European HRC prices at a 5-year low – factors suppressing a recovery

Marina Maliushkina June 18th, 2015

From US to Europe: 2015 Steel Market Update

This document does not constitute an offer or solicitation to buy or sell any investment product(s). It does not take into account the specific investment objectives, financial situation or particular needs of any person. Investors should seek advice from a financial adviser before investing in any investment products or adopting any investment strategies. In the event that the investor chooses not to seek advice from a financial adviser, he/she should consider whether the product in question is suitable for him/her. The investment product(s) discussed herein are subject to significant investment risks, including the possible loss of the principal amount invested. Past performance of investment products is not necessarily a guide to future performance.

Unless expressly stated, we do not make any representations nor give any warranties in respect of the information contained in this presentation. To the extent permitted by the applicable law, we hereby exclude all warranties, conditions, representations or duties whatsoever and howsoever arising (whether express or implied) including but not limited to any representations or warranties as to the ownership of intellectual property or other rights in the presentation, or the satisfactory quality, merchantability or fitness for a particular purpose of, any goods or services referred to at any time in this presentation, any express or statutory warranties, and any warranties or duties regarding accuracy, timeliness, completeness, performance, availability, lack of negligence or of workmanlike effort.

To the fullest extent allowed by applicable law, you agree that we will not be liable to you or your business under any circumstances whatsoever (whether in contract, negligence or any other tort, breach of statutory duty or otherwise) for any loss of profits, income, business interruption, loss of business information or for increase in any costs, liabilities or expenses or any other loss whatsoever and however arising directly or indirectly out of or in connection with or relating to the information in this presentation and we shall not be liable for any loss, damages, costs, expenses or other liability which you incur or suffer as a result of your use of the information in this presentation.

We take all such steps as are reasonably necessary to provide information that is accurate and reliable, but exclude to the fullest extent permitted by law any liability for the inaccuracy of the information in this report.

The Steel Index (TSI) used all reasonable endeavours to certify the correctness of the information contained in this presentation.

Without limiting the above, you acknowledge and agree that we shall not be liable for matters beyond our reasonable control including but not limited to information gathered during field visits, third party information presented or the acts of third parties.

You understand and expressly agree that use of the information presented here is at your sole risk, that any content, material and/or data presented or verbalised or otherwise obtained through your use of the information in this presentation is at your own discretion and risk and that you will be solely responsible for any damage to you personally or your company or organization or business associates whatsoever which in any way results from the use, reliance or application of such content material and/or data and/or information.

All INFORMATION PRESENTED IN THIS REPORT IS AGREED TO BE CONFIDENTIAL AND CANNOT BE REPRODUCED WITHOUT THE EXPRESSED PERMISSION OF THE STEEL INDEX

Disclaimer

Introduction to TSI

Impartial organisation focused on compiling prices for ferrous metal products

Founded in in 2006 as subsidiary of the Steel Business Briefing (SBB) Group, acquired by Platts in July 2011

Continues to operate under TSI brand as a separate unit within Platts, part of McGraw-Hill Financial

Data-driven methodology using transaction data to calculate volume-weighted price indices

TSI “Data Providers” submit spot transaction data to TSI under confidentiality agreement; physical market participants only (over 600 registered today)

Submission direct to TSI database through secure on-line channel

Data normalised and “cleaned” before volume-weighted averages calculated for the day or week

TSI is a specialist price information service

European HR Coil Prices

Source: TSI

HRC Prices: Downward Trend

EUR/tonne

• Persistent declining price trend

• Affected by weak raw materials prices, subdued demand, pressure from imports

360

380

400

420

440

460

480 N. Europe S. Europe

€415/t €405/t

€391/t €376/t

European HR Coil Prices

Source: TSI

Low Price Volatility

EUR/tonne

94

100

58

24

92

86

57

29

2012 2013 2014 2015 YTD360

380

400

420

440

460

480

500

520

540

560

580 S. Europe HRC N. Europe HRC

Source: Eurofer

Gradual Recovery in Demand EU Apparent Steel Consumption

Million tonnes

203

187

122

148 158

141 141 146 149 153

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012 2013 2014 2015 (f) 2016 (f)

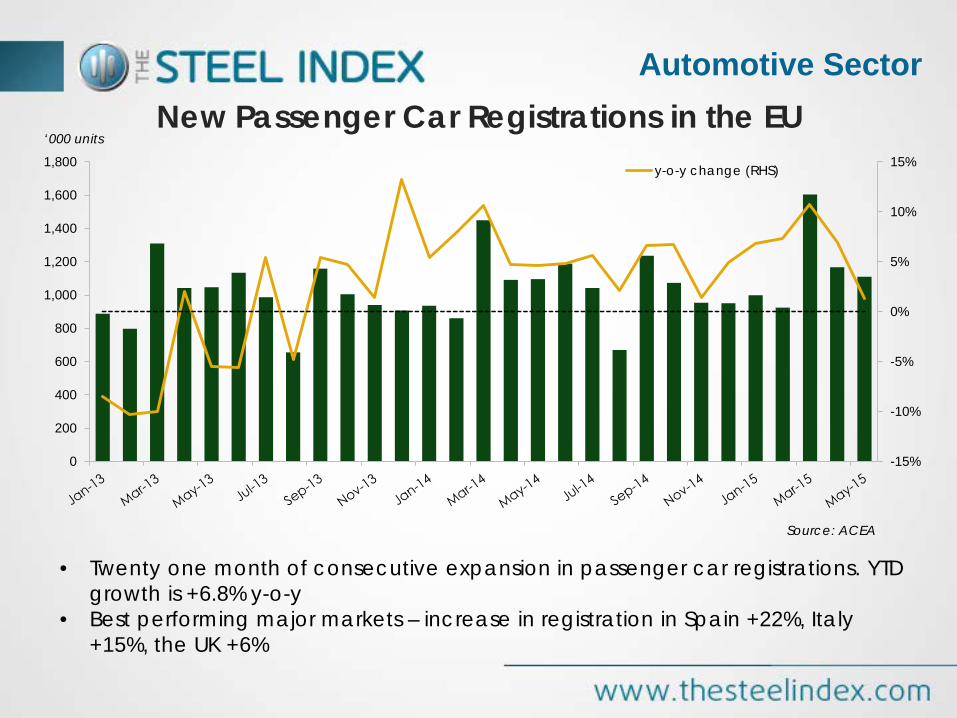

New Passenger Car Registrations in the EU Automotive Sector

Source: ACEA

‘000 units

-15%

-10%

-5%

0%

5%

10%

15%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800 y-o-y change (RHS)

• Twenty one month of consecutive expansion in passenger car registrations. YTD growth is +6.8% y-o-y

• Best performing major markets – increase in registration in Spain +22%, Italy +15%, the UK +6%

West European Car Sales and 2015 Forecast

Automotive Sector

Source: LMC Automotive

Million units

12.98 12.81

11.77

11.55

12.10

12.88

10.5

11

11.5

12

12.5

13

13.5

2010 2011 2012 2013 2014 2015 (f)

• Eurofer: total automotive output – including production of parts and components - is expected to increase by around +4.5% in 2015

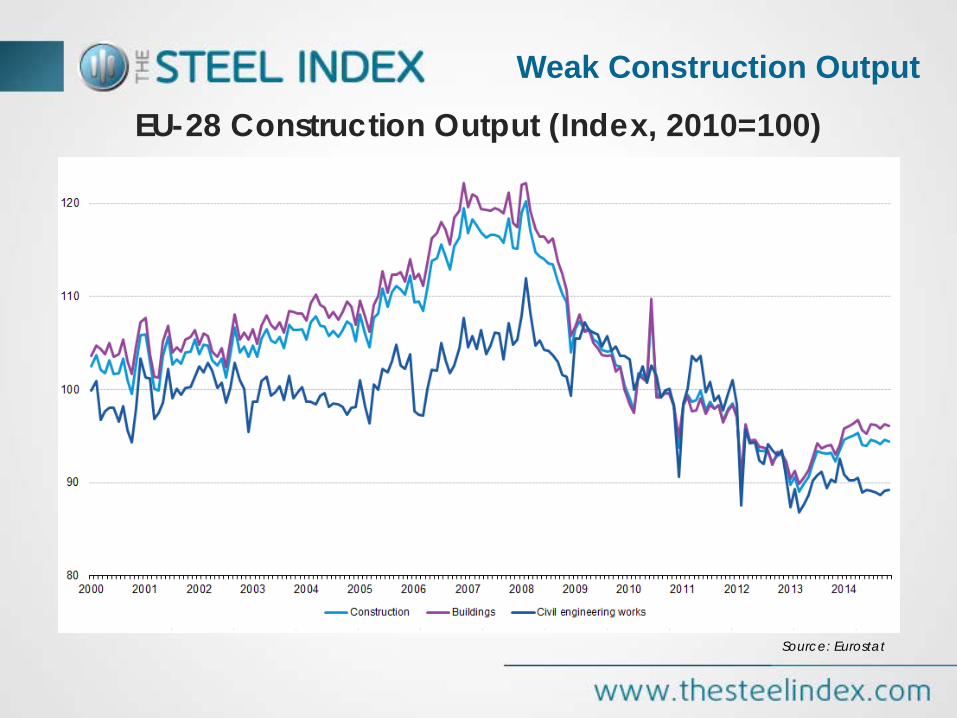

EU-28 Construction Output (Index, 2010=100)

Source: Eurostat

Weak Construction Output

Source: EUROCONSTRUCT

Growth Phase

EU-19 Construction Output Growth Y-o-y % Change

2.2

-4.0

-8.8

-3.5

0.3

-5.4

-2.7

1.0

2.1 2.2 2.2

-10

-8

-6

-4

-2

0

2

4

2007 2008 2009 2010 2011 2012 2013 2014 2015 (f) 2016 (f) 2017 (f)

Source: WSA

Cuts in Steel Production

EU Crude Steel Production ‘000 tonnes

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014 2015

German Distributors' Steel Inventories

Source: BDS

Lower Stock Levels

‘000 tonnes

2,000

2,100

2,200

2,300

2,400

2,500

2,600

2,700

2,800

• Negative impact of overcapacity on the distribution sector – estimated by Eurometal to be around 30% of the total capacity

• With expectations of stable or lower prices, YTD level of inventories, held by the German distributors, is -6% lower y-o-y

EU Flat Steel Imports

Source: Eurofer

Growth in Imports

‘000 tonnes

• Imports into EU outpace growth of demand • Flat steel imports into the EU rose by +16% y-o-y in 2014. • First indications in 2015: imports rising further. Eurofer forecasts a +4% increase

in total steel imports in 2015

0

200

400

600

800

1,000

1,200

1,400

1,600

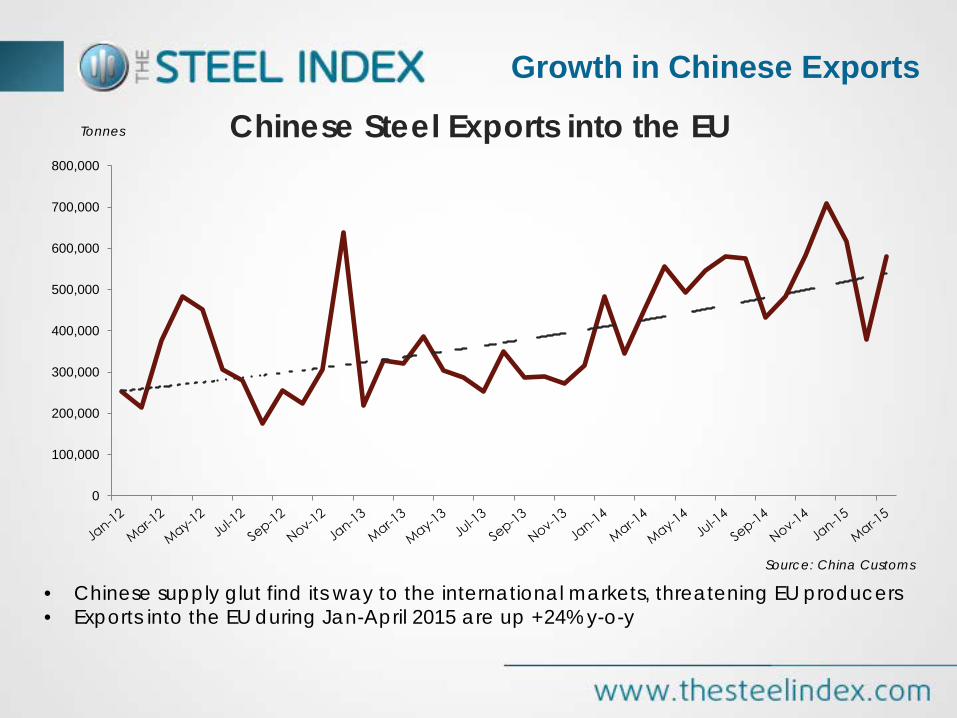

Chinese Steel Exports into the EU

Source: China Customs

Growth in Chinese Exports

Tonnes

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

• Chinese supply glut find its way to the international markets, threatening EU producers • Exports into the EU during Jan-April 2015 are up +24% y-o-y

Duties and AD Investigations in 2015

Trade Protectionism

April 2015: • The EC started an AD investigation into imports of ‘high fatigue performance’ rebar

from China. Primarily affected imports of rebar into the UK and Ireland.

May 2015: • Provisional AD measures are introduced against imports of grain-oriented electrical

steel from Russia, USA, Japan, Korea and China; duties are ranging from 21.6% to 35.9%.

• The EC opened an AD investigation into imports of CRC from China and Russia.

March 2015 • The European Commission (EC) imposed provisional

anti-dumping duties of up to 25.2 % on Stainless Steel CR imports from China and up to 12.0 % on imports from Taiwan, following the complaint which was filed by Eurofer in May 2014.

EU Flat Steel Exports into the USA

Source: AISI

Export Opportunities

Tonnes

• With weaker prices in the domestic US market, export opportunities for the EU producers decreased

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

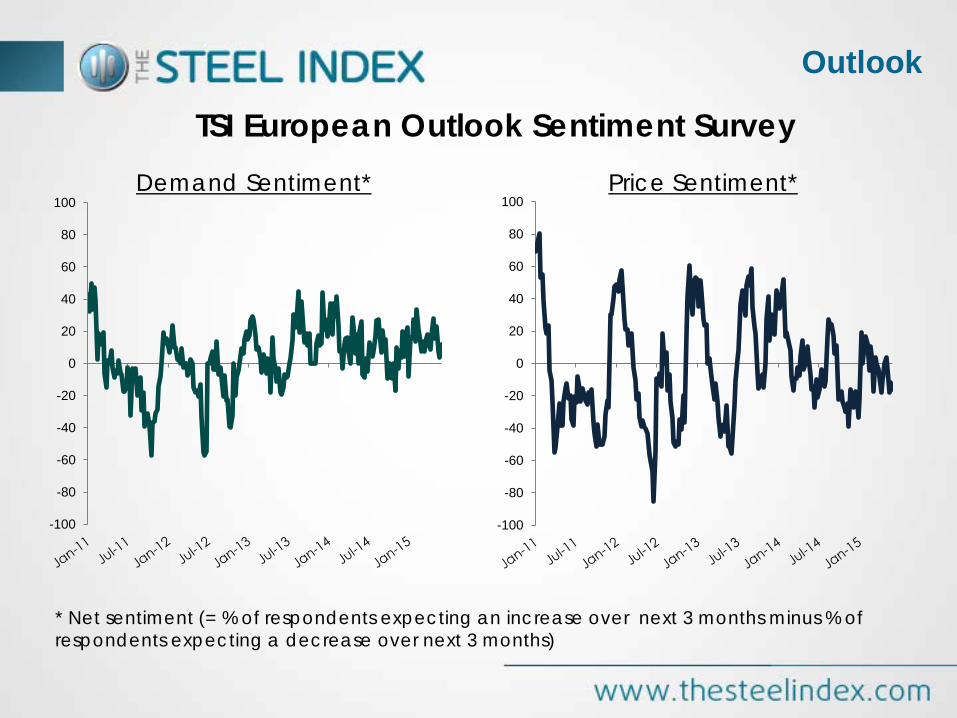

TSI European Outlook Sentiment Survey

Outlook

Demand Sentiment* Price Sentiment*

* Net sentiment (= % of respondents expecting an increase over next 3 months minus % of respondents expecting a decrease over next 3 months)

-100

-80

-60

-40

-20

0

20

40

60

80

100

-100

-80

-60

-40

-20

0

20

40

60

80

100

North European HRC Swaps – Cumulative Volume Cleared

Steel Derivatives

Sources: LCH.Clearnet, CME Europe

Tonnes

0

50,000

100,000

150,000

200,000

250,000

300,000

• LCH.Clearnet and CME Clearing Europe offer North and South European HR coil steel contracts basis TSI’s daily indices

Recommended