P a g e | 1

TRIPURESHWAR SAH 1205816

SUMMER TRAINING REPORT SUBMITTED TOWARDS THE PARTIAL FULFILLMENT

OF Bachelors of Business Administration DEGREE

COMPARATIVE STUDY OF FINANCIAL MANAGMENT OF BANK

SUBMITTED BY:

TRIPURESHWAR SAH

BBA (2012-2015)

Regd. No.-1205816

INDUSTRY GUIDE FACULTY GUIDE

Mr.Mukesh Kumar Sah Mr.Dharamvir uppal

Assistant manager of Globel IME Bank GNA-IMT

PUNJAB TECHINICAL UNIVERSITY

P a g e | 2

TRIPURESHWAR SAH 1205816

DECLARATION

I hereby declare that the project work entitled “FINANCIAL MANAGEMENT

OF BANK ” submitted to the PTU JALANDHAR, is a record of an original work done

by me under the guidance of MR. Dharamvir uppal

T h i s p r o j e c t w o r k i s s u b m i t t e d i n t h e p a r t i a l f u l f i l l m e n t o f

t h e requirements for the award of the degree of Bachelors of business

administration. The results embodied in this thesis have not been submitted to any

other University or Institute for the award of any degree.

(Signature of the candidate)

P a g e | 3

TRIPURESHWAR SAH 1205816

CERTIFICATE BY GUIDE

This is to certify that the report of the project submitted is the outcome of the

project work entitled “FINANCIAL MANAGMENT OF BANK” carried out by

Tripureshwar sah bearing Roll no. 1205816 carried by under my guidance and

supervision for the award of degree in Bachelor of Business Administration of

Punjab Technical University, Jalandhar.

To the best of my knowledge the report

I. Embodies the work of the Candidate him/ herself.

II. Has duly been completed.

III. Fulfils the requirement of the ordinance relating to the BBA degree of the university.

IV. Is up to the described standard for the purpose of which is submitted.

(Signature of the Guide)

Ms. Dharamvir uppal

Designation: Lecturer

GNA-IMT

P a g e | 4

TRIPURESHWAR SAH 1205816

ACKNOWLEDGEMENT

Every work involves efforts and inputs of various kinds and people. I am thankful to all those

people who have been helpful enough to me to the extent of their being instrumental in the

completion and accomplishment of the project entitled “Financial management of bank at

Globel IME Bank”.

I sincerely acknowledge with deep sense of gratitude to my industry guide Assistant

manager(AM) Mr. Mukesh kumar sah , for enhancing my understanding of the subject and

enabling me to appreciate finer nuances of the subject.

I would also like to express my deepest gratitude to Branch manager(BM) Mr.Mukesh kumar

shah and the entire Credit & CSD Department for their help and guidance, without which the

completion of this project would have been extremely difficult.

Tripureshwar sah

Reg no.-1205816

Punjab techinical University

P a g e | 5

TRIPURESHWAR SAH 1205816

CHAPTER PLAN

Table of Content

CHAPTER 1 EXECUTIVE SUMMARY………………………………..

CHAPTER 2 INTRODUCTION OF FINANCIAL MANAGEMENT…………………

CHAPTER 3 OBJECTIVES…………………………………………...

CHAPTER 4 RESEARCH METHODOLOGY…………………………….

CHAPTER 5 INDUSTRY PROFILE…………………………………….

CHAPTER 6 COMPANY PROFILE…………………………………….

CHAPTER 7 FINANCIAL ANALYSIS……………………………………

CHAPTER 8 CONCLUSION , FINDINGS & REFRENCE……...…………

Conclusion………………………………………..

Findings………………………………………….

Refrence.......................................................................

P a g e | 6

TRIPURESHWAR SAH 1205816

Chapter 1 EXECUTIVE SUMMARY

This project was undertaken at the Bank Circle in the financial Department. Financial requirements

of the business are taken care of in the Credit Department. Companies that intend to seek credit

facilities approach the bank. Primarily, credit is required for following purposes:

a. Working capital finance

b. Term loan for mega projects

c. Non Fund Based Limits like Letter of Guarantee, Letter of Credit etc.

Project Financing discipline includes understanding the rationale for project financing, how to

prepare the financial plan, assess the risks, design the financing mix, and raise the funds. In

addition, one must understand some project financing plans have succeeded while others have

failed. A knowledge-base is required regarding the design of contractual arrangements to support

project financing; issues for the host government legislative provisions, public/private

infrastructure partnerships, public/private financing structures; credit requirements of lenders, and

how to determine the project's borrowing capacity; how to analyze cash flow projections and use

them to measure expected rates of return; tax and accounting considerations; and analyt ica l

techniques to validate the project's feasibility.

Project finance is different from traditional forms of finance because the credit risk associated with

the borrower is not as important as in an ordinary loan transaction; what is most important is the

identification, analysis, allocation and management of every risk associated with the project.

The purpose of this project is to explain, in a brief and general way, the manner in which risks are

approached by financiers in a project finance transaction. Such risk minimization lies at the heart

of project finance. Efficient management of credit portfolio is of utmost importance as it has a

P a g e | 7

TRIPURESHWAR SAH 1205816

tremendous impact on the Banks’ assets quality & profitability. The ongoing financial reforms

have no doubt provided unparallel opportunities to banks for growth, but have simultaneous ly

exposed them to various risks, which need to be effectively managed.

Also, lending continues to be a primary function in banking. In the liberalized Nepali economy,

clientele have a wide choice. External Commercial Borrowings and the domestic capital markets

compete with banks. In another dimension, retail lending- both personal advances and SME

advances- competes with corporate lending for funds and for human resources. But lending by

nature cannot be an aggressive selling activity, disregarding the risks involved. Bank has to be

competitive without compromising on the basic integrity of lending. The quality of the Bank’s

credit portfolio has a direct and deep impact on the Bank’s profitability.

P a g e | 8

TRIPURESHWAR SAH 1205816

Chapter 2 FINANCIAL MANAGEMENT – AN INTRODUCTION

Financial management refers to the efficient and effective management of money (funds) in such a

manner as to accomplish the objectives of the organization. It is the specialized function directly

associated with the top management. The significance of this function is not only seen in the 'Line' but

also in the capacity of 'Staff' in overall administration of a company. It has been defined differently by

different experts in the field.

It includes how to raise the capital, how to allocate it i.e. capital budgeting. Not only about long term

budgeting but also how to allocate the short term resources like current assets. It also deals with the

dividend policies of the share holders.

Definitions of Financial Management

“Financial Management is the Operational Activity of a business that is responsible for obtaining

and effectively utilizing the funds necessary for efficient operation.” by Joseph Massie

The primary goal of financial management is to maximize or to continually increase

shareholder value. Maximizing shareholder value requires managers to be able to balance

capital funding between investments in projects that increase the firm's long term profitability

and sustainability, along with paying excess cash in the form of dividends to shareholders.

Managers of growth companies (i.e. firms that earn high rates of return on invested capital)

will use most of the firm's capital resources and surplus cash on investments and projects so

the company can continue to expand its business operations into the future. When companies

reach maturity levels within their industry (i.e. companies that earn approximately average or

lower returns on invested capital), managers of these companies will use surplus cash to

payout dividends to shareholders. Managers must do an analysis to determine the appropriate

allocation of the firm's capital resources and cash surplus between projects and payouts of

dividends to shareholders, as well as paying back creditor related debt.

Choosing between investment projects will be based upon several inter-related criteria.

(1) Corporate management seeks to maximize the value of the firm by investing in projects

which yield a positive net present value when valued using an appropriate discount rate in

consideration of risk.

(2) These projects must also be financed appropriately.

(3) If no growth is possible by the company and excess cash surplus is not needed to the firm,

then financial theory suggests that management should return some or all of the excess cash

to shareholders (i.e., distribution via dividends).

P a g e | 9

TRIPURESHWAR SAH 1205816

Finance management includes:

Managerial Finance

Corporate finance

Financial management for the IT services

Financial management association

Financial management services

Some basic concept used in the finance

Buyers credit:- Buyer's credit is short term credit availed to an importer (buyer) from

overseas lenders such as banks and other financial institution for goods they are importing.

The overseas banks usually lend the importer (buyer) based on the letter of comfort (a bank

guarantee) issued by the importer's bank. For this service the importer's bank or buyer's

credit consultant charges a fee called an arrangement fee.

Capitalization rate:- Capitalization rate is the ratio between the net operating income

produced by an asset and its capital cost (the original price paid to buy the asset) or

alternatively its current market value.

Financial management

Investment decision

Financing decision

dividend decision

waorking capital

decision

P a g e | 10

TRIPURESHWAR SAH 1205816

Cash flow:-cash flow is the movement of the money in or out of a business ,product, or

financial product. It is usually measured during a specified, limited period of time.

Measurement of cash flow can be used for calculating other parameters that give

information on a company's value and situation. Cash flow can be used, for example, for

calculating parameters: it discloses cash movements over the period.

Collateral(finance):- In lending agreements, collateral is a borrower's pledge of

specific property to a lender, to secure repayment of a loan. The collateral serves as

protection for a lender against a borrower's default—that is, any borrower failing to pay

the principal and interest under the terms of a loan obligation. If a borrower does default

on a loan (due to insolvency or other event), that borrower forfeits (gives up) the property

pledged as collateral, with the lender then becoming the owner of the collateral.

Compound interest: - Compound interest arises when interest is added to the principal of

a deposit or loan, so that, from that moment on, the interest that has been added also earns

interest. This addition of interest to the principal is called compounding

Discounting: - Discounting is a financial mechanism in which a debtor obtains the right

to delay payments to a creditor, for a defined period of time, in exchange for a charge or

fee. Essentially, the party that owes money in the present purchases the right to delay the

payment until some future date. The discount, or charge, is the difference (expressed as a

difference in the same units (absolute) or in percentage terms (relative), or as a ratio)

between the original amount owed in the present and the amount that has to be paid in the

future to settle the debt.

Division of labour:- The division of labour is the specialization of cooperating

individuals who perform specific tasks and roles. Because of the large amount of labour

saved by giving workers specialized tasks in Industrial Revolution-era factories, classical

economists such as Adam Smith and mechanical engineers such as Charles Babbage were

proponents of division of labour

Down payment:- Down payment is a payment used in the context of the purchase of

expensive items such as a car and a house, whereby the payment is the initial upfront

portion of the total amount due and it is usually given in cash at the time of finalizing the

transaction.

Down side risk:- Downside risk is the financial risk associated with losses. That is, the

risk of difference between the actual return and the expected return (when the actual return

is less), or the uncertainty of that return

Letter of credit:- A letter of credit is a document issued by a financial institution, or a

similar party, assuring payment to a seller of goods and/or services provided certain

documents have been presented to the bank. These are documents that prove that the seller

has performed the duties under an underlying contract (e.g., sale of goods contract) and the

goods (or services) have been supplied as agreed. In return for these documents, the

beneficiary receives payment from the financial institution that issued the letter of credit.

P a g e | 11

TRIPURESHWAR SAH 1205816

Maturity:- In finance, maturity or maturity date refers to the final payment date of

a loan or other financial instrument, at which point the principal (and all

remaining interest) is due to be paid. The term fixed maturity is applicable to any form of

financial instrument under which the loan is due to be repaid on a fixed date. This includes

fixed interest and variable rate loans or debt instruments, whatever they are called, and

also other forms of security such as redeemable preference shares, provided their terms of

issue specify a date. It is similar in meaning to 'redemption date'.

Mortgage calculator:- Mortgage calculators are used to help a current or potential real

estate owner determine how much they can afford to borrow on a piece of real estate.

Mortgage calculators can also be used to compare the costs, interest rates, payment

schedules, or help determine the change in the length of the mortgage loan by making

added principal payments.

Leverage:- In finance, leverage (sometimes referred to as gearing in the United Kingdom

and Australia) is a general term for any technique to multiply gains and losses. Most often

it involves buying more of an asset by using borrowed funds, with the belief that the income

from the asset will be more than the cost of borrowing. Almost always this involves the

risk that borrowing costs will be larger than the income from the asset – causing a reduction

in profits.

P a g e | 12

TRIPURESHWAR SAH 1205816

Chapter 3 OBJECTIVES

To study broad contours of management of credit, the loan policy, credit appraisal for

business units i.e. for working capital loan or Term Loan

To understand the basis of credit risk rating and its significance

To utilize the above learning and appraise the creditworthiness organizations those

approach BANKS for credit. This would entail undertaking of the following procedures:

i. Management Evaluation

ii. Business / Industry Evaluation

iii. Technical Evaluation

iv. Legal Evaluation

v. Financial Evaluation

vi. Credit Risk Rating

P a g e | 13

TRIPURESHWAR SAH 1205816

The methodology being used involves two basic sources of information primary sources and

secondary source.

Primary sources of Information

Meetings and discussion with the Chief Manager and the Senior Manager of both Credit

and Credit Risk Management Department

Meetings with the clients

Secondary sources of Information

Research papers, power point presentations and PDF files prepared by the bank and its

related officials

1. http://www.wikipedia.com

2. http://www.slideshare.net/

3. http://www.intranic.in

4. http://www.globelimebank.in

Chapter 4 RESEARCH METHODOLOGY

P a g e | 14

TRIPURESHWAR SAH 1205816

Chapter 5

INDUSTRY PROFILE

The initiation of formal banking system in Nepal commenced with the establishment in

1937 of Nepal Bank Limited (NBL), the first Nepalese commercial bank.9 The country's central bank, Nepal Rastra Bank (NRB) was established in 1956 by Act of 1955, after nearly two decades of NBL having been in existence. A decade after the establishment of

NRB, Rastriya Banijya Bank (RBB), a commercial bank under the ownership of His Majesty’s Government of Nepal (HMG/N) was established. Thereafter, HMG/N adopted open and liberalized policies in the mid 1980s reflected by the structural adjustment

process, which included privatization, tariff adjustments, liberalization of industrial licensing, easing of terms of foreign investment and more liberal trade and foreign exchange regime was initiated. With the adoption of liberalization policy, there has been

rapid development of the domestic financial system both in terms of number of financial institutions and as ratio of financial assets to the GDP. As of July 2005, the number of commercial banks has reached 17 and their branches numbered 375. A total of 60 finance

companies and other Development Banks and numerous credit cooperatives have also been established. Total financial assets in 2004/2005 reached around 54.09 percent of GDP and the M2/GDP ratio, which shows the financial sector development or financial deepening increased from in 12.4 percent in 1975 to 50.9 percent in 2000.

In the context of banking development, the 1980s saw a major structural change in financial sector policies, regulations and institutional developments. HMG/N emphasized the role of the private sector for the investment in the financial sector. The financial sector

liberalization, started already in the early eighties with the liberalization of the interest rates, encompassed further deregulation of interest rates, relaxation of entry barriers for domestic and foreign banks, restructuring of public sector commercial banks and

withdrawal of central bank control over their portfolio management (Acharya et al, 2003). These policies opened the doors for foreigners to enter into banking sector under joint venture. Consequently, the third commercial bank in Nepal, or the first foreign joint

venture bank, was set up as Nepal Arab Bank Ltd( now called as NABIL Bank Ltd ). in 1984. There after, two foreign joint venture banks, Nepal Indosuez Bank Ltd. (now called as

Nepal Investment Bank) and Nepal Grindlays Bank Ltd (now called as Standard Chartered Bank Nepal Ltd.) was established in 1986 and 1987 respectively. There after, another 12 commercial banks have been established within the period of 12 years. Nepalese banking system has now a wide geographic reach and institutional diversification. Although,

Nepalese financial sector is dynamic, a lot of scope for development of this sector exists. This is because the banking and non-banking sectors have not been able to capture all the potentialities of business till this time. It is evident from the Rural Credit Survey Report

that the majority of rural credit is supplied by the unorganized sector at a very high cost – perhaps being at two or three time of the formal sector - suggesting that the financial sector is still in the path of gradual development. Overdue loans and inefficiency of the

older and the larger of commercial banks have aggravated and have been made to compete with the new trim banks with no rural operations. Also, the commercial banks,

P a g e | 15

TRIPURESHWAR SAH 1205816

domestic or joint venture have shown little innovation and positive attitude in identifying new areas of saving and investment opportunities. Following table reflects the present

development of commercial banking institutions in Nepal.

SN. NAME OPERATION DATE

NO. OF

BRANCH

Paid Up Capital

Rs.in million

Pattern of ownership

Participatin

g foreign Bank

1 Nepal Bank Ltd 1937 106 380.4

Government-

49% Nepalese-51%

2 Rastriya Banijya Bank 1996 114 1172.3

Government –100%

3 Nabil Bank Ltd. 1984 17 491.7

Nepalese-50% Foreign Joint venture-50%

NB International, Ireland

4 Nepal Investment Bank Ltd. 1986 12 587.7

Nepalese-100%

5

Standard

Chartered Bank Nepal 1987 8 374.6

Nepalese-25%

Foreign Joint venture-75%

Standard

chartered Group

6 Himalayan Bank Ltd 1991 15 643.5

Nepalese-80%

Foreign Joint venture-20%

Habib Bank

Ltd, Pakistan

7 Nepal SBI Bank Ltd 1993 13 431.9

Nepalese-50%

Foreign Joint venture 50%

State Bank of

India, India

8

Nepal Bangladesh

Bank 1994 17 719.9

Nepalese- 75% Foreign Joint

venture-25%

IFIC,

Bangladesh

9 Everest Bank Ltd 1994 16 455

Nepalese-80%

Foreign Joint venture-20%

Punjab

National Bank, India

10

Bank of

Kathmandu 1995 9 463.6

Nepalese-

100%

11 Nepal Credit & Commerce Bank 1996 17 693.6

Nepalese-100%

12 Nepal Industrial & Commercial Bank 1998 8 500

Nepalese-100%

13 Lumbini Bank Ltd. 1998 4 500

Nepalese-

100%

14 Machhapuchere Bank 2000 9 550

Nepalese-100%

P a g e | 16

TRIPURESHWAR SAH 1205816

15 Kumari Bank Ltd 2001 4 500 Nepalese-100%

16 Laxmi Bank Ltd. 2002 3 610 Nepalese-100%

17 Siddhartha Bank 2002 3 350

Nepalese-

100% 18 Global Bank Ltd. 2006 1

EXISTING SCENARIO OF BANKING SECTOR As mentioned in the previous section, there are 17 commercial banks presently in operation. Among these banks some are established under joint venture with foreign banks while some are fully domestic bank. Out of total commercial banks, 6 commercial

banks are with foreign joint venture and 11 are fully domestic banks. ABOVE TABLE ABOVE exhibits the position of capital structure and foreign participation towards these banks.

Capital Structure of Banks: The current regulation of NRB prescribes that all the new commercial banks are to be established in Kathmandu at national level should have minimum paid up capital Rs. 1 billion; the existing banks in operation are required to

enhance the capital level to Rs. 1 billion by the end of FY 2065/66 BS. For this purpose and objective all the commercial banks have furnished their plans to enhance the level of capital accordingly. In the mean time, there are separate provisions on capital

requirements for the national level banks to be operated outside the Kathmandu. Banks to be established out side the Kathmandu valley are required to have a minimum paid up capital of Rs. 250 million.10 The total paid up capital of 17 banks as at July 2005 has

reached at Rs 9.423million. The paid up capital of commercial banks operating in Nepal is on an average of Rs. 554 million Banks Under Foreign Participation: All together nine banks were established under foreign participation in Nepal but three of these have divested their stake to Nepalese

promoters. Six banks still have foreign joint ventures. The banks operating under foreign participation are NABIL Bank Ltd, Standard Chartered Bank Nepal Ltd, Himalayan Bank Limited, Nepal SBI Bank Ltd, Everest Bank Limited and Nepal Bangladesh Bank Ltd.

Initially, Bank of Kathmandu, Nepal Credit and Commerce Bank and Nepal Investment Bank were also established under foreign joint venture. Assets of Banks Under Foreign Participation: The banking asset with the foreign

joint venture banks is gradually increasing. As of July 2005, the commercial banks under foreign participation hold 37.54 percent of total banking assets. The deposits and credits are still of greater proportion. Foreign joint venture banks possess 39.65 percent of total

deposits and 38.45 percent of total credit of the banking system. DOMESTIC LEGAL PROVISIONS REGARDING BANKING SECTOR Nepal Rastra Bank Act, 2002 has given full authority to the Nepal Rastra Bank regarding

regulation, inspection and supervision of the banks and financial institutions. Bank and Financial Institution Ordinance, 2060, which is popularly known as Umbrella Act, has recently been enacted in unified form. Agricultural Development Bank Act, 1967, Commercial Bank Act, 1974, Finance Company Act, 1986, Nepal Industrial Development

P a g e | 17

TRIPURESHWAR SAH 1205816

Corporation Act, 1990 and Development Bank Act 1996 have been repealed with the promulgation of this ordinance. The ordinance governs the functional aspect of banks

and financial institutions. Some of the important provisions in the ordinance regarding the banking sector have been analyzed in this chapter as follows: Any person wishing to incorporate a bank or financial institution to carry on financial

transactions should incorporate a bank or financial institution as a registered public limited company under the prevailing law of Nepal with prior approval of NRB by fulfilling the conditions prescribed in section 4 of the ordinance. The individual desiring for the

incorporation of such entity is required to submit an application to NRB for prior approval with the prescribed documents. The NRB is required to conduct necessary investigation and grant permission to establish a bank or financial institution with or without terms or conditions if all the criteria are met and information of disapproval with reason is also to

be given to the concerned person in case the application is denied. Similarly, any foreign bank or financial institution wishing to establish a bank or financial institution by making joint venture investment with a corporate body incorporated in Nepal or with a Nepali

citizen or as a subsidiary company with 100% share is eligible to furnish the application to establish a bank or financial institution. However, the ordinance is silent about the percentage of equity investment in joint venture, such foreign corporate body can invest.

It has been regulated by regulation till now as 75%. The ordinance prohibits anybody to conduct financial transaction except an established bank or financial institution and no bank or financial institution can use the proposed

name for the purpose of carrying financial transaction without obtaining license from NRB. The bank or financial institution desiring to conduct financial transaction must submit an application for license to the NRB in the prescribed form including the

prescribed fees, documents and description. NRB will grant license if it is satisfied with the basic physical infrastructure of the bank or financial institution; if the issuance of license for operating financial transaction will promote healthy and competitive financial intermediary and protect the interest of the depositors, the applicant is competent to

operate financial transaction in accordance with the provision of this ordinance and its regulation, directives, order or provisions of Memorandum and Article of Association and there are sufficient grounds to believe that the entity is competent to operate financial

transaction. The NRB will classify the institutions into "A" "B" "C" "D" groups on the basis of the minimum paid-up capital and provide the suitable license to the bank or financial

institution.. The authorized, issued and paid up capital of a license holder institution will be as prescribed by NRB from time to time. The NRB can issue directives to the license holder entity to increase its authorized, issued and paid-up capital if it deems necessary.

Similarly, the license holder entity must maintain a capital fund according to ratio prescribed by NRB based on the basis of its total asset or risk weighted assets, and other transactions. At the same time, the license holder entity must maintain a risk fund

according to ratio prescribed by NRB based on the basis of liability relating to its total asset and the other risk to be borne from off balance sheet transaction. The license holder entity must maintain general reserve fund regularly every year till the amount becomes double of the paid up capital of such entity.

P a g e | 18

TRIPURESHWAR SAH 1205816

The bank or financial institution can be upgraded if the authorized capital is enough for upper class, the institution has been able to make profit for last five years and the non-

performing asset is within the prescribed limit. Similarly, the bank or financial institution can be degraded if it fails to meet prescribed capital within the time period, it has been making loss for last five years, it has violated the directives of Rastra Bank time and again

and it fails to maintain Risk Management Fund as prescribed by it. The NRB will make necessary investigation and avail opportunity to clarify before taking such decisions. The NRB is in full power to deny license for financial transaction if the conditions stipulated

in ordinance are not met and it is also authorized to impose necessary conditions taking into account the existing financial position of the bank or financial institution, the interest of depositors and healthy operation of financial transaction. Similarly, it may increase, decrease or modify the terms and conditions time to time. The NRB can suspend the

license of the license holder for a specific period of time issued for the purpose of carrying financial activities or it may order the bank or financial institution to close the operation of their office partially or fully if such a license holder acts against the provisions of the

Nepal Rastra Bank Act, 2002, or the regulation made there under or fails to act in accordance with the order or directives issued by it or fails to act for the welfare and in the interest of the depositors. The NRB may cancel the license issued under this ordinance

to carry on the financial transactions of the license holder under the certain circumstances as stipulated in the ordinance. A foreign bank or financial institution desiring to open its office within the Kingdom of

Nepal must submit an application to NRB in the form as prescribed along with the fees and particulars as prescribed. The NRB may issue a license to foreign bank or financial institution to carry on financial transaction by allowing them to open a office within the

Kingdom of Nepal taking into account the situation of competition existing in the banking sector, the contribution that could be rendered in the Nepalese banking sector and the reputation of such foreign bank or financial institution. The NRB may specify necessary terms and conditions in the course of granting transaction license and it shall be the duty

of the foreign bank or financial institution to comply with such terms and conditions. The section 34(4) of the ordinance reiterates that the provisions of the ordinance are to be complied by such foreign bank or financial institution. The foreign bank or financial

institution, which has been issued license to operate financial transaction by opening its office within the Kingdom of Nepal, can not open another bank or financial institution in joint venture within the Kingdom of Nepal. However, the provision for the contact or

representative office of any foreign bank or financial institution will be as prescribed by NRB. Some of the important issues such as relationship with parent bank in case of liquidation and supervisory role of the different institutions (parent bank and parent

bank's supervisory authority) have not been adequately addressed in this ordinance. Provisions relating to capital requirement are also silent in ordinance. However, it can be fixed by regulation.

The section 47 of the ordinance prescribes functions of the bank or financial institutions. The entities functioning under sub-section (1) only can keep their name as bank of class "A" category. The functions of such bank are incorporated in subsection (1) (A) – (AF) which are in very detail. As per Nepal's commitments foreign bank branches are only

P a g e | 19

TRIPURESHWAR SAH 1205816

allowed for wholesale banking functions. So all of the provisions stipulated in subsection (1) will not be relevant to the foreign bank branches. According to the ordinance, NRB

has authority to make necessary regulation in this aspect. See Attached annex (technical) 1.1 for details EXISTING RULES AND REGULATIONS RELATING TO THE BANKING SECTOR

Followings are the requirements for establishing a new commercial bank in Nepal Regarding Paid up capital Requirements 1 To establish a new commercial bank of national level, the paid up capital of such bank

must be at Rs. 1000 million. 2 To have an office in Kathmandu, the bank is required to have either joint venture with foreign banks and financial institutions or a technical service agreement (TSA) at least for three years with such institutions.

3 In general, the share capital of commercial banks will be available for the promoters up to 70 percent and 30 percent to general public. The foreign banks and financial institutions could have a maximum of 75 percent share investment on the commercial

banks of national level. In order to provide adequate opportunity for investment to Nepali promoters in National level banks, only 20 percent of total share capital will be made available to general public on the condition that the foreign bank and financial institution

are going to acquire 50 percent of total share. 4 Banks that are already in operation and those who have already obtained letter of intent before the enforcement of these provisions have to bring their capital level within seven

years, i.e., by 16 July 2009 as per this recently declared provision. In order to increase in the capital such increase should be at a rate of 10 percent per annum at the minimum. 5 Banks to be established with foreign promoters' participation have also to be registered

fulfilling all the legal processes prescribed by the prevalent Nepal laws. 6 To establish the commercial banks in all the places in the kingdom other than in the Kathmandu valley, the paid up capital must be Rs. 250 million. In this case, the commercial banks to be established outside Kathmandu Valley, share investment of

promoters and general public should stand at 70 percent and 30 percent respectively. 7 Banks to be established outside Kathmandu Valley could be allowed to operate throughout the kingdom including Kathmandu Valley only on the condition that they have

operated satisfactorily at least for a period of three years and they have brought their paid up capital level up to Rs. 1000 million and also fulfilled other prescribed conditions. Unless and until such banks do not get licence to operate throughout the kingdom, they

will not be allowed to open any office in Kathmandu Valley. 8 Of the total committed share capital, the promoters has to deposit in NRB an amount equal to 20 percent along with the application and another 30 percent at the time of

receiving the letter of intent on the interest free basis. The bank should put into operation within one year of receiving the letter of intent. The promoters have to pay fully the remaining balance of committed total share capital before the banks comes into

operation. Normally, within 4 months from the date of filing of the application, NRB should give its decision on the establishment of the bank whether it is in favor or against it. If it declines to issue license, it has to inform in writing with reasons to the concern body. Regarding Promoters Qualification

P a g e | 20

TRIPURESHWAR SAH 1205816

1 Action on the promoters' application will not be initiated by the Nepal Rasta Bank if it is proved that their collateral has been put on auction by the bank and financial institution

as a result of non-payment of loans in the past, who have not cleared such loans or those in the black list of the Credit Information Bureau and five years have not elapsed from the date of removal of their name from such list. The application will be deemed

automatically cancelled irrespective of it being on any stage of process of license issuance if the above events are proved. 2 Of the total promoters, one-third should be its Chartered accountants or at least a

graduate of Tribhuvan University or recognized institutions with major in economics or accountancy, finance, law, banking or statistics. Likewise, at least 25 percent of promoters group should have the work experience of the bank or financial institution or similar professional experience.

3 An individual, who is already serving as a director in one of the bank and financial institutions licensed by Nepal Rastra Bank, cannot be considered eligible to become the director in other banks or financial institutions.

4 Stockbrokers, market makers, or any individual/institution - involved as an auditor of the bank and institution carrying on financial transactions - cannot be a director. Regarding the Sale of Promoters' Share

1 Promoter group's share can be disposed or transferred only on the condition that the bank has been brought in operation, the share allotted to the general public has been floated in the market and after completion of three year from the date it has been

registered in the Stock Exchange. Prior to the disposal of such shares, it is mandatory to get approval from the Nepal Rastra Bank. 2 The share allotted to the general public has to be issued and sold within three years

from the date the bank has come into operation. Failing to fulfill such provisions, the bank cannot issue bonus share or declare and distribute dividends. 3 Shareholders of the promoters group and their family members cannot have access to loans or facilities from the same institution. For this purpose, the meaning of the family

members will comprise of husband, wife, son, daughter, adopted-son, adopted-daughter, father, mother, step-mother and depended brother and sister. Regarding Branch Expansion Policy

The Commercial banks established with a head office in Kathmandu will initially be authorized to open a main branch office in the Valley and thereafter, they will be authorised to open one more branch in Kathmandu Valley only after they have opened

two branches outside Kathmandu Valley. PROCEDURAL ASPECTS FOR ESTABLISHING A COMMERCIAL BANK The following documents should be submitted sequentially while applying for the

establishment of a Commercial Bank. 1. Following documents are required to be submitted along with the application to establish a commercial bank: -

1.1. Application 1.2. Bio-data of promoters 1.3. Feasibility Study Report on the proposed commercial bank in the format prescribed by the Nepal Rasta Bank.

P a g e | 21

TRIPURESHWAR SAH 1205816

1.4. Attested photocopies of the minutes within the promoters to organize the bank. 1.5. Promoters agreement relating to operation of the bank

1.6. Copies of Articles of Association and Memorandum in the prescribed format in the Company Act, 1996. The memorandum should compulsorily include, inter alia, the provision that no person, firm, company and related group of company will be allowed to

hold beyond the 10 percent stake on the issued capital in one bank and altogether 15 percent stake in all the commercial banks. 2. Requirements in the case of participation of the firm established in Nepal:

2.1. Photocopy of firm registration certificate 2.2. Broad resolution stating the amount to be invested in the proposed bank 2.3. Certified photocopies of Articles of Association and Memorandum of the investing firm.

2.4. List of Directors and proportion of their share ownership 2.5. Tax clearance Certificate of the firm and its directors 3. Certified documents on prescribed amount deposited in the Nepal Rastra Bank

4. Commitment document of the collaborating foreign bank and financial institutions providing Technical Service Agreement in the case of proposed national level commercial bank to be established in the Kathmandu valley.

5. Additional requirements in the case of joint venture of foreign banks: 5.1 Certified minute of the board of directors of the foreign bank with a commitment of the amount to invest on the proposed bank establishing in Nepal.

5.2 Clearance letter from the regulatory authority or the central bank of the collaborating foreign bank. 5.3 Last three year's audited balance sheet, profit and loss statement and cash flow

statements. 5.4 Certified copies of joint venture agreement with Nepalese promoters to invest in the proposed bank 5.5 A statement, in the case of the joint venture foreign bank has a holding bank and

financial institution or a branch office or a representative office or liaison office in Nepal. 5.6 A justification, in the case of the joint venture foreign bank already has a joint venture in any bank or financial institution in Nepal.

Nepal Rasta bank will provide the letter of intent to the applicants to establish a bank within the four months of period the promoters of the proposed commercial banks have had submitted all the necessary documents and after the study and analysis of such

documents only if it would be appropriate to incorporate the bank. For this, to obtain a the Letter of Intent form the Nepal Rasta Bank, the certified document stating that the prescribed amount has been deposited, should be produced. If the bank

is not appropriate to establish, the applicant will be notified by such information. The Nepal Rastra Bank will also provide the required period to make the bank operation while granting the letter of Intent. If the bank will not come into the operation within such time

period, it can cancel the letter of intent provided to such bank. Providing of letter of intent shall not be regarded as the approval to conduct the banking transactions.

P a g e | 22

TRIPURESHWAR SAH 1205816

After obtaining the letter of intent, following additional documents should be produced to the Nepal Rastra Bank seeking the approval to conduct banking transactions:

1. An Application 2. Technical service agreement in case of foreign joint venture 3. Certified documents stating that the committed amount by promoters has been

deposited fully in the Nepal Rastra Bank. 4. The agreement document, if the bank premises are in rent, and the site plan of the bank building along with necessary layout required for bank operation.

5. Information on recruitments of Staffs 6. Statements on Software Application 7. Credit Policy Guidelines (CPG) of the Bank 8. Employees by-laws

9. Information on all the physical infrastructure that are required to operate a bank The operating license will be provided only after the conformation that all the statements and documents are complete and on the basis of physical infrastructure inspection report

submitted by physical inspection team comprising of members from Bank Operations Department, Inspection and supervision Department and Information Technology Department of this Bank.

Existing Supervision relating to the Banking Sector: Promotion of financial stability, development of safe and efficient payment systems, regulation and supervision of banking and financial system and the promotion of healthy

and competitive financial system are some of the objectives of functioning of Nepal Rastra Bank. To attain the above objectives Section 84 of the Nepal Rastra Bank Act 2002 has entrusted

Nepal Rastra Bank with the necessary powers to perform inspection and examination of any commercial banks or obtain necessary information for the purpose of supervision of the commercial banks. Currently the Bank Supervision Department in Nepal Rastra Bank carries out the function

of supervision of all commercial banks in Nepal. Since foreign banks have their presence only in the form of Joint Venture establishments – that is in collaboration with the local entrepreneurs – Nepal Rastra Bank supervises foreign establishes in the same manner as

it supervises other local banks. For the purpose of supervision, the department is required to prepare annual supervision plan for onsite examinations as well off site surveillance of the commercial banks. The same is to be approved by the Governor of the Bank.

The Bank Supervision Department carries out both onsite examinations as well as off site surveillance of the commercial banks as per its annual supervision plan.

P a g e | 23

TRIPURESHWAR SAH 1205816

Chapter 6 COMPANY PROFILE

Global IME Bank Ltd. emerged after successful merger of Global Bank Ltd (an “A” class commercial bank), IME Financial Institution (a “C” class finance company) and Lord Buddha Finance Ltd. (a “C” class finance company) in year 2012. Two more Development Banks (Social Development Bank and Gulmi Bikas Bank) merged with Global IME Bank Lrd in year 2013. Global Bank Limited (GBL) was established in 2007 as an ‘A’ class commercial bank in Nepal which provides entire commercial banking services. The bank was established with the largest capital base at the time with a paid up capital of NPR 1.0 billion. The paid up capital of the bank has since been increased to NPR 4.14 billion. The bank's shares are publicly traded as an 'A' category company in the Nepal Stock Exchange. Pursuant to the liberalized economic policy of the government, majority of the commercial banks have established their head office in the Kathmandu valley. Witnessing the incredible potential the country offers outside the capital, the promoters have established the bank in Birgunj, the commercial hub of the nation. It is in line with the aim of the bank to be “The Bank for All” by giving necessary impetus to the economy through world class banking service. For the day to day operations, the bank has been using the world renowned FINACLE software that provides real time access to customer database across all branches and corporate locations of the bank. This state of the art customer database has also been linked to a Management Information System that provides easy reach to all possible database information for balanced and informed decision making. A disaster recovery system (DRS) of the Bank has also been established in the Western Region of Nepal (200 kms west of Kathmandu). The bank has been able to achieve excellent diversification of its assets. A well balanced distribution of exposure in areas of national interest has been

P a g e | 24

TRIPURESHWAR SAH 1205816

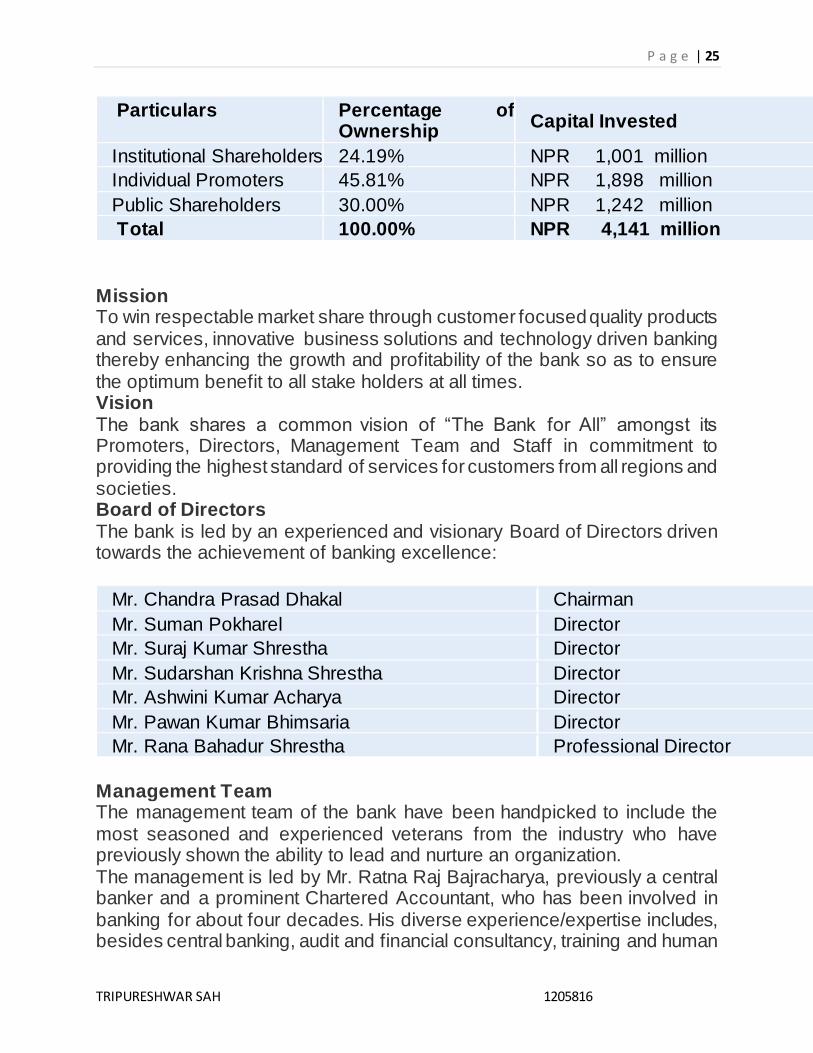

possible through long term forecasting and timely strategic planning. The bank has diversified interests in hydro power, manufacturing, textiles, services industry, aviation, exports, trading and microfinance projects, just to mention a few. The exemplary performance of the bank in these last five years has elevated it to a premier status in the industry. The bank has been handling government transactions and is officially among the only 5 banks in Nepal to do so. The bank has been able to earn the trust and confidence of the public, which is reflected in the large and ever expanding customer base of the bank. Through all this the bank has been able to truly achieve its vision of being “The Bank for All”. Even with all this success, the bank remains internally focused towards manpower development, product innovation and process innovation etc, to have a strong and solid foundation, which are ongoing and continuous improvement initiatives undertaken by the management and staff alike. Promoters GIBL has been promoted by a group of prominent indigenous entrepreneurs who have written a history of success in their field of ever growing business. The promoters of the bank include renowned, well established and respected businessmen/industrialists in Nepal from a variety of different sectors that include finance, remittance, trading, export, automotive services, manufacturing, media services and hydropower to name a few. The collective experience of the promoters have been realized to customize the bank's offerings and services to compete with best in the banking industry and instill a culture based on our core values of integrity, business ethics, teamwork, respect, humility, professionalism, loyalty and good governance. Shareholders Structure Authorized Capital of Global IME Bank is NPR 5,000 million and Paid up Capital is NPR 4,141 million. The promoters hold 70.00% while 30.00% is floated for the public. Current shareholder structure of the bank remains as below:

P a g e | 25

TRIPURESHWAR SAH 1205816

Particulars Percentage of Ownership

Capital Invested

Institutional Shareholders 24.19% NPR 1,001 million

Individual Promoters 45.81% NPR 1,898 million

Public Shareholders 30.00% NPR 1,242 million

Total 100.00% NPR 4,141 million

Mission To win respectable market share through customer focused quality products and services, innovative business solutions and technology driven banking thereby enhancing the growth and profitability of the bank so as to ensure the optimum benefit to all stake holders at all times. Vision The bank shares a common vision of “The Bank for All” amongst its Promoters, Directors, Management Team and Staff in commitment to providing the highest standard of services for customers from all regions and societies. Board of Directors The bank is led by an experienced and visionary Board of Directors driven towards the achievement of banking excellence:

Mr. Chandra Prasad Dhakal Chairman

Mr. Suman Pokharel Director

Mr. Suraj Kumar Shrestha Director

Mr. Sudarshan Krishna Shrestha Director

Mr. Ashwini Kumar Acharya Director

Mr. Pawan Kumar Bhimsaria Director

Mr. Rana Bahadur Shrestha Professional Director

Management Team The management team of the bank have been handpicked to include the most seasoned and experienced veterans from the industry who have previously shown the ability to lead and nurture an organization. The management is led by Mr. Ratna Raj Bajracharya, previously a central banker and a prominent Chartered Accountant, who has been involved in banking for about four decades. His diverse experience/expertise includes, besides central banking, audit and financial consultancy, training and human

P a g e | 26

TRIPURESHWAR SAH 1205816

resource development, project development (particularly banking and financial institutions, besides hydro, etc.) and their establishment, worked as the main local member with a team of expatriates for the management of a World Bank financed project under the Financial Sector Reform Project for the oldest bank of Nepal, Nepal Bank Limited. Thereafter, he led as the CEO of NCC Bank, turning around the bank’s balance sheet from a heavy negative net worth to a far better positive growth. Presently he is associated with GBL as its CEO. Similarly, the Deputy Chief Executive Officer, Mr. Janak Sharma Poudyal, possesses about 25 years of banking experience. His experience includes working in entire gamut of banking activities, worked as the senior most founder member of staff for the establishment and operations of two indigenous commercial banks. Holds an international MBA from London, UK and also carries with him an international banking experience having previously worked for Barclays Bank, London.

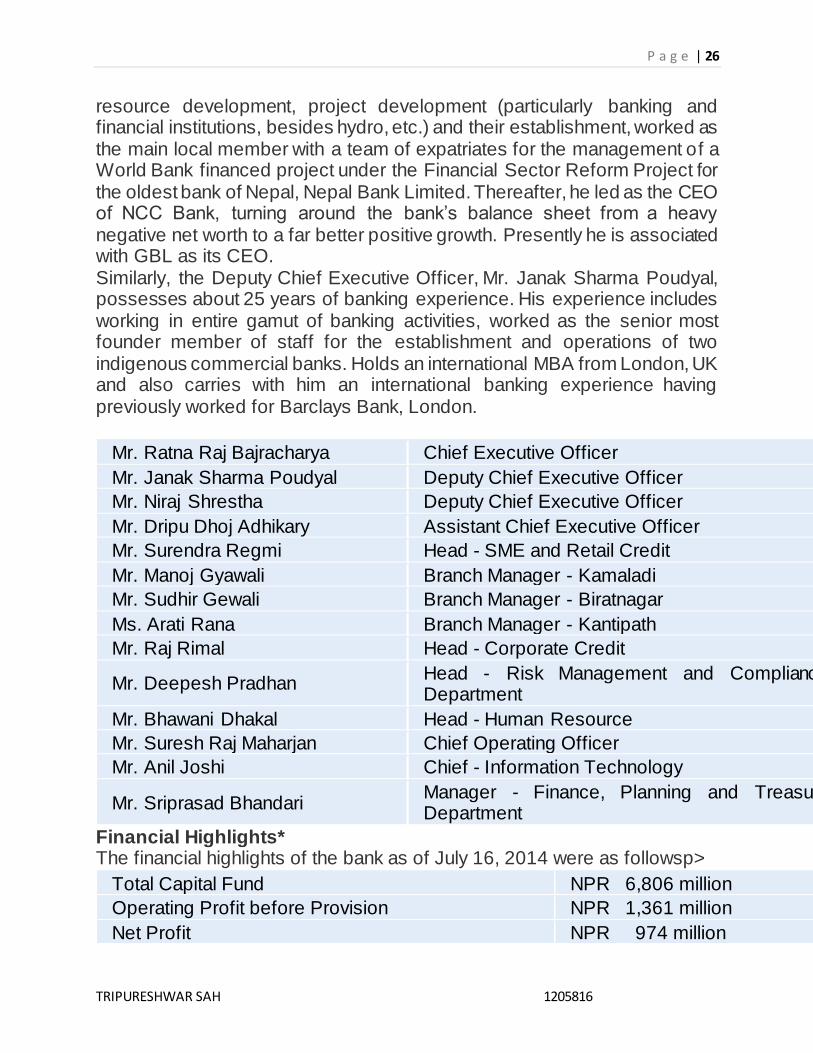

Mr. Ratna Raj Bajracharya Chief Executive Officer

Mr. Janak Sharma Poudyal Deputy Chief Executive Officer

Mr. Niraj Shrestha Deputy Chief Executive Officer

Mr. Dripu Dhoj Adhikary Assistant Chief Executive Officer

Mr. Surendra Regmi Head - SME and Retail Credit

Mr. Manoj Gyawali Branch Manager - Kamaladi

Mr. Sudhir Gewali Branch Manager - Biratnagar

Ms. Arati Rana Branch Manager - Kantipath

Mr. Raj Rimal Head - Corporate Credit

Mr. Deepesh Pradhan Head - Risk Management and Compliance Department

Mr. Bhawani Dhakal Head - Human Resource

Mr. Suresh Raj Maharjan Chief Operating Officer

Mr. Anil Joshi Chief - Information Technology

Mr. Sriprasad Bhandari Manager - Finance, Planning and Treasury Department

Financial Highlights* The financial highlights of the bank as of July 16, 2014 were as followsp>

Total Capital Fund NPR 6,806 million

Operating Profit before Provision NPR 1,361 million

Net Profit NPR 974 million

P a g e | 27

TRIPURESHWAR SAH 1205816

Total Deposits NPR 52,292 million

Total Lending NPR 43,019 million

Credit to Capital and Deposit Ratio 73.69%

Liquidity Ratio 31.11%

Capital Adequacy Ratio 12.38% *Highlights as per latest Audited Financial Statements. Unaudited current financial reports posted are in the Report section of this website. Correspondent Network The bank has been maintaining harmonious correspondent relationships with 62 different international banks from various countries to facilitate trade, remittance and other cross border services. Through these correspondents the bank is able to provide services in any major currencies in the world. The bank also maintains its extension offices in India and Middle East to assist in the remittance of funds from overseas Nepalese workers. These services are soon to be expanded to South Korea. Branch Network The bank is now operating 85 branches spread throughout Nepal. All of the bank's branches have been established as full service outlets that offer a large range of banking services to its customers. The bank also operates 81 ATMs throughout the country strategically placed for the convenience of customers.

1. FEATURE

DEALING IN MONEY

AGENCY

ACCEPTANCE OF DEPOSIT

GRANT OF LOAN AND ADVANCES

PAYMENT AND WITHDRAWAL

P a g e | 28

TRIPURESHWAR SAH 1205816

COMMERCIAL NATURE

2. Funds & Investments

Mutual Funds

Portfolio Management services

Alternative investments

Deposits

3. Banking Services

iMobile

Locker

VISA debit and VISA credit cards

4. Insurance & Risk Protection

Life Insurance

General Insurance

5. Banking Products

Savings Account

Family wealth Account

P a g e | 29

TRIPURESHWAR SAH 1205816

Home Loans

HP loan & Auto loan

Foreign Exchange Services

Lockers

6. Business Banking

Business Loans

Business Insurance

Business advice by Experts

P a g e | 30

TRIPURESHWAR SAH 1205816

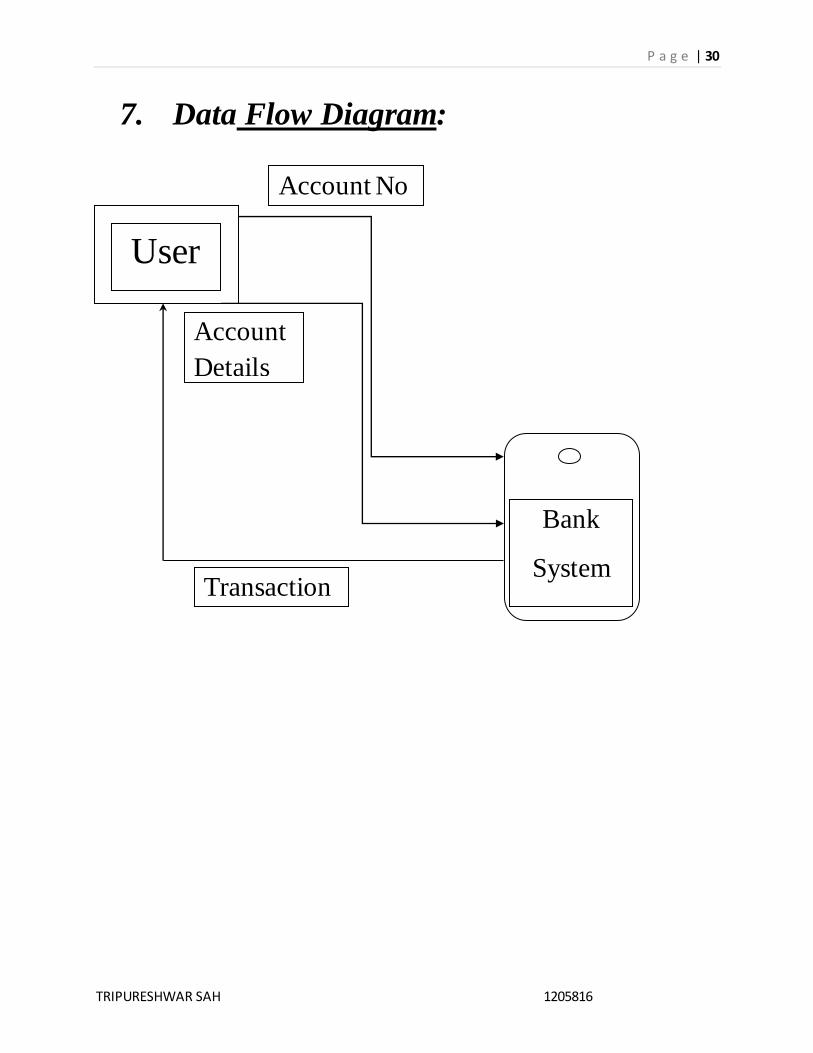

7. Data Flow Diagram:

User

Bank

System

Account No

Transaction

Account

Details

P a g e | 31

TRIPURESHWAR SAH 1205816

Flow chart

BANK h

CUSTOMER

ACC. NO. ADDRESS.

BALANCE.

Done

by

TRANSACTION

DEBIT CREDIT

NAME

START

P a g e | 32

TRIPURESHWAR SAH 1205816

CUSTOMER

has has

FIXED

DEPOSITE

ACCOUNT

AMOUNT

DURATION BALANCE

ID. NO.

ACC. ID.

START

P a g e | 33

TRIPURESHWAR SAH 1205816

Transaction Process

TRANSACTION CUSTOMER

CURRENT BALANCE

DEBIT CREDIT

UPDATE BALANCE UPDATE BALANCE

BALANCE

P a g e | 34

TRIPURESHWAR SAH 1205816

Chapter 7 FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

The aspects which need to be analyzed under this head should include cost of project, means of

financing, cost of production, break-even analysis, financial statements as also profitability/funds

flow projections, financial ratios, sensitivity analysis which are discussed as under:

Cost of Project & Means of Financing

a. The major cost components of any project are land and building including transfer, registrat ion

and development charges as also plant and machinery, equipment for auxiliary services,

including transportation, insurance, duty, clearing, loading and unloading charges etc. It also

involves consultancy and know-how expenses which are payable to foreign collaborators or

consultants who are imparting the technical know-how. Recurring annual royalty payment is

not reflected under this head but is accounted for under the profitability statements. Further,

preliminary expenses, such as, cost of incorporation of the Company, its registrat ion,

preparation of feasibility report, market surveys, pre-operative expenses like salary, travelling,

start up expenses, mortgage expenses incurred before commencement of commercia l

production also form part of cost of project. Also included in it are capital issue expenses

which can be in the form of brokerage, commission, advertisement, printing, stationery etc.

Finally, provisions for contingencies to meet any unforeseen expenses, such as, price

escalation or any other expense which have been inadvertently omitted like margin for

working capital requirements required to complete the production cycle, interest during

construction period, etc. are also part of capital cost of project. It is to be ensured while

appraising the project that cost and various estimates given are realistic and there is no

under/over estimation. Further, these cost components should be supported by proper

quotations, specifications and justifications of land, machinery and know-how expenses etc.

ii. Besides Bank’s loan, the project cost is normally financed by bringing capital by the promoters

and shareholders in the form of equity, debentures, unsecured long term loans and deposits

raised from friends and relatives which are not repayable till repayment of Bank's loan.

P a g e | 35

TRIPURESHWAR SAH 1205816

Resources are raised for financing project by raising term loans from Institutions/Banks which

are repayable over a period of time, deferred term credits secured from suppliers of machinery

which are repayable in installments over a period of time. The above is an illustrative list, as

the promoters have now started raising funds through Euro-issues, Foreign Currency loans,

premium on capital issues, etc. which are sometimes comparatively cheap means of finance.

Subsidies and development loans provided by the Central/State Government in notified

backward districts to attract entrepreneurs are also means of financing a project. It is to be

ascertained that requirement of finance has been properly tied-up for unhindered

implementation of a project. The financing structure accepted must be in consonance with

generally accepted levels along with adequate Promoters' stake. The resourcefulness,

willingness and capacity of promoter to contribute the same have also to be investigated.

In case of project finance, the promoter/borrower may bring in upfront his contribution (other

than funds to be provided through internal generation) and the branches should commence its

disbursement after the stipulated funds are brought in by the promoter/borrower. A condition

to this effect should be stipulated by the sanctioning authority in case of project finance, on

case to case basis depending upon the resourcefulness and capacity of the promoter to

contribute the same. It should be ensured that at any point of time, the promoter’s contribution

should not be less than the proportionate share.

Profitability Statement

The profitability statement which is also known as `Income and Expenditure Statement' is

prepared after considering the net sales figure and details of direct costs/expenses relating to

raw material, wages, power, fuel, consumable stores/spares and other manufacturing expenses

to arrive at a figure of gross profit. Thereafter, all other expenses like salaries, office expenses,

packing, selling/distribution, interest, depreciation and any other overhead expenses and taxes

are taken into account to arrive at the figure of net profit. The projections of profit/loss are

prepared for a period covering the repayment of term loans. The economic appraisal includes

P a g e | 36

TRIPURESHWAR SAH 1205816

scrutinizing all the items of cost, and examining the assumptions, if any, to ensure that these

are realistic and achievable. There should not be any optimism or pessimism in working out

profitability projections since even a little change in the product-mix from non-remunerat ive

to remunerative or vice-versa can distort the picture. While preparing profitability projections,

the past trends of performance in an industry and other environmental factors influencing the

cost and revenue items should also be considered objectively.

Generally speaking, a unit may be considered as financially viable, progressive and efficient if it

is able to earn enough profits not only to service its debts timely but also for future

development/growth.

Break-Even Analysis

Analysis of break-even point of a business enterprise would help in knowing the level of output

and sales at which the business enterprise just breaks even i.e. there is neither profit nor loss. A

business earns profit if it operates at a level higher than the break-even level or break-even point.

If, on the other hand, production is below this level, the business would incur loss. The break-

even point in an algebraic equation can be put as under:

The fixed costs include all those costs which tend to remain the same up to a certain level of

production while variable costs are those costs which tend to change in proportion with the volume

of production. As regards unit sales price, it is generally the same for all levels of output.

The break-even analysis can help in making vital decisions relating to fixation of selling price

make or buy decision, maximizing production of the item giving higher contribution etc. Further,

Break-even point

(Volume or Units) Total Fixed Cost / (Sales price per unit - Variable Cost per unit)

Break-even point

(Sales in rupees) (Total Fixed Cost x Sales) / (Sales - Variable Costs)

P a g e | 37

TRIPURESHWAR SAH 1205816

the break-even analysis can help in understanding the impact of important cost factors, such as,

power, raw material, labor, etc. and optimizing product-mix to improve project profitability.

Fund-Flow Statement

A fund-flow statement is often described as a ‘Statement of Movement of Funds’ or ‘where got:

where gone statement’. It is derived by comparing the successive balance sheets on two specified

dates and finding out the net changes in the various items appearing in the balance sheets.

A critical analysis of the statement shows the various changes in sources and applications (uses)

of funds to ultimately give the position of net funds available with the business for repayment of

the loans. A projected Fund Flow Statement helps in answering the under mentioned points.

How much funds will be generated by internal operations/external sources?

How the funds during the period are proposed to be deployed?

Is the business likely to face liquidity problems?

Balance Sheet Projections

The financial appraisal also includes study of projected balance sheet which gives the position of

assets and liabilities of a unit at a particular future date. In other words, the statement helps to

analyze as to what an enterprise owns and what it owes at a particular point of time.

An appraisal of the projected balance sheet data of the unit would be concerned with whether the

projections are realistic looking to various aspects relating to the same industry.

Financial Ratios

While analyzing the financial aspects of project, it would be advisable to analyze the important

financial ratios over a period of time as it may tell us a lot about a unit's liquidity position,

P a g e | 38

TRIPURESHWAR SAH 1205816

managements' stake in the business, capacity to service the debts etc. The financial ratios which

are considered important are discussed as under:

P a g e | 39

TRIPURESHWAR SAH 1205816

Ratio Formula Remarks

1 Debt-Equity

Ratio

Debt (Term Liabilities)

Equity

(Where, Equity = Share

capital, free reserves,

premium on shares, , etc.

after adjusting loss

balance)

There cannot be a rigid rule to a satisfactory debt-

equity ratio, lower the ratio higher is the degree of

protection enjoyed by the creditors. These days the

debt equity ratio of 1.5:1 is considered reasonable.

It, however, is higher in respect of capital intens ive

projects. But it is always desirable that owners have

a substantial stake in the project. Other features like

quality of management should be kept in view while

agreeing to a less favorable ratio. In financ ing

highly capital intensive projects like infrastructure,

cement, etc. the ratio could be considered at a higher

level.

2

Debt-

Service

Coverage

Ratio

Debt + Depreciation +

Net Profit (After Taxes) +

Annual interest on long

term debt

Annual interest on long

term debt + Repayment of

debt

This ratio of 1.5 to 2 is considered reasonable. A

very high ratio may indicate the need for lower

moratorium period/repayment of loan in a shorter

schedule. This ratio provides a measure of the ability

of an enterprise to service its debts i.e. `interest' and

`principal repayment' besides indicating the margin

of safety. The ratio may vary from industry to

industry but has to be viewed with circumspec tion

when it is less than 1.5.

3 TOL / TNW

Ratio

Tangible Net Worth (Paid

up Capital + Reserves and

Surplus -

Intangible Assets)

Total outside Liabilit ies

(Total Liability - Net

Worth)

This ratio gives a view of borrower's capital

structure. If the ratio shows a decreasing trend, it

indicates that the borrower is relying more on his

own funds and less on outside funds and vice versa

P a g e | 40

TRIPURESHWAR SAH 1205816

4 Profit-Sales

Ratio

Operating Profit (Before

Taxes excluding Income

from other Sources)

Sales

This ratio gives the margin available after meeting

cost of manufacturing. It provides a yardstick to

measure the efficiency of production and margin on

sales price i.e. the pricing structure

5

Sales-

Tangible

Assets Ratio

Sales

Total Assets - Intangib le

Assets

This ratio is of a primary importance to see how best

the assets are used. A rising trend of the ratio

reveals that borrower has been making effic ient

utilization of his assets. However, caution needs to

be exercised when fixed assets are old and

depreciated, as in such cases the ratio tends to be

high because the value of the denominator of the

ratio is very low.

6 Current

Ratio

Current Assets

Current Liabilities

Higher the ratio greater the short term liquidity. This

ratio is indicative of short term financial position of

a business enterprise. It provides margin as well as

it is measure of the business enterprise to pay-off the

current liabilities as they mature and its capacity to

withstand sudden reverses by the strength of its

liquid position. Ratio analysis gives indications; to

be made with reference to overall tendencies and

parameters in relation to the project.

7

Output

Investment

Ratio

Sales

Total capital employed

(in fixed & current assets)

This ratio is indicative of the efficiency with which

the total capital is turned over as compared to other

units in similar lines.

P a g e | 41

TRIPURESHWAR SAH 1205816

Internal Rate of Return

The discount rate often used in capital budgeting that makes the net present value of all cash flows

from a particular project equal to zero. Higher a project's IRR the more desirable it is to undertake

the project. IRR should be higher than the Cost of the project (interest rate in case of project

financing)

P a g e | 42

TRIPURESHWAR SAH 1205816

Chapter 8 CONCLUSION ,FINDINGS & REFRENCE

CONCLUSION

Banking activities are considered to be the life blood of the national Economy. Without banking

services, trading and business activities cannot be carried on smoothly. Banks are the distributors

and protectors of liquid capital which is of vital significance to a developing country.

Efficient administration of the banking system helps in the economic Growth of the nation.

Banking is useful to trade and commerce.

The study at GLOBAL IME BANK gave a vast learning experience to me and has helped to

enhance my knowledge. During the study I learnt how the theoretical financial analysis aspects are

used in practice during the working capital finance and term loan assessment. I have realized

during my project that a credit analyst must own multi-disciplinary talents like financial, technical

as well as legal know-how.

The credit appraisal for business loans has been devised in a systematic way. It is a process of

appraising the credit worthiness of loan applicants. Thus it extremely important for the lender bank

to assess the risk associated with credit; thereby ensure the security for the funds deposited by the

depositors. There are clear guidelines on how the credit analyst or lending officer has to analyze a

loan proposal. It includes phase-wise analysis which consists of 6 phases:

1. Financial statement analysis

2. Working capital and its assessment techniques

3. Techno Economic Feasibility Analysis

4. Credit risk assessment

5. Documentation

6. Loan administration

FINDINGS

P a g e | 43

TRIPURESHWAR SAH 1205816

For the day to day operations, the bank has been using the world renowned FINACLE software

that provides real time access to customer database across all branches and corporate locations

of the bank. This state of the art customer database has also been linked to a Management

Information System that provides easy reach to all possible database information for balanced

and informed decision making.

After completing the entire project at Global IME Bank the following key findings as mentioned

below were observed.

1. At, Global IME Bank Circle Office the priority to appraise a proposal was given to new

or fresh clients over the existing clients presenting proposals for renewal

2. Ratings, as being performed at Global IME Bank, are done once a year. Therefore, the

ratings do not take into account short term drastic changes like price level changes (which

are an issue with any method based on accounting statements, since annual reports are

based on historical cost basis of accounting and other changes like sudden mishap/ of the

counterparty are not readily accounted for by the rating system due to long lag between

repeat ratings on the same account.

3. Some of the parameters in Business and industry evaluation are based on the information

provided by company, which in some cases may not be sufficient. No specific guidelines

are followed in such cases. Also, some of the parameters here may be rendered redundant

in some cases and may push up/ push down the rating needlessly in these cases.

4. The present risk rating model does not have any mechanism to prioritize certain sectors of

the economy. There are certain sector in the economy where risk spread is low and certain

sectors where spread of risk is high like real estate. Also, there are certain infrastructura l

projects which need to be prioritized. The risk rating model is not flexible to incorporate

all these issues.

REFRENCES

1. http://www.wikipedia.com

2. http://www.slideshare.net/

3. http://www.intranic.in

P a g e | 44

TRIPURESHWAR SAH 1205816

4. http://www.globelimebank.in

5. Jagdish Capoor. Risk Management in Financial Institutions. From

http://www.coolavenues.com/know/fin/jagdish_capoor_a.php3

6. Principles for the Management of Credit Risk, from http://www.bis.org/publ/bcbsc125.pd f

7. M.Y.Khan & P.K.Jain, Financial Management

Recommended