12th SCC – Small Cap Conference Frankfurt/Main, 2 September 2014

GESCO – an association of industrial SMEs with market and technology leaders

Segments tool manufacture/mechanical engineering and plastics technology

Currently 17 operating subsidiaries under the roof of GESCO AG as a holding company

We think and act in a sustainable and entrepreneurial manner

We do business in established sectors with innovative technologies

We provide technology “made in Germany” for global markets

GESCO is comprised of adaptable, independent operating units that benefit from being part of a strong group

1. Business model

2

GESCO AG’s investment philosophy We acquire and develop industrial SMEs We have long-term goals and no intention to exit We take over majorities, almost always 100 % Most takeovers are part of succession planning The new managing directors invest up to 20 %

in their own companies (“entrepreneur companies”)

Our vision: “Best of both worlds” – We maintain the spirit of family businesses and enhance their strengths while compensating their weaknesses.

1. Business model

3

When you buy shares in GESCO, you get 17 “Hidden Champions” from the industrial German “Mittelstand”...

Mechanical engineering /

tool manufacture segment

Plastics technology segment

1. GESCO Group

4

...serving broadly diversified customer sectors.

1. GESCO Group

→

5

2%

4% 5% 5%

8%

8%

12%

13%

14%

25%

4%

Passenger and commercial vehicles

Other

Agricultural engineering

Machine and plant construction

Consumer goods Energy / supply

Iron, plate and metal processing, tool construction

Chemical / petrochemical industry

Foundries and rolling mills Electrical, medical technology, household goods

Construction, air conditioning, sanitary industry

6

1. Business model – Strategic drivers for our business

Together with her, in the last 15 years

1,000,000,000 people worldwide have joined the middle class –

in other words: the class of consumers *)

*) Source: Deutsches Institut für Entwicklungspolitik, 2012

6

7

1. Business model – Strategic drivers for our business

By the time she starts her business career in 2030, the world’s middle class will total

5,000,000,000 people *)

*) Forecast for 2030; source: Deutsches Institut für Entwicklungspolitik, 2012

7

1. Business model – Strategic drivers for our business

All these people are improving their standard of living.

They spend money on food, energy and

transportation, cars and consumer goods.

The GESCO Group provides materials, machines, tools and components “made in Germany” to fulfil these needs, via direct or indirect export.

8

1. Business model

And: the US is back! Shale gas is a game changer US to become a net exporter of energy Declining energy costs boost

reindustrialization

GESCO Group products are at hand

9

1. Business model

Materials

Machines

Tools

Components

10

11

1. Materials

Founded: 1860

Acquired: 1996

Sales 2013: € 162 m Staff: 495

Subsidiaries: Singapore, China, Taiwan, South Korea

JVs: Spain, Turkey

Leading European specialist for tool steel

Business segments:

• Tool steel (trade)

• Tool steel mould castings

• Steel works

• Precision castings

• Surface technology

Dörrenberg Edelstahl GmbH

Trigger:

In-depth expertise in metallurgy, own patents on tool steel, one-stop-shop with full range of tool steel products and services; excellent, well established customer access; strong internationalization

12

1. Machines (example)

Founded: 1931

Acquired: 1997

Sales 2013: € 34 m Staff: 140

Subsidiary in China; in Jan. 2014 acquisition of US competitor Eitel Presses Inc.

MAE Maschinen- und Apparatebau Götzen GmbH

Highly innovative, first straightening machine worldwide for big parts (30,000 mm x 850 mm)

World market leader (>60%):

• Automatic straightening machines

• Wheel set presses

Trigger:

Niche markets with high entry bar-riers; far from being overengineered; e.g. the wheel set presses are absolutely competitive compared to low-tech Chinese alternatives

13

1. Machines (example)

Founded: Roots go back to the 1960s

Acquired: 2002

Sales 2013: € 52 m Staff: 187

SVT GmbH

High-quality systems for loading and unloading liquids and gases

Specialty LNG: superior technology, No. 2 worldwide in terms of volume

Export ratio: 80%

Triggers:

The world‘s hunger for energy, and the growth of the industrial sector in emerging markets (biggest installed base: Formosa Plastics Group, Taiwan)

14

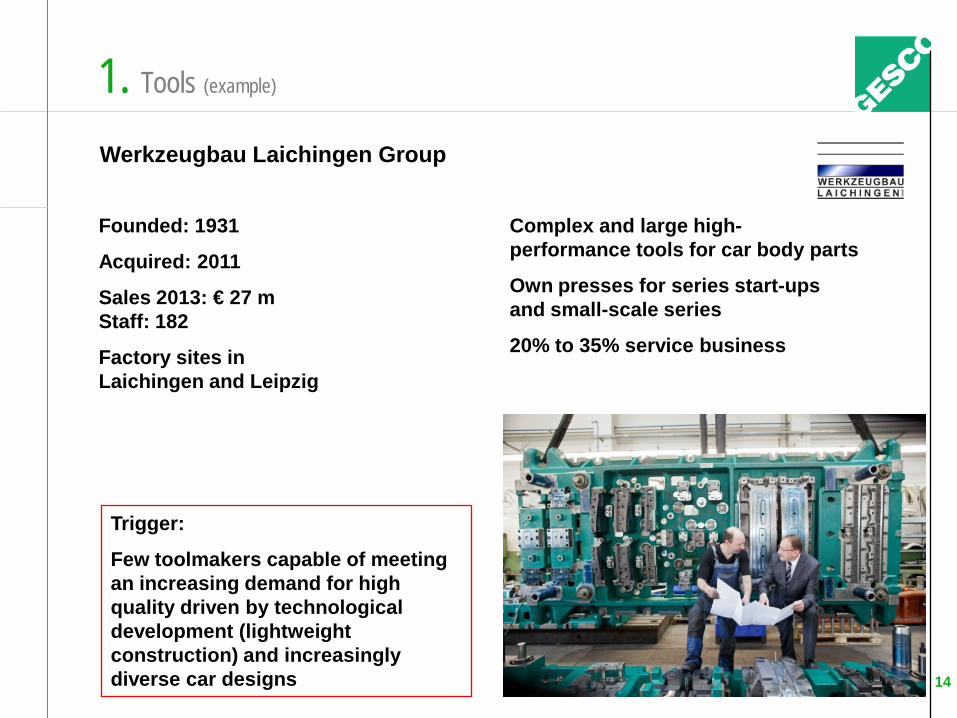

1. Tools (example)

Founded: 1931

Acquired: 2011

Sales 2013: € 27 m Staff: 182

Factory sites in Laichingen and Leipzig

Werkzeugbau Laichingen Group

Complex and large high-performance tools for car body parts

Own presses for series start-ups and small-scale series

20% to 35% service business

Trigger:

Few toolmakers capable of meeting an increasing demand for high quality driven by technological development (lightweight construction) and increasingly diverse car designs

15

1. Components (example)

Founded: 1836

Acquired: 2006

Sales 2013: € 34 m Staff: 297

Company sites in Hatzfeld/Germany, Hungary and Ukraine

Frank Walz- und Schmiedetechnik Group

Europe‘s leading forge for wearparts for the agricultural industry

Well-established brand name ORIGINAL FRANK with excellent reputation

70% of sales go to OEMs

30% go to specialized wholesale distributors and farmers

Trigger:

The world population continues to grow; in order to feed all these people, agriculture needs profes-sionalism, industrialization and reliable equipment

16

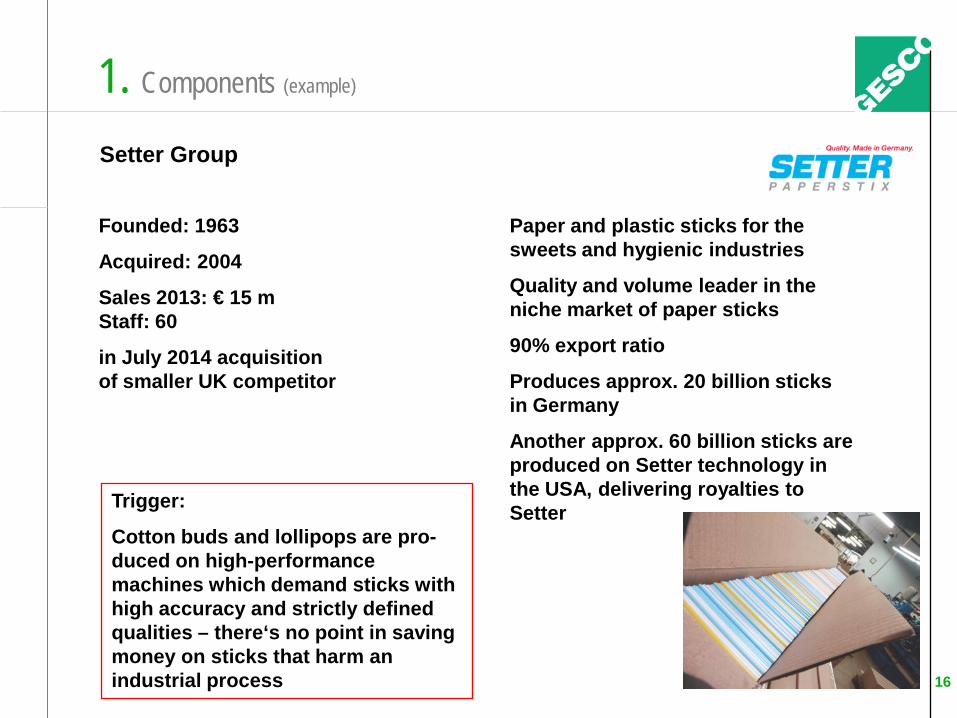

1. Components (example)

Founded: 1963

Acquired: 2004

Sales 2013: € 15 m Staff: 60

in July 2014 acquisition of smaller UK competitor

Setter Group

Paper and plastic sticks for the sweets and hygienic industries

Quality and volume leader in the niche market of paper sticks

90% export ratio

Produces approx. 20 billion sticks in Germany

Another approx. 60 billion sticks are produced on Setter technology in the USA, delivering royalties to Setter Trigger:

Cotton buds and lollipops are pro-duced on high-performance machines which demand sticks with high accuracy and strictly defined qualities – there‘s no point in saving money on sticks that harm an industrial process

2. Financial year 2014/2015

Keep in mind:

GESCO AG and GESCO Group financial year = 1 April to 31 March

Subsidiaries’ financial year = calendar year

17

2. Financial year 2014/2015

Starting position and expectations (as at Annual Accounts Press Conference on 26 June 2014)

Economic forecasts pointed to recovery (GDP: +1.9 %, VDMA: production + 3 %, GKV: sales +4 % to +5 %)

Ukraine/Russia crises affected Frank Walz- und Schmiedetechnik (wearparts for agricultural machines)

Positive signals at GESCO Group since the start of the year Demand from China has recovered

Stop on investments at major automotive suppliers no longer as strict

Situation at the companies particularly affected in 2013/2014 is improving

Special steel business at Dörrenberg Edelstahl GmbH at an appealing level good sign for the German capital goods industry

Sales at GESCO Group set to rise

Two issues weighing down earnings performance

18

2. Financial year 2014/2015

Issue 1: Protomaster GmbH

Manufactures metal forming tools Produces body parts and assemblies for small and medium-scale

series using these tools Niche position, few comparable suppliers Dramatic rise in call-off orders for several ongoing (major) orders;

labour shortage and organisational deficits Concrete support by GESCO Group, investments in future development

Issue 2: MAE Maschinen- und Apparatebau Götzen GmbH

International market leader for automatic straightening machines and wheel presses

Growth driven strongly by innovation; sales more than doubled between 2006 and 2013; extensive construction and expansion projects with new administration and production building

Burdens on several fronts due to strong operating growth, construction activities, technical challenges, Eitel acquisition and organisational development, labour bottlenecks

Active support by GESCO AG

19

2. Financial year 2014/2015

General current situation :

Geopolitical risks affect general business climate and customers’ willingness to invest

VDMA cuts outlook for production from +3 % to + 1 %

GDP outlook expected to be lowered

The Ukraine/Russia crisis, sanctions against Russia and Russian countermeasures will have impact on German industry

20

2. Financial year 2014/2015 – Q1

Q1: mixed picture

Includes operating months January to March 2014 at subsidiaries

Stable business – sales slightly up

Earnings burdened by the two subsidiaries

Order intake on an encouragingly high level

21

2. Financial year 2014/2015 – Q1

QI 2013/2014

QI 2014/2015

Change

Order intake € million 110.4 126.7 14.7 %

Sales € million 108.9 109.5 0.6 % EBITDA € million 11.9 11.4 -4.6 %

EBIT € million 7.9 6.9 -12.8 % Group net income after minority interest

€ million

4.5

3.7

-16.7 %

EPS acc. to IFRS € 1.35

31.03.2014

1.13

30.06.2014

-16.7 %

Equity € million 176.6 180.5 2.2 % Equity ratio % 46.5 44.9 - Liquid funds € million 38.8 48.3 24.5 %

22

2. Financial year 2014/2015 – Q2

Q2: Less lively development

Includes operating months April to June 2014 at subsidiaries

Sales approx. € 110 million – on par with Q1, slightly above Q2 prev. year (€ 108.9 million)

Order intake approx. € 100 million – clearly below Q1, slightly below Q2 prev. year (€ 101.5 million)

23

2. Financial year 2014/2015

Sales and incoming orders by quarter (in €'000)

─ Incoming orders ─ Sales

24

20.000

40.000

60.000

80.000

100.000

120.000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2009 2010 2011 2012 2013 2014

2. Financial year 2014/2015

2013/2014 Actual figures

2014/2015e

Target June 2014

2014/2015e

Target Aug. 2014

Change

yoy

Group sales € million 453.3 470 to 480 470 +3.7 %

Group net income for the year after minority interest

€ million 18.1 17.5 to 18.5 17.5 -3.3 %

Earnings per share acc. to IFRS

€ 5.45 5.26 to 5.56 5.26 -3.3 %

Target figures

25

Current M&A situation Fewer offers, probably because …many industrial companies recorded declines in

incoming orders, sales and earnings in 2013 not an ideal basis for approaching investors

…business owners wonder what to do with the money in a zero-interest environment

Increasing competition, e.g. from family offices

Nevertheless: two projects currently in due diligence A direct acquisition by GESCO AG A strategic enhancement of a subsidiary abroad

2. M&A

26

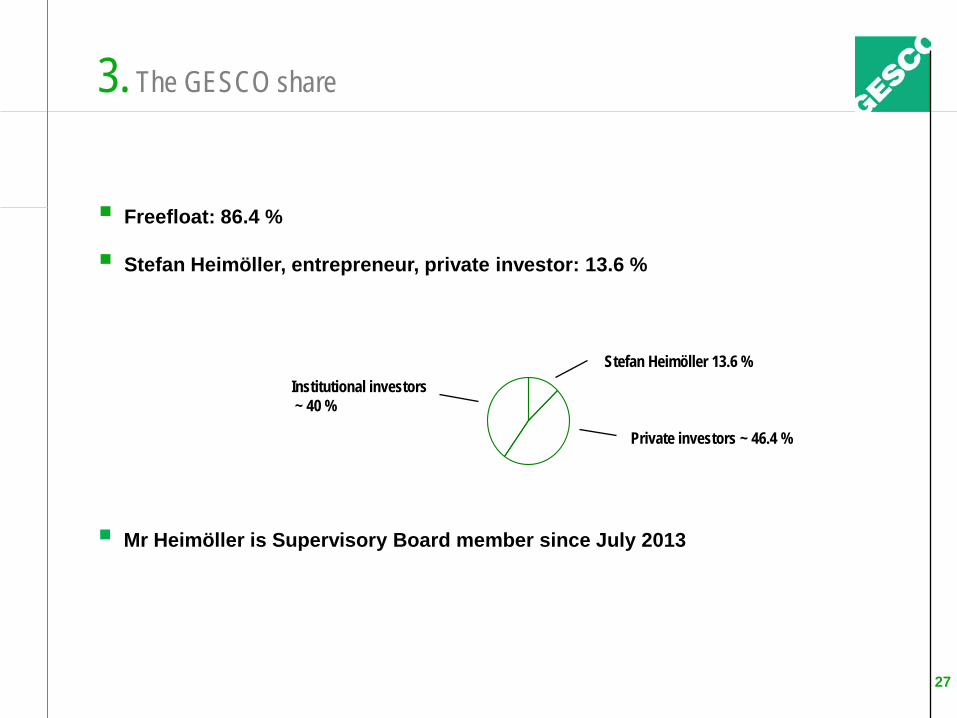

3. The GESCO share

Freefloat: 86.4 %

Stefan Heimöller, entrepreneur, private investor: 13.6 %

Stefan Heimöller 13.6 %

Private investors ~ 46.4 %

Institutional investors ~ 40 %

Mr Heimöller is Supervisory Board member since July 2013

27

3. Dividend

2010/2011 2005/2006 2006/2007 2007/2008

€ 2.00

€ 1.25

€ 1.50

€ 2.20 base dividend

€ 0.22 dividend bonus

€ 2.42 € 2.50

2008/2009 2009/2010

€ 1.30

2011/2012

€ 2.90

€ 2.50

2012/2013 2013/2014

€ 2.20

28

3. Share price development (in %) – 1 and 5 years

GESCO vs. SDAX, 1 year GESCO vs. SDAX, 5 years

29

90

100

110

120

130

GESCO

SDAX

80

100

120

140

160

180

200

220

240

GESCO

SDAX

3. Share price development (in %) – 10 years

GESCO vs. SDAX, 10 years

30

0

100

200

300

400

500

GESCO

SDAX

Founded: 1989 Share capital: € 8,645,000 Shares: 3,325,000 registered shares Free float: 86.4 % Stock markets: Xetra; Frankfurt (regulated market); Berlin, Düsseldorf, Hamburg, Hanover, Munich, Stuttgart (open market) Sec. identification number: A1K020 ISIN: DE000A1K0201 IPO: 24 March 1998 Index: SDAX End of financial year: 31 March Designated sponsors: equinet Bank AG Close Brothers Seydler Bank AG

Facts and figures on GESCO AG

31

GESCO Group overview Company Sales 2013

€‘000 Staff

31/12/2013 GESCO AG

shareholding

Astroplast Kunststofftechnik GmbH & Co. KG 14,282 77 80%

Paul Beier GmbH Werkzeug- und Maschinenbau & Co. KG 8,901 114 100%

C.F.K. CNC-Fertigungstechnik Kriftel GmbH 6,740 49 80%

Dömer GmbH & Co. KG Stanz- und Umformtechnologie 13,716 102 100%

Dörrenberg Edelstahl GmbH 161,782 495 90%

Frank Group 33,547 297 100%

Franz Funke Zerspanungstechnik GmbH & Co. KG 16,130 81 80%

Haseke GmbH & Co. KG 12,359 61 80%

Hubl GmbH 10,257 106 80%

Georg Kesel GmbH und Co. KG 10,723 68 90%

MAE Maschinen- und Apparatebau Götzen GmbH 34,078 140 100%

Modell Technik GmbH & Co. Formenbau KG 13,979 106 100%

Protomaster Riedel & Co. GmbH 7,700 85 82.17%

Setter Group 14,773 60 100%

SVT GmbH 51,770 187 90%

VWH Vorrichtungs- und Werkzeugbau Herschbach GmbH 10,809 105 80%

Werkzeugbau Laichingen Group 26,573 182 85% 32

Financial calendar and investor relations contact

Financial calendar

28 August 2014 Annual General Meeting

2 September 2014 Small Cap Conference, Frankfurt/Main

14 November 2014 Q2 figures (01.04 to 30.09.2014)

25 November 2014 German Equity Forum, Frankfurt/Main

February 2015 Q3 figures (01.04 to 31.12.2014)

25 June 2015 Annual Accounts Press Conference and Analysts’ Meeting

Investor Relations

GESCO AG Phone: +49 202 24820-18 Investor Relations Fax: +49 202 24820-49 Oliver Vollbrecht E-mail: [email protected] Johannisberg 7 Internet: www.gesco.de 42103 Wuppertal

Germany

33

Recommended