GRAPH 12

TOTAL LOANS AND DEPOSITSCheyenne Area Banks

2000 - 2012

00 01 02 03 04 05 06 07 08 09 10 11 120

100

200

300

400

500

600

Millions

Total Loans Total Deposits

12

CONSTRUCTION

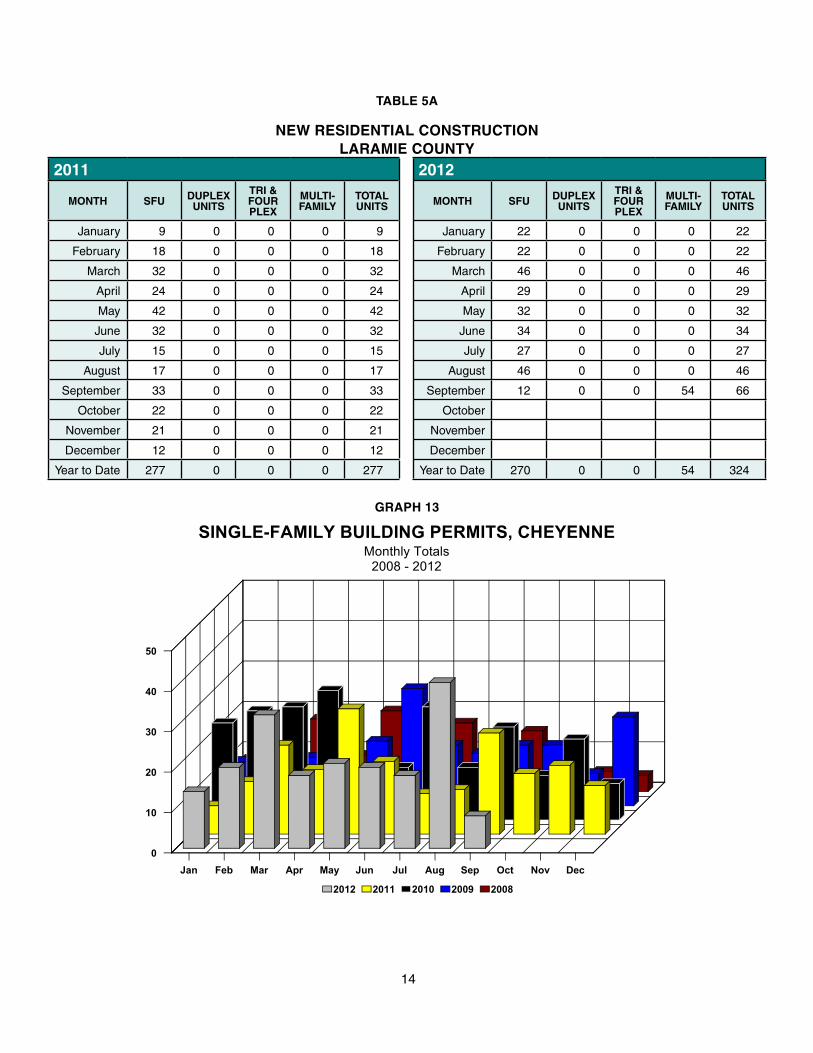

Residential ConstructionTable 5 provides various measures for new residential construction within Laramie County. The number of new residential construction permits skyrocketed within city borders over the third quarter of 2012. This indicator increased 45.7 percent from third quarter 2011 and rose 13.6 percent from second quarter 2012. Even with this large increase, the monthly average through September of 2012 still lagged 2011’s annual average by 2.0 percent. The dollar value of residential construction also did well over the current quarter, up 46.4 percent from the comparable period one year ago. In Table 5A, the total number of new single-family residential permits issued throughout all of Laramie County through the end of September, stood at 270 as compared to 222 over the same period in 2011, an increase of 21.7 percent. Most importantly, one multi-family housing complex was permitted in September and it will contain 54 units. This was the first new apartment complex to be permitted since September 2009.

The average value of a city issued residential home permit was $153,993 over the first three quarters of 2012 as compared to $169,555 for all of 2011 which left the average 2012 value down 9.2 percent from last year. Rural permits for 2012 are also down 2.0 percent over the comparable period.

TABLE 5

CONSTRUCTIONPERCENTAGE PERCENTAGE PERCENTAGEA B C D CHANGE CHANGE CHANGE3Q10 3Q11 2Q12 3Q12 A TO D B TO D C TO D

CONSTRUCTION

Single Fam Bldg Permits – Chey 64 46 59 67 4.69 45.65 13.56

Single Fam Bldg Permits – LarCo 13 19 36 18 38.46 -5.26 -50.00

Total Bldg Permits – (Chey) (a) 148 164 188 170 15.35 3.65 -9.24

Septic Permits – (Rural) 14 14 14 15 7.14 7.14 7.14

Value of Authorized Construction ($000) 6,049 4,540 8,173 16,283 169.17 258.63 99.23

Residential ($000) 3,303 2,416 3,253 3,538 7.12 46.43 8.78

UTILITIES

Commercial Electric Power 52 52 51 48 -6.63 -6.77 -5.15

(‘000,000) Kwh

Residential Gas Usage 56 56 125 53 -6.31 -5.19 -57.56

(‘000) Mcf

Metered Taps – Water (CBPU) 22,251 22,455 22,530 22,620 1.66 0.74 0.40

Metered Taps – Water (SCW & SD) 3,304 3,307 3,310 3,310 0.18 0.08 0.00

(a) Data includes building and non-building.Single Family Building Permits are a total of the figures for three months.All other construction figures are the monthly average for the quarter.CPBU – Cheyenne Board of Public UtilitiesSCW&SD – South Cheyenne Water & Sewer District

13

TABLE 5A

NEW RESIDENTIAL CONSTRUCTION LARAMIE COUNTY

2011 2012

MONTH SFU DUPLEXUNITS

TRI & FOURPLEX

MULTI-FAMILY

TOTALUNITS MONTH SFU DUPLEX

UNITS

TRI & FOURPLEX

MULTI-FAMILY

TOTALUNITS

January 9 0 0 0 9 January 22 0 0 0 22

February 18 0 0 0 18 February 22 0 0 0 22

March 32 0 0 0 32 March 46 0 0 0 46

April 24 0 0 0 24 April 29 0 0 0 29

May 42 0 0 0 42 May 32 0 0 0 32

June 32 0 0 0 32 June 34 0 0 0 34

July 15 0 0 0 15 July 27 0 0 0 27

August 17 0 0 0 17 August 46 0 0 0 46

September 33 0 0 0 33 September 12 0 0 54 66

October 22 0 0 0 22 October

November 21 0 0 0 21 November

December 12 0 0 0 12 December

Year to Date 277 0 0 0 277 Year to Date 270 0 0 54 324

GRAPH 13

SINGLE-FAMILY BUILDING PERMITS, CHEYENNEMonthly Totals

2008 - 2012

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec0

10

20

30

40

50

2012 2011 2010 2009 2008

14

GRAPH 14

COMMERCIAL ELECTRIC POWER SALES, CHEYENNEMonthly Totals

1995 - 2012

0

10

20

30

40

50

60Millions

GRAPH 15

CHEYENNE METERED WATER TAPSMonthly Average

1995 - 2012

Metered Water Taps (CBPU)

18,1

54

18,4

44

18,6

91

18,8

90

19,1

00

19,1

93

19,3

55

19,5

32

19,8

32

20,2

46

20,7

21

21,2

25

21,6

00

21,6

78

21,9

29

22,0

48

22,3

38

22,5

16

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 1217,000

17,500

18,000

18,500

19,000

19,500

20,000

20,500

21,000

21,500

22,000

22,500

15

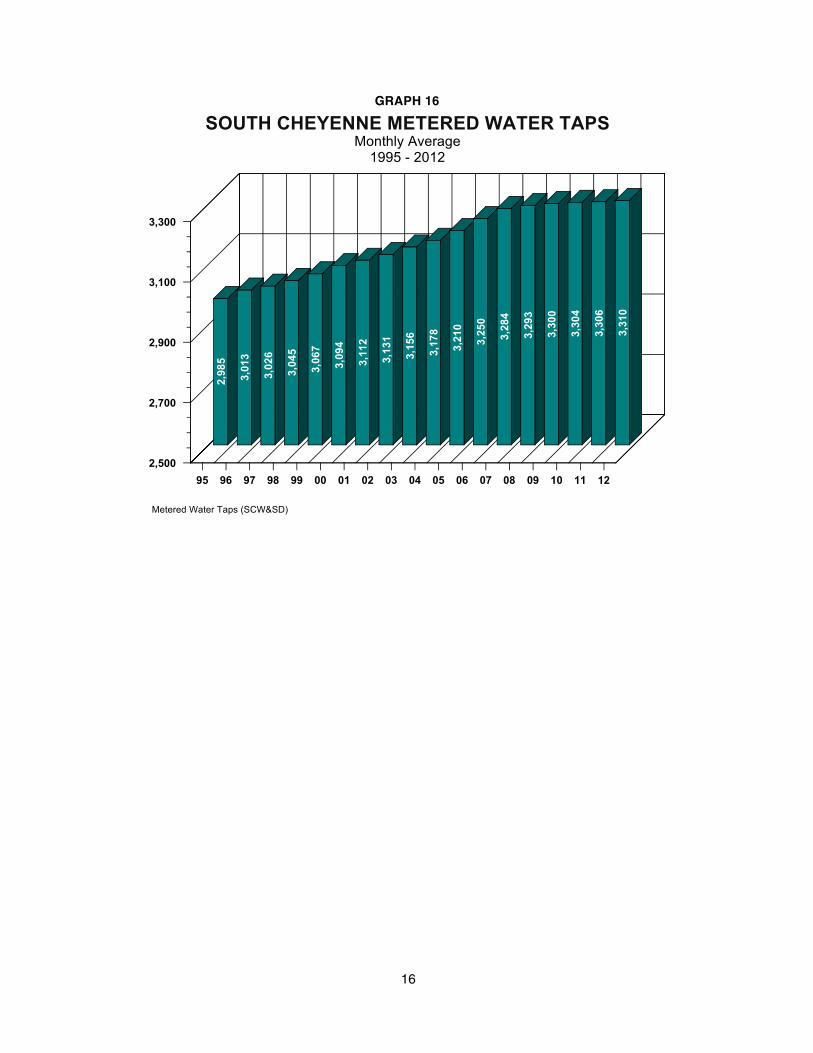

GRAPH 16

SOUTH CHEYENNE METERED WATER TAPSMonthly Average

1995 - 2012

Metered Water Taps (SCW&SD)

2,98

5

3,01

3

3,02

6

3,04

5

3,06

7

3,09

4

3,11

2

3,13

1

3,15

6

3,17

8

3,21

0

3,25

0

3,28

4

3,29

3

3,30

0

3,30

4

3,30

6

3,31

0

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 122,500

2,700

2,900

3,100

3,300

16

Commercial/Industrial ConstructionTable 5 also presents total building permits issued within city limits. Such permits again increased this quarter but at a smaller rate of increase than second quarter 2012, 3.7 percent currently versus 18 percent in second quarter. On an even more positive note, the average monthly dollar valuation of city permits rose by 55.6 percent through the third quarter of this year when compared to all of 2011’s monthly average. This year’s monthly average stood at $10,066,640 through September with 2011’s comparable average at $6,471,434. This increase in commercial construction was driven by the hospital’s new construction projects (parking garage and cancer treatment center) and a permit for the new Menard’s building.

While new commercial construction did very well this quarter within city limits, it paled compared to the 100 million dollar plus value of industrial permits issued in the county over the third quarter of 2012. The latter driven by the permit for construction of Microsoft’s new datacenter. When city and county commercial and industrial construction activities were combined, there were 12 new commercial structures permitted during the third quarter of this year with a total dollar valuation of 130,959,307 dollars. After a long and painful wait, it appears the commercial construction sector has finally shaken off the effects of the Great Recession.

GRAPH 17

TOTAL BUILDING PERMITS, CHEYENNEMonthly Totals

2008 - 2012

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec0

50

100

150

200

250

2012 2011 2010 2009 2008

17

Commercial Property VacanciesTable 6 presents a summary of the number of commercial properties for sale and/or lease in the greater Cheyenne market from first quarter 2010 through the end of third quarter 2012 along with total square footage and vacancy rates. Available properties are categorized by warehousing, retail and office space. Average rental rates are also provided. Retail and warehousing vacancy rates inched up over the third quarter with retail at 8.4% as compared to its second quarter rate of 8.0%.

The warehouse vacancy rate climbed to 9.3% versus its second quarter rate of 8.4% even though the number of available units declined from 46 to 35 over the third quarter.

NOTE: For a complete listing of available commercial properties in the greater Cheyenne area and discussion of changes in the commercial building market over the second quarter of 2012, please go to the Data Center’s homepage (www.wyomingeconomicdata.com) and click on Commercial Property Opportunities.

18

Updated: 09/30/2012

TABLE 6

COMMERCIAL PROPERTY(For Sale & Lease)

PROPERTYTYPE

#PROPERTIES

SQUAREFOOTAGE

AVG.LEASE RATE

MIN./MAX.RATE

VACANCYRATE

FIRST QUARTER 2010Warehouse 45 521,350 $5.23 3.34-10.00 10.9%(FR)

Retail 53 343,180 $10.64 4.61-16.00 8.1%(FR)

Office Space 86 490,256 $14.34 4.80-17.00 21.2%(FR)

SECOND QUARTER 2010Warehouse 54 755,892 $5.57 3.34-13.06 15.1%(FR)

Retail 66 376,641 $11.25 4.61-17.00 9.9%(FR)

Office Space 88 520,529 $12.18 4.80-18.00 26.5%(FR)

THIRD QUARTER 2010Warehouse 51 605,041 $5.99 3.34-13.06 10.3%(FR)

Retail 74 321,469 $10.84 4.61-17.00 7.1%(FR)

Office Space 77 473,770 $11.53 4.00-17.64 20.5%(FR)

FOURTH QUARTER 2010Warehouse 36 476,507 $5.89 3.34-13.06 8.9%(FR)

Retail 68 358,737 $11.66 7.00-16.00 8.0%(FR)

Office Space 72 413,248 $11.99 5.14-17.00 18.7%(FR)

FIRST QUARTER 2011Warehouse 40 500,960 $5.43 3.34-15.60 9.2%(FR)

Retail 71 438,941 $14.91 7.00-27.00 7.9%(FR)

Office Space 78 453,668 $12.39 5.14-19.00 17.7%(FR)

SECOND QUARTER 2011Warehouse 39 485,557 $7.33 3.34-19.00 10.3%(FR)

Retail 69 471,264 $14.83 6.00-27.00 7.9%(FR)

Office Space 78 444,962 $12.34 5.14-17.00 19.1%(FR)

THIRD QUARTER 2011Warehouse 40 395,449 $7.51 3.95-19.00 6.4%(FR)

Retail 65 556,105 $14.38 7.00-23.50 6.7%(FR)

Office Space 73 454,493 $13.02 5.14-22.00 21.3%(FR)

FOURTH QUARTER 2011Warehouse 41 331,361 $7.51 4.50-19.00 5.7%(FR)

Retail 72 598,138 $13.88 7.00-23.50 7.5%(FR)

Office Space 66 391,942 $12.38 5.14-22.00 18.3%(FR)

FIRST QUARTER 2012Warehouse 44 378,210 $7.76 4.29-19.00 7.1%Retail 80 670,323 $14.25 6.00-23.50 9.4%Office Space 68 428,336 $13.31 5.14-22.00 20.5%SECOND QUARTER 2012Warehouse 46 444,917 $7.27 4.25-19.00 8.4%Retail 72 641,817 $13.35 5.00-20.00 8.0%Office Space 63 384,705 $13.48 5.14-22.00 18.5%THIRD QUARTER 2012Warehouse 35 468,066 $7.01 3.20-19.00 9.3%Retail 73 634,151 $13.80 5.00-23.50 8.4%Office Space 62 386,327 $13.26 5.00-22.00 17.6%FR – Final Revision

19

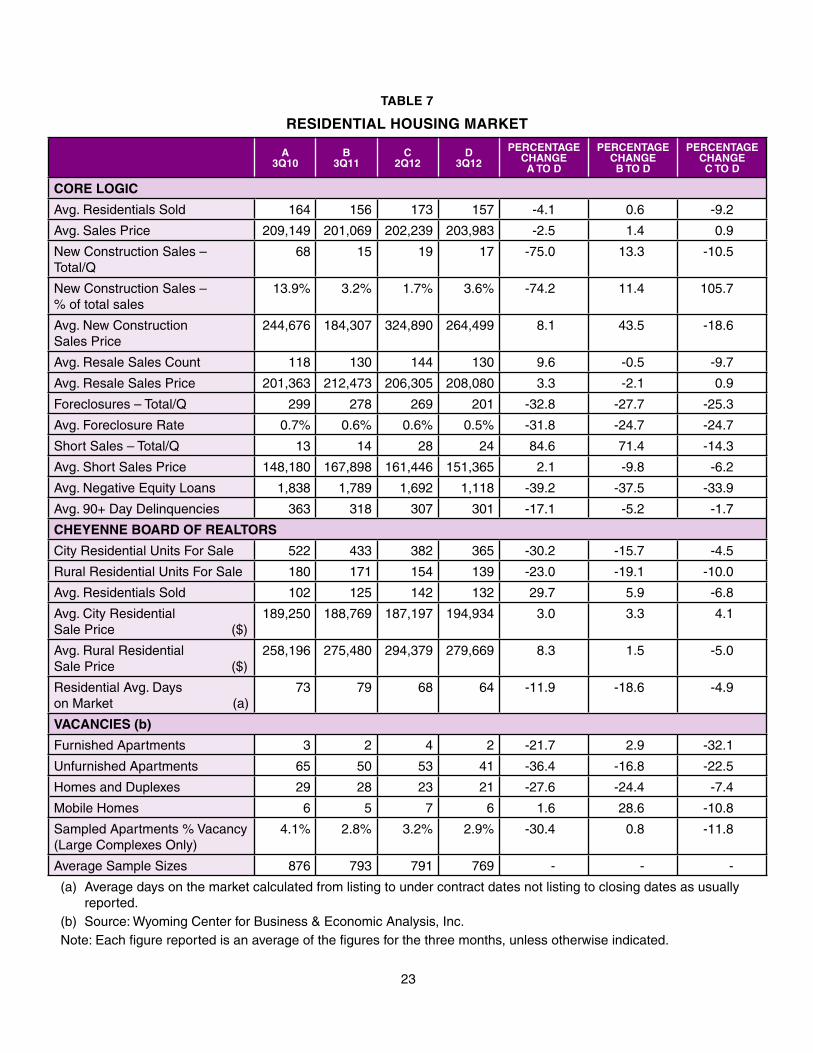

Residential Housing MarketTable 7 below presents statistics for the local residential housing market, both city and rural areas. The first part of the table presents 13 different series measuring residential housing activity throughout Laramie County. These new statistics are from Core Logic (CL) and provide a more comprehensive and in-depth look at the residential housing market than previously available. Below the Core Logic data, the reader will find statistics from the Cheyenne Board of Realtors (CBR) and can compare the two data sets. Core Logic data are derived from a considerably larger sample than CBR statistics and provide a higher degree of reliability and accuracy.

The reader will quickly see the differences between the two sets of data. CL statistics showed the residential housing market expanding at slower rates than CBR rates, but also showed that the absolute number of sales was far larger than those reported by the CBR group. The number of home sales dropped from second quarter 2012 by 9.2 percent and still lagged third quarter 2010 by 4.1 percent. Average sales prices preformed similarly. CL’s new construction series showed strong improvements in this area and supported the data presented earlier in this report concerning new residential construction activity.

CL data reported sharp decreases in the number of foreclosures since 2010 and from one year ago. A solid sign of the improving conditions in the local housing market. The one downside to this improvement was the increase in short sales and drop in sale prices for short sales so far in 2012. Even so, further underlying strength in the housing market could be seen in the 38 percent drop in negative equity loans reported in third quarter 2012 as compared to third quarter 2011 along with a similar decline from third quarter 2010. The number of 90+ Day delinquencies also fell this quarter (-.5.2%) from one year ago and were down 17.1 percent from two years ago.

Due to their small absolute size, the number of REO units was not included in Table 7. There have been only 2 such sales through the first 9 mines of 2012 and the REO rate average only 0.31 percent over this period.

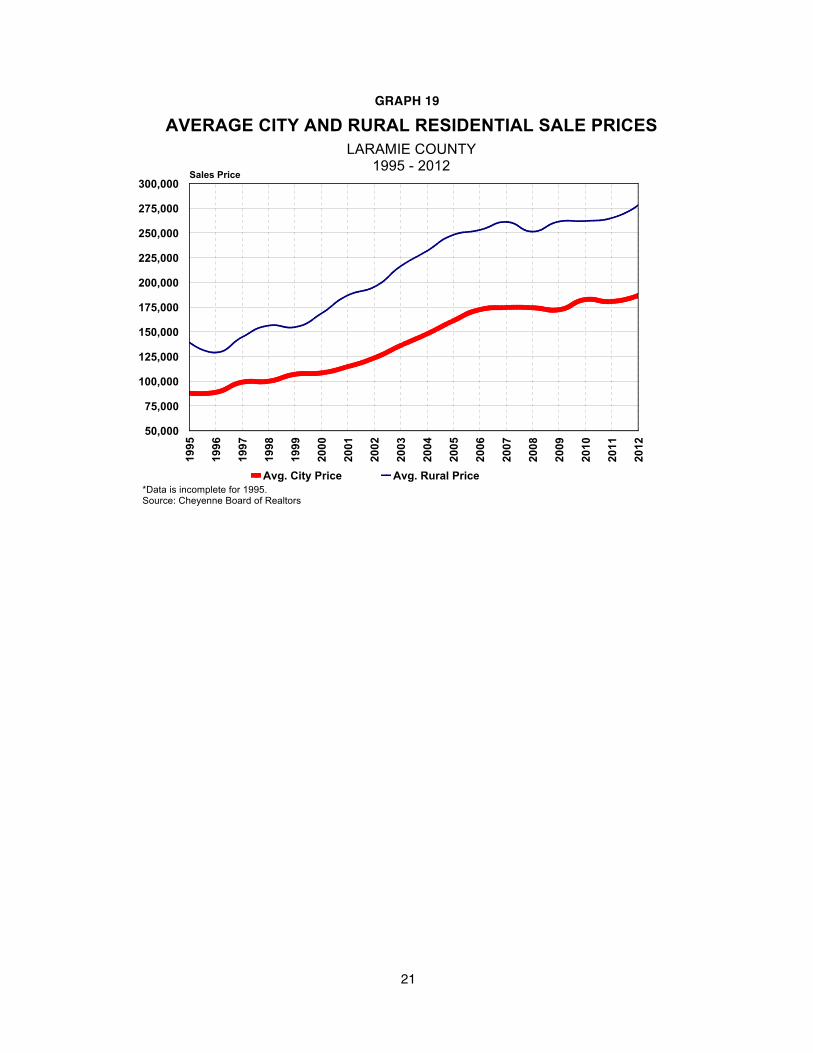

Graph 19 presents the long-term spread between city and rural residential home proces.

GRAPH 18

RESIDENTIAL UNITS SOLDMonthly Totals

2006- 2012

2006 2007 2008 2009 2010 2011 20120

50

100

150

200

250

Condo Units Sold Rural Units Sold City Units Sold Total Units Sold

20

GRAPH 19

AVERAGE CITY AND RURAL RESIDENTIAL SALE PRICESLARAMIE COUNTY

1995 - 2012

*Data is incomplete for 1995.Source: Cheyenne Board of Realtors

199 5

199 6

199 7

199 8

199 9

200 0

200 1

200 2

200 3

200 4

200 5

200 6

200 7

200 8

200 9

201 0

201 1

201 2

50,000

75,000

100,000

125,000

150,000

175,000

200,000

225,000

250,000

275,000

300,000Sales Price

Avg. City Price Avg. Rural Price

21

Apartment VacanciesThe supply of rental units in the local market tightened considerably during third quarter 2012 with the number of unfurnished apartments down 17 percent. Homes and duplexes also fell by 24 percent. The vacancy rate at large apartment complexes averaged 2.9 percent this quarter which was essentially unchanged from one year ago. The new 54-unit apartment complex recently permitted should help ease the apparent tight apartment rental market.

Graphs 20 and 21 below present the above data.

GRAPH 20

UNFURNISHED APARTMENT VACANCIES, CHEYENNEMonthly Totals

1995 - 2012

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 120

20

40

60

80

100

120

GRAPH 21

SAMPLED APARTMENTS - PERCENT VACANT, CHEYENNEMonthly Totals

1995 - 2012

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

0

5

10

15

20

25

22

TABLE 7

RESIDENTIAL HOUSING MARKET

A 3Q10

B 3Q11

C 2Q12

D 3Q12

PERCENTAGE CHANGE A TO D

PERCENTAGE CHANGE B TO D

PERCENTAGE CHANGE C TO D

CORE LOGIC

Avg. Residentials Sold 164 156 173 157 -4.1 0.6 -9.2

Avg. Sales Price 209,149 201,069 202,239 203,983 -2.5 1.4 0.9

New Construction Sales – Total/Q

68 15 19 17 -75.0 13.3 -10.5

New Construction Sales – % of total sales

13.9% 3.2% 1.7% 3.6% -74.2 11.4 105.7

Avg. New Construction Sales Price

244,676 184,307 324,890 264,499 8.1 43.5 -18.6

Avg. Resale Sales Count 118 130 144 130 9.6 -0.5 -9.7

Avg. Resale Sales Price 201,363 212,473 206,305 208,080 3.3 -2.1 0.9

Foreclosures – Total/Q 299 278 269 201 -32.8 -27.7 -25.3

Avg. Foreclosure Rate 0.7% 0.6% 0.6% 0.5% -31.8 -24.7 -24.7

Short Sales – Total/Q 13 14 28 24 84.6 71.4 -14.3

Avg. Short Sales Price 148,180 167,898 161,446 151,365 2.1 -9.8 -6.2

Avg. Negative Equity Loans 1,838 1,789 1,692 1,118 -39.2 -37.5 -33.9

Avg. 90+ Day Delinquencies 363 318 307 301 -17.1 -5.2 -1.7

CHEYENNE BOARD OF REALTORS

City Residential Units For Sale 522 433 382 365 -30.2 -15.7 -4.5

Rural Residential Units For Sale 180 171 154 139 -23.0 -19.1 -10.0

Avg. Residentials Sold 102 125 142 132 29.7 5.9 -6.8

Avg. City Residential Sale Price ($)

189,250 188,769 187,197 194,934 3.0 3.3 4.1

Avg. Rural Residential Sale Price ($)

258,196 275,480 294,379 279,669 8.3 1.5 -5.0

Residential Avg. Days on Market (a)

73 79 68 64 -11.9 -18.6 -4.9

VACANCIES (b)

Furnished Apartments 3 2 4 2 -21.7 2.9 -32.1

Unfurnished Apartments 65 50 53 41 -36.4 -16.8 -22.5

Homes and Duplexes 29 28 23 21 -27.6 -24.4 -7.4

Mobile Homes 6 5 7 6 1.6 28.6 -10.8

Sampled Apartments % Vacancy (Large Complexes Only)

4.1% 2.8% 3.2% 2.9% -30.4 0.8 -11.8

Average Sample Sizes 876 793 791 769 - - -

(a) Average days on the market calculated from listing to under contract dates not listing to closing dates as usually reported.

(b) Source: Wyoming Center for Business & Economic Analysis, Inc.Note: Each figure reported is an average of the figures for the three months, unless otherwise indicated.

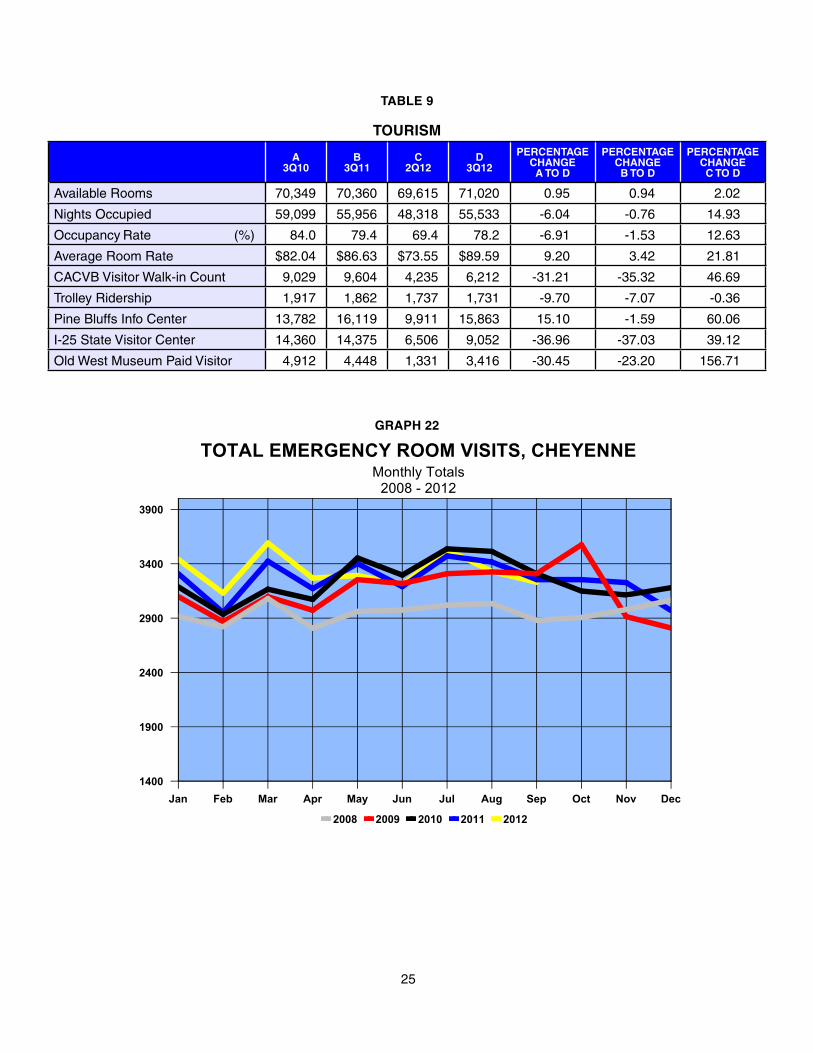

23

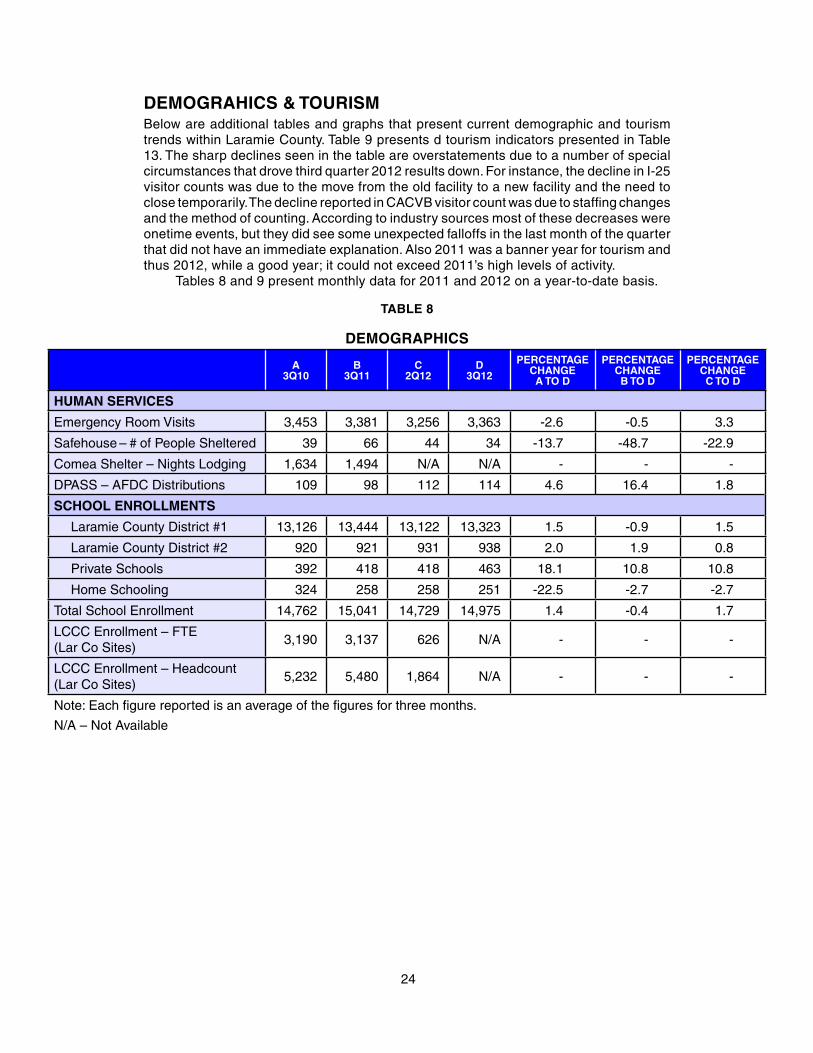

DEMOGRAHICS & TOURISMBelow are additional tables and graphs that present current demographic and tourism trends within Laramie County. Table 9 presents d tourism indicators presented in Table 13. The sharp declines seen in the table are overstatements due to a number of special circumstances that drove third quarter 2012 results down. For instance, the decline in I-25 visitor counts was due to the move from the old facility to a new facility and the need to close temporarily. The decline reported in CACVB visitor count was due to staffing changes and the method of counting. According to industry sources most of these decreases were onetime events, but they did see some unexpected falloffs in the last month of the quarter that did not have an immediate explanation. Also 2011 was a banner year for tourism and thus 2012, while a good year; it could not exceed 2011’s high levels of activity.

Tables 8 and 9 present monthly data for 2011 and 2012 on a year-to-date basis.

TABLE 8

DEMOGRAPHICS

A 3Q10

B 3Q11

C 2Q12

D 3Q12

PERCENTAGECHANGEA TO D

PERCENTAGECHANGEB TO D

PERCENTAGECHANGEC TO D

HUMAN SERVICES

Emergency Room Visits 3,453 3,381 3,256 3,363 -2.6 -0.5 3.3

Safehouse – # of People Sheltered 39 66 44 34 -13.7 -48.7 -22.9

Comea Shelter – Nights Lodging 1,634 1,494 N/A N/A - - -

DPASS – AFDC Distributions 109 98 112 114 4.6 16.4 1.8

SCHOOL ENROLLMENTS

Laramie County District #1 13,126 13,444 13,122 13,323 1.5 -0.9 1.5

Laramie County District #2 920 921 931 938 2.0 1.9 0.8

Private Schools 392 418 418 463 18.1 10.8 10.8

Home Schooling 324 258 258 251 -22.5 -2.7 -2.7

Total School Enrollment 14,762 15,041 14,729 14,975 1.4 -0.4 1.7

LCCC Enrollment – FTE (Lar Co Sites)

3,190 3,137 626 N/A - - -

LCCC Enrollment – Headcount (Lar Co Sites)

5,232 5,480 1,864 N/A - - -

Note: Each figure reported is an average of the figures for three months.

N/A – Not Available

24

TABLE 9

TOURISM

A 3Q10

B 3Q11

C 2Q12

D 3Q12

PERCENTAGECHANGEA TO D

PERCENTAGECHANGEB TO D

PERCENTAGECHANGEC TO D

Available Rooms 70,349 70,360 69,615 71,020 0.95 0.94 2.02

Nights Occupied 59,099 55,956 48,318 55,533 -6.04 -0.76 14.93

Occupancy Rate (%) 84.0 79.4 69.4 78.2 -6.91 -1.53 12.63

Average Room Rate $82.04 $86.63 $73.55 $89.59 9.20 3.42 21.81

CACVB Visitor Walk-in Count 9,029 9,604 4,235 6,212 -31.21 -35.32 46.69

Trolley Ridership 1,917 1,862 1,737 1,731 -9.70 -7.07 -0.36

Pine Bluffs Info Center 13,782 16,119 9,911 15,863 15.10 -1.59 60.06

I-25 State Visitor Center 14,360 14,375 6,506 9,052 -36.96 -37.03 39.12

Old West Museum Paid Visitor 4,912 4,448 1,331 3,416 -30.45 -23.20 156.71

GRAPH 22

TOTAL EMERGENCY ROOM VISITS, CHEYENNEMonthly Totals

2008 - 2012

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec1400

1900

2400

2900

3400

3900

2008 2009 2010 2011 2012

25

GRAPH 23

LARAMIE COUNTY SCHOOLSMonthly Totals

Thousands 2008 - 2012

15

10

5

0Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2012 2011 2010 2009 2008

26

TAB

LE

10

JAN

FE

BM

AR

AP

RM

AY

JUN

JUL

AU

GS

EP

OC

TN

OV

DE

CA

VG

YE

AR

EM

PL

OY

ME

NT

*

Tota

l Civ

ilian

Lab

or

For

ce (

LAU

S)

44,5

9744

,699

45,3

5845

,205

44,6

9544

,899

45,6

4145

,546

44,4

1944

,994

45,4

3145

,287

45,0

6420

11

45,4

9046

,110

45,7

0745

,041

45,1

5745

,974

46,2

7445

,843

44,5

8245

,575

2012

Tota

l Em

ploy

men

t (L

AU

S)

40,9

2941

,281

42,0

5742

,326

41,8

8141

,948

42,7

2942

,585

41,6

4442

,223

42,6

5042

,338

42,0

4920

11

42,1

5843

,017

42,6

6242

,313

42,6

0443

,071

43,4

5343

,186

42,2

5742

,747

2012

Tota

l Em

ploy

men

t (C

ES

)42

,600

42,7

0043

,300

44,1

0044

,300

44,9

0044

,900

45,0

0044

,800

45,1

0045

,100

44,9

0044

,308

2011

44,2

0044

,600

44,9

0044

,700

45,7

0046

,400

46,3

0046

,300

45,7

0045

,422

2012

Tota

l Une

mpl

oym

ent

(LA

US

)3,

668

3,41

83,

301

2,87

92,

814

2,95

12,

912

2,96

12,

775

2,77

12,

781

2,94

93,

015

2011

3,33

23,

093

3,04

52,

728

2,55

32,

903

2,82

12,

708

2,32

52,

834

2012

Une

mpl

oym

ent R

ate

(LA

US

)8.

2%7.

6%7.

3%6.

4%6.

3%6.

6%6.

4%6.

5%6.

2%6.

2%6.

1%6.

5%6.

7%20

11

7.3%

6.7%

6.7%

6.1%

5.7%

6.3%

6.1%

5.9%

5.2%

6.2%

2012

Initi

al U

nem

ploy

men

t C

laim

s18

897

9681

6662

8373

6381

8514

093

2011

147

8479

5863

7478

8069

8120

12

Hel

p W

ante

d A

ds52

5560

7158

7364

8879

7361

5065

2011

4648

6567

8072

6484

6265

2012

GE

NE

RA

L B

US

INE

SS

AC

TIV

ITY

Aut

o R

egis

trat

ions

2,45

62,

399

3,39

13,

051

3,14

03,

584

2,83

64,

081

3,97

43,

752

2,86

32,

650

3,18

120

11

2,41

72,

737

3,37

13,

244

3,43

63,

451

3,29

73,

787

2,87

93,

180

2012

Enp

lane

men

ts –

C

hey.

Air

port

1,78

91,

397

1,78

31,

787

2,00

32,

139

2,28

12,

373

1,98

21,

801

1,75

61,

685

1,89

820

11

1,55

71,

467

1,68

996

61,

079

1,01

71,

208

1,10

21,

148

1,24

820

12

Ret

ail S

ales

($)

99,2

54,1

0068

,616

,400

78,5

95,6

0063

,720

,600

86,3

74,3

0094

,370

,000

71,5

52,8

0010

3,63

3,30

010

1,88

6,20

092

,750

,000

102,

580,

600

90,8

67,6

0087

,850

,125

2011

91,3

09,2

0098

,401

,800

76,6

18,5

0084

,056

,000

96,1

24,6

0088

,808

,200

97,3

03,6

0010

9,45

3,30

095

,927

,100

93,1

11,3

6720

12

Ban

krup

tcie

s17

1532

3133

1920

1927

2212

1021

2011

515

2329

2112

2723

2019

2012

* La

bor

stat

istic

s ar

e co

mpi

led

from

two

maj

or s

ourc

es:

Cur

rent

Pop

ulat

ion

Sur

vey

(CP

S)

and

Cur

rent

Em

ploy

men

t Sta

tistic

s (C

ES

). L

ocal

Are

a U

nem

ploy

men

t Sta

tistic

s (L

AU

S)

are

estim

ated

bas

ed o

n C

PS

dat

a w

hich

is c

olle

cted

thro

ugh

hous

ehol

d su

rvey

s w

hich

indi

vidu

als

are

repo

rted

as

em

ploy

ed, u

nem

ploy

ed o

r no

t in

the

labo

r fo

rce.

Thi

s da

ta in

clud

es e

mpl

oym

ent f

or b

oth

agric

ultu

re a

nd n

onag

ricul

tura

l ind

ustr

ies.

CE

S d

ata

is

base

d on

est

ablis

hmen

t rec

ords

com

pile

d th

roug

h m

onth

ly s

urve

ys o

f non

farm

em

ploy

ers.

Indi

vidu

als

who

wor

ked

in m

ore

than

one

est

ablis

hmen

t, fu

ll or

par

t-tim

e, a

re c

ount

ed e

ach

time

thei

r na

mes

app

ear

on p

ayro

lls.

27

TAB

LE

11

JAN

FE

BM

AR

AP

RM

AY

JUN

JUL

AU

GS

EP

OC

TN

OV

DE

CA

VG

YE

AR

HO

US

ING

Tota

l Res

iden

tial

Uni

ts fo

r S

ale

646

624

639

744

688

715

726

665

634

608

582

492

647

2011

547

537

551

596

618

611

583

586

552

576

2012

Tota

l Res

iden

tial U

nits

Sol

d74

7312

813

012

511

913

811

612

213

994

9011

220

11

7591

120

147

136

143

133

138

126

123

2012

Ave

rage

Res

iden

tial S

old

Pric

e (c

ity)

167,

186

178,

630

181,

633

164,

487

171,

879

191,

802

179,

702

200,

592

186,

013

185,

008

184,

113

177,

071

180,

676

2011

157,

916

191,

122

185,

535

181,

817

184,

478

195,

295

184,

490

197,

053

203,

258

186,

774

2012

Fur

nish

ed A

part

men

ts2

41

22

33

23

35

53

2011

34

26

33

22

33

2012

Unf

urni

shed

Apa

rtm

ents

7365

4445

5154

5347

5048

5857

5420

11

5852

5457

4955

4537

4350

2012

Hom

es &

Dup

lexe

s36

2320

2014

1922

2733

3532

3026

2011

3122

2221

2423

1923

2023

2012

Mob

ile H

omes

57

77

55

74

45

46

520

11

57

67

59

75

66

2012

Sam

pled

Apa

rtm

ents

%

Vac

ant

4.6%

5 .1%

4.2%

3.3%

2.9%

2.8%

2.9%

2.9%

2.4%

3.9%

3.5%

3.8%

3.5%

2011

3.8%

3.5%

2.9%

3.9%

3.3%

2.5%

2.6%

3.5%

2.5%

3.2%

2012

CO

NS

TR

UC

TIO

N

Sin

gle

Fam

ily B

ldg.

Per

mits

(C

heye

nne)

713

2216

3118

1011

2515

1712

1620

11

1420

3318

2120

1841

821

2012

Sin

gle

Fam

ily B

ldg.

Per

mits

(L

aram

ie C

ount

y)2

510

811

145

68

74

07

2011

82

1311

1114

95

49

2012

Sep

tic P

erm

its –

Rur

al8

714

811

277

2016

619

1213

2011

78

812

1217

1516

1312

2012

Tota

l Bui

ldin

g P

erm

its

(Che

yenn

e)90

115

161

145

149

146

126

158

209

197

166

225

157

2011

128

113

192

187

189

187

166

210

135

167

2012

Val

ue o

f Aut

horiz

ed C

onst

($

000)

(C

heye

nne)

2,15

73,

760

15,3

514,

713

7,06

215

,032

5,20

137

98,

041

8,50

73,

612

3,84

16,

471

2011

3,47

05,

419

8,34

56,

009

11,5

676,

942

6,02

110

,471

32,3

5610

,067

2012

Res

iden

tial (

$000

) (C

heye

nne)

1,31

82,

330

4,02

02,

876

4,69

03,

611

1,41

71,

766

4,06

52,

498

2,24

02,

275

2,75

920

11

1,99

62,

903

4,61

12,

470

3,26

54,

024

2,96

16,

525

1,12

83,

320

2012

Not

e: D

ata

is n

ot s

easo

nally

adj

uste

d.

Sin

gle

fam

ily b

uild

ing

perm

its fo

r C

heye

nne

incl

udes

new

res

iden

ces

and

new

tow

nhou

ses.

28

TAB

LE

12

JAN

FE

BM

AR

AP

RM

AY

JUN

JUL

AU

GS

EP

OC

TN

OV

DE

CA

VG

YE

AR

UT

ILIT

IES

Com

mer

cial

Ele

ctric

Pow

er

(Kw

h) (

‘0,0

00)

5,10

34,

889

4,94

24,

867

4,43

84,

939

5,12

85,

255

5,22

25,

020

5,11

45,

178

5,00

820

11

5,10

04,

992

5,12

85,

155

5,13

05,

053

5,45

74,

504

4,58

65,

012

2012

Res

iden

tial G

as U

sage

(M

cf)

(‘000

)4,

155

3,98

13,

283

2,49

22,

008

1,21

359

750

657

093

32,

496

3,48

72,

143

2011

3,68

33,

652

3,45

91,

748

1,22

576

452

550

955

31,

791

2012

Met

ered

Wat

er T

aps

(CB

PU

)22

,219

22,1

8321

,987

22,2

4722

,336

22,3

8722

,392

22,4

8522

,488

22,4

9122

,419

22,4

2022

,338

2011

22,3

8522

,400

22,4

0522

,468

22,5

5122

,571

22,5

8722

,680

22,5

9422

,516

2012

Met

ered

Wat

er T

aps

(S

CW

& S

D)

3,30

53,

305

3,30

53,

305

3,30

53,

305

3,30

73,

307

3,30

83,

308

3,30

83,

308

3,30

620

11

3,30

83,

309

3,31

03,

310

3,31

03,

310

3,31

03,

310

3,31

03,

310

2012

HU

MA

N S

ER

VIC

ES

Tota

l Em

erge

ncy

R

oom

Vis

its3,

309

2,95

23,

424

3,17

13,

402

3,19

03,

472

3,41

73,

254

3,25

43,

227

2,97

03,

254

2011

3,44

13,

130

3,59

13,

268

3,29

23,

207

3,53

13,

329

3,23

03,

335

2012

Saf

ehou

se –

Num

ber

of

Peo

ple

She

ltere

d36

2521

2735

4052

7768

5339

2842

2011

3127

2844

4839

2244

3535

2012

Com

ea S

helte

r –

To

tal N

ight

s Lo

dgin

g1,

205

1,11

01,

382

1,27

11,

527

1,50

5N

/AN

/A1,

494

1,31

5N

/AN

/A1,

351

2011

2,00

11,

540

1,67

2N

/AN

/AN

/AN

/AN

/AN

/A1,

738

2012

SC

HO

OL

EN

RO

LL

ME

NT

S

Lara

mie

Cou

nty

Dis

tric

t #1

13,1

2613

,126

13,1

2612

,785

12,7

85-

-13

,444

13,4

4413

,444

13,3

6013

,360

13,2

0020

11

13,3

6013

,360

13,1

6513

,122

13,1

22-

-13

,336

13,3

0913

,253

2012

Lara

mie

Cou

nty

Dis

tric

t #2

937

928

929

928

928

--

926

915

921

921

930

926

2011

930

925

930

931

931

--

938

938

932

2012

Tota

l Sch

ool E

nrol

lmen

t14

,779

14,7

7014

,771

14,4

2914

,429

--

15,0

4615

,035

15,0

4114

,957

14,9

6614

,822

2011

14,9

6614

,961

14,7

7114

,729

14,7

29-

-14

,988

14,9

6114

,872

2012

LCC

C E

nrol

lmen

t –

FT

E (

Lar

Co

Site

s)34

15.5

934

15.5

934

15.5

934

15.5

934

15.5

971

6.75

716.

7531

36.6

831

36.6

831

36.6

831

36.6

831

36.6

82,

849.

5720

11

3240

.50

3240

.50

3240

.50

3240

.50

3240

.50

626.

1662

6.16

N/A

N/A

2,49

3.55

2012

LCC

C E

nrol

lmen

t –

Hea

dcou

nt (

Lar

Co

Site

s)

5,96

25,

962

5,96

25,

962

5,96

21,

964

1,96

45,

480

5,48

05,

480

5,48

05,

480

5,09

520

11

5,69

45,

694

5,69

45,

694

5,69

41,

864

1,86

4N

/AN

/A4,

600

2012

N/A

– N

ot A

vaila

ble

Not

e: D

ata

is n

ot s

easo

nally

adj

uste

d.

29

TAB

LE

13

JAN

FE

BM

AR

AP

RM

AY

JUN

JUL

AU

GS

EP

OC

TN

OV

DE

CA

VG

YE

AR

TAX

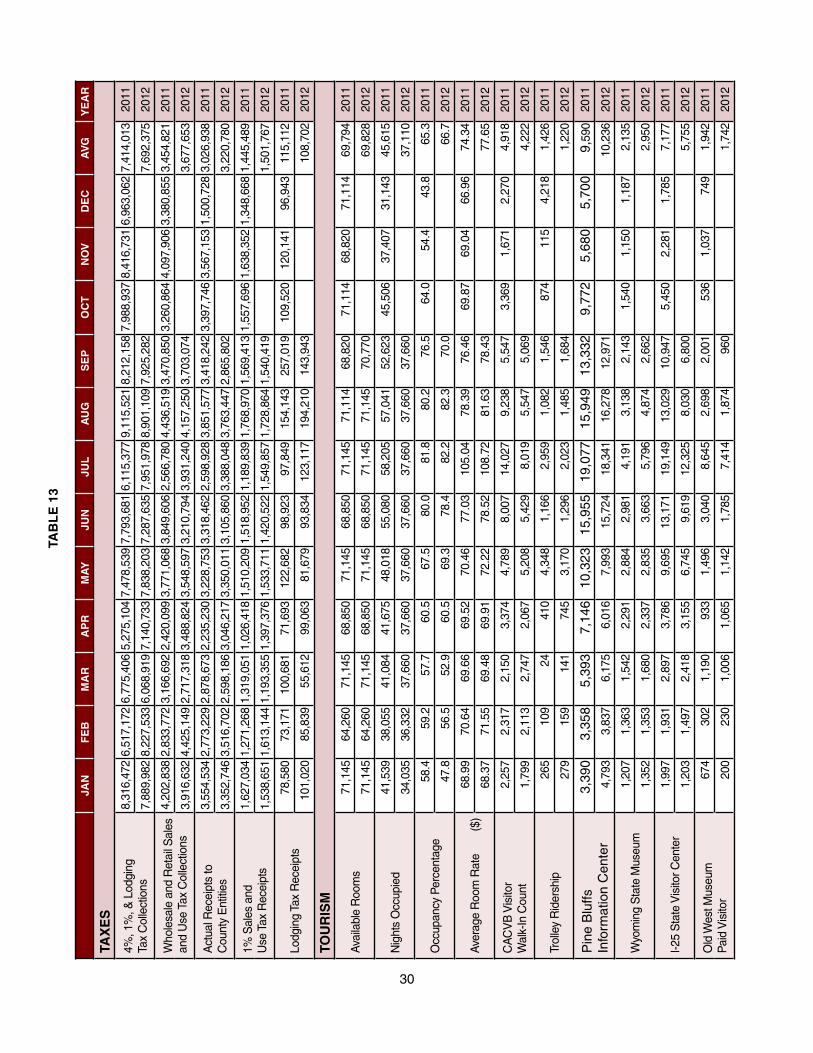

ES

4%, 1

%, &

Lod

ging

Ta

x C

olle

ctio

ns8,

316,

472

6,51

7,17

2 6,

775,

406

5,27

5,10

4 7,

478,

539

7,79

3,68

1 6,

115,

377

9,11

5,52

1 8,

212,

158

7,98

8,93

7 8,

416,

731

6,96

3,06

2 7,

414,

013

2011

7,88

9,98

2 8,

227,

533

6,06

8,91

9 7,

140,

733

7,83

8,20

3 7,

287,

635

7,95

1,97

8 8,

901,

109

7,92

5,28

2 7,

692,

375

2012

Who

lesa

le a

nd R

etai

l Sal

es

and

Use

Tax

Col

lect

ions

4,20

2,83

8 2,

833,

772

3,16

6,69

2 2,

420,

099

3,77

1,06

8 3,

849,

606

2,56

6,78

0 4,

436,

519

3,47

0,85

0 3,

260,

864

4,09

7,90

6 3,

380,

855

3,45

4,82

1 20

11

3,91

6,63

2 4,

425,

149

2,71

7,31

8 3,

488,

824

3,54

8,59

7 3,

210,

794

3,93

1,24

0 4,

157,

250

3,70

3,07

4 3,

677,

653

2012

Act

ual R

ecei

pts

to

Cou

nty

Ent

ities

3,55

4,53

4 2,

773,

229

2,87

8,67

3 2,

235,

230

3,22

8,75

3 3,

318,

462

2,59

8,92

8 3,

851,

577

3,41

8,24

2 3,

397,

746

3,56

7,15

3 1,

500,

728

3,02

6,93

8 20

11

3,35

2,74

6 3,

516,

702

2,59

8,18

6 3,

046,

217

3,35

0,01

1 3,

105,

860

3,38

8,04

8 3,

763,

447

2,86

5,80

2 3,

220,

780

2012

1% S

ales

and

U

se T

ax R

ecei

pts

1,62

7,03

4 1,

271,

268

1,31

9,05

1 1,

026,

418

1,51

0,20

9 1,

518,

952

1,18

9,83

9 1,

768,

970

1,56

9,41

3 1,

557,

696

1,63

8,35

2 1,

348,

668

1,44

5,48

9 20

11

1,53

8,65

1 1,

613,

144

1,19

3,35

5 1,

397,

376

1,53

3,71

1 1,

420,

522

1,54

9,85

7 1,

728,

864

1,54

0,41

9 1,

501,

767

2012

Lodg

ing

Tax

Rec

eipt

s78

,580

73

,171

10

0,68

1 71

,693

12

2,68

2 98

,923

97

,849

15

4,14

3 25

7,01

9 10

9,52

0 12

0,14

1 96

,943

11

5,11

2 20

11

101,

020

85,8

39

55,6

12

99,0

63

81,6

79

93,8

34

123,

117

194,

210

143,

943

108,

702

2012

TOU

RIS

M

Ava

ilabl

e R

oom

s71

,145

64,2

6071

,145

68,8

5071

,145

68,8

5071

,145

71,1

1468

,820

71,1

1468

,820

71,1

1469

,794

20

11

71,1

4564

,260

71,1

4568

,850

71,1

4568

,850

71,1

4571

,145

70,7

7069

,828

20

12

Nig

hts

Occ

upie

d41

,539

38,0

5541

,084

41,6

7548

,018

55,0

8058

,205

57,0

4152

,623

45,5

0637

,407

31,1

4345

,615

20

11

34,0

3536

,332

37,6

6037

,660

37,6

6037

,660

37,6

6037

,660

37,6

6037

,110

20

12

Occ

upan

cy P

erce

ntag

e58

.459

.257

.760

.567

.580

.081

.880

.276

.564

.054

.443

.865

.3

2011

47.8

56.5

52.9

60.5

69.3

78.4

82.2

82.3

70.0

66.7

20

12

Ave

rage

Roo

m R

ate

($

)68

.99

70.6

469

.66

69.5

270

.46

77.0

310

5.04

78.3

976

.46

69.8

769

.04

66.9

674

.34

2011

68.3

771

.55

69.4

869

.91

72.2

278

.52

108.

7281

.63

78.4

377

.65

2012

CA

CV

B V

isito

r W

alk-

In C

ount

2,25

72,

317

2,15

03,

374

4,78

98,

007

14,0

279,

238

5,54

73,

369

1,67

12,

270

4,91

8 20

11

1,79

92,

113

2,74

72,

067

5,20

85,

429

8,01

95,

547

5,06

94,

222

2012

Trol

ley

Rid

ersh

ip26

510

924

410

4,34

81,

166

2,95

91,

082

1,54

687

411

54,

218

1,42

6 20

11

279

159

141

745

3,17

01,

296

2,02

31,

485

1,68

41,

220

2012

Pin

e B

luffs

In

form

atio

n C

ente

r3,

390

3,35

85,

393

7,14

610

,323

15,9

5519

,077

15,9

4913

,332

9,77

25,

680

5,70

09,

590

2011

4,79

33,

837

6,17

56,

016

7,99

315

,724

18,3

4116

,278

12,9

7110

,236

20

12

Wyo

min

g S

tate

Mus

eum

1,20

71,

363

1,54

22,

291

2,88

42,

981

4,19

13,

138

2,14

31,

540

1,15

01,

187

2,13

5 20

11

1,35

21,

353

1,68

02,

337

2,83

53,

663

5,79

64,

874

2,66

22,

950

2012

I-25

Sta

te V

isito

r Cen

ter

1,99

71,

931

2,89

73,

786

9,69

513

,171

19,1

4913

,029

10,9

475,

450

2,28

11,

785

7,17

7 20

11

1,20

31,

497

2,41

83,

155

6,74

59,

619

12,3

258,

030

6,80

05,

755

2012

Old

Wes

t Mus

eum

P

aid

Vis

itor

674

302

1,19

093

31,

496

3,04

08,

645

2,69

82,

001

536

1,03

774

91,

942

2011

200

230

1,00

61,

065

1,14

21,

785

7,41

41,

874

960

1,74

2 20

12

30

CHEYENNE/LARAMIE COUNTY PROFILEITEMS MOST RECENT PERIOD PREVIOUS PERIOD % CHANGE

IN VALUEYEAR VALUE YEAR VALUEDemographyTotal Population – Cheyenne¹ 2011 58,640 2010 59,466 -1.39%

Total Population – Laramie County 2011 90,394 2010 91,738 -1.47%

Total Male Population 2011 45,020 2010 45,875 -1.86%

Total Female Population 2011 45,374 2010 45,863 -1.07%

% of Population – Under 20 Years Old 2011 27.2% 2010 27.4% -0.73%

% of Population – 65 Years & Older 2011 12.3% 2010 12.5% -1.60%

Median Age 2011 37.1 2010 37.0 0.27%

% of Population – White Alone (Non-Hispanic) 2011 87.2% 2010 88.5% -1.47%

% of Population – Native American Alone 2011 1.1% 2010 1.0% 10.00%

% of Population – Hispanic or Latino 2011 12.9% 2010 13.1% -1.53%

Households – County 2011 36,566 2010 37,576 -2.69%

Average Household Size – County 2011 2.4 2010 2.4 0.00%

Households – City 2011 24,693 2010 25,557 -3.38%

% of Households (HH) Headed by Married Couples 2011 50.9% 2010 43.1% 18.10%

% of HH Headed by Single Female (w/own children <18 yrs.) 2011 10.4% 2010 7.7% 35.06%

Weather & GeographyTotal Area (sq. miles)¹ 2000 2,688 - -

Total Area (sq. miles)¹¹ – Cheyenne 2011 25.48 2010 25.15 1.31%

Water Area (sq. miles) 2000 1.6 - -

Mean Elevation (ft.) 2000 6,100 - -

Normal Mean Temperature (F) – Cheyenne2 1949-06 45.9 1971-00 44.9 2.23%

Average Annual Precipitation (inches) – Cheyenne2 1949-06 14.6 1971-00 15.5 -5.50%

Average Wind Speed (mph) 1996-06 12.4 1992-02 12.6 -1.59%

Crime & Law EnforcementCrimes3 2011 2,784 2010 2,972 -6.33%

Crimes per 10,000 Persons 2011 308.0 2010 324.0 -4.93%

Homicides per 10,000 Persons 2011 0.2 2010 0.0

Rapes per 10,000 Persons 2011 4.3 2010 4.9 -11.44%

Robberies per 10,000 Persons 2011 3.3 2010 2.7 21.44%

Aggravated Assaults per 10,000 Persons 2011 16.9 2010 14.1 19.70%

Burglaries per 10,000 Persons 2011 43.6 2010 40.0 8.85%

Larcenies & Thefts per 10,000 Persons 2011 228.8 2010 277.2 -17.47%

Motor Vehicle Thefts per 10,000 Persons 2011 10.8 2010 14.1 -23.33%

Education% of Pop. (25 yrs. & older) with High School Diploma¹ 2011 92.2% 2010 93.8% -1.71%

% of Pop. (25 yrs. & older) with Bachelor’s Degree 2011 24.4% 2010 22.6% 7.96%

Pupil -Teacher Ratio in LCSD #14 2006-07 10.38 2005-06 10.36 0.19%

Pupil -Teacher Ratio in LCSD #2 2006-07 7.47 2005-06 6.53 14.40%

Expenditures Per Pupil in LCSD #1 2010-11 $15,170 2009-10 $14,585 4.01%

Expenditures Per Pupil in LCSD #2 2010-11 $20,462 2009-10 $18,930 8.09%

LCSD #1 Enrollment 2010-11 13,370 2009-10 13,171 1.51%

LCSD #2 Enrollment 2010-11 916 2009-10 925 -0.97%

Total School Enrollments Laramie County 2010-11 14,966 2009-10 14,776 1.29%

% of Students in Private Schools 2010-11 2.79% 2009-10 2.65% 5.28%

% of Students Home-Schooled 2010-11 1.72% 2009-10 2.19% -21.38%

ACT Average Composite Score (range 1-36) LCSD #1 2010-11 20.2 2009-10 19.1 5.76%

ACT Average Composite Score (range 1-36) LCSD #2 2010-11 20.5 2009-10 19.6 4.59%

31

ITEMS MOST RECENT PERIOD PREVIOUS PERIOD % CHANGEIN VALUEYEAR VALUE YEAR VALUE

LCSD #1 Graduation Rate5 2010-11 75.72% 2009-10 76.61% -1.16%

LCSD #2 Graduation Rate 2010-11 89.29% 2009-10 83.05% 7.51%

Average Student Age at LCCC (Fall Semester)7 2011 26 2010 27 -3.70%

Median Student Age at LCCC (Fall Semester) 2011 22.36 - -

Full-time Equivalent (FTE) Enrollment at LCCC (Fall Semester) 2011 3,137 2010 3,190 -1.66%

3 – Year Graduation Rate at LCCC 2010 17.6% 2009 25.3% -30.55%

3 – Year Rate of Transfer from LCCC 2010 28.4% 2009 24.9% 14.18%

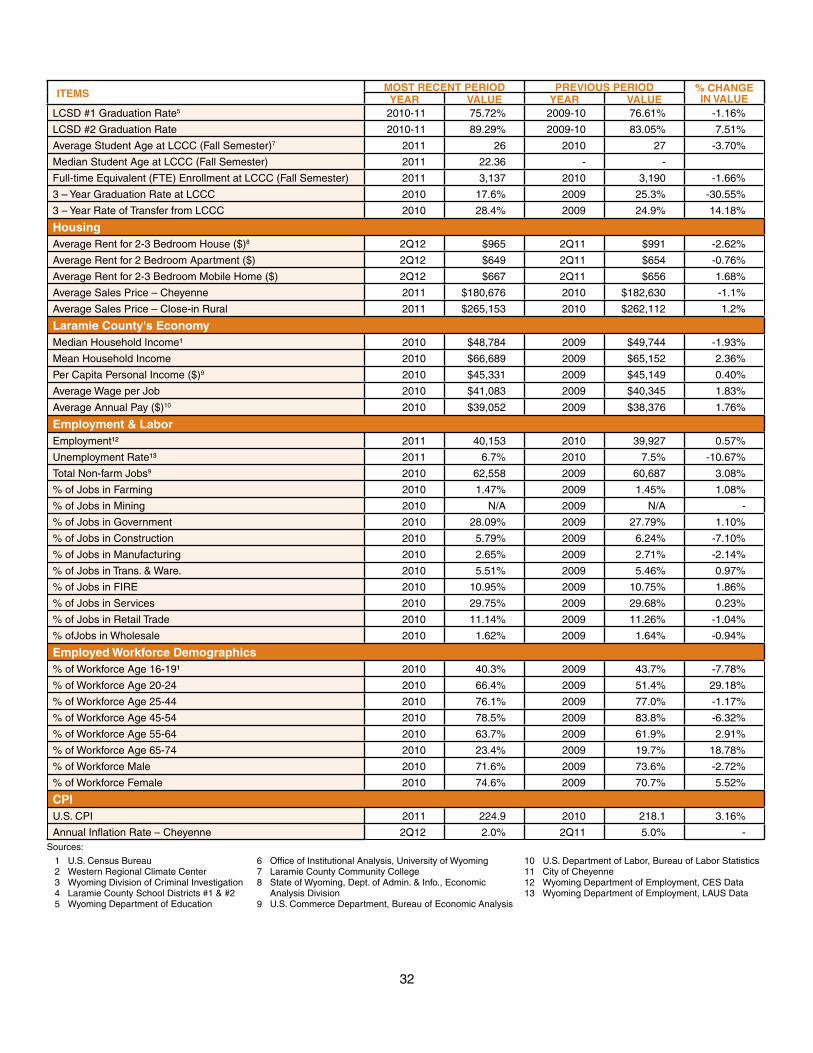

HousingAverage Rent for 2-3 Bedroom House ($)8 2Q12 $965 2Q11 $991 -2.62%

Average Rent for 2 Bedroom Apartment ($) 2Q12 $649 2Q11 $654 -0.76%

Average Rent for 2-3 Bedroom Mobile Home ($) 2Q12 $667 2Q11 $656 1.68%

Average Sales Price – Cheyenne 2011 $180,676 2010 $182,630 -1.1%

Average Sales Price – Close-in Rural 2011 $265,153 2010 $262,112 1.2%

Laramie County's EconomyMedian Household Income¹ 2010 $48,784 2009 $49,744 -1.93%

Mean Household Income 2010 $66,689 2009 $65,152 2.36%

Per Capita Personal Income ($)9 2010 $45,331 2009 $45,149 0.40%

Average Wage per Job 2010 $41,083 2009 $40,345 1.83%

Average Annual Pay ($)10 2010 $39,052 2009 $38,376 1.76%

Employment & LaborEmployment¹² 2011 40,153 2010 39,927 0.57%

Unemployment Rate¹³ 2011 6.7% 2010 7.5% -10.67%

Total Non-farm Jobs9 2010 62,558 2009 60,687 3.08%

% of Jobs in Farming 2010 1.47% 2009 1.45% 1.08%

% of Jobs in Mining 2010 N/A 2009 N/A -

% of Jobs in Government 2010 28.09% 2009 27.79% 1.10%

% of Jobs in Construction 2010 5.79% 2009 6.24% -7.10%

% of Jobs in Manufacturing 2010 2.65% 2009 2.71% -2.14%

% of Jobs in Trans. & Ware. 2010 5.51% 2009 5.46% 0.97%

% of Jobs in FIRE 2010 10.95% 2009 10.75% 1.86%

% of Jobs in Services 2010 29.75% 2009 29.68% 0.23%

% of Jobs in Retail Trade 2010 11.14% 2009 11.26% -1.04%

% ofJobs in Wholesale 2010 1.62% 2009 1.64% -0.94%

Employed Workforce Demographics% of Workforce Age 16-19¹ 2010 40.3% 2009 43.7% -7.78%

% of Workforce Age 20-24 2010 66.4% 2009 51.4% 29.18%

% of Workforce Age 25-44 2010 76.1% 2009 77.0% -1.17%

% of Workforce Age 45-54 2010 78.5% 2009 83.8% -6.32%

% of Workforce Age 55-64 2010 63.7% 2009 61.9% 2.91%

% of Workforce Age 65-74 2010 23.4% 2009 19.7% 18.78%

% of Workforce Male 2010 71.6% 2009 73.6% -2.72%

% of Workforce Female 2010 74.6% 2009 70.7% 5.52%

CPIU.S. CPI 2011 224.9 2010 218.1 3.16%

Annual Inflation Rate – Cheyenne 2Q12 2.0% 2Q11 5.0% -Sources:

1 U.S. Census Bureau 2 Western Regional Climate Center 3 Wyoming Division of Criminal Investigation 4 Laramie County School Districts #1 & #2 5 Wyoming Department of Education

6 7 8

9

Office of Institutional Analysis, University of WyomingLaramie County Community CollegeState of Wyoming, Dept. of Admin. & Info., Economic Analysis DivisionU.S. Commerce Department, Bureau of Economic Analysis

10 11 12 13

U.S. Department of Labor, Bureau of Labor Statistics City of CheyenneWyoming Department of Employment, CES DataWyoming Department of Employment, LAUS Data

32

DATA SOURCES

1. Automobile Registrations: Laramie County Auto Titles Bureau

2. Construction, Permits, Valuation, Residential: City of Cheyenne Building Permits Agency Laramie County Planning & Development Office

3. Employment: Wyoming Department of Workforce Services

4. Help-Wanted Advertisements: Center for Economic and Business Data

5. Sales and Use Tax Collections: Wyoming Department of Revenue and Taxation Department of Administration & Information – DA

6. Utilities, Electrical, and Natural Gas: Cheyenne Light, Fuel & Power

7. Water Usage – Metered Taps: Board of Public Utilities South Cheyenne Sewer & Water District

8. Banking Data: Cheyenne Area Credit Unions (9) Cheyenne Area Banks (5)

9. Enplanements: Cheyenne Airport Board

10. Housing: Center for Economic and Business Data Cheyenne Board of Realtors

11. Human Services: Cheyenne Police Department United Medical Center Safehouse Comea Shelter Department of Family Services School Districts No. 1 and No. 2 Private Schools (5)

12. Tourism: Visit Cheyenne

13. Bankruptcies: U.S. Clerk of Bankruptcy Court

Wyoming Center for Business & Economic Analysis, Inc.1720 Carey Ave., Suite 520 • Cheyenne, Wyoming 82001

(307) 632-1347

33

Recommended