Corporate Presentation September 2016

Prepared with data at closing of June 30th 2016, unless noticed otherwise

Committed to trustworthy and profitable banking

2

Disclaimer

The purpose of this presentation is purely informative and the information contained herein is subject to, and must be read in conjunction with, all other publicly available information. In particular, regarding the data provided by third parties, neither CaixaBank, S.A. (“CaixaBank”), nor any of its administrators, directors or employees, is obliged, either explicitly or implicitly, to vouch that these contents are exact, accurate, comprehensive or complete, nor to keep them updated, nor to correct them in the case that any deficiency, error or omission were to be detected. Moreover, in reproducing these contents in any medium, CaixaBank may introduce any changes it deems suitable, may omit partially or completely any of the elements of this document, and in case of any deviation between such a version and this one, assumes no liability for any discrepancy.

This document has at no time been submitted to the Comisión Nacional del Mercado de Valores (CNMV – the Spanish Stock Markets regulatory body) for approval or scrutiny. In all cases its contents are regulated by the Spanish law applicable at time of writing, and it is not addressed to any person or legal entity located in any other jurisdiction. For this reason it may not necessarily comply with the prevailing norms or legal requisites as required in other jurisdictions.

CaixaBank cautions that this presentation might contain forward-looking statements. While these statements represent our judgment and future expectations concerning the development of our business, a number of risks, uncertainties and other important factors could cause actual developments and results to differ materially from our expectations.

Statements as to historical performance, historical share price or financial accretion are not intended to mean that future performance, future share price or future earnings for any period will necessarily match or exceed those of any prior year. Nothing in this presentation should be construed as a profit forecast.

This presentation on no account should be construed as a service of financial analysis or advice, nor does it aim to offer any kind of financial product or service. In particular, it is expressly remarked here that no information herein contained should be taken as a guarantee of future performance or results.

In making this presentation available, CaixaBank gives no advice and makes no recommendation to buy, sell or otherwise deal in CaixaBank shares, or any other securities or investment whatsoever. Any person at any time acquiring securities must do so only on the basis of such person’s own judgment as to the merits or the suitability of the securities for its purpose and only on such information as is contained in such public information having taken all such professional or other advice as it considers necessary or appropriate in the circumstances and not in reliance on the information contained in this presentation.

Without prejudice to legal requirements, or to any limitations imposed by CaixaBank that may be applicable, permission is hereby expressly refused for any type of use or exploitation of the contents of this presentation, and for any use of the signs, trademarks and logotypes which it contains. This prohibition extends to any kind of reproduction, distribution, transmission to third parties, public communication or conversion into any other medium, for commercial purposes, without the previous express permission of CaixaBank and/or other respective proprietary title holders. Any failure to observe this restriction may constitute a legal offence which may be sanctioned by the prevailing laws in such cases.

With regards to Alternative Performance Measures (APMs) as defined in the guidelines on Alternative Performance Measures issued by the European Securities and Markets Authority on 30 June 2015 (ESMA/2015/1057), this report uses certain APMs, which have not been audited, for a better understanding of the company's financial performance. These measures are considered additional disclosures and in no case replace the financial information prepared under IFRS. Moreover, the way the Group defines and calculates these measures may differ to the way similar measures are calculated by other companies. Accordingly, they may not be comparable. Refer to the quarterly report for a list of the APMs used, along with a reconciliation between certain management indicators and the indicators presented in the consolidated financial statements prepared under IFRS.

In so far as it relates to results from investments, this financial information from CaixaBank Group for 1H 2016 has been prepared mainly on the basis of estimates.

3

Index

1. CaixaBank at a glance p. 4

2. Competitive stance p. 11

3. Strategic Plan 2015-2018 p. 29

4. International presence & Investments p. 36

5. Results and activity update: 1H16 p. 39

Appendix p. 62

4

CaixaBank [At a glance]

5

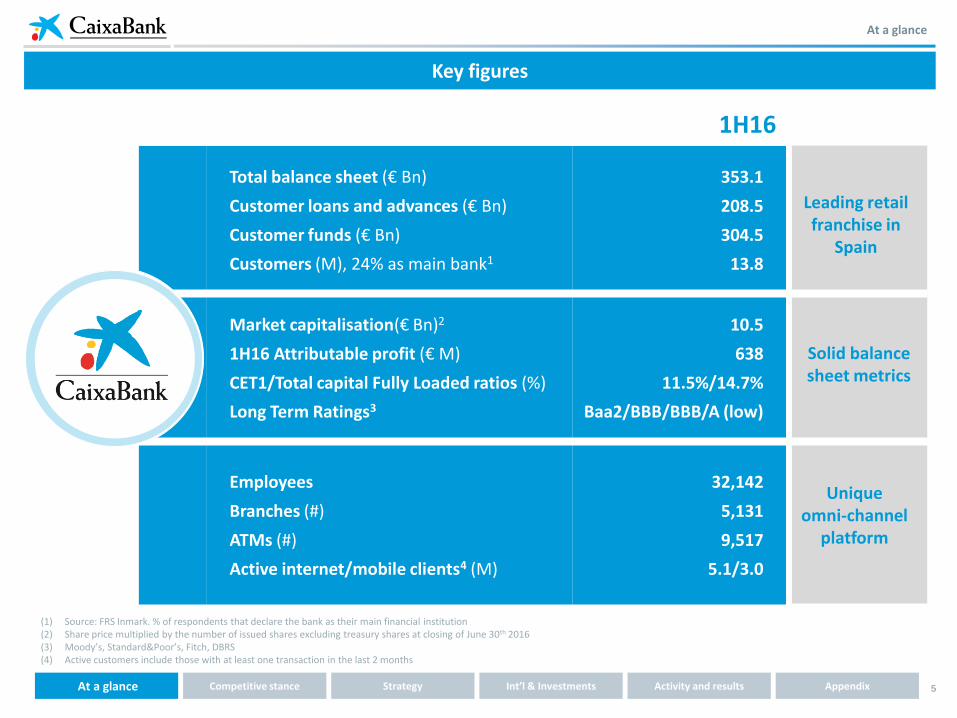

Total balance sheet (€ Bn)

Customer loans and advances (€ Bn)

Customer funds (€ Bn)

Customers (M), 24% as main bank1

353.1

208.5

304.5

13.8

Market capitalisation(€ Bn)2

1H16 Attributable profit (€ M)

CET1/Total capital Fully Loaded ratios (%)

Long Term Ratings3

10.5

638

11.5%/14.7%

Baa2/BBB/BBB/A (low)

Employees

Branches (#)

ATMs (#)

Active internet/mobile clients4 (M)

32,142

5,131

9,517

5.1/3.0

At a glance

1H16

Leading retail franchise in

Spain

Solid balance sheet metrics

Unique omni-channel

platform

(1) Source: FRS Inmark. % of respondents that declare the bank as their main financial institution (2) Share price multiplied by the number of issued shares excluding treasury shares at closing of June 30th 2016 (3) Moody’s, Standard&Poor’s, Fitch, DBRS (4) Active customers include those with at least one transaction in the last 2 months

Key figures

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

6

At a glance

(1) Fully diluted stake considering the €750M Criteria exchangeable into CaixaBank shares maturing in Nov 2017 and excluding treasury shares (2) Latest figures reported by CriteriaCaixa. “Other” incl. stakes in Aigües de Barcelona, Aguas de Valencia;100% of Caixa Capital Risc, Mediterranea Beach and Golf Community and RE business

49%1

Other Investments2

Other 2

(34.3%)

(18.9%)

(5.7%)

(50.1%)

(20%)

Non-controlled stakes

Welfare program

In June 2014, “la Caixa” became a banking foundation and in October 2014 it completed the formal reorganisation of the Group after segregating to CriteriaCaixa liabilities and assets, including its stake in CaixaBank.

1

3

2

3

A streamlined organisation of the Group

(4.6%)

(9.0%) (17.3%)

100% 2

1

(10.2%)

(5.0%) (45.2%)

(9.9%)

Bank-Insurance activities, supported by financial subsidiaries

100%

100%

100%

49%

CaixaBank AM

VidaCaixa Group (Insurance) 100%

CaixaBank Payments (Credit Cards)

CaixaBank Consumer Finance

Comercia Global Payments (PoS payments)

RE activities

Building Center (100%); Servihabitat Serv. Inm. (49%)

Group structure

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

7

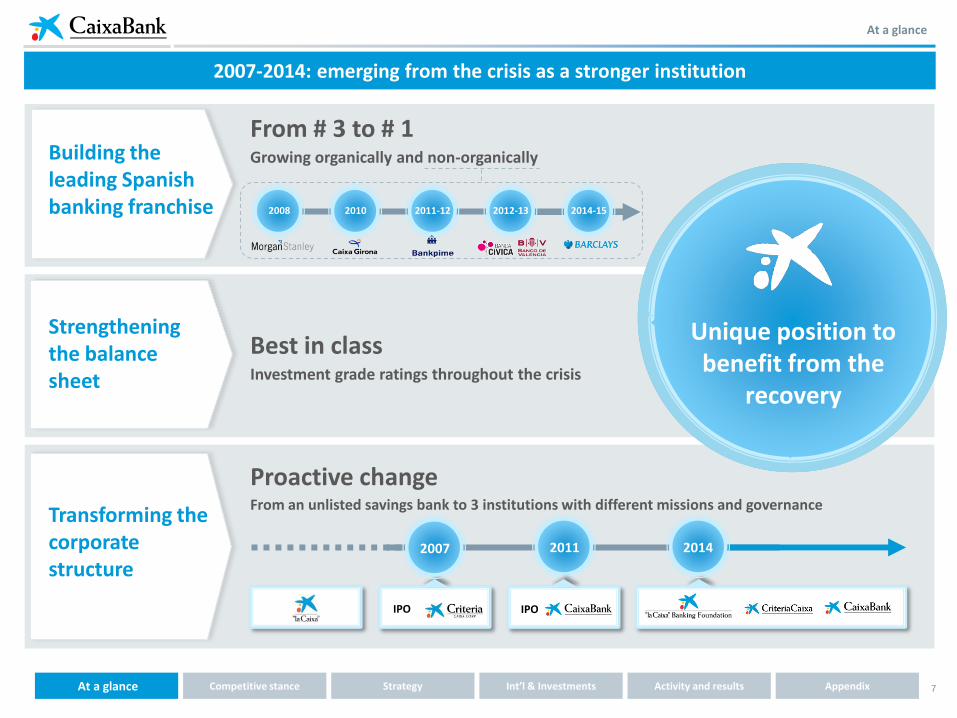

Unique position to benefit from the

recovery

Building the leading Spanish banking franchise

Strengthening the balance sheet

Proactive change From an unlisted savings bank to 3 institutions with different missions and governance

From # 3 to # 1 Growing organically and non-organically

Best in class Investment grade ratings throughout the crisis

2007-2014: emerging from the crisis as a stronger institution

2011 2014

IPO IPO

2007

Transforming the corporate structure

2008 2010 2011-12 2012-13 2014-15

At a glance

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

8

At a glance

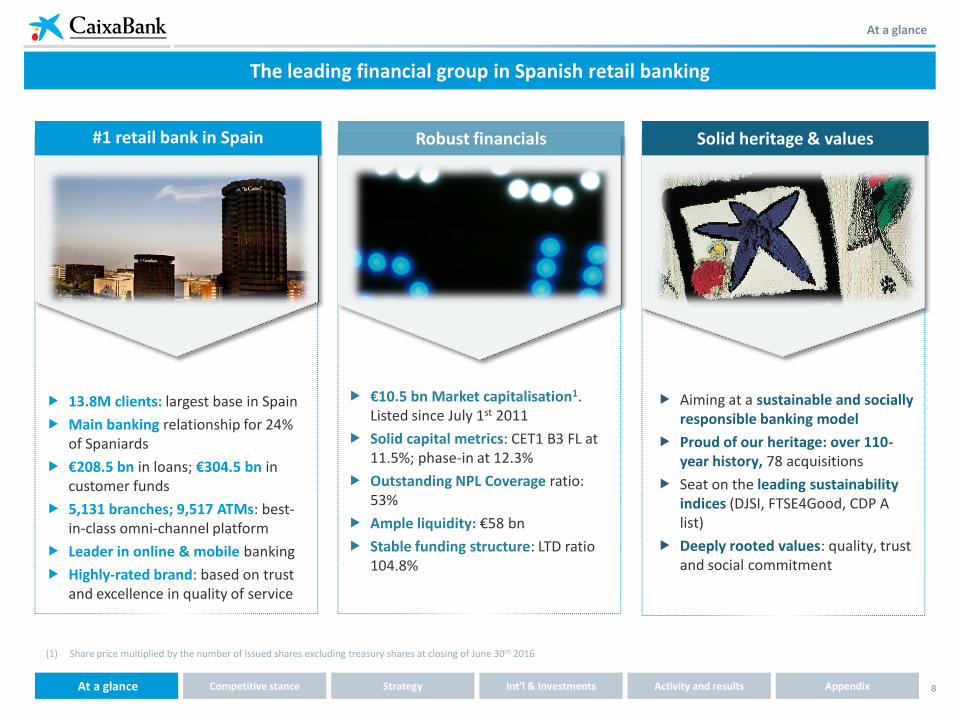

13.8M clients: largest base in Spain

Main banking relationship for 24% of Spaniards

€208.5 bn in loans; €304.5 bn in customer funds

5,131 branches; 9,517 ATMs: best-in-class omni-channel platform

Leader in online & mobile banking

Highly-rated brand: based on trust and excellence in quality of service

€10.5 bn Market capitalisation1. Listed since July 1st 2011

Solid capital metrics: CET1 B3 FL at 11.5%; phase-in at 12.3%

Outstanding NPL Coverage ratio: 53%

Ample liquidity: €58 bn

Stable funding structure: LTD ratio 104.8%

Aiming at a sustainable and socially responsible banking model

Proud of our heritage: over 110-year history, 78 acquisitions

Seat on the leading sustainability indices (DJSI, FTSE4Good, CDP A list)

Deeply rooted values: quality, trust and social commitment

#1 retail bank in Spain

The leading financial group in Spanish retail banking

Robust financials Solid heritage & values

(1) Share price multiplied by the number of issued shares excluding treasury shares at closing of June 30th 2016

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

9

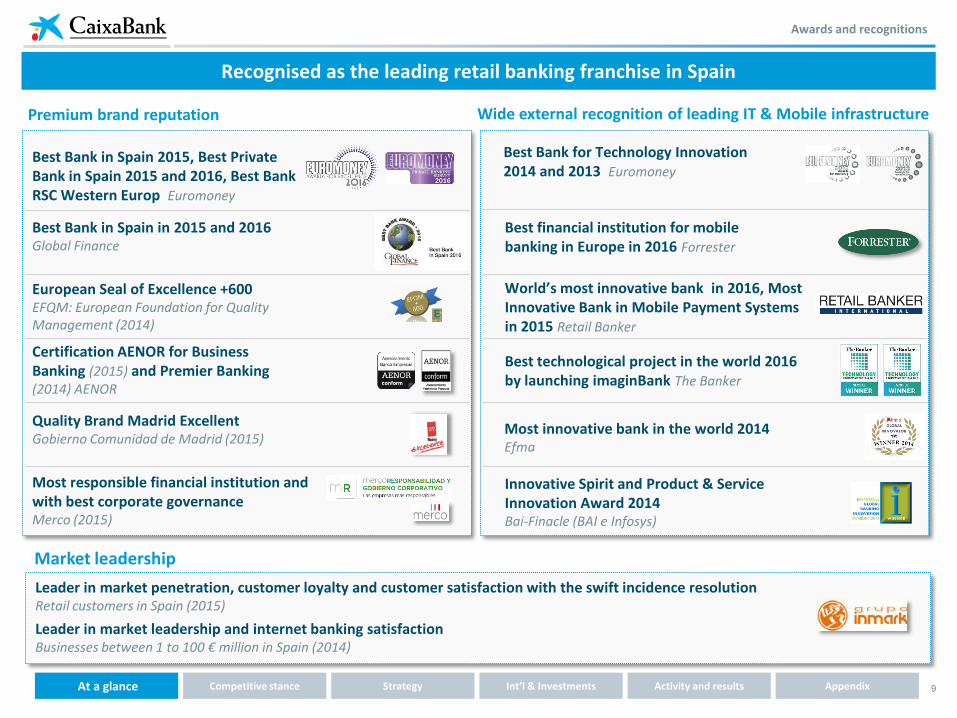

Premium brand reputation Wide external recognition of leading IT & Mobile infrastructure

European Seal of Excellence +600 EFQM: European Foundation for Quality Management (2014)

Best Bank in Spain in 2015 and 2016 Global Finance

Certification AENOR for Business Banking (2015) and Premier Banking (2014) AENOR

Best Bank in Spain 2015, Best Private Bank in Spain 2015 and 2016, Best Bank RSC Western Europ Euromoney

Quality Brand Madrid Excellent Gobierno Comunidad de Madrid (2015)

Best financial institution for mobile banking in Europe in 2016 Forrester

Best Bank for Technology Innovation 2014 and 2013 Euromoney

Innovative Spirit and Product & Service Innovation Award 2014 Bai-Finacle (BAI e Infosys)

World’s most innovative bank in 2016, Most Innovative Bank in Mobile Payment Systems in 2015 Retail Banker

Most responsible financial institution and with best corporate governance Merco (2015)

Market leadership

Leader in market penetration, customer loyalty and customer satisfaction with the swift incidence resolution Retail customers in Spain (2015)

Leader in market leadership and internet banking satisfaction Businesses between 1 to 100 € million in Spain (2014)

Awards and recognitions

Recognised as the leading retail banking franchise in Spain

Best technological project in the world 2016 by launching imaginBank The Banker

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

Most innovative bank in the world 2014 Efma

10 Int’l & Investments Performance Balance sheet At a glance Competitive stance Strategy Appendix

Macro & Industry Backdrop

Geared to the performance of the Spanish economy

24.8% 26.1% 24.4% 22.1% 19.8% 18.4% 17.1%

2012 2013 2014 2015 2016 2017 2018

-9.9% -9.4% -7.1%

-4.3% -2.2%

0.1% 1.4%

0.6% 1.4% -0.3% 1.0%

2.0% 2.3% 2.1%

2012 2013 2014 2015 2016 2017 2018

The economic recovery in Spain remains strong

GDP growth, % yoy

The banking system is supporting the recovery

-2.6% -1.7%

1.4%

3.2% 3.1% 2.4% 2.2%

2012 2013 2014 2015 2016 2017 2018

Labor market remains in recovery mode RE market has stabilised and starts an upward trend

Unemployment rate, % yoy

% yoy, industry forecasts

Housing prices (nominal) % yoy

forecast

forecast forecast

(1) Loans to the “Other Resident Sectors” excluding to financial services companies (Bank of Spain statistics). (2) Includes time and demand deposits as well as promissory notes of households and non-financial companies. Source: CaixaBank Research. Forecasts as of Aug 01, 2016

forecast

deposits2

credit1

• Largest client base • Premium network • Better asset quality

Economic activity continues to grow strongly: GDP increased by 0.8% qoq (3.2% yoy) in 2Q16. We forecast a slight decrease in future growth rates due to the loss of strength of some temporary tailwinds (less expansionary fiscal policy, increase in oil prices). We expect the negative impact of Brexit to be concentrated in the UK, with a limited negative effect on global confidence.

Macro dynamics support volume growth and improved asset quality: New credit is accelerating as a result of pent-up demand and improved financial conditions while the cost of risk is steadily declining. The main challenge is to achieve sustainable profitability levels.

-8.8% -5.8% -2.4%

1.1% 3.0% 4.0% 5.5%

2012 2013 2014 2015 2016 2017 2018

11

Competitive [Stance]

12

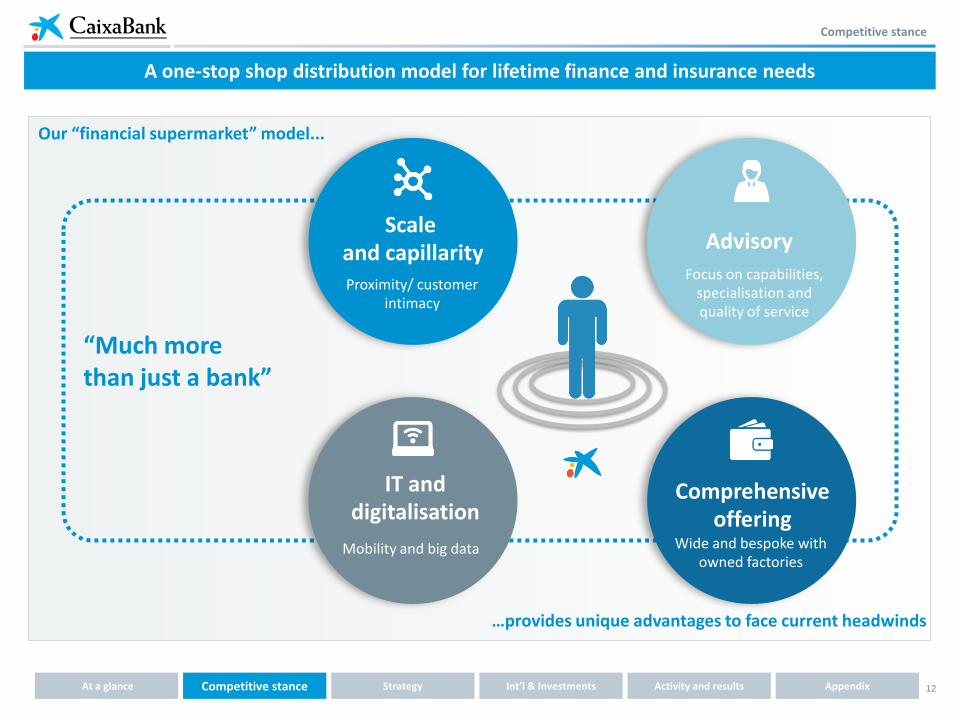

A one-stop shop distribution model for lifetime finance and insurance needs

Our “financial supermarket” model...

…provides unique advantages to face current headwinds

“Much more than just a bank”

Scale and capillarity Proximity/ customer

intimacy

Advisory

Focus on capabilities, specialisation and quality of service

Competitive stance

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

IT and digitalisation

Mobility and big data

Comprehensive offering

Wide and bespoke with owned factories

13

Market leadership

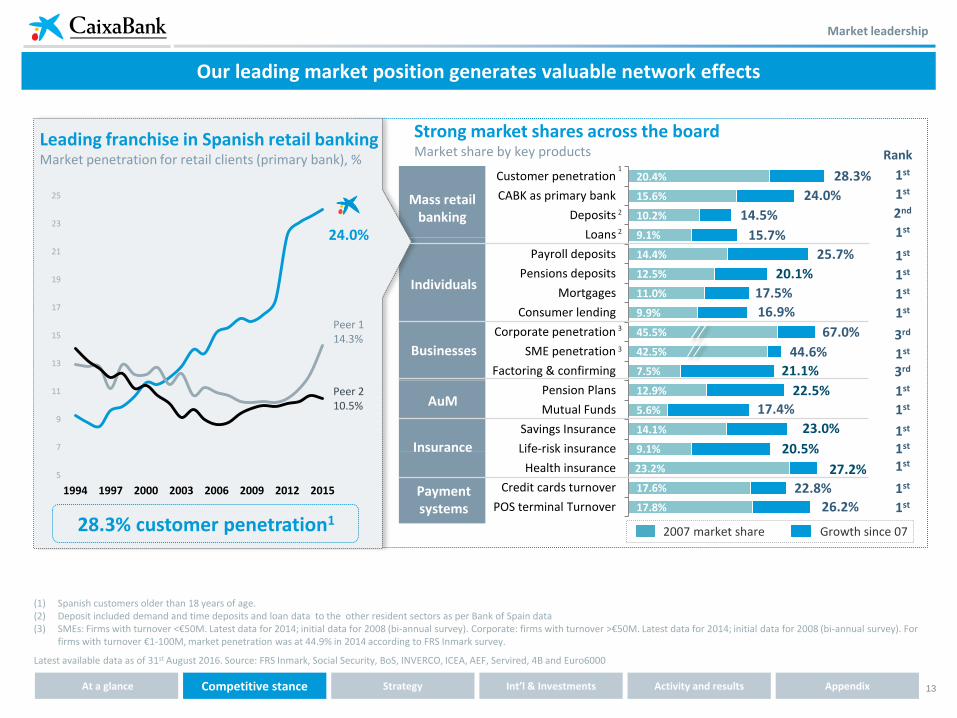

Our leading market position generates valuable network effects

17.8%

17.6%

23.2%

9.1%

14.1%

5.6%

12.9%

7.5%

42.5%

45.5%

9.9%

11.0%

12.5%

14.4%

9.1%

10.2%

15.6%

20.4%

POS terminal Turnover

Credit cards turnover

Health insurance

Life-risk insurance

Savings Insurance

Mutual Funds

Pension Plans

Factoring & confirming

SME penetration

Corporate penetration

Consumer lending

Mortgages

Pensions deposits

Payroll deposits

Loans

Deposits

CABK as primary bank

Customer penetration 28.3%

24.0%

15.7%

25.7%

16.9%

44.6%

23.0%

22.8%

14.5%

67.0%

17.4%

22.5%

20.5%

26.2%

2007 market share Growth since 07

1st

Rank

Mass retail banking

AuM

Payment systems

Insurance

Individuals

Businesses

20.1%

17.5%

21.1%

1st

2nd

1st

3rd

1st

3rd

1st

1st

1st

1st

1st

1st

1

2

3

1st

1st

1st

1st

1st 27.2%

3

2

Leading franchise in Spanish retail banking Market penetration for retail clients (primary bank), %

28.3% customer penetration1

(1) Spanish customers older than 18 years of age. (2) Deposit included demand and time deposits and loan data to the other resident sectors as per Bank of Spain data (3) SMEs: Firms with turnover <€50M. Latest data for 2014; initial data for 2008 (bi-annual survey). Corporate: firms with turnover >€50M. Latest data for 2014; initial data for 2008 (bi-annual survey). For

firms with turnover €1-100M, market penetration was at 44.9% in 2014 according to FRS Inmark survey.

Latest available data as of 31st August 2016. Source: FRS Inmark, Social Security, BoS, INVERCO, ICEA, AEF, Servired, 4B and Euro6000

24.0%

Peer 1 14.3%

Peer 2 10.5%

5

7

9

11

13

15

17

19

21

23

25

1994 1997 2000 2003 2006 2009 2012 2015

Strong market shares across the board Market share by key products

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

14

Proven integration track record

(1) Time lapsed from closing, legal merger or acquisition agreement until completion of IT integration (2) It involved completing 4 sequential integrations

Acquisitions

Strict financial discipline for acquisitions

Growth and market leadership have been reinforced by acquisitions

Synergies as % of initial costs Synergies 2016E (€M)

Timing (begin/completed)

Initial target Achieved

59% 63% 580 2012/2015

52% 62% 101 2013/2015

45% 56% 189 2015/2016

Effective delivery of synergies exceeding targets and earlier than expected. In €M

0.3x 0.0x

0.5x

Attractive multiples (P/BV multiples)

2008 2010 2011-12 2012-13 2014-15

10 months1 6 months1 4 months1 8.5 months1,2 5 months1 4.5 months1

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

15

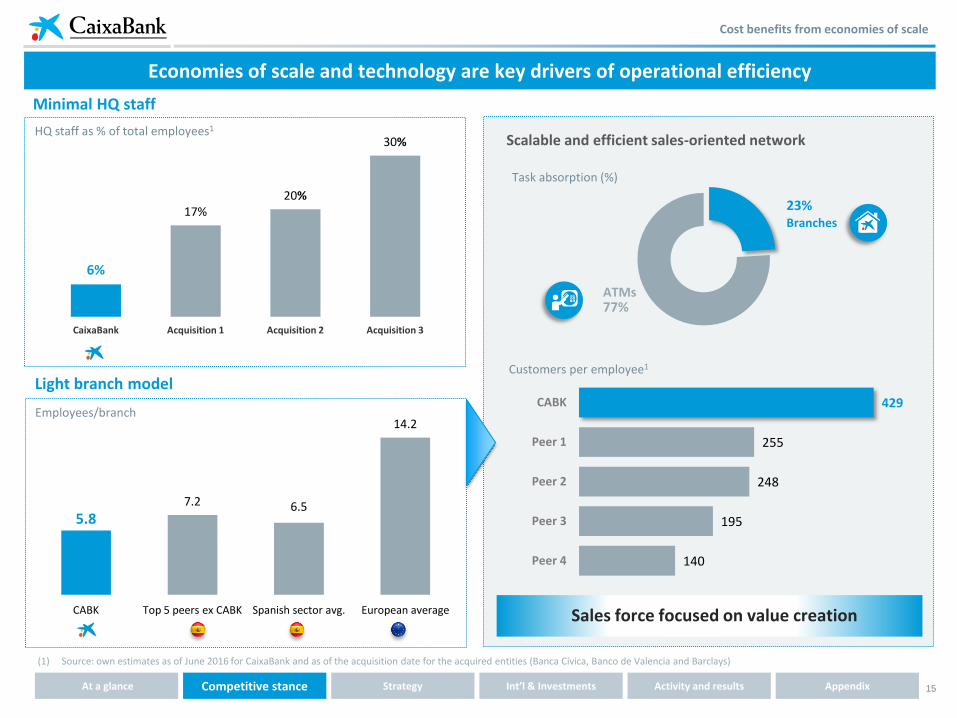

Economies of scale and technology are key drivers of operational efficiency

(1) Source: own estimates as of June 2016 for CaixaBank and as of the acquisition date for the acquired entities (Banca Cívica, Banco de Valencia and Barclays)

Cost benefits from economies of scale

Minimal HQ staff

HQ staff as % of total employees1

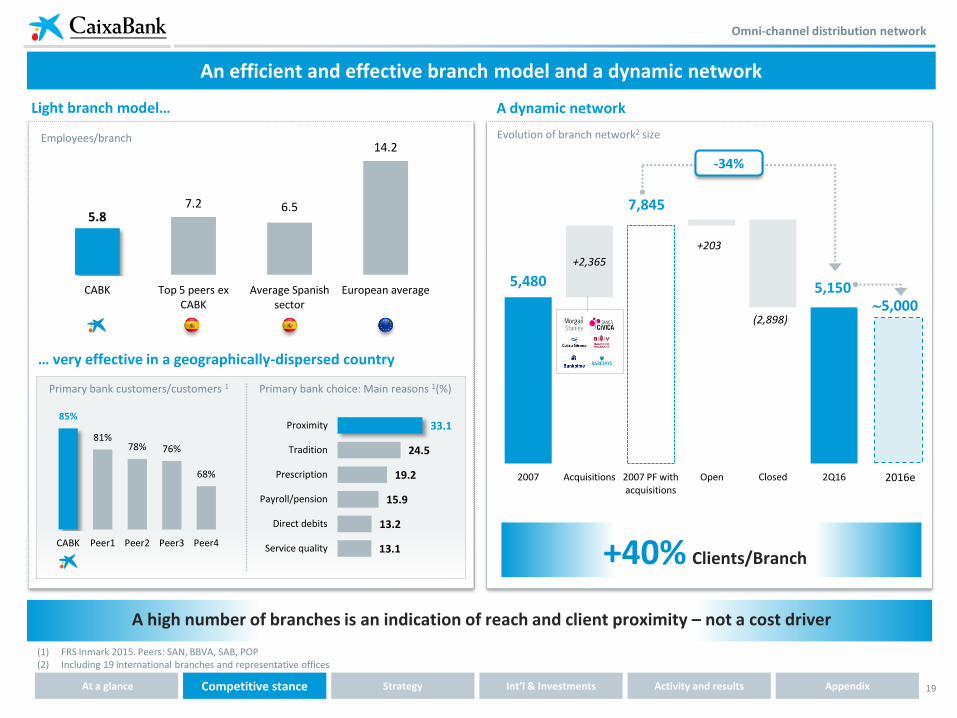

Light branch model

Employees/branch

5.8 7.2 6.5

14.2

CABK Top 5 peers ex CABK Spanish sector avg. European average

23%

77%

Task absorption (%)

Branches

ATMs

Sales force focused on value creation

Customers per employee1

Scalable and efficient sales-oriented network

6%

17% 20%

30%

CaixaBank Acquisition 1 Acquisition 2 Acquisition 3

429

255

248

195

140

CABK

Peer 1

Peer 2

Peer 3

Peer 4

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

16

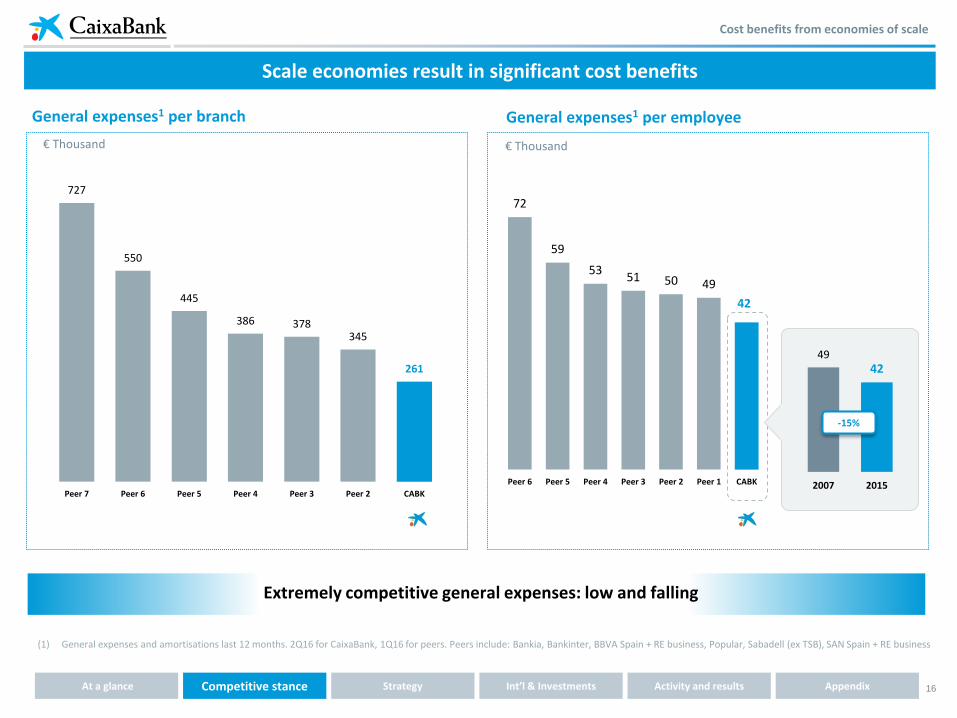

Scale economies result in significant cost benefits

(1) General expenses and amortisations last 12 months. 2Q16 for CaixaBank, 1Q16 for peers. Peers include: Bankia, Bankinter, BBVA Spain + RE business, Popular, Sabadell (ex TSB), SAN Spain + RE business

Cost benefits from economies of scale

€ Thousand € Thousand

72

59

53 51 50 49

42

Peer 6 Peer 5 Peer 4 Peer 3 Peer 2 Peer 1 CABK

General expenses1 per branch

49 42

2007 2015

-15%

General expenses1 per employee

Extremely competitive general expenses: low and falling

727

550

445

386 378 345

261

Peer 7 Peer 6 Peer 5 Peer 4 Peer 3 Peer 2 CABK

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

17

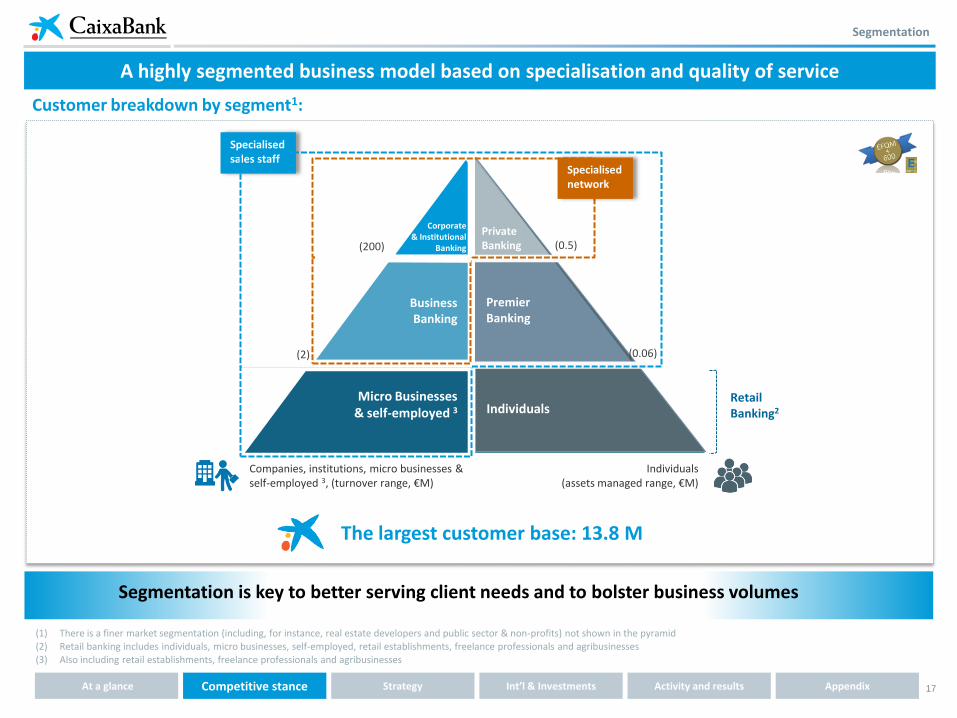

Segmentation

Business Banking

(0.06)

Individuals (assets managed range, €M)

Companies, institutions, micro businesses & self-employed 3, (turnover range, €M)

(1) There is a finer market segmentation (including, for instance, real estate developers and public sector & non-profits) not shown in the pyramid (2) Retail banking includes individuals, micro businesses, self-employed, retail establishments, freelance professionals and agribusinesses (3) Also including retail establishments, freelance professionals and agribusinesses

Customer breakdown by segment1:

(0.5)

Micro Businesses & self-employed 3 Individuals

Retail Banking2

Specialised sales staff

The largest customer base: 13.8 M

A highly segmented business model based on specialisation and quality of service

Segmentation is key to better serving client needs and to bolster business volumes

Premier Banking

Private Banking

Specialised network

(2)

Corporate & Institutional

Banking (200)

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

18

Omni-channel distribution network

Best-in-class omni-channel distribution platform with multi-product capabilities

Powerful IT architecture allows for total seamlessness, flexibility, reliability and sales-force mobility Staff time is freed-up to concentrate on building relationships and innovation

(1) As of March 2016 (2) Active customers include those with at least one transaction in the last 2 months. Sources: ComsCore (online customer penetration) and Bank of Spain. Latest available data (3) As of May 2016. Source: ComScore

5,131 branches

17.5% market share1

Branch market share by province1, %

The largest physical footprint in Spain

<10%

>15%

10-15%

Employees with mobile equipment

9,517 ATMs

19.1% market share1

Leader in digital channels

European leader in internet banking

5.1 M active customers2

37% of transactions

33% penetration3

European leader in mobile banking

3.0 M active customers2

+ 53% CAGR 2012-2015

20% of transactions

Best mobile banking platform in Europe

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

19

5,480

7,845

5,150

+2,365

+203

(2,898)

2007 Acquisitions 2007 PF with acquisitions

Open Closed 2Q16

An efficient and effective branch model and a dynamic network

Omni-channel distribution network

5.8 7.2 6.5

14.2

CABK Top 5 peers ex CABK

Average Spanish sector

European average

Employees/branch

Light branch model…

… very effective in a geographically-dispersed country

13.1

13.2

15.9

19.2

24.5

33.1

Service quality

Direct debits

Payroll/pension

Prescription

Tradition

Proximity

Primary bank choice: Main reasons 1(%)

85%

81% 78% 76%

68%

CABK Peer1 Peer2 Peer3 Peer4

Primary bank customers/customers 1

A high number of branches is an indication of reach and client proximity – not a cost driver

(1) FRS Inmark 2015. Peers: SAN, BBVA, SAB, POP (2) Including 19 international branches and representative offices

Evolution of branch network2 size

2016e

5,000

-34%

A dynamic network

+40% Clients/Branch

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

20

CaixaFuturo

Private Banking

Premier Banking

Business Banking

Personalised saving strategy– Investment and Protection

Best private banking in Spain 2015 y 2016 Euromoney

AENOR conform certified

Preferred and personal service based on quality

Rapid implementation of our advisory model

Transforming branches into advisory hubs

New commercial protocols

Differentiated relationship

Reinforced capabilities

Redesigned tools and spaces

Advisory focus

Focus on the quality of service

Advisory

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

21

Innovation & Technology

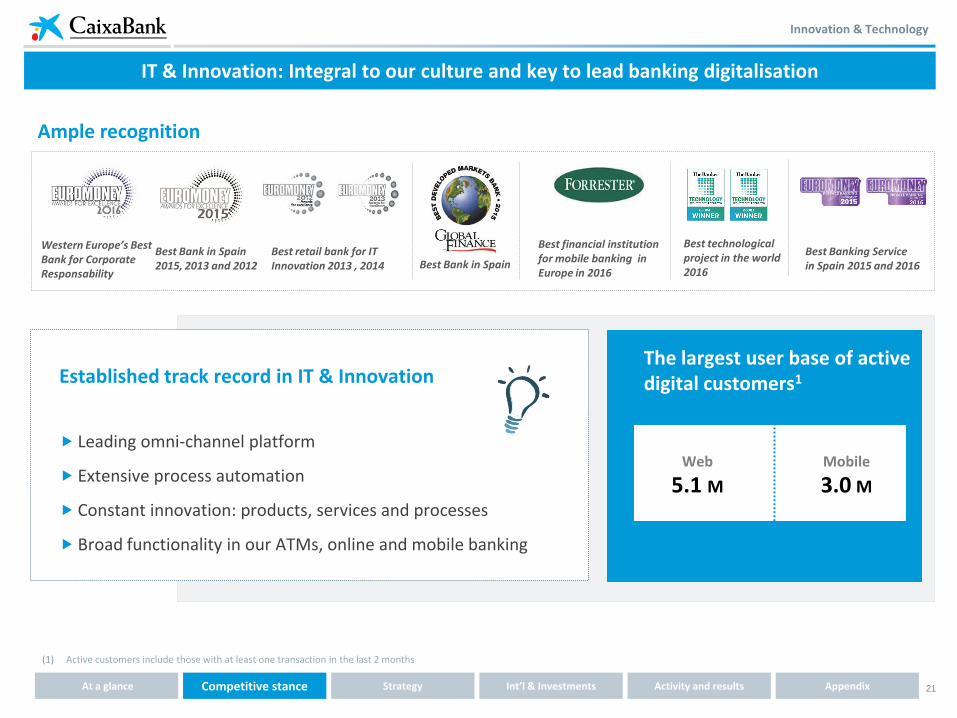

IT & Innovation: Integral to our culture and key to lead banking digitalisation

(1) Active customers include those with at least one transaction in the last 2 months

Established track record in IT & Innovation

Leading omni-channel platform

Extensive process automation

Constant innovation: products, services and processes

Broad functionality in our ATMs, online and mobile banking

The largest user base of active digital customers1

Ample recognition

Web

5.1 M

Mobile

3.0 M

Best Bank in Spain Best Bank in Spain 2015, 2013 and 2012

Best financial institution for mobile banking in Europe in 2016

Best Banking Service in Spain 2015 and 2016

Best retail bank for IT Innovation 2013 , 2014

Western Europe’s Best Bank for Corporate Responsability

Best technological project in the world 2016

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

22

Focus on omni-channel banking reduces costs and increases client’s perceived value

(1) Total number of transactions in 1H16: 4,108M. A transaction is defined as any action initiated by a client through a contract with CaixaBank. (2) Click & Go loans represent 19% of total personal loans sold through CaixaBank network

21% 11% 9% 8% 7% 7%

20%

14% 10% 9% 8% 7%

41%

34%

29% 29% 30% 29%

18%

41% 52% 54% 54% 57%

2004 2009 2013 2014 2015 1H16

Digital channels gain importance Transactions by channel1 (%)

Internet &

Mobile

(Mobile: 20%)

Branches ATMs

POS terminals and

automated

...remaining complementary to the physical channel

… freeing up retail staff time to concentrate on building relationships, advisory and innovation

+ Quality

+ Convenience

+ Efficiency

Recently ranked as the best financial institution for mobile banking in Europe

Branches

ATMs

Online

Mobile

25% 39%

11% 25%

70% of Click & Go2 loans sales sold through electronic channels

Pre-approved instant consumer loan (Click & Go loans2) sales by channel, % of total sold 1H16

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

Innovation & Technology

23

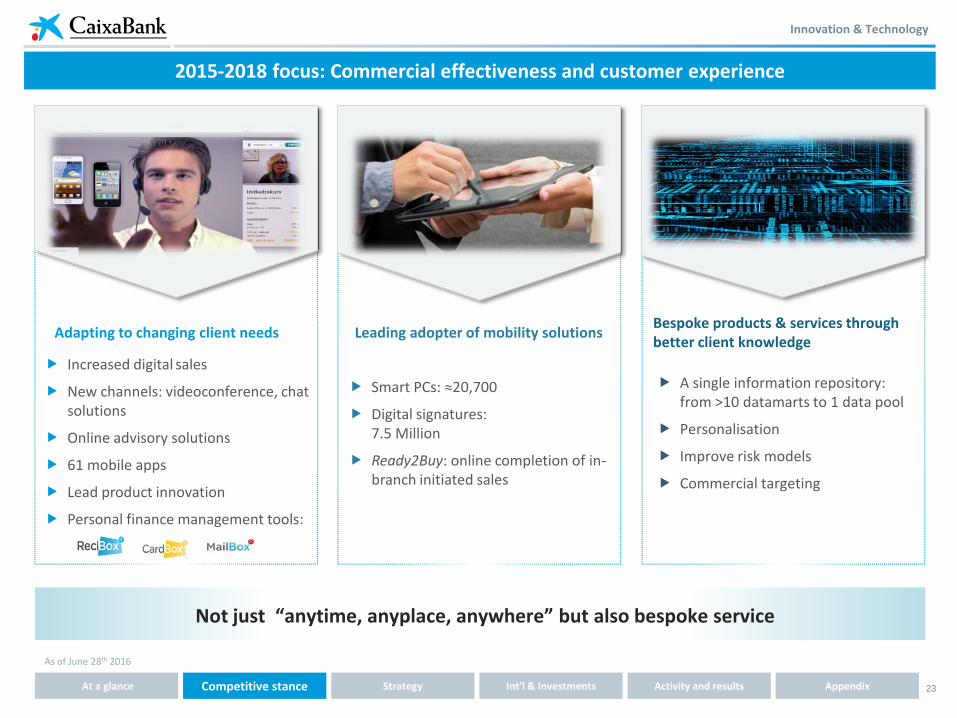

Increased digital sales

New channels: videoconference, chat solutions

Online advisory solutions

61 mobile apps

Lead product innovation

Personal finance management tools:

Adapting to changing client needs

Smart PCs: ≈20,700

Digital signatures: 7.5 Million

Ready2Buy: online completion of in-branch initiated sales

Leading adopter of mobility solutions Bespoke products & services through better client knowledge

A single information repository: from >10 datamarts to 1 data pool

Personalisation

Improve risk models

Commercial targeting

Not just “anytime, anyplace, anywhere” but also bespoke service

2015-2018 focus: Commercial effectiveness and customer experience

As of June 28th 2016

Innovation & Technology

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

24

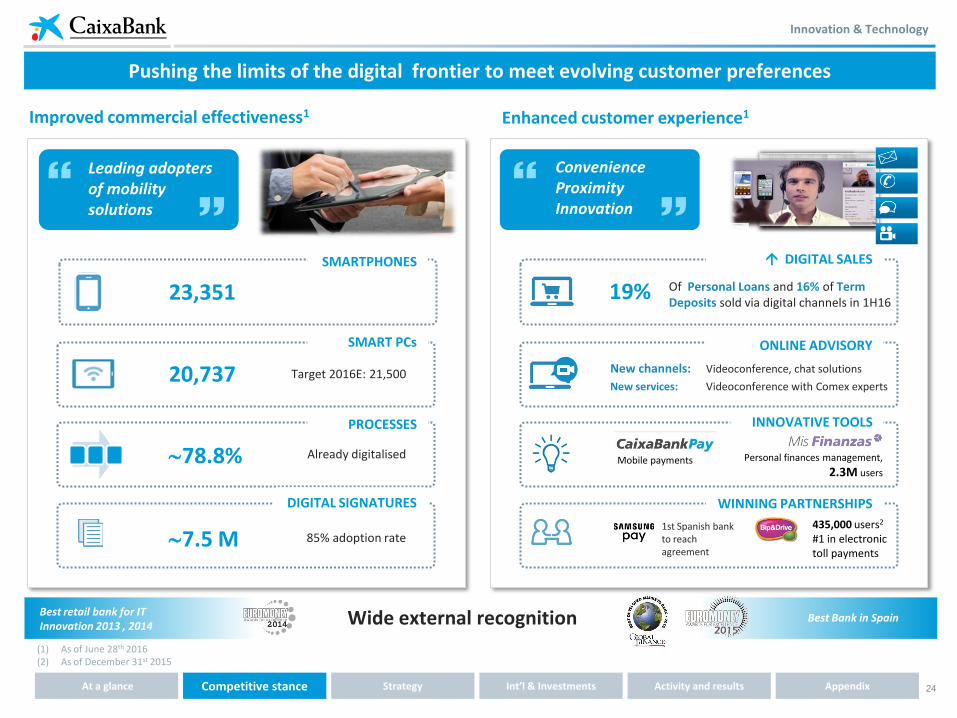

Improved commercial effectiveness1

Pushing the limits of the digital frontier to meet evolving customer preferences

Enhanced customer experience1

Leading adopters of mobility solutions

Convenience Proximity Innovation

Best retail bank for IT Innovation 2013 , 2014

Best Bank in Spain Wide external recognition

23,351

20,737

7.5 M

Target 2016E: 21,500

85% adoption rate

19% Of Personal Loans and 16% of Term Deposits sold via digital channels in 1H16

ONLINE ADVISORY

New channels: Videoconference, chat solutions

New services: Videoconference with Comex experts

INNOVATIVE TOOLS

Personal finances management,

2.3M users Mobile payments

435,000 users2

#1 in electronic toll payments

1st Spanish bank to reach agreement

SMARTPHONES DIGITAL SALES

SMART PCs

DIGITAL SIGNATURES WINNING PARTNERSHIPS

PROCESSES

78.8% Already digitalised

Innovation & Technology

(1) As of June 28th 2016 (2) As of December 31st 2015

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

25

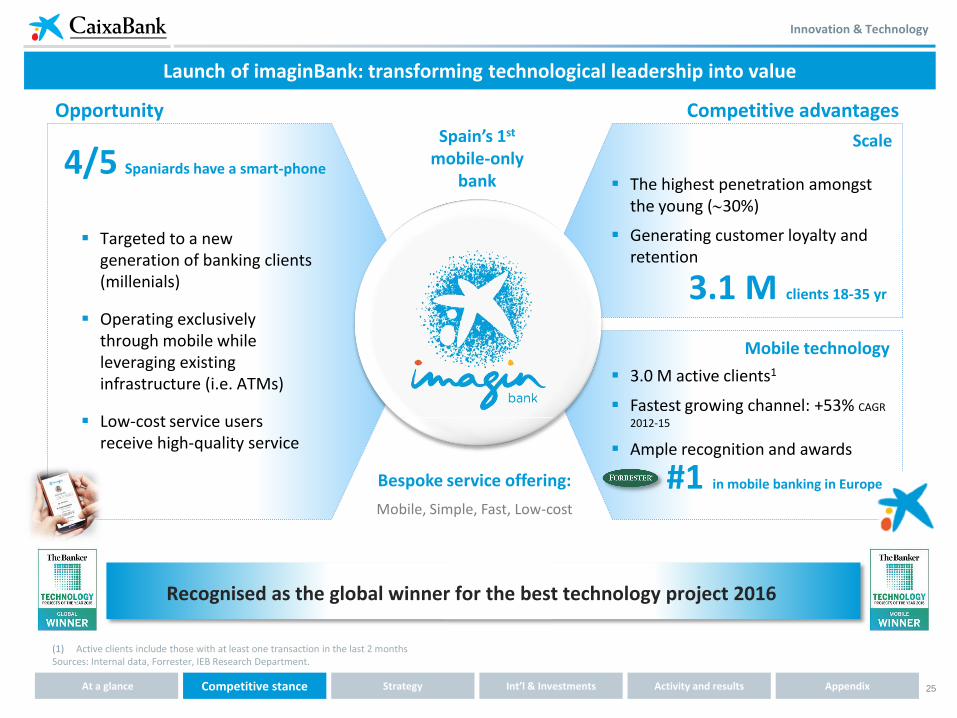

Launch of imaginBank: transforming technological leadership into value

Spain’s 1st mobile-only

bank

Targeted to a new generation of banking clients (millenials)

Operating exclusively through mobile while leveraging existing infrastructure (i.e. ATMs)

Low-cost service users receive high-quality service

4/5 Spaniards have a smart-phone

Bespoke service offering:

Mobile, Simple, Fast, Low-cost

Opportunity Competitive advantages

The highest penetration amongst the young (30%)

Generating customer loyalty and retention

3.1 M clients 18-35 yr

#1 in mobile banking in Europe

3.0 M active clients1

Fastest growing channel: +53% CAGR

2012-15

Ample recognition and awards

Scale

Mobile technology

Recognised as the global winner for the best technology project 2016

(1) Active clients include those with at least one transaction in the last 2 months Sources: Internal data, Forrester, IEB Research Department.

Innovation & Technology

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

26

Ownership preserved and growth fostered throughout the crisis

Integrated management of client savings and spending needs

Agile time-to-market

Flexibility in pricing, packaging and distribution

No conflicting views with partners

Through a single integrated distribution platform

Business Key figures 1H16 Company %

ownership

Life insurance €61bn Assets #1 in Spain

100%

Non-life insurance

€1.7bn premia(1) #1 in Health ins.(2)

49.9%

Asset management

€49.8bn AuM

#1 in Spain 100%

Consumer Finance

€1.5 Bn New business

€2.1 Bn assets 100%

Credit cards €31.5bn turnover

#1 in Spain 100%

Payments at point of sale

€18.8bn turnover

325,545 PoS 49%

Microcredit +64% new microcredit to households (yoy)(1)

100%

One-stop financial shop

(1) Latest available data (2) In Spain

A financial supermarket providing a one-stop shop for lifetime finance & insurance needs

Market-leading factories provide revenue diversification and benefits from scope

A key competitive advantage to lead to RoTE higher than peers

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

27

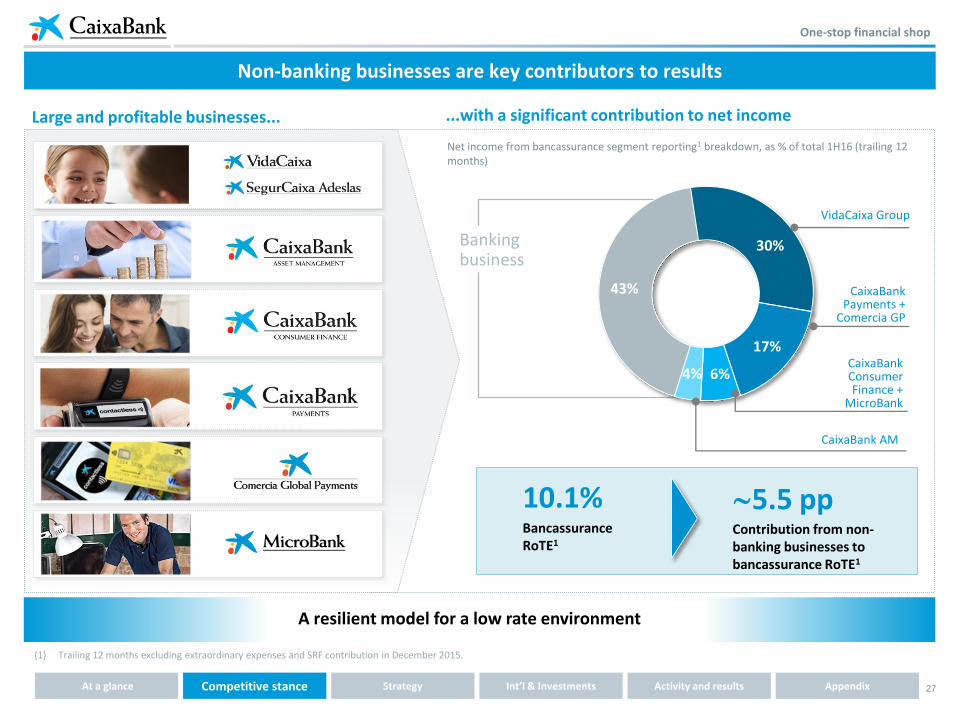

Non-banking businesses are key contributors to results

...with a significant contribution to net income

Net income from bancassurance segment reporting1 breakdown, as % of total 1H16 (trailing 12 months)

Large and profitable businesses...

(1) Trailing 12 months excluding extraordinary expenses and SRF contribution in December 2015.

Banking business

43%

30%

17%

6% 4%

VidaCaixa Group

CaixaBank Payments +

Comercia GP

CaixaBank AM

CaixaBank Consumer Finance +

MicroBank

10.1% Bancassurance RoTE1

5.5 pp Contribution from non-banking businesses to bancassurance RoTE1

A resilient model for a low rate environment

One-stop financial shop

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

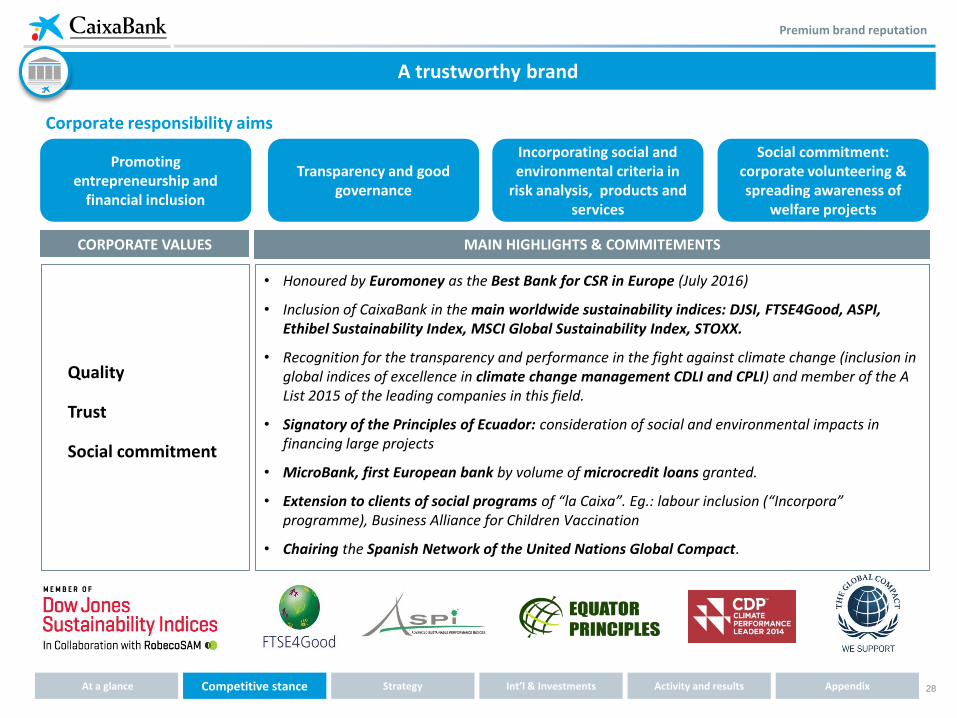

28

• Honoured by Euromoney as the Best Bank for CSR in Europe (July 2016)

• Inclusion of CaixaBank in the main worldwide sustainability indices: DJSI, FTSE4Good, ASPI, Ethibel Sustainability Index, MSCI Global Sustainability Index, STOXX.

• Recognition for the transparency and performance in the fight against climate change (inclusion in global indices of excellence in climate change management CDLI and CPLI) and member of the A List 2015 of the leading companies in this field.

• Signatory of the Principles of Ecuador: consideration of social and environmental impacts in financing large projects

• MicroBank, first European bank by volume of microcredit loans granted.

• Extension to clients of social programs of “la Caixa”. Eg.: labour inclusion (“Incorpora” programme), Business Alliance for Children Vaccination

• Chairing the Spanish Network of the United Nations Global Compact.

CORPORATE VALUES MAIN HIGHLIGHTS & COMMITEMENTS

Quality

Trust

Social commitment

Premium brand reputation

Promoting entrepreneurship and

financial inclusion

Transparency and good governance

Social commitment: corporate volunteering & spreading awareness of

welfare projects

Incorporating social and environmental criteria in

risk analysis, products and services

Corporate responsibility aims

A trustworthy brand

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

29

Strategic Plan [2015-2018]

30

Strategic Plan 2015-2018

Strategic priorities 2015-2018

Best-in-class in quality of service and reputation

Sustainable profitability above cost of capital

Optimisation of capital allocation

Enhance our leadership in banking digitalisation

Retain and attract the best talent

strategic priorities

Committed to trustworthy and profitable banking

5

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

31

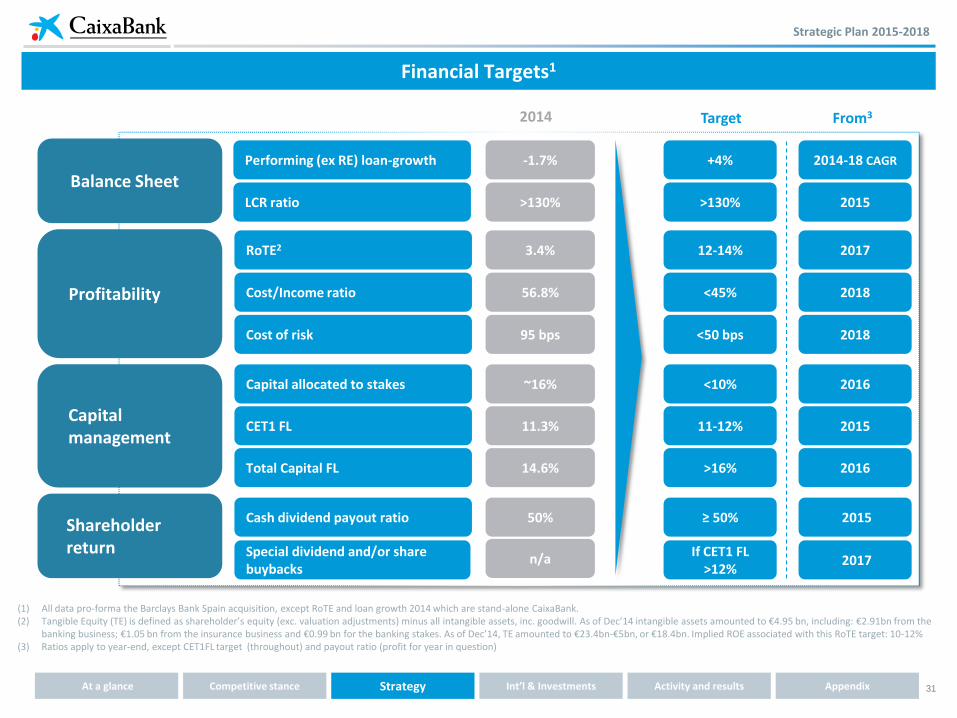

Financial Targets1

2014 Target From3

(1) All data pro-forma the Barclays Bank Spain acquisition, except RoTE and loan growth 2014 which are stand-alone CaixaBank. (2) Tangible Equity (TE) is defined as shareholder’s equity (exc. valuation adjustments) minus all intangible assets, inc. goodwill. As of Dec’14 intangible assets amounted to €4.95 bn, including: €2.91bn from the

banking business; €1.05 bn from the insurance business and €0.99 bn for the banking stakes. As of Dec’14, TE amounted to €23.4bn-€5bn, or €18.4bn. Implied ROE associated with this RoTE target: 10-12% (3) Ratios apply to year-end, except CET1FL target (throughout) and payout ratio (profit for year in question)

Profitability

Capital management

CET1 FL

Capital allocated to stakes

Cash dividend payout ratio

RoTE2

Total Capital FL

Cost/Income ratio

Cost of risk

Performing (ex RE) loan-growth

11-12%

<10%

≥ 50%

12-14%

>16%

<45%

<50 bps

+4%

Balance Sheet LCR ratio >130%

2015

2016

2015

2017

2016

2018

2018

2014-18 CAGR

2015

Shareholder return Special dividend and/or share

buybacks If CET1 FL

>12% 2017

11.3%

~16%

50%

3.4%

14.6%

56.8%

95 bps

-1.7%

>130%

n/a

Strategic Plan 2015-2018

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

32

↓ Cost to income

%

56.8% <45%

2014 PF 2018

2014 2017-2018

3.4%

12-14%

RoTE1

x4

Core income: NII+Fees

CoR normalisation C/I ratio, in %

Capital optimisation

95 <50

2014 PF 2018

Value distribution

Strong solvency & liquidity

6.4

~8

2014 PF 2018

€ bn

bps

16% <10%

2014PF 2016

Capital consumption of non-controlled stakes as % of total

6% CAGR

Note: 2014 data is pro forma the acquisition of Barclays Bank Spain (2014PF) except RoTE data, which corresponds to CaixaBank standalone (1) Breakdown of €4.95 bn of intangible assets as of December 2014: €2.91 bn from the banking business; €1.05 bn from the insurance business and €0.99 bn for banking stakes

RoTE to be boosted by improved operating performance and cost of risk normalisation

Strategic Plan 2015-2018

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

33

3.4%

12-14%

2.9% 1.1%

2.1%

2.1%

7.3%

1.9%

-6.6%

-1.3%

ROTE 2014 (CaixaBank standalone)

NII Fees Other income Operating costs Loan loss and other provisions

Loss on disposal of RE assets

Taxes Accumulated equity exceeding

11% target

ROTE 2017-2018

1

2

3

2

Higher core revenues

Lower provisioning and lower RE losses

Flat costs

(1) RoTE decomposition by change of contribution of P&L lines (2014 pro forma the acquisition of Barclays Bank Spain) as % of regulatory capital excluding intangibles. The item labelled “Accumulated equity exceeding 11% target” measures the decrease in RoTE associated with a higher capital base.

(2) Other income includes dividends and income from associates, trading income and “other income” as defined in quarterly reporting.

Increased revenues combined with a lower cost of risk are the key RoTE drivers1

Strategic Plan 2015-2018

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

34

Freeing up capital from equity portfolio and real estate exposure

Freeing up capital from the equity portfolio

Early and over-delivery of strategic ambition

2011

2014

2016

24%

16%

<7%

June

December

June

Capital allocated to non-controlled stakes, as % of total capital charge(1)

(1) Capital allocation defined as the capital consumption of the investment portfolio over total capital charge

Further optimisation with continued wind-down of RE NPAs

~11

<5

2014 PF Barclays 2018 Ambition

-60%

Over the life of the strategic plan

Ambition 2015-18: 60% net non-performing RE assets

OREO plus RE developer NPLs (net of provisions), €Bn

Strategic Plan 2015-2018

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

vs. Strategic target of

<10% by YE16

35

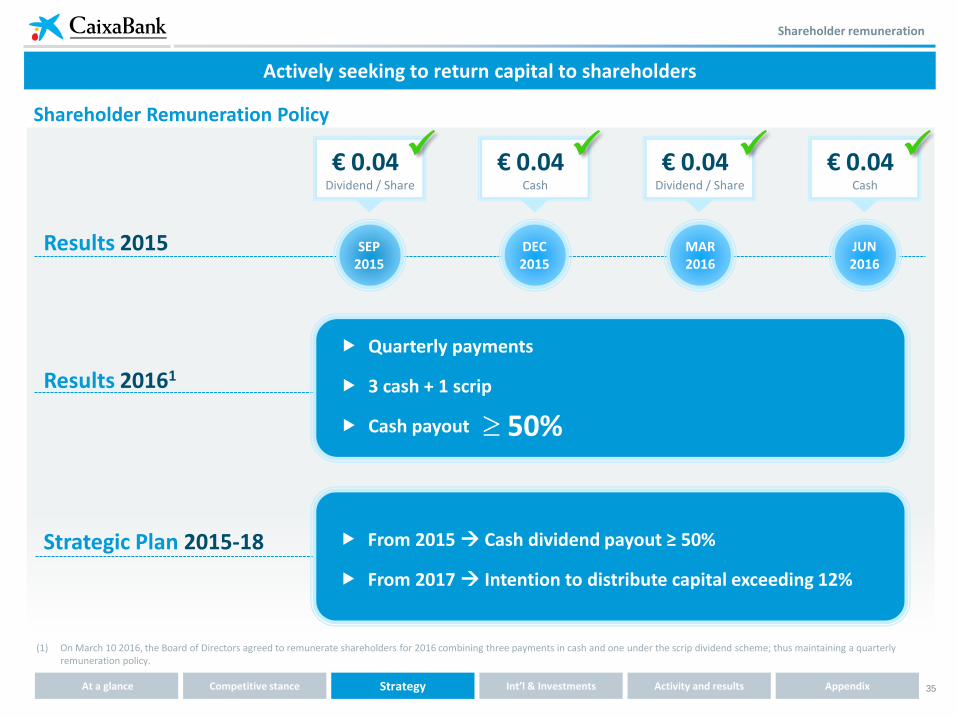

Results 20161

Shareholder remuneration

Actively seeking to return capital to shareholders

Shareholder Remuneration Policy

(1) On March 10 2016, the Board of Directors agreed to remunerate shareholders for 2016 combining three payments in cash and one under the scrip dividend scheme; thus maintaining a quarterly remuneration policy.

Results 2015 SEP 2015

DEC 2015

MAR 2016

JUN 2016

Dividend / Share

€ 0.04 Cash

€ 0.04 Dividend / Share

€ 0.04 Cash

€ 0.04

Quarterly payments

3 cash + 1 scrip

Cash payout 50%

Strategic Plan 2015-18

From 2015 Cash dividend payout ≥ 50%

From 2017 Intention to distribute capital exceeding 12%

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

36

International presence & [Investments]

37

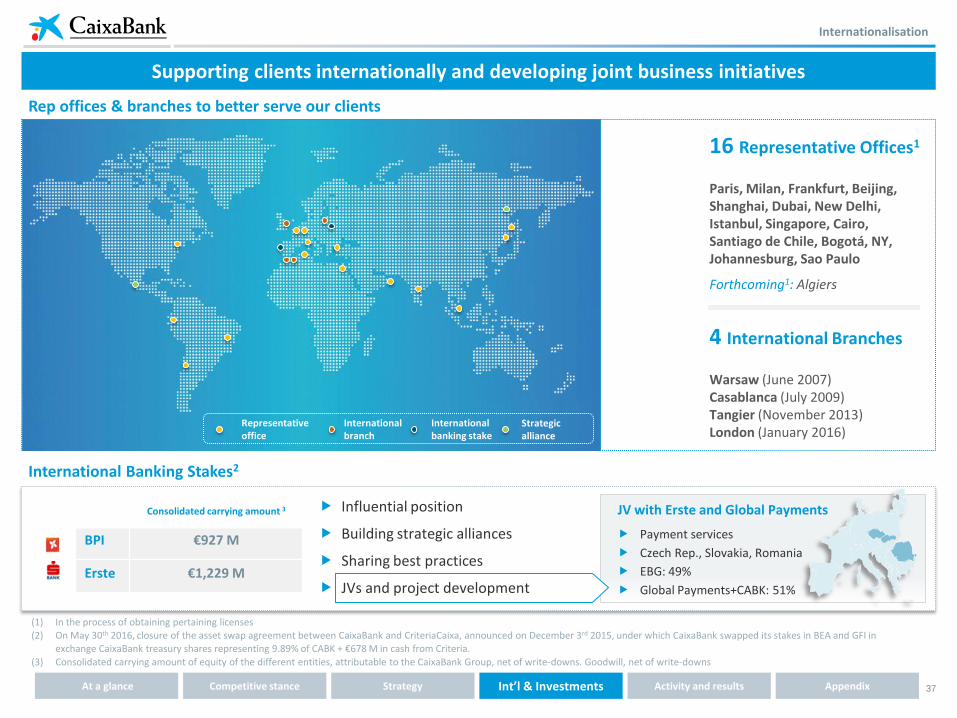

Internationalisation

Supporting clients internationally and developing joint business initiatives

16 Representative Offices1

Paris, Milan, Frankfurt, Beijing, Shanghai, Dubai, New Delhi, Istanbul, Singapore, Cairo, Santiago de Chile, Bogotá, NY, Johannesburg, Sao Paulo

Forthcoming1: Algiers

4 International Branches

Warsaw (June 2007) Casablanca (July 2009) Tangier (November 2013) London (January 2016)

Rep offices & branches to better serve our clients

International Banking Stakes2

Consolidated carrying amount 3

BPI €927 M

Erste €1,229 M

(1) In the process of obtaining pertaining licenses (2) On May 30th 2016, closure of the asset swap agreement between CaixaBank and CriteriaCaixa, announced on December 3rd 2015, under which CaixaBank swapped its stakes in BEA and GFI in

exchange CaixaBank treasury shares representing 9.89% of CABK + €678 M in cash from Criteria.

(3) Consolidated carrying amount of equity of the different entities, attributable to the CaixaBank Group, net of write-downs. Goodwill, net of write-downs

JV with Erste and Global Payments

Payment services

Czech Rep., Slovakia, Romania

EBG: 49%

Global Payments+CABK: 51%

Influential position

Building strategic alliances

Sharing best practices

JVs and project development

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

Representative office

International branch

International banking stake

Strategic alliance

38

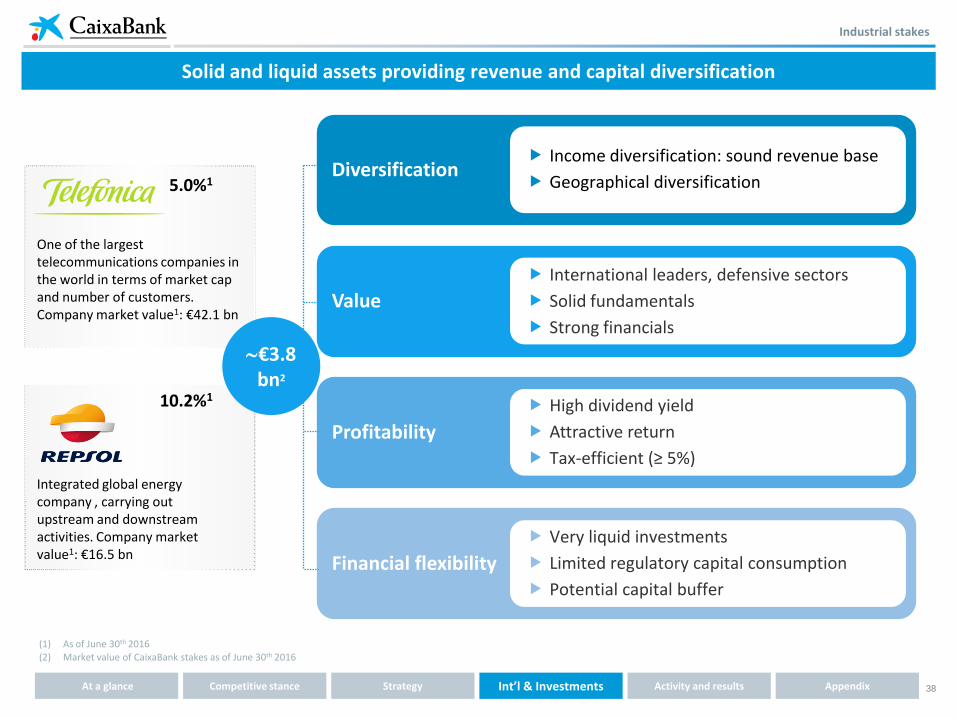

Industrial stakes

5.0%1

One of the largest telecommunications companies in the world in terms of market cap and number of customers. Company market value1: €42.1 bn

10.2%1

Integrated global energy company , carrying out upstream and downstream activities. Company market value1: €16.5 bn

(1) As of June 30th 2016 (2) Market value of CaixaBank stakes as of June 30th 2016

Diversification

Value

Profitability

Financial flexibility

Income diversification: sound revenue base

Geographical diversification

Very liquid investments

Limited regulatory capital consumption

Potential capital buffer

High dividend yield

Attractive return

Tax-efficient (≥ 5%)

International leaders, defensive sectors

Solid fundamentals

Strong financials

€3.8bn2

Solid and liquid assets providing revenue and capital diversification

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

39

Activity & results [1H 2016]

40

Earnings rebound as key operating metrics improve

2Q 2016 Highlights

Performing loan-book inflection confirmed (+1.6% ytd/+1.4% qoq)

Further growth in production of consumer and retail mortgage loans (58% and 46% yoy)

Sharp increase in customer funds (+2.7% ytd/+3.0% qoq)

Insurance (+8.4% ytd/+4.1% qoq) bolsters on-B/S funds and increases contribution to core business

Revenues grow on solid operating performance

Positive asset

quality trends continue

Solid capital metrics despite persistent market volatility: CET1 FL at 11.5% (-9 bps ytd); total FL capital at 14.7% (+6 bps ytd)

Rationalisation of non-controlled stakes and early delivery of strategic target:

closing of BEA/GFI disposal reduces capital consumption of stakes to <7% while TBVPS +0.5% qoq

Improvement in activity levels confirmed

1

2

3

Solid solvency

metrics and better capital allocation

4

Steady reduction in NPLs (-5.9% ytd/-2.0% qoq) with ratio down 56 bps ytd to 7.3%

Gradual decline in foreclosed RE assets confirmed (-1.9% ytd/-1.0% qoq)

Another quarter of profits on OREO sales: 3% over sale price in 1H

Net income up 34% qoq

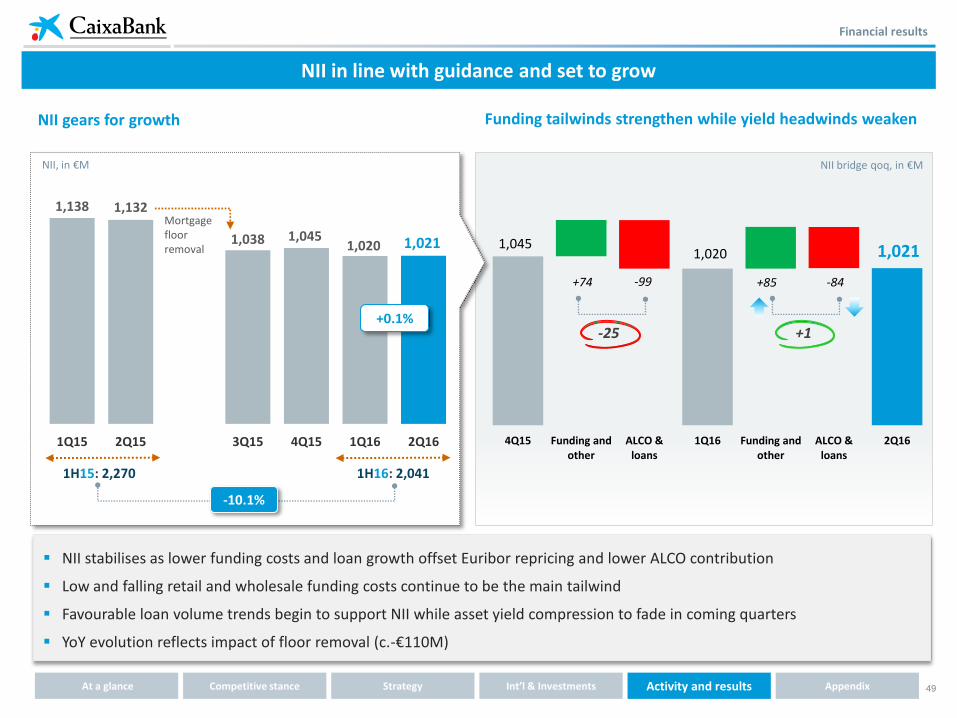

NII stabilises as expected (+0.1% qoq)

Strict margin discipline on both funding and lending: deposit FB yields at 9 bps (-11bps qoq) and loan FB yields at 313 bps1 (+22bps qoq)

Fees show strong recovery across the board (+6.8% qoq)

Profits from VISA Europe disposal offset early retirement provisions

Recurrent costs keep trending down (-0.4% qoq)

CoR at 0.45%2 remains below year-end guidance (0.50%)

(1) Loans to the private sector (2) Trailing 12 months

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

41

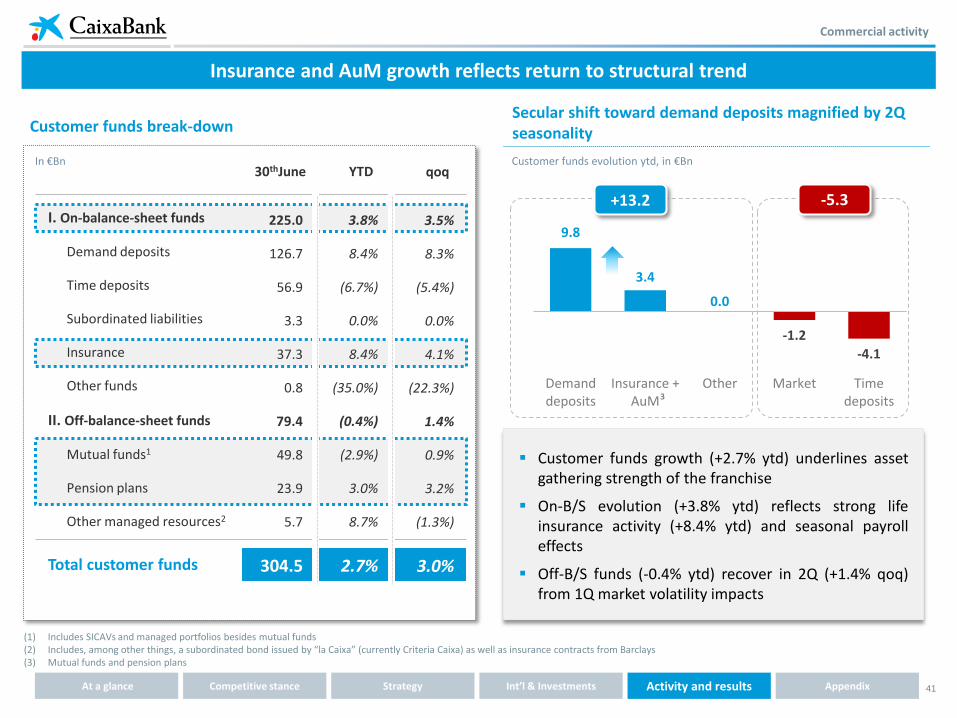

Commercial activity

(1) Includes SICAVs and managed portfolios besides mutual funds (2) Includes, among other things, a subordinated bond issued by “la Caixa” (currently Criteria Caixa) as well as insurance contracts from Barclays (3) Mutual funds and pension plans

Secular shift toward demand deposits magnified by 2Q seasonality

Insurance and AuM growth reflects return to structural trend

Customer funds break-down

Customer funds evolution ytd, in €Bn

I. On-balance-sheet funds

Demand deposits

Time deposits

Subordinated liabilities

Insurance

Other funds

II. Off-balance-sheet funds

Mutual funds1

Pension plans

Other managed resources2

Total customer funds

225.0

126.7

56.9

3.3

37.3

0.8

79.4

49.8

23.9

5.7

304.5

30thJune

3.8%

8.4%

(6.7%)

0.0%

8.4%

(35.0%)

(0.4%)

(2.9%)

3.0%

8.7%

2.7%

YTD In €Bn

Customer funds growth (+2.7% ytd) underlines asset gathering strength of the franchise

On-B/S evolution (+3.8% ytd) reflects strong life insurance activity (+8.4% ytd) and seasonal payroll effects

Off-B/S funds (-0.4% ytd) recover in 2Q (+1.4% qoq) from 1Q market volatility impacts

3.5%

8.3%

(5.4%)

0.0%

4.1%

(22.3%)

1.4%

0.9%

3.2%

(1.3%)

3.0%

qoq

+13.2 -5.3

-4.1

-1.2

0.0

3.4

9.8

Time deposits

Market Other Insurance + AuM

Demand deposits 3

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

42

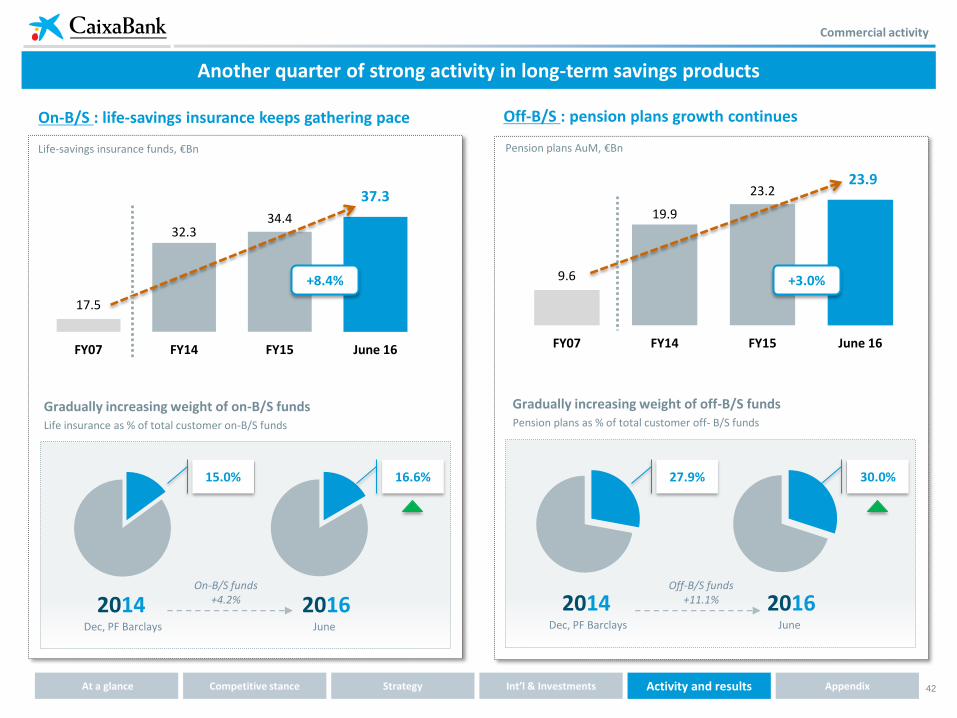

Another quarter of strong activity in long-term savings products

Commercial activity

2016 June

2014 Dec, PF Barclays

On-B/S : life-savings insurance keeps gathering pace

Life-savings insurance funds, €Bn

Off-B/S : pension plans growth continues

Pension plans AuM, €Bn

17.5

32.3 34.4

37.3

FY07 FY14 FY15 June 16

+8.4% 9.6

19.9

23.2 23.9

FY07 FY14 FY15 June 16

+3.0%

15.0%

Gradually increasing weight of on-B/S funds

16.6%

Life insurance as % of total customer on-B/S funds

Gradually increasing weight of off-B/S funds Pension plans as % of total customer off- B/S funds

2016 June

2014 Dec, PF Barclays

27.9% 30.0%

On-B/S funds +4.2%

Off-B/S funds +11.1%

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

43

Delivering steady market share growth in insurance and pensions

Commercial activity

Production, €Bn

Life-risk insurance Savings insurance and pension plans

Sources: INVERCO, ICEA

Production, €M

Market share in savings insurance and pension plans, %

Production2, €Bn

Market share2 in non-life, %

1H16

Market share in life-risk , %

Market share, % 1H16 Market share, % 1H16 +13% yoy +78% yoy +6% yoy +20% yoy CABK network3

+57 bps YTD

+677 bps since 2010

+306 bps YTD

+1,040 bps

since 2010

27.2% Health ins.

9.0% Household ins.

Non-life insurance

375 390 433 497

569 656

732

2010 2011 2012 2013 2014 2015 1H16 TTM

4.8

6.1 5.6

6.1 6.7

8.4

10.4

2010 2011 2012 2013 2014 2015 1H16 TTM

16.0%

22.8%

2010 Jun 16

5.8%

9.8%

2010 Jun 16

10.1%

20.5%

2010 Mar 16

1 1 1

1.9 2.0

2.4 2.6

2.8 3.0 3.1

2010 2011 2012 2013 2014 2015 1H16 TTM

(1) Trailing 12 months (2) Production and market share of SegurCaixa Adeslas (3) Production of CABK network accounts for 40% of total SegurCaixa Adeslas production in 1H16

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

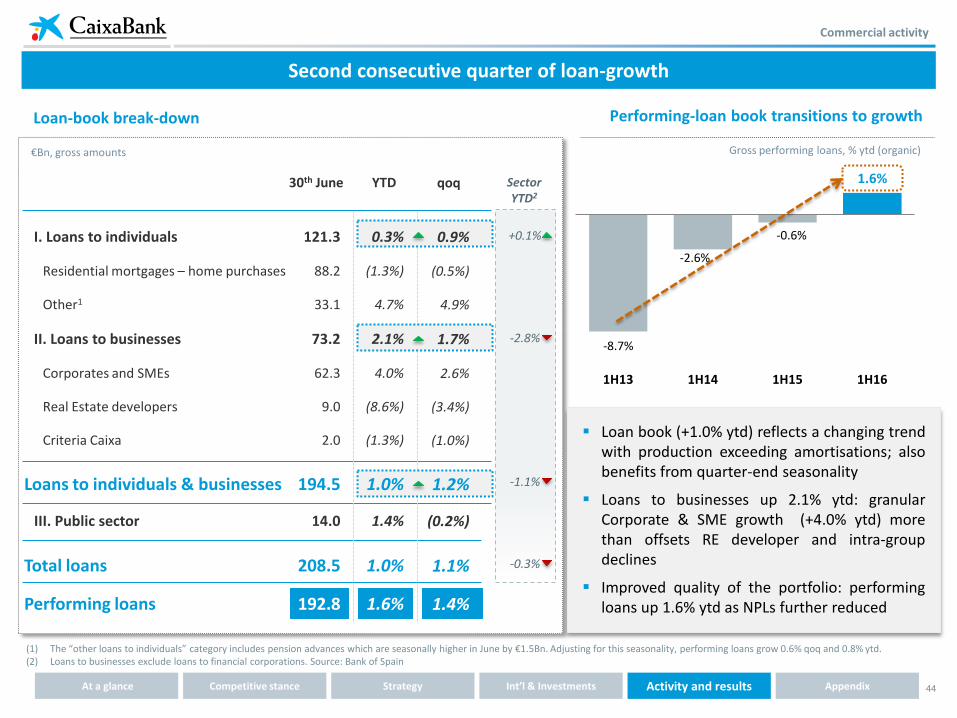

44

-8.7%

-2.6%

-0.6%

1.6%

1H13 1H14 1H15 1H16

I. Loans to individuals

Residential mortgages – home purchases

Other1

II. Loans to businesses

Corporates and SMEs

Real Estate developers

Criteria Caixa

Loans to individuals & businesses

III. Public sector

Total loans

Performing loans

30th June YTD

€Bn, gross amounts

qoq

Loan-book break-down

121.3

88.2

33.1

73.2

62.3

9.0

2.0

194.5

14.0

208.5

192.8

Performing-loan book transitions to growth

Gross performing loans, % ytd (organic)

Second consecutive quarter of loan-growth

Loan book (+1.0% ytd) reflects a changing trend with production exceeding amortisations; also benefits from quarter-end seasonality

Loans to businesses up 2.1% ytd: granular Corporate & SME growth (+4.0% ytd) more than offsets RE developer and intra-group declines

Improved quality of the portfolio: performing loans up 1.6% ytd as NPLs further reduced

(1) The “other loans to individuals” category includes pension advances which are seasonally higher in June by €1.5Bn. Adjusting for this seasonality, performing loans grow 0.6% qoq and 0.8% ytd. (2) Loans to businesses exclude loans to financial corporations. Source: Bank of Spain

Commercial activity

-2.8%

-1.1%

+0.1%

Sector YTD2

0.9%

(0.5%)

4.9%

1.7%

2.6%

(3.4%)

(1.0%)

1.2%

(0.2%)

1.1%

1.4%

0.3%

(1.3%)

4.7%

2.1%

4.0%

(8.6%)

(1.3%)

1.0%

1.4%

1.0%

1.6%

-0.3%

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

45

Positive production dynamics drive loan book and margin growth

Commercial activity

Loan production gathers pace

New lending growth, % 1H16 vs. 1H15

... with increasing margins

796 863

950 970

1,150

1,463

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

+27%

+70%

Consumer lending1

Residential mortgages

Corporate and SMEs

+58%

+46%

+24%

Loans to the private sector front book yields, bps qoq

Faster growth in higher yielding segments

(1) CaixaBank and MicroBank personal loans plus new lending by CaixaBank Consumer Finance (2) Front book yield includes CaixaBank and MicroBank personal loans but excludes CaixaBank Consumer Finance (3) Click & Go loans represent 19% of total personal loans sold through CaixaBank network

New consumer lending1 evolution, in €M

FB yield2

9%

+22

+10

+38

Total

Retail & SMEs

Corporate

25% online

Pre-approved instant consumer loan (Click & Go loans3) sales by channel, % of total sold 1H16

+194% yoy

Technology enables seamless combination of purchasing and financing decisions

39% branches

25% mobile 11% ATMs

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

46

Growth in lending to individuals further supported by better mortgage trends

Commercial activity

46% of 1H16 household mortgages at fixed rates

... also supported by slower mortgage deleveraging

Change in residential mortgages portfolio qoq in €Bn

-1.0 -1.0 -1.0

-1.1

-0.7

-0.4

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

New mortgages on clear upward trend

657

1,062

1,554

2Q14 2Q15 2Q16

+46%

+136%

... supported by positive macro dynamics

-6%

10%

16%

1H15 1H16 1H14

Sector data: housing sales1, % yoy

(1) Source: INE. For 1H16, growth for the period refers to Jan-May (latest available data)

New residential mortgages, €M

Outperforming the sector in credit to individuals

Loans to individuals, % ytd

0.3%

0.1%

Sector

FB yield

2%

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

47

Recovery in revenues and falling costs lead to significant bottom line improvement

1H16

Consolidated income statement1

(1) In relation to the income statement for 2015 and for 1Q 2016, Bank of Spain Circular 5/2014 has resulted in the restatement of gains and losses on the purchase and sale of foreign currency, which are no longer presented under Trading income, but under Net fee and commission income.

(2) Barclays Spain consolidated from 1st January 2015. 1H15 includes, among others, €602M of badwill from the Barclays Spain acquisition (including fair value adjustments of the assets and liabilities of Barclays); €64M of impairment due to asset obsolescence and €257M in restructuring costs associated with the Barclays Spain acquisition

yoy (%) In €M

Net interest income

Net fees and commissions1

Income from investments & associates

Trading income1

Income and exp. from insurance

Other operating income & exp.

Gross income

Recurring expenses

Extraordinary operating expenses

Pre-impairment income

Impairment losses & others

Gains/losses on assets disposals & others2

Pre-tax income

Income tax

Profit for the period

Minority interests

Profit attributable to the Group

(10.1)

(6.1)

(18.8)

(8.1)

38.3

(11.3)

(2.5)

3.9

(36.6)

59.4

(9.1)

(9.9)

2,041

1,010

400

593

140

(135)

4,049

(2,002)

0

2,047

(912)

(247)

888

(243)

645

7

638

2,270

1,076

492

647

101

(22)

4,564

(2,053)

(541)

1,970

(1,439)

26

557

152

709

1

708

0.1

6.8

91.9

22.0

18.6

47.4

10.7

(0.4)

22.7

22.5

(13.7)

35.9

38.3

35.0

34.0

qoq (%) NII stabilises as lower funding costs and loan

growth offset Euribor repricing

Fees (+6.8% qoq) back to sustainable levels after an exceptionally low 1Q

TEF dividend and solid Erste results more than compensate for BEA/GFI sale

VISA Europe disposal grows trading income while 2Q contribution to SRF impacts other operating expenses

Cost discipline brings recurring cost base below €1bn/quarter

CoR down by half in 12 months, from 88 bps in 2Q15 to 45 bps (-13 bps qoq)

Early retirements affect charges to other provisions

Gains/losses on disposals continues to improve on profits from RE sales and absence of 1Q one-offs (REP bond conversion)

Well-entrenched improvement below the line

Solid operating performance

1H15

Financial results

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

48

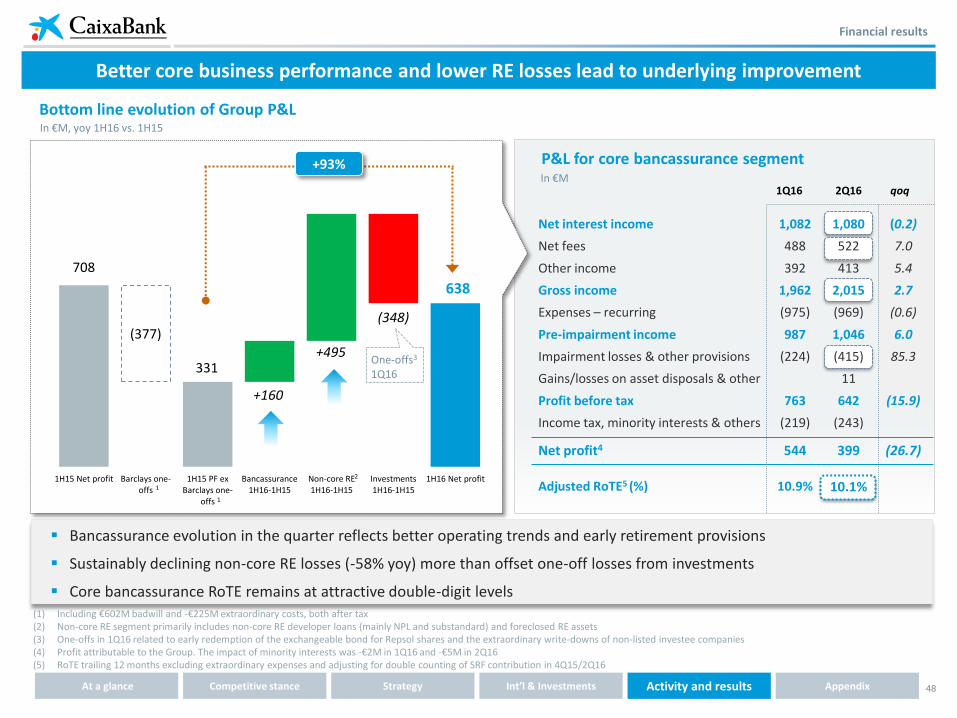

Better core business performance and lower RE losses lead to underlying improvement

Financial results

(1) Including €602M badwill and -€225M extraordinary costs, both after tax (2) Non-core RE segment primarily includes non-core RE developer loans (mainly NPL and substandard) and foreclosed RE assets (3) One-offs in 1Q16 related to early redemption of the exchangeable bond for Repsol shares and the extraordinary write-downs of non-listed investee companies (4) Profit attributable to the Group. The impact of minority interests was -€2M in 1Q16 and -€5M in 2Q16 (5) RoTE trailing 12 months excluding extraordinary expenses and adjusting for double counting of SRF contribution in 4Q15/2Q16

Bottom line evolution of Group P&L In €M, yoy 1H16 vs. 1H15

Net interest income

Net fees

Other income

Gross income

Expenses – recurring

Pre-impairment income

Impairment losses & other provisions

Gains/losses on asset disposals & other

Profit before tax

Income tax, minority interests & others

Net profit4

Adjusted RoTE5 (%)

2Q16 1Q16

1,082

488

392

1,962

(975)

987

(224)

763

(219)

544

10.9%

(0.2)

7.0

5.4

2.7

(0.6)

6.0

85.3

(15.9)

(26.7)

qoq

Bancassurance evolution in the quarter reflects better operating trends and early retirement provisions

Sustainably declining non-core RE losses (-58% yoy) more than offset one-off losses from investments

Core bancassurance RoTE remains at attractive double-digit levels

1,080

522

413

2,015

(969)

1,046

(415)

11

642

(243)

399

10.1%

In €M

P&L for core bancassurance segment

2

1

1

708

331

638

(377)

+160

+495

(348)

1H15 Net profit Barclays one-offs

1H15 PF ex Barclays one-

offs

Bancassurance 1H16-1H15

Non-core RE 1H16-1H15

Investments 1H16-1H15

1H16 Net profit

One-offs3 1Q16

+93%

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

49

NII in line with guidance and set to grow

NII gears for growth

1,138 1,132

1,038 1,045 1,020 1,021

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

+0.1%

NII bridge qoq, in €M

NII, in €M

Funding tailwinds strengthen while yield headwinds weaken

NII stabilises as lower funding costs and loan growth offset Euribor repricing and lower ALCO contribution

Low and falling retail and wholesale funding costs continue to be the main tailwind

Favourable loan volume trends begin to support NII while asset yield compression to fade in coming quarters

YoY evolution reflects impact of floor removal (c.-€110M)

Mortgage floor removal 1,045

1,020 1,021

+74 -99 +85 -84

4Q15 Funding and other

ALCO & loans

1Q16 Funding and other

ALCO & loans

2Q16

+1 -25

1H15: 2,270 1H16: 2,041

-10.1%

Financial results

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

50

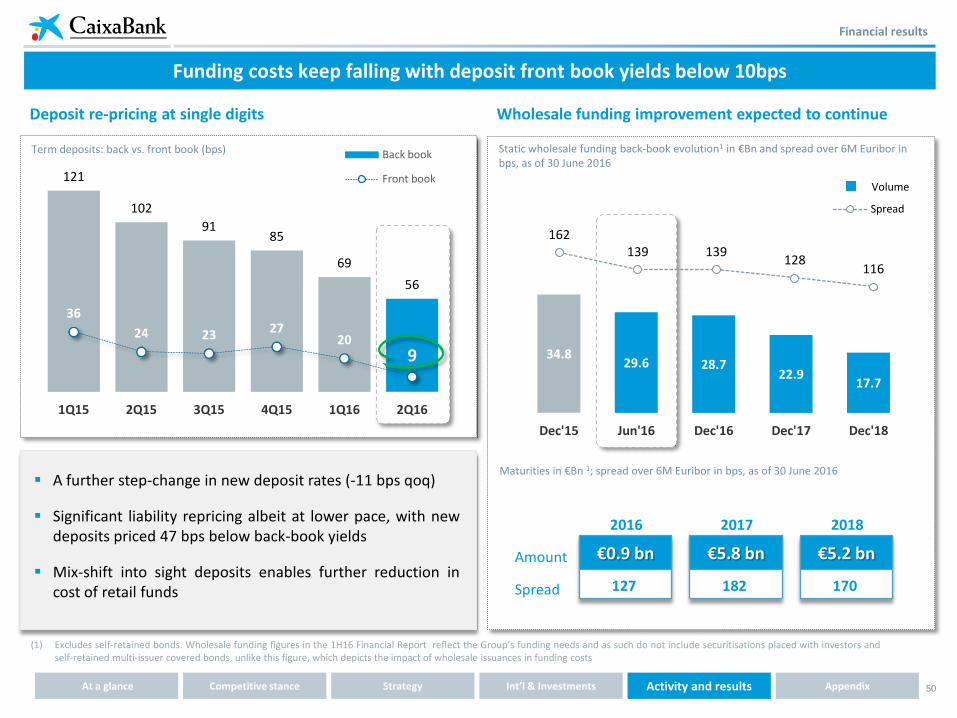

€0.9 bn

2016

127 Spread

€5.8 bn

2017

182

€5.2 bn

2018

170

Amount

Maturities in €Bn 1; spread over 6M Euribor in bps, as of 30 June 2016

162 139 139

128 116

Spread

(1) Excludes self-retained bonds. Wholesale funding figures in the 1H16 Financial Report reflect the Group’s funding needs and as such do not include securitisations placed with investors and self-retained multi-issuer covered bonds, unlike this figure, which depicts the impact of wholesale issuances in funding costs

Funding costs keep falling with deposit front book yields below 10bps

Static wholesale funding back-book evolution1 in €Bn and spread over 6M Euribor in bps, as of 30 June 2016

Wholesale funding improvement expected to continue Deposit re-pricing at single digits

Term deposits: back vs. front book (bps)

A further step-change in new deposit rates (-11 bps qoq)

Significant liability repricing albeit at lower pace, with new deposits priced 47 bps below back-book yields

Mix-shift into sight deposits enables further reduction in cost of retail funds

Volume

34.8 29.6 28.7

22.9 17.7

Dec'15 Jun'16 Dec'16 Dec'17 Dec'18

121

102

91 85

69

56

36

24 23 27 20

9

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Back book

Front book

Financial results

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

51

(1) Banking book fixed-income securities portfolio, excluding trading book assets and liquidity management portfolio of €3.9 Bn, as of the end of the quarter. As part of its ALCO management CaixaBank holds a portfolio of fixed income investments including, among others, bonds guaranteed by the Kingdom of Spain such as ICO, FADE, FROB and others); ESM bonds; as well as Spanish covered bonds. The sovereign bond portfolio is made up mostly of Spanish and Italian government bonds.

(2) Peers include Bankia, Bankinter, BBVA Spain + RE business, Popular, Sabadell (ex TSB). Latest available data: CaixaBank, Bankia, Bankinter and Sabadell (ex TSB) as of 2Q16; other peers as of 1Q16. Sources: Based on company information

Active management of ALCO book to benefit from market opportunities

ALCO portfolio1 evolution

25.4

17.2 15.6 15.0 13.5 12

6.7

6.4 7.7 7.0 5.5

4.7

32.1

23.6 23.3 22.0 19.0

16.6

Mar'15 Jun'15 Sep'15 Dec'15 Mar'16 June'16

Spanish sovereign bonds

Other

In €Bn

ALCO book yields fall qoq:

Lower average life of the portfolio due to tactical risk reduction, taking advantage of market opportunities to realise gains

Lower portfolio yields reflect maturities of high-yielding bonds

Low dependence on carry trade and lower risk relative to peers with option to grow if market opportunities arise

4.7%

7.7% 9.6%

13.6% 14.6% 14.7%

CaixaBank Peer 1 Peer 2 Peer 3 Peer 4 Peer 5

Lower dependence on ALCO book ALCO book over total assets2, %

3.4% 3.6% 3.5% 3.1% 3.0% 2.7%

3.1 3.4 4.2 4.6 3.9 3.7

Average life Years

Yield %

-29.7%

-12.6%

Financial results

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

52

Loan-book yields

FB (ex public sector) up 22 bps qoq and accretive to the BB underpinned by mix shift to higher-yielding segments

BB yields down -10 bps qoq still dragged by Euribor repricing (-5 bps), commercial flows and other

Asset yield compression expected to fade in coming quarters

In bps

(1) The cost of customer funds reflects the cost of both demand and time deposits, as well as repos with retail clients. Excludes the cost of institutional issuance and subordinated liabilities

Front book yields in loan portfolio are widening

Margins supported by steady liability repricing

Customer funds1 Loans and credits Customer spread

Customer spread, in %

2.16 2.18 2.03 2.06 2.07 2.04

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

2.80 2.70 2.47 2.47 2.38 2.28

0.64 0.52 0.44 0.41 0.31 0.24

NIM, in %

1.32 1.33 1.23 1.21 1.20 1.21

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Customer spread declines slightly on lower BB asset yields

NIM slightly up as disposal of BEA/GFI reduces proportion of non-interest bearing assets in balance sheet

280 270 247 247 238 228

293 311 305

283 291

313

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Back book

Front book ex public sector

Financial results

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

53

Insurance and pension fees on an upward trend

Banking and other fees

Mutual funds

Pension plans

Insurance distribution fees

yoy (%) 1H16

646

196

89

79

(11.1)

(4.9)

22.0

12.1

qoq (%)

8.1

1.9

12.2

3.6

Net fees breakdown, €M

Fees show strong recovery in the quarter

Improvement across the board in 2Q

Net fee income1, €M

(1) In relation to the income statement for 2015 and for 1Q 2016, Bank of Spain Circular 5/2014 has resulted in the restatement of gains and losses on the purchase and sale of foreign currency, which are no longer presented under Trading income, but under Net fee and commission income.

Net fees recover sustainable levels after an exceptionally low 1Q

Asset management and insurance fees grow +4.1% yoy, with a rising contribution to total fees (+3 pp yoy)

+6.8%

1H15: 1,076 1H16: 1,010

Insurance + AuM revenues offsetting lower banking fees

Revenues from insurance (ex trading income) and AM activity vs. banking fees, €M

726 646

636 712

1,362 1,358

Banking fees

Revenues from insurance and AuM activity

1H15 1H16

+12%

-11%

-0.3%

538 538 524

515

488

522

+26

+8

1Q15 2Q15 3Q15 4Q15 1Q16 Banking AuM + insurance

2Q16

Financial results

-6.1%

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

54

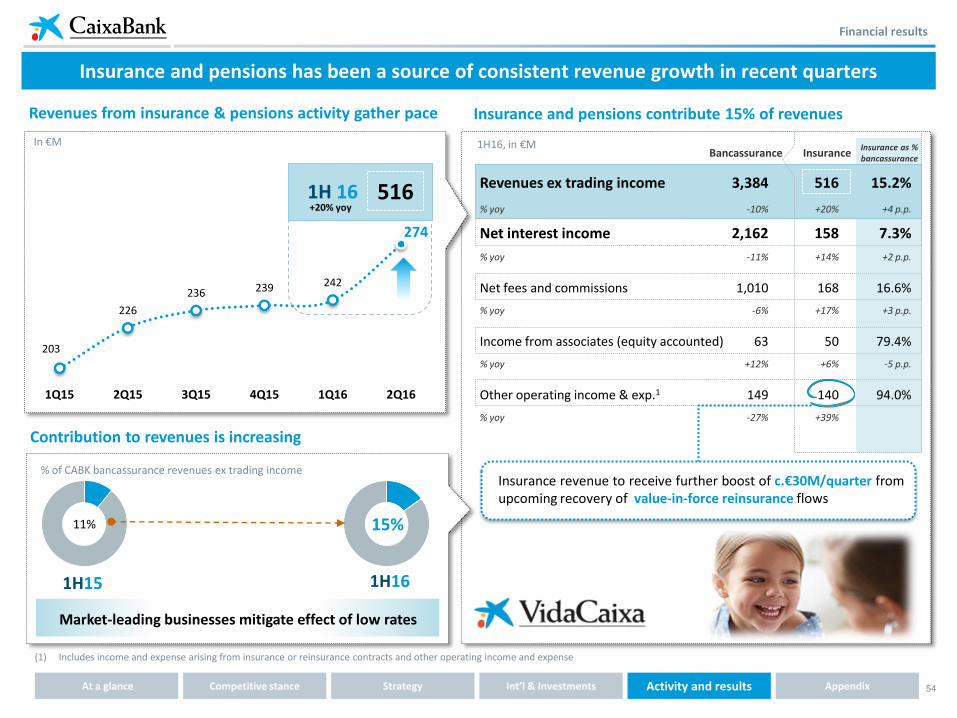

Insurance and pensions has been a source of consistent revenue growth in recent quarters

203

226

236 239 242

274

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Revenues from insurance & pensions activity gather pace

11% 15%

% of CABK bancassurance revenues ex trading income

Market-leading businesses mitigate effect of low rates

Bancassurance 1H16, in €M Insurance as %

bancassurance Insurance

Revenues ex trading income

% yoy

Net interest income

% yoy

Net fees and commissions

% yoy

Income from associates (equity accounted)

% yoy

Other operating income & exp.1

% yoy

3,384

-10%

2,162

-11%

1,010

-6%

63

+12%

149

-27%

516

+20%

158

+14%

168

+17%

50

+6%

140

+39%

15.2%

+4 p.p.

7.3%

+2 p.p.

16.6%

+3 p.p.

79.4%

-5 p.p.

94.0%

Insurance and pensions contribute 15% of revenues

1H15 1H16

Contribution to revenues is increasing

Insurance revenue to receive further boost of c.€30M/quarter from upcoming recovery of value-in-force reinsurance flows

516 1H 16 +20% yoy

Financial results

In €M

(1) Includes income and expense arising from insurance or reinsurance contracts and other operating income and expense

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

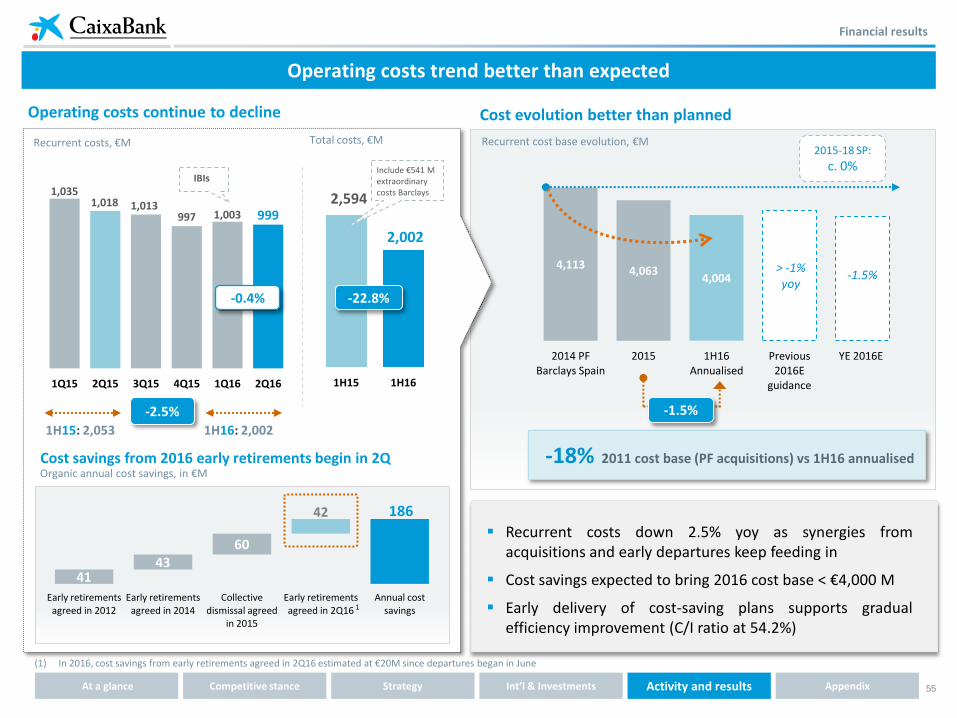

55

Financial results

Operating costs trend better than expected

Operating costs continue to decline

Recurrent costs, €M Total costs, €M

1H15 1H16

-22.8%

2,594

2,002

Include €541 M extraordinary costs Barclays

-2.5%

1,035 1,018 1,013

997 1,003 999

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

IBIs

-0.4%

Cost savings from 2016 early retirements begin in 2Q

186

41 43

60

42

Early retirements agreed in 2012

Early retirements agreed in 2014

Collective dismissal agreed

in 2015

Early retirements agreed in 2Q16

Annual cost savings

Organic annual cost savings, in €M

1H15: 2,053 1H16: 2,002

Cost evolution better than planned

Recurrent cost base evolution, €M

4,113 4,063 4,004 3.999

2014 PF Barclays Spain

2015 1H16 Annualised

Previous 2016E

guidance

YE 2016E

> -1% yoy

-1.5%

2015-18 SP:

c. 0%

Recurrent costs down 2.5% yoy as synergies from acquisitions and early departures keep feeding in

Cost savings expected to bring 2016 cost base < €4,000 M

Early delivery of cost-saving plans supports gradual efficiency improvement (C/I ratio at 54.2%)

-18% 2011 cost base (PF acquisitions) vs 1H16 annualised

-1.5%

1

(1) In 2016, cost savings from early retirements agreed in 2Q16 estimated at €20M since departures began in June

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

56

Financial results

(1) Loan-loss provisions over total gross customer loans plus contingent liabilities, as of the end of the period on a trailing 12 months and on an annualised quarterly basis

Loan loss provisions down by 56% in 12 months

0.99% 0.97%

0.52% 0.40% 0.41% 0.46%

0.91% 0.88%

0.82%

0.73%

0.58%

0.45% 0.50%

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 Guidance YE16

Quarterly annualised

Trailing 12 months

In %

CoR1 below YE guidance

Quarterly annualised

LLPs down more than halve yoy

In €M

1H15: 1,087 1H16: 478

-56.0% -51 bps

CoR down 13 bps qoq to 0.45% below year-end guidance of 0.50%

LLPs down 56 % yoy with slight qoq uptick related to some non-granular NPL entries in Q2

550 537

288

218 225 253

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

12.4%

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

57

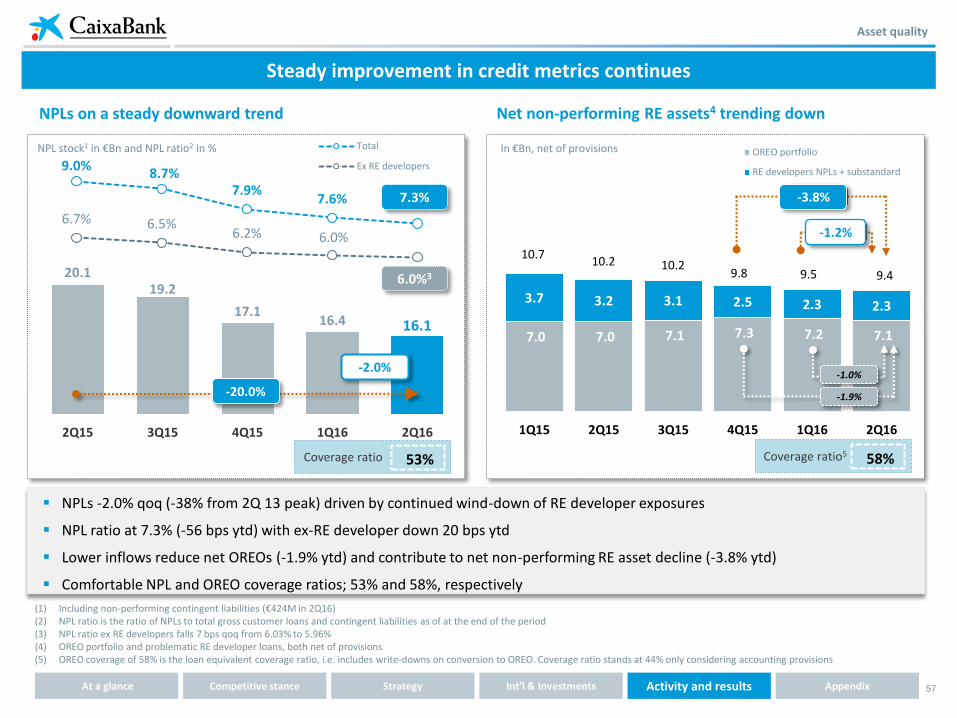

NPLs on a steady downward trend

Asset quality

Steady improvement in credit metrics continues

Net non-performing RE assets4 trending down

(1) Including non-performing contingent liabilities (€424M in 2Q16) (2) NPL ratio is the ratio of NPLs to total gross customer loans and contingent liabilities as of at the end of the period (3) NPL ratio ex RE developers falls 7 bps qoq from 6.03% to 5.96% (4) OREO portfolio and problematic RE developer loans, both net of provisions (5) OREO coverage of 58% is the loan equivalent coverage ratio, i.e. includes write-downs on conversion to OREO. Coverage ratio stands at 44% only considering accounting provisions

NPLs -2.0% qoq (-38% from 2Q 13 peak) driven by continued wind-down of RE developer exposures

NPL ratio at 7.3% (-56 bps ytd) with ex-RE developer down 20 bps ytd

Lower inflows reduce net OREOs (-1.9% ytd) and contribute to net non-performing RE asset decline (-3.8% ytd)

Comfortable NPL and OREO coverage ratios; 53% and 58%, respectively

NPL stock1 in €Bn and NPL ratio2 in %

20.1 19.2

17.1 16.4 16.1

2Q15 3Q15 4Q15 1Q16 2Q16

-2.0%

-20.0%

7.3%

6.0%3

In €Bn, net of provisions

7.0 7.0 7.1 7.3 7.2 7.1

3.7 3.2 3.1 2.5 2.3 2.3

10.7 10.2 10.2

9.8 9.5 9.4

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

OREO portfolio

RE developers NPLs + substandard

-3.8%

-1.2%

-1.0%

-1.9%

53% Coverage ratio 58% Coverage ratio5

9.0% 8.7%

7.9% 7.6%

6.7% 6.5% 6.2% 6.0%

Total

Ex RE developers

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

58

Asset quality

(1) Revenue of RE sales (2) Source: CaixaBank Research forecasts and Spanish Government data

An additional quarter of RE profits with increased sales

Robust and profitable sales with a positive outlook

Disposals, in €M

1

+20% Sales 2Q16 vs. 1Q16

651 610

395

217

Sales Rental

1H15 1H16

Profits, as % of sale price

-11%

+3% +14pp

1H15 1H16

-12%

-9%

-6%

-3%

0%

3%

6%

Mar-10 Sep-11 Mar-13 Sep-14 Mar-16

Spanish housing prices evolution and outlook2, % yoy

RE inflows on downward trend

Better RE fundamentals continue to drive profits on sale of RE assets

Progressive stabilisation of stock and positive price outlook supports focus on value-preservation

Sales maintained at high levels of €610M in 1H16

1.8

1.2

0.6

1H15 1H16 1H14

-48%

Inflows (net of provisions) to OREO portfolio, in €Bn

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

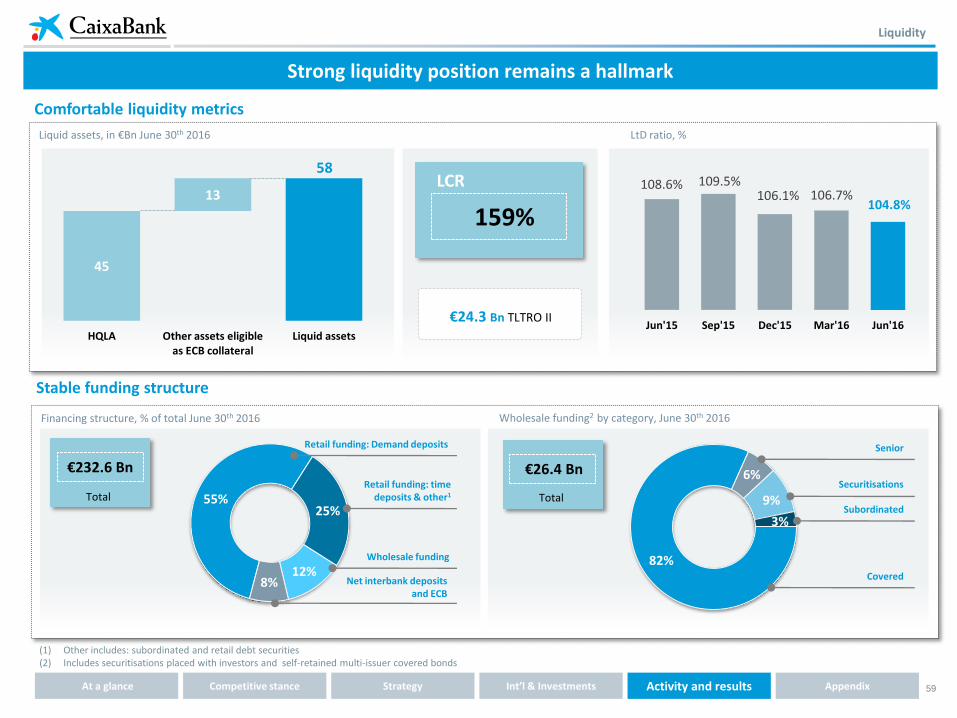

59

Strong liquidity position remains a hallmark

Liquidity

(1) Other includes: subordinated and retail debt securities (2) Includes securitisations placed with investors and self-retained multi-issuer covered bonds

159%

LCR

Comfortable liquidity metrics

Liquid assets, in €Bn June 30th 2016

108.6% 109.5% 106.1% 106.7%

104.8%

Jun'15 Sep'15 Dec'15 Mar'16 Jun'16

LtD ratio, %

Stable funding structure

Financing structure, % of total June 30th 2016

55% 25%

12% 8%

Retail funding: Demand deposits

Retail funding: time deposits & other1

Wholesale funding

Net interbank deposits and ECB

82%

6%

9%

3%

Senior

Securitisations

Subordinated

Covered

Wholesale funding2 by category, June 30th 2016

€232.6 Bn

Total

€26.4 Bn

Total

€24.3 Bn TLTRO II

45

58

13

HQLA Other assets eligible as ECB collateral

Liquid assets

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

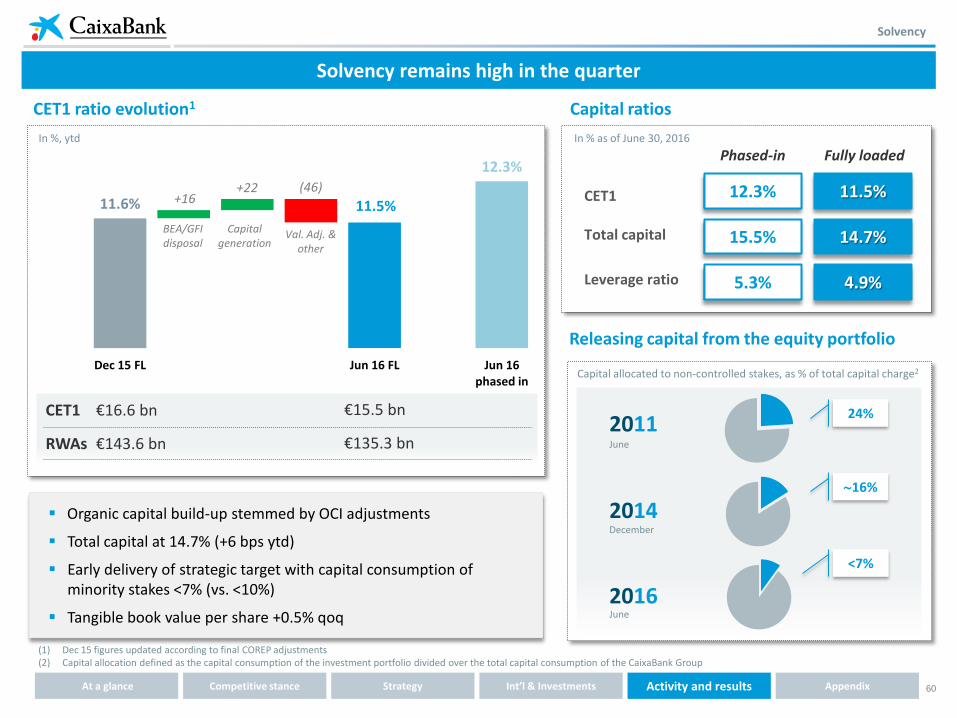

60

Solvency

CET1 ratio evolution1

Solvency remains high in the quarter

Organic capital build-up stemmed by OCI adjustments

Total capital at 14.7% (+6 bps ytd)

Early delivery of strategic target with capital consumption of minority stakes <7% (vs. <10%)

Tangible book value per share +0.5% qoq

CET1

Total capital

Phased-in Fully loaded

12.3% 11.5%

15.5% 14.7%

Leverage ratio 5.3% 4.9%

In % as of June 30, 2016

Capital ratios

(1) Dec 15 figures updated according to final COREP adjustments (2) Capital allocation defined as the capital consumption of the investment portfolio divided over the total capital consumption of the CaixaBank Group

11.6% 11.5%

12.3%

+16 +22 (46)

Dec 15 FL Jun 16 FL Jun 16 phased in

RWAs €143.6 bn

CET1 €16.6 bn

In %, ytd

Capital generation

€15.5 bn

€135.3 bn

Val. Adj. & other

BEA/GFI disposal

Releasing capital from the equity portfolio

24%

16%

<7%

2011 June

2014 December

2016 June

Capital allocated to non-controlled stakes, as % of total capital charge2

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

61

Solvency reinforced in the quarter 2Q 2016: key takeaways

4 NPA rundown continues

3

1 Rebound in revenues with costs down

5

2 Outstanding performance of insurance businesses

Early delivery of capital allocation targets

Improvement in both volumes and margins

Well-equipped to navigate a low rate environment

Final remarks

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

62

[Appendix]

63

(1) As of 20/04/16 (2) As of 22/04/16 (3) As of 26/04/16 (4) As of 13/04/16 (5) As of 18/06/15 (6) As of 27/05/16 (7) As of 10/03/16

Moody’s Investors Service Baa2

BBB

BBB

P-2

A-2

F2

negative

positive

Long term Short term Outlook

Aa2

A+

Rating of covered bond program

stable

A (low) R-1 (low)

stable

(2)

(1)

- (3)

(4)

Appendix

CaixaBank Credit Ratings

(5)

(6)

AA (high) (7)

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

64

Shareholder base and corporate governance

Transparency, independence and good governance are key priorities

Increased free float with diversified investor base

51% Retail

Free float 41%

49% Institutional

Shareholder base by group, In % of share capital as of June 2016

US and Canada 34%

UK/Ireland 23%

Spain 16%

RoW 10%

Geographical distribution of institutional investors1

% of total shares owned by institutional investors, Dec-2015

Rest of Europe 17%

(1) Percentage calculated on the institutional capital base identified at the Shareholder identification elaborated by Nasdaq OMX (2) As of July 19th 2016, two members of the Board (1 proprietary and 1 independent) appointed on June 30th 2016 are pending for approval by the ECB (3) Including 2 from Cajas (Fundación Bancaria Caja Navarra, Fundación Cajasol, Fundación Caja Canarias and Fundación Caja de Burgos Fundación Bancaria). The total number of proprietary directors

including the executive director appointed by “la Caixa” Banking Foundation is 9. (4) One executive director is appointed by “la Caixa” Banking Foundation and, as such, is both executive and proprietary

Number of shareholders, in thousands

Control and management of the bank is shared by the AGM, Board of Directors and Board committees: Audit and control; Executive; Appointments; Remuneration; Risks. The majority shareholder is not overrepresented in the board.

CABK’s relationship with other Group entities is immaterial, performed on an arm’s length basis and governed by the Internal Relations Protocol

Int’l & Investments Activity and results At a glance Competitive stance Strategy Appendix

Board of Directors composition2

Proprietary directors2,3 8 2 Executive directors4

Independent directors2 8

59%

CriteriaCaixa,

Board of

Directors, and

Treasury stock

360

698

2007 June-2016

65

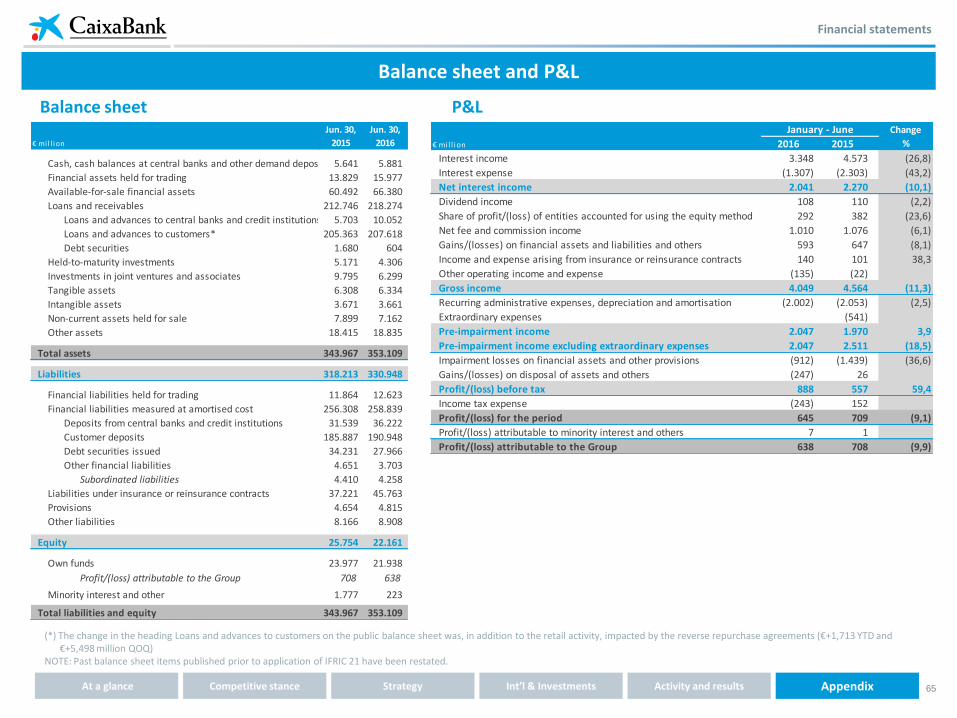

Financial statements

Balance sheet P&L

Balance sheet and P&L

(*) The change in the heading Loans and advances to customers on the public balance sheet was, in addition to the retail activity, impacted by the reverse repurchase agreements (€+1,713 YTD and €+5,498 million QOQ)

NOTE: Past balance sheet items published prior to application of IFRIC 21 have been restated.

€ mi l l ion 2016 2015

Interest income 3.348 4.573 (26,8)

Interest expense (1.307) (2.303) (43,2)

Net interest income 2.041 2.270 (10,1)

Dividend income 108 110 (2,2)

Share of profit/(loss) of entities accounted for using the equity method 292 382 (23,6)

Net fee and commission income 1.010 1.076 (6,1)

Gains/(losses) on financial assets and liabilities and others 593 647 (8,1)

Income and expense arising from insurance or reinsurance contracts 140 101 38,3

Other operating income and expense (135) (22)

Gross income 4.049 4.564 (11,3)

Recurring administrative expenses, depreciation and amortisation (2.002) (2.053) (2,5)

Extraordinary expenses (541)

Pre-impairment income 2.047 1.970 3,9

Pre-impairment income excluding extraordinary expenses 2.047 2.511 (18,5)

Impairment losses on financial assets and other provisions (912) (1.439) (36,6)

Gains/(losses) on disposal of assets and others (247) 26

Profit/(loss) before tax 888 557 59,4

Income tax expense (243) 152

Profit/(loss) for the period 645 709 (9,1)

Profit/(loss) attributable to minority interest and others 7 1

Profit/(loss) attributable to the Group 638 708 (9,9)

Change

%

January - June

Cash, cash balances at central banks and other demand deposits 5.641 5.881

Financial assets held for trading 13.829 15.977

Available-for-sale financial assets 60.492 66.380

Loans and receivables 212.746 218.274

Loans and advances to central banks and credit institutions 5.703 10.052