Guide to business in Spain

Spain profile

Ñ1

Spain is in an outstanding position worldwide in terms ofthe importance of its economy: the 9th largest economyin the world by GDP, the 6th largest receiver of foreigndirect investment (FDI), the 8th largest issuer of FDI andthe 7th largest exporter of commercial services. What’smore, two of the three most prestigious rating agencies inthe world (Fitch and Moody´s) have given Spain their topscore in 2010.

Spain has a modern economy based on knowledge, inwhich services represent 71.09% of business activity. It isan international center for innovation that benefits from ayoung and highly qualified population of a proactivenature, and competitive costs, especially as regardsgraduate and post-graduate employees.

The country has worked hard to equip itself with state-ofthe-art infrastructures capable of fostering the futuregrowth of the economy. And this has been done alongsidea major commitment to R&D. Public spending in this fieldhas increased by a factor of 2.2 since 2004.

There are interesting business opportunities for foreigninvestors in Spain in high value-added and strategic fieldswith a huge potential for future growth such as the ICT,renewable energy, biotechnology, environment,aerospace and automotive sectors, because of theattractive competitive environment.

And in addition to gaining access to the Spanish nationalmarket, an attractively large market of nearly 47 millionconsumers with a high purchasing power, companies canalso gain access to the markets of the EMEA region(Europe, Middle East and North Africa), and especially tothose of Latin America, as a consequence of the prestigeand strong presence of Spanish companies in theseregions.

The main characteristics of our country are described inthis chapter: demographics, political and territorialstructure, economy and the foreign trade sector.

Guide to business in SpainSpain profile2

1. Introduction

2. The country, its people and quality of life

3. Spain and the European Union

4. Infrastructure

5. Economic overview

6. Domestic market

7. Foreign trade and investment

8. Legislation on foreign investment and

exchange control regulations

3

4

9

11

15

17

18

21

Guide to business in Spain

Spain profile

Ñ1

Guide to business in SpainSpain profile3

1. Introduction

1. INTRODUCTION

Spain is one of the most significant economies in the world: 9th in terms of size and an attractive

destination for foreign investment, making Spain the 6th largest recipient of FDI worldwide1. Spain’s

appeal for foreign investment lies not only in its domestic market, with its high purchasing power, but

also in the possibility of operating with third markets from Spain. This is so because Spain offers a

privileged geo-strategic position within the European Union giving access to over 1,700 million

potential clients in the EMEA Region (Europe, Middle East and Africa). Its strong economic, historic

and cultural ties also make Spain the perfect gateway to Latin America.

Furthermore, Spain is a modern knowledge-based economy with services accounting for 71.09

percent of economic activity. The country has become a center of innovation supported by a young,

highly-qualified work force and competitive costs in the context of Western Europe.

This chapter gives a brief description of Spain’s vital statistics - the latest facts and figures which

explain the demographics, the political framework and the economic structure of the country.

1 “World Investment Report 2009” (2008 figures)

Guide to business in SpainSpain profile4

2. THE COUNTRY, ITS PEOPLE AND QUALITY OF LIFE

2.1 Geography, climate and living conditions

The Kingdom of Spain occupies an area of 504,782 square kilometers in the southwest of Europe,

and is the second largest country in the EU. The territory of Spain covers most of the Iberian

Peninsula, which it shares with Portugal, and also includes the Balearic Islands in the Mediterranean

Sea, the Canary Islands in the Atlantic Ocean, the North African cities of Ceuta and Melilla and some

surrounding rocky islands.

Despite the differences among the various regions of Spain, the country can be said to have a typical

Mediterranean climate. The weather in the northern coastal region (looking onto the Atlantic and

the Bay of Biscay) is mild and generally rainy throughout the year, with temperatures neither very low

in the winter nor very high in the summer. The climate on the Mediterranean coastline, including the

Balearic Islands, Ceuta and Melilla, is mild in the winter and hot and dry in the summer. The most

extreme differences occur in the interior of the Peninsula, where the climate is rather dry, with cold

winters and hot summers. The Canary Islands have a climate of their own, with temperatures

constantly around 20 Celsius degrees and only minor variations in temperature between seasons or

between day and night.

Spain has an excellent quality of life and is very open to foreigners. More than 10,000 kilometers of

coastline, abundant sporting facilities and events and social opportunities are crowned by the

diversity of the country’s cultural heritage as a crossroads of civilizations (Celts, Romans, Visigoths,

Arabs, Jews, etc.).

Galicia

Asturias Cantabria PaísVasco

La Rioja

Navarra

Castilla y León

Extremadura

Andalucía

Castilla - La Mancha

Comunidad de Madrid

Aragón

Cataluña

Murcia

ComunidadValenciana

Canarias

Baleares

FRANCE

PORTUGAL

MORROCO

La Coruña

Santiago de Compostela Lugo

Orense

OviedoSantander

León

Palencia

Valladolid

Segovia

Ávila

Soria

Logroño

Vitoria

Pamplona

Huesca

Zaragoza

Lérida

Tarragona

Castellón de la Plana

Valencia

Alicante

Murcia

Albacete

Cuenca

Madrid

Toledo

Cáceres

Mérida

Córdoba

Sevilla

Huelva

Cádiz

Ceuta

Málaga

Granada

Jaén

Almería

Melilla

BadajozCiudad Real

Guadalajara

Palma De Mallorca

Barcelona

Gerona

Teruel

BilbaoSan Sebastián

Salamanca

Burgos

Zamora

Pontevedra

Las Palmas de Gran Canaria

Santa Cruz de Tenerife

2. The country, its people and quality of life

Guide to business in SpainSpain profile5

Spanish is the official language of the country. There are other Spanish languages that are also

official in the corresponding Autonomous Communities (regions), according to their “Statutes of

Autonomy”. Education is compulsory until the age of 16 and English is the main foreign language

studied at school.

Spain has a labor force of 22.9 million people, representing 59.76% of the country’s population over

16 years old according to the Labor Force Survey (released in the fourth quarter 2009). Compared

with other OECD countries, Spain’s population is relatively young: 15.5% is under 16 years old, 67.8%

is between 16 and 64 years old, and only 16.7% is 65 and over, according to year 2009 figures.

Additionally, as seen in Table 2 below, Spain has been receiving a significant inflow of immigrants in

recent years that has offset the consequences of an aging population.

2.2 Population and human resources

The population of Spain in 2009 was 46.7 million people, with a population density of more than

92.60 inhabitants per square kilometer.

Spain is a markedly urban society (see Table 1), as evidenced by the fact that more than 32% of the

population lives in the capitals of the provinces.

Table 1

THE BIGGEST CITIES IN SPAIN*

POPULATION

Madrid 3,255,944Barcelona 1,621,537Valencia 814,208Sevilla 703,206Zaragoza 674,317Málaga 568,305Murcia 436,870

Palma de Mallorca 401,270Las Palmas de Gran Canaria 381,847Bilbao 354,860

* Figures refer only to the municipal district of each city.

Source: Report about population in Spanish cities at January 1, 2009. Official State Gazette.

Guide to business in SpainSpain profile6

2007 2008 2009

Europe 1,661,636 1,917,069 2,007,633America 1,234,688 1,354,158 1,479,014Asia 238,740 270,210 299,743Africa 841,561 922,635 944,696Oceania 1,989 1,839 1,903Unknown 1,130 7,588 8,243TOTAL 3,979,744 4,473,499 4,791,232

Source: Ministerio de Trabajo y Asuntos Sociales (Ministry of Labour and Social Affairs)2.

Data at December 31, 2009.

2 www.mtas.es

Table 2

FOREIGNERS RESIDENT IN SPAIN BY CONTINENT OF ORIGIN

Spain’s labor force structure by economic sector underwent significant changes sometime ago, with a

noteworthy increase in the working population employed in the services industry and a drop in the

number of people working in agriculture and industry (Chart 1 and Table 3).

The labor force is highly qualified, productive and capable of adapting to technological changes.

Lastly, in keeping with the commitment entered into with the European Union to promote job

creation, the Spanish government has implemented significant changes to the job market since the

mid-nineties, introducing a greater degree of flexibility in employment. Nevertheless, as a result of

the current global economic crisis, the significant migratory flow received by our country over the last

decade, and the change in the Spanish economy, which has moved away from labor-intensive sectors

towards sectors involving new technologies, the unemployment rate in Spain has increased

significantly.

As a result, the government prepared an ambitious Economic and Employment Stimulus Plan, called

Plan E. This Plan combines short-term fiscal stimulus measures with measures aimed at supporting

demand and making structural reforms, which will serve to enhance the competitiveness of the

Spanish productive system.

The economic effort linked to this Plan is very significant, accounting for approximately 2% of GDP in

2009 and are focused on supporting employment, mainly through the Local Investment Fund, on

reducing taxes for businesses and families and on increasing access to financing through the Official

Credit Institute (ICO). Also, in coordination with other Member States, measures have been

implemented to provide support to hard-hit industries, such as the automotive, and more recently

tourism, sectors.

In addition, the Spanish Government has approved the Preliminary Sustainable Economy Bill as part

of its strategy to change Spain’s economic model with a view to boosting competitiveness,

Guide to business in SpainSpain profile7

Chart 1

LABOR FORCE STRUCTURE BYECONOMIC SECTOR IN 2009

Source: Instituto Nacional de Estadística

(National Statistics Institute)

Services

Construction

Industry

Agriculture

4%

14%

10% 72%

2007 2008 2009

Agriculture 4.4 4.0 4.2Industry 16.0 15.3 14.4Construction 13.1 11.0 9.7Services 66.4 69.7 71.7

Source: Instituto Nacional de Estadística (National Statistic Institute). Labor Force Survey, 4Q of 2009.

Table 3

EVOLUTION OF LABOR FORCE STRUCTURE BY ECONOMIC SECTOR (Percentage)

strengthening financial oversight, combating payment delinquency, increasing transparency in

relation to compensation at listed companies and facilitating public-private procurement. This Bill

forms part of a strategy the main objective of which is to lay the foundations for a more sustainable

development and growth model for the Spanish economy. This strategy also includes a capital fund

of €20 billion, managed by the Official Credit Institute, as well as a program of structural reforms

with a 10-year horizon.

At the local level, the Government has approved a new State Fund for Employment and Local

Sustainability, which gives continuity to the State Fund of Local Investment that began to operate in

2009. The new investment program, funded with a budget of €95.3 million, places the emphasis

this time on promoting initiatives aimed at environmental conservation, savings, energy efficiency,

new technologies and local services.

Guide to business in SpainSpain profile8

3 www.casareal.es4 www.poderjudicial.es5 www.congreso.es6 www.la-moncloa.es

2.3 Political institutions

Spain is a parliamentary monarchy. The King is the Head of State3 and his primary mission is to

arbitrate and moderate the regular functioning of the country’s institutions in accordance with the

Constitution. He also formally ratifies the appointment or designation of the highest holders of public

office in the legislative, executive and judicial branches4.

The Constitution of 1978 enshrined the fundamental civil rights and public freedoms as well as

assigning legislative power to the Cortes Generales (Parliament)5, executive power to the

Government of the nation, and judicial powers to independent judges and magistrates.

The responsibility for enacting laws is entrusted to the Cortes Generales, comprising the Congreso de

los Diputados (Lower House of Parliament) and the Senado (Senate), the members of which are

elected by universal suffrage every four years.

The Cortes Generales exercise the legislative power of the nation, approve the annual State budgets,

control the actions of the Government and ratify international treaties.

The Government6 is headed by the Presidente del Gobierno (President of the Government) who is

elected by the Cortes Generales and is, in turn, in charge of electing the members of the Consejo de

Ministros (Council of Ministers).

The members of the Council of Ministers are appointed and removed by the President of the

Government at his or her discretion. For administrative purposes, Spain is organized into 17

Autonomous Communities (Regions) each of which generally comprises one or more provinces, plus

the Autonomous Cities of Ceuta and Melilla in Northern Africa; the total number of provinces is 50.

Each Autonomous Community (Region) exercises the powers assigned to it by the Constitution as

specified in its “Statute of Autonomy”. These Statutes also stipulate the institutional organization of

the Community concerned, consisting generally of: a legislative assembly elected by universal

suffrage, which enacts legislation applicable in the Community; a Government with executive and

administrative functions, headed by a President elected by the Assembly, who is the Community’s

highest representative; and a Superior Court of Justice, in which judicial power in the Community’s

territory is vested. A Delegate appointed by the Central Government directs the Administration of the

State in the Autonomous Community (Region), and co-ordinates it with the Community’s

administration.

The Autonomous Communities (Regions) are financially autonomous and also receive allocations

from the general State budgets.

As a result of the structure described above Spain has become one of the most decentralized

countries in Europe.

Guide to business in SpainSpain profile9

3. SPAIN AND THE EUROPEAN UNION

Spain became a full member of the European Economic Community in 1986. Therefore, EU

legislation is fully applicable in Spain. In this connection and according to figures published by the

European Commission, Spain fully complies with the objectives established by the European Council

and has implemented 3,000 Directives into national law.

A major impact of European Union membership for Spain, and for the other Member States, came in

the mid-nineties with the advent of the European Single Market and the European Economic Area,

which created a genuine barrier-free trading space.

Since then, the EU has advanced significantly in the process of unification by strengthening the

political and social ties among its citizens. Spain, throughout all this process, has always stood out as

one of the leaders in the implementation of liberalization measures.

Since January 1, 2007, with the addition of Rumania and Bulgaria, the European Union membership

now stands at 277.

With the aim of strengthening democracy, efficiency and transparency within the EU and, in turn, its

ability to meet global challenges such as climate change, security, and sustainable development, the

27 EU Member States gathered together on December 13, 2007, to sign the Treaty of Lisbon, which

entered into force – subject to prior ratification by each of the 27 member states – on December 1,

2009. Previously, between June 4 and 7 the European Parliament elections took place8.

Spain holds significant responsibilities within the EU, evidenced by the fact that it is, along with

Poland, the fifth country in terms of voting power in the Council of Ministers. Currently of note is the

fact that Spain has assumed the Council Presidency of the European Union for the fourth time and

for the period running from January to June 2010.

The introduction of the Euro (on January 1, 2002) heralded the start of the third Spanish presidency

of the European Council and represented the culmination of a long process and the opening-up of a

veritable array of opportunities for growth for Spanish and European markets. Since January 1, 2009,

with the addition of Slovakia, Euro Zone membership now stands at sixteen.

The euro has led to the creation of a single currency area within the EU that makes up the world’s

largest business area, bringing about the integration of the financial markets and economic policies

of the area’s member states, strengthening ties between the member states’ tax systems and

bolstering the stability of the European Union.

Furthermore, the adoption of a single European currency has had a clear impact at an international

level, raising the profile of the Euro-Zone at both international and financial gatherings (G-7

meetings) and within multilateral organizations. The economic and business stability offered by the

3. Spain and the European Union

7 www.mae.es8 http://europa.eu

Guide to business in SpainSpain profile10

9 Annual Report of Progress 2009-PEIT

euro have been contributing to the growth of the Spanish economy, as well as its international

political standing.

Spain is the EU member state that has received the most structural and cohesion funds, which have

been put to use to finance infrastructure and development projects. Indeed, it is estimated that

between 2007 and 2013, Spain is set to receive upwards of €31.5 billion in the guise of various

structural and cohesion funds, making it the EU’s second largest recipient of such funds, second only

to Poland.

Under the decisions adopted by the Council of Europe in London in 2005, Spain was also awarded a

special €2-billion allowance set aside for R&D activities, with which the government, in partnership

with the private sector, has set in motion initiatives in this area to co-finance. Noteworthy among

such initiatives was the launch of Programa Ingenio 2010 in a bid, essentially, to reach a situation in

which public and private investment in R&D&I accounts for 2% of GNP by 2010. In this connection,

the initial results of Programa Ingenio 2010, released in 2008, reveal that R&D investment

accounted for 1.2% of GNP in 2006 (representing the largest increase since 1991), while business

investment in this area reached 0.67% of GNP.

The Government’s determination to boost investment in R&D&I is evidenced by the fact that in the

2004-2009 period, the Central Government’s budget for civil R&D&I nearly tripled, surpassing €8.2

billion in 2009, a particularly significant increase within the context of the budgetary constraints

brought about by the current economic situation. If the extraordinary items from Plan E are also

taken into account, the total funds devoted in 2009 to civil R&D&I amount to €8.69 billion, 12%

more than in 2008.

In addition, to improve business competitiveness, in 2009 the Interempresas program was created

with both domestic (€36.5 million) and international (€10 million) components aimed at co-

financing R&D&I projects undertaken by companies, mainly small and medium-sized, in the Health

and Energy industries9.

Guide to business in SpainSpain profile11

4. Infrastructure

4. INFRASTRUCTURE

The Government intends to continue with its program of heavy investment in this area in the future, as is

borne out by the Strategic Infrastructure and Transport Plan, which plans to make a total investment of over

€248 billion in the period 2005-202010. In this regard, with accumulated investment of over €62 billion,

more than 25% of the Plan has been executed in the 4 years that it has existed, thereby exceeding its

objectives both in terms of the total executed and the percentage of GDP of such execution. Railway

transportation takes center stage in the Plan, accounting for almost 50% of the total investment.

The motorway and dual carriageway network, of nearly 14,000 kilometers, has undergone constant

renovation with a view to enhancing its efficiency. The Government’s investment package means that

Spain will be able to call on a wide-reaching motorway and dual carriageway network, granting

direct access to all Spaniards and meaning that 94% of the population is never more than 30

kilometers from a high capacity road. With this in mind, 1,500 kilometers of motorway are expected

to enter into service during the period 2008-2012, with work underway on a further 1,600

kilometers. According to data as of March 31, 2009, 1,564 kilometers of motorways and dual

carriageways are under construction or under tender.

As far as railway transport is concerned (where Spain has a network of over 15,000 kilometers), high-

speed networks have become one of the top priorities in the Government’s infrastructure plans, with

plans for a 10,000 kilometer network by 2020. Consequently, all Spanish cities will have direct access

to the network, and 90% of the country’s citizens will be less than 50 kilometers away from a station

on the network. In this regard, at the outset of 2008, the number of provinces already benefiting

from the existing high-speed infrastructure was 33, covering 63.8% of the total surface area of Spain

and some 73% of the country’s total population.

Moreover, Madrid will be connected by high-speed train to the French border, via Zaragoza (Aragón),

Barcelona (Cataluña) and via Vitoria and Irún (the Basque Country). As things stand, Madrid already

has high-speed train connections to numerous Spanish cities via the following lines: 1) Madrid-

Seville; 2) Madrid-Zaragoza-Huesca; 3) Madrid-Zaragoza-Camp de Tarragona-Barcelona; 4) Madrid-

Malaga; and 5) Madrid-Segovia-Valladolid. In addition, as of March 31, 2009, 2,199 kilometers are

under construction or under tender, thus enabling 1,300 kilometers of high-speed lines to be put into

service during the 2008-2012 period, including the high speed Barcelona-Gerona, Madrid-Valencia

and La Coruña-Pontevedra-Vigo connections, to name but a few.

Finally, it is worth noting the freight sector liberalization since January 2005, which has led to the creation

of private enterprises that transport goods by railway. The ultimate aim is to encourage the

transportation of goods by railway in general, with a view to reducing the costs of the Spanish industrial

sector, increasing the energy efficiency of transportation and reducing greenhouse gas emissions.

Air transport links up the main Spanish cities and, with approximately 250 airlines operating out of

the country’s 49 airports, Spain is connected to the world’s leading cities. Spain is a major hub for

10 www.mfom.es

Guide to business in SpainSpain profile12

lines linking the Americas and Africa to Europe. Thus, the most significant investments in the pipeline

are aimed at the two principal international airports in Madrid and Barcelona. With the inauguration

of Terminal 4 in February 2006, Madrid’s airport saw its capacity increase to 70 million passengers

per year, having been recognized in 2008 as the world’s eleventh largest airport (by passenger

footfall) by the Airport Council International. Elsewhere, investment in the Barcelona airport will

enable capacity to be increased up to 70 million passengers per year. In line with the 2005-2020

Strategic Infrastructure and Transport Plan, the “Plan Canarias” has been launched, paving the way

for an investment of almost €3 billion in Canary Islands airports11.

Furthermore, with over 53 international ports on the Atlantic and Mediterranean coasts, Spain can

boast excellent maritime transport links. The Strategic Infrastructure and Transport Plan forecasts an

increase of up to 75% in the capacity of Spanish ports, cementing their position as intermodal hubs by

2020. Specifically, during the period 2008-2012 it will increase in the capacity of sheltered water,

docking space and land surface area by 7, 26 and 30%, respectively. In addition, 2009 will see the start-

up of the first two Seaside Motorways between the ports of Algeciras, Vigo and Gijón, and those of

Nantes-Saint Nazaire and Le Havre in France. Negotiations have begun with the Italian Government for

a similar process. This will permit a more sustainable alternative in some of the main flows with the EU.

In addition, with a view to improving the competitiveness of ports, the Spanish Parliament is working on

a new Ports Law that will reduce restrictions on inter- and intra-port competition.

Spain is well equipped in terms of technological and industrial infrastructure, having seen a boom in

recent years in technological parks in the leading industrial areas, as well as around universities and

R&D centers. There are currently 79 technological parks12 (32 of which are now fully operational)

housing over 4,500 companies, mainly engaged in the telecommunications and IT industries, in

which a large number of workers are employed in R&D activities.

€9,271 million has been budgeted for R&D&I for 2010.

As mentioned before, with a view to achieving new goals, the government has created the new

INGENIO 2010 Program.

Spain can also boast a solid telecommunications network, with an extensive conventional fiber optic

cable network (64,000 km) covering the country almost in its entirety, on top of one of the world’s

largest undersea cable networks and satellite link-ups spanning the five continents. Particularly

noteworthy is the significant deregulation set in place some years ago in the majority of industries,

the telecommunications industry included, meeting the deadlines set for such purpose by the EU

with ease. Among other advantages, this deregulation has meant a more competitive range of

products on offer as borne out by costs, essential for economic development.

Last, it is worth noting the significant investments made in hydraulic infrastructures, which have

improved the possibility of guaranteed water availability.

11 www.aena.es (press release)12 www.apte.org

Guide to business in SpainSpain profile13

ROAD NETWORK

RAILWAYS

Galicia

AsturiasCantabria País

Vasco

La Rioja

Navarra

Castilla y León

Extremadura

Andalucía

Castilla - La Mancha

Comunidad de Madrid

Aragón

Cataluña

Murcia

ComunidadValenciana

Canarias

Baleares

FRANCE

PORTUGAL

MORROCO

Freeways

Freeways in construction

Freeways of toll

Other main highways

La Coruña

Santiago de Compostela

Lugo

Orense

Oviedo

Santander

LeónPalencia

Valladolid

Segovia

Ávila

Soria

Logroño

Vitoria

Pamplona

Huesca

ZaragozaLérida

Tarragona

Castellón de la Plana

Valencia

Alicante

Murcia

Albacete

Cuenca

Madrid

ToledoCáceres

Mérida

Córdoba

Sevilla

Huelva

Cádiz

Ceuta

Málaga

Granada

Jaén

Almería

Melilla

BadajozCiudad Real

Guadalajara

Palma de Mallorca

Barcelona

Gerona

Teruel

BilbaoSan Sebastián

Salamanca

Burgos

Zamora

Pontevedra

Las Palmas de Gran Canaria

Santa Cruz de Tenerife

Galicia

AsturiasCantabria País

Vasco

La Rioja

Navarra

Castilla y León

Extremadura

Andalucía

Castilla - La Mancha

Comunidad de Madrid

Aragón

Cataluña

Murcia

ComunidadValenciana

Canarias

Baleares

FRANCE

PORTUGAL

MORROCO

High speed (more than 250 km/hour)

High planned speed

High speed in construction

Fast line (more than 200 km/hour)

Long distance rail routes

La Coruña

Santiago de Compostela

Lugo

Orense

Oviedo

Santander

LeónPalencia

Valladolid

Segovia

Ávila

Soria

Logroño

Vitoria

Pamplona

Huesca

ZaragozaLérida

Tarragona

Castellón de la Plana

Valencia

Alicante

Murcia

Albacete

Cuenca

Madrid

ToledoCáceres

Mérida

Córdoba

Sevilla

Huelva

Cádiz

Ceuta

Málaga

Granada

Jaén

Almería

Melilla

BadajozCiudad Real

Guadalajara

Palma de Mallorca

Barcelona

Gerona

Teruel

BilbaoSan Sebastián

Salamanca

Burgos

Zamora

Pontevedra

Las Palmas de Gran Canaria

Santa Cruz de Tenerife

Guide to business in SpainSpain profile14

PORTS

AIRPORTS

Galicia

AsturiasCantabria País

Vasco

La Rioja

Navarra

Castilla y León

Extremadura

Andalucía

Castilla - La Mancha

Comunidad de Madrid

Aragón

Cataluña

Murcia

ComunidadValenciana

Canarias

Baleares

FRANCE

PORTUGAL

MORROCO

Main ports

Bahía de Cádiz

Bahía de Algeciras

Málaga Motril Almería

Cartagena

Alicante

Valencia

Castellón

TarragonaBarcelona

Pasajes

BilbaoSantanderGijónAvilésFerrol-San Cimbrao

La Coruña

Vilagarcía

Marín- Pontevedra

Vigo

Baleares

Ceuta

Santa Cruz de Tenerife

Las Palmas

Melilla

Huelva

La Coruña

Santiago de Compostela

Lugo

Orense

Oviedo Santander

LeónPalencia

Valladolid

Segovia

Ávila

Soria

Logroño

Vitoria

Pamplona

Huesca

ZaragozaLérida

Tarragona

Castellón de la Plana

Valencia

Alicante

Murcia

Albacete

Cuenca

Madrid

ToledoCáceres

Mérida

Córdoba

SevillaHuelva

Cádiz

Ceuta

Málaga Granada

Jaén

Almería

Melilla

BadajozCiudad Real

Guadalajara

Palma de Mallorca

Barcelona

Gerona

Teruel

BilbaoSan Sebastián

Salamanca

Burgos

Zamora

Pontevedra

Las Palmas de Gran Canaria

Santa Cruz de Tenerife

Galicia

AsturiasCantabria País

Vasco

La Rioja

Navarra

Castilla y León

Extremadura

Andalucía

Castilla - La Mancha

Comunidad de Madrid

Aragón

Cataluña

Murcia

ComunidadValenciana

Canarias

Baleares

FRANCE

PORTUGAL

MORROCO

Madrid/Barajas

Salamanca

León Burgos

Valladolid

LogroñoPamplona

Zaragoza

Valencia

Alicante

Murcia/San Javier

Almería

Granada

CórdobaSevilla

Badajoz

JerezMálaga

Melilla

Huesca

Reus Barcelona

Sabadell

Gerona

San SebastiánBilbao

Vitoria

SantanderAvilés

La Coruña

Santiago

Vigo

Madrid/Torrejón

Madrid/Cuatro Vientos

AlbaceteIbiza

Menorca

Palma de Mallorca

International Airports

Control centers of Navigation

National Airports

Tenerife Sur

Tenerife Norte

Gran Canaria

Fuerteventura

El Hierro

La Gomera

La Coruña

Santiago de Compostela

Lugo

Orense

Oviedo

Santander

León

Palencia

Valladolid

Segovia

Ávila

Soria

Logroño

Vitoria

Pamplona

Huesca

ZaragozaLérida

Tarragona

Castellón de la Plana

Valencia

Alicante

Murcia

Albacete

Cuenca

Madrid

ToledoCáceres

Mérida

Córdoba

SevillaHuelva

Cádiz

Ceuta

Málaga

Granada

Jaén

Almería

Melilla

BadajozCiudad Real

Guadalajara

Palma de Mallorca

Barcelona

Gerona

Teruel

BilbaoSan Sebastián

Salamanca

Burgos

Zamora

Pontevedra

Las Palmas de Gran Canaria

Santa Cruz de Tenerife

Guide to business in SpainSpain profile15

5. Economic overview

2007 2008 2009

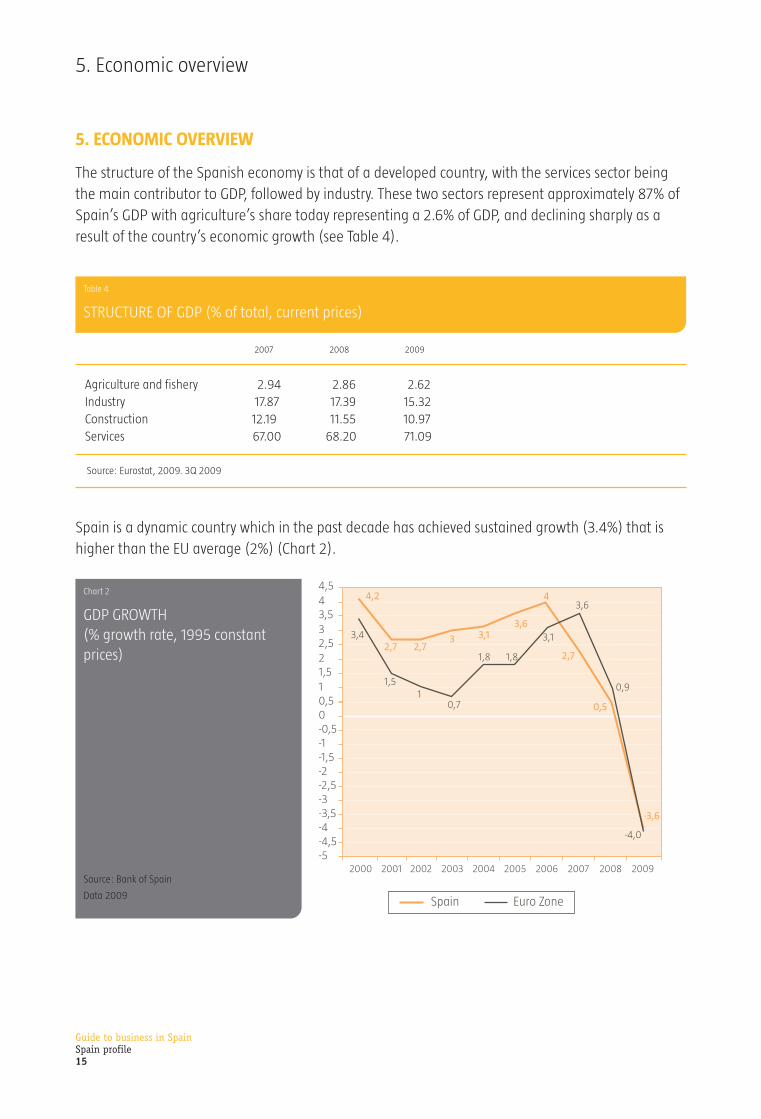

Agriculture and fishery 2.94 2.86 2.62Industry 17.87 17.39 15.32Construction 12.19 11.55 10.97Services 67.00 68.20 71.09

Source: Eurostat, 2009. 3Q 2009

5. ECONOMIC OVERVIEW

The structure of the Spanish economy is that of a developed country, with the services sector being

the main contributor to GDP, followed by industry. These two sectors represent approximately 87% of

Spain’s GDP with agriculture’s share today representing a 2.6% of GDP, and declining sharply as a

result of the country’s economic growth (see Table 4).

Table 4

STRUCTURE OF GDP (% of total, current prices)

Spain is a dynamic country which in the past decade has achieved sustained growth (3.4%) that is

higher than the EU average (2%) (Chart 2).

Chart 2

GDP GROWTH(% growth rate, 1995 constantprices)

Source: Bank of Spain

Data 2009 Spain Euro Zone

4,2

2,7 2,73 3,1

3,63,4

1,51

0,7

1,8

11,522,533,544,5

2000 2001 2002 2003 2004 2005 2006

3,1

4

2007

2,7

3,6

2008

0,5

0,9

1,8

0,50-0,5-1-1,5-2-2,5-3-3,5-4-4,5-5

2009

-3,6

-4,0

Guide to business in SpainSpain profile16

However, since August 2007 we have been immerse in an international crisis which has grown

gradually worse and has spread around the world until becoming a global crisis. In this respect, the

prudent budgetary policy followed in Spain in recent years (with a ratio of government debt to GDP

that is 20 points below the European average) permits the pursuit of counter-cyclical and structural

policies aimed at favoring an economic model based on growth offered by new sectors located

higher up in the value chain, such as renewable energy, biotechnology or information technologies

and telecommunications.

Moreover, inflation in Spain has slowly fallen since the end of the 1980s. Average inflation between

1987 and 1992 was 5.8%; it dropped below 5% for the first time in 1993, and it has been shrinking

progressively since then. The year-on-year inflation rate for 2009 was 0.8%.

Table 5

GROWTH FOR OECD COUNTRIES (Percentages)

Real GDP Growth

2007 2008 2009

EU countriesGermany 2.6 1 -4.9France 2.3 0.3 -2.2Italy 1.5 -1 -4.9United Kingdom 2.6 0.5 -4.8Spain 3.6 0.9 -3.6Other countriesUnited States 2.1 0.4 -2.4Japan 2.3 -1.2 …Total Euro Zone 2.7 0.5 -4.0Total OCDE 2.7 0.5 …

Source: Banco de España (Bank of Spain). Data 2009

Guide to business in SpainSpain profile17

6. DOMESTIC MARKET

The growth of the Spanish economy in recent years has been driven by strong demand and a

substantial expansion of production in the context of an increasingly open economy.

Today Spain has a domestic market of 46.7 million people with a per capita income (ppp) of 23,874

by INE for the year 2008, and an additional injection of demand coming from the 52.2 million

tourists13 who visit the country every year. The close links with Latin America and North Africa and the

obvious advantages of using Spain as a gateway to those countries are worthy of mention.

Table 6 reflects the evolution of production and demand components. The slowdown in the Spanish

economy’s growth has been due to a drop-off in domestic demand and private consumption,

alongside a sharp reduction in external demand. Moreover, the only element of domestic demand

that showed a slight decline was final consumption.

6. Domestic market

Table 6

GROWTH OF PRODUCTION AND DEMANDCOMPONENTS (Percentages)

2008 2009

Production componentsAgriculture and fishery -0.8 -2.4Industry -2.1 -14.7Energy 1.9 -8.2Construction -1.3 -6.3Services 2.2 -1Demand componentsPrivate consumption -0.6 -4.8Public consumption 5.4 3.8Gross fixed capital formation -4.4 -15.3Domestic demand -0.5 -6Exports of goods and services -1.0 -11.5Imports of goods and services -4.9 -17.9

Source: Banco de España (Bank of Spain). (Data 2009)

13 www.iet.tourspain.es. (Data January-December 2009)

Guide to business in SpainSpain profile18

7. Foreign trade and investment

Table 7

DISTRIBUTION OF EXPORTS AND IMPORTS 2009*(as a % of total)

Exports Imports

Capital goods 20.4% Capital goods 20.6%Automobile industry 17.6% Energy products 16.2%Food 15.6% Chemical products 15.6%Chemical products 14.6% Automobile industry 12.5%Semi-manufactured non-chemical products 11.3% Food 11.1%Consumer goods 9.3% Consumer goods 10.9%Energy products 4.5% Semi-manufactured non-chemical products 6.9%Other goods 2.7% Durable consumer goods 3.1%Durable consumer goods 2.1% Raw materials 2.7%Raw materials 1.9% Other goods 0.4%

Source: Ministerio de Industria, Turismo y Comercio (Ministry of Industry, Tourism and Trade).

* Data available for the period January-November 2009

14 WTO “International Trade Statistics 2009” report.15 Annual data published by the Spanish Ministry of Industry, Tourism andTrade.

7. FOREIGN TRADE AND INVESTMENT

In recent years, rapid growth in international trade and foreign investments has made Spain one of

the most internationally-oriented countries in the world.

With regard to the trading of goods, Spain is ranked 17th in the world as an exporter and 12th as an

importer; while in the trading of services it occupies 7th place as an exporter and 9th place as an

importer14.

The share of Spanish exports and imports of goods with respect to global figures amount to 1.7% and

2.4%, respectively. The share of exports and imports of services with respect to global figures stand at

3.8% and 3.0%.

The breakdown by industry of foreign trade is relatively diversified, as can be seen in the following

table:

As would be expected, the countries of the EU are Spain´s main trading partners. Accordingly, during

200915, Spanish exports to the European Union accounted for 69.3% of total exports and sales to the

Euro Zone 57.1% of the total. As for imports, those originating from the European Union accounted

for 58.3% of the total and those from the Euro Zone 48.1%.

Guide to business in SpainSpain profile19

Graph 3

FOREIGN INVESTMENT INSPAIN (1994-2009*)(Million euros)

*Data available for the period January-

September 2009.

Source: Registro de Inversiones

Exteriores Ministerio de Industria,

Turismo y Comercio. (Registry of Foreign

Investments. Ministry of Industry,

Tourism and Trade).

Specifically, Spain’s leading trade partners are France and Germany. Beyond the EU, of note are Asia

and Africa, which have displaced Latin and North America from their traditional role as Spain’s main

trade partners outside the EU.

As regards investment, Spain is positioned as one of the main recipients of investment worldwide.

Specifically, according to the UNCTAD, in 2008 Spain was the 6th largest recipient of foreign direct

investment in the world, 4th in the EU. Moreover, Spain is also one of the main foreign direct

investors in the world: $77 billion in 2008 for a rank of 8th largest investor worldwide16.

16 UNCTAD ”World Investment Report 2009” Report.

Gross investment Net investment

0

5.000

10.000

15.000

20.000

25.000

30.000

–5.000

2009

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Guide to business in SpainSpain profile20

2008 2009

I. Current account -97,786 -50,593Trade Balance -81,077 -41,733Services Balance 25,422 24,166Income -31,414 -24,652Net Current Transfers -10,717 -8,374II. Capital Account 5,297 3,159III. Financial Account 92,557 48,374Total (excluding Bank of Spain) 70,786 49,071Direct investment -4,597 -4,833Portfolio investment 6,064 47,031Other investment 76,953 11,929Financial derivatives -7,635 -5,056Bank of Spain 21,771 -697Reserves -473 -1,120Claims with the Eurosystem 23,185 -5,435Other net assets -942 5,858IV. Net errors & omissions -68 -940

(*) Data available for the period January-November 2008 and 2009.

N.B.: A positive sign in the current and capital accounts means a surplus (receipts greater than payments) and represents a net loan from Spain to

the rest of the world (increase in assets or decrease in liabilities), whereas in the financial account a positive sign means a net inflow of capital and

represents a net loan from the rest of the world to Spain. A negative sign in reserves means an increase.

Source: Banco de España (Bank of Spain)

Table 8

SPAIN’S BALANCE OF PAYMENTS* (Millions of euros)

As a summary of Spanish foreign trade, the balance of payments is attached.

Guide to business in SpainSpain profile21

8. LEGISLATION ON FOREIGN INVESTMENT AND EXCHANGE CONTROL REGULATIONS

This section covers the main aspects of the Spanish legislation on exchange control and foreign

investments. Although these areas are fully liberalized, there are specific reporting obligations to be

accomplished.

As a general rule, foreign investments are subject only to notification after the investment has been

made. Exchange controls and capital movements are fully liberalized and in all areas there is

complete freedom of action.

8.1 Legislation on foreign investment

Royal Decree 664/1999 deregulated practically all transactions of this kind (with the provisions and

exceptions set forth below), eliminating the requirement for “prior verification” and adapting

Spanish domestic law to the rules on the freedom of movement of capital contained in Articles 56 et

seq. of the Treaty of the European Union.

The most noteworthy aspects of the applicable rules are as follows:

• Foreign investments are, as a general rule, subject only to notification after the investment has

been made. The only exceptions are: (i) Investments from tax havens, which in general must be

notified beforehand, and (ii) foreign investments in activities directly related to national security,

and real estate investments for diplomatic missions by States that are not members of the

European Union and require “prior verification” from the Spanish Council of Ministers.

• There is no obligation for foreign investments to be formalized in the presence of a Spanish notary

public (unless specific legislation provides otherwise).

• Solely investments in the air transportation and radio industries, in industries relating to minerals

and raw mineral materials of strategic interest and mining rights, in the television, gaming,

telecommunications and private security industries, in industries concerned with the

manufacturing, marketing or distributing of arms and explosives for civilian use, and in national

security-related activities (these latter activities are subject to the clearance rules contained in the

Royal Decree), will be subject to the requirements imposed by the relevant body established by

industry-specific legislation.

8.1.1. Investors

Investors can be:

• Non-resident individuals (that is, Spanish nationals or foreigners domiciled abroad, or who have

their principal place of residence there).

• Legal entities whose registered offices are located abroad.

• Public agencies of foreign States.

8. Legislation on foreign Investment and exchange control regulations

Guide to business in SpainSpain profile22

A Spanish company in which foreign shareholders have a majority holding is not deemed to be an

investor. A change of registered office of legal entities or a change of residence of individuals is

enough to change the classification of an investment as a Spanish investment abroad or a foreign

investment in Spain.

8.1.2 Regulated Investments

Foreign investments in Spain, for the purpose of the obligation to report which is analyzed later,

could be carried out through any of the next operations:

• Participation in Spanish companies, including their incorporation and subscription and acquisition

of shares in corporations or the subscription of shares in limited liability companies, and any legal

transaction under which voting and other non financial rights are acquired.

• Establishment of and increase of capital allocated to branches.

• The subscription and acquisition of marketable debt securities issued by residents (debentures,

bonds, promissory notes).

• Participation in mutual funds recorded in the Registers of the Spanish National Securities Market

Commission17.

• The acquisition by non-residents of real estate located in Spain valued at more than €3,005,060,

or where the investment originates from a tax haven, whatever its amount.

• The formation, formalization or participation in joint ventures, foundations, economic interest

groupings, cooperatives and joint-property entities, with the same characteristics as in the

previous paragraph regarding the value of the investment.

Foreign investments not included in the above list (such as participating loans), are totally

deregulated, and no notice is required. Notwithstanding the foregoing, said investments may be

subject to industry-specific regulations and the rules on exchange control and notification of

monetary flows to or from other countries remain in force.

8.1.3 The party required to report foreign investments

As a general rule, the owner of the investment and, in addition, any Spanish notary public acting in

the transaction, is obliged to report the investment to the authorities. However, investments in

certain assets (mutual funds, securities, registered shares) may require other individuals to report the

investment (credit, financial, deposit-taking or management entities, the Spanish company receiving

the investment).

17 http://www.cnmv.es/index.htm

Guide to business in SpainSpain profile23

8.1.4 Reporting rules

(i) General rule

As a general rule, foreign investments indicated in section 8.1.2 above and the liquidation thereof

must be reported after the event to the Investments Register at the Ministry of Industry, Tourism and

Trade18.

(ii) Exceptions

Investments from tax havens must be reported before and after the event, except in the following

cases:

• Investments in marketable debt securities issued or offered publicly, whether or not they are

traded on an official secondary market, and units in mutual funds recorded in the Registers of the

Spanish National Securities Market Commission.

• Where the foreign interest does not exceed 50% of the capital stock of the Spanish company in

which the investment is made.

It is important to stress that this prior reporting obligation is not equivalent to a verification or

authorization requirement and once the investment has been reported, the investor may make his

investment without having to wait for any reply from the authorities.

8.1.5 Monitoring of foreign investments

The General Directorate for Trade and Investments19 (“DGCI”) of the Ministry of Industry, Tourism and

Trade can require Spanish companies which have foreign shareholders and Spanish branches of non-

resident persons specifically or generally to file an annual report on the status of their foreign

investments. The General Directorate may also require the parties required to report foreign

investments to provide the information necessary in each particular case.

8.1.6 Suspension of the deregulation rules

The Spanish Council of Ministers can suspend the application of the deregulation rules in certain

cases, which will require investments concerned to undergo a prior procedure to obtain

administrative clearance from the Council of Ministers.

Up to date, the Council of Ministers has exercised the powers of suspension described above only in

respect of foreign investments in Spain in activities directly related to national security, such as the

production or marketing of arms, munitions, explosives and other armaments (except in the case of

listed companies, in which case only acquisitions by non-residents of more than 5% of their capital

stock, or acquisitions of less than 5% that enable such investors to form, directly or indirectly, part of

their managing bodies, will require clearance).

18 www.mityc.es19 www.mcx.es

Guide to business in SpainSpain profile24

8.2 Exchange control regulations

Exchange control and capital movements are fully liberalized and in all areas there is complete

freedom of action.

In this sense, Law 19/2003, on Movement of Capital and Foreign Transactions and for the Prevention

of Money Laundering, repealed Law 40/1979, on Exchange Control Legal System (with the exception

of chapter II), and modified Law 19/1993, on Certain Measures for the Prevention of Money

Laundering, but maintained the principle of liberalization of movements of capital.

Law 19/2003 should have been implemented by regulations before January 8, 2004, but this has

been done only partially. In this regard, Royal Decree 54/2005 has modified the regulations of Law

19/1993, approved by Royal Decree 925/1995. However, no other regulations have been

implemented and, until they are, according to the First Temporary Provision of Law 19/2003, all

regulations approved implementing Law 40/1979 will remain in force in everything not opposed to

Law 19/2003.

Additionally, Law 36/2006, on measures for the prevention of tax fraud, has modified Law 19/1993

in connection with certain aspects of the prevention of money laundering.

The main features of the Spanish exchange control scenario currently in force can be summarized as

follows:

8.2.1 Freedom of action

As a general rule, all acts, businesses, transactions and operations between residents and non-

residents which involve or may involve payments abroad or receipts from abroad are completely

deregulated. This deregulation includes payments or receipts made either directly or by offset of the

underlying transactions, as well as transfers to or from abroad and variations in accounts or financial

debtor or creditor positions abroad. It also covers the import or export of means of payment.

8.2.2 Safeguard clauses and exceptional measures

The EU provisions will be able to prohibit or restrict the performance of certain transactions and the

respective collections, payments, bank transfers or variations in accounts or financial positions in

respect of third countries.

The Spanish Government may also impose prohibitions or restrictions in respect of one or a group of

States, a certain territory or an extra-territorial centre, or suspend the system of liberalization for

certain acts, businesses, transactions or operations.

8.2.3 Statistical information

In order to calculate the Spanish balance of payments and to maintain statistical control of monetary

flows there are certain mechanisms for payments to and receipts from abroad.

Guide to business in SpainSpain profile25

Currently, these mechanisms are as follows:

• As a general rule, payments, receipts and transfers between residents and non-residents,

denominated either in euros or in foreign currency, should be made through deposit-taking

entities (normally banks) registered in the Bank of Spain’s Official Register20 to whom the resident

party must provide with certain data (e.g. names and addresses of both parties) and specifically

with a description of the transaction giving rise to the payment, receipt or transfer.

The debits and credits posted to bank accounts held in Spain by non-residents are also subject to

this regime.

• The debits and credits posted to bank accounts held abroad by residents must be notified to the

Bank of Spain using specific forms if they exceed a specified threshold or if expressly requested by

the Bank of Spain.

• Payments and receipts between residents and non-residents can be made, in Spain or abroad, in

coins, bank notes and bearer checks, denominated either in euros or in foreign currency, and must

be declared by the resident party within 30 days if they, in general terms, exceed €6,000

(although the limit depends on the form of payment).

• Non-residents intending to credit bank accounts held in Spain by non-residents by means of bank

notes or bearer checks, in euros or foreign currency, or to transfer abroad such means of payment,

are obliged to evidence the origin of such funds. Otherwise, the registered entities will not be able

to proceed with these transactions.

Additionally, non-residents are required to justify the origin of the funds they use to acquire bank

checks, payment orders or other instruments, both in euros and in foreign currency, at a registered

entity, or to carry out sales and purchases of bills against other bills in authorized currency

exchange establishments.

Exceptionally, the Spanish Ministry of Industry, Tourism and Trade may, by making the relevant

regulations, require prior clearance or declaration for payments, receipts or transfers to or from

abroad arising from certain transactions yet to be specifically defined.

8.2.4 Specific transactions to be reported to the Bank of Spain

For purely statistical and informative reasons, residents involved in businesses or transactions abroad

should declare them in the following cases:

• Financing and deferrals of payments and receipts for more than one year between residents and

non-residents deriving from commercial transactions or the provision of services.

• Offsets of credits and debits between residents and non-residents deriving from commercial

transactions or the provision of services.

20 http://www.bde.es/

Guide to business in SpainSpain profile26

• Offsets of credits and debits deriving from intermediation in financial markets by intermediary

entities.

• Financial loans received by residents from non-residents or granted by residents to non-residents.

Securities such as bonds, promissory notes, etc. not traded on Spanish stock exchanges issued by

Spanish residents and acquired by non-residents are considered as financial loans from non-

residents.

The notification of foreign loans and credits provided by non-residents to residents requires (prior

to the first draw-down of funds of the loan or credit provided) the resident borrower concerned to

obtain a financial transaction number (“NOF”) when the amount thereof is equal to or higher

than €3,000,000, and it is not necessary to file any returns for lower amounts. This NOF must be

indicated in all the collection and payment notices relating to the transaction.

Specifically, the procedure for the assignment of a NOF is as follows:

— If the amount of the financing is less than €3,000,000, the transaction is excluded from the

reporting obligation unless the Bank of Spain requires it because the aggregate amount of

various transactions exceeds the limit established.

— If the amount is between €3,000,000 and €6,000,000, unless the financing is provided by a

non-resident that is resident in a tax haven in accordance with RD 1080/1991, the NOF may be

assigned not only by the Bank of Spain but also directly by any registered entity acting on

behalf of the Bank of Spain, for which the resident borrower concerned must fill out a Form PE-

2 containing a preprinted number which is the NOF.

— In any other cases, the NOF must be assigned by the Bank of Spain, for which a Form PE-1 must

be filled out.

— With regard to loans and credits exceeding €3,000,000 deriving from tax havens, the Bank of

Spain may request from the resident borrowers all the information it may deem relevant or

make as many verifications needed in order to identify the conditions of the transaction before

proceeding to register the transaction and assign the NOF.

Additionally, the Spanish authorities and the Bank of Spain may request any data in order to monitor

such transactions for statistical and tax purposes.

8.2.5 Import and export of certain means of payment and movement in national territory

Order EHA/1439/2006, on the declaration of movements of means of payment for the purposes of

the prevention of money laundering, in force from February 13, 2007, establishes that the export of

coins, bank notes and bearer checks, denominated either in euros or in foreign currency, although

deregulated, is subject to prior declaration for purely informative purposes if the amount involved

exceeds €10,000 per individual per trip. If the declaration is not made, the Spanish customs officials

will retain these means of payment.

Guide to business in SpainSpain profile27

The import of the above-mentioned means of payment by non-residents is subject in certain cases to

prior declaration to the Spanish customs authorities if higher than €10,000 (per individual per trip).

The movement in national territory of forms of payment consisting of cash, bank bills and bank

checks made out to bearer and denominated in national or any other currency, or any physical

means, including electronic, that are designed for use as a form of payment, for amounts equal to or

higher than €100,000, must also be reported previously. For purposes of this Order, “movement”

shall be deemed to mean any change of place or position verified outside the domicile of the holder

of the means of payment.

8.2.6 Types of bank accounts

Non-resident individuals and legal entities can hold bank accounts on the same conditions as

resident individuals and legal entities. The only requirement is to provide documentary evidence, on

opening the bank account, of the non-resident status of the holder of the account. Additionally, such

status must be confirmed to the authorized bank every two years. Other minor formalities are

stipulated.

Moreover, residents may, subject to certain declaration requirements, freely open and hold bank

accounts abroad either in euros or in foreign currency (the opening of such bank accounts by resident

parties must be declared to the Bank of Spain)and bank accounts in Spain denominated in foreign

currencies at registered entities (without being subject to any information requirement).

8.2.7 Residence for exchange control purposes

For exchange control purposes, individuals are deemed to be resident in Spain if they have their

customary place of residence in Spain. Legal entities with registered offices in Spain, and the

permanent establishments and branches in Spain of legal entities or of individuals who are resident

abroad, are likewise resident in Spain for exchange control purposes.

Non-residents for exchange control purposes are individuals with their customary place of residence

abroad, legal entities with registered offices abroad, and the permanent establishments and

branches abroad of Spanish resident individuals or entities.

Individuals or entities are deemed to have their customary residence in Spain if they comply with the

requirements set forth in the tax legislation to be considered as residents in Spain for tax purposes

but with the specifications established by regulations (currently there are no regulations on this

matter).

8.2.8 Notaries’ anti-money laundering obligations

The recently approved Royal Decree 1804/2008, of November 3, 2008, and Order EHA/114/2008, of

January 29, 2008, have detailed and implemented the manner in which notaries have to meet

certain anti-money laundering-related obligations to which they are subject under the provisions of

Law 19/1993 and its implementing regulations approved by Royal Decree 925/1995, as well as the

Notarial Organization and Regime Regulations.

Guide to business in SpainSpain profile28

Indeed, notaries’ status as public attesting officials, deriving from their continuous involvement in

economic and financial transactions, as well as their capacity as public officials with an obligation to

collaborate with the central government authorities, constitutes the ultimate basis of the duty

incumbent on them to supply and require information regarding such transactions.

Sociedad Estatal para la Promoción y Atracción de las

Inversiones Exteriores, S.A.U. RM: Tomo 21818, libro 0, folio

15, sección 8, hoja M-388683,

Inscripción 1. NIF: A-84479013. Depósito legal: M-3674-2007.

Published 2010

This guide was researched and written by Garrigues on behalf

of INVEST IN SPAIN.

This guide is correct to the best of our knowledge and belief at

the date indicated below. It is, however, written as a general

guide so it is necesary that specific professional advice be

sought before any action is taken.

Madrid, January 2010

Prepared by:

Guide to business in Spain

Establishing abusiness in Spain

!2

Setting up a business in Spain is simple. Thetype of business entities available are in keepingwith those existing in other OECD countries andthere is also a wide range of possibilitiescapable of meeting the needs of the differenttypes of investor who wish to invest in or fromSpain.

It is also worth noting that foreign investmentrestrictions and exchange controls have beenvirtually eliminated in line with the EUlegislation on deregulation in this area.

This chapter describes the basic requirements ofthe different business structures for investing inSpain, as well as the key formalities that aforeign investor must fulfill in order to set up orstart up each of therm.

Currently being updated owing

to a change in legislation

Guide to business in SpainEstablishing a business in Spain2

Guide to business in Spain

Establishing abusiness in Spain

!2

1. Introduction

2. Different ways of doing business in spain

3. Tax identification number (N.I.F.) and

foreigner identity number (N.I.E.)

4. Incorporation of a corporation

5. Formation of a branch

6. Other alternatives for operating in spain

7. Other alternatives to INVEST IN SPAIN

8. Dispute resolution

3

4

5

6

11

14

21

24

Galicia

Asturias Cantabria PaísVasco

La Rioja

Navarra

Castilla y León

Extremadura

Andalucía

Castilla - La Mancha

Comunidad de Madrid

Aragón

Cataluña

Murcia

ComunidadValenciana

Canarias

Baleares

FRANCE

PORTUGAL

MORROCO

La Coruña

Santiago de Compostela Lugo

Orense

OviedoSantander

León

Palencia

Valladolid

Segovia

Ávila

Soria

Logroño

Vitoria

Pamplona

Huesca

Zaragoza

Lérida

Tarragona

Castellón de la Plana

Valencia

Alicante

Murcia

Albacete

Cuenca

Madrid

Toledo

Cáceres

Mérida

Córdoba

Sevilla

Huelva

Cádiz

Ceuta

Málaga

Granada

Jaén

Almería

Melilla

BadajozCiudad Real

Guadalajara

Palma De Mallorca

Barcelona

Gerona

Teruel

BilbaoSan Sebastián

Salamanca

Burgos

Zamora

Pontevedra

Las Palmas de Gran Canaria

Santa Cruz de Tenerife

Guide to business in SpainEstablishing a business in Spain3

1. Introduction

1. INTRODUCTION

This chapter takes a practical look at the main alternatives open to a foreign investor interested in

establishing a business in Spain, as well as the main steps, costs and legal requirements involved.

Several alternatives are analyzed in this chapter, including both the establishment of business by the

investor itself, either through the incorporation of a company or a branch, or through a joint venture

with other enterprises already established in Spain. Other channels for conducting business without a

physical presence, such as distribution, agency, commission and franchising agreements are also

considered.

The following steps are explained throughout this chapter:

• Setting-up of a Spanish corporation and formation of a Spanish branch (sections 3 and 4).

• Acquisition of shares in an existing Spanish corporation (section 6.1).

• Acquisition of real estate located in Spain (section 6.2).

Finally, this Chapter contains a section on disputes resolution in Spain, to be carried out through the

national courts or arbitration, this last having proven well-suited to the settlement of such disputes.

Guide to business in SpainEstablishing a business in Spain4

2. DIFFERENT WAYS OF DOING BUSINESS IN SPAIN

Various alternatives are open to the foreign investor once the decision to invest in Spain has been

taken:

• The incorporation of a Spanish company (an S.A. or any other of the forms of undertakings

described in Appendix I, section 2 of this Guide), or the formation of a branch or permanent

establishment. Spanish law provides for a variety of vehicles that can be used by foreign

companies or individuals for investing in Spain.

Traditionally, the corporation (S.A.) has been the form most commonly used, although the limited

liability company (S.L.) has gained popularity in recent years.

• Association with other businesses already established in Spain. Foreign investors may find a joint

venture with a Spanish company to be the most appropriate form of presence in Spain, since it

allows the parties to share risks and combine resources and expertise.

A joint venture can be set up under Spanish law in a number of ways:

— An Economic Interest Grouping (“Agrupación de Interés Económico”, E.I.G.) or a European

E.I.G. (E.E.I.G.).

— A Temporary Business Association (“Unión Temporal de Empresas” or U.T.E.).

— A silent partnership (contrato de cuenta en participación) with a Spanish company.

— Joint ventures through Spanish corporations or limited liability companies.

• However, it is not necessary for every investor willing to operate and/or distribute his goods or

services in Spain to set up a new business or enter into an association with an existing one.

Penetration of the Spanish market and a satisfactory response to existing demand may be

achieved using the various forms of distribution agreements available in Spain, without

establishing a centre of operations. The alternatives include:

— Signing a distribution agreement.

— Operating through an agent.

— Operating through commission agents.

— Franchising.

Each of these forms of doing business in Spain offers different advantages that should be balanced

against the potential problems that each may pose and that need to be considered from the tax and

legal points of view.

2. Different ways of doing business in Spain

Guide to business in SpainEstablishing a business in Spain5

3. TAX IDENTIFICATION NUMBER (N.I.F.) AND FOREIGNER IDENTITY NUMBER (N.I.E.)

The applicable Spanish legislation currently requires that any individual or legal entity with economic

or professional interests in Spain, or involved in a relevant way for tax purposes, must hold a tax

identification number (in the case of legal entities) or a foreigner identity number (for individuals).

These documents, the first of which is issued free of charge and the second at a small cost, must be

obtained in order to set up a company, but also to file and process certain documentation with the

Spanish authorities. The steps to be taken are as follows:

(a) Assignment of a tax identification/foreigner identity number to non-resident directors of the

company to be set up: (a) if the director is a legal entity, a specific form must be filed with the

competent authorities, along with certain documentation, and a number is automatically

assigned; (b) if the director is an individual, a Foreigner Identity Number (N.I.E.)1, which will

also serve as a N.I.F., must be applied for by either one of the following methods:

• In Spain: at the General Directorate of Police2. If directors do not appear in person, a duly

notarized and apostilled or legalized general or special power of attorney is needed for each of

the directors, as well as a certified true copy of their passport.

• Abroad: at Spanish diplomatic missions or consular offices.

(b) Assignment of a tax identification/foreigner identity number to any shareholders of the

company: A specific form must be submitted to the competent authorities (in the case of legal

entities) or a N.I.E. must be applied for (for individuals) following the procedures described

above.

Throughout the above process, the shareholders and/or director(s) acting through a representative

must grant sufficient powers of attorney to fulfil these formalities.

3. Tax identification number (N.I.F.) and foreigner identity number (N.I.E.)

1 http://www.mir.es/2 http://www.policia.es/

Guide to business in SpainEstablishing a business in Spain6

4. Incorporation of a corporation

4. INCORPORATION OF A CORPORATION

The most common form of legal entity under Spanish corporate law is the corporation (“Sociedad

Anónima” - S.A.), and the second most common is the limited liability company (“S.L.”). (Other

corporate forms are described in Appendix I, section 2 of this Guide).

However, it should be noted that similar steps and expenses are involved for both legal forms, so this

chapter describes only those necessary for establishing a corporation.

4.1. Legal steps

Example: incorporation of an S.A. through cash contributions. The formal act of incorporation takes

place in the presence of a notary public, who executes the related public deed of incorporation

(including the articles of incorporation). The share capital must be fully subscribed and at least 25%

paid in at the time of incorporation; the remaining 75% must be paid in within the period stipulated

in the by-laws. The minimum share capital required is €60,102 (compared with the much lower

figure of €3,005 for an S.L., which must be paid in full at incorporation).

The basic requirements for establishing a corporation are as follows:

• Issue by the Spanish Central Mercantile Register3 of a certificate of clearance for use of the name

of the new company. This step should precede all others, to ensure that the proposed name can in

fact be used. The certificate of clearance is valid for six months from the date of issue.

• Execution by the future shareholders of an agreement of intent to set up the new company. The

minimum terms of such an agreement are as follows: (a) the type of company to be set up; (b)

the corporate purpose of the company; (c) the initial share capital; and (d) the registered office.

However, this document is executed for the mere purpose of the assignment of a provisional N.I.F.

to the new company, which is why the terms of the agreement can later be amended in the deed

of incorporation.

• Assignment of a provisional N.I.F. to the new company. This is a necessary formality for the

payment of transfer tax (see below) and the registration of the company in the Mercantile

Register. Fulfilment of this formality, which is free of charge, requires a specific form and certain

other documents (including the future shareholders’ agreement of intent to set up a company) to

submitted to the competent authorities, with a provisional number being assigned automatically

to the company. Once the company has been registered in the Mercantile Register, it must obtain

a definitive N.I.F. within a maximum of six months from assignment of the provisional N.I.F.

However, in order for the Spanish authorities to issue a definitive N.I.F., the formalities relating to

assignment of a N.I.F. and N.I.E. to the foreign shareholders and directors of the company must be

completed, as detailed in Chapter 2, section 3.

3 http://www.rmc.es/

Guide to business in SpainEstablishing a business in Spain7

• Execution of the public deed of incorporation of the company before a Spanish notary public.

• Evidence of the identity of the founder shareholders.

The notary public will require the persons who appear before him for this purpose to exhibit: (i)

evidence of their identity; (ii) the powers of attorney (if applicable) to represent a third party on

whose behalf any of them appears; (iii) evidence of payment and whether it is to be made in cash

or in kind (if applicable); (iv) the name clearance certificate from the Mercantile Register (see

above); and (v) the form (to be signed by the notary, if applicable) for subsequent declaration of

the foreign investment to the General Directorate for Trade and Investment of the Ministry of

Economy and Finance (“D.G.C.I.”)4 (See Chapter 1, section 8 for further information). It is also

necessary to provide the notary with the by-laws of the company.

If a shareholder is represented at the act of incorporation, the powers of attorney used must

satisfy certain requirements and, if issued abroad, must be duly legalized. There are two main

procedures for such legalization:

— Execution of the powers of attorney in the presence of the Spanish Consul in the foreign

investor’s home country. The foreign investor appears before the Spanish Consul, provides

evidence of his identity and grants the related powers of attorney. If a company, rather than

an individual, is the foreign shareholder, apart from his identity, the person appearing before

the Spanish Consul must provide evidence of his authorization to act in the name and on

behalf of the shareholder and to grant the powers of attorney to the designated person.

The Spanish Consul may demand any documentation he considers necessary, and will

proceed to execute a public deed of powers of attorney, in Spanish, to the person

designated. These powers of attorney can be used directly in Spain.

— Execution of the powers of attorney in the presence of a foreign public authenticating officer.

The foreign investor appears before the authenticating officer, gives evidence of his identity

and grants the related powers of attorney. If the foreign investor is a company, its

representative shall execute the powers of attorney in the presence of the public

authenticating officer, who certifies the document as well as the identity and authorization

of the representative of the foreign investor to grant the powers of attorney. The signature

of the foreign authenticating officer would also require subsequent legalization (either by the

“apostille” procedure approved by The Hague Convention of October 5, 1961, when

applicable, or by a Spanish Consul abroad). Under this second procedure, the powers would

normally be issued in the language of the authenticating officer who attests to the act so an

sworn translation into Spanish would also have to be prepared.

• Bank documents must be delivered to the acting notary public as evidence of payment.