1

Paper to be presented at OECD Workshop on Productivity Analysis and

Measurement, Bern, 16-18 October 2006

Estimates of Labor and Total Factor Productivity

by 72 industries in Korea (1970-2003)

October 16, 2006

Hak K. Pyo, Keun Hee Rhee and Bongchan Ha*

*Seoul National University, Korea Productivity Center and Korea Institute

for Industrial Economics respectively. An earlier version of this paper (data

structure part) was presented at EU-KLEMS Workshop in Valencia, May 7-9,

2006. We acknowledge financial support by the Bank of Korea and Korea

Institute of International Economic Policy and research assistance of

Eunkyung Jeon and Sun Young Jung at Seoul National University.

[email protected] for correspondence.

2

Estimates of Labor and Total Factor Productivity by 72 industries in Korea (1970-2003)

Hak K. Pyo, Keun Hee Rhee and Bongchan Ha*

Abstract

As Krugman (1994), Young (1994), and Lau and Kim (1994)'s studies showed,

the East Asian economic miracle may be characterized as `input-led' growth.

However, both the stagnation in investment and the decrease in average

working hours combined with decrease in the fertility rate require a productivity

surge for a renewed sustainable growth in East Asia. The purpose of our study

is to identify the sources of economic growth based on a KLEMS model for the

Republic of Korea which experienced a financial crisis in 1997 after joining

OECD. We report estimates of KLEMS inputs and gross output in Korea based

on 72-industry classification following EU KLEMS project guidelines. We also

provide estimates of 72 industry-level labor productivity and total factor

productivity. We have found that Korea’s catch-up process with industrial

nations in its late industrialization has been predominantly input-led and

manufacturing based as documented in Timmer(1999) and Pyo (2001). We

have also found that TFP growth has been positively affected by the growth of

labor productivity and output growth. However, since its financial crisis in

December 1997, the sources of growth seem to have switched to TFP-growth

based and IT-intensive Service based. But lower productivity in service

industries due to regulations and lack of competition seems to work against

finding renewed sustainable growth path.

JEL-Classification: O14, O47

Key-Words: Labor Productivity, Total Factor Productivity, sustainable growth

*Seoul National University, Korea Productivity Center and Korea Institute for I

ndustrial Economics respectively. [email protected] for correspondence.

3

1. Introduction In recent years, especially since the 1997 economic crisis in the East Asian

countries including Korea, considerable changes have taken place in the

Korean economy, such as investment stagnation (see e.g. Pyo(2006) Pyo and

Ha (2005)), changes in production input patterns, and so on. One of the most

important changes is the demand for high productivity, which would

compensate the recent slowdowns of growth rates in capital and labor inputs.

As Krugman (1994), Young (1994), and Lau and Kim (1994) showed, the East

Asian economic miracle may be summarized as `input-led' growth. Korea was

no exception in this respect of growth pattern.

However, both the stagnation in investment and the decrease in average

working hours require a productivity surge for long-term growth in Korea. In

addition, a sharp decrease in the fertility rate in Korea necessitates productivity

increase in order to improve the present income level and facilitate the support

of the large elderly population by the small numbers of working age adults. For

these reasons, `productivity-driven' growth is indispensable for Korea.

According to Lewis (2004), the fast economic growth in Korea is the result of

both large labor input and capital accumulation. He argues that the average

working hours is 40% higher than that of the U.S., and almost a third of GDP

has been allocated to investment, while GDP per capita in Korea is about half of

the U.S. GDP per capita. The focus is changing from how much inputs are put

into production to how well those are organized.

The purpose of this paper is to explain the data structure of Korea for the

estimation of productivities by industry in KLEMS model and present preliminary

estimates of labor productivity and total factor productivity (TFP) at reasonably

detailed industry level. We have used 72-sector industrial classification following

the guidelines of EU KLEMS project for the future comparability with EU

member countries, the United States, and Japan. Therefore, an analysis based

on detailed industrial classification gives us better views on productivity and

growth, which is difficult to grasp in broader industrial classifications. Industries

in an economy have shown different productivity trends and growth patterns

according to their characteristics of production, competition policies, and other

economic and non-economic circumstances.

4

KLEMS model is a kind of gross output growth accounting in which output is

measured by gross output and inputs are decomposed by capital (K), labor (L),

energy (E), material (M), and service (S). Since this methodology is basically

based on gross output, it has the advantage of eliminating effects of

intermediate inputs from other industries on productivity, therefore allowing

productivities by industry to be more accurate. Moreover, the assumption on

real value-added production function (separability assumption) is not usually

guaranteed1, which also gives legitimacy to gross output growth accounting.

However, gross output growth accounting requires more information on

intermediate inputs than value-added growth accounting. Therefore, the data

structure for estimating productivity has to be consistent with not only national

income accounts but also input-output tables, Use and Make Matrix etc. and the

estimation methodology for unavailable data should be examined more carefully.

We have found that Korea’s catch-up process with industrial nations in its late

industrialization has been predominantly input-led and manufacturing based.

We have also found that TFP growth has been positively affected by the growth

of labor productivity and output growth. However, since its financial crisis in

December 1997, the sources of growth seem to have switched to TFP-growth

based and IT-intensive Service based. But lower productivity in service

industries due to regulations and lack of competition seems to work against

finding renewed sustainable growth path.

This paper is organized as follows. Section 2 examines data structure including

the methodology of measuring gross output by industry from Input-Output

Tables and National Accounts published by the Bank of Korea and input

measurements. Section 3 presents the estimates of labor productivity and TFP

by 72-industry and examines the relations between labor productivity and TFP

and between output growth and TFP growth by periods. Section 4 concludes

the paper.

1See Berndt and Christensen (1973,1974), Berndt and Wood (1974), Denny

and Fuss (1977), and Yuhn (1991) for the U.S., and Pyo and Ha (2006) for

Korea

5

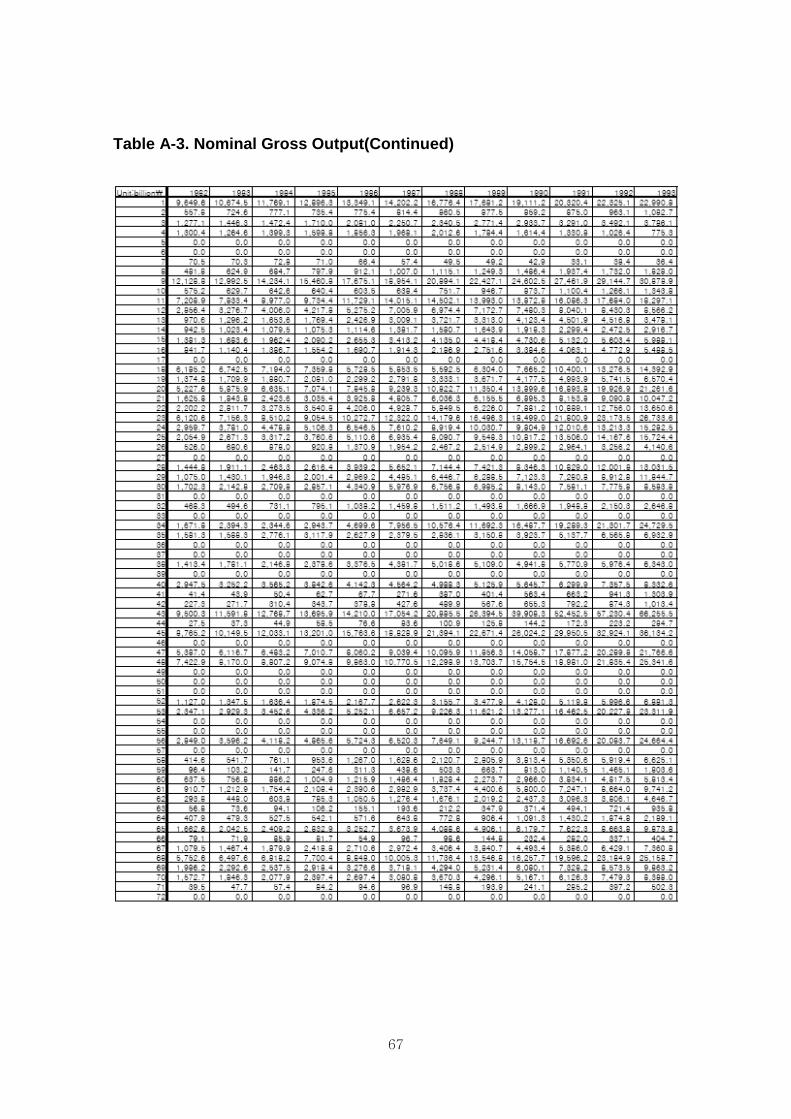

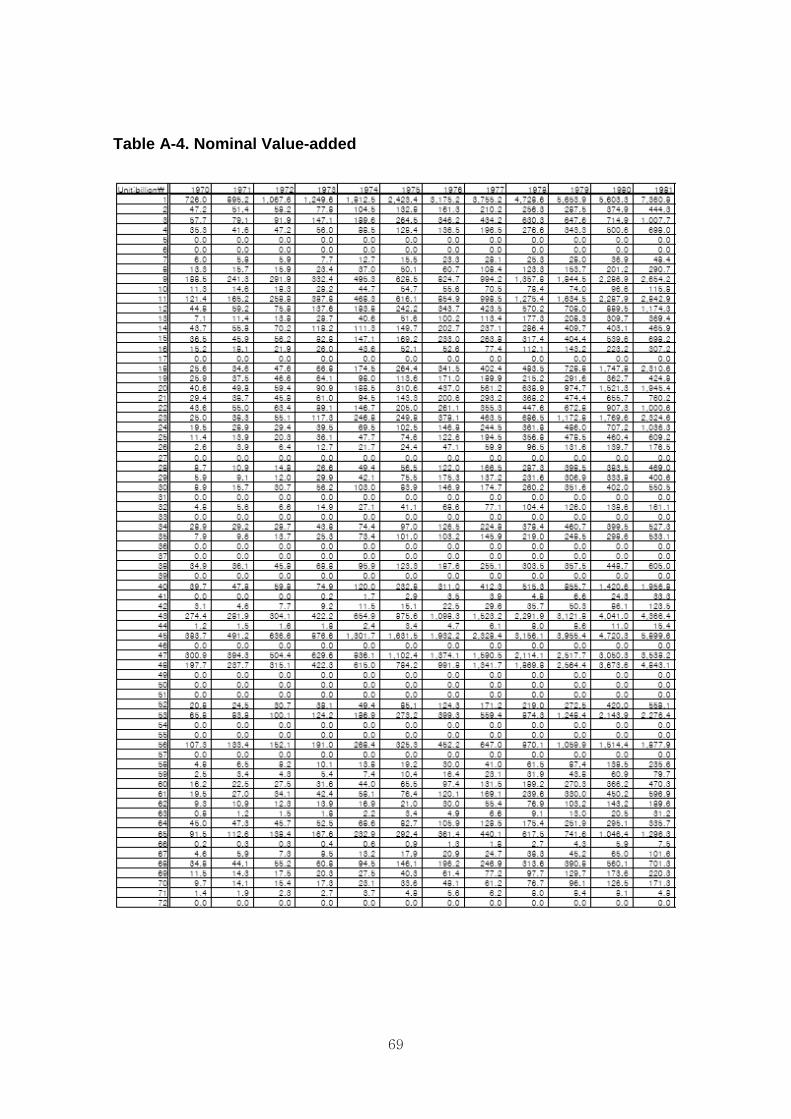

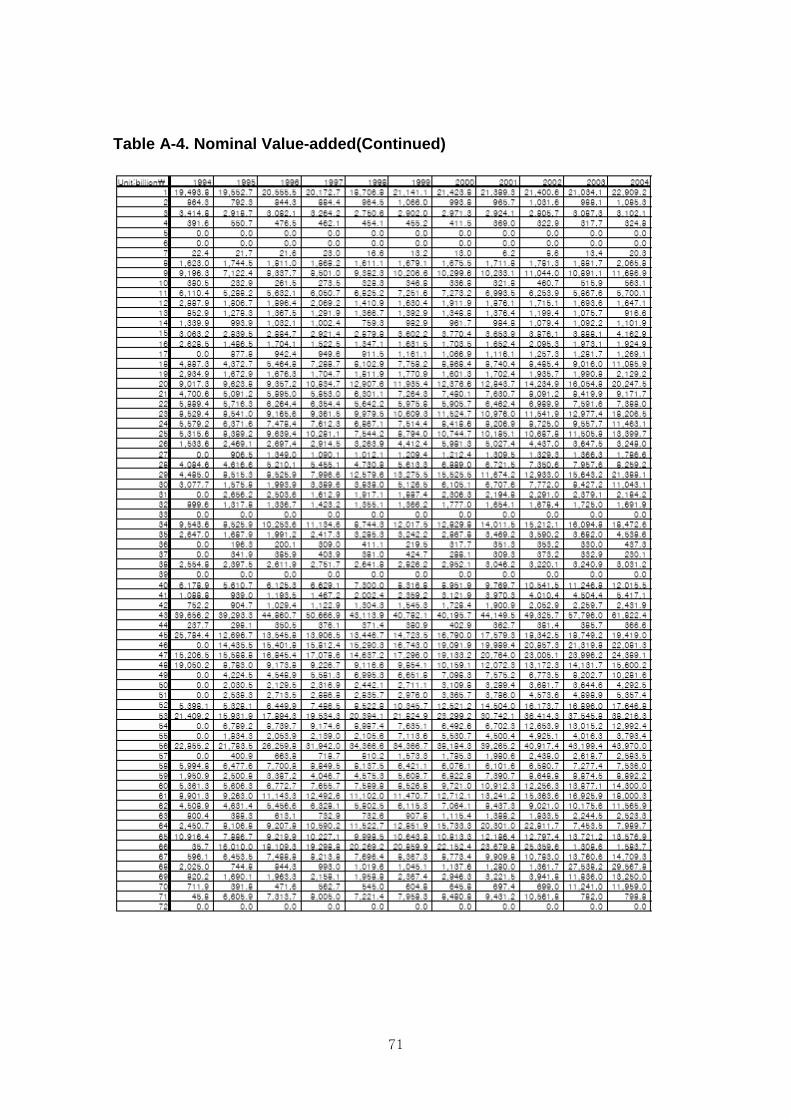

2. Data Structure

2.1 Gross Output Data

National Accounts by the Bank of Korea (1999, 2004) report annual series

(1970-2002) of nominal gross outputs at basic prices, both nominal and real

value-added at basic prices, nominal compensation of employees, and

operating surplus at current prices of 21 industries including 9 manufacturing

industries. Those data can be extended to the year 2005 from ECOS (Economic

Statistics System) in the Bank of Korea website2. National Accounts (1987,

1994, 1999, 2004) also reports annual series (1985-2002) of both nominal and

real Make Tables (V-Tables) and real Use Tables (U-Tables).

In addition to nominal gross output and both nominal and real value-added, real

gross output at basic prices and real intermediate inputs at purchase prices can

be obtained from Use Tables. However, since Make Tables and Use Tables for

the years 1970-1984 and 2003-2004 are unavailable, we have generated them

through RAS method using annual data from National Accounts and Input-

Output Tables, and benchmark tables of 1985 and 2000, respectively. As the

published Use Tables of National Accounts in Korea present the Domestic and

Import Use Tables combined, we have not been able to isolate them into two

separate tables. In the case of Use Tables before 1995, all the intermediate

commodity inputs by industry are measured at purchase prices. Since 1995,

those inputs have been measured at incomplete basic prices in the sense that

those inputs include trade and transportation margins but isolate net production

tax to the last row of intermediate input matrix. Because we have no information

for transformation of the Use Tables from purchase prices to basic prices before

1995 and the Use Tables after 1995 have been measured at incomplete basic

prices, we have changed the Use Tables at basic price after 1995 into Use

Tables at purchase price allocating net production tax to each commodity

proportional to each volume.

2http://www.bok.or.kr

6

The Bank of Korea has also published Input-Output Tables (commodity-by-

commodity) since 1960. Its most recent 2000 Input-Output Table is the 19th

Table. The detailed description of Input-Output Tables during 1970-2000 is

summarized in Table 1. Input-Output Tables of Korea have relatively detailed

information, even though they are restricted to commodity-by-commodity tables.

For example, the table for 2000 has 28, 77, 168, 404 commodities in large,

medium, small, and basic classifications, respectively.

Table 1. Input-Output Tables in Korea

Year Basic Small Medium Large

1970 153 56

1973 153 56

1975 392 164 60

1978 164 60

1980 396 162 64

1983 396 162 64 19

1985 402 161 65 19

1986 161 65 20

1987 161 65 20

1988 161 65 20

1990 405 163 75 26

1993 163 75 26

1995 402 168 77 28

1998 168 77 28

2000 404 168 77 28

(Number of commodity classification)

(1) Estimation of Use Tables

While National Accounts do not contain detailed information about industries

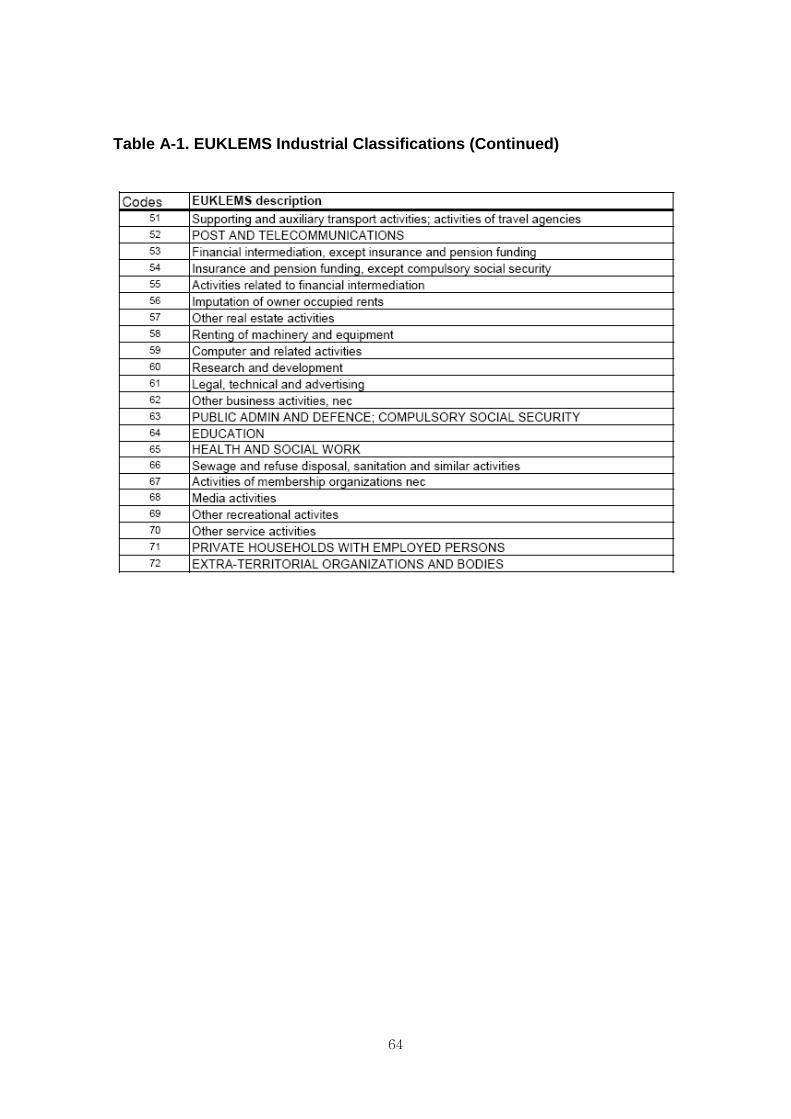

(21 industries), our industrial classification is 72 industries according to EU

KLEMS classification (See Appendix Table A-1). In order to reconcile the

National Accounts data to our industrial classification, we have used other data

sources, such as Mining & Manufacturing Census and Surveys, Wholesale and

7

Retail Surveys, and so on. Since we do not have detailed information on

intermediate input structures, we have assumed the same intermediate input

structures for the industries belonging to the same category of National

Accounts classification. As for Input-Output Tables, they have detailed

commodity classifications enough to match the 21-commodity classification in

National Accounts. However, since they are not annually published, we have used interpolation method for the missing years. We have attached

reclassification of National Accounts into 72 industries in Appendix Table A-2.

Since the Bank of Korea reports nominal and real Make(V) Tables and real

Use(U) Tables, nominal Use Tables should be generated for obtaining nominal

intermediate input shares, which are used in estimating total factor productivity.

Following Timmer (2005), we have used the commodity prices to nominalize all

uses of the commodities under the assumption that the same commodity has

the same price whichever industry uses it.

where PijX

denotes a price index for intermediate input of commodity i in

industry j , and PiC denotes a price index of commodity i .

The commodity prices ( PiC ) we have used are the weighted averages of

domestic and imported commodity prices, since the Use Tables cannot be

separated into domestic and imported Use Tables to apply separated prices.

Producer's Price Index (PPI) has been used as a proxy for domestic commodity

prices ( PiD ), and Imported Price Index (CIF) has been used as imported

commodity prices( PiIM ). Even though PPI is not purchaser's price for the lack

of transportation and trade margins, it is a reasonable proxy for domestic

commodity price index.

The above procedure can be shown as follows:

We can derive real domestic commodity inputs ( XiD ) subtracting real imported

8

commodity inputs in Input-Output Tables ( XiIM ) from real commodity inputs in

Use Tables ( Xi ).

From Eq (2), we can calculate the weighted average commodity price index

using nominal domestic and imported intermediate commodity inputs.

Using Eq (1) and (3) we have nominalized each intermediate input in Use

Tables, and normalized its value in order to equalize it with the nominal

intermediate inputs in National Accounts as following:

where PXij1

and PXij denote a first estimate and a final estimate of

intermediate input commodity i in industry j , respectively. Xij denotes

real intermediate input commodity i in industry j , and PXj denotes

total nominal intermediate input in industry j .

9

(2) Estimation of Make and Use Tables for the Missing

Years

We have estimated the Make and Use Tables for the missing years, 1970-1984

and 2003-2004 through a biproportional adjustment methodology, RAS. For the

years 1970-1984 we have used the 1985 tables as benchmark tables, and for

the years 2003-2004 we have used the 2002 tables. We have annual series of

each industry's gross output, value-added, intermediate input, and so on.

However, because we do not have annual series of each commodity's data in

Input-Output Tables, we have applied the interpolation method between existing

tables and normalized them to the National Accounts data.

(3) Aggregation Issues

A Make and Use Table framework gives more detailed information of

transactions in an economy than aggregated National Accounts data: constant

values, volume indices, and price indices of commodities. In addition to this, the

ESA 95 Input-Output Manual (2002) gives more advantages: (1) the numerical

consistency, reliability and plausibility, (2) different volume indices and deflators

according to different level of aggregation, and (3) relationship between trade

and transport margin, taxes, subsidies, and so on.

We have applied a simple summation for the Make Table aggregation over

commodities under the assumption of the same deflator over all commodities

produced in the same industry following Timmer (2005). With regard to the

aggregation in Use Tables, we have not applied any aggregation technique

considering each commodity as different inputs.

In order to aggregate detailed industrial data, we have used chained Laspeyres

Index following Timmer (2005). While the major advantage of chained

Laspeyres index is additivity, it can also give us an advantage of a better match

between products in consecutive time periods than between periods that are far

apart (SNA -1993). Since this index uses changing weights, the problems of

rapid shifts in the composition of an economy are minimized.

10

(4) Make Tables at Purchase Prices and Use Tables at

Basic Prices

Purchase prices and basic prices are defined as follows:

We will explain the method of transforming Make Tables at basic prices into

those at purchase prices, but the reverse procedure can be applied without

significant modification.

In order to transform Make Tables at basic prices into those at purchase prices,

valuation matrices of the above four components ( TRij , TTij , TVij , and

Tij ) are needed. However, the information we have regarding those

components are only the commodity vectors of TR, TT, and T3. The data

regarding non-deductible VAT does not exist. Due to data unavailability, we

have not been able to transform Make Tables at basic prices into those at

purchase prices in matrix forms as follows:

3Those vectors have been obtained from Input-Output Tables (commodity-by-

commodity), so we are not able to know industry-by-commodity matrix.

11

where PYijpur

and PYijbas

denote the supply of commodity i in industry

j. We have transformed Make Tables at purchase prices into vector forms of commodity adding up the rows over industry like the following

Also, in order to isolate imported commodities from total commodity supply, we

have used the information on imported commodity vectors from Input-Output

Tables to derive the following vectors:

where PYiD and PYi

IM denote domestic and imported (before tariffs)

commodity supply, respectively. Trade margins and Transportation margins are

normalized to equal the total supply of the respective commodity. Net taxes on

products and imports are also normalized to respective National Accounts

annual series.

The above procedures have been applied to transform Use Tables at purchase

prices into those at basic prices. Use Tables at basic prices have also been

generated incompletely by subtracting the valuation commodity vectors from the

commodity directions.

The above procedures have been shown in Figure 1 and 2, and the trends of

gross output and value-added have been shown in Figure 3. As can be seen in

Figure 3, there was no real break in gross output growth in Korea’s economy-

wide economic performance except in the year 1998 after the financial crisis in

December 1997. Even during the years of first oil crisis of 1974-1975 and the

second oil crisis of 1980-1981, the Korean economy’s real gross output

continued to grow without major setbacks.

After the economic crisis of December 1997, Korean economy had to go

through IMF-mandated adjustment and restructuring program as documented in

12

Pyo (2004). We observe that even though economy-wide labor productivity

continues to grow, the disparity between labor productivity in Manufacturing and

that in Service has been widening. As the IMF-mandated restructuring in

Manufacturing sector has improved on labor productivity gain through cut-back

of unnecessary manpower, the restructuring in most of Service sector except a

few IT-related finance and communication sectors has been lagging behind.

Figure 1. Make Table at purchase prices

commodity

industry PYijbas PYj

PYiD

PYiIM

TRi

TTi

Ti

PYipur

13

Figure 3. Trend of Real Gross Output (2000 prices)

0

200

400

600

800

1000

1200

1400

1600

1800

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Trilli

on W

on

14

2.2 Measurement of Capital Input

The success of late industrialization by newly industrializing economies could

not have been made possible if both the rapid accumulation of capital and its

changing distribution among sectors were not realized in their development

process. However, it is difficult to identify these factors empirically because the

time series data of capital stocks in fast-developing economies by both types of

assets and by industries are not readily available. The lack of investment data

for a sufficiently long period of time to apply the perpetual inventory estimation

method was the main cause of the problem. However, the National Statistical

Office of the Republic of Korea has conducted nation-wide national wealth

survey four times since 1968. Korea is one of a few countries which have

conducted economy-wide national wealth surveys at a regular interval. Since

the first National Wealth Survey (NWS) was conducted in 1968, the subsequent

surveys were made in every ten years in 1977, 1987, and 1997, respectively.

Since such regular surveys with nation-wide coverage are very rare in both

developed and developing countries, an analysis on the dynamic profile of

national wealth seems warranted to examine how national wealth in a fast

growing economy is accumulated and distributed among different sectors.

The estimation of national wealth by types of assets and by industries was

made by Pyo (2003) by modified perpetual inventory method and polynomial

benchmark year estimation method using four benchmark-year estimates. We

have extended his estimates to the year 2004, and changed the base year from

1995 to 2000.

(1) Estimation of Capital Stock4

1) Estimating Method for 1970-1997 In principle the existence of four benchmark year estimates of gross and net

capital stocks makes it possible for us to apply the polynomial benchmark year

estimation method. In Pyo's earlier studies (Pyo 1988, 1992, and 1998), he

estimated proportional retirement rates and depreciation rates both by types of

4This section has been quoted from Pyo, Rhee, and Ha (2004)

15

assets and by industries based on the polynomial equations.

When we applied the polynomial benchmark year equation to estimate the

proportional retirement rates for the sub-periods of 1977-87 and 1987-97, most

of estimates became negative including the average economy-wide retirement

rates (-3.0% for 1977-87 and --3.1% for 1987-97) except other Construction

(0.6%) and Transport Equipment (3.4%) in 1977-87 and Nonresidential Building

(0.9%) in 1987-97. Therefore, following Pyo (1998), we have applied the

polynomial benchmark year estimation method to estimating depreciation by

types of assets only. Thus we have generated net stocks by types of assets first

for the period of 1968-97 and then, distributed them over different sectors of

industries by using interpolated industrial weights between the respective

benchmark years.

We have decided to estimate net capital stock first and then to estimate gross

capital stock by using interpolated net-gross conversion ratios for the following

two reasons. The basic reason is due to the fact that the margin of prediction

error from the polynomial benchmark year equation turns out to be larger with

gross capital stock than with net capital stock as had been observed in Pyo

(1992).

2) Estimating Method after 1997 National Statistical Office of Korea has decided to terminate National Wealth

Survey by 1997 and to switch from direct estimation to indirect estimation of

national wealth following the method of BEA and OECD. The cost of such direct

national wealth survey has increased significantly as the size of national

economy has expanded considerably. In addition, some of the participating

institutions such as Kookmin Bank for unincorporated business enterprises

have been privatized so that National Statistical Office alone can no longer

afford national wealth survey. Japan had terminated its National Wealth Census

in 1970 for almost the same reasons.

Therefore, for the period after 1997, which is the last year of national wealth

survey, we have to estimate capital stocks by a modified perpetual inventory

method using 1997 NWS as benchmark estimates. First, we estimate net stocks

by type of assets in constant prices by using the depreciation rates estimated

from the period of 1987-1977 and distribute them across industries using both

industrial weights in 1997 NWS and those in subsequent Mining &

Manufacturing Census and Surveys and Wholesale and Retail Surveys. In the

16

long run, the estimated depreciation rates by type of assets may need to be

updated and revised by the micro data-based studies. Second the generated

net stocks by type of assets and by industries have to be converted into gross

stock by using the net-gross conversion ratio of 1997 NWS for the time being.

But ultimately we may need further studies on the trend of net-gross conversion

ratio by type of assets and by industries and the average asset life.

3) Reconciliation with Database of Pyo (2003) Since the database of Pyo (2003) covers 10 broad categories of industrial

sector together with 28 sub-sectors of Manufacturing, it has been reclassified

and reconciled with 72 industry classification using other sources such as

Mining & Manufacturing Census and Surveys, Wholesale and Retail Surveys,

and so on. We have classified assets into five categories; residential building,

non-residential building, other construction, transportation vehicles, and

machinery, while excluding large animals & plants, household durables, and

inventory stocks as shown in Table 2.

Table 2. Depreciation Rates of Assets (Unit: %)

before 1978 1978-1987 after 1988

Residential Building 5.5 1.2 3.3

Non-residential Building -6.7 -1.3 3.0

Other Construction 9.7 8.4 1.0

Transportation Vehicles 49.3 28.7 16.9

Machinery 1.1 11.4 9.2

Source : Pyo (2003)

(2) Estimation of Capital Service Inputs

The purpose of this subsection is to outline the estimation of capital service

flows in Korea. We have followed the method of Jorgenson, Ho, and Stiroh

(2005) except the adjustment for a rapid IT asset price decline. The capital

service flows for each asset have been estimated from the capital stocks, and

have been aggregated over all the assets.

17

We have assumed that the flow of capital service is proportional to the average

of current and one-year lagged capital stocks, which means that currently

installed capital stock is available in the midpoint of the installed period. The k

-type capital service flow in industry j at time t can be defined as in (eq10).

where Zk,j,t denotes the k -type capital service flow in industry j at time

t , and qk,t denotes normalizing factor.

We have estimated the price of capital service through the user cost of capital

formula. This methodology derives the cost of capital by the equality between

two alternative investments: earning a nominal rate of return (it ) and investing in asset earning a rental fee and selling the depreciated asset:

where denotes the (expected) capital gains ( ),

and denotes the depreciation rate specific to k -type asset.

We have used yields of corporate bonds for nominal rates of return ( it ) and Pyo's (2003) results for depreciation rates as shown in Table 2. We did not

consider tax effects in estimating cost of capital for the unavailability of data.

Using the above capital service flow and capital service price of each asset, we

have derived aggregated capital service input by a Tornqvist index.

where the vk,j are the two-period average shares of the k -type capital

income in total capital income.

We have also estimated implicit price index of capital inputs (PjK

) from the

18

following equality:

2.3 Measurement of Labor Input

(1) Data

In order to measure labor input for KLEMS model, we have to obtain both

quantity data of labor input such as employment by industries and hours worked

and quality factors such as sex, education and age. Both availability and

reliability of labor statistics in Korea have improved since 1980. But the

measurement of labor input by industries cannot be readily made because the

statistics of employment by industries are not detailed enough to cover 72

sectors. Therefore, we have used other sources for breaking down the labor

data. More detailed classifications of employment will have to rely on

Employment Table, which is published as a supporting table to Input-Output

Table. But it is available only every five year when main Input-Output Tables are

published. Mining and Manufacturing Census and Survey by National Statistical

Office also report employment statistics but it is limited to mining and

manufacturing only.

Economically Active Population Yearbook by National Statistical Office reports

the number of employment, unemployment, not-economically-active population

and economically active population. Report on Monthly Labor Survey by

Ministry of Labor publishes monthly earnings and working days of regular

employees. Survey Report on Wage Structure by the same ministry reports

wages. Nominal wages are also available from this survey.

For the present study, we have obtained the raw data file of Survey Report on

Wage Structure from the Ministry of Labor and Economically Active Population

Survey from National Statistical Office for the period of 1980-2003. The data are

classified by two types of gender (Male and Female), three types of age (below

30, 30-49, and 50 above), and four types of education (middle school and under,

19

high school, college, and university above) and, therefore, there is a total of 24

categories of labor as shown Table 3.

Table 3. Classification of Labor Input

Categories

Gender (1) male (2) female

Age (1) below 30 (2) 30-49 (3) above 50

Education (1) middle school and under (2) high school

(3) college (4) university or above

(2) Estimating Labor Quantity and Quality Inputs

Since the raw-data file of the Survey Report on Wage Structure contains more

detailed industrial classification than that of the Economically Active Population

Survey, we have calculated the quantity of labor from the Economically Active

Population Survey and the quality of labor from the Survey Report on Wage

Structure. This enables us to include self-employed labor as well as to use more

detailed data. However, since the Survey Report on Wage Structure does not

include Agriculture and Government sectors, we had to use the average value

of the entire economy for the quality measure of these two sectors.

In order to make quality adjustments to the employment data, we have taken

the following steps5:

(1) Defining PLlj

as wage rate for j industry and l type category of labor,

the share of labor income by l type category of labor in j industry can be expressed as;

5Jorgenson, Gollop, and Fraumeni (1987)

20

The average weight of j industry and l type labor income during the period of ( t-1 ) and t can be generated as;

(2) In order to make a quality adjustment to labor input data, we have further

decomposed labor input of j industry and l type as follows:

where denotes relative weight of working hours of l type in j

industry. In other words, measures labor input of l type labor in j

industry. and denote the employment and average working

hours of j industry respectively.

(3) Finally, the growth rate of j industry labor input has been computed as follows:

where the first bracket on the right-hand side measures change in employment,

the second bracket measures change in average working hours, and the third

bracket measures the change in quality of labor through change in weighted

working hours. This method defines that total labor input growth is measured by

the sum of separate growth of different categories of labor and that the quality

of labor is measured by the difference between the growth of aggregated labor

and the sum of the separate growth of different categories of labor.

21

2-4 Energy, Material, and Service and Input Shares

In order to decompose intermediate inputs into energy (E), material (M), and

service (S) inputs, we have identified coal and lignite, crude petroleum and

natural gas, uranium and thorium ores, metal ores, coke, refined petroleum

products and nuclear fuel, gas, water, and electricity commodities as energy

inputs, both primary commodities and remaining manufacturing commodities as

material inputs, and remaining service inputs as service inputs.

Regarding shares of inputs, we have used compensation of employees as

shares of labor inputs and remaining value-added as shares of capital inputs.

This method may underestimate the shares of labor input by allocating the

compensation of self-employed to the shares of capital input, and this gap

would be especially large in primary industry. There are some adjustment

processes to correct underestimation of labor share as attempted by, for

example Harberger (1978), but we have not applied it in order to avoid arbitrary

adjustments. This can be improved in future studies. As for energy, material,

and service inputs, we have used nominal inputs for their own shares.

22

3. Estimates of Labor Productivity and TFP by 72-

industry

3.1 Trend of Labor Productivity Level and Growth Rates

by Sector

(1) The Level of Labor Productivity and its Trend

As shown in Figure 4, the general trend of labor productivity reveals a rising

trend but with a remarkable difference between Manufacturing and Service.

While the labor productivity level in Manufacturing measured as the ratio of real

price output to working hours increased sharply, the level in Service increased

very slowly. The role of productivity gain in Manufacturing in the catch-up

process of Korea has been well-documented by Timmer (1999) and Pyo (2001).

As observed in Pyo and Ha (2005), the labor productivity level was not reduced

during the years (1997-1998) of the Asian Financial Crisis because of IMF-

mandated industrial restructuring: the reduced output was matched by reduced

employment leaving labor productivity level unaffected.

The relatively sluggish productivity gain in Service sector has been pointed out

by IMF in their recent consultation with the Korean authorities as a bottleneck of

sustainable growth for Korea. Inklaar, Timmer and van Ark (2006) also pointed

out the slower productivity gain of service industries in Europe relative to those

in the United States. A more detailed decomposition of labor productivity by

sector and by sub-period is presented in Table 4 and 5. According to Kim(2006),

while the share of Service sector in Korean economy has increased sharply

reaching 56 percent level of GDP and 65 percent of total employment in 2005,

the Service productivity is not only low in level terms compared to industrial

nations’ levels but also lags behind in terms of growth rate. She also points out

that Korea’s inter-industry linkage effect between Manufacturing and Service is

also only about half the size of industrial nations.

23

Figure 4 Trend of labor productivity level

<unit: gross output per hour(won)>

0

10000

20000

30000

40000

50000

60000

70000

80000

70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03

Economy-wide Manufacturing Service

Table 4 Labor Productivity Level by industries: Sectoral labor productivity

level in manufacturing by period <unit: gross output per hour(won)>

Before

crisis

After

crisis Code Industry '72-'79 '80-'89 '90-'99

'90-'98 '99-'03

'72-'03

9 Food products and beverages 36,999 39,367 55,163 54,193 90,177 50,884

10 Tobacco products 36,922 40,586 90,594 89,379 195,570 77,609

11 Textiles 6,452 14,174 22,709 22,007 38,216 18,203

12 Wearing apparel, dressing and dying of fur 12,161 9,768 13,732 13,860 19,494 13,037

13 Leather, leather products and footwear 16,679 7,605 17,031 16,130 34,307 16,444

14 Wood and products of wood and cork 4,834 13,773 26,831 26,364 47,559 20,359

15 Pulp, paper and paper products 11,621 13,755 39,931 38,555 71,876 29,278

16 Publishing 12,699 23,025 41,144 37,476 76,242 32,823

17* Printing and reproduction 151,732 388,216 23,194 23,570 15,967 168,374

18 Coke, refined petroleum products and nuclear fuel 274,511 339,248 482,051 468,709 1,013,717 464,860

19 Pharmaceuticals 6,287 12,999 20,620 20,665 1,451,946 238,313

20 Chemicals excluding pharmaceuticals 19,562 20,168 100,634 90,439 133,936 57,556

21 Rubber and plastics products 3,070 8,368 27,769 26,649 47,226 18,257

22 Other non-metallic mineral products 8,884 11,959 27,173 25,961 56,995 22,165

23 Basic metals 13,314 36,861 69,079 66,241 115,772 51,567

24

24 Fabricated metal products 9,132 35,166 38,886 38,054 62,489 33,739

25 Machinery, nec 9,241 10,268 20,074 19,024 45,098 17,916

26 Office, accounting and computing machinery 20,453 35,659 51,379 48,471 169,000 56,296

27 Insulated wire 24,917 13,769 26,158 23,513 155,335 41,416

28 Other electrical machinery and apparatus nec 2,854 7,251 27,079 26,237 52,172 18,511

29 Electronic valves and tubes 2,631 61,877 54,903 54,209 57,471 44,220

30 Telecommunication equipment 3,756 10,289 44,215 33,205 55,150 22,110

31 Radio and television receivers 4,067 6,231 23,202 18,350 39,864 14,354

32 Scientific instruments 1,959 10,277 42,768 41,220 37,830 21,205

33 Other instruments - - - - - -

34 Motor vehicles, trailers and semi-trailers 19,467 36,677 61,206 61,482 88,334 47,422

35 Building and repairing of ships and boats 158,390 286,959 83,660 88,164 89,862 168,109

36 Aircraft and spacecraft 132* 858 31,281 29,831 90,103 26,004*

37 Railroad equipment and transport equipment nec 2,838 1,879 14,641 14,314 7,200 6,448

38 Manufacturing nec 3,614 7,591 16,945 16,630 23,283 11,591

39 Recycling - - - - - -

* In case of the industrial classification code #36, the labor productivity is applied to the period of 1976-

1979 or 1976-2003 because of the data insufficiency,

Table 5 Labor Productivity Level by industries: Sectoral labor productivity

level in Service by period

<unit: gross output per hour(won)>

Before

crisis

After

crisis Code Industry '72-'79 '80-'89 '90-'99

'90-'98 '99-'03

'72-'03

40 Electricity supply 15,448 52,504 90,511 86,384 179,068 72,544

41 Gas supply 14,371 51,533 153,843 130,874 225,650 91,763

42 Water supply 14,372 51,534 344,577 338,580 784,980 237,576

43 Construction 10,256 14,659 22,949 22,739 26,014 17,605

44 Sale, maintenance and repair of motor vehicles and

motorcycles 67,587 4,234 1,800 1,942 699 18,875

45 Wholesale trade and commission trade 95,249 4,307 5,265 5,198 6,288 27,603

46 Retail trade 162,844 3,970 10,885 10,959 11,857 46,886

47 Hotels and restaurants 105,649 6,820 7,673 7,651 7,820 31,917

48 Inland transport 3,973 6,180 9,958 9,726 12,768 7,655

25

49 Water transport 12,758 44,351 189,712 191,043 209,677 103,542

50 Air transport 48,873 47,013 73,068 75,421 136,955 69,521

51 Supporting and auxiliary transport activities 22,824 22,252 13,633 13,781 12,904 18,552

52 Post and telecommunications 22,668 14,465 30,773 27,838 69,494 28,875

53 Financial intermediation 4,580 9,163 23,830 23,034 39,388 16,641

54 Insurance and pension funding 6,943 20,992 33,231 35,061 29,756 22,806

55 Activities related to financial intermediation - 28,342* 34,939 31,599 46,941 35,137*

56 Imputation of owner occupied rents 447,193 200,889 440,570 461,481 90,498 318,508

57 Other real estate activities 437,768 211,920 43,026 47,409 42,199 195,594

58 Renting of machinery and equipment 437,408 211,920 316,158 321,506 1,928,040 567,257

59 Computer and related activities 437,418 211,920 65,469 68,565 24,535 198,697

60 Research and development 417,881 211,920 94,137 98,492 89,770 212,423

61 Legal, technical and advertising 13,404 110,908 34,166 35,704 20,800 51,302

62 Other business activities, nec 13,075 110,945 12,612 12,089 14,119 43,545

63 Public admin and defence 13,557 251,094 2,552 2,751 1,256 82,826

64 Education 13,370 247,426 5,595 5,444 6,734 83,246

65 Health and social work 5,168 10,412 18,945 18,564 19,182 12,764

66 Sewage and refuse disposal, sanitation and similar

activities 2,473 6,329 74,183 60,749 102,172 35,646

67 Activities of membership organizations nec 6,656 7,046 23,951 24,048 18,522 13,523

68 Media activities 5,870 7,046 27,001 29,255 30,274 16,627

69 Other recreational activities 151,168 319,953 85,555 93,977 17,390 166,925

70 Other service activities 55,559 114,660 73,632 81,243 9,723 74,090

71 Private households with employed persons 60,947 122,708 41,276 41,789 34,584 70,740

72 Extra-territorial organizations and bodies - - - - - -

* In case of the industrial classification code #55, the labor productivity growth is applied to the period of

1986-89 or 1986-03 because of the data insufficiency

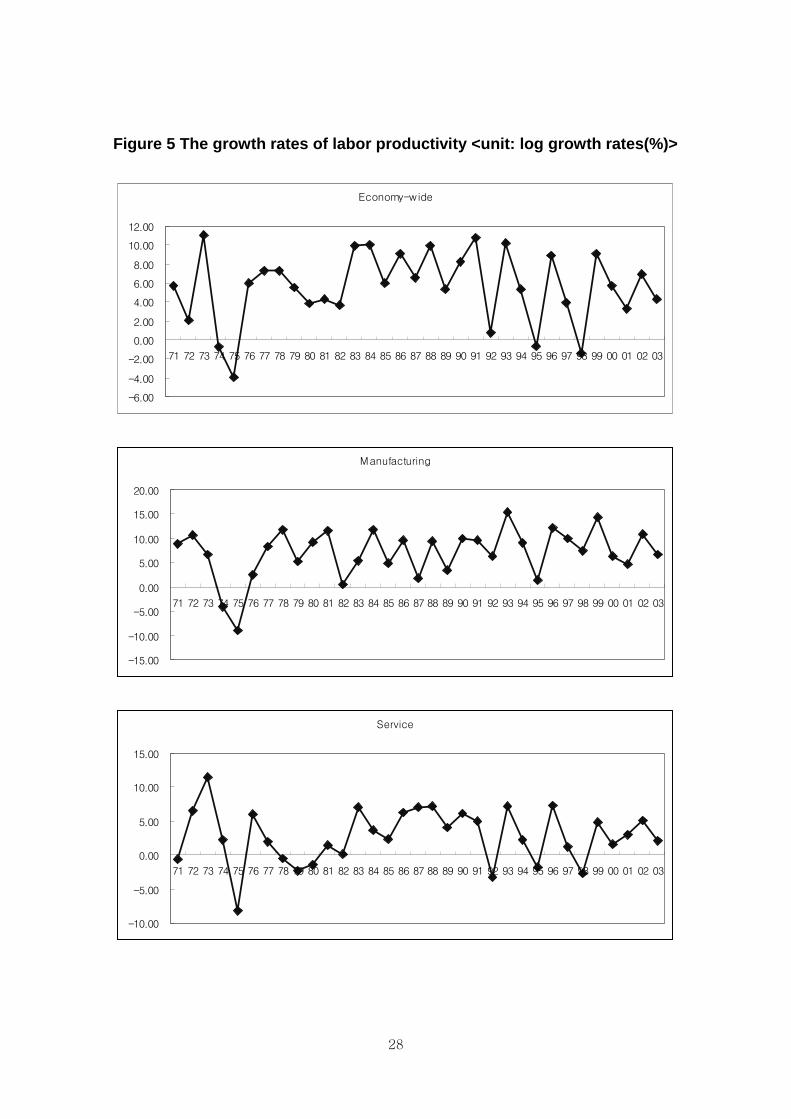

(2) The growth rates of labor productivity by Sector

The growth rates of labor productivity as summarized in Table 4 and shown in

Figure 5 confirm the remarkable difference between Manufacturing and Service

sector. Throughout the entire period of 1971-2003, the economy-wide labor

productivity has grown at the average rate of 5.59 percent but with the sectoral

difference between Manufacturing (6.99 %) and Service (2.91 %). The

26

difference did not shrink but rather has expanded as the process of

industrialization continued. For example, the difference in the 1990’s (9.55 % vs.

2.64 %) has been more than doubled since 1970’s (4.01 % vs. 2.15 %).

The observed difference in both levels and growth rates of labor productivity

between Manufacturing and Service can signal the difference in the degree of

foreign competition, the proportion of tradable and non-tradable and the degree

of domestic competition due to historically different regulatory environments. For

example, the proportion of public enterprises and their subsidiaries in total

output of many service industries such as utilities (electricity, water and gas),

transportation and communication is a lot greater than their proportion in

Manufacturing so that their productivity improvement could have been sluggish

over time. In addition, many non-tradable sectors of service industries such as

retail trade, real estate and financial services, hotels and restaurants etc. have

been subject to all kinds of regulations such as zoning, sanitary standards and

segregated financial market services etc.

Table 6 Growth Rates of Labor Productivity by Sector (%)

Period Economy-wide Manufacturing Service

72-'79 4.32 4.01 2.15

80-'89 6.87 6.75 3.77

90-'99 5.54 9.55 2.64

90-'98 5.14 9.01 2.40

99-'03 5.87 8.61 3.33

72-'03 5.59 6.99 2.91

A more detailed analysis of labor productivity can be made by looking at growth

rates of labor productivity by sub-sectors of both Manufacturing and Service

industries. Table 7 reports our estimates of growth rates of labor productivity in

sub-manufacturing industries. Within Manufacturing, we also observe a large

difference in growth rates of labor productivity ranging from Aircraft and

Spacecraft (27.08 %) to Tobacco Products (- 4.78 %). In general, export-

oriented manufacturing industries such as Electrical Machinery and Electronic

devices (14 % range) and Computing Machinery and Television and Radio

27

Receivers etc. (10 % range) have been leader industries in improving labor

productivity.

In Service industries, the intra-industry difference of labor productivity growth is

even larger than in Manufacturing. As presented in Table 8, Water Supply

(17.92 %), Electricity (14.48 %) and Gas Supply (14.08 %) have been leader

industries because they have been under the public enterprises with rising

demand for social overhead capital. On the other hand, Private House Hold with

Employed Persons (- 26.69 %), Other Service Activities (- 19.47 %) and Public

Administration and defense (- 15.84 %) have been on the lower end of the labor

productivity growth.

28

Figure 5 The growth rates of labor productivity <unit: log growth rates(%)>

Economy-wide

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03

Manufacturing

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03

Service

-10.00

-5.00

0.00

5.00

10.00

15.00

71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03

29

Table 7 Growth Rates of Labor productivity in Manufacturing ( %)

Before

crisis

After

crisis Code Industry '72-'79 '80-'89 '90-'99

'90-'98 '99-'03

'72-'03

9 Food products and beverages 0.31 3.30 3.20 5.01 4.66 3.16

10 Tobacco products -36.96 6.28 4.62 3.62 15.92 -4.78

11 Textiles 9.92 5.39 6.41 6.43 8.39 7.36

12 Wearing apparel, dressing and dying of fur -3.42 4.67 -0.02 -1.44 13.19 2.09

13 Leather, leather products and footwear -29.77 -3.24 12.76 14.89 7.83 -3.85

14 Wood and products of wood and cork 20.78 9.02 6.89 9.38 7.69 12.12

15 Pulp, paper and paper products 1.08 7.14 9.92 11.27 6.95 6.58

16 Publishing 4.33 11.98 6.67 -1.60 16.64 6.90

17 Printing and reproduction 43.17 -28.17 -2.81 1.59 -15.13 1.38

18 Coke, refined petroleum products and nuclear fuel -2.51 -0.44 4.61 4.47 8.51 1.69

19 Pharmaceuticals -46.09 9.57 0.48 -0.22 86.74 3.41

20 Chemicals excluding pharmaceuticals 8.03 12.46 17.43 15.67 -2.05 9.93

21 Rubber and plastics products 14.20 11.13 7.33 6.45 6.65 10.01

22 Other non-metallic mineral products 3.36 6.95 8.00 7.40 15.07 7.33

23 Basic metals 17.40 10.13 6.81 7.59 4.78 10.61

24 Fabricated metal products 7.66 9.06 4.28 4.69 7.95 7.32

25 Machinery, nec 2.22 9.11 7.18 5.60 14.70 7.12

26 Office, accounting and computing machinery 18.78 0.47 9.44 5.43 22.29 10.12

27 Insulated wire -10.61 -2.90 13.39 12.05 26.55 3.53

28 Other electrical machinery and apparatus nec 24.09 5.52 12.22 13.82 15.00 14.29

29 Electronic valves and tubes 23.64 26.52 -2.40 -5.89 9.88 14.37

30 Telecommunication equipment -0.95 16.22 21.79 18.65 -12.66 7.82

31 Radio and television receivers 11.99 6.38 20.71 6.30 22.66 10.36

32 Scientific instruments -5.03 19.82 14.73 13.77 0.56 8.48

33 Other instruments - - - - - -

34 Motor vehicles, trailers and semi-trailers -7.21 9.42 -1.52 -6.68 19.98 2.09

35 Building and repairing of ships and boats 5.27 8.21 -21.86 -29.82 28.56 0.12

36 Aircraft and spacecraft 28.90* 20.70 34.72 41.48 12.83 27.08*

37 Railroad equipment and transport equipment nec -12.47 -3.28 23.10 26.82 -30.80 -1.75

38 Manufacturing nec 3.43 13.34 5.20 6.12 3.80 7.23

39 Recycling - - - - - -

30

* In case of the industrial classification code #36, the labor productivity growth is applied to the period of

1977-1979 or 1977-2003 because of the data insufficiency,

Figure 6 Growth Rates of Labor Productivity in Manufacturing (1972-03/ %)

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Aircraft and spacecra

ft

Electronic valves and tubes

Oth

er electrical machinery and a

pparatus nec

Wood a

nd p

roduc

ts o

f wood and c

ork

Basic m

etals

Office, accoun

ting and c

omputing m

achinery

Chemicals e

xcluding p

harm

aceuticals

Rubber and plastics produc

ts

Radio and television receivers

Scientific instruments

Manufacturing nec

Oth

er non-meta

llic m

inera

l pro

duc

ts

Fabricate

d m

etal pro

duc

ts

Textiles

Machinery, nec

Pub

lishing

Telecommun

ication equipment

Pulp, paper and paper products

Insulate

d w

ire

Pharm

aceuticals

Food p

roduc

ts a

nd b

eve

rages

Moto

r vehicles, traile

rs a

nd semi-traile

rs

Wearing a

pparel, d

ressing a

nd dying of fur

Coke

, refined p

etroleum

pro

duc

ts a

nd n

uclear fuel

Printing and repro

duc

tion

Building a

nd repairing o

f ships and b

oats

Railroad e

quipment and tra

nsport e

quipment nec

Leath

er, leath

er pro

ducts and footw

ear

Tobacco p

roduc

ts

* In case of EU-KLEMS Code, #33, #39, they are excluded because of data insufficiency.

31

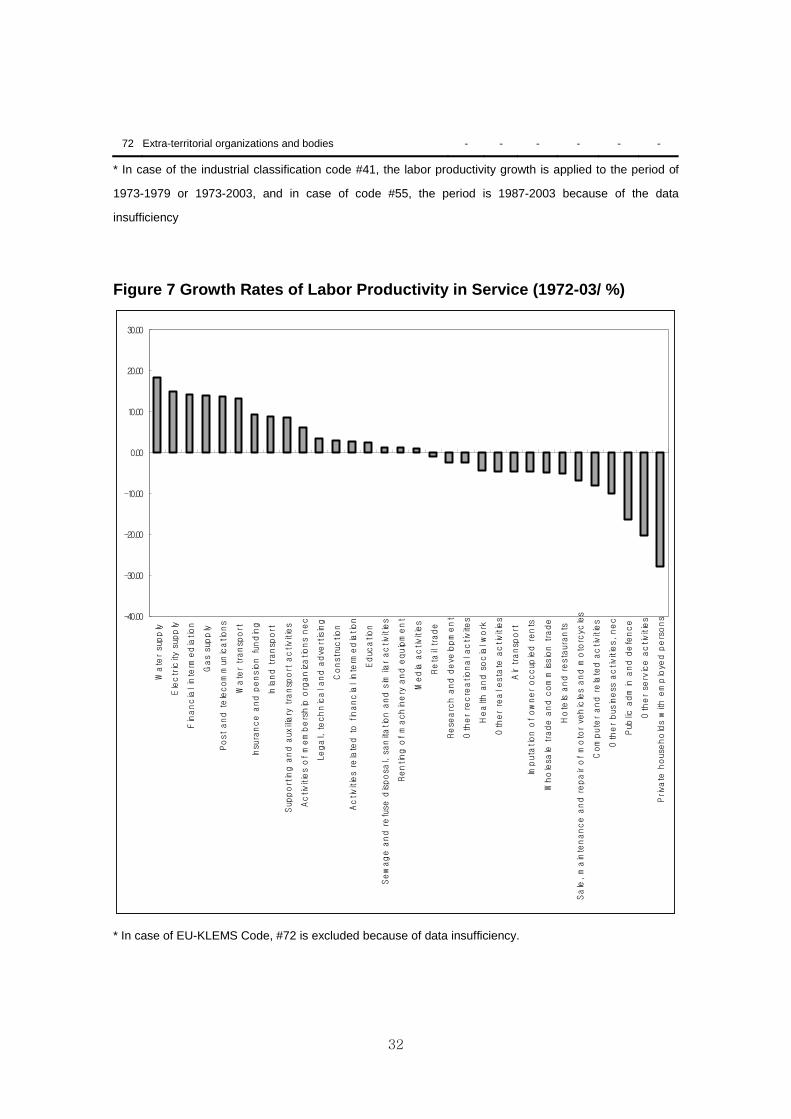

Table 8 Growth Rates of Labor Productivity in Service Industries (%)

Before

crisis

After

crisis Code Industry '72-'79 '80-'89 '90-'99

'90-'98 '99-'03

'72-'03

40 Electricity supply 26.31 15.59 7.68 8.61 5.98 14.81

41 Gas supply 23.56 16.87 17.62 13.12 -3.01 14.08

42 Water supply 25.62 16.87 18.63 17.48 11.31 18.36

43 Construction -0.51 6.42 2.40 3.57 0.38 2.94

44 Sale, maintenance and repair of motor vehicles and motorcycles 13.79 -15.96 -23.47 -28.17 16.66 -6.86

45 Wholesale trade and commission trade -4.76 -13.27 0.87 -1.15 5.07 -4.87

46 Retail trade 7.37 -16.64 6.21 8.79 1.00 -0.73

47 Hotels and restaurants -4.40 -11.82 -1.48 -3.88 4.03 -5.25

48 Inland transport 18.24 7.47 4.88 4.47 5.24 8.97

49 Water transport 17.01 15.25 10.69 15.66 -1.83 13.13

50 Air transport -39.14 9.24 0.55 3.70 8.22 -4.57

51 Supporting and auxiliary transport activities 24.37 9.56 -3.03 -2.14 0.61 8.57

52 Post and telecommunications 24.86 8.02 13.67 12.91 9.89 13.90

53 Financial intermediation 26.19 15.41 6.30 4.88 9.98 14.29

54 Insurance and pension funding 8.50 20.12 -7.05 0.57 6.51 9.59

55 Activities related to financial intermediation - - 7.53 -1.36 10.07 2.65

56 Imputation of owner occupied rents -1.02 -2.03 4.83 16.70 -53.65 -4.58

57 Other real estate activities -0.64 -2.25 -37.80 -44.38 56.47 -4.52

58 Renting of machinery and equipment -0.64 -2.25 5.36 17.35 -17.72 1.25

59 Computer and related activities -0.64 -2.25 -14.28 -17.68 -15.33 -8.23

60 Research and development -0.64 -2.25 -10.49 -10.71 9.57 -2.38

61 Legal, technical and advertising -3.09 9.08 2.02 3.95 2.85 3.62

62 Other business activities, nec -48.15 9.49 0.16 -6.08 5.19 -9.97

63 Public admin and defense -48.33 10.66 -32.22 -37.57 19.98 -16.20

64 Education 20.70 4.18 -3.65 -5.20 -17.05 2.36

65 Health and social work -40.34 13.67 6.55 7.03 -2.79 -4.27

66 Sewage and refuse disposal, sanitation and similar activities 0.80 6.42 33.68 32.77 -64.78 1.30

67 Activities of membership organizations nec 3.48 6.82 11.15 15.97 -7.60 6.30

68 Media activities -38.79 6.82 -1.19 -6.79 67.04 1.00

69 Other recreational activities -3.66 14.34 -33.19 -39.83 33.58 -2.39

70 Other service activities -89.32 19.18 -32.34 -31.03 29.95 -20.38

71 Private households with employed persons -88.61 19.22 -13.20 -16.44 -45.18 -27.83

32

72 Extra-territorial organizations and bodies - - - - - -

* In case of the industrial classification code #41, the labor productivity growth is applied to the period of

1973-1979 or 1973-2003, and in case of code #55, the period is 1987-2003 because of the data

insufficiency

Figure 7 Growth Rates of Labor Productivity in Service (1972-03/ %)

-40.00

-30.00

-20.00

-10.00

0.00

10.00

20.00

30.00

Wate

r su

pply

Electricity su

pply

Financial interm

ediation

Gas su

pply

Post a

nd telecommun

ications

Wate

r transp

ort

Insu

rance a

nd p

ension fun

ding

Inland transp

ort

Sup

porting a

nd a

uxiliary transp

ort a

ctivities

Activities of membership o

rganizations nec

Legal, technical and adve

rtising

Construction

Activities related to financial interm

ediation

Educ

ation

Sewage and refuse

disposa

l, sanitation a

nd sim

ilar activities

Renting o

f machinery and e

quipment

Media a

ctivities

Reta

il trade

Rese

arc

h a

nd deve

lopment

Oth

er re

cre

ational activite

s

Health and social work

Oth

er real estate

activities

Air tra

nsp

ort

Imputation o

f owner occup

ied rents

Wholesa

le trade and c

ommission trade

Hotels a

nd restaurants

Sale, maintenance and repair of motor ve

hicles and m

oto

rcyc

les

Computer and related activities

Other bus

iness a

ctivities, nec

Pub

lic admin a

nd defence

Oth

er se

rvice activities

Priva

te households with e

mploye

d persons

* In case of EU-KLEMS Code, #72 is excluded because of data insufficiency.

33

(3) Trend of TFP Growth by Sector

The growth rates of TFP by sector are shown in Figure 8. Throughout the entire

period 1972-2003, Korean economy experienced about 2 break-points: mid-

1970s which was the first oil shock and in 1997 which was the financial crisis.

The difference between two break points can be summarized as follows. During

the second half of 1970’s, the growth rate of gross output was not low, but the

growth rates of inputs such as capital(4.56%), labor(1.79%), energy(0.69%),

intermediate goods(3.34%) especially, were relatively higher. Therefore, the

growth rates of TFP have been estimated as negative. In case of late 1990’s

the negative growth of TFP has been resulted from the shrink of gross output

rooted from economic crisis.

In addition we observe that the estimated TFP growth rates in Manufacturing

are in general greater than in Service. It maybe due to the fact that an

innovation process such as product innovation or process innovation is more

sensitive and stronger in manufacturing than in service. Also the R&D

investment for innovation is in general more intensive in manufacturing than in

service. So the growth rates of TFP in Manufacturing seem to be greater than in

Service.

34

Figure 8 The growth rates of TFP (%)

Economy-wide

-6.00

-5.00

-4.00

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03

Manufacturing

-5.00

-4.00

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03

Service

-6.00

-5.00

-4.00

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03

35

3.2 Gross Output Growth Accounting and TFP Growth

The growth rate of economy-wide TFP has been estimated as -0.59 percent.

The growth rates of TFP in Manufacturing and Service are estimated as 0.48

percent and -0.92 percent respectively throughout the entire period of 1972-

2003 as shown in Table 7-9. Also the economy-wide TFP growth rate during the

pre-crisis period (1990-1998) has been estimated as -0.84 percent. And the

growth rate during the post-crisis period (1999-2003) has been estimated as

0.86 percent.

After the economic crisis in 1997-1998, the economy-wide growth rate of gross

output has been recovered, at the same time the growth rates of input factors

such as capital, labor and service have also been reduced from those during

the pre-crisis period. Accordingly, the growth rate of TFP during the post-crisis

period has been relatively higher than that during the pre-crisis period.

Secondly the contributions of TFP to economy-wide gross output growth during

the entire period of 1972-2003 are -7.5 percent, and 4.7 percent in

Manufacturing, and -12.8 percent in Service. Then we can examine the relative

contribution ratio of the input factors to the output growth. The relative

contribution ratios to output growth during the entire period are in order of

intermediate goods(52.3 percent), capital(15.6 percent), energy(11.3 percent),

service(10.2 percent), labor(5.8 percent) in Manufacturing. So the innovation or

the role of intermediate goods for enhancing productivity is more important in

Manufacturing than in Service. And the contribution ratio of TFP to

Manufacturing output growth (4.7 percent) is of rather insignificant magnitude.

On the other hand, in Service the contribution are in order of capital(48.7

percent), service(23.9 percent), labor(20.1 percent), intermediate goods(15.8

percent ), energy(4.2 percent). Hence we can see the input’s role for enhancing

productivity is different between Manufacturing and Service.

Thirdly the total factor productivity growth in gross output growth accounting is

lower than that without quality adjustment in input data. The quality of labor has

affected the growth of output about 2.4 percent in Manufacturing and 3.9

percent in Service during the entire period, Also the quantity of labor has

36

affected the growth of output by about 3.4 percent in Manufacturing and about

16.3 percent in Service during the entire period, Thus the labor input in Service

has influenced output growth both in quantity and quality of labor than that in

Manufacturing. The quantity of labor input in Manufacturing has been reduced

during the pre-crisis period. It reflects a drastic structural adjustment in Korea’s

labor market after the crisis of 1997-1998. As a consequence, the contribution

rate of labor to output growth has become negative in Manufacturing after the

crisis.

Table 9 Gross Output Growth Accounting and TFP growth in economy-

wide

<unit: log growth rates(%)>

Labor input

Period Gross

output

Capital

input Total

labor

Quantity

labor

Quality

labor

Energy

input

Intermediate

input

Service

input TFP

'72-79 9.48 4.56 1.79 1.03 0.76 0.69 3.34 1.13 -2.03

'80-'89 8.36 3.05 0.62 0.28 0.34 0.45 3.18 0.98 0.08

'90-'99 6.43 2.40 0.49 0.19 0.31 0.70 1.64 1.76 -0.56

'90-'98 5.84 2.54 0.49 0.15 0.34 0.63 1.30 1.71 -0.84

'99-'03 7.61 1.11 0.48 0.33 0.14 0.75 2.78 1.62 0.86

'72-'03 7.81 2.98 0.85 0.44 0.41 0.61 2.63 1.32 -0.59

contribution to output growth

'72-79 100.0 48.1 18.9 10.9 8.1 7.3 35.3 11.9 -21.5

'80-'89 100.0 36.5 7.4 3.4 4.0 5.3 38.0 11.8 0.9

'90-'99 100.0 37.3 7.7 2.9 4.8 10.9 25.6 27.3 -8.7

'90-'98 100.0 43.5 8.4 2.5 5.8 10.8 22.4 29.4 -14.4

'99-'03 100.0 14.6 6.3 4.4 1.9 9.9 36.6 21.3 11.4

'72-'03 100.0 38.2 10.9 5.6 5.3 7.8 33.7 17.0 -7.5

37

Table 10 Gross Output Growth Accounting and TFP growth in

manufacturing <unit: log growth rates(%)>

Labor input

Period Gross

output

Capital

input Total

labor

Quantity

labor

Quality

labor

Energy

input

Intermediate

input

Service

input TFP

'72-79 15.30 2.41 1.72 1.28 0.43 1.66 8.29 1.17 0.06

'80-'89 10.27 1.68 0.59 0.40 0.19 0.88 5.83 0.80 0.49

'90-'99 6.94 1.20 -0.14 -0.34 0.20 1.19 2.94 1.17 0.58

'90-'98 5.56 1.26 -0.22 -0.44 0.22 1.08 2.17 1.04 0.23

'99-'03 10.11 0.70 0.26 0.16 0.09 1.02 5.26 1.32 1.55

'72-'03 10.18 1.59 0.59 0.35 0.24 1.15 5.33 1.04 0.48

contribution to output growth

'72-79 100.0 15.8 11.2 8.4 2.8 10.8 54.2 7.6 0.4

'80-'89 100.0 16.3 5.7 3.9 1.8 8.6 56.8 7.8 4.8

'90-'99 100.0 17.3 -2.0 -4.9 2.8 17.2 42.3 16.9 8.4

'90-'98 100.0 22.6 -3.9 -7.9 4.0 19.5 39.0 18.7 4.1

'99-'03 100.0 6.9 2.5 1.6 0.9 10.1 52.1 13.0 15.3

'72-'03 100.0 15.6 5.8 3.4 2.4 11.3 52.3 10.2 4.7

38

Table 11 Gross Output Growth Accounting and TFP growth in service

<unit: log growth rates(%)>

Labor input

Period Gross

output

Capital

input Total

labor

Quantity

labor

Quality

labor

Energy

input

Intermediate

input

Service

input TFP

'72-79 7.86 4.77 2.05 1.52 0.54 0.26 1.43 1.36 -2.01

'80-'89 7.92 3.70 1.33 1.11 0.22 0.18 1.52 1.27 -0.08

'90-'99 6.54 3.17 1.28 1.12 0.16 0.37 0.69 2.37 -1.35

'90-'98 6.61 3.37 1.39 1.22 0.17 0.34 0.69 2.40 -1.58

'99-'03 5.87 1.39 0.86 0.68 0.18 0.54 0.73 2.02 0.33

'72-'03 7.22 3.51 1.45 1.17 0.28 0.30 1.14 1.73 -0.92

contribution to output growth

'72-79 100.0 60.7 26.1 19.3 6.8 3.3 18.1 17.3 -25.6

'80-'89 100.0 46.6 16.8 14.0 2.8 2.3 19.2 16.0 -0.9

'90-'99 100.0 48.5 19.6 17.2 2.5 5.7 10.6 36.3 -20.7

'90-'98 100.0 51.1 21.0 18.4 2.6 5.1 10.5 36.4 -24.0

'99-'03 100.0 23.6 14.7 11.6 3.1 9.3 12.4 34.4 5.6

'72-'03 100.0 48.7 20.1 16.3 3.9 4.2 15.8 23.9 -12.8

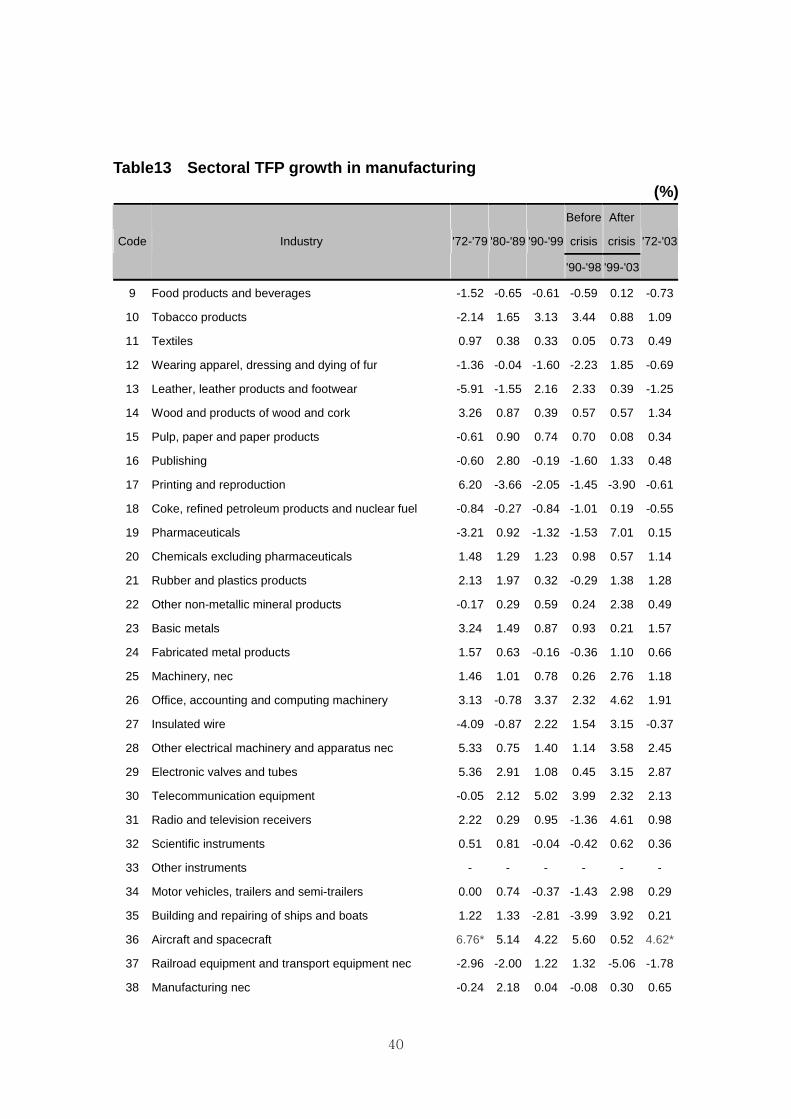

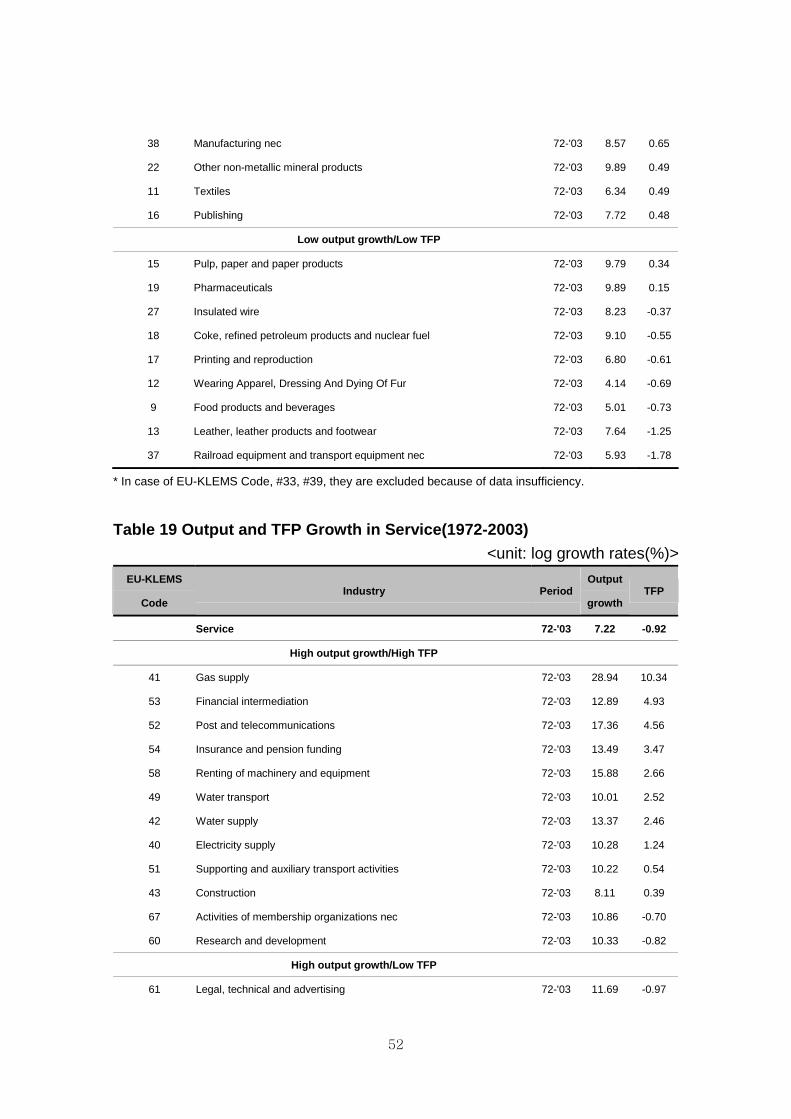

On the one hand the sectors which were based on IT technology such as i)

Office, accounting and computing machinery (1.91 percent), ii) Other electrical

machinery (2.45 percent), iii) Electronic valves and tubes(2.87 percent), iv)

Telecommunication equipment(2.13%) in Manufacturing, have shown higher

growth rate of TFP during the entire period(1972-2003) as shown in Table 11.

But the labor intensive sectors such as i) Leather and foot wear(-1.25 percent),

ii) Food products and beverages(-0.73percent), iii) Wearing apparel, dressing

and dying of fur(-0.69percent), iv)Printing and reproduction(-0.61 percent) have

shown negative growth rates of total factor productivity.

In Service, Post and telecommunication which is related strongly with IT

technology has recorded a relatively higher growth rate (4.93 percent) of TFP

among service sectors as shown in Table 12. But the social and private sectors

such as i) Public administration and defense (-10.36 percent), ii) Private

households with employed persons (-8.95 percent), iii) Other service activities(-

8.74 percent) have shown negative growth rates of TFP.

Therefore, we can see that the leading sectors for enhancing productivity

39

growth are related with IT sectors. Korean economy has heavily invested in IT

sectors on a full scale since 1995 (Table 10) as analyzed in Ha and Pyo (2004).

Table 12 The investment in IT sector

Year IT Investment (billion won) Growth(%)

1995 15,125.7 -

1996 17,916.0 16.9

1997 19,122.0 6.5

1998 17,099.2 -11.2

1999 23,716.0 32.7

2000 32,190.9 30.6

2001 31,502.0 -2.2

2002 33,143.8 5.1

2003 31,551.8 -4.9

2004 31,391.9 -0.5

*Investment is real value in 2000 prices

*Source: Bank of Korea (http://ecos.bok.or.kr

40

Table13 Sectoral TFP growth in manufacturing

(%)

Before

crisis

After

crisis Code Industry '72-'79 '80-'89 '90-'99

'90-'98 '99-'03

'72-'03

9 Food products and beverages -1.52 -0.65 -0.61 -0.59 0.12 -0.73

10 Tobacco products -2.14 1.65 3.13 3.44 0.88 1.09

11 Textiles 0.97 0.38 0.33 0.05 0.73 0.49

12 Wearing apparel, dressing and dying of fur -1.36 -0.04 -1.60 -2.23 1.85 -0.69

13 Leather, leather products and footwear -5.91 -1.55 2.16 2.33 0.39 -1.25

14 Wood and products of wood and cork 3.26 0.87 0.39 0.57 0.57 1.34

15 Pulp, paper and paper products -0.61 0.90 0.74 0.70 0.08 0.34

16 Publishing -0.60 2.80 -0.19 -1.60 1.33 0.48

17 Printing and reproduction 6.20 -3.66 -2.05 -1.45 -3.90 -0.61

18 Coke, refined petroleum products and nuclear fuel -0.84 -0.27 -0.84 -1.01 0.19 -0.55

19 Pharmaceuticals -3.21 0.92 -1.32 -1.53 7.01 0.15

20 Chemicals excluding pharmaceuticals 1.48 1.29 1.23 0.98 0.57 1.14

21 Rubber and plastics products 2.13 1.97 0.32 -0.29 1.38 1.28

22 Other non-metallic mineral products -0.17 0.29 0.59 0.24 2.38 0.49

23 Basic metals 3.24 1.49 0.87 0.93 0.21 1.57

24 Fabricated metal products 1.57 0.63 -0.16 -0.36 1.10 0.66

25 Machinery, nec 1.46 1.01 0.78 0.26 2.76 1.18

26 Office, accounting and computing machinery 3.13 -0.78 3.37 2.32 4.62 1.91

27 Insulated wire -4.09 -0.87 2.22 1.54 3.15 -0.37

28 Other electrical machinery and apparatus nec 5.33 0.75 1.40 1.14 3.58 2.45

29 Electronic valves and tubes 5.36 2.91 1.08 0.45 3.15 2.87

30 Telecommunication equipment -0.05 2.12 5.02 3.99 2.32 2.13

31 Radio and television receivers 2.22 0.29 0.95 -1.36 4.61 0.98

32 Scientific instruments 0.51 0.81 -0.04 -0.42 0.62 0.36

33 Other instruments - - - - - -

34 Motor vehicles, trailers and semi-trailers 0.00 0.74 -0.37 -1.43 2.98 0.29

35 Building and repairing of ships and boats 1.22 1.33 -2.81 -3.99 3.92 0.21

36 Aircraft and spacecraft 6.76* 5.14 4.22 5.60 0.52 4.62*

37 Railroad equipment and transport equipment nec -2.96 -2.00 1.22 1.32 -5.06 -1.78

38 Manufacturing nec -0.24 2.18 0.04 -0.08 0.30 0.65

41

39 Recycling - - - - - -

Table14 Sectoral TFP Growth in Service

(%)

Before

crisis

After

crisisCode Industry '72-'79 '80-'89 '90-'99

'90-'98 '99-'03

72-'03

40 Electricity supply 2.20 0.76 1.10 1.18 0.77 1.24

41 Gas supply 15.03 14.00 7.31 7.10 2.29 10.34

42 Water supply 8.67 3.38 -2.19 -2.51 -0.39 2.46

43 Construction -0.13 2.31 -0.91 -0.36 -1.27 0.39

44 Sale, maintenance and repair of motor vehicles and motorcycles - - -12.91 -14.71 2.09 -8.71*

45 Wholesale trade and commission trade -3.04 -2.46 -1.28 -2.21 1.26 -1.95

46 Retail trade -0.77 -3.31 -0.73 -0.71 0.41 -1.36

47 Hotels and restaurants -4.75 -4.69 -4.59 -6.20 1.80 -4.11

48 Inland transport 4.14 3.06 -0.42 -0.72 1.90 2.09

49 Water transport 4.72 2.21 1.31 1.92 0.71 2.52

50 Air transport -10.49 -0.79 -2.20 -1.85 2.70 -2.97

51 Supporting and auxiliary transport activities 5.71 0.76 -4.52 -4.83 1.50 0.54

52 Post and telecommunications 6.51 2.24 5.36 5.08 5.18 4.56

53 Financial intermediation 7.45 5.61 3.20 3.05 2.89 4.93

54 Insurance and pension funding 1.46 5.81 0.99 4.76 -0.28 3.47

55 Activities related to financial intermediation - - -2.77 -9.28 7.03 -3.46*

56 Imputation of owner occupied rents -8.68 -7.03 5.12 7.66 -11.66 -4.03

57 Other real estate activities -6.44 -3.41 -2.86 -3.70 12.35 -1.79

58 Renting of machinery and equipment -1.69 3.45 4.14 9.44 -4.13 2.66

59 Computer and related activities - - -7.89 -10.08 0.07 -6.45*

60 Research and development -0.73 -1.19 -2.51 -2.91 3.54 -0.82

61 Legal, technical and advertising -2.67 -0.04 -1.22 -1.24 0.38 -0.97

62 Other business activities, nec -11.74 3.97 -2.54 -4.20 2.69 -2.46

63 Public admin and defense -29.94 4.94 -18.73 -22.09 11.51 -10.36

64 Education 16.39 2.01 -2.35 -3.77 -12.68 1.68

65 Health and social work -32.93 9.88 1.43 1.88 -4.19 -5.27

66 Sewage and refuse disposal, sanitation and similar activities - - - - - -

67 Activities of membership organizations nec -3.54 -0.31 1.36 2.52 -2.73 -0.70

68 Media activities -16.43 -0.25 -9.24 -11.98 29.66 -2.92

69 Other recreational activities -4.15 2.90 -17.29 -20.27 13.60 -3.71

42

70 Other service activities -30.77 6.08 -18.93 -19.42 16.12 -8.74

71 Private households with employed persons -32.53 3.78 5.72 5.77 -23.15 -8.95

72 Extra-territorial organizations and bodies - - - - - -

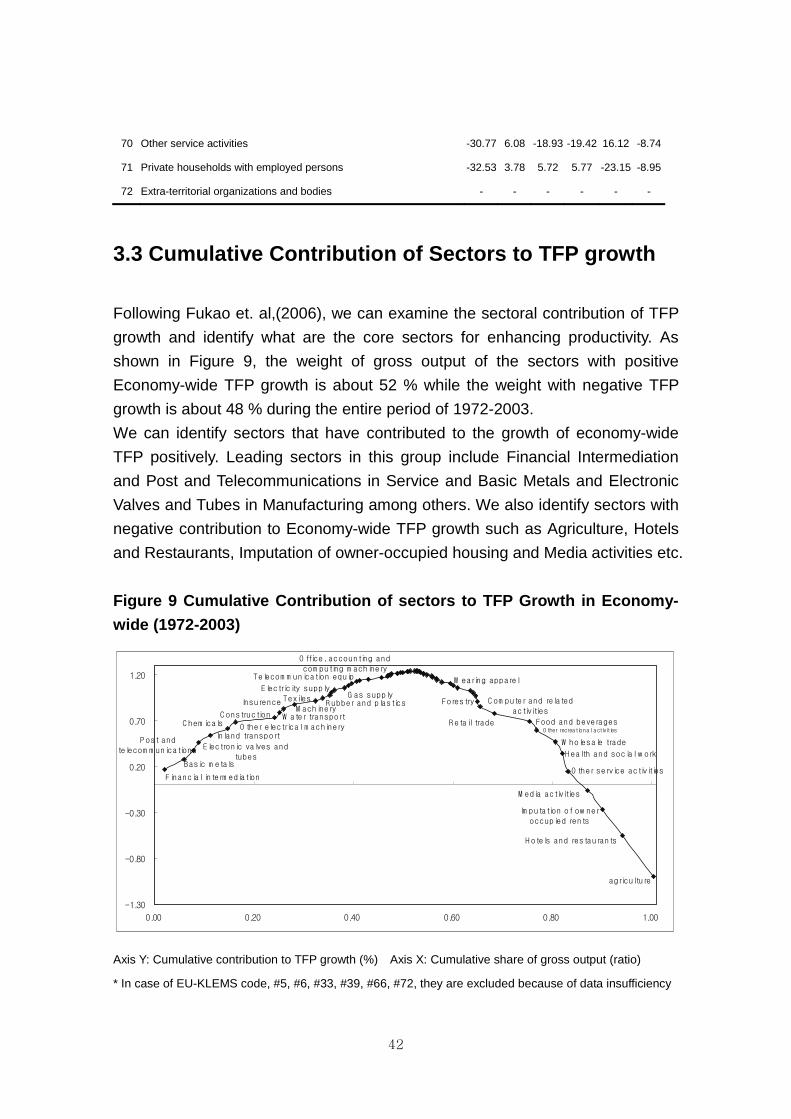

3.3 Cumulative Contribution of Sectors to TFP growth

Following Fukao et. al,(2006), we can examine the sectoral contribution of TFP

growth and identify what are the core sectors for enhancing productivity. As

shown in Figure 9, the weight of gross output of the sectors with positive

Economy-wide TFP growth is about 52 % while the weight with negative TFP

growth is about 48 % during the entire period of 1972-2003.

We can identify sectors that have contributed to the growth of economy-wide

TFP positively. Leading sectors in this group include Financial Intermediation

and Post and Telecommunications in Service and Basic Metals and Electronic

Valves and Tubes in Manufacturing among others. We also identify sectors with

negative contribution to Economy-wide TFP growth such as Agriculture, Hotels

and Restaurants, Imputation of owner-occupied housing and Media activities etc.

Figure 9 Cumulative Contribution of sectors to TFP Growth in Economy-

wide (1972-2003)

O ffice, accounting and

com puting m achineryTelecom m unication equip

Forestry C om puter and related

activities

R etail trade Food and beveragesO ther recreational activities

W holesale trade

H ealth and social w ork

O ther service activities

M edia activities

Im putation of ow ner

occupied rents

H otels and restaurants

agriculture

Electricity supplyG as supply

Inland transportP ost and

telecom m unications Electronic valves and

tubesBasic m etals

Financial interm ediation

C hem icals O ther electrical m achinery

C onstructionM achinery

Insurence

W ater transport

TexilesR ubber and plastics

W earing apparel

-1.30

-0.80

-0.30

0.20

0.70

1.20

0.00 0.20 0.40 0.60 0.80 1.00

Axis Y: Cumulative contribution to TFP growth (%) Axis X: Cumulative share of gross output (ratio)

* In case of EU-KLEMS code, #5, #6, #33, #39, #66, #72, they are excluded because of data insufficiency

43

As shown in Figure 10, the weight of gross output of the sectors with positive

TFP growth in Manufacturing is 72.4% while the weight with negative TFP

growth is 27.6% during the period of 1972-2003. The sub-sectors with positive

TFP growth are basic metals, chemicals, machinery, textiles, rubber and plastic,

fabricated metal, wood, other non metallic mineral, motor vehicles and trailers

as non IT sectors, and electronic valves and tubes, office, accounting and

computing machinery, telecommunications, radio and TV receivers as IT

sectors. The sub-sectors with negative TFP growth are leather and footwear,

wearing and apparel, coke and refined petroleum etc.

Figure 10 Cumulative Contribution of sectors to TFP Growth in

Manufacturing (1972-2003)

Motor vehicles , trailers

Other non metallic mineral

Radio and TV receivers

Wood

Leather and footwear

Wearing apparelCoke, refines petroleum

Food and beverages

Office, accounting and

computing machinery

Telecommunication

Fabricated metalRubber and plas tics

TexilesMachinery

Other eletrical machinery

Chemicals

Eletronic valves and tubes

Bas ic metals

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0

Axis Y: Cumulative contribution to TFP growth (%) Axis X: Cumulative share of gross output (ratio)

On the other hand, we can look at Service industry separately. As shown in

Figure 11, the weight of gross output of the sectors with positive TFP growth in

Service is only about 40 % while the weight with negative TFP growth is 60 %

during the period of 1972-2003. The group of service industries with positive

TFP growth includes Financial intermediation, Post and communication, Inland

Transport, Water Transport, Construction etc. The group with negative TFP

growth includes Hotels and Restaurants, Imputation of owner-occupied housing,

Media activities and Wholesale trade etc.

44

Figure 11 Cumulative Contribution of sectors to TFP Growth in Service

(1972-2003)

Post and telecom m unicatios

Financial interm edition

Inland transportC onstruction W ater transport

Insurance and pentionG as supply

Electricity supply

H otel and restaurants

M edia activities

Im putation of ow ner

occupied rents

O ther service activities

W holesale trade

Health and social w orkO ther recreational

activities

Retail tradeC om puter and related activities

A ir transportO ther business activities

Legal,technical and advertising

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

0.00 0.20 0.40 0.60 0.80 1.00

Axis Y: Cumulative contribution to TFP growth (%) Axis X: Cumulative share of gross output (ratio)

* In case of EU-KLEMS code, #66, #72, they are excluded because of data insufficiency

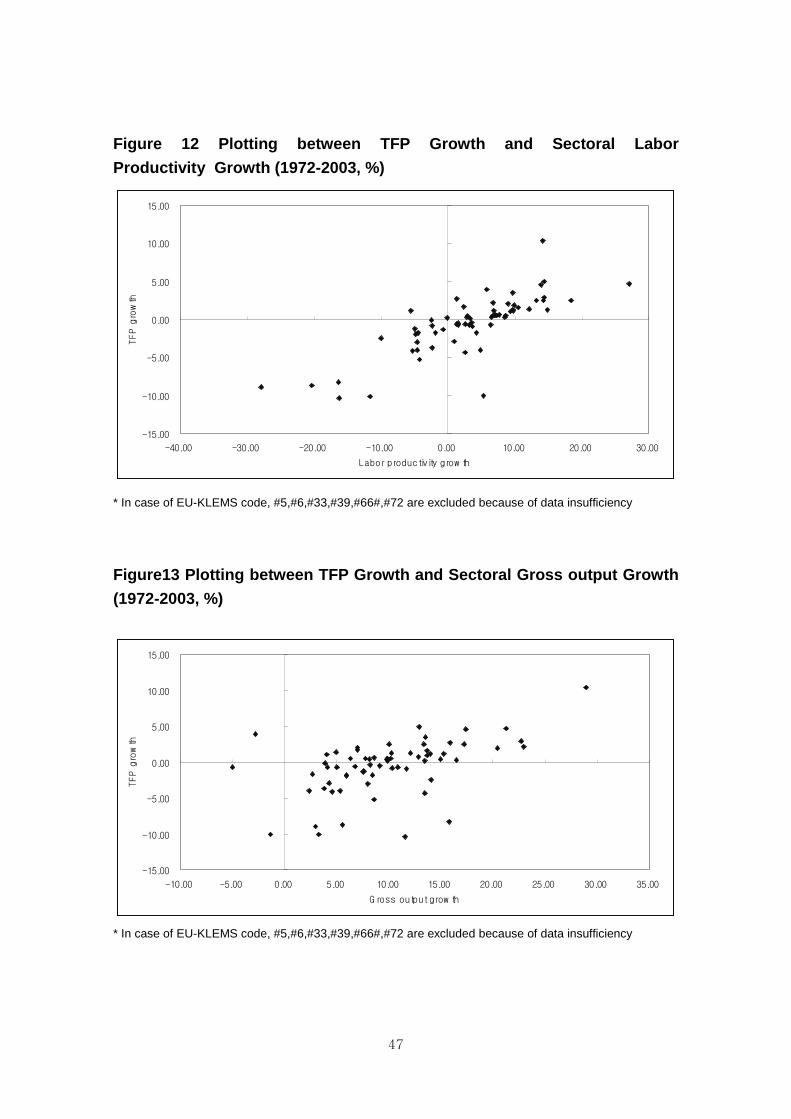

3.4 Relations of TFP growth with Labor Productivity

and Output Growth

In order to identify the relation between labor productivity growth and TFP

growth, we can divide sectors into 4 groups by the average of growth rates in

Manufacturing or Service as follows:

In Manufacturing, the sectors that are above the average growth rates of both

labor productivity and TFP are:

- Electronic valves and tubes

- Other electrical machinery and apparatus

- Office, accounting and computing machinery

- Basic metal etc

The sectors in Manufacturing that are below the average growth rates of both

45

labor productivity and TFP are:

- Pulp, paper and paper products

- Printing and reproduction

- Wearing apparel

- Food and beverage

- Leather, leather products and footwear etc

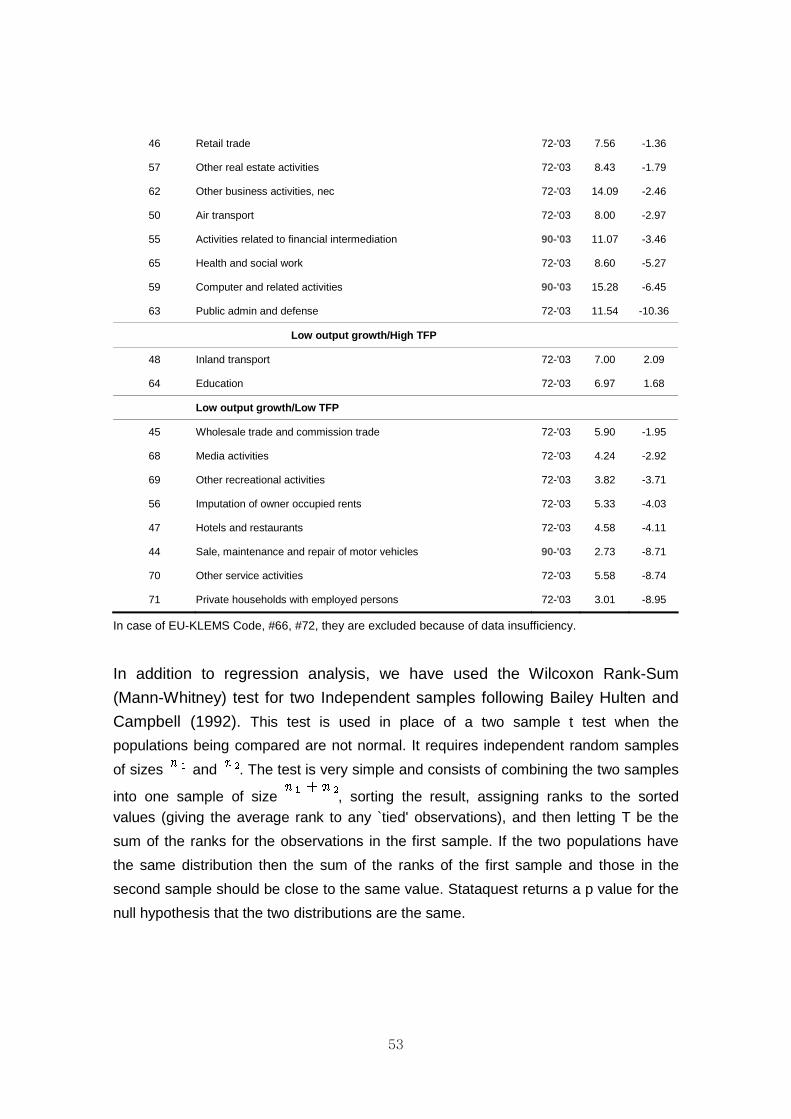

On the other hand, in Service the sectors that are below the average growth

rates of both labor productivity and TFP are:

- Wholesale and retail and Hotels and Restaurants such as i) Retail trade,

ii) Wholesale trade and commission trade, iii) Sale, maintenance and

repair of motor vehicles, iv)Hotel and restaurants, and

- Business service such as i) Other business activities, ii) Computer and

related activities, and

- Social and private service such as i) Private households with employed

persons, ii) Public administration and defense etc.

In order to examine the relation between output growth and TFP growth, we can

divide sectors into 4 groups by the average of growth rates in Manufacturing or

Service as follows:

In Manufacturing (Table 15), the sectors that are above both the average growth

rate of output and that of TFP are over the average growth rates in

manufacturing in terms of output or TFP are:

- IT manufacturing sectors such as i) Electronic valves and tubes, ii)

Telecommunication equipment, iii) Office, accounting and computing

machinery, iv) Radio and television receivers, v) Other electrical

machinery and apparatus etc, and

- Traditional manufacturing sectors such as i) Machinery, ii) Chemicals etc.

Furthermore the sectors, labor intensive and relative advantage in Korean

economy during 1970s-1980s, which the growth rates are over the average

growth rates in manufacturing in terms of output or TFP simultaneously are:

- Pulp, paper and paper products

- Printing and reproduction

- Wearing apparel

- Food and beverage

46

- Leather, leather products and footwear etc

On the other hand, the sectors in Service that are above the average growth

rates (Table 16) of both output and TFP are:

- Gas supply

- Financial intermediation

- Post and telecommunication

The sectors in Service that are under the average growth rates of both output

and TFP are:

- Wholesale trade and commission trade,

- Hotels and restaurants

- Sale, maintenance and repair of motor vehicles etc

In case of i) Gas supply, ii) Financial intermediation, iii) Post and

telecommunication, they seem to have relative advantages in terms of

sectoral potential growth. But in case of i) Wholesale trade and commission