International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

123

CORPORATE GOVERNANCE IN AUTOMOBILE

INDUSTRY IN INDIA

DR. PRIYANKA KAUSHIK SHARMA

RAJDHANI COLLEGE, DEPTT.OF COMMERCE

UNIVERSITY OF DELHI

_____________________________________________________________________________________

ABSTRACT

The present study seeks to examine critically the governance practice and to evaluate the needs

of corporate governance in the Auto Industry in India. The study has been made to evaluate the

state of compliance of the key governance parameter in Auto Sector in line with the statutory and

non-mandatory requirements stipulated by the Revised Clause 49 of (SEBI) Listing Agreement

as also the provisions required by the Companies Act, 1956.

The study is based on secondary data. For the purpose of analysis, various tools have been used

in the study like percentage growth, Compound Annual Growth Rate, simple average,

percentage, rank and paired t test. The study covers only listed companies of Automobile Sector.

The sample size of the study is 12 companies. An effort was made to collect the data of sample

companies over a period of five years (2003-04 to 2007-08).

The main objectives of the study are: To study the concept of corporate governance and check

the level of compliance of corporate governance codes by Auto Sector‟s companies in India.

Findings say that most companies adhere to compliance of mandatory requirements of corporate

governance codes and standards as per Clause 49 of Listing agreement. As far as non-mandatory

requirements are concerned companies are reluctant to abide by them.

KEYWORDS: Automobile Industry, Corporate Governance, Clause 49, Mandatory and Non-

Mandatory Requirements. _____________________________________________________________________________________

INTRODUCTION

Corporate governance is the current buzzword in corporate jargon. It has become a subject of

discussion in corporate boardroom, academic circles and government around the globe. High

profile corporate collapses in India (for example Harsad Mehta‟s securities scam, Ketan Parikh

scam, C R Bansal scam & most recent of all Satyam fraud) and overseas (for example; Qwest,

Global Crossing, Andersen, Enron & WorldCom) have shattered the dreams of various investors,

shocked the government and regulators alike and led to questioning the accounting practices of

statutory auditors and corporate governance norms. Unethical business conduct and behavior,

laxity on the part of board, failure of external audit, unfettered powers in the hands of the

Chairman/CEO, lack of transparency, inadequate disclosures, fraud, lack of proper internal audit

are the most common governance problems/flaws noticed in the collapses of all such corporate

failures in India, USA, UK and the other parts of the world.

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

124

What is Corporate Governance?

In simple terms, Corporate Governance is a system by which corporate entities are directed and

controlled. It potentially covers the entire gamut of activities having direct or indirect influence

on the financial health of the corporate entities. The concept of governance covers a broad range

of fields from economics and management to law and accounting, and thus varies depending on

the particular focus.

“The origin of the word governance can be found in Latin where „gubernare‟ means to rule, or to

steer. According to J. Wolfenshon, “Corporate governance is about promoting fairness,

transparency and accountability.” In the proceedings of the silver jubilee National Convention of

ICSI, “Corporate governance is not just corporate management; it is something much broader to

include a fair, efficient and transparent administration to meet certain well defined objectives. It

is a system of structuring, operating and controlling a company with a view to achieve long term

strategic goal to satisfy shareholders, creditors, employees, customers and suppliers and

complying with the legal and regulatory requirements, apart from meeting environmental and

local community needs. When it is practiced under a well laid out system, it leads to the building

of a legal, commercial and institutional framework and demarcates the boundaries within which

these functions are performed.”

Kumar Mangalam Birla Committee report on corporate governance states in the end note,

“Corporate governance extends beyond corporate laws. Its fundamental objective is not mere

fulfillment of the requirement of law but ensuring the board‟s commitment to managing the

company in a transparent manner for maximizing long-term shareholder value.”

The debate on corporate governance transcends in the realm of socio-economic-political and

cultural environment. Hence, the model of corporate governance cannot be universal. As aptly

cautioned by Sir Adrian Cadbury, “Governance systems are not exportable”. They evolve in

different parts of the world in different contexts. Hence, they need to be adopted in context of

specific socio-economic-political and cultural context.

No literature on corporate governance would be completed without giving the reader an insight

into the actual ground realities of what happens in the corridors of power in the corporation. The

present study seeks to examine critically the governance practice and to evaluate the needs of

corporate governance in the Auto Industry in India. The study has been made to evaluate the

state of compliance of the key governance parameter in Automobile Industry in India in line with

the statutory and non-mandatory requirements stipulated by the Revised Clause 49 of (SEBI)

Listing Agreement as also the provisions required by the Companies Act, 1956.

Scope of the Study

It is imperative to study the applicability of corporate governance norms in all industrial sectors

of India. However, due to constraints imposed by non-availability of sufficient funds as well as

owing to the time required for the study of such massive magnitude, it was decided to confine the

study of corporate governance in Automobile Industry, in the hope that it may at least provide

indications, general directions and practices followed in respect of corporate governance in

Indian industry as a whole.

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

125

Objectives of the Study

Corporate Governance, whether applied to Auto Industry or any other corporate, is essential as it

provides incentives for management to act in ways that raise the firm‟s net present value and

assure shareholders an adequate return. The purpose of this study is to evaluate the need of

corporate governance in the expanding Auto Industry in India.

Research Questions

1) To what extent Indian Automobile Sector has accepted & implemented corporate

governance principles compared to norms?

2) Is there any difference in level of compliance of corporate governance norms before 2005

and after 2005?

Research Methodology

The study is based on secondary data, obtained from books, journals, reports of various

committees including famous Cadbury Committee (UK), Combined Code of Best Practices

(London Stock Exchange), Blue Ribbon Committee (USA), Euro Shareholders Corporate

Governance Guidelines, Smith Report (UK) on Audit Committee, Kumaramangalam Birla

Committee (India) and Sarbanes-Oxley (SOX) Act, 2002 in USA. The study has utilized

Prowess Database Package supplied by CMIE1, several publications of SIAM2, CII3, and annual

reports of DHI4 for obtaining basic data for research. Review of Annual Reports of various

Automobile companies, articles and newsletters available through electronic media are also the

major sources of secondary information.

Tools Used for Analysis

For the purpose of analysis, various tools are used in the study like percentage growth, CAGR5,

simple average, percentage, rank and paired t test. In order to ascertain how far sample

companies are compliant of governance standard a point value system has been applied, whereby

adequate weightage in terms of points provided to these governance parameter according to their

importance. Thereby each of these sample companies has been awarded points on key

parameters, which constitutes the governance process in a company. These key governance

parameters and the criterion for evaluation of governance standard have been selected on a 100-

point scale and are shown in appendix 3.

Sample Size

The study covers only listed companies of Automobile Sector, located in India. The sample size

of the study is 9 Auto sector Companies. Further the 12 Auto Companies are bifurcated into 3

two wheelers, 3 passenger cars, 3 commercial vehicles and 3 auto components. Sample

companies consist of only those companies, which feature in top 200 India‟s biggest companies,

ranking based on their turnover.

1 CMIE stand for the Centre for Monitoring Indian Economy, whose basic task is to collect and provide financial

data of the companies in a consolidated manner as presented in the Prowess Database Package. 2 Society of Indian Automobile Manufacturers(SIAM)

3 Confederation of Indian Industries(CII)

4 Department of Heavy Industry (DHI), Ministry of Heavy Industries and Public Enterprises

5 CAGR, Compound Annual Growth Rate.

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

126

Period of Study

An effort was made to collect the data of sample companies over a period of five years6 (2003-04

to 2007-08). It provides a sufficiently reasonable period for analyzing fundamental shifts in

governance culture in companies.

Review of Literature

Das, S.C. (2007) the present study critically examine the governance practices prevailing in the

corporate sector in India within the regulatory framework. He has conducted an empirical study

on four renowned Indian companies in the Information Technologies Industry viz., Infosys

Technologies Limited, Wipro Limited, TCS Limited and Satyam Computer Service Limited. The

study has been made to evaluate the state of compliance of key governance parameters in these

companies in line with the statutory and non-mandatory requirement of Clause 49 of the Listing

Agreement.

Findings: The result shows that the IT industry represented by these major companies scored

68.5 point out of 100. The highest score was obtained by Infosys and lowest was obtained by

Satyam.

Black, Bernard S. &Khanna, Vikramaditya S. (2007) studying the valuation effect of

corporate governance reforms is that most reforms affect all firms in a country. Thus, if share

prices move when governance reforms are announced, the price changes may reflect the reforms,

but could also reflect other new information. They address this identification issue by studying

India‟s adoption in 2000 of major governance reforms (Clause 49), a number of which resemble

and predate Sarbanes Oxley. Clause 49 requires, among other things, audit committees, a

minimum number of independent directors, and CEO/CFO certification of financial statements

and internal controls. The reforms were sponsored by the Confederation of Indian Industry (an

organization of large Indian public firms), applied initially to larger firms, and reached smaller

public firms only after a several-year lag. The difference in effective dates offers a natural

experiment: Large firms are the treatment group for the reforms. Small firms provide a control

group for other news affecting India generally. If investors consider the reforms to be valuable

(or more valuable for larger firms) large firms' share prices should react positively to reform

announcements, relative to small firms.

Mukherjee, Diganta&Ghosh, Tejamoy(2004-06) the agency problem of the problem due to the

separation of ownership and control, which is starkly manifested in the corporate sector, are

discussed in this literature. The conclusion seems to be that corporate governance is still in a

very nascent stage in the Indian industry. The decision and policy making is still taken mostly as

a routine matter. The management is also not yet on its feet and their operating decisions may be

more effected by culture and tradition rather than scientific optimization or sound business sense.

Among the institutional investors also, it seems that the FIIs are the most consistent in stock

6 „Year‟ in this study connotes financial year i.e. the period beginning from 1

st April of a particular year to 31

st

march of next year. CMIE database allows the user to adopt any dates as relevant for a year although income tax

requires adoption of financial year for all accounting purposes.

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

127

picking whereas the performances of the domestic institutional investors are sporadic and

volatile at best. This is also serious shortcoming on the part of the capital market, not being able

to enforce better governance on the part of the directors or performance on the part of the

managers.

Bhattacharyya, Asish K &Rao, SadhalaxmiVivek (2005) examine whether adoption of Clause

49 predicts lower volatility and returns for large Indian firms. They compare a one-year period

after adoption (starting June 1, 2001) to a similar period before adoption (starting June 1, 1998).

The logic is that Clause 49 should improve disclosure, thus reduce information asymmetry, and

thereby reduce share price volatility. Share prices would increase when risk drops, but expected

returns would thereafter be lower. The authors find insignificant results for volatility (volatility is

lower post-adoption for both large and small firms, by similar amounts), and mixed results for

returns post-adoption returns are lower for the largest firms, but positive for a second set of large

firms which are also subject to Clause 49. (The authors also study whether firm betas change

after adoption of Clause 49. Their reasons for expecting a change in beta are unclear to us.)

Sareen, V.K. &Chander, Subbash (2003) in their paper has captured the glimpses of corporate

voluntary disclosure practices of the private sector in India. It focuses on studying both the item

wise and corporate wise disclosure of selected companies in the private sector. Annual reports of

50 companies (listed on BSE) for the year 1997-98 belonging to different age groups, listing

status, industries, sizes (turnover and shareholders‟ fund wise) and profitability levels constituted

the „sample‟ of the study. To conclude, they state that annual report is the most vital document

containing comprehensive information about a joint stock company. This document is present

more information to the users in a manner, which suits the requirement of corporate sector.

Though well managed companies are presenting statistical (financial and non-financial) and

other information but their style of presentation and method of accounting treatment and

reporting vary. Emphasis on corporate governance by accounting standards as issued by ICM

and amendments in the Companies Act, 1956 is likely to improve corporate disclosure. They are

hopeful that with more and more companies trying to be listed in foreign countries, disclosure

practice would improve to be in consonance with the international practice.

Jairus, Banaji&Mody, Gautam (2001)examine the issue of corporate governance in the

context of large private sector companies in India against a regulatory background that is

changing rapidly. The study highlights the ineffectiveness of boards in Indian companies, the

lack of transparency surrounding transactions within business groups, the divergence of Indian

accounting practices from international standards, and the changing role of, and controversy

surrounding, institutional shareholders. The authors argue that regulatory intervention needs a

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

128

much stronger definition of „independence‟ for directors, in line with best practice definitions

now adopted in the US and UK, as well as the mandatory introduction of nomination

committees. Finally, the presence of institutional nominees is a unique feature of Indian

corporate governance and there has been a powerful corporate lobby in favor of removing them

from boards. While this would reduce the accountability of Indian boards even further, the

reports argue that a more active approach to corporate governance on the part of institutional

investors requires larger changes in the nature of the FIs‟ ownership and control by government,

greater autonomy for institutional managers, and the active development of a market for

corporate control.

Evaluation of Corporate Governance Compliance

An attempt was made to analyze the compliance of Corporate Governance provisions in the

nineteen sample companies individually over a period of five years with respect to Clause 49 of

Listing Agreement. The analysis is mainly based on ten key areas that are: 1) Statement of the

Company‟s Philosophy on Code of Governance, 2) Board of Directors / Board Issues,

3)Statutory/ Mandatory Board Committees, 4) Non-Mandatory Board Committees, 5)Disclosures

and Transparency, 6)General Body Meetings, 7) Means of Communication and General

Shareholder Information, 8) CEO & CFO Certification, 9) Compliance of Corporate Governance

and Auditors‟ Certificate and 10) Disclosure of Stakeholders‟ Interests.

In order to ascertain how far these companies have been compliant to governance standards a

point value system has been applied, whereby adequate weightage in term of points has been

provided to these conditions according to their importance. Accordingly, each of these sample

companies has been awarded points on key parameters, which constitutes the governance process

in company. These key governance parameters and the criterion for evaluation of governance

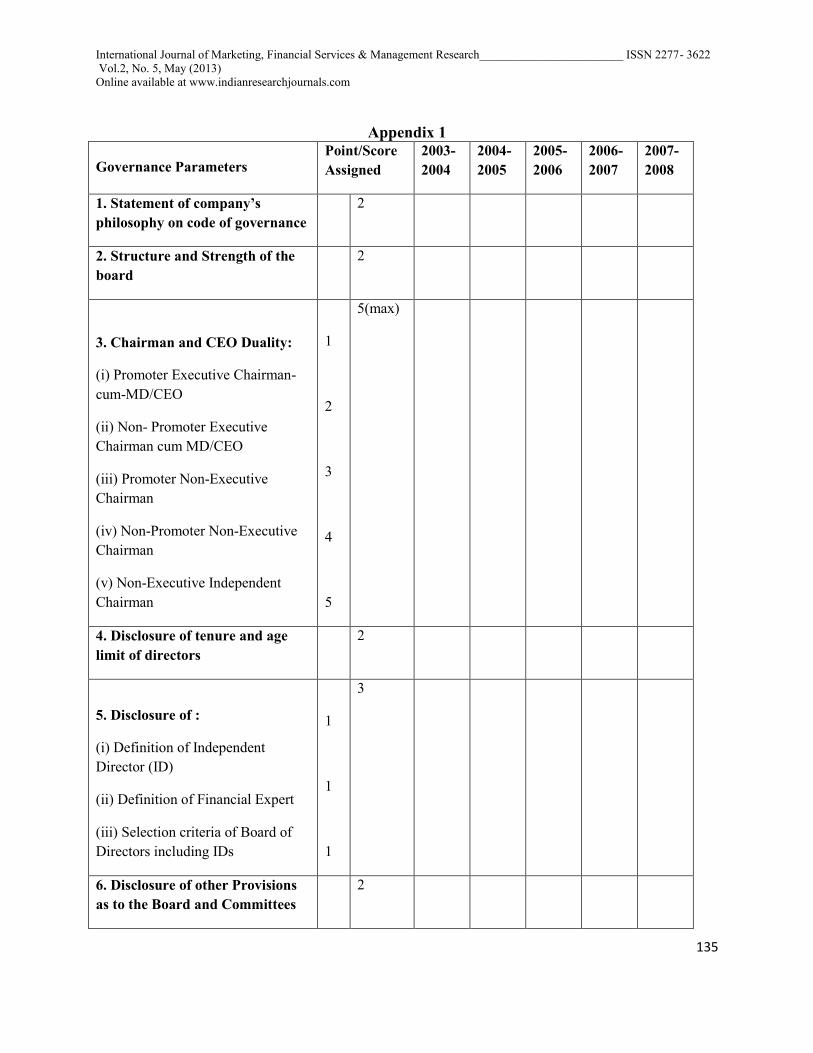

standard have been selected on a 100-point scale (Appendix 1).

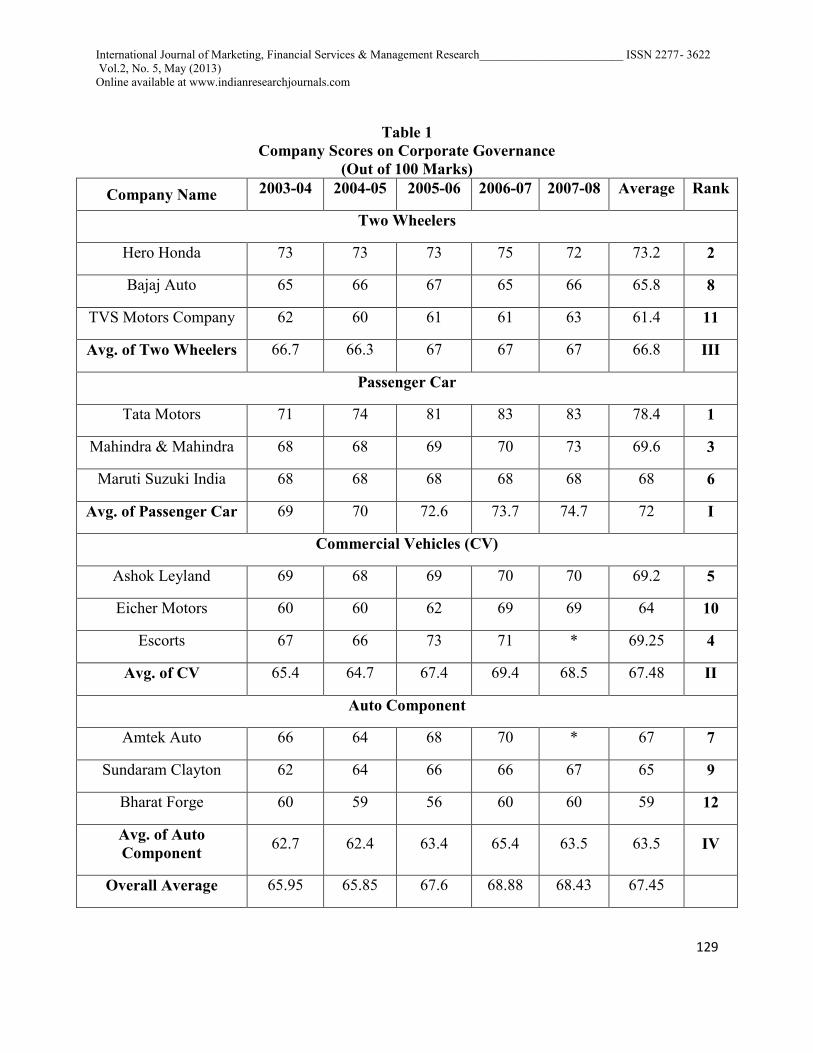

Table 1 shows the companies scores based on corporate governance out of 100 marks, average of

scores, and ranking based on corporate governance scores; Calculation of scores has been done

by using parameters as shows in Appendix 1.

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

129

Table 1

Company Scores on Corporate Governance

(Out of 100 Marks)

Company Name 2003-04 2004-05 2005-06 2006-07 2007-08 Average Rank

Two Wheelers

Hero Honda 73 73 73 75 72 73.2 2

Bajaj Auto 65 66 67 65 66 65.8 8

TVS Motors Company 62 60 61 61 63 61.4 11

Avg. of Two Wheelers 66.7 66.3 67 67 67 66.8 III

Passenger Car

Tata Motors 71 74 81 83 83 78.4 1

Mahindra & Mahindra 68 68 69 70 73 69.6 3

Maruti Suzuki India 68 68 68 68 68 68 6

Avg. of Passenger Car 69 70 72.6 73.7 74.7 72 I

Commercial Vehicles (CV)

Ashok Leyland 69 68 69 70 70 69.2 5

Eicher Motors 60 60 62 69 69 64 10

Escorts 67 66 73 71 * 69.25 4

Avg. of CV 65.4 64.7 67.4 69.4 68.5 67.48 II

Auto Component

Amtek Auto 66 64 68 70 * 67 7

Sundaram Clayton 62 64 66 66 67 65 9

Bharat Forge 60 59 56 60 60 59 12

Avg. of Auto

Component 62.7 62.4 63.4 65.4 63.5 63.5 IV

Overall Average 65.95 65.85 67.6 68.88 68.43 67.45

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

130

Highest average Score is 78.4 and lowest average score is 59. Ranking 1 is given to TATA

Motors Ltd. while lowest ranking i.e. ranking 19 is given to Bharat Forge Ltd. Within the Auto

sector passenger car segment performed best in corporate governance while auto component

segment performed worst. 2006-07 year recorded highest score indicating best corporate

governance while year 2004-05 recorded lowest overall average score reflecting low level of

compliance of corporate governance norms.

The analysis of annual reports from year 2003-04 to 2007-08 for checking the level of

compliance of corporate governance provisions of 12 sample companies representing Auto

Sector reveals that the majority of companies are complying with the condition of Corporate

Governance as stipulated in the Clause 49 of the Listing Agreement. All the companies are

fulfilling most of the mandatory requirements of Clause 49 of the Listing Agreement. Therefore,

in order to check the actual level of compliance of Corporate Governance provisions in

company, it becomes necessary to look into compliance of non-mandatory requirements, besides

just relying on the compliance of mandatory requirements of Clause 49 of the Listing

Agreement.

However, few companies are not complying even with the mandatory requirements of Clause 49

also. Like Bajaj Auto and Sundaram Ltd have not complied with the requirement regarding

minimum number of Audit Committee meetings held during the year 2007-08 and 2003-04

respectively. Similarly, 5 companies namely Eicher motors Ltd, Escorts Ltd, Ashok Leyland

Ltd, TVS Motors ltd, Amtek Auto Ltd, are not fulfilling some of the mandatory requirements

relating to Audit Committee concerning to literacy and financial expertise of the committee

members and information about participation of head of finance, statutory auditors, chief internal

auditor and other invitees in the committee meetings.

The highest percentages (75%) of independent directors were found in Eicher Motors Ltd.,

lowest 30% was found in Ashok Leyland Ltd. Hero Honda Ltd, and Ashok Leyland Ltd failed to

comply with the minimum statutory requirement for independent directors in the year 2007-08

and 2004-05 respectively. The largest percentage (92%) of non-executive directors was found in

Ashok Leyland. All the companies complied with the minimum number of meetings held in a

year required as per Clause 49 and Companies Act 1956 also.

Tata Motors was the sole company to provide training to board members and to follow the

procedures for evaluation of non-executive directors and also adopted whistle blower policy.

Paired-Difference “t” test (Dependent Sample)

The matched pairs or related „t‟ test is used when testing for significant differences between two

samples which are „related‟. When two observations are related to each other, then in such

situation concerned with the “difference” between the pair of related observations. The

distribution of these paired differences is assumed to be normal. Paired t-test is used where the

sample sizes are equal, i.e., n1 = n2= n3 and sample observations are not completely independent

but are dependent in pairs.

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

131

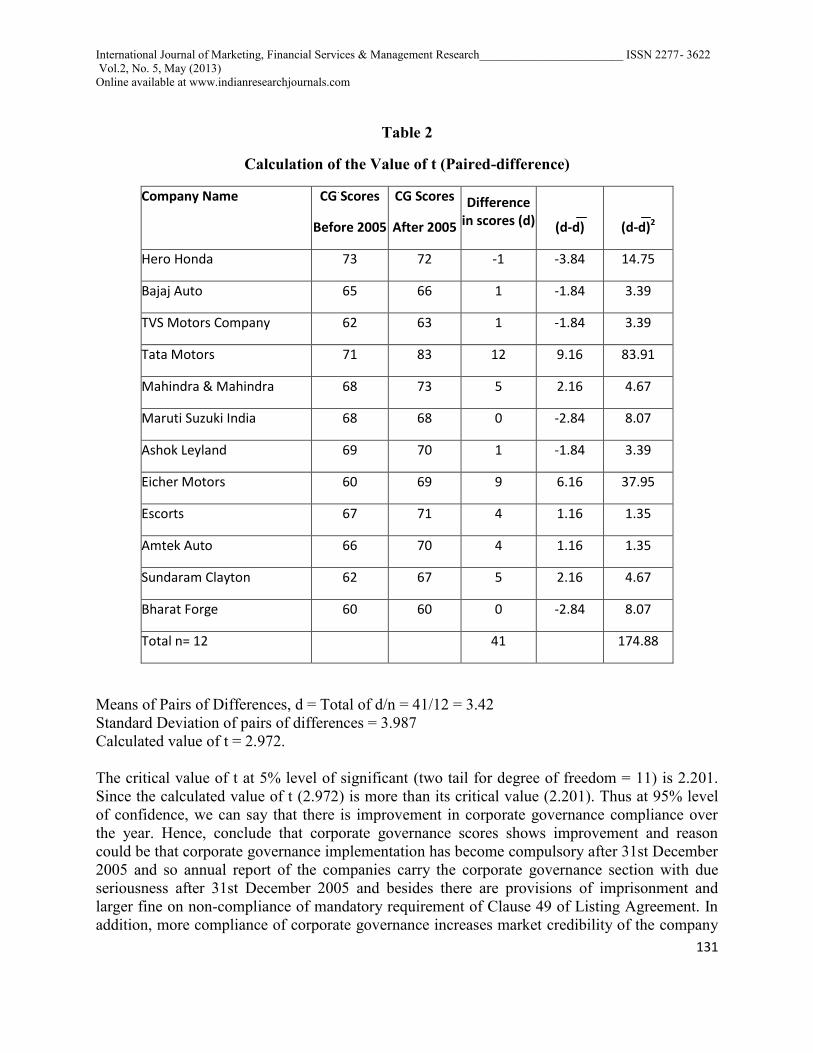

Table 2

Calculation of the Value of t (Paired-difference)

Company Name CG Scores

Before 2005

CG Scores

After 2005

Difference in scores (d)

(d-d)

(d-d)2

Hero Honda 73 72 -1 -3.84 14.75

Bajaj Auto 65 66 1 -1.84 3.39

TVS Motors Company 62 63 1 -1.84 3.39

Tata Motors 71 83 12 9.16 83.91

Mahindra & Mahindra 68 73 5 2.16 4.67

Maruti Suzuki India 68 68 0 -2.84 8.07

Ashok Leyland 69 70 1 -1.84 3.39

Eicher Motors 60 69 9 6.16 37.95

Escorts 67 71 4 1.16 1.35

Amtek Auto 66 70 4 1.16 1.35

Sundaram Clayton 62 67 5 2.16 4.67

Bharat Forge 60 60 0 -2.84 8.07

Total n= 12 41 174.88

Means of Pairs of Differences, d = Total of d/n = 41/12 = 3.42

Standard Deviation of pairs of differences = 3.987

Calculated value of t = 2.972.

The critical value of t at 5% level of significant (two tail for degree of freedom = 11) is 2.201.

Since the calculated value of t (2.972) is more than its critical value (2.201). Thus at 95% level

of confidence, we can say that there is improvement in corporate governance compliance over

the year. Hence, conclude that corporate governance scores shows improvement and reason

could be that corporate governance implementation has become compulsory after 31st December

2005 and so annual report of the companies carry the corporate governance section with due

seriousness after 31st December 2005 and besides there are provisions of imprisonment and

larger fine on non-compliance of mandatory requirement of Clause 49 of Listing Agreement. In

addition, more compliance of corporate governance increases market credibility of the company

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

132

that also encourages company to become more transparent and accountable towards their

stakeholders.

Areas for Improvement

From the analysis of the annual reports of the nineteen companies, it appears that there is ample

scope for improvement in the level of corporate governance standards and quality of disclosures

to be practiced by these companies. In this perspective, we highlight some of the important areas

of governance in which these companies require to take appropriate action.

(i) Director attendance seemed to be less than satisfactorily which is a prerequisite to

effective corporate governance

(ii) Disclosure of tenure and age Limit of directors (executive, non-executive as well as

independent)

(iii) Transparency in disclosure whether the chairman of the company is the promoter or not

(iv) Disclosure of definition of independent director and financial expert

(v) Disclosure of selection criteria of non-executive and independent directors

(vi) Adequate disclosure of break up of „salary‟, „allowances‟, „perks‟, and „benefits‟ and

„other payments‟ to directors

(vii) Disclosure of remuneration policy

(viii) Disclosure of audit committee charter and publishing of audit committee report

(ix) Introducing of a system of conducting shareholders‟ survey for assessing their

satisfaction level and disclosure of survey results

(x) Publishing of risk management report

(xi) Disclosure of the report of remuneration committee in the corporate governance report

(xii) Non-mandatory requirements:

a) Audit qualification

b) Training of board members

c) Evaluation of non-executive directors

d) Whistle blower policy

(xiii) Establishment of non-mandatory committee of the board

a) Nomination committee

b) Health safety & environment committee

c) Ethics and compliance committee

d) Investment committee

e) Share transfer committee

Suggestions

The spirit in which corporate governance is taken matters a lot. Satyam‟s failure has become an

exciting case study of the biggest corporate governance failure. New York-listed Satyam did

everything by the rulebook. Along with dozens of others kinds of awards, Satyam has received

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

133

the World Council for Corporate Governance‟s Golden Peacock Award for excellence in

corporate governance not once but twice. It clearly point out corporate governance mechanisms

cannot prevent unethical activity by top management completely, but they can at least act as a

means of detecting such activity before it is too late. Some suggestions to improve corporate

governance in the country are:

1) First of all the compliance of corporate governance codes and standards should not just

be on paper rather needed to be present in sprit. Therefore, voluntary compliance by companies

is welcome in place of forced compliance of standards. Nevertheless, in the event of frauds

stringent enforcement of the existing regulation and legislative rules across different ownership

structures are required.

2) There is no substitute of ethics and integrity and there always exist company who commit

fraud and manipulate accounts to hide frauds, a case in point is Satyam Ltd. Therefore, all the

committees that are set up in a company should be impartial and ethical.

3) Many Indian companies retain their auditors for years, which results in „collusion‟

between promoters and auditors. The demand for auditor‟s rotation is gaining ground after

Satyam‟s Fiasco and it is time companies in India change auditors periodically.

4) There is a need to get company‟s internal audits reviewed by an outsider. Internal

auditors are employees of the firm who can never work against the management; an outsider has

no such obligation and therefore can do a fairer job.

5) There is a need to make the price sensitive information available to all other shareholders

in case of pledging of promoter shareholding.

6) The market regulator SEBI should review the practice of nominating independent

directors on a company board by the promoters, as this affects directors‟ independence.

Independent directors in many cases are handpicked by the promoters and in most cases they are

family friends.

7) Directors who guide the board should meet independent of management in times of crisis.

8) Board members may be constrained by certain information, which can lead to less

informed decisions, they should insist on additional data and also try to verify the information

provided for a decision making process.

9) There is also need to have a kind of whistle blower policy that empowers the ordinary

shareholders of companies to critically examine the decision of the companies, and if they feel

something wrong, complain to the government.

10) There is a need to have close supervision, greater accountability and disclosure of rating

methodologies of rating agencies.

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

134

11) In case of any non-compliance with the mandatory requirements of Clause 49 of the

Listing Agreement, the regulator could impose punitive measures. This could also to de-listing of

the companies‟ stock from the stock exchanges.

12) There is a need to have in place longer imprisonment provision and larger fines for

willful financial mis-statements and fraudulent acts on the part of senior management like have

in Sarbanes-Oxley (SOX) Act.

13) Lastly, companies should consider non-mandatory requirements as important as the

mandatory requirements and not adopt a policy of fulfilling mandatory requirements just to keep

law of land and subsequent penalties at bay for non-compliance.

To summarize it can be said that most companies adhere to compliance of mandatory

requirements of corporate governance codes and standards as per Clause 49 of Listing

agreement. As far as non-mandatory requirements are concerned companies are reluctant to

abide by them.

Refrences

1) Bhattacharyya, Asish K. and RaoSadhalaxmiVivek, 2005, „Economic Impact of

„Regulation on Corporate Governance: Evidence from India‟.

2) Black, Bernard S. &Khanna, Vikramaditya S., 2007, „Can Corporate Governance

Reforms Increase Firms‟ Market Values: Event Study Evidence from India‟.

3) Das, S.C., 2007, „Corporate Governance Standards and Practices in Information

Technologies Industry in India‟, The Management Accountant, Volume 42 No. 8.

4) Economics Times, ET 500 October 2008, pp. 30 - 45.

5) Jairus, Banaji and Mody, Gautam, 2001 „Corporate Governance and the Indian Private

Sector‟, QEH Working Paper Series no 73, University of Oxford.

6) Mukherjee, Diganta and Ghosh, Tejamoy, 2004-06 „An Analysis of Corporate

Performance and Governance in India: Study of Some Selected Industries‟, Diganta,

Indian Statistical Institute, Kolkata, India.

7) Sareen, V.K. and Dr. Chander, Subbash, 2003, „Corporate Disclosure Practices- An

Empirical Study of Corporate Governance‟, pp. 145-158.

8) Sharma, J.P., 2008, “Satyam- A case of Unethical Conduct and Fake Audit”, The Indian

Journal of Commerce, Vol. 62, pp. 80-89.

9) Wolfenshon, J., 21 June 1999, President of World Bank, Corporate Governance, The

Financial Times.

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

135

Appendix 1

Governance Parameters Point/Score

Assigned

2003-

2004

2004-

2005

2005-

2006

2006-

2007

2007-

2008

1. Statement of company’s

philosophy on code of governance

2

2. Structure and Strength of the

board

2

3. Chairman and CEO Duality:

(i) Promoter Executive Chairman-

cum-MD/CEO

(ii) Non- Promoter Executive

Chairman cum MD/CEO

(iii) Promoter Non-Executive

Chairman

(iv) Non-Promoter Non-Executive

Chairman

(v) Non-Executive Independent

Chairman

1

2

3

4

5

5(max)

4. Disclosure of tenure and age

limit of directors

2

5. Disclosure of :

(i) Definition of Independent

Director (ID)

(ii) Definition of Financial Expert

(iii) Selection criteria of Board of

Directors including IDs

1

1

1

3

6. Disclosure of other Provisions

as to the Board and Committees

2

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

136

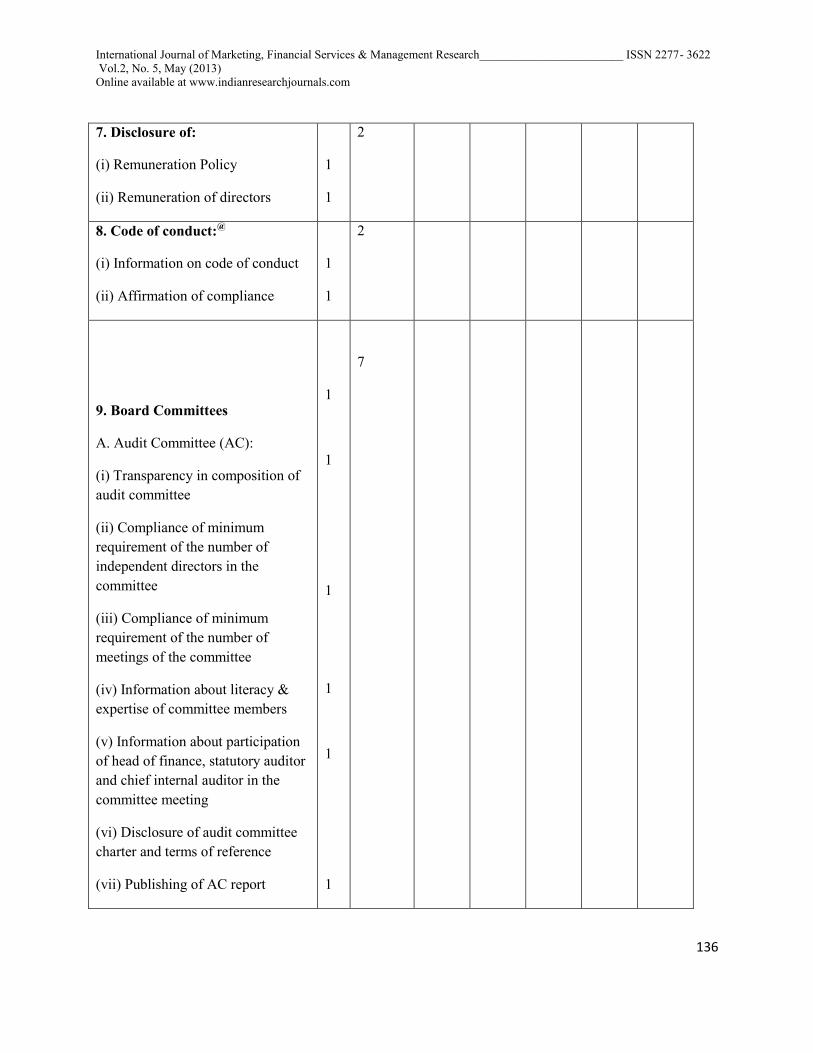

7. Disclosure of:

(i) Remuneration Policy

(ii) Remuneration of directors

1

1

2

8. Code of conduct:@

(i) Information on code of conduct

(ii) Affirmation of compliance

1

1

2

9. Board Committees

A. Audit Committee (AC):

(i) Transparency in composition of

audit committee

(ii) Compliance of minimum

requirement of the number of

independent directors in the

committee

(iii) Compliance of minimum

requirement of the number of

meetings of the committee

(iv) Information about literacy &

expertise of committee members

(v) Information about participation

of head of finance, statutory auditor

and chief internal auditor in the

committee meeting

(vi) Disclosure of audit committee

charter and terms of reference

(vii) Publishing of AC report

1

1

1

1

1

1

7

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

137

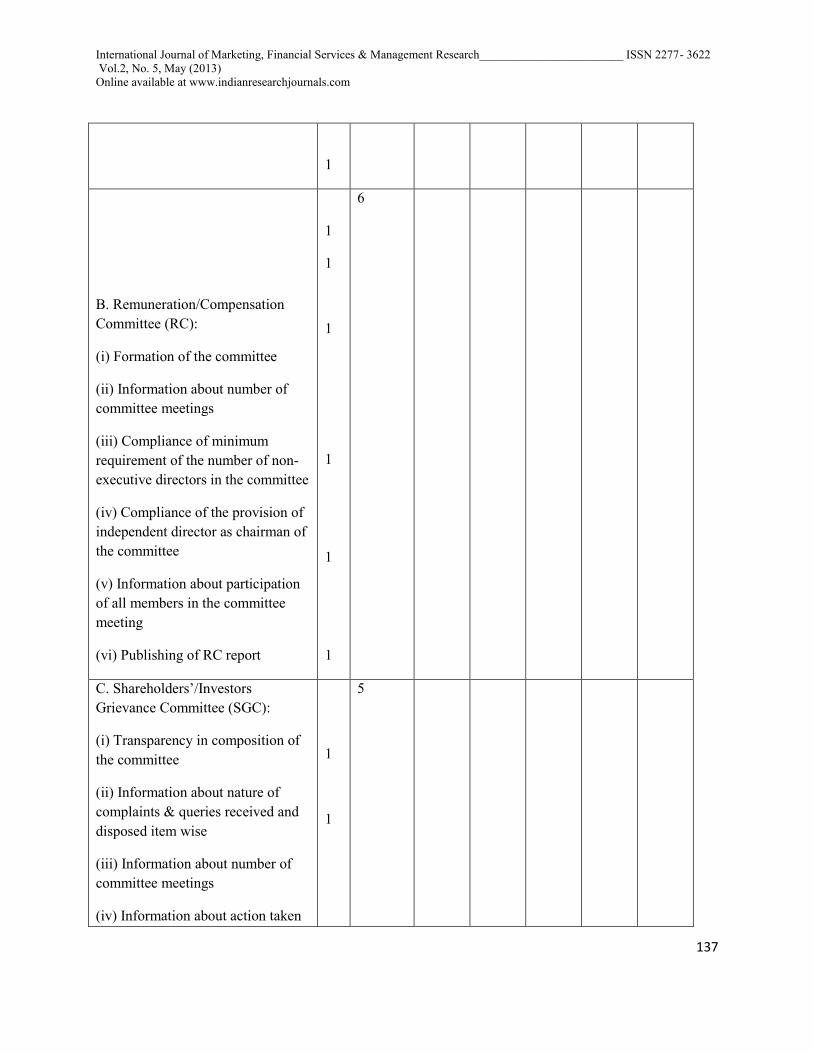

1

B. Remuneration/Compensation

Committee (RC):

(i) Formation of the committee

(ii) Information about number of

committee meetings

(iii) Compliance of minimum

requirement of the number of non-

executive directors in the committee

(iv) Compliance of the provision of

independent director as chairman of

the committee

(v) Information about participation

of all members in the committee

meeting

(vi) Publishing of RC report

1

1

1

1

1

1

6

C. Shareholders‟/Investors

Grievance Committee (SGC):

(i) Transparency in composition of

the committee

(ii) Information about nature of

complaints & queries received and

disposed item wise

(iii) Information about number of

committee meetings

(iv) Information about action taken

1

1

5

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

138

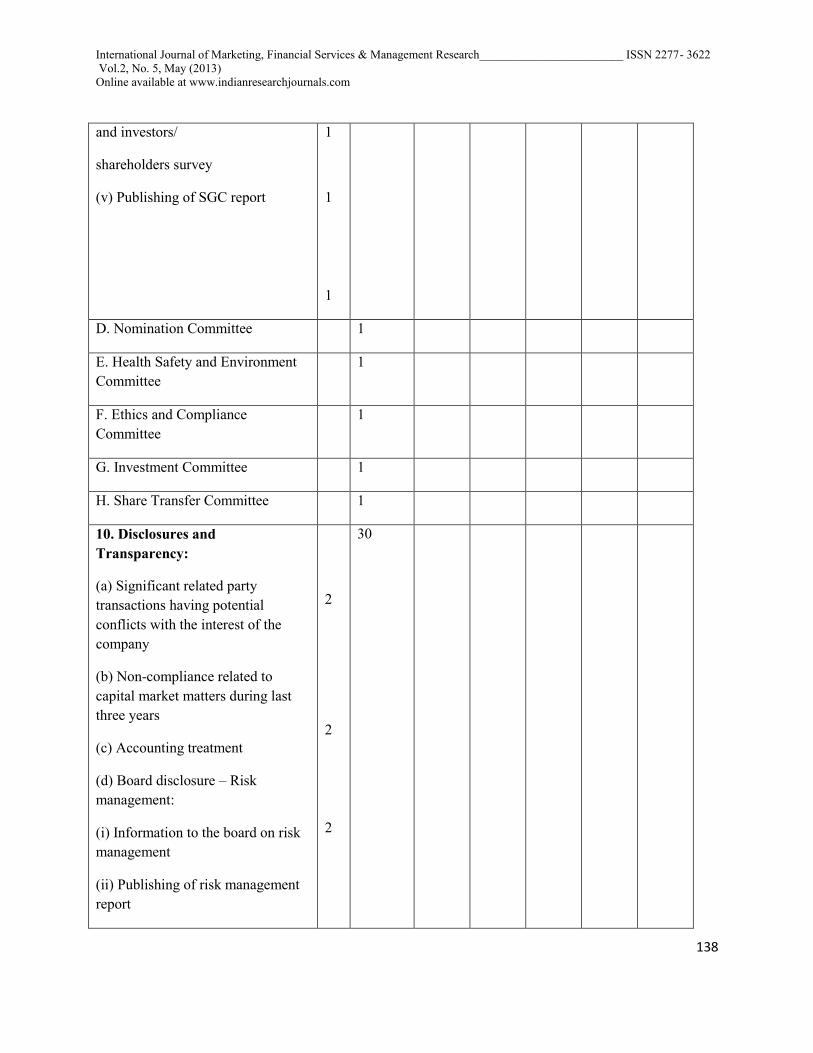

and investors/

shareholders survey

(v) Publishing of SGC report

1

1

1

D. Nomination Committee 1

E. Health Safety and Environment

Committee

1

F. Ethics and Compliance

Committee

1

G. Investment Committee 1

H. Share Transfer Committee 1

10. Disclosures and

Transparency:

(a) Significant related party

transactions having potential

conflicts with the interest of the

company

(b) Non-compliance related to

capital market matters during last

three years

(c) Accounting treatment

(d) Board disclosure – Risk

management:

(i) Information to the board on risk

management

(ii) Publishing of risk management

report

2

2

2

30

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

139

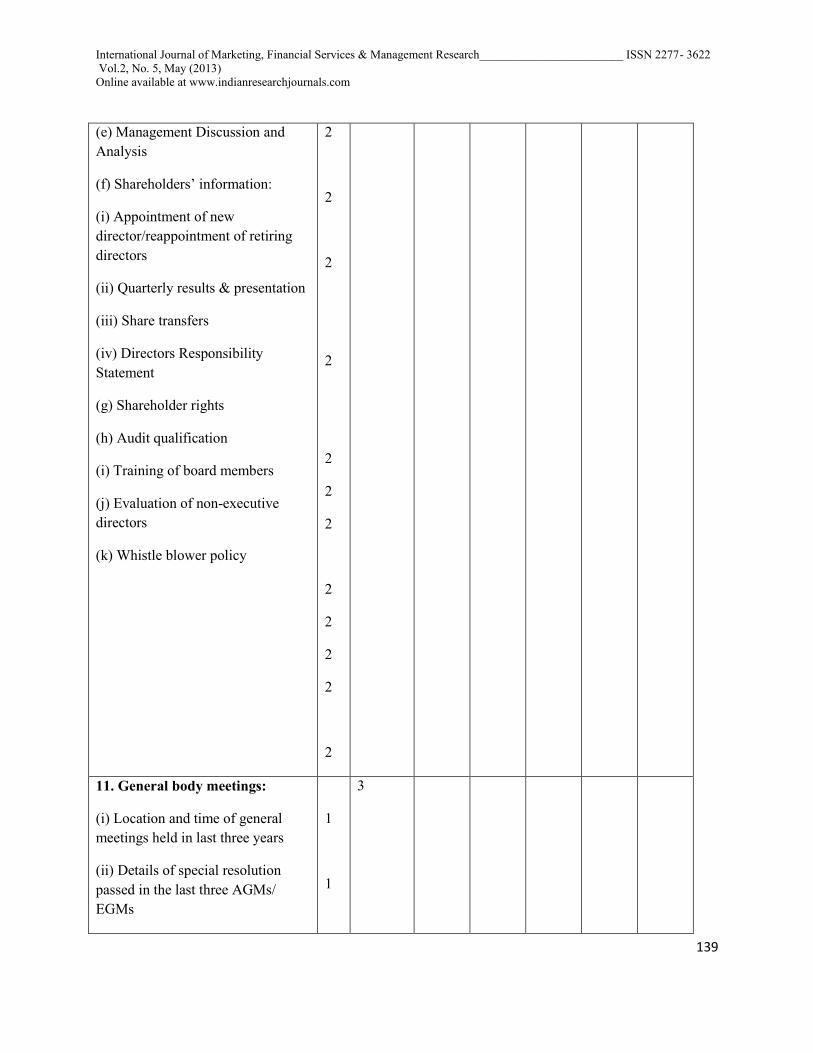

(e) Management Discussion and

Analysis

(f) Shareholders‟ information:

(i) Appointment of new

director/reappointment of retiring

directors

(ii) Quarterly results & presentation

(iii) Share transfers

(iv) Directors Responsibility

Statement

(g) Shareholder rights

(h) Audit qualification

(i) Training of board members

(j) Evaluation of non-executive

directors

(k) Whistle blower policy

2

2

2

2

2

2

2

2

2

2

2

2

11. General body meetings:

(i) Location and time of general

meetings held in last three years

(ii) Details of special resolution

passed in the last three AGMs/

EGMs

1

1

3

International Journal of Marketing, Financial Services & Management Research________________________ ISSN 2277- 3622

Vol.2, No. 5, May (2013)

Online available at www.indianresearchjournals.com

140

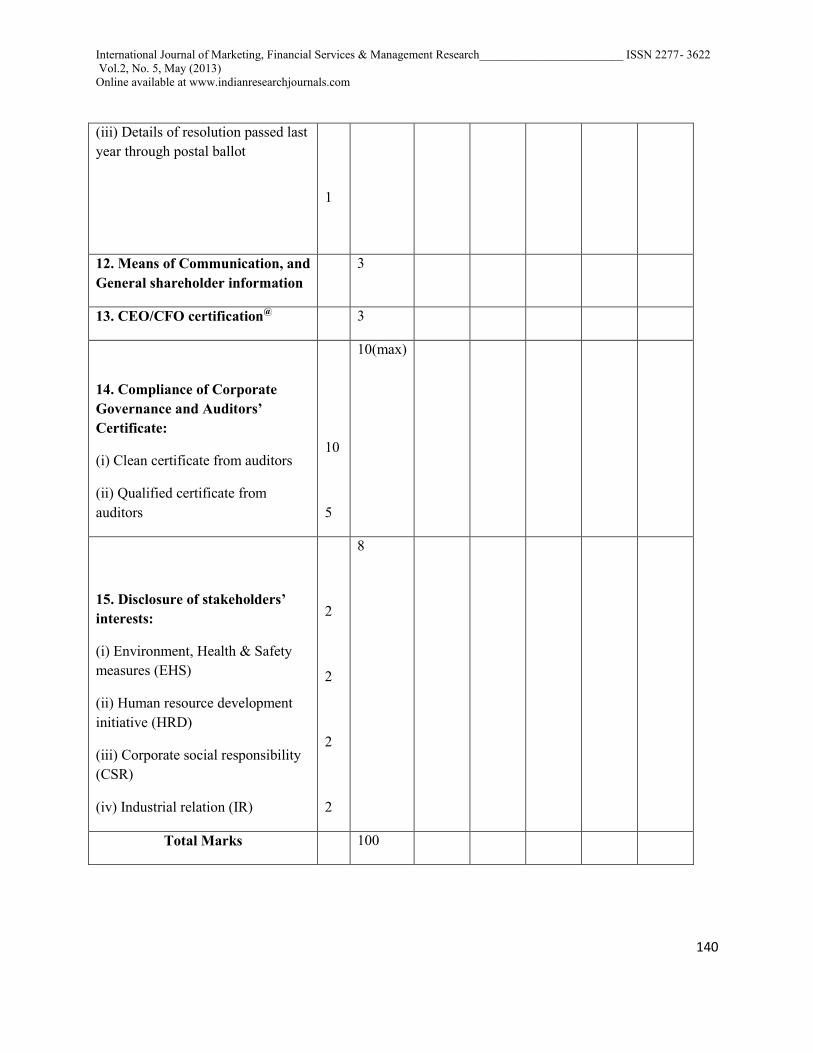

(iii) Details of resolution passed last

year through postal ballot

1

12. Means of Communication, and

General shareholder information

3

13. CEO/CFO certification@

3

14. Compliance of Corporate

Governance and Auditors’

Certificate:

(i) Clean certificate from auditors

(ii) Qualified certificate from

auditors

10

5

10(max)

15. Disclosure of stakeholders’

interests:

(i) Environment, Health & Safety

measures (EHS)

(ii) Human resource development

initiative (HRD)

(iii) Corporate social responsibility

(CSR)

(iv) Industrial relation (IR)

2

2

2

2

8

Total Marks 100

Recommended