Strategic Management JournalStrat. Mgmt. J.,22: 1–23 (2001)

DOES CORPORATE STRATEGY MATTER?

EDWARD H. BOWMAN1 and CONSTANCE E. HELFAT2*1The Wharton School, University of Pennsylvania, Philadelphia, Pennsylvania,U.S.A.2The Amos Tuck School, Dartmouth College, Hanover, New Hampshire, U.S.A.

A revisionist view that corporate strategy does not matter has gained considerable influencein recent years. This view largely stems from empirical results of early variance decompositionstudies that found negligible corporate effects associated with profitability differences betweenbusinesses. Our analysis of the variance decomposition literature shows this view to be incorrect.Not only do the studies as a group show that factors at the corporate level of organizationscontribute to profitability differences, but also evidence suggests that factors specificallyassociated with corporate strategy contribute to corporate effects. Corporate strategy in factdoes matter.Copyright 2001 John Wiley & Sons, Ltd.

INTRODUCTION

Literature on strategic management typicallydistinguishes between business and corporatestrategy. Business strategy deals with the waysin which a single-business firm or an individualbusiness unit of a larger firm competes within aparticular industry or market. Corporate strategydeals with the ways in which a corporation man-ages a set of businesses together (Grant, 1995).In the past several years, researchers have soughtto assess the relative importance of industry, busi-ness, and corporate factors in determining prof-itability differences between firms. Perhaps thebest known of these works in the field of strategy(Rumelt, 1991) finds that effects specific to indi-vidual businesses explain the largest portion ofthe variance of business-level profitability, fol-lowed by much smaller industry effects. Rumeltalso finds that corporate effects explain almost

Key words: corporate effects; corporate strategy; firmperformance; variance decomposition*Correspondence to: Constance E. Helfat, The Amos TuckSchool, 100 Tuck Hall, Dartmouth College, Hanover, NH03755, U.S.A.

Copyright 2001 John Wiley & Sons, Ltd. Received 13 July 1998Final revision received 16 June 2000

none of the variance of profitability. Based inpart on Rumelt’s work, a number of scholars havesuggested that industry effects on profitability aresmall and that corporate effects do not exist (e.g.,Carroll, 1993; Ghemawat, 1994; Ghemawat andRicart i Costa, 1993; Hoskisson, Hill and Kim,1993). By implication, the large amount ofresearch, teaching, and consulting related tocorporatestrategy may be a waste of time. In thisarticle, we ask: does corporate strategy matter?

To answer this question, we focus on empiricalstudies that use variance decomposition tech-niques, because these studies incorporate the roleof entire classes of effects in explaining differ-ences in profitability. Although we are parti-cularly interested in corporate effects, many ofthe variance decomposition studies emphasize theimportance of industry effects (e.g., Schmalensee,1985; McGahan and Porter, 1997), especiallyrelative to business-level effects (Rumelt, 1991).The emphasis on industry reflects a continuingdebate in the literature about the relative impor-tance of the market (looking through the window)vs. the company itself (looking in the mirror)(Bowman, 1990). This debate has centered largelyon issues of business rather than corporate strat-

2 E. H. Bowman and C. E. Helfat

egy. In the economics literature, for example,Demsetz (1973) argued that the efficiency ofindividual businesses rather than industry struc-ture (Bain, 1956) determined profitability. Dis-cussions of the resource-based view in strategyhave made similar arguments that business-levelresources are at least as important as industry-level factors in determining competitive advantagewithin a market (e.g., Barney, 1991). Theresource-based view, however, also contains asignificant role for corporate strategy based onutilization of common resources by related busi-nesses within a firm (Peteraf, 1993).

Until recently, the variance decomposition stud-ies have placed less emphasis on the issue ofcorporate effects on profitability (with the notableexception of Wernerfelt and Montgomery, 1988).Some recent studies, however, focus directly onthe corporate effect (Bercerra, 1997; Brush andBromiley, 1997; Chang and Singh, 1997). Theseand some other newer studies (Roquebert, Phil-lips, and Westfall, 1996; McGahan, 1997; McGa-han and Porter, 1999) contain noticeably largerestimates of corporate effects than do Rumelt(1991) and Schmalensee (1985) (as well asMcGahan and Porter, 1997). We provide a com-prehensive analysis and critique of what the vari-ance decomposition studies as a group tell usabout the importance of corporate strategy.

Our analysis begins with a brief introductionto variance decomposition techniques. Next weexamine corporate-level factors that in theoryinfluence profitability, and the extent to whichthese corporate influences reflect corporate strat-egy. Then we discuss some conceptual issuesregarding the use of variance decomposition tomeasure corporate influence on profitability, andexplain what the findings of these studies poten-tially can or cannot tell us about the usefulness ofcorporate strategy. We also provide an integrativesummary of the results of the various studiesregarding corporate, business, and industryeffects, and show that the studies encompass amuch larger range of estimated corporate effectsthan is commonly thought. This summaryincludes a completely separate literature in man-agement that asks some similar questions, usessome similar techniques, and predates Rumelt(1991) by almost 20 years, but which none ofthe current authors discuss. Our analysis thenturns to a non-technical and intuitive discussionof some of the data and statistical issues that

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

affect interpretation of the findings in the variancedecomposition studies regarding the importanceof corporate effects.

Based on analysis of the evidence, we thenanswer our original question. Yes, corporate strat-egy matters. Contrary to common perception,many of the studies contain sizeable estimates ofcorporate effects. Moreover, the methodology andsample composition in many of the studies tendto produce estimates of corporate effects that donot fully reflect the influence of corporate strategyon profitability. Some of the sample selection andmethodological issues can be easily remedied andsome cannot. Despite these issues, a preponder-ance of the evidence from these studies showsthat corporate effects are non-negligible.Additional evidence that we bring to bear sug-gests that corporate strategy contributes to theestimated corporate effects. We also makesuggestions for future research on the questionof whether corporate strategy matters.

VARIANCE DECOMPOSITION

The current empirical debate about the importanceof industry, business, and corporate effects beganwith a study by Schmalensee (1985), followedby studies by Kessides (1987), Wernerfelt andMontgomery (1988), Kessides (1990), Rumelt(1991), Roquebertet al. (1996), McGahan andPorter (1997, 1998), McGahan (1997), Brush andBromiley (1997), Bercerra (1997), Chang andSingh (1997), and Fox, Srinivasan, and Vaaler(1997). All of these studies decompose the vari-ance of business or firm returns (or businessmarket share in one study) into componentsassociated with industry, business, and corporateeffects, and some studies include year effectsand interaction terms as well. Other studies haveanalyzed the importance of industry effects only(Powell, 1996), of industry and firm effects(Cubbin and Geroski, 1987; Mauri and Michaels,1998), and of industry and organizational effects(Hansen and Wernerfelt, 1989). Only the variancedecomposition studies examined here, however,separate corporate from business and industryeffects on profitability (even though the earlystudies focused more on industry and businessthan on corporate effects).

The variance decomposition studies use twomethods to estimate corporate, business, and

Does Corporate Strategy Matter? 3

industry effects on the variance of profitability:analysis of variance and variance components.Both techniques utilize the average of returns toindividual corporations, industries, and businessesin the estimation procedures for decomposing thevariance of returns.1 Corporate effects, forexample, generally derive from differencesbetween multiple-business firms in the averageof returns to individual businesses within eachcorporation. Industry effects derive from differ-ences between industries in the average of returnsto individual businesses within each industry.Finally, business effects typically derive fromdifferences between businesses in the average ofannual returns to each business.

As noted previously, scholars have made infer-ences about the importance of corporate strategybased on estimates of corporate effects in thevariance decomposition studies. In order to evalu-ate such inferences, we first ask: whatin theoryare the corporate-level factors that influence firmor business profitability, and to what extent dothese factors reflect corporate strategy? Theanswer to this theoretical question can then helpus to understand the extent to which empiricalestimates of corporate effects may inform usabout corporate strategy.

CORPORATE INFLUENCE ANDCORPORATE STRATEGY

Corporate influence on profitability results fromfactors associated with membership of multiplebusinesses within individual corporations. Of themany corporate-level factors that theoreticallyaffect profitability, much research has focused onscope of the firm, including selection of industriesin which to operate. Building on the work ofRumelt (1974), research has analyzed the linkbetween relatedness in diversification and firmperformance. A large amount of research also hasinvestigated the consequences of vertical inte-gration for firms, including the seminal work ofWilliamson (1975, 1985), who pointed to theadvantages of vertical integration when trans-actions costs are high.

1 Schmalensee (1985) and Rumelt (1991) make clear thatvariance components estimation utilizes average returns. Stan-dard analysis of variance techniques also utilize averagereturns (see, for example, Bowman and Fetter, 1967).

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

As another well-known example of corporate-level factors thought to affect profitability, Pra-halad and Hamel (1990) point to the importancefor corporate success ofcore competenciesthatspan businesses within a corporation. With regardto corporations, Chandler (1962, 1977) and Willi-amson (1975) have emphasized the advantage ofthe multidivisional (M-form) organization overthe functional organization of multiple-businessfirms. In analyzing the advantages of particularorganizational structures for multiple-businessfirms, both Chandler and Williamson argue forthe importance of the corporation, as distinct fromindividual lines of business within the company.Additional research related to firm organizationhas shown thatorganizational climate affectscorporate profitability (Hansen and Wernerfelt,1989). Other research has dealt with systems ofplanning and control, including the use of stra-tegic versus financial control (e.g., Goold andCampbell, 1987). With regard to financial controland financing of investments, Williamson (1975)has argued for the benefits of internal capitalmarkets in corporations, followed by much sub-sequent research (see Liebeskind, 2000).

Additionally, profitability may be influenced bycorporate management, which includes managerialability, and manifests itself concretely in mana-gerial plans, decisions, directives, advice, and goalsetting for the company as a whole and for indi-vidual businesses within the corporation (e.g.,Andrews, 1987; Hambrick and Mason, 1984).

Which, if any, of the foregoing corporateinfluences on profitability stem from corporatestrategy? To answer this question, we first requirea working definition of corporate strategy. Grant(1995: 396–397), for example, identifies the fivefollowing concerns of corporate-level strategicmanagement (to which we have added items initalics from the aforementioned corporate influ-ences on profitability): composition of businesses(scope of the firm); resource allocation betweenbusinesses (planning and control); formulation ofbusiness unit strategies (planning and control,corporate management); control of business unitperformance (planning and control); coordinationof business units and creation of company cohe-siveness and direction (core competencies,organizational structure, organizational climate,corporate management).

As another example, Jack Welch, the highlyregarded CEO of General Electric, has described

4 E. H. Bowman and C. E. Helfat

important corporate goals and activities at GE (towhich we again have added items in italics):require each business to be number one or twoin its industry (planning and control); reducethe number of management levels (organizationalstructure); seek managerial self-confidence, sim-plicity, and speed (organizational climate); utilizefree-form ‘workout’ discussions among managersat many levels and functional responsibilitiesto resolve business problems (corporatemanagement); select managers with attention tostyle and performance (planning and control,corporate management); provide in-house execu-tive education focused on active rather than pas-sive (i.e., book) learning (corporate management);share best practices across divisions and also lookto other companies and countries (core com-petencies and resources); set stretch goals formargins, inventory turnover (planning and con-trol, corporate management); provide stock com-pensation to 20,000 employees (planning andcontrol) (General Electric, 1995).

The Grant and Welch examples touch on manycorporate-level factors thought to influence prof-itability, as indicated by the terms in italics.Additionally, in these examples, corporate man-agement has at least some impact on all othercorporate-level factors that influence profitability.Grant’s representative typology, for example,describes strategicmanagementand covers factorslargely under management control (e.g., allocationof resources). Jack Welch’s list reflects the goalsof GE’s top managers and the activities they putin place (e.g., workout sessions). Research in thefield of strategic management commonly usesthe terms ‘strategy’ and ‘strategic management’interchangeably. Similarly, we use the termcorporate strategyas synonymous withcorporatestrategic management, to reflect the contributionof corporate management to corporate-level fac-tors that affect profitability.

Given the foregoing working definition ofcorporate strategy, we suggest that as atheo-retical matter, corporate management has someimpact on, but not complete control of, corporate-level factors that influence profitability. Forexample, corporate management by itself cannotbuild core competencies, which generally residewithin an organization and consist in part oforganizational routines (Nelson and Winter,1982). Top management, however, may have animportant role in targeting and helping to develop

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

and sustain organizational capabilities (Castaniasand Helfat, 1991, 1992). Thus, in theory corporatemanagement and corporate strategy have animpact on but do not fully determine corporateinfluence on profitability.

Implications for variance decomposition

Based on our discussion thus far, we draw someimplications for the variance decomposition stud-ies. First, since in theory corporate strategy is asubset of total corporate influence on profitability,in order to draw conclusions from the variancedecomposition studies about corporate strategy, itis important to first determine the accuracy withwhich estimated corporate effects measure corpo-rate influence. In what follows, we show thatestimated corporate effects do not fully capturecorporate influence on profitability in general, andthe impact of corporate strategy in particular.Therefore, even low estimates of corporate effectsmay be consistent with a positive influence ofcorporate strategy on the variability of profitability.

Secondly, if estimated corporate effects aresignificant rather than nil, then we would like toknow if corporate strategy contributes to corpo-rate effects. The variance decomposition studiesdo not provide evidence related to this issue. Thatis, the studies do not estimate the contributionof corporate strategicmanagementto corporateeffects. We therefore introduce evidence from adifferent and earlier set of ‘leadership’ studiesthat estimate the effect of top management, inthe form of different CEOs, on the varianceof profitability.

THE VARIANCE OF PROFITABILITY

As a foundation for our analysis, we next addresssome fundamental issues regarding the variancedecomposition studies, before summarizing theresults of the studies and presenting more detailedanalysis of the methods and data. To begin, it isuseful to note that the variance decompositionstudies treat as similar entities both single-business firms and businesses in larger corpo-rations that are wholly contained within individualindustries.2 The studies also use different terms

2 Two studies (Bercerra, 1997; Roquebertet al., 1996) includeonly multiple-business firms.

Does Corporate Strategy Matter? 5

to denote these entities. To prevent confusion,we use the termbusinessto refer to companyoperations contained within an industry, whetherin a single-business or a multiple-business firm.

Variance of returns

The variance decomposition studies measure thecorporate effect as a percent of the total varianceof the dependent variable.3 This use ofvarianceas a measure provides information about differ-ences between multiple-business firms. A negli-gible estimate of the corporate effect suggeststhat even if corporate influence has an impacton the level of profitability of individual firms,differencesbetween firms in corporate influenceare zero. Thus,the finding of a negligible corpo-rate effect combined with a large business effect(e.g., Rumelt, 1991) implies the elimination ofdifferences in profitability at the corporate levelbut not at the business level.Consider how thisimplication affects the resource-based view, forexample. Large business effects but zero corpo-rate effects together suggest equalization ofreturns to corporate-level resources across corpo-rations, but not to business-level resources acrossbusinesses. Such a stark difference in the vari-ation of returns to resources at different levels ofthe organization obviously would requireadditional explanation.

In addition to using variance to measure effectson profitability, the studies measure the ‘impor-tance’ of each effect by its magnitude. That is,the larger the percentage of profitability varianceassociated with an effect, the greater is the pre-sumed importance of the effect.4 The studies alsogenerally compare the percent of the total vari-ance of profitability associated with the corporateeffect to the percentages of the varianceassociated with business and industry effects.Such a comparison, however, doesnot provide auseful answer to the question of whether corpo-

3 In general, the minimum corporate effect is zero in thesestudies. A small negative value is usually interpreted as zero(Rumelt, 1991).4 Brush and Bromiley (1997) argue that the size of an effectis more properly interpreted as the square root of the percentof profitability variance for that effect. Our point here insteadhas to do with comparisons between the sizes of differenteffects, and the difficulty of using such comparisons to makeinferences about strategy.

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

rate strategy matters in explaining profitabilitydifferences between firms, for two reasons.

First, just as corporate influence on profitabilityin theory may reflect factors in addition to corpo-rate strategy, business and industry influences onprofitability in theory may reflect factors otherthan business and industry-level strategy. Forexample, business effects may include substantialinfluence of the histories of individual businessesunrelated to strategic management, such as idio-syncratic and difficult-to-change organizationallearning paths (Nelson and Winter, 1982). There-fore, even if estimated business effects comprisea larger portion of the total variance of prof-itability than do corporate effects, it does notnecessarily follow that corporate strategy is lessimportant than business strategy. Business as wellas industry effects may reflect difficult-to-changeand idiosyncratic factors unrelated to strategy.Hence, the relative size of each effect—corporate,business, or industry—does not allow us to makeinferences about the importance of any type ofstrategy, corporate or otherwise. Instead, it isappropriate to ask whether the corporate effect isnon-negligible, i.e., differs statistically signifi-cantly from zero.5

Second, as analyzed in detail later, empiricalestimates of corporate effects may not fully andaccurately capture the influence of corporate strat-egy on the variance of profitability. As oneexample, consider the way in which a companysuch as Disney uses its cartoon characters inmultiple businesses as an important element ofcorporate strategy. Suppose that use of the Disneycharacters greatly improves the performance ofthe theme-park business relative to theme-parkbusinesses in other companies, but only slightlyimproves the performance of Disney’s filmbusiness relative to film businesses in othercompanies. The estimated corporate effect wouldcapture only the average improvement across Dis-ney’s two businesses. The analysis further would

5 Of the statistical techniques used in the variance decomposi-tion studies, analysis of variance and some variance compo-nents techniques produce standard errors that can be used toevaluate statistical significance. Rumelt (1991) also showshow approximate standard errors can be estimated for othervariance components techniques. Statistical significance ofcorporate effects in variance decomposition studies, however,is complicated by the fact that variance components techniquesin general have low power (Brush and Bromiley, 1997), asdoes analysis of variance when firms operate in only a fewindustries (Kessides, 1987).

6 E. H. Bowman and C. E. Helfat

attribute the additional improvement in the theme-park business to the business effect rather thanthe corporate effect.6 Thus, while as a theoreticalmatter, corporate strategy is a subset of corporateinfluence on profitability, as an empirical matter,estimated corporate effects may leave outimportant elements of corporate strategy. As aresult, comparison of corporate and other effectsmay provide incomplete information regarding theimportance of corporate strategy.

In sum, contrary to common perception, thesizes of estimated effects other than the corporateeffect do not provide a relevant standard forassessing the importance of corporatestrategy.

Average returns

As noted earlier, in decomposing the variance ofreturns, the studies use average returns in theestimation procedures. Therefore, only theaver-age of the returns to all of the businesses withina corporation has an impact on the estimatedcorporate effect.As a result, individual corpo-rations do not have to have an impact onallbusinesses in which they participate in order toproduce a corporate effect.Corporations musthave an impact on only enough of their busi-nesses to produce a statistical effect. Empiricalconfirmation of this comes from the results ofBrush and Bromiley (1997), which show thatmeasurable corporate effects are possible if eachcorporation has an impact on only half of itsbusinesses.7 Furthermore, the use of averagereturns within each firm implies that individualcorporations need not have an identical impacton each of their businesses in order for studiesto find a corporate effect.

Additionally, individual corporate-level factorsthat contribute to corporate effects do not neces-sarily have the same impact on all of the busi-nesses in a firm. Some corporate-level factorsmay increase returns to some businesses butdecrease returns to others—the average effect ofsuch factors within each multiple-business firmcontributes to the estimated corporate effect. Assuggested by our earlier discussion of corporate-level factors that may influence profitability, anynumber of empirical studies have found that indi-

6 We are grateful to an anonymous reviewer for this example.7 Brush and Bromiley (1997), however, used this result tomake a different point than we make here.

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

vidual sorts of corporate-level factors statistically‘explain’ the variability of at least a portion ofthe profitability of multiple-business firms, e.g.,strategic planning (Miller and Cardinal, 1994),diversification (Montgomery, 1994), vertical inte-gration (Rumelt, 1974), organizational climate(Hansen and Wernerfelt, 1989), organizationalstructure (Teece, 1981), and international activity(Hitt, Hoskisson, and Kim, 1997). These findingsdo not preclude the possibility that some corpo-rate-level factors may raise firm profitability over-all and others may lower it. Again, the net impactof all corporate-level factors on the average returnwithin each multiple-business firm contributes toestimated corporate effects.

EMPIRICAL STUDIES

The foregoing overarching considerations regard-ing the structure of variance decomposition stud-ies affect interpretation of the results with regardto the importance of corporate strategy, as do anumber of more detailed issues related to dataselection and statistical methods. To provide abasis for further analysis of these issues, we nextpresent a summary of the results of the variousstudies. We also summarize the results of theempirical ‘leadership’ studies that estimate topmanagement effects on the variance of prof-itability.

Variance decomposition studies

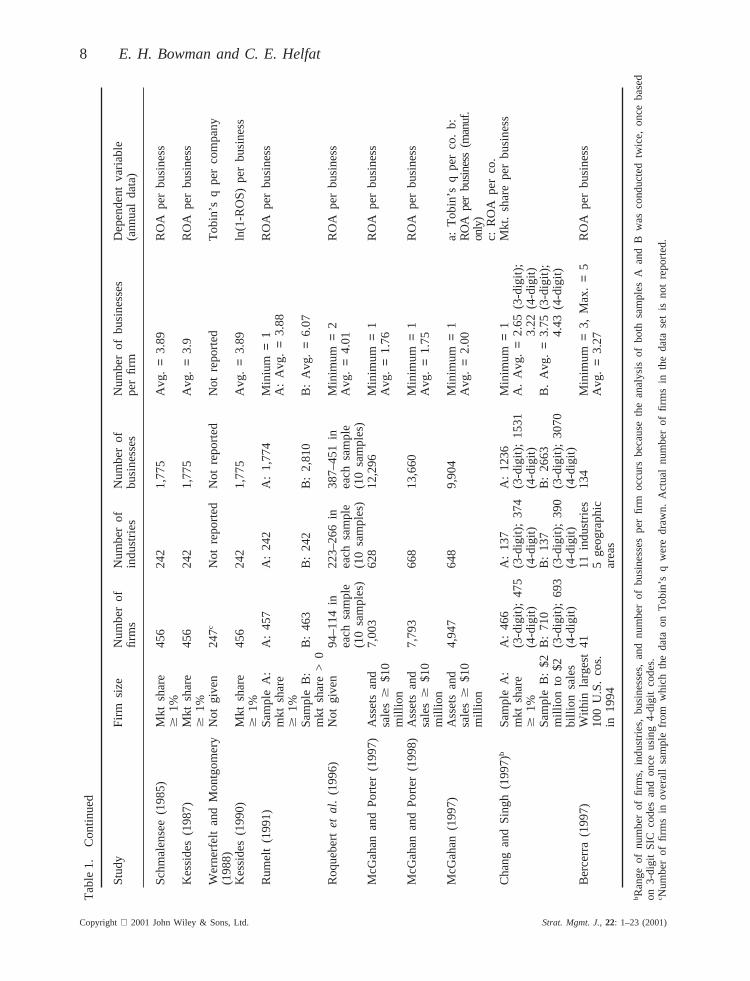

Table 1 provides a comprehensive summary ofthe data, empirical techniques, and results of thevariance decomposition studies that includecorporate effects. Of the variance decompositionstudies cited in the prior section, the table omitsthe studies by Brush and Bromiley (1997) andFox et al. (1997), because the results includesimulations. The table includes not only well-known studies, but also less well-known yet pub-lished studies and research in circulation as work-ing papers.

Table 1 denotes each study by author in theleft-hand column of each page of the table, andfor each study the table reports: data sources;years included; definition of an industry; types ofindustries included; definition of a business; sizesof firms; number of firms, businesses, and busi-nesses per firm; dependent variable; statistical

Does Corporate Strategy Matter? 7

Tab

le1.

Var

ianc

ede

com

posi

tion

stud

ies

Stu

dyD

ata

base

Yea

rsin

clud

edIn

dust

ryde

finiti

onT

ypes

ofD

efini

tion

ofa

busi

ness

indu

strie

s

Sch

mal

ense

e(1

985)

FT

CLO

Ba

1975

LOB

>3

1/2-

digi

tS

ICM

anuf

actu

ring

All

co.

busi

ness

inea

chLO

Bon

lyca

tego

ryK

essi

des

(198

7)F

TC

LOB

Sam

ple

A:

1975

LOB>3

1/2-

digi

tS

ICM

anuf

actu

ring

All

co.

busi

ness

inea

chLO

BS

ampl

eB

:19

74–

only

cate

gory

1976

Wer

nerf

elt

and

Mon

tgom

ery

Trin

et/E

IS;

FT

C;

1976

2-di

git

SIC

Indu

stria

lan

dA

llco

.bu

sine

ssin

each

LOB

(198

8)ot

her

sour

ces

utili

tyco

s.ca

tego

ryK

essi

des

(199

0)F

TC

LOB

1975

LOB>

31/

2-di

git

SIC

Man

ufac

turin

gA

llco

.bu

sine

ssin

each

LOB

only

cate

gory

Rum

elt

(199

1)F

TC

LOB

1974

–197

7LO

B>3

1/2-

digi

tS

ICM

anuf

actu

ring

All

co.

busi

ness

inea

chLO

Bon

lyca

tego

ryR

oque

berte

ta

l.(1

996)

Com

pust

at19

85–1

991

4-di

git

SIC

(bro

adly

defin

ed)

Man

ufac

turin

gA

llco

.bu

sine

ssin

each

SIC

only

code

McG

ahan

and

Por

ter

(199

7)C

ompu

stat

1981

–199

44-

digi

tS

IC(b

road

lyde

fined

)N

on-fi

nanc

ial

All

co.

busi

ness

inea

chS

ICco

deM

cGah

anan

dP

orte

r(1

998)

Com

pust

at19

81–1

994

4-di

git

SIC

(bro

adly

defin

ed)

Non

-fina

ncia

lA

llco

.bu

sine

ssin

each

SIC

code

McG

ahan

(199

7)C

ompu

stat

1981

–199

44-

digi

tS

IC(b

road

lyde

fined

)N

on-fi

nanc

ial

All

co.

busi

ness

inea

chS

ICco

deC

hang

and

Sin

gh(1

997)

Trin

et/E

IS19

81,

1983

,i)

4-di

git

SIC

(nar

row

lyde

fined

)M

anuf

actu

ring

All

co.

busi

ness

inea

ch:

i)4

1985

,19

87,

ii)3-

digi

tS

ICon

lydi

git

SIC

code

;ii)

3di

git

SIC

1989

code

Ber

cerr

a(1

997)

Com

pust

at19

91–1

994

4-di

git

SIC

(bro

adly

defin

ed):

Non

eex

clud

edA

llco

.bu

sine

ssin

broa

dw

orld

stud

yal

soin

clud

escl

assi

ficat

ion

geog

raph

icar

ea(m

ultin

atio

nal

bybr

oad

wor

ldge

ogra

phic

area

cos.

only

)

a LO

Bis

anab

brev

iatio

nfo

r‘li

neof

busi

ness

,’w

hich

isan

indu

stry

clas

sific

atio

n(R

umel

t,19

91).

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

8 E. H. Bowman and C. E. Helfat

Tab

le1.

Con

tinue

d

Stu

dyF

irmsi

zeN

umbe

rof

Num

ber

ofN

umbe

rof

Num

ber

ofbu

sine

sses

Dep

ende

ntva

riabl

efir

ms

indu

strie

sbu

sine

sses

per

firm

(ann

ual

data

)

Sch

mal

ense

e(1

985)

Mkt

shar

e45

624

21,

775

Avg

.=

3.89

RO

Ape

rbu

sine

ss$

1%K

essi

des

(198

7)M

ktsh

are

456

242

1,77

5A

vg.

=3.

9R

OA

per

busi

ness

$1%

Wer

nerf

elt

and

Mon

tgom

ery

Not

give

n24

7c

Not

repo

rted

Not

repo

rted

Not

repo

rted

Tob

in’s

qpe

rco

mpa

ny(1

988)

Kes

side

s(1

990)

Mkt

shar

e45

624

21,

775

Avg

.=

3.89

ln(1

-RO

S)

per

busi

ness

$1%

Rum

elt

(199

1)S

ampl

eA

:A

:45

7A

:24

2A

:1,

774

Min

ium=

1R

OA

per

busi

ness

mkt

shar

eA

:A

vg.=

3.88

$1%

Sam

ple

B:

B:

463

B:

242

B:

2,81

0B

:A

vg.=

6.07

mkt

shar

e>

0R

oque

berte

ta

l.(1

996)

Not

give

n94

–114

in22

3–26

6in

387–

451

inM

inim

um=2

RO

Ape

rbu

sine

ssea

chsa

mpl

eea

chsa

mpl

eea

chsa

mpl

eA

vg.

=4.

01(1

0sa

mpl

es)

(10

sam

ples

)(1

0sa

mpl

es)

McG

ahan

and

Por

ter

(199

7)A

sset

san

d7,

003

628

12,2

96M

inim

um=

1R

OA

per

busi

ness

sale

s$$1

0A

vg.=

1.76

mill

ion

McG

ahan

and

Por

ter

(199

8)A

sset

san

d7,

793

668

13,6

60M

inim

um=

1R

OA

per

busi

ness

sale

s$$1

0A

vg.=

1.75

mill

ion

McG

ahan

(199

7)A

sset

san

d4,

947

648

9,90

4M

inim

um=1

a:T

obin

’sq

per

co.

b:sa

les$

$10

Avg

.=2.

00R

OA

per

busi

ness

(man

uf.

mill

ion

only

)c:

RO

Ape

rco

.C

hang

and

Sin

gh(1

997)b

Sam

ple

A:

A:

466

A:

137

A:

1236

Min

imum

=1

Mkt

.sh

are

per

busi

ness

mkt

shar

e(3

-dig

it);

475

(3-d

igit)

;37

4(3

-dig

it);

1531

A.

Avg

.=2.

65(3

-dig

it);

$1%

(4-d

igit)

(4-d

igit)

(4-d

igit)

3.22

(4-d

igit)

Sam

ple

B:

$2B

:71

0B

:13

7B

:26

63B

.A

vg.=

3.75

(3-d

igit)

;m

illio

nto

$2(3

-dig

it);

693

(3-d

igit)

;39

0(3

-dig

it);

3070

4.43

(4-d

igit)

billi

onsa

les

(4-d

igit)

(4-d

igit)

(4-d

igit)

Ber

cerr

a(1

997)

With

inla

rges

t41

11in

dust

ries

134

Min

imum=

3,M

ax.=

5R

OA

per

busi

ness

100

U.S

.co

s.5

geog

raph

icA

vg.=3.

27in

1994

area

s

bR

ange

ofnu

mbe

rof

firm

s,in

dust

ries,

busi

ness

es,

and

num

ber

ofbu

sine

sses

per

firm

occu

rsbe

caus

eth

ean

alys

isof

both

sam

ples

Aan

dB

was

cond

ucte

dtw

ice,

once

base

don

3-di

git

SIC

code

san

don

ceus

ing

4-di

git

code

s.c N

umbe

rof

firm

sin

over

all

sam

ple

from

whi

chth

eda

taon

Tob

in’s

qw

ere

draw

n.A

ctua

lnu

mbe

rof

firm

sin

the

data

set

isno

tre

port

ed.

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

Does Corporate Strategy Matter? 9

Tab

le1.

Con

tinue

d

Stu

dyS

tatis

tical

tech

niqu

ed

Cor

pora

teef

fect

Bus

ines

sef

fect

Indu

stry

effe

ctY

ear

effe

ctIn

dust

ry3

Oth

erin

tera

ctio

nsY

ear

Sch

mal

ense

e(1

985)

i)O

LShi

erar

chic

alre

gres

sion

i)ze

roM

ktsh

are

effe

ct:

i)18

.8to

Not

incl

uded

Not

incl

uded

i)ne

gativ

eco

v.(A

NO

VA

)i)

0.2

to0.

6%19

.3%

bus.

&in

d.ii)

varia

nce

com

pone

nts

ii)no

tin

clud

edii)

0.6%

ii)19

.5%

sugg

este

dii)

cov.

bus.

&in

d:2

0.6%

Kes

side

s(1

987)

OLS

hier

arch

ical

regr

essi

onA

:1

to8%

eM

ktsh

are

effe

ct:

A:

not

Not

incl

uded

Not

incl

uded

Not

incl

uded

(AN

OV

A)

B:

11to

54%

fA

:no

tre

port

edre

port

edB

:5

to39

%f

B:

9to

45%

f

Wer

nerf

elt

and

OLS

hier

arch

ical

regr

essi

onC

orp.

focu

sM

ktsh

are

effe

ct:

10.9

to20

.1%

Not

incl

uded

Not

incl

uded

Not

incl

uded

Mon

tgom

ery

(198

8)(A

NO

VA

)(r

elat

edne

ss):

0.2

0to

2.3%

to3.

7%K

essi

des

(199

0)W

eigh

ted

leas

tsq

uare

sw

itha

5.1

to9.

8%M

ktsh

are

effe

ct:

4.7

to25

.2%

Not

incl

uded

Not

incl

uded

Not

incl

uded

mix

offix

edan

dra

ndom

6.6

to27

.5%f

effe

cts—

hier

arch

ical

regr

essi

ong

Rum

elt

(199

1)i)

sequ

entia

lan

alys

isof

i)A

:14

.8to

i)A

:33

.9to

i)A

:15

.3to

i)A

:0%

i)A

:9.

6to

i)N

otin

clud

edva

rianc

e17

.6%

34.0

%17

.9%

B:

0.1%

9.8%

ii)co

v.in

d.&

B:

10.9

toB

:41

.3to

B:

9.8

toB

:6.

8to

corp

orat

ion;

11.6

%41

.4%

10.3

%7.

1%ii)

varia

nce

com

pone

nts

hii)

A:

0%ii)

A:

47.2

%ii)

A:

7.3%

ii)A

:0%

ii)A

:8.

9%A

:0.

76%

B:

1.6%

B:

44.2

%B

:4.

0%B

:0%

B:

5.3%

B:

0%R

oque

berte

ta

l.V

aria

nce

com

pone

nts

17.9

%(a

vg.

37.1

%(a

vg.

10.1

%(a

vg.

0.4%

(avg

.2.

3%(a

vg.

(199

6)ac

ross

sam

ples

)ac

ross

sam

ples

)ac

ross

acro

ssac

ross

sam

ples

)sa

mpl

es)

sam

ples

)

dF

oran

alys

isof

varia

nce,

size

sof

estim

ated

effe

cts

may

have

ara

nge

depe

ndin

gon

varia

ble

orde

rof

entr

y.e K

essi

des

(198

7)pr

ogre

ssiv

ely

elim

inat

edfir

ms

with

less

than

2,3,

or4

busi

ness

es.

f Kes

side

s(1

987)

allo

wed

the

coef

ficie

nton

mar

ket

shar

eto

vary

byin

dust

ry.

Thi

saf

fect

sal

lth

ees

timat

edef

fect

s.gK

essi

des

(199

0)el

imin

ated

outli

ers,

soth

atre

sults

repo

rted

here

are

base

don

1711

obse

rvat

ions

.K

essi

des

also

allo

wed

the

coef

ficie

nton

mar

ket

shar

eto

vary

byin

dust

ry.

hR

esul

tsar

efr

omT

able

1in

Rum

elt

(199

1).

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

10 E. H. Bowman and C. E. Helfat

Tab

le1.

Con

tinue

d

Stu

dyS

tatis

tical

tech

niqu

eC

orpo

rate

effe

ctB

usin

ess

effe

ctIn

dust

ryef

fect

Yea

ref

fect

Indu

stry

3O

ther

inte

ract

ions

Yea

r

McG

ahan

and

i)se

quen

tial

anal

ysis

ofi)

9.1

to11

.9%

i)34

.9to

35.1

%i)

6.8

to9.

4%N

otin

clud

edN

otin

clud

edi)

Not

incl

uded

Por

ter

(199

7)va

rianc

eii)

varia

nce

com

pone

nts

ii)4.

3%ii)

31.7

%ii)

18.7

%ii)

cov.

ind.

and

corp

.:−5

.5%

McG

ahan

and

OLS

hier

arch

ical

8.8

to23

.7%

32.5

to59

.1%

6.9

to16

.3%

0.2

to1.

1%N

otin

clud

edN

otin

clud

edP

orte

r(1

998)

regr

essi

oni(A

NO

VA

)M

cGah

anS

eque

ntia

lan

alys

isof

a:co

rp.

focu

s=

Ass

etsh

are

effe

ct:

a:21

.6to

29.4

%a:

0to

2.9%

Not

incl

uded

Not

incl

uded

(199

7)va

rianc

ei0

to1%

b:8.

3%a:

35.3

to66

.0%

b:7.

6%b:

1.2%

c:co

rp.

focu

s=b:

28.7

%c:

8.6

to10

.6%

c:1.

7to

2.1%

0to

0.1%

c:14

.8to

31.2

%C

hang

and

Var

ianc

eco

mpo

nent

s3-

digi

tS

IC:

3-di

git

SIC

:3-

digi

tS

IC:

3-di

git

SIC

:3-

digi

tS

IC:

Not

incl

uded

Sin

gh(1

997)

A:0

%B

:1.6

%A

:15.

2%B

:13.

7%A

:1.6

%B

:3.1

%A

:2.4

%B

:1.0

%A

:6.2

%B

:11.

4%4-

digi

tS

IC:

4-di

git

SIC

:4-

digi

tS

IC:

4-di

git

SIC

:4-

digi

tS

IC:

A:4

.3%

B:8

.5%

A:5

2.7%

B:4

6.8%

A:1

9.4%

B:2

5.4%

A:0

.9%

B:0

.3%

A:0

.9%

B:1

.8%

Sam

ple

BS

ampl

eB

Sam

ple

BS

ampl

eB

Sam

ple

BN

otin

clud

ed(4

-dig

itS

IC)

(4-d

igit

SIC

)(4

-dig

itS

IC)

(4-d

igit

SIC

)(4

-dig

itS

IC)

Firm

size

Firm

size

Firm

size

Firm

size

Firm

size

larg

e:10

.9%

larg

e:44

.4%

larg

e:24

.1%

larg

e:0.

7%la

rge:

1.3%

med

ium

:25

.7%

med

ium

:15

.8%

med

ium

:40

%m

ediu

m:

0%m

ediu

m:

6.9%

smal

l:6.

3%sm

all:

15.6

%sm

all:

59.4

%sm

all:

0%sm

all:

12.5

%

Ber

cerr

ai)

hier

arch

ical

i)12

%i)

not

repo

rted

i)no

tgi

ven

i)no

tre

port

edi)

not

incl

i)no

tin

clud

ed(1

997)

regr

essi

on(AN

OV

A)

ii)4.

71%

ii)27

.2%

ii)In

dust

ry:

ii)no

tin

clii)

not

incl

ii)no

neii)

varia

nce

com

pone

nts

iii)

3.05

toiii

)no

tin

clud

ed30

.4%

Geo

gr.

iii)

not

sign

ifica

ntiii

)si

gnifi

cant

iii)

year

3co

rp.

iii)

repe

ated

mea

sure

s10

.95%

area

:6.

9%si

gnifi

cant

rand

omfa

ctor

siii

)In

dust

ry:

41.9

%(A

NO

VA

)to

46.8

%G

eogr

.ar

ea:

0to

1%

i The

rang

eof

resu

ltsre

port

edhe

rein

clud

esal

lof

the

estim

ates

give

nin

the

stud

y,in

clud

ing

for

subs

ampl

esof

the

data

.

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

Does Corporate Strategy Matter? 11

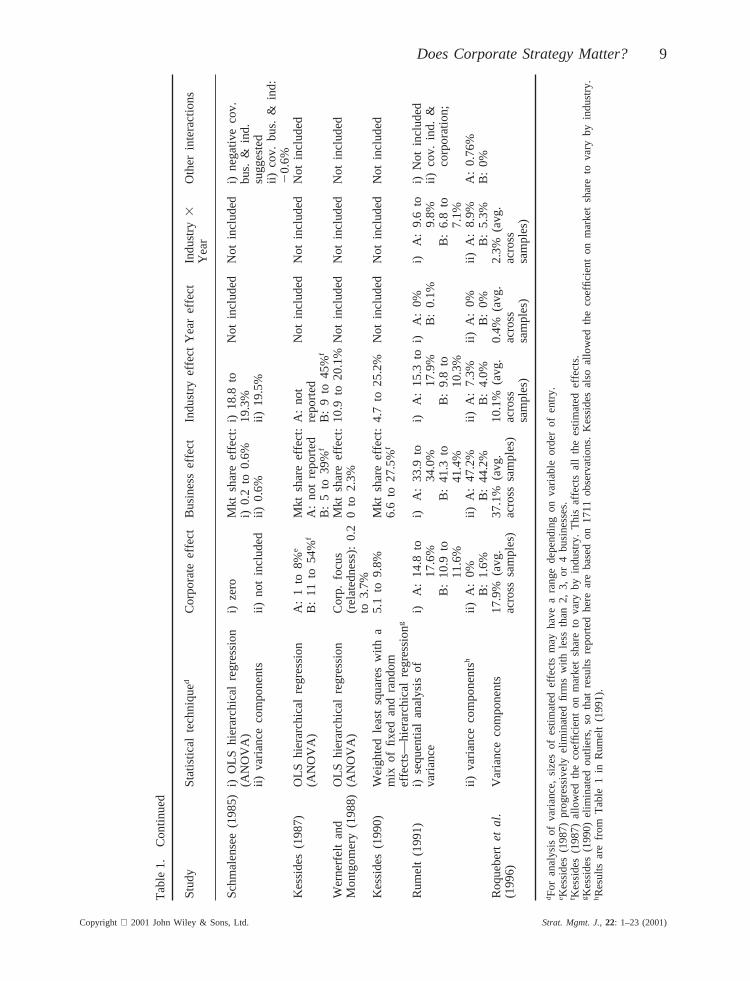

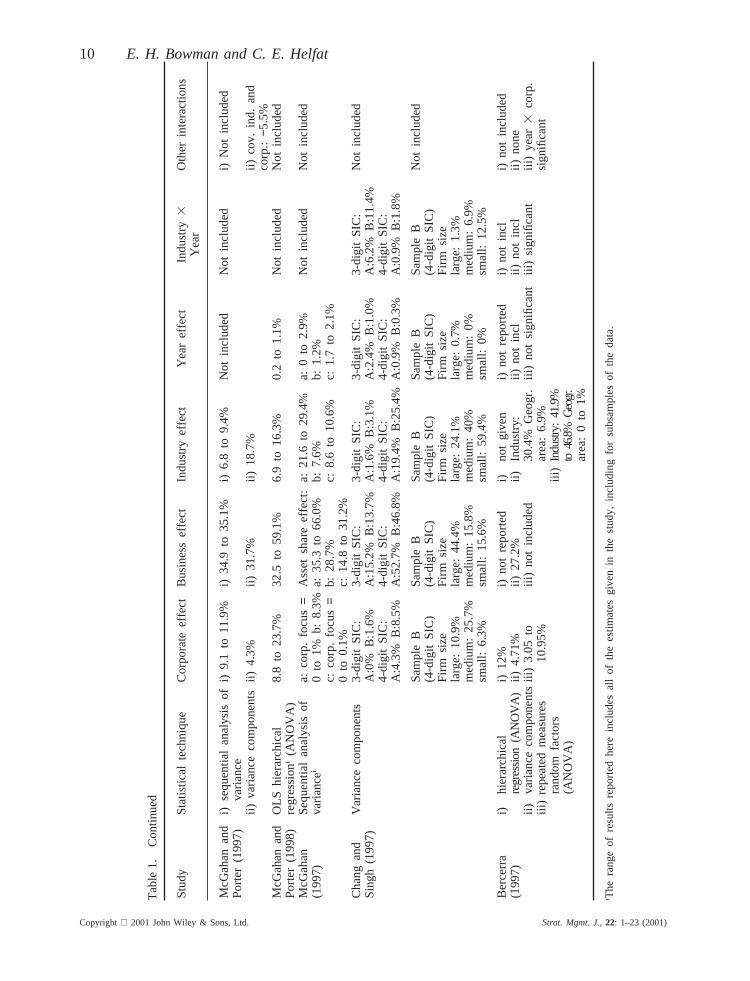

techniques employed; estimated corporate, busi-ness, industry, year, and interaction or covarianceeffects. Several of the studies use more than onestatistical technique. For each study, the tabledenotes each technique by number, and in thecolumns that report the various estimated effects,each technique number denotes estimates obtainedusing that particular technique. For each studythat uses analysis of variance, the table alsoreports a range of estimates, due to differentorderings of variable entry. Additionally, somestudies contain two main samples, denoted A andB in the columns that describe either the yearsincluded in the sample or firm size, and in thecolumns that report estimated effects. Sample Busually includes all of sample A plus additionalfirms. One study (McGahan, 1997) also uses threedifferent dependent variables, which are denotedwith different lower case letters in the columnsthat list the different dependent variables and thatreport estimated effects.

Table 1 shows that the studies as a groupinclude three sorts of dependent variables—individual business profitability using account-ing measures, firm-level return measured as Tob-in’s q (market value of the firm divided byreplacement cost of firm assets), and individualbusiness market share. These three measuresof firm performance incorporate differentinformation and in general are imperfectly corre-lated. Accounting profitability reflects historicalprofits relative to sales or book value of assets;Tobin’s q reflects investor expectations about firmvalue relative to asset replacement cost; marketshare reflects business revenues relative to rev-enues of other businesses in the same industry(McGahan, 1997). The studies use two main tech-niques: variance components and analysis of vari-ance. Some studies include only manufacturingindustries, and some studies include other indus-tries as well. The studies also differ in theinclusion or exclusion of single-business firms,the definition of a business and an industry, thenumber of years included, the sizes of firmsin the sample, and the number of businessesper corporation.

Importantly, the studies in Table 1 show awide range of estimated corporate effects. Inmany of these studies, corporate effects are farfrom nil—sometimes on the order of 18 percentor more, for the full sample or subsamples ofthe data.

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

Leadership studies

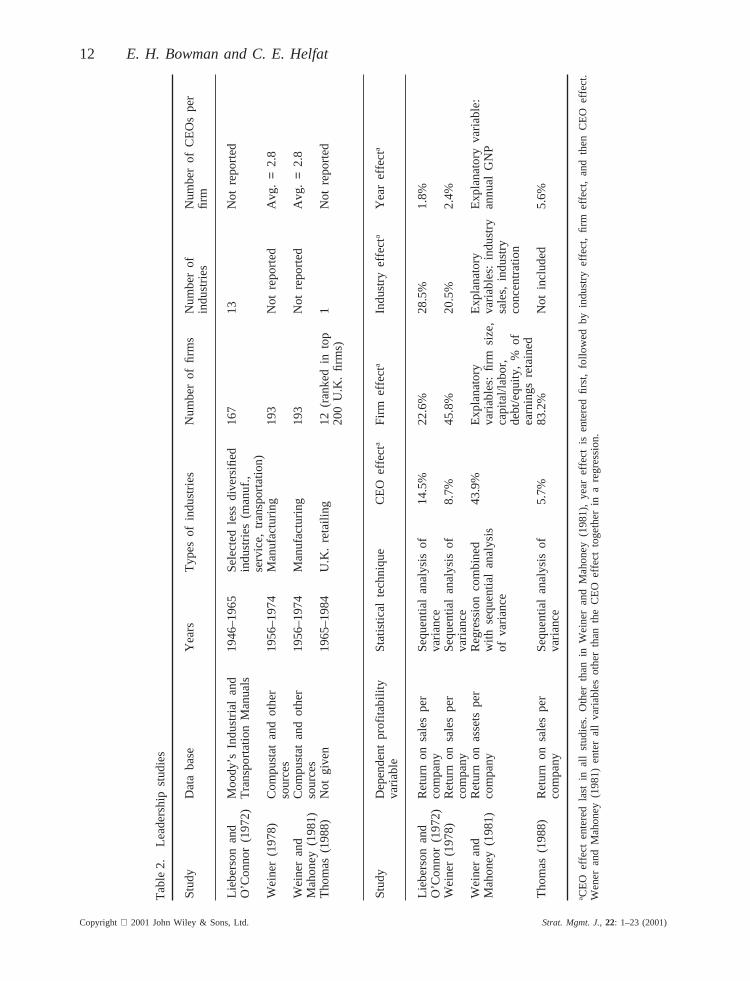

In addition to the variance decomposition studiesin Table 1, a separate and earlier set of studiesuses similar techniques to estimate top man-agement effects on profitability. The studiesdecompose the variance of profitability into year,industry, company, and ‘leadership’ effects, whereleadership effects result from differences betweenindividual chief executives in firm performance.(Strictly speaking, a ‘leadership’ effect can resultfrom any factor at the firm level associated withthe terms in office of chief executives.) Thedependent variables used in the leadership studiesare substantially the same as those in the variancedecomposition studies.

Table 2 summarizes the results of the leader-ship studies.8 The table lists each study by author,and for each study reports: data sources; yearsincluded; types of industries included; number offirms, industries, and CEOs per firm; dependentvariable; statistical technique; estimated CEO(i.e., leadership), firm, industry, and year effects.The studies include multiple-business as well assingle-business firms (except perhaps the studyby Thomas, 1988), and assign each firm to abroadly defined primary industry.9 Using analysisof variance, the studies first estimate year effects,then primary industry effects, and then firmeffects. These firm and industry effects are fixed(or ‘stable’) effects that reflect differencesbetween firms (or industries) in the average ofeach firm’s (or industry’s) annual returns overthe time period of a study. The firm effects inparticular capture differences in average prof-itability between firms due to corporate-level fac-tors (for multiple-business firms), business-levelfactors, and industry-level factors other than thoseassociated with the primary industry. After esti-mating year, industry, and firm effects, the analy-ses then estimate the leadership effect.10 The latterreflects differences between CEOs in the averageannual return per CEO during his term in office,

8 Table 2 omits one empirical study in this literature bySalancik and Pfeffer (1977), which deals with mayors andcity budgets rather than with for-profit companies of interesthere. In addition, for purposes of comparability with thevariance decomposition studies in Table 1, Table 2 omitsresults for dependent variables such as total sales or profitsthat do not reflect rates of return.9 Even the Thomas (1988) study may include diversified firmswhose primary business is retailing.10 Weiner (1978) also varies the order of variable entry.

12 E. H. Bowman and C. E. Helfat

Tab

le2.

Lead

ersh

ipst

udie

s

Stu

dyD

ata

base

Yea

rsT

ypes

ofin

dust

ries

Num

ber

offir

ms

Num

ber

ofN

umbe

rof

CE

Os

per

indu

strie

sfir

m

Lieb

erso

nan

dM

oody

’sIn

dust

rial

and

1946

–196

5S

elec

ted

less

dive

rsifi

ed16

713

Not

repo

rted

O’C

onno

r(1

972)

Tra

nspo

rtat

ion

Man

uals

indu

strie

s(m

anuf

.,se

rvic

e,tr

ansp

orta

tion)

Wei

ner

(197

8)C

ompu

stat

and

othe

r19

56–1

974

Man

ufac

turin

g19

3N

otre

port

edA

vg.

=2.

8so

urce

sW

eine

ran

dC

ompu

stat

and

othe

r19

56–1

974

Man

ufac

turin

g19

3N

otre

port

edA

vg.

=2.

8M

ahon

ey(1

981)

sour

ces

Tho

mas

(198

8)N

otgi

ven

1965

–198

4U

.K.

reta

iling

12(r

anke

din

top

1N

otre

port

ed20

0U

.K.

firm

s)

Stu

dyD

epen

dent

prof

itabi

lity

Sta

tistic

alte

chni

que

CE

Oef

fect

aF

irmef

fect

aIn

dust

ryef

fecta

Yea

ref

fecta

varia

ble

Lieb

erso

nan

dR

etur

non

sale

spe

rS

eque

ntia

lan

alys

isof

14.5

%22

.6%

28.5

%1.

8%O

’Con

nor

(197

2)co

mpa

nyva

rianc

eW

eine

r(1

978)

Ret

urn

onsa

les

per

Seq

uent

ial

anal

ysis

of8.

7%45

.8%

20.5

%2.

4%co

mpa

nyva

rianc

eW

eine

ran

dR

etur

non

asse

tspe

rR

egre

ssio

nco

mbi

ned

43.9

%E

xpla

nato

ryE

xpla

nato

ryE

xpla

nato

ryva

riabl

e:M

ahon

ey(1

981)

com

pany

with

sequ

entia

lan

alys

isva

riabl

es:

firm

size

,va

riabl

es:

indu

stry

annu

alG

NP

ofva

rianc

eca

pita

l/lab

or,

sale

s,in

dust

ryde

bt/e

quity

,%

ofco

ncen

trat

ion

earn

ings

reta

ined

Tho

mas

(198

8)R

etur

non

sale

spe

rS

eque

ntia

lan

alys

isof

5.7%

83.2

%N

otin

clud

ed5.

6%co

mpa

nyva

rianc

e

a CE

Oef

fect

ente

red

last

inal

lst

udie

s.O

ther

than

inW

eine

ran

dM

ahon

ey(1

981)

,ye

aref

fect

isen

tere

dfir

st,

follo

wed

byin

dust

ryef

fect

,fir

mef

fect

,a

ndth

enC

EO

effe

ct.

Wen

eran

dM

ahon

ey(1

981)

ente

ral

lva

riabl

esot

her

than

the

CE

Oef

fect

toge

ther

ina

regr

essi

on.

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

Does Corporate Strategy Matter? 13

once the mean effects of year, industry, and firmhave been accounted for.

The leadership effect represents a transient firm-level effect, in that the leadership effect is esti-mated based on average annual firm returns perCEO. Each of the firms included in these studieshas multiple CEOs. Although estimated corporateeffects in some of the variance decompositionstudies in Table 1 include transient effects(Schmalensee, 1985; Wernerfelt and Montgomery,1988; Kessides, 1990),11 many other studies esti-mate only stable corporate effects (e.g., Rumelt,1991; Roquebertet al., 1996; McGahan and Porter,1997, 1998; McGahan, 1997; Chang and Singh,1997). The latter reflect any effects of top man-agement only onaverage profitability over thetime period of a study. Top management effects inthe leadership studies capture additional transitoryeffects, based on variation in average firm prof-itability per CEO (Lieberson and O’Connor, 1972;Weiner and Mahoney, 1981).12 The firm effects inthe leadership studies are roughly equivalent to thesum of stable business and corporate effects inthe variance decomposition studies,13 whereas theleadership effect captures one type of transientfirm effect for both single-business and multiple-business firms.

Table 2 shows a range of leadership effects.The well-known initial study by Lieberson andO’Connor (1972) estimated substantial leadershipeffects of 14.5 percent of the total variance of

11 Bercerra (1997) includes an interaction term between yearand corporation in one part of the study, to capture corporateeffects that vary through time. The studies that include onlyone year of data (Schmalensee, 1985; Wernerfelt andMontgomery, 1988; Kessides, 1990) capture both stable effectsand transient effects for that year (Rumelt, 1991).12 Studies that cover multiple years will have some turnoverin top management. Most studies have found that the averagetenure for a CEO in a large U.S. company is 8–10 years,which suggests that on average 1/8 to 1/10 of all CEOs leaveoffice each year. Thus, even in a study of short duration(e.g., the 4-year period in Rumelt, 1991), executive turnovercan be substantial.13 The firm effects in the leadership studies are not identicalto the sum of the business and corporate effects in thevariance decomposition studies, because the leadership studiesassign eachfirm to a single industry, whereas the variancedecomposition studies generally assign eachbusinessto asingle industry. The firm effects in the leadership studies maypick up some residual industry-level effects due to individualcompany participation in more than one industry that businesseffects in the variance decomposition studies may or may notpick up, depending on the particular study in question.

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

profitability.14 The estimated leadership effects onthe variance of profitability in the other studiesrange from 6 to 44 percent. Since the studies(except perhaps Thomas, 1988) include somemultiple-business firms, the leadership effectshould include at least a portion of the transientcorporate effect. Surprisingly, none of the studieslisted in Table 1 refer to this earlier literature.

A simple look at Tables 1 and 2 suggests thatthe view that corporate effects are nil is notnecessarily correct. Instead, if we were to looksimply at the large range of estimates in thetables, we might conclude that we don’t knowwhat to think. As we explain in the next sections,however, a more detailed look at the data andmethods employed in the individual studies sug-gests that corporate effects are substantial. Inwhat follows, we first discuss the variancedecomposition studies shown in Table 1, and thenreturn to the leadership studies in Table 2.

SAMPLE SELECTION AND DATAISSUES

Table 1 shows that the variance decompositionstudies employ different dependent variables,explanatory variables, and data, and cover differ-ent time periods. The studies also differ in theirdefinitions of individual variables and utilize dif-ferent statistical techniques. Given the sensitivityof statistical analysis in general to all of thesesorts of factors, they are likely to account formany of the differences in the findings of thestudies. In what follows, we discuss some system-atic ways in which differences in the studiesproduce different estimates of corporate effects.We begin with a discussion of issues related toconstruction of the data samples that apply toboth the analysis of variance and variance compo-nents techniques used in the studies. Then weturn to issues related to the use of each sta-tistical technique.

Inclusion and exclusion of single-business firms

One of the most important factors that has animpact on the size of the estimated corporate

14 This study also estimated smaller leadership effectsassociated with the dollar value of sales and profits (7.5%and 6.5% respectively).

14 E. H. Bowman and C. E. Helfat

effect has to do with the inclusion or exclusionof single-business firms, which is reflected inTable 1 in the number of businesses per firm.Statistically, corporate effects derive from multi-ple-business firms. Many of the variancedecomposition studies that include single-businessfirms define corporate effects as zero in thosefirms (McGahan, 1997), because otherwise corpo-rate effects are difficult to distinguish from busi-ness effects.Thus, inclusion of single-businessfirms masks the corporate effect: the larger theproportion of single-business firms in a sample,the smaller is the estimated corporate effect. Con-versely, when a study excludes single-businessfirms, the estimated corporate effect rises.

As empirical confirmation, we point to thelarger corporate effect of 18 percent found byRoquebertet al. (1996), who excluded single-business firms,15 as compared with a corporateeffect of 4.3 percent estimated by McGahan andPorter (1997). Both of these studies used Compu-stat data, but McGahan and Porter (1997)included single-business firms, which compriseda majority of the businesses in their sample.Additional evidence comes from a separate andlater study by McGahan and Porter (1998) thatexcluded single-business firms from one of manysubsamples of data, for purposes of comparisonwith the results of Roquebertet al. (1996). McGa-han and Porter (1998) found that exclusion ofsingle-business firms increased the estimatedcorporate effect by 10 percentage points, from13.7 to 23.7 percent (with a drop in the estimatedbusiness effect of similar magnitude and littlechange in the estimated industry effect).16

Thus, an estimated corporate effect in a samplethat has a large proportion of single-business

15 The only other study to include only multiple-businessfirms also found non-negligible corporate effects of between5 and 11 percent (Bercerra, 1997). Since the study definedbusinesses very broadly as large geographic areas of theworld, as discussed in the following section, these numbersmay understate corporate influence on profitability.16 The number of businesses in a firm also may affect theestimated corporate effect in another way: the greater thenumber of businesses within a single firm, the lower thelikely effect of a corporation on any single business (perhapsbeyond some small number of businesses). A corporationthat has a large number of businesses may delegate moreresponsibility to individual businesses than does a firm thathas fewer businesses. Roquebertet al. (1996) and McGahanand Porter (1998) provide evidence that the estimated corpo-rate effect falls as the average number of businesses in asample increases beyond two or three.

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

firms may tell us little about whether corporateinfluence and corporate strategy matter to firmsfor which this is relevant, i.e., for multiple-business firms. In studies that include single-business firms, a negligible or small corporateeffect may reflect the proportion of single-business firms in the sample.

Definition of industry and business

The inclusion or exclusion of single-businessfirms has implications for a second issue thataffects estimation of the corporate effect: breadthof industry definition. In the variance decomposi-tion studies, the definition of a business dependson the definition of an industry, because thestudies identify each business in a firm as belong-ing to one particular industry.17 A broad definitionof an industry in terms of product scope thereforeimplies a broad definition of an individual busi-ness within a firm. Additionally, many of thestudies utilize data that define a business asallof the operations of a company in a single indus-try. As a result, the more broadly a study definesan industry and a business, the fewer the numberof businesses per firm, and the larger the numberof single-business firms in the sample than wouldresult with a narrower industry definition.Thus,a broad definition of industry makes it moredifficult to discern corporate effects, in partbecause the sample contains a greater proportionof single-business firms that dampen the estimatedcorporate effect.

Most of the variance decomposition studiesdefine an industry based on 4-digit StandardIndustrial Classification (SIC) codes in the Com-pustat business segment or Trinet/EIS data, orbased on line of business classifications in theFederal Trade Commission (FTC) data. SIC codesinclude broad 2-digit classifications of productmarkets, more narrow 3-digit classifications, andeven narrower 4-digit classifications. TheTrinet/EIS data contain the most precise infor-mation about the industries in which firms oper-ate, since the data include 4-digit SIC codesassigned to individual plants within companies.The Compustat business segment data containless precise information, since firms often identify

17 Bercerra (1997) instead defines a business as all of acompany’s operations in a broadly defined geographic areaof the world.

Does Corporate Strategy Matter? 15

operations in several 4-digit SIC code industriesas a single business (McGahan and Porter, 1997).Variance decomposition studies that rely on Com-pustat data generally use the primary SIC codefor each business.

In the FTC data, the individual line of businessclassifications vary between approximately the 3-digit and the 4-digit SIC code level (Ravenscraft,1983). Because the FTC data define a singlebusiness as all company operations in one lineof business, these data combine into one businessall business units within a firm that participate ina single industry (e.g., GM’s several autodivisions). In contrast, Compustat allows a com-pany to report more than one business in the sameSIC code industry (although many companies inCompustat do equate one set of SIC codes witha single company business).

Chang and Singh (1997) point out that whena variance decomposition study defines industriesand businesses broadly, some cross-businessinfluences that occur within a broadly definedbusiness will be attributed to business rather thancorporate effects. Only two studies have empiri-cally examined the sensitivity of results to pre-cision in industry definition. Chang and Singh(1997) used the Trinet data to show that definitionof industry and business at the narrower 4-digitSIC code level yields corporate effects that are 4–7 percentage points greater than corporate effectsestimated using broader 3-digit SIC codes. As analternative approach, using the FTC data, Foxetal. (1997) applied simulation techniques to con-struct industries defined more narrowly than theFTC lines of business. Foxet al. (1997) foundthat incorporating more narrowly defined indus-tries into a variance components analysis causedthe corporate effect to increase from 1.5 to 8.2percent in the final run of the simulation.Byimplication, studies that contain broadly definedindustries and businesses, for example based onthe Compustat and FTC data, underestimatecorporate influence on profitability.

STATISTICAL APPROACHES

The variance decomposition studies in Table 1use two main statistical techniques to decomposethe variance of profitability or market share:sequential analysis of variance (often usingregression methods) and variance components

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

analysis. Some studies employ both techniquesand others use just one, the choice of whichvaries. Next we discuss issues specific to eachmethodology (with supplementary technicalfootnotes).

Analysis of variance

In analysis of variance, a researcher typicallyestimates a null regression model of no effectson the dependent variable other than a constantterm, and then progressively adds variables thatrepresent each effect in the model. (Some of thestudies have large numbers of observations, andtherefore use alternate methods to derive least-squares estimates.) After adding each set of vari-ables, the researcher calculates the increment tothe adjustedR2 of the regression, as an unbiasedestimate of the fraction of variance ‘explained’(Schmalensee, 1985). The models often includedummy variables for each industry, each business,and each corporation. Some of the studies replacethe individual business dummy variables withmarket (or asset) shares for individual businesses(Schmalensee, 1985; Kessides, 1987; Wernerfeltand Montgomery, 1988: Kessides, 1990; McGa-han, 1997), or replace the corporate dummy vari-ables with a measure of corporate focus designedto capture the extent of relatedness in diversifi-cation (Wernerfelt and Montgomery, 1988;McGahan, 1997).

As in all hierarchical regression, the order ofentry of the sets of dummy variables can havea large impact on the results (Kennedy, 1985).Furthermore, the business-level dummy variablesare completely collinear with the corporate-leveldummy variables, since each corporation has adummy variable for every business within thefirm. As a result, if a regression that includesboth sets of dummy variables enters the business-level variables first, these variables will captureall of the corporate effect. In recognition of thisfact, analysis of variance models that include bothbusiness and corporate-level dummy variables(rather than share or focus variables) enter thecorporate dummy variables prior to the business-level dummy variables.

The latter approach creates an opposite problemthat the corporate dummy variables may pick upsome of the variability associated with the busi-ness dummy variables. For example, althoughRumelt (1991) finds in his analysis of variance

16 E. H. Bowman and C. E. Helfat

(estimated using an approach analogous to stan-dard regression techniques) that the incrementalcontribution to adjustedR2 for the corporationranges from about 11 to 17.5 percent (dependingon the sample of firms and the order of variableentry), he discounts these estimates because theymight arise from business effects not yet enteredinto the model. This conservative approach toreporting results, however, neglects useful infor-mation contained in analysis of variance estimatesof corporate effects.All else equal, a corporateeffect which is entered before the business effectand after year, industry, and industry-year inter-action effects provides an upper-bound estimateof the corporate effect, in that the estimate doesnot also reflect year and industry effects.18

Variance components

The alternative methodology of variance compo-nents estimation, sometimes termed a ‘randommodel’ of analysis of variance (e.g., Bowman andFetter, 1967), utilizes statistical techniques forestimating random effects rather than fixed (or‘stable’) effects estimated in standard analysis ofvariance. Estimation of random effects incorpo-rates the assumption that each effect represents arandom sample of the true population effect, andthat each effect (whether a main or an interactioneffect) is independent of the other effects in themodel. Schmalensee (1985) used this techniqueto decompose the variance of business prof-itability into separate classes of effects (i.e.,components of variance), followed by Rumelt(1991) and others.

In a comprehensive critique of the approach,Brush and Bromiley (1997) show that differentdraws from the same underlying distribution ofeffects produce very different estimates. Brushand Bromiley (1997) further note that accurateestimation of variance components of profitabilityrequires adjustment for the number of industries,number of corporations per industry, and numberof businesses per corporation in each sample ofdata. With regard to the number of businesses

18 Note that this upper bound may be affected by factorsdiscussed earlier, such as inclusion or exclusion of single-business firms and broad definition of industries and busi-nesses. Additionally, as noted in a subsequent section oninteraction effects, the estimate generally will not reflectcorporate choices of industries in which to operate or corpo-rate influence on industry returns.

Copyright 2001 John Wiley & Sons, Ltd. Strat. Mgmt. J.,22: 1–23 (2001)

per firm, for different reasons we have previouslynoted the sensitivity of variance decompositionestimates of corporate effects (for both analysisof variance and variance components) to theinclusion or exclusion of single-business firms.

Interaction effects

The final statistical issue that we raise has to dowith interaction or covariance effects. FollowingRumelt (1991), most of the studies that havemultiple years of data include an effect for theinteraction between industry and year, to capturetransient industry effects that vary from year toyear.19 Of greater importance for our discussionof corporate effects, few studies include inter-action or covariance effects between corporationsand years or industries.20 We examine each ofthese possible interactions in turn.

First, few variance decomposition studies pro-vide estimates of corporate effects that fluctuatethrough time, for example by using a corporate-year interaction term.21 Most studies estimate only‘stable’ (i.e., fixed) corporate effects, whichreflect differences between corporations only inthe average of their returns over time. As a result,if corporations differ in the pattern of their returnsthrough time but nevertheless have the same aver-age return over time, a study that estimates onlythe stable portion of the corporate effect will findno corporate effect.

With regard to corporate–industry interactioneffects, only Schmalensee (1985), Rumelt (1991),and McGahan and Porter (1997) include a covari-ance term in their variance component analyses.(It often is difficult to include a corporate–indus-try interaction term separate from the businesseffect in studies that rely on analysis ofvariance.22) Schmalensee (1985) and Rumelt

19 McGahan and Porter (1997) use a somewhat differentapproach to remove transient industry effects, as well astransient business and corporate effects, from their estimates.20 Brush and Bromiley (1997) also suggest that it is importantto account for covariance of corporate and business effects,a complicated issue that is beyond the scope of this analysis.21 In Table 1, the exception is Bercerra (1997). Foxet al.(1997) and McGahan and Porter (1999) also estimate bothstable and transitory corporate effects.22 For example, the studies that use analysis of variance, havemultiple years of data, and rely on dummy variables (or anequivalent technique) for businesses and corporations, essen-tially estimate business effects as the corporate–industry inter-action (i.e., the intersection of industries within corporations)(see, for example, DeGroot, 1975; Bowman and Fetter, 1967).

Does Corporate Strategy Matter? 17

(1991) note that corporations that have greaterinfluence on their businesses also may have iden-tified and entered industries that are either moreprofitable or less profitable than the average;McGahan and Porter (1997) note that some indus-tries may have greater opportunities for corporateinfluence than others. Thus, the corporate–industry covariance term may reflect importantaspects of corporatestrategy. Although Schma-lensee (1985) and Rumelt (1991) found almostno effect of covariance between corporation andindustry, McGahan and Porter (1997) found anegative and non-negligible covariance effect ofa similar magnitude to their estimated corporateeffect. McGahan and Porter (1997) suggest thatthe negative covariance indicates that corporationshave a more positive influence in less profitableindustries, and by implication, a less positive (oreven negative) influence in more profitable indus-tries.

In sum, many of the analyses in Table 1 cannotor do not separately account for the covarianceor interaction effects of corporations with indus-tries or years. The corporate-year interaction cap-tures variation in corporate influence over time,and the covariance effect between industry andcorporation may reflect corporate choices ofindustries.As a result, omission of covariance orinteraction effects leads to an incomplete descrip-tion of the influence of corporations, and ofcorporate strategy in particular, on the varianceof profitability.

DISCUSSION