EMEA conference

Transforming tax –

making it work

The Crystal, London

9-10 June 2015

1

2

EMEA conference

Plenary 2

Transformation –

what and how?

“God grant me the serenity to accept the things I cannot change, the courage to

change the things I can and the wisdom to know the difference”

Ignatius Loyola c 1520

3

4

Tax

Transformation

What and how?

Tax transformed – the “professionalisation” of tax

5

People and

organisation

Processes

Systems

Tax Risk Management

Risks

ControlsTest

Report

Tax Policy Framework

Risk

appetite

Decision

making

Control

standards

Oversight

KPIs/KRIsCulture

and

ethics

Accountabilities

Tax Vision, Goals

and StrategyTax Outputs and

Communication

6

Tax policy, risk

and operations

Increasing formalisation of tax policy

7

Accountabilities for taxes getting clearerGroups are increasingly defining their tax policy

Source: Deloitte Global Market Research, 2014

47%

29%

23%No

Yes, for some areas

Yes, for all four areas

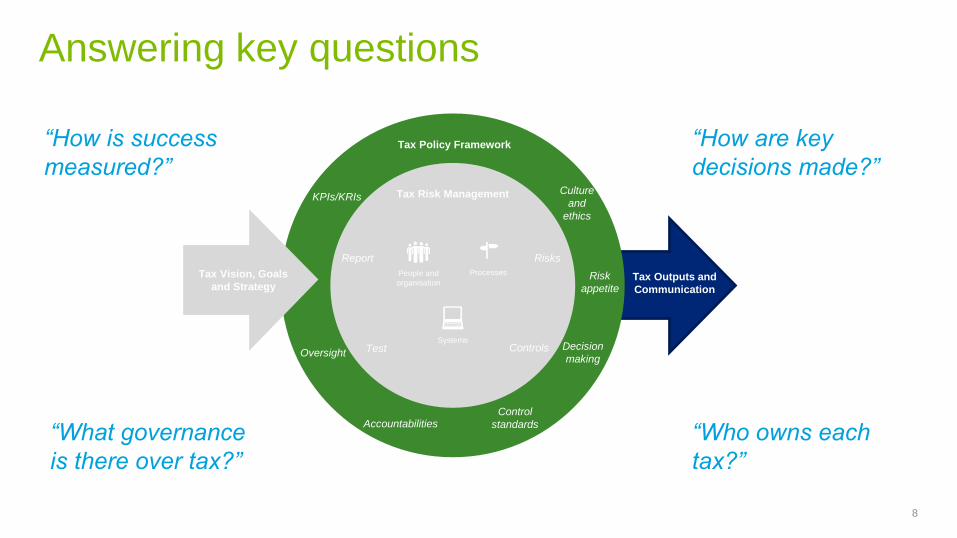

Answering key questions

8

People and

organisation

Processes

Systems

Tax Risk Management

Risks

ControlsTest

Report

Tax Policy Framework

Risk

appetite

Decision

making

Control

standards

Oversight

KPIs/KRIsCulture

and

ethics

Accountabilities

Tax Vision, Goals

and StrategyTax Outputs and

Communication

“How is success

measured?”

“How are key

decisions made?”

“Who owns each

tax?”

“What governance

is there over tax?”

Identifying, controlling and reporting tax risks

9

Groups generally have processes for

identifying, controlling and reporting tax risk

More and more third parties have a specific

interest in tax risks and how they are managed

• Tax Authorities – e.g. UK,

Australia, Netherlands, Japan,

Spain

• International bodies – e.g. OECD

• Other regulators – e.g. FRC

• Investors – e.g. Local Authority

Pension Fund Forum

• Analysts – e.g. Schroders, Citi

• Indices – e.g. Dow Jones

Sustainability Index, MSCI World

• NGOs – e.g. Action Aid

Source: Deloitte Global Market Research, 2014

Developing a risk-based approach

10

People and

organisation

Processes

Systems

Tax Risk Management

Risks

ControlsTest

Report

Tax Policy Framework

Risk

appetite

Decision

making

Control

standards

Oversight

KPIs/KRIsCulture

and

ethics

Accountabilities

Tax Vision, Goals

and StrategyTax Outputs and

Communication

“How do we report to

the Tax Committee?”

“What are our key

tax risks?”

“Who are our ‘lines

of defence’?”

“When is Internal

Audit testing tax?”

Global tax operating models

11

Increasingly centralised decision-making

12

Global tax operating models: past, present and future

Source: Deloitte Global Market Research, 2012 and 2014

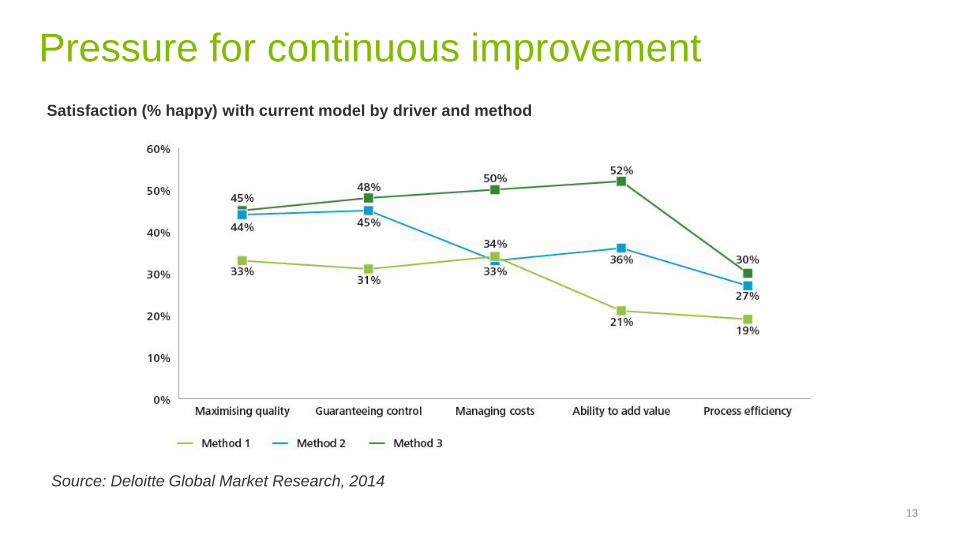

Pressure for continuous improvement

13

Satisfaction (% happy) with current model by driver and method

Source: Deloitte Global Market Research, 2014

Evolving the operating model

14

“Do we have the

right scale, roles,

locations?”

“Can we streamline

adjacent

processes?”

“What is the right

in/out/co-source

model?”

People and

organisation

Processes

Systems

Tax Risk Management

Risks

ControlsTest

Report

Tax Policy Framework

Risk

appetite

Decision

making

Control

standards

Oversight

KPIs/KRIsCulture

and

ethics

Accountabilities

Tax Vision, Goals

and StrategyTax Outputs and

Communication

“Can we leverage

our Shared Service

Centres?”

15

Tax

technology

Technology satisfaction levels

16

Source: Deloitte Global Market Research, 2014

Plan, budget, responsibility

17

Source: Deloitte Global Market Research, 2014

18

WHAT

can and cannot be solved with tax

technology?

solutions are relevant for tax?

do you choose: buy or build your

own?

Tax technology

19

WHAT

Tax technology

can and cannot be solved with tax

technology?

20

WHAT

Tax technology

solutions are relevant for tax?

21

WHAT

Tax technology

do you choose: buy or build your

own?

22

What are companies doing?

23

AIM

Tax technology

technology to support both your tax

function as well as your organisation

as a whole

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities.

DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see

www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. With a globally

connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights

they need to address their most complex business challenges. Deloitte’s more than 210,000 professionals are committed to becoming the standard of excellence.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte

Network”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained

by any person who relies on this communication.

© 2015. For information, contact Deloitte Touche Tohmatsu Limited. 24

Recommended