Mike McNamara Investor Day – May 2012

1

2

Executive Overview

• Extensive global footprint, manufacturing technologies and

services

• Growth business with structurally higher growth rates than

the GDP and the electronics industry

• Business transformation leading to optimized portfolio

generating less volatility and higher margins

• Sustainable business model generating strong free cash

flow and >20% ROIC

• Expanding operating margin to 3.5% this year

• Exceptionally well positioned for eco-system shifts

3

Flextronics Manufacturing

Austin, Dallas, Longview & Houston, TX

Milpitas, CA Asheville, Charlotte, Creedmoor, NC

Boeblingen & Paderborn, Germany

Dongguan, Ganzhou, Gushu, Huangtian, Shenzhen, Xixiang

& Zhuhai, China

Althofen, Austria

Kallang & Joo Koon Singapore

Columbia, SC

Northfield, MN

Aguascalientes, MX

Guadalajara, MX

Nogales, MX

Tijuana, MX Ramos Arizpe, MX

Manaus, Brazil

Sao Paulo, Brazil

Sorocaba, Brazil

Sarvar, Tab & Zala, Hungary Cork, Ireland

Arad, Migdal Haemek, Ofakim & Yavne, Israel

Tczew, Poland

Timisoara, Romania

Karlskrona, Sweden

Beregovo & Mukachevo, Ukraine Nanjing, Malu/Shanghai

& Suzhou, China

Chennai, India

Batam, Indonesia

Ibaraki, Japan

Bukit, Penang, PTP & Senai, Malaysia

Chengdu, China Juarez, MX

Treviso, Italy Valencia, CA

>100 Locations │ 25 Million Square Feet │ 200,000 Employees

3

4

Flextronics Global Services and Software

Austin & Laredo, TX

Milpitas, CA Raleigh, NC

Hong Kong & Shenzhen, China

Changi, Singapore

Memphis, TN

Louisville, KY

Guadalajara, MX

Sorocaba, Brazil

Budapest & Pecs, Hungary

Cork & Limerick, Ireland

Lodz, Poland

Dubai, UAE

Manchester & Swindon, UK

Istanbul, Turkey Shanghai, China

Bangalore & Chennai, India

Koriyama, Japan

Senai, Malaysia

Juarez, MX Milan, Italy

Toronto, Canada

Venray, Netherlands Pardubice,

Czech Republic

Delhi, India

Mumbai, India

>25 Locations │ 7 Million Square Feet │ 11,000 Employees

4

5

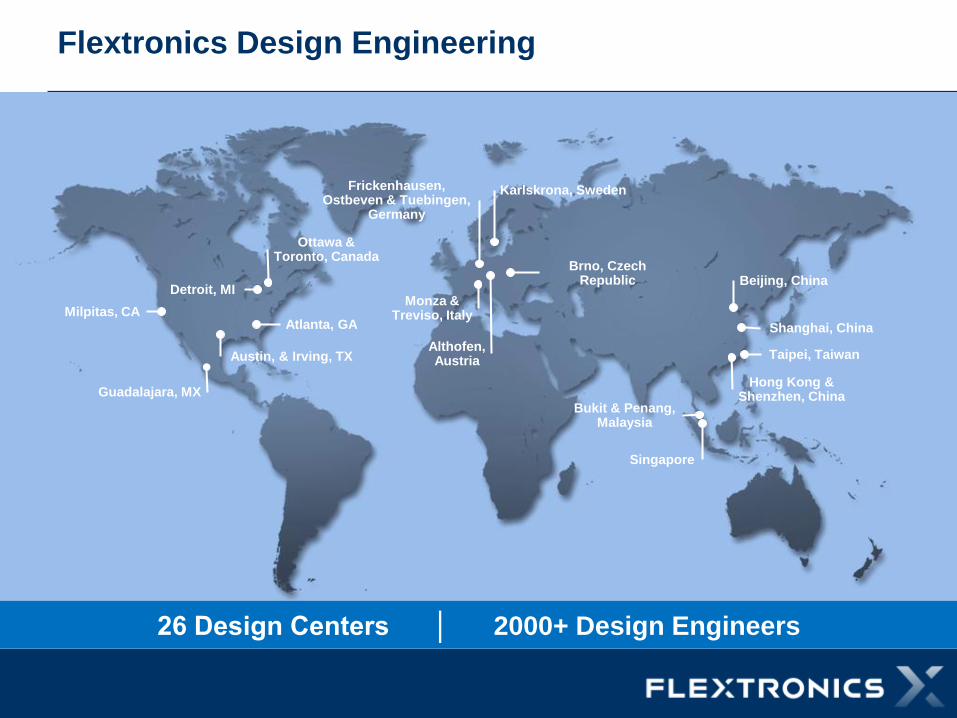

Flextronics Design Engineering

Austin, & Irving, TX

Milpitas, CA

Ottawa & Toronto, Canada

Frickenhausen, Ostbeven & Tuebingen,

Germany

Hong Kong & Shenzhen, China

Althofen, Austria

Singapore

Atlanta, GA

Detroit, MI

Guadalajara, MX

Brno, Czech Republic

Karlskrona, Sweden

Shanghai, China

Bukit & Penang, Malaysia

Monza & Treviso, Italy

Beijing, China

Taipei, Taiwan

26 Design Centers │ 2000+ Design Engineers

6

Broad Base of Manufacturing Technologies and Services

Total FY13E Revenue ~ $5B

Many ways to create competitive differentiation

• PCB

• Flexible Circuits

• Rigid/Flex Circuits

• Power Solutions

• Metal Fabrication

• Precision Machining

• Plastics

• Cables

• Advanced Displays

• Global Services

• Electronic Materials

• Advanced Manufacturing Services

7

Extensive Relationships with our Customers

Top Ten

Customers PCB Power Services PCBA

System

Integration Countries

Customer

HQ

A X X X X X 4 North America

B X X X 5 North America

C X X X X 5 China

D X X X 5 China

E X X X X X 16 North America

F X X X X X 9 North America

G X X X X 8 Europe

H X X X X X 6 North America

I X X X X 9 Europe

J X X X 4 North America

Sophisticated worldwide management system required to

support international OEMs

8

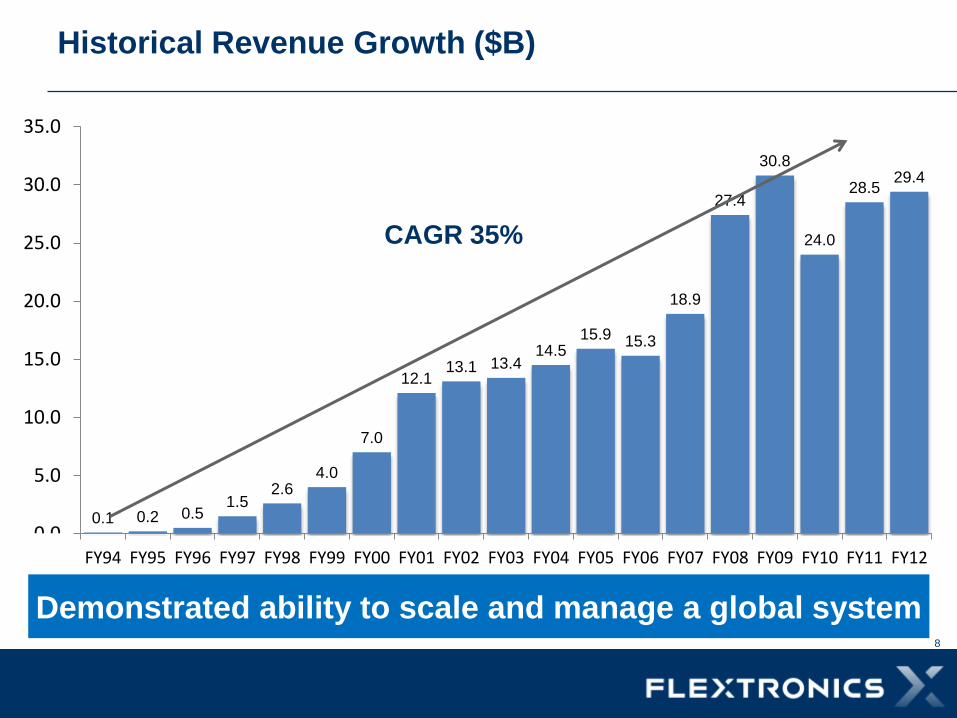

Historical Revenue Growth ($B)

Demonstrated ability to scale and manage a global system

0.1 0.2 0.5 1.5

2.6 4.0

7.0

12.1 13.1 13.4

14.5 15.9 15.3

18.9

27.4

30.8

24.0

28.5 29.4

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

FY94 FY95 FY96 FY97 FY98 FY99 FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

CAGR 35%

9

GDP, Electronics and EMS Growth Rates Last 10 Years

• Potential size is limitless

• Large outsourcing deals

continue

• New markets drive new

outsourcing revenue

• Economics of

outsourcing are

compelling

GDP

3.8%

Electronics

6.0%

EMS

8.6%

2%

4%

8%

6%

10%

A structurally higher growth Industry than the

GDP or electronics

Source: GDP- IMF, EMS – IDC, Electronics - Prismark

10

Our Four Primary Business Groups

High Reliability Solutions Medical, Automotive, Aerospace & Defense

Integrated Network Solutions Telecom, Networking and Server &

Storage

Industrial & Emerging Industries Energy Management, Application & Lifestyle,

Renewable Energy, Equipment & Automation

High Velocity Solutions Consumer, Mobile, Computing, Internet

Access Products

11

28%

11%

3%

58% 39%

14% 8%

39% ~45%

~15% ~10%

~30%

Our Portfolio Transformation

Actively manage the portfolio to adapt to market and

eco-system shifts and expand margins

FY07 FY12 FY13E

Revenue $18.9B Revenue $29.4B Revenue $26-$27B

High Velocity Integrated Network Industrial & Emerging High Reliability

12

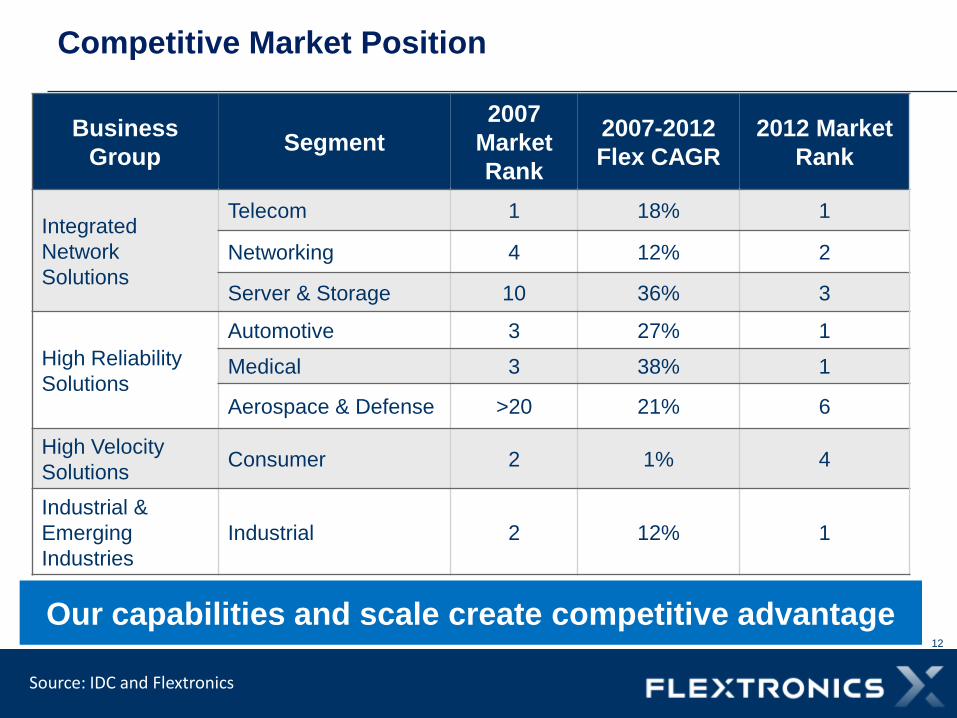

Business

Group Segment

2007

Market

Rank

2007-2012

Flex CAGR

2012 Market

Rank

Integrated

Network

Solutions

Telecom 1 18% 1

Networking 4 12% 2

Server & Storage 10 36% 3

High Reliability

Solutions

Automotive 3 27% 1

Medical 3 38% 1

Aerospace & Defense >20 21% 6

High Velocity

Solutions Consumer 2 1% 4

Industrial &

Emerging

Industries

Industrial 2 12% 1

Source: IDC and Flextronics

Our capabilities and scale create competitive advantage

Competitive Market Position

13

• Longer product life cycles

• Less forecast variability

• Higher margins

• Higher complexity

• Closer proximity to

customer’s design centers

required

• Regional manufacturing

footprint essential

Less competition

2012 Revenue ($B) Key Attributes

Leading position in low volume/high mix business

Low Volume/High Mix Revenue for the North American

Competitors

0

2

4

6

8

10

12

14

16

18

20

FLEX

$17.8B

14

Low Volume/High Mix Business Revenue ($M)

Steady, predictable growth

-

5,000

10,000

15,000

20,000

25,000

FY10 FY11 FY12 FY'13E*

CAGR 10.4%

FY13E

15

0

200

400

600

800

1000

1200

FY07 FY08 FY09 FY10 FY11 FY12 FY13E

Flextronics Power

• 4th largest power supply

company

• Innovative patented

technology for high

efficiency servers,

chargers and adapters

• 3 dedicated manufacturing

sites – final factory closure

complete in the September

quarter

• Expect margin expansion

in the second half of FY13

Revenue ($M) Differentiators

77% CAGR

16

Multek

• Invested in complex and

mobile PCBs, and flex/rigid

flex circuits

• Highly diversified:

- No Customer > 10%

- Top 50% of revenue is

spread across 15

customers

• Strong growth forecasted this

year based on state of the art

manufacturing facilities

• Expect margin expansion in

the second half of FY13

Revenue ($M) Differentiators

0

200

400

600

800

1000

1200

FY07 FY08 FY09 FY10 FY11 FY12 FY13E

6.5% CAGR

17

Flextronics Power Revenue ($M) Multek Revenue ($M)

These are very valuable assets that are not reflected in

our stock price today

0

200

400

600

800

1000

1200

FY07 FY08 FY09 FY10 FY11 FY12 FY13E

77% CAGR

0

200

400

600

800

1000

1200

FY07 FY08 FY09 FY10 FY11 FY12 FY13E

6.5% CAGR

18

GAAP EPS

18

Quality of earnings has become exceptionally high

FY08 – Restructuring and Solectron Integration

FY09 – Goodwill impairment

FY10 - Restructuring, Aircent Investment and N/R Impairment

FY13E - GAAP Adjusted Consensus

-$0.31

-$0.16

-$0.67

$0.60

$0.12

$0.47

-$0.92

-$7.46

$0.03

$0.77 $0.70

$0.89

-$2.0

-$1.0

$0.0

$1.0

$2.0

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13E -$8.0

FY08 – Solectron Integration

FY09 – Goodwill impairment

FY10 - Restructuring and investment impairment

FY13E - GAAP Adjusted Consensus

GAAP EPS

19

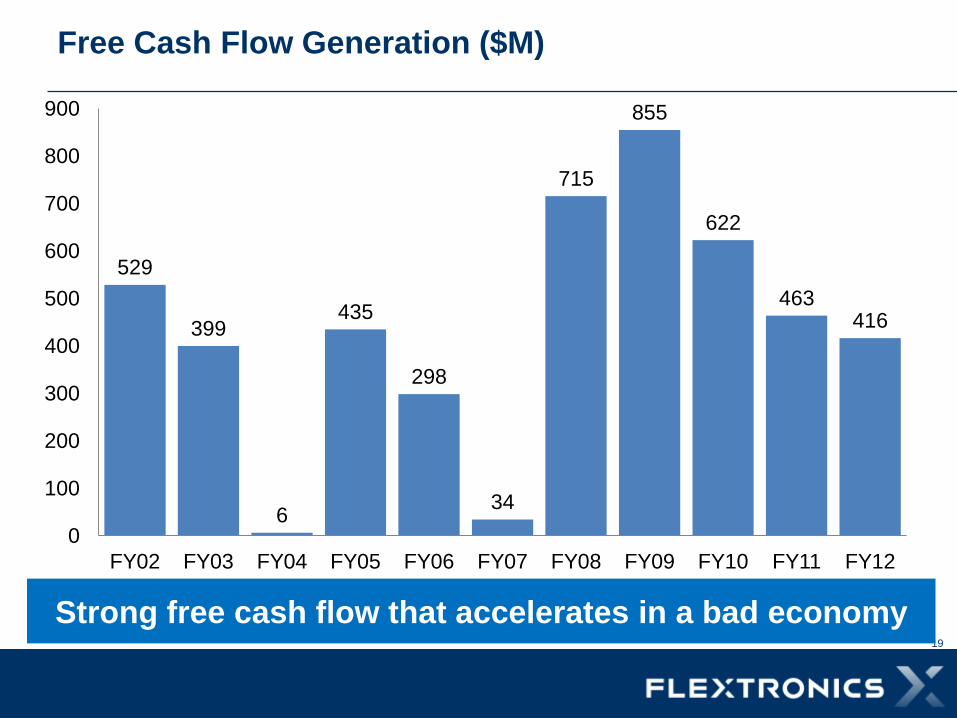

Free Cash Flow Generation ($M)

Strong free cash flow that accelerates in a bad economy

529

399

6

435

298

34

715

855

622

463 416

0

100

200

300

400

500

600

700

800

900

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

20

Key Ecosystem

Shifts

Flex Competitive Position

and Response

Large scale manufacturing sites in Malaysia, India, Indonesia,

Mexico, Brazil, Ukraine and Eastern Europe, employing more

than 75,000 people

Rising Manufacturing

Costs in China

Increasing Regulation

Driving Regional

Manufacturing

Broadest footprint outside of China and greater than any North

America or Taiwanese competitor

Product Convergence

Requiring Multiple

Technologies

Manufacture the largest and most diverse set of products in the

world

End to End Supply

Chain Services

Innovative development of end-to-end supply chain software

tools for customer intelligence leveraging analytics

Mobility and the Cloud Broad expertise in products, design engineering and product

technologies for mobile, server, storage, telecom and networking

Outstanding competitive position for the future

21

Conclusion

• Well positioned with scale, capabilities and cost

structure to win

• Operating a product portfolio with longer product life

cycles, less forecast variability and higher margins

• Generating strong free cash flow

• Fundamentally structured to achieve 3.5% operating

margin this fiscal year

• Well positioned for eco-system shifts

Recommended