Effective Customer Retention Techniques in Group Lending

Objectives

• At the end of this training, you will

– Identify reasons why customer retention is critical for any

business

– Understand why customers leave the financial institutions or

the groups they belong to

– Determine challenges associated with the group lending

methodology

– Identify strategies for retaining customers in the financial

institution and the group

Content

• What is customer retention?

• Group lending and its benefits

• Why members desert groups or the FI

• Customer retention techniques

What is customer retention? Session 1

Customer retention

• What is customer retention?

• The process where customers continue to buy

products and services within a determined time period

– Simply put…

• the ability of a business to keep its customers over a specific period

of time

• the activities and actions that businesses take in order to reduce the

number of customers who leave.

• The goal of customer retention is to help businesses keep as

many customers as possible.

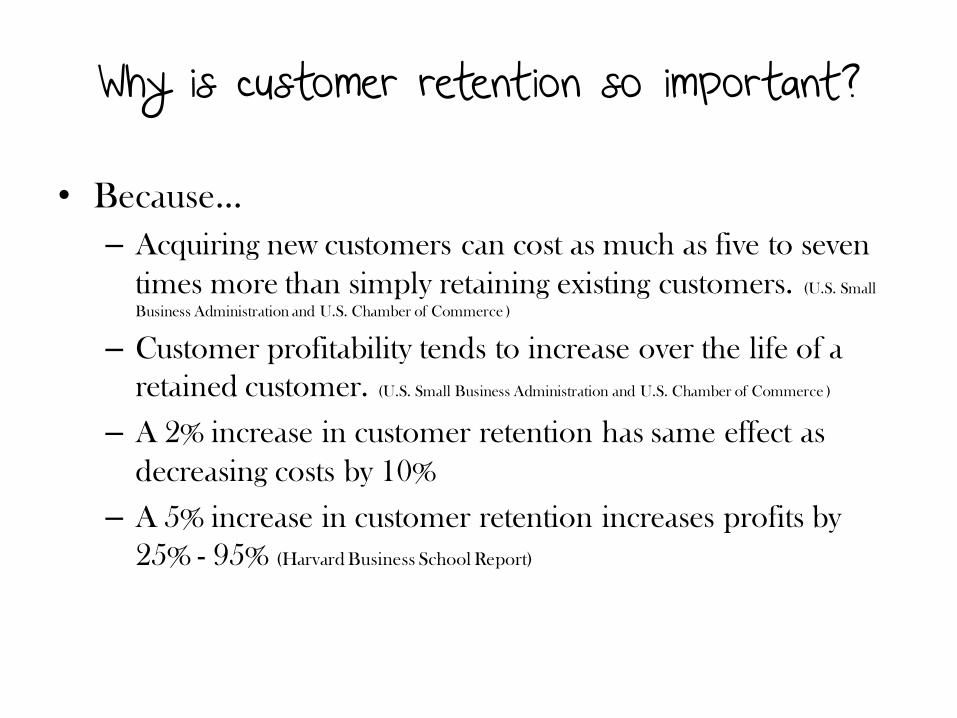

Why is customer retention so important?

• Because…

– Acquiring new customers can cost as much as five to seven

times more than simply retaining existing customers. (U.S. Small

Business Administration and U.S. Chamber of Commerce )

– Customer profitability tends to increase over the life of a

retained customer. (U.S. Small Business Administration and U.S. Chamber of Commerce )

– A 2% increase in customer retention has same effect as

decreasing costs by 10%

– A 5% increase in customer retention increases profits by

25% - 95% (Harvard Business School Report)

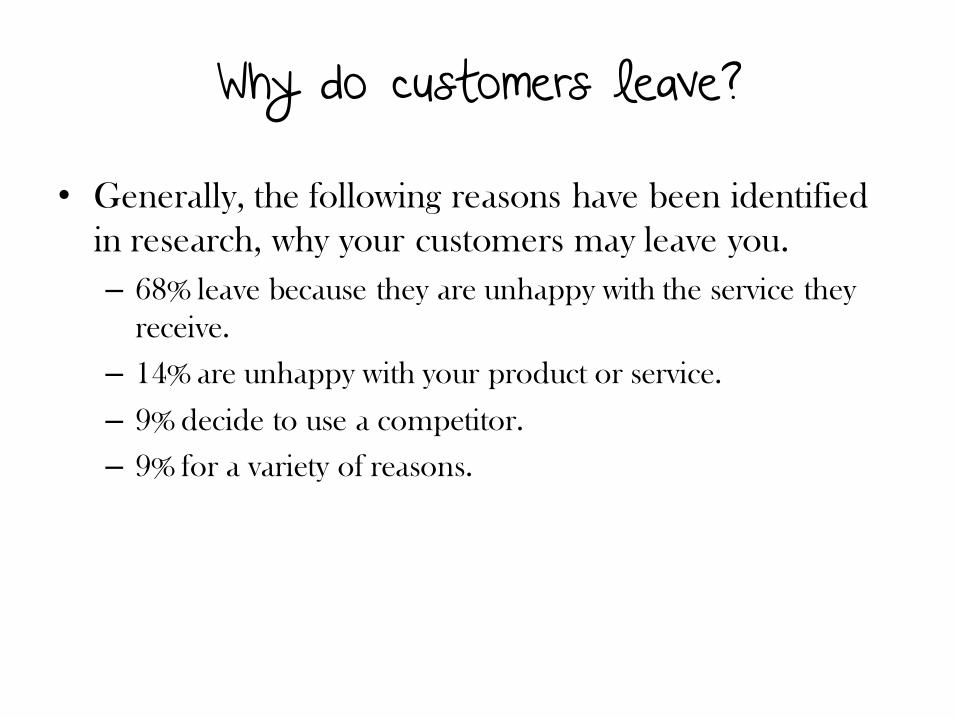

Why do customers leave?

• Generally, the following reasons have been identified

in research, why your customers may leave you.

– 68% leave because they are unhappy with the service they

receive.

– 14% are unhappy with your product or service.

– 9% decide to use a competitor.

– 9% for a variety of reasons.

Why do customers leave?

• Lets assume that nothing can be done about the

– 9% who decide to use a competitor and

– 9% who leave for various reasons

• Why?

– Because some customers will still leave you no matter how much

effort you put into making them happy…you can’t win them all

• That leaves us with 82% of our customers

– Let’s focus our energies on what to do to retain this percentage of

our customer base.

Why do customers leave?

• But why do customers leave a financial institution (FI)

or a solidarity group to which they belong in the FI?

– When we know why customers leave, then we can devise

better strategies and techniques to retain them.

– To understand why customers leave, we need to take a look

at what group lending entails

Group lending and its benefits Session 2

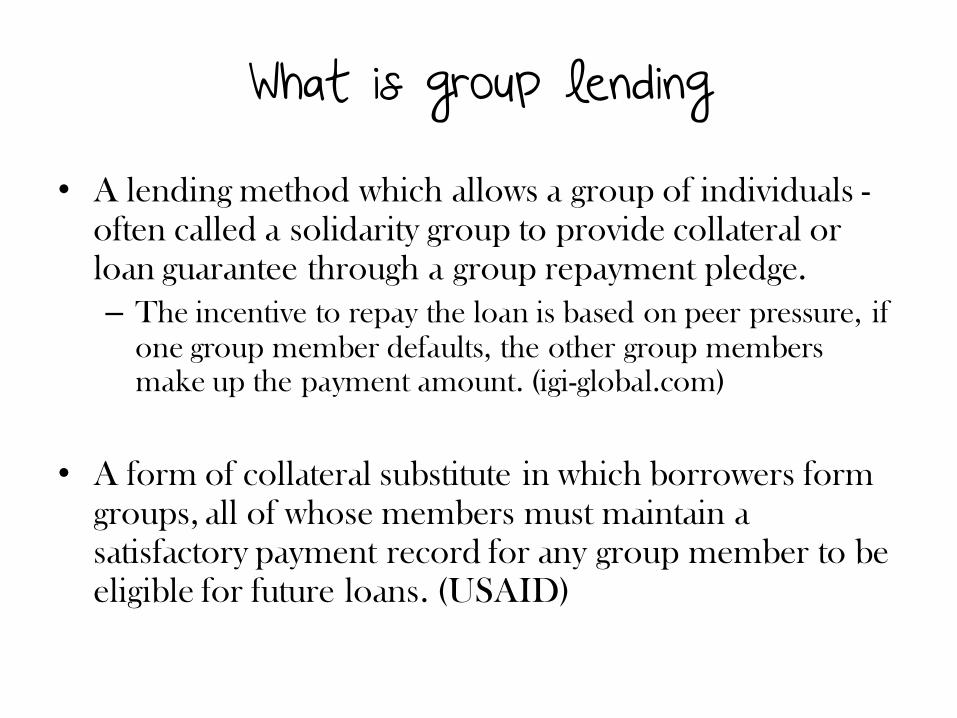

What is group lending

• A lending method which allows a group of individuals - often called a solidarity group to provide collateral or

loan guarantee through a group repayment pledge.

– The incentive to repay the loan is based on peer pressure, if

one group member defaults, the other group members make up the payment amount. (igi-global.com)

• A form of collateral substitute in which borrowers form

groups, all of whose members must maintain a

satisfactory payment record for any group member to be eligible for future loans. (USAID)

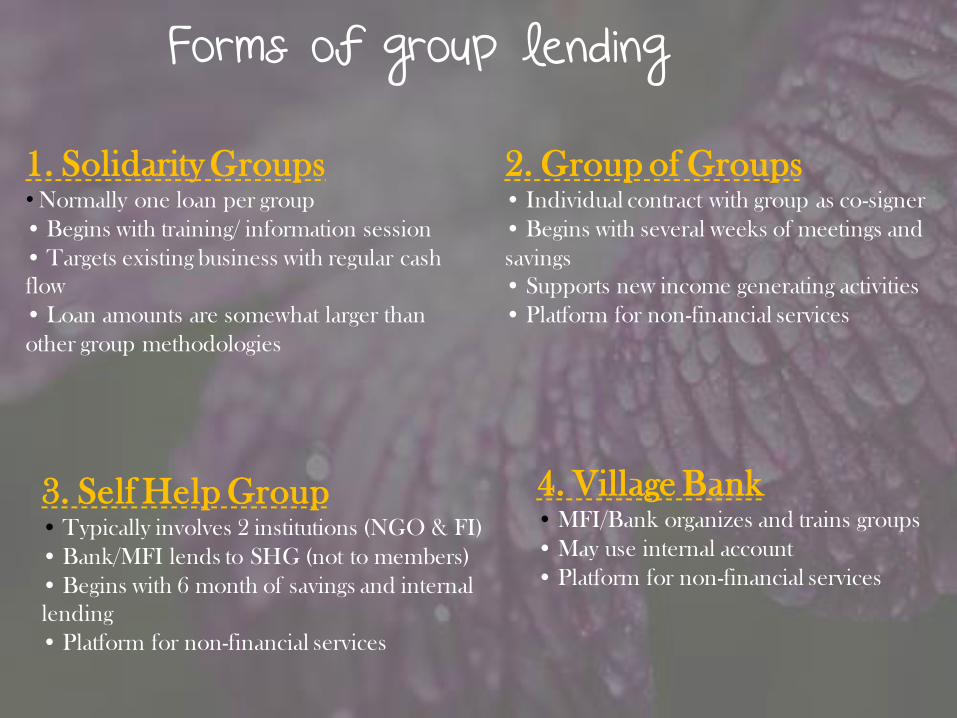

1. Solidarity Groups • Normally one loan per group

• Begins with training/ information session

• Targets existing business with regular cash

flow

• Loan amounts are somewhat larger than

other group methodologies

4. Village Bank • MFI/Bank organizes and trains groups

• May use internal account

• Platform for non-financial services

2. Group of Groups • Individual contract with group as co-signer

• Begins with several weeks of meetings and

savings

• Supports new income generating activities

• Platform for non-financial services

3. Self Help Group • Typically involves 2 institutions (NGO & FI)

• Bank/MFI lends to SHG (not to members)

• Begins with 6 month of savings and internal

lending

• Platform for non-financial services

Forms of group lending

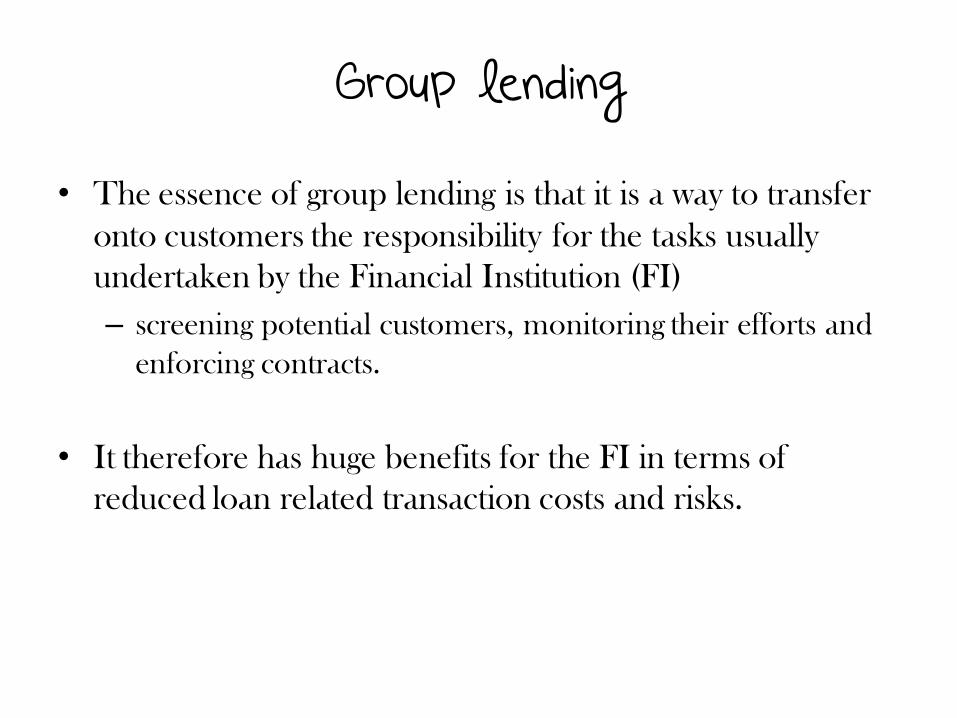

Group lending

• The essence of group lending is that it is a way to transfer

onto customers the responsibility for the tasks usually

undertaken by the Financial Institution (FI)

– screening potential customers, monitoring their efforts and

enforcing contracts.

• It therefore has huge benefits for the FI in terms of

reduced loan related transaction costs and risks.

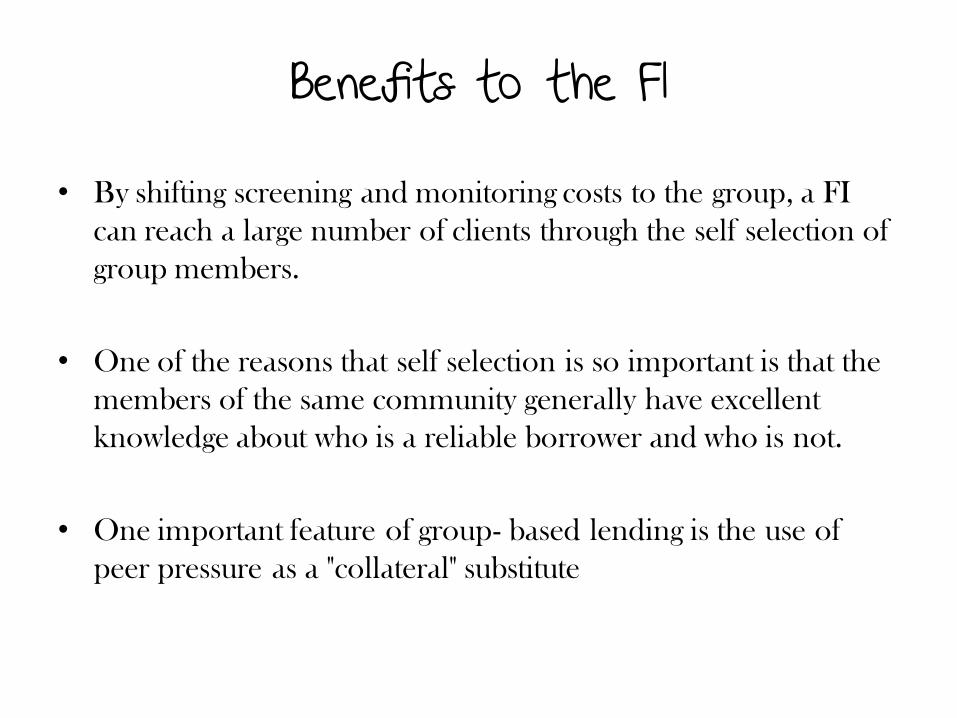

Benefits to the FI

• By shifting screening and monitoring costs to the group, a FI

can reach a large number of clients through the self selection of

group members.

• One of the reasons that self selection is so important is that the

members of the same community generally have excellent

knowledge about who is a reliable borrower and who is not.

• One important feature of group- based lending is the use of

peer pressure as a "collateral" substitute

Benefits to the customer

• Group lending also has a wide range of benefits for the customers or group members. Lets look at some of them:

• Many group-based lending programs target the very poor, who cannot meet the traditional collateral requirements of most

formal financial institutions such as commercial banks and non-

bank financial institutions.

• Group lending therefore enables people who would otherwise

not have access to financial capital due to lack of collateral, to do so. – Thus the very poor and underprivileged can also do business

Benefits to the customer

• Dynamic group membership could lead to

empowerment

• Customers have the liberty to choose their group members,

ensuring that members choose people they trust as credible

borrowers

– Where the group is dynamic enough, they can, as a group, access

various services, not only from the bank. There are NGOs who

provide business development services to community groups and

they can take advantage of this and other services as well.

– People are however, usually very careful about who they admit into

their group, given the threat of losing their own access to credit or

having their own savings used to repay other people's loans.

Group lending

• If the FI is important to the business survival of the

customer and

• If group lending has good benefits for the customer,

– why do the customers still leave and

– What measures can we take to ensure that we retain them?

Why members desert the financial institution and/or the group

Session 3

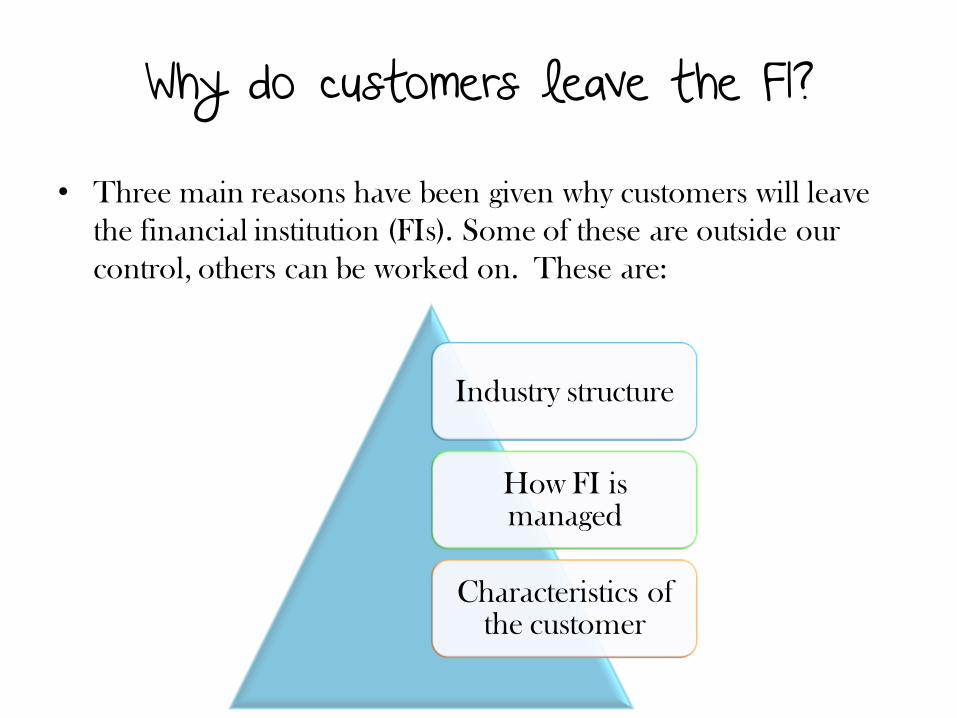

Why do customers leave the FI?

• Three main reasons have been given why customers will leave

the financial institution (FIs). Some of these are outside our

control, others can be worked on. These are:

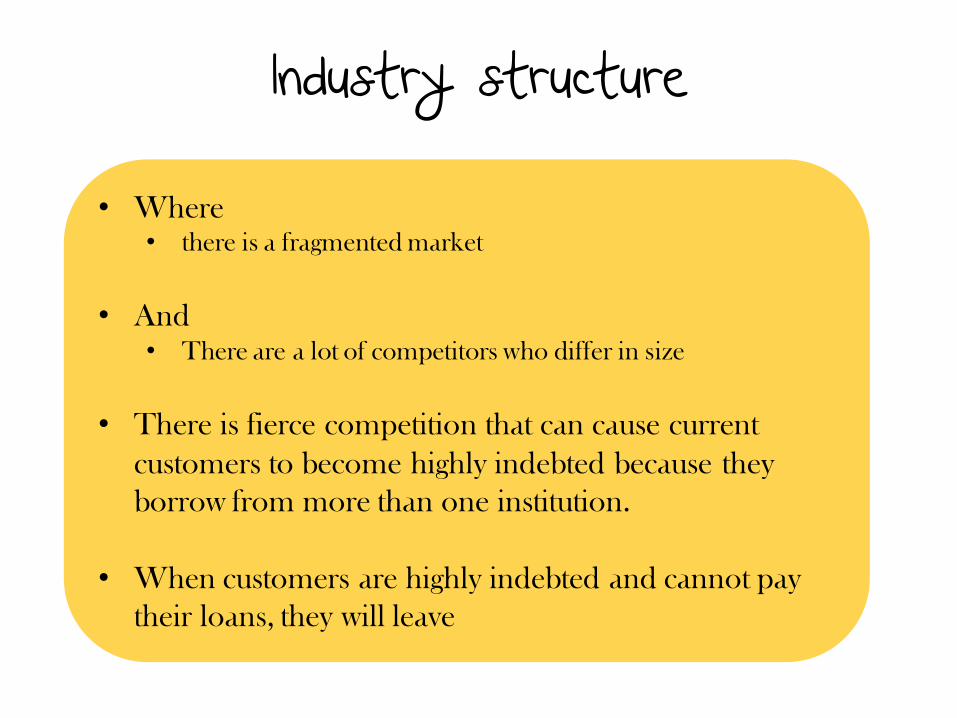

Industry structure

How FI is managed

Characteristics of the customer

• Where • there is a fragmented market

• And • There are a lot of competitors who differ in size

• There is fierce competition that can cause current

customers to become highly indebted because they

borrow from more than one institution.

• When customers are highly indebted and cannot pay

their loans, they will leave

Industry structure

Satisfaction with the product

•Customers have needs and the FI has products. Customers want solutions to their needs and if the products do not solve their needs, they will go.

•Are your products flexible enough to meet their needs in terms of credit use, maximum amounts, repayment periods etc.

•Where products are seen as the same from one FI to the other, there is not much incentive to remain. Develop unique products

Emotional involvement with FI

• Customers tolerate their FI’s weaknesses because of the emotional bond they have with loan officers, other staff or the FI itself. Without emotional involvement, they will leave. There must be emphasis on relationship building with customers.

• Loyalty is based on emotions, which is why it is important to identify and meet customer’s emotional needs. When customers emotional needs are not met they will leave. ie To be:

• respected

• Acknowledged

• Remembered etc.

How the FI is managed

Quality of Customer Service

•Customers expect some minimum level of customer service and when they don’t get it, they may leave.

•Key contact points with customers in the lending process are opportunities to provide excellent customer service. Customers however face challenges at these contact points. We’ll look at some of them.

Image or reputation of the FI

•Sometimes, positioning the FI as a small one makes some customers see it as a temporary solution. Once their business grows bigger, they start looking for other service providers. eg. Some institutions are positioned as credit providers so customers only take credit from them but open savings accounts with other institutions.

•Other FIs have earned the reputation of being ruthless when it comes to collection of loans, they use all kinds of methods to get it. People will be reluctant to come to you. Do business with a human face

How the FI is managed

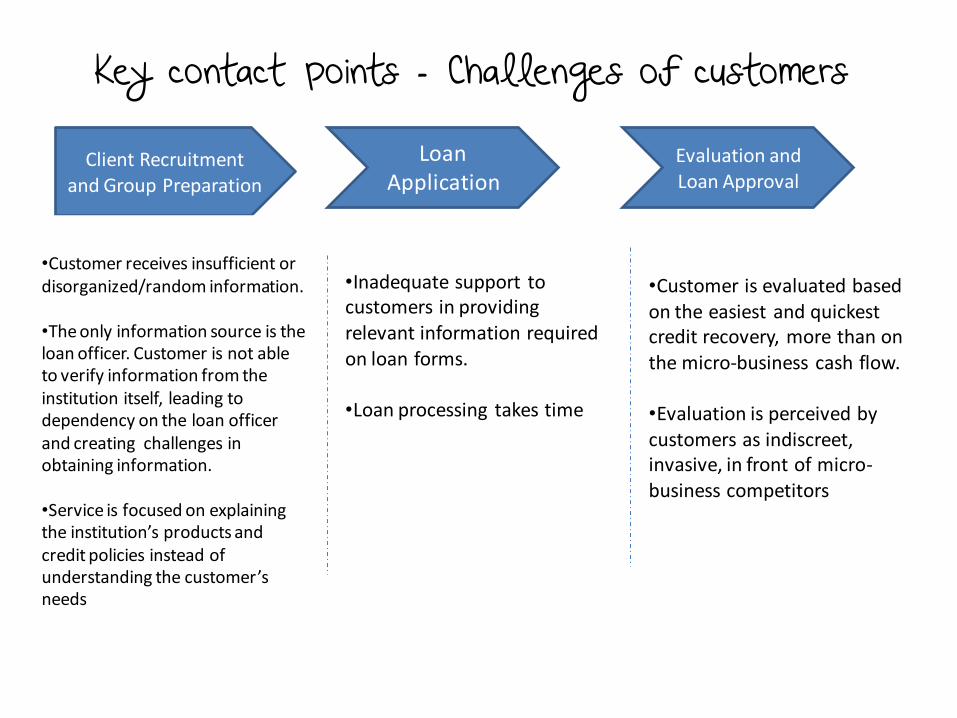

Client Recruitment and Group Preparation

Loan Application

Evaluation and Loan Approval

•Customer receives insufficient or disorganized/random information. •The only information source is the loan officer. Customer is not able to verify information from the institution itself, leading to dependency on the loan officer and creating challenges in obtaining information. •Service is focused on explaining the institution’s products and credit policies instead of understanding the customer’s needs

•Customer is evaluated based on the easiest and quickest credit recovery, more than on the micro-business cash flow. •Evaluation is perceived by customers as indiscreet, invasive, in front of micro-business competitors

Key contact points – Challenges of customers

•Inadequate support to customers in providing relevant information required on loan forms. •Loan processing takes time

Key contact points – Challenges of customers

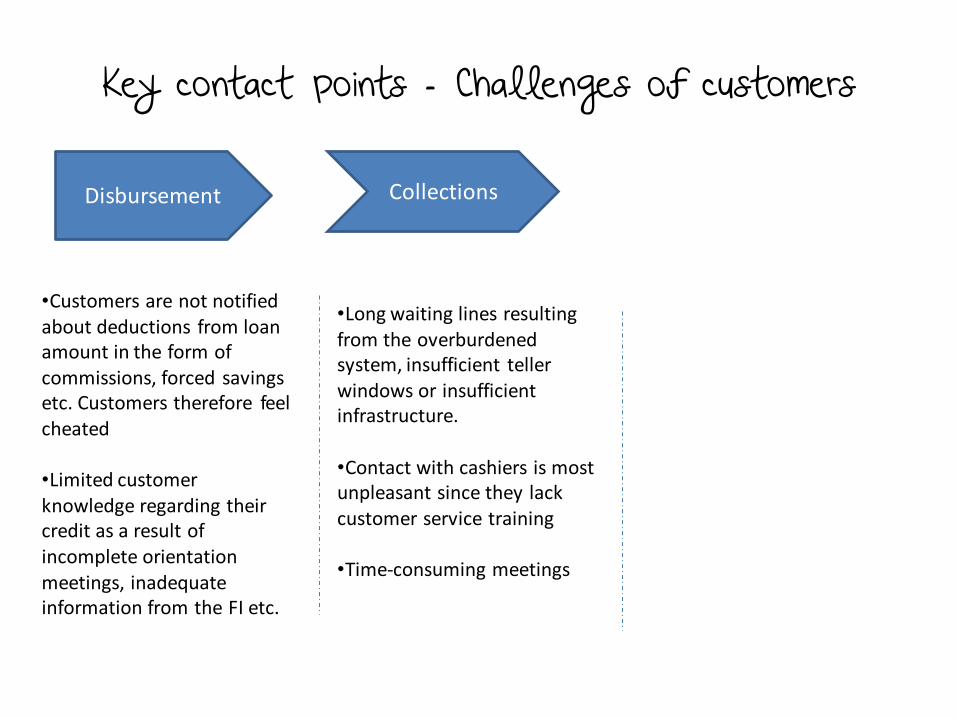

Disbursement Collections

•Customers are not notified about deductions from loan amount in the form of commissions, forced savings etc. Customers therefore feel cheated •Limited customer knowledge regarding their credit as a result of incomplete orientation meetings, inadequate information from the FI etc.

•Long waiting lines resulting from the overburdened system, insufficient teller windows or insufficient infrastructure. •Contact with cashiers is most unpleasant since they lack customer service training •Time-consuming meetings

Group Activity

• Let’s take another look at the lending process

– 1. For each stage in the lending process, identify

other challenges that customers may be facing,

which have not been discussed.

– 2. For each stage, prescribe ‘workable solutions’ to

the challenges that have already been discussed and

any new ones you have identified.

– Use sheet 1

Characteristics of the customer

• Many FIs take for granted that their customers need credit.

• Customers do not seek credit as such: rather they are looking

for solutions to their needs

• Besides, micro-entrepreneurs have a variety of financial needs

such as

– savings,

– training,

– networking,

– business advisory services and related

– micro business services.

Do you know your

customers’ needs?

Customers leave because

their needs are not being

met.

Why do members desert the groups?

• Let’s now turn our attention to why members leave the

group.

• Two key reasons have been identified as to why

members may desert a group:

– Features of the group lending method

– Interpersonal challenges with group members

Let’s discuss some of the

features of the group lending

method which may be driving

away our customers

Why do members desert the groups?

– Customers suffer through no fault of theirs because a group member has defaulted in their payments.

• Thus the default of one member in a group generally means that further lending to other group members is stopped until the loan is repaid.

– For instance, in the event that several members of a group encounter repayment difficulties, then the entire group is

faced with economic challenges and the group collapses.

– Sometimes a borrower through no fault of her own has liquidity problems. What happens then?

Excessive group pressure and lack of flexibility

Why do members desert the groups?

– Customers have little privacy over their financial

matters as every group member is aware of

payments or defaults of others.

• The use of public payments as a way of shaming

customers is unattractive

Lack of privacy

– Customers are entitled to limited or fixed loan amounts

whether it serves their needs or not

– Customers are forced to make payments at fixed periods ie.

weekly, whether it corresponds with their cash flow or not .

– It is sometimes unrealistic to impose regular payments in

areas with highly seasonal occupations, such as agriculture.

Lack of flexibility with respect to credit

Fixed payment durations

– Customers feel detached from the FI as no real relationship

is established on an individual level between loan officers

and customers, especially where the practice is that the loan

officer deals with the group leader more frequently, not

necessarily all group members.

– Attending meetings can be costly, both in terms of time and

money, particularly in sparsely populated areas.

Individual relationship with the FI is not established over time

Making time to attend meetings

How do we overcome this

challenge?

– Customers need to find other borrowers in order to be

eligible for a loan

– This comes with its own risks that most customers do not

want to bear

– In sparsely populated areas and urban areas, customers

might not have good information on each other and may

therefore make wrong choices in selecting group members

– a mistake they will have to pay for dearly in the form of

financial punishment by being forced to repay other people's

loans due to their lack of " financial discipline"

The risk of finding credible borrowers to partner with

– A group loan product may not be suited to the needs of a

particular area or business

– You need to do your own assessment to determine if the

social/geographical/business context is ideal for group

lending

Group-based lending does not work well in all contexts

or circumstances

Why do members desert the groups

• Interpersonal challenges also play a role in why people leave groups.

• Interpersonal skills are those skills which are necessary for relating and working with others – such as verbal and non-verbal communication, listening, giving and receiving feedback.

• As with any human gathering, there are bound to be challenges because we

– Are all different,

– Come from different backgrounds

– Have different experiences

– Relate to people differently

Why members desert the group

• Being able to understand and work with others in teams or

groups is an important aspect of interpersonal skills.

– The focus is on ensuring teamwork, group effectiveness, decision making, running meetings etc.

• Loan officers need provide interpersonal skills training

from time to time as part of group meetings.

• This will prepare groups to expect such challenges since

they are inevitable as well as give them the skills to handle them

Strategies to retain customers Session 4

Customer retention strategies

Group lending related

Product or service related

Customer related

Strategies relating to group lending

• Embark on progressive lending as against fixed credits

– Progressive lending promises larger and larger loans for groups and

individuals in good standing. This will even encourage customers to

quickly pay back their loans since they will receive bigger amounts with

time.

• Match repayment schedules to business cash flow

– Where possible, micro-entrepreneurs involved in the same line of

business should be encouraged to form a group since their business cash

flows may be similar especially in seasonal businesses. This may make it

easier for the FI to match repayment schedules to their cash flow and

make it easier for them to pay back their loans.

Strategies relating to group lending

• Eliminating or relaxing the rules of joint liability.

– Given that many micro entrepreneurs do not want to be

penalized for the defaults of other group members, other

measures to ensure repayments needs to be adopted such

that the rules of joint liability can be relaxed or eliminated.

– FIs can give incentives to customers by threatening to

exclude defaulting customers from future access to loans,

not necessarily punishing the whole group for one person’s

default

Strategies relating to group lending

• Ensuring that existing customers do not contract new

loans either

– From the same institution

• this can be easily done by cross checking internal records

– From another institution in the area

• This can be done by using credit bureaus or designing ways that

promote information sharing between FIs, so that a customer that

defaults on one FI loan would not be able to turn to another FI

within a certain catchment area and be granted a loan

Strategies relating to group lending

• Financial literacy

– Promoting financial literacy among clients may help them in

their borrowing decisions, which in turn may limit multiple

loan-taking.

• Provide short training during group meetings

• Give them hands-on support to help them understand financial

issues

Product & service related strategies

• Be the expert – Provide technical support

• Micro-entrepreneurs are usually people with very little

understanding of business and business skills.

– Provide them with technical skills training, how to manage

their capital etc. and follow up on them.

• No matter what industry your customers operate in, if

you can be an expert to them in the area of managing

their businesses, you will likely retain more customers

Product & service related strategies

• Product or service integrity

• There must always be total consistency between what

you say and do and what your customers experience.

– Long-term success and customer retention belongs to those

who do not take ethical shortcuts.

• The design, quality and serviceability of your product

or service must be of the standard your customers

want, need and expect.

Product & service related strategies

• Service integrity is also demonstrated by the way you

handle the small things, as well as the large.

• Customers will be attracted to you if you are

– open and honest with them,

– care for them,

– take a genuine interest in them,

– don’t let them down and

– practice what you preach … and they will avoid you if you

don’t.

Customer related strategies

• Know your customers’ needs and expectations in

terms of product and service.

• The customer has 2 separate needs that must be met:

– needs relating to your product

• Is your product a solution to their business needs?

• Is it only credit they need as a micro/small business? How about

savings?, technical skills? Etc.

Customer related strategies • Needs relating to your service

– Customers are first and foremost individuals

– As individuals we like to be:

• Heard

• Understood

• Respected

• How well are you meeting both needs of your

customers?

46

Other customer retention strategies

• You can also retain customers by

• Reducing attrition

– The easiest way to grow your business is not to

lose your customers.

– Once you stop the leakage, it is often possible to

double or triple your growth rate because you’re

no longer forced to make up lost ground, you can

just stand still.

• Virtually every business loses some customers, but few ever measure or recognize how many of their customers become inactive.

– Take some time to cross check on the number of customers who have left and you may be surprised at how much your institution is losing

• Most businesses, ironically, invest an enormous amount of time, effort and expense in building that initial customer relationship.

– Then they let that relationship go unattended.

• In some cases they even lose interest as soon as the sale has been made, or even worse, they abandon the customer as soon as a problem occurs. Rather than resolve the problem, they spend another small fortune to replace that customer.

By building relationships with customers

• Build trust through relationships

– As the age old saying goes, you do business with people you

trust.

– Trust is essential in business, and building relationships with

clients will give you that trust

– Implement a relationship marketing strategy in order to

ensure consistent relationship building with customers. This

is of particular importance because you are a service-based

business

By giving good customer service

• Customer service is the provision of service to customers

– before,

– during, and

– after a purchase.

• Customer service has often been done badly because it has

been defined badly.

Class Activity: In what ways can we give good customer service

• Before service delivery

• During service delivery

• After service delivery

By following up on old customers

• Bring back the “lost sheep”

• Reactivate customers who already know you and your product. This is one of the easiest and quickest ways to retain customers and increase your revenues.

– It is sometimes easier to go back to a relationship you had which has ended than to embark on a new one, especially if the old relationship is promising change

• There is little point in dedicating a lot of resources to finding new customers when 25-60% of your dormant customers will be receptive to your attempts to do business with you if you approach them the right way, with the right offer.

• Get in touch with former customers

• Remind them of your existence as an institution

• Find out why they’re no longer with you

• Take note of their concerns and act on them

• Demonstrate that you still value and respect them by being

consistent in the areas they had problems with you before

– This approach is cheaper than exploring new relationships with totally

new customers and may lead to some of your best and most loyal

customers.

By taking complaints seriously

• A complaint is a gift

• 96 percent of dissatisfied customers don’t complain. They just walk away, and you’ll never know why. That is because they

– often don’t know how to complain or who to complain to

– can’t be bothered

– are too frightened, or

– don’t believe it’ll make any difference.

• Though they may not tell you what is wrong, they will certainly tell many others. A system for unearthing complaints can therefore be the lifeblood of the institution because customers who complain are giving you a gift.

• Complaints are gift packages waiting to be opened because they:

– Are given freely

– Are not solicited

• You do not incur any cost to get them – free information

– Are unexpected…they come as a surprise (usually)

– Hold the key to happiness for the FI

• If they are well handled

• A complaint gives you:

– Free direct communication from the customer about

• service failures, competitors offerings etc. without the added cost of

conducting a survey

– Readily available market research: they define what

customers want

55

• A complaint gives you the opportunity to:

– Increase customer trust

– Build long term relationships-

• customers will use your services again if they believe complaints are

welcomed and addressed

– Rectify service failures

– Engage customers as advocates

So how should complaints be handled?

• Listen to the customer

• Get a proper understanding of the

problem

• Apologise as if you caused the problem,

not someone else

• Acknowledge the customer’s pain or

frustration

• Explain the action you are going to take

and give a time frame for resolving the

problem if possible

• Thank the customer

• Follow up to ensure that the problem has

been solved

• Don’t take it personally

• Remain calm

• Focus on the problem and not

the person

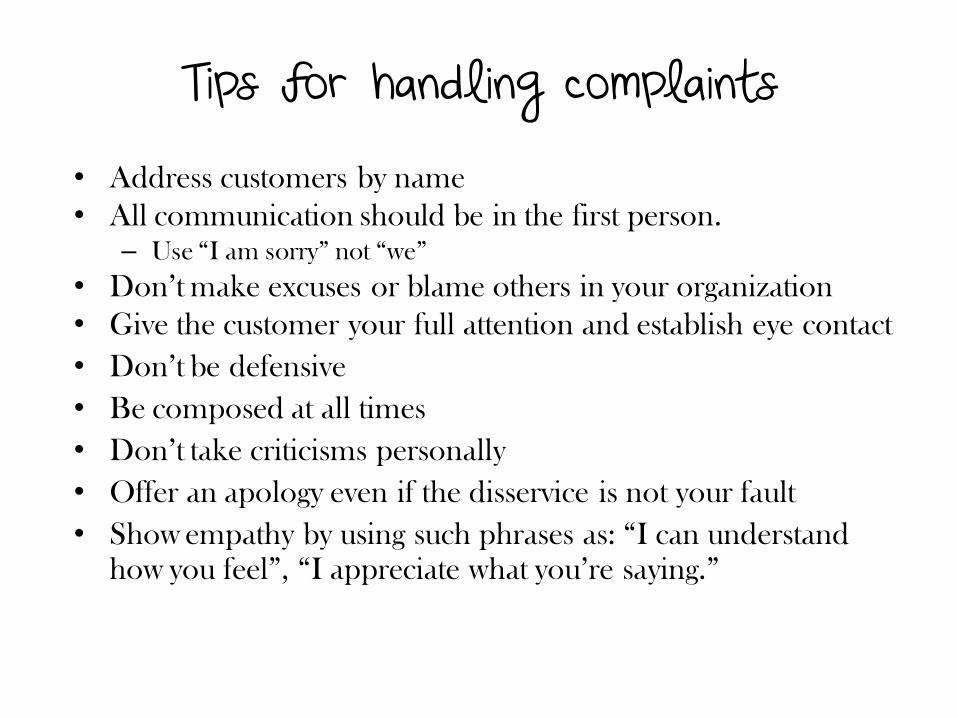

• Address customers by name

• All communication should be in the first person. – Use “I am sorry” not “we”

• Don’t make excuses or blame others in your organization

• Give the customer your full attention and establish eye contact

• Don’t be defensive

• Be composed at all times

• Don’t take criticisms personally

• Offer an apology even if the disservice is not your fault

• Show empathy by using such phrases as: “I can understand

how you feel”, “I appreciate what you’re saying.”

Tips for handling complaints

• If you don’t know the answer to their problem, don’t lie.

• Call back when you say you will, even if for some reason, you

haven’t been able to obtain a satisfactory answer by then

• Tell them what you can do…not what you can’t do

• Find out what it will take to turn their dissatisfaction into satisfaction

• If they agree to that solution, act quickly before they change their mind

• And remember:

– You can never win an argument with a customer

– If you do, it will be to the detriment of the institution because the customer will leave.

Tips for handling complaints

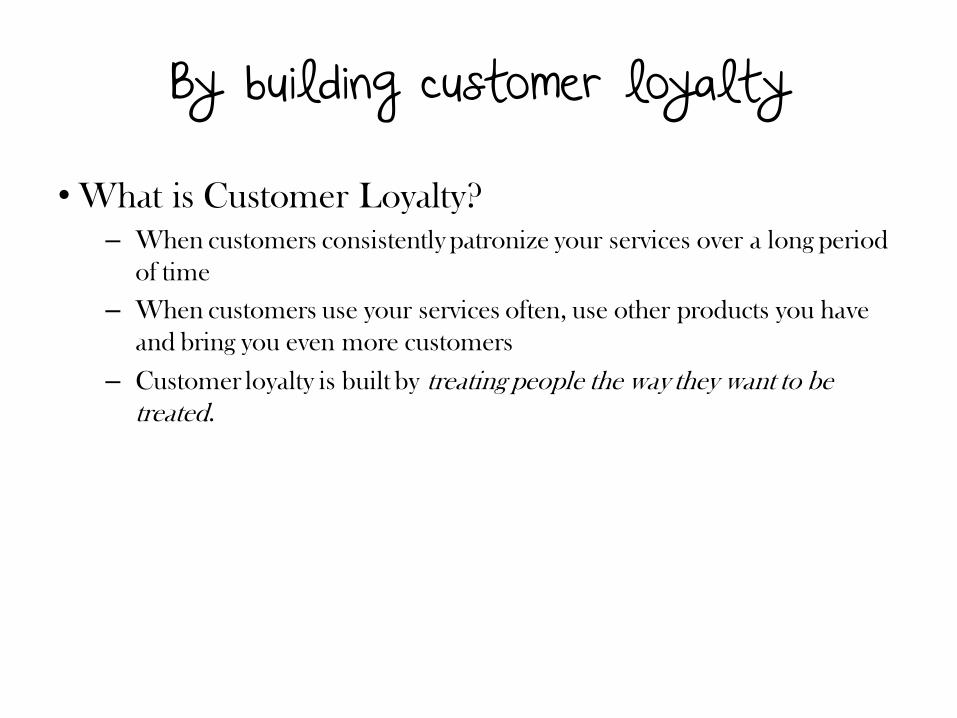

By building customer loyalty

• What is Customer Loyalty?

– When customers consistently patronize your services over a long period

of time

– When customers use your services often, use other products you have

and bring you even more customers

– Customer loyalty is built by treating people the way they want to be

treated.

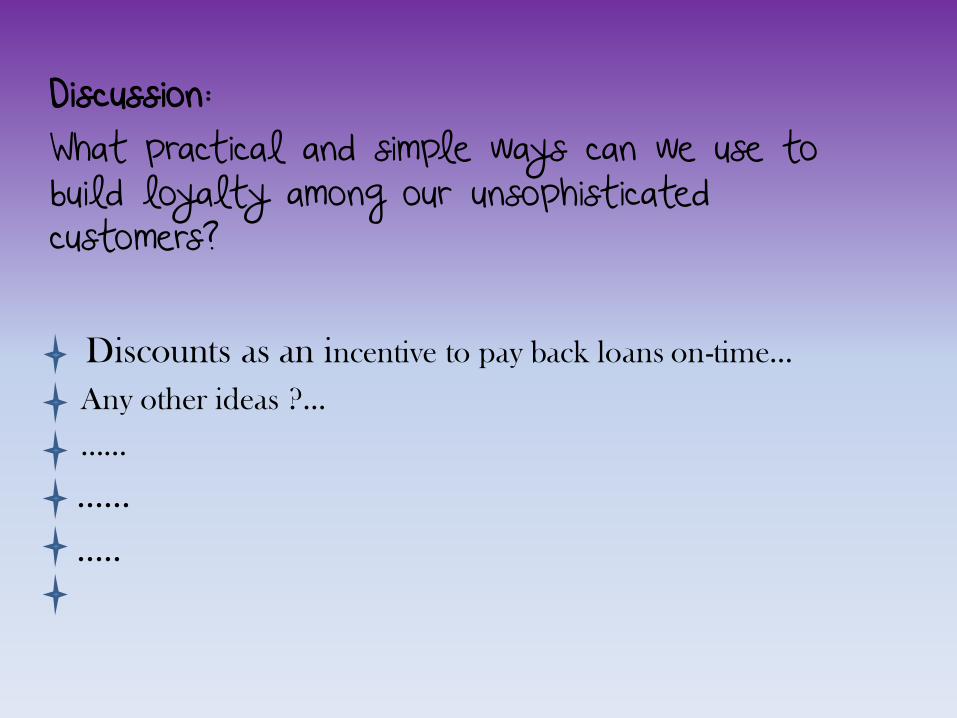

Discussion: What practical and simple ways can we use to build loyalty among our unsophisticated customers?

Discounts as an incentive to pay back loans on-time…

Any other ideas ?…

……

……

…..

Other ways to build loyalty…

• Personal thank you messages

• Showing that you care and remembering what your

customers like and don’t like.

• Ask your customers how they’re doing – and take it to

heart!

• Treat your team well so they treat your customers well.

Resources:

– Urquizo Jacqueline (2006): Improving and Monitoring Customer

Retention

– Riecken Julie & Paulsen Rick: Building Customer Loyalty

– Viswanath P.V.: Beyond group lending

– Davide Castellani (2015): Microfinance Lending Technologies

Recommended