluation Activities

• These activities were outside the scope of other standards

• IASB concluded that your existing policy is OK,e.g. expense or capitalize

• Pre-exploration and evaluation activities should be expensed

• Development expenditures are generally capitalized

• Impairment is considered in IFRS 6 but reversal may be required

6

IFRS for The Mining Industry

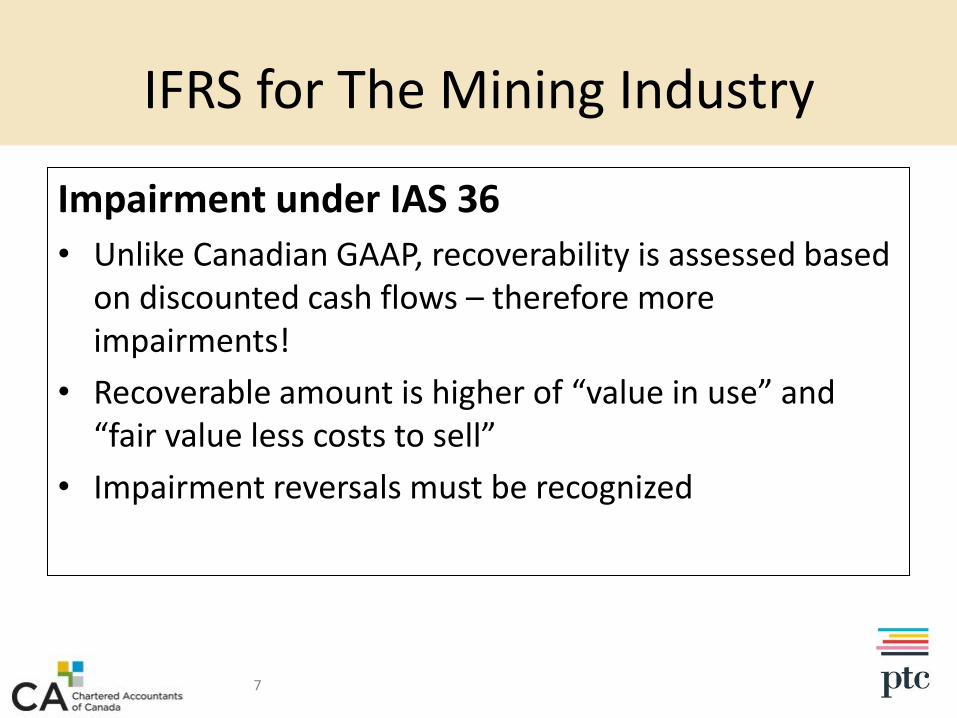

Impairment under IAS 36

• Unlike Canadian GAAP, recoverability is assessed based on discounted cash flows – therefore more impairments!

• Recoverable amount is higher of “value in use” and “fair value less costs to sell”

• Impairment reversals must be recognized

7

IFRS for The Mining Industry

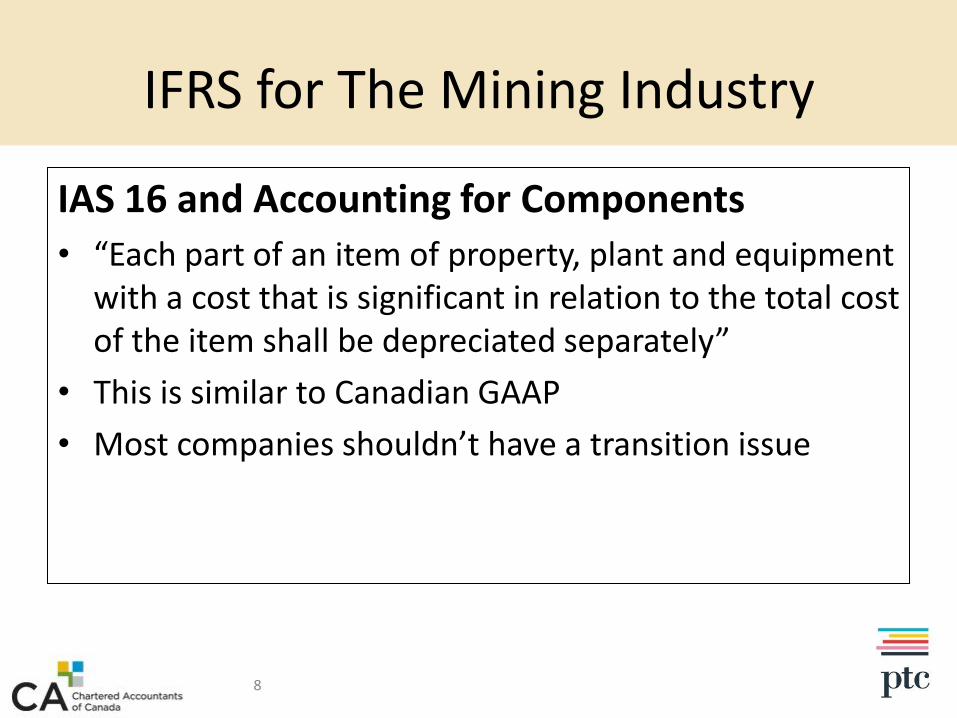

IAS 16 and Accounting for Components

• “Each part of an item of property, plant and equipment with a cost that is significant in relation to the total cost of the item shall be depreciated separately”

• This is similar to Canadian GAAP

• Most companies shouldn’t have a transition issue

8

IFRS for The Mining Industry

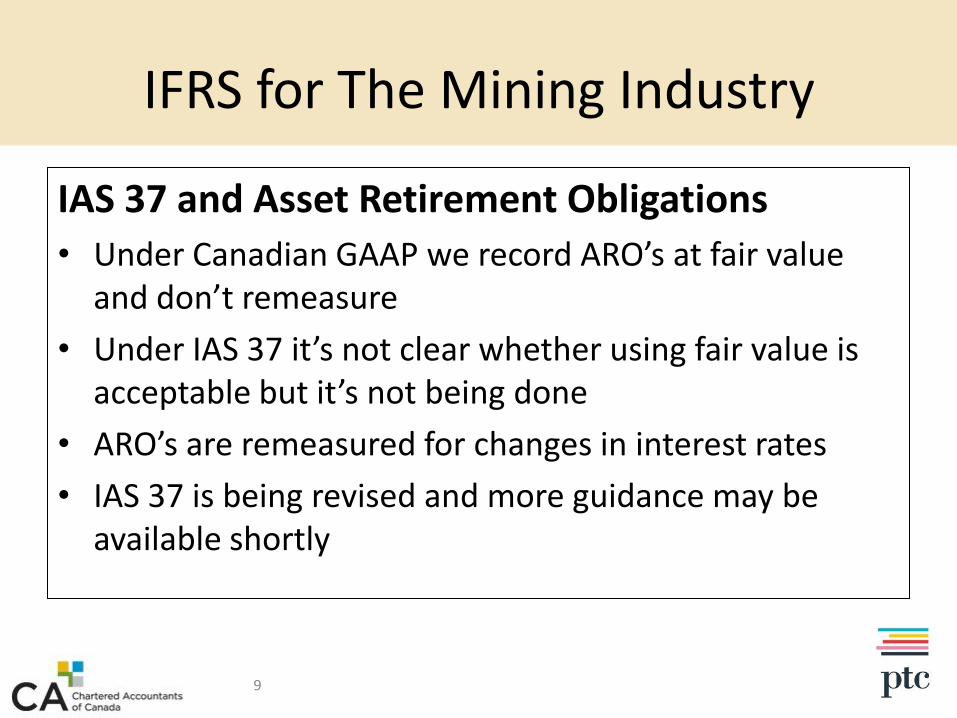

IAS 37 and Asset Retirement Obligations

• Under Canadian GAAP we record ARO’s at fair value and don’t remeasure

• Under IAS 37 it’s not clear whether using fair value is acceptable but it’s not being done

• ARO’s are remeasured for changes in interest rates

• IAS 37 is being revised and more guidance may be available shortly

9

IFRS for The Mining Industry

Final Thoughts

• Expense exploration and evaluation costs and you may be done

• Using fair value as deemed cost may be appealing

• Good luck!

10

And now the views of the regulator…..

11

Regulatory Update on IFRS Issues

• IFRS adoption – timing issues• MD&A disclosure of expected changes• Interim financial statements in the year of IFRS

adoption• 1st annual IFRS financial statements• ‘Old’ Canadian GAAP and IFRS – different principles for

different periods?• Changes to securities rules and policies• Early adoption?

12

IFRS adoption – timing issues

• The train has left the station - CSA fully supports Canada’s move to IFRS, including the January 1, 2011 transition date

• Change is coming - CSA rules and policies are being revised to reflect the transition to IFRS

• An ounce of prevention - Issuers should plan for filing challenges during the first half of 2011

13

IFRS adoption – timing issues

Filing challenges during the first half of 2011

• 2010 annual filings – “old” Canadian GAAP

MD&A – disclosure re IFRS changes

• First interims in 2011 – IFRS

transition date balance sheet

restated comparatives

extensive disclosure

certification implications

14

MD&A disclosure of expected changes

• MD&A requires discussion and analysis of any change in accounting policy, including

description of the new accounting standard

methods of adoption

expected effects on the issuer’s F/S

potential effects on the issuer’s business

15

MD&A disclosure of expected changes

• Incremental approach for disclosure in years prior to changeover

Staff Notice 52-320 Disclosure of expected changes in accounting policies relating to changeover to IFRS

published May 9, 2008

Other useful guidance published by Canadian Performance Reporting Board (CPRB) of the CICA (2008)

16

Two years before changeover (2009)

IFRS changeover plan

• key elements and timing - 2008 MD&A

• 2009 MD&A discuss progress regarding

Accounting policies, choices, decisions

IT and data systems

Internal control over financial reporting

Disclosure controls & procedures

Financial reporting expertise

Business activities affected by accounting metrics17

MD&A disclosure of expected changes

Two years before changeover (2009) cont’d

Major identified differences between the issuer’s current accounting policies and those under IFRS

May be narrative description only

Consider IFRS as at the MD&A date; may also consider IASB projects in-process

18

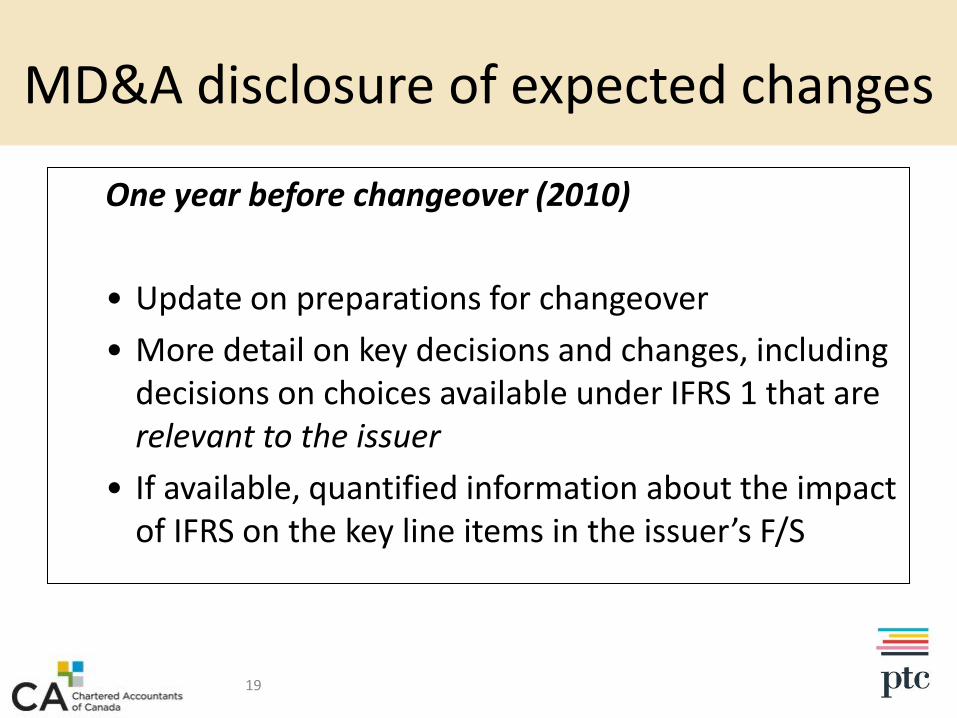

MD&A disclosure of expected changes

One year before changeover (2010)

• Update on preparations for changeover

• More detail on key decisions and changes, including decisions on choices available under IFRS 1 that are relevant to the issuer

• If available, quantified information about the impact of IFRS on the key line items in the issuer’s F/S

19

MD&A disclosure of expected changes

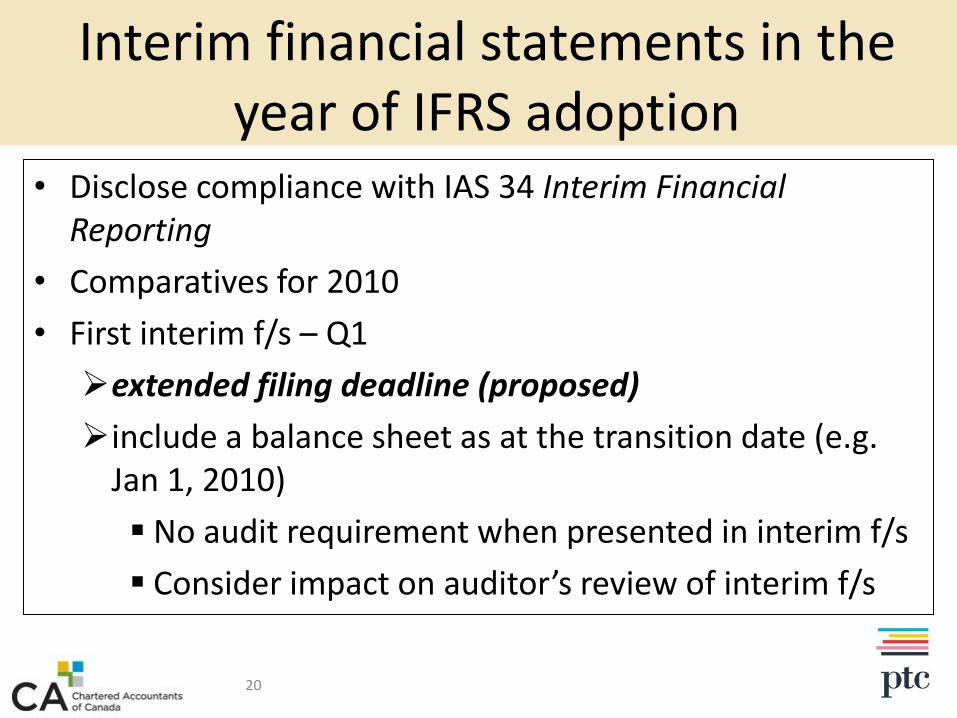

Interim financial statements in the year of IFRS adoption

• Disclose compliance with IAS 34 Interim Financial Reporting

• Comparatives for 2010

• First interim f/s – Q1

extended filing deadline (proposed)

include a balance sheet as at the transition date (e.g. Jan 1, 2010)

No audit requirement when presented in interim f/s

Consider impact on auditor’s review of interim f/s

20

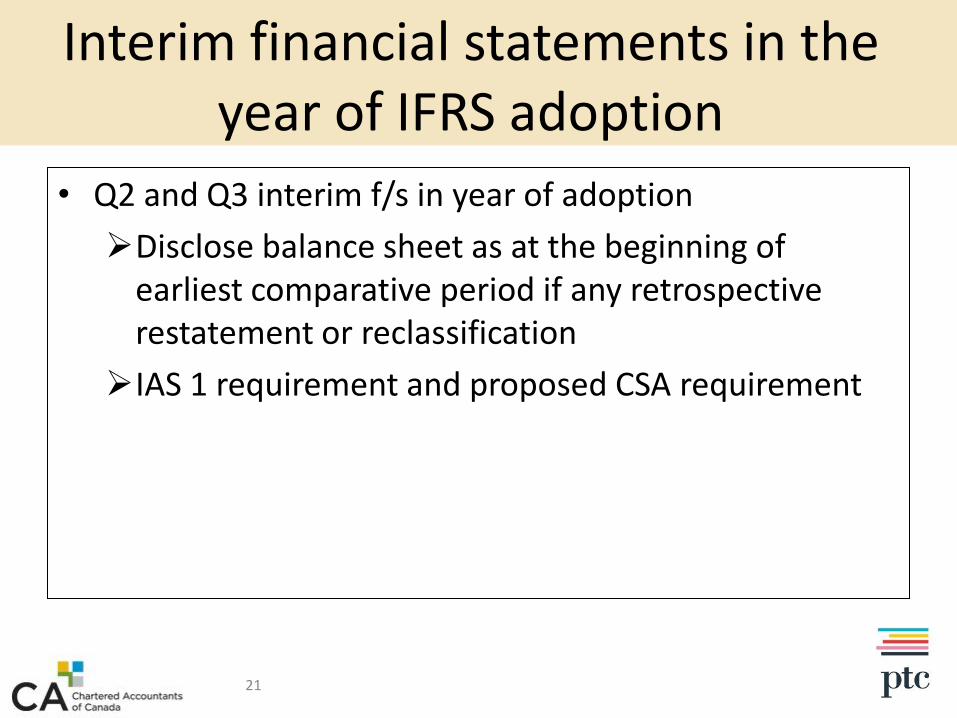

Interim financial statements in the year of IFRS adoption

• Q2 and Q3 interim f/s in year of adoption

Disclose balance sheet as at the beginning of earliest comparative period if any retrospective restatement or reclassification

IAS 1 requirement and proposed CSA requirement

21

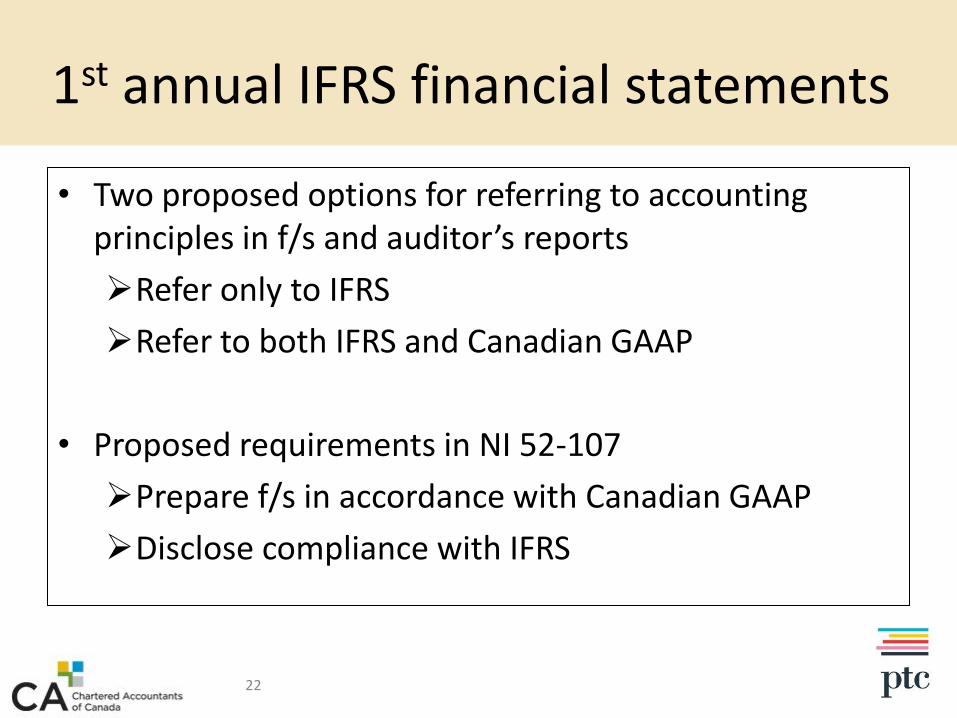

1st annual IFRS financial statements

• Two proposed options for referring to accounting principles in f/s and auditor’s reports

Refer only to IFRS

Refer to both IFRS and Canadian GAAP

• Proposed requirements in NI 52-107

Prepare f/s in accordance with Canadian GAAP

Disclose compliance with IFRS

22

1st annual IFRS financial statements

• Transition date balance sheet and related reconciliation information – IFRS 1

• MD&A discussion of changes in accounting policies

• Certification implications

23

‘Old’ Canadian GAAP and IFRS – different principles for different periods?

• Existing requirement for all periods presented in f/s to be prepared in accordance with the same accounting principles

• Proposed relief for earliest of three years (subject to specified conditions)

• A document may include f/s for pre 2011 periods in “old” Canadian GAAP and f/s for 2011 in IFRS

24

Changes to securities rules and policies - IFRS

• Changes to NI 52-107 Acceptable Accounting Principles, Auditing Standards and Reporting Currency IFRS terminology and transition issues transition to International Standards of Auditing

(ISA)• Changes to other national rules and policies for

terminology and transition issuesContinuous disclosure ProspectusNon-GAAP measuresRegistrants Investment funds

25

Early adoption?

• Domestic issuers may apply for exemptive relief to use IFRS before 2011 – see CSA Staff Notice 52-324

• Exemptive relief required for periods beginning before January 1, 2011 even once IFRS is incorporated into the Handbook

• IFRS interim f/s required in year of adoption

26

Early adoption?

• Early adopters should consider

Readiness of staff, directors, audit committee, auditors, & investors

Impact on obligations under securities legislation including those relating to:

Certifications

Business acquisition reports

Offering documents

Forward-looking information

27

Resources

• All instruments and notices referred to in this presentation are available on the BCSC website at www.bcsc.bc.ca

• Other commissions– Ontario Securities Commission www.osc.gov.on.ca– Alberta Securities Commission www.albertasecurities.com– Autorité des marchés financiers www.lautorite.qc.ca

• CICA IFRS Transition Resources at www.cica.ca/ifrs

• CICA IFRS Education and Training at www.cica.ca/ifrseducation

• IASB webpage www.iasb.org

28

Contact information

James Saloman, CA, CPA, FCA Partner, PricewaterhouseCoopers LLP(email) [email protected]

Mike Moretto, CA, CPA (Illinois)Manager, Corporate FinanceBritish Columbia Securities Commission(email) [email protected]

29

Questions

Questions and Answers

30

Recommended