Clubs & SocietiesClubs & Societies

Done by: Koh Ngin Lan Edna

Preparation of Final Accounts

Sole Proprietorship– Trading & Profit &

Loss Account– Balance Sheet

Partnership– (see sole

proprietorship)– Profit & Loss &

Appropriation A/c• Interest on

drawings• Interest on capital• Salary• Share of profits

– Balance Sheet• Capital A/c• Current A/c

Recap: What have we learnt ?

They are business organisations:– involved in trading activities, ie. the

buying & selling of goods or services

– operate solely to make a profit for their owners

What do they have in common?

Topic for Today … …

Clubs & SocietiesClubs & Societies

At the end of the lesson, you should be able to:– state the difference between a

trading and non-trading organisation

– distinguish between the different accounts kept by a trading and non-trading organisation

Lesson Objectives

Non-Trading Organisations

Clubs, societies and associations

formed to cater and promote

the sporting, cultural and recreational interests of its members.

What are they?

They are not formed with the purpose of making profits.

Clubs & Societies

School

Clubs & Societies

School

Guitar Club

Swimming Club

Mathematics Societysocial,

music

sports, outdoor activities

social, maths puzzles

What are the sources of income & expenses?

What are some of the non-trading organisations in Singapore?– Purpose of existence?

– Sources of income?

– Expenses incurred?

Clubs & Societies

CDAC, Mendaki, Sinda– Purpose:

• To provide tuition schemes at affordable rates• To assist low-income, low-skilled workers to

upgrade their skills• To enhance the well-being of the community

– Income:• Donations, grants from the Govt.

– Expenses:• Day-to-day activities, scholarships, training

programmes

In Singapore … …

Non-Profit Organisations:

National Kidney Foundation (NKF)– Purpose:

• To provide kidney patients with dialysis treatment & drugs at affordable cost.

– Income: • Donations only

– Expenses: • Day-to-day activities, dialysis machines,

research.

In Singapore … …

In Singapore … …

Chinese Swimming Club– Purpose:

• To provide facilities & activities that cater to the sports, recreation & social needs of the family & individual

– Income: • Entrance fees, subscriptions fees, restaurant & karaoke

operations, fruit machines & video games

– Expenses:• Day-to-day activities, eg. repairs & maintenance, utilities

Recreational Activities:

Clubs & Societies

Trading Concern1. Sale of goods2. Receipts from services3. Rent received4. Commission received5. Discount received6. Interest received7. Bad debts recovered8. Profits from the sale of

fixed assets

Non-Trading1. Subscriptions2. Entrance fees3. Profit from sale of

refreshments4. Interest received5. Donations6. Fun fair7. Life membership

subscriptions8. Grants from the

Govt.

Compare the income of a trading & non-trading organisation:

Clubs & Societies

Do you remember?

Receipts

Expenditure

Revenue

Capital Revenue Capital

Clubs & Societies

Trading Concern– Sale of goods– Other income:

• Cash discount received for prompt payment

• Commission revenue

• Rent revenue• Interest on deposit

Clubs & Societies– Membership

subscriptions– Donations– Proceeds from

social activities– Receipts from sale

of refreshments in bar/restaurant

– Rental fees for courts, lockers

Revenue Receipts

Clubs & Societies

Trading Concern– Cost of goods sold– Administrative

expenses, staff wages, stationery, utilities, rental

– Distributive expenses:

• Transport, commission, bad debts

– Depreciation of fixed assets

Clubs & Societies– Entertainment

expenses– Competition prizes– Repairs &

maintenance– Sundry expenses:

• Utilities, staff wages

– Honorarium– Depreciation of fixed

assets– Bar/ Restaurant

expenses

Revenue Expenditure

Trading Concern– Bank loans– Owner’s

contribution

Clubs & Societies– Legacies– Entrance fees (if

capitalised)– Life membership

fees

Clubs & Societies

Capital Receipts

Trading Concerns– Purchase of fixed

assets

Clubs & Societies– Purchase of fixed

assets:• Office equipment• Sports equipment• Furniture, billiard

tables

– Extension of club houses, including legal fees

Clubs & Societies

Capital Expenditure

Clubs & Societies

Similar to trading concerns, clubs & societies need to keep accounts according to accounting concepts & principles

Financial statements are presented to members during the Annual General Meeting (AGM)

Also submitted to the Registrar of Societies

How are the accounts of clubs & societies different from trading concerns?

Clubs & Societies

Trading Concern– Trading Account

• Gross Profit =

Net Sales – Cost of Sales

Clubs & Societies– Bar Trading A/c

• Trading profit =Trading Revenue-

Trading Expenses

Recall that … Difference …

Trading Concern– Cash or Bank

Account:• Records cash

inflows & outflows

Clubs & Societies– Receipts &

Payments Account:

• Is actually a cash book by another name

Recall that … Difference …

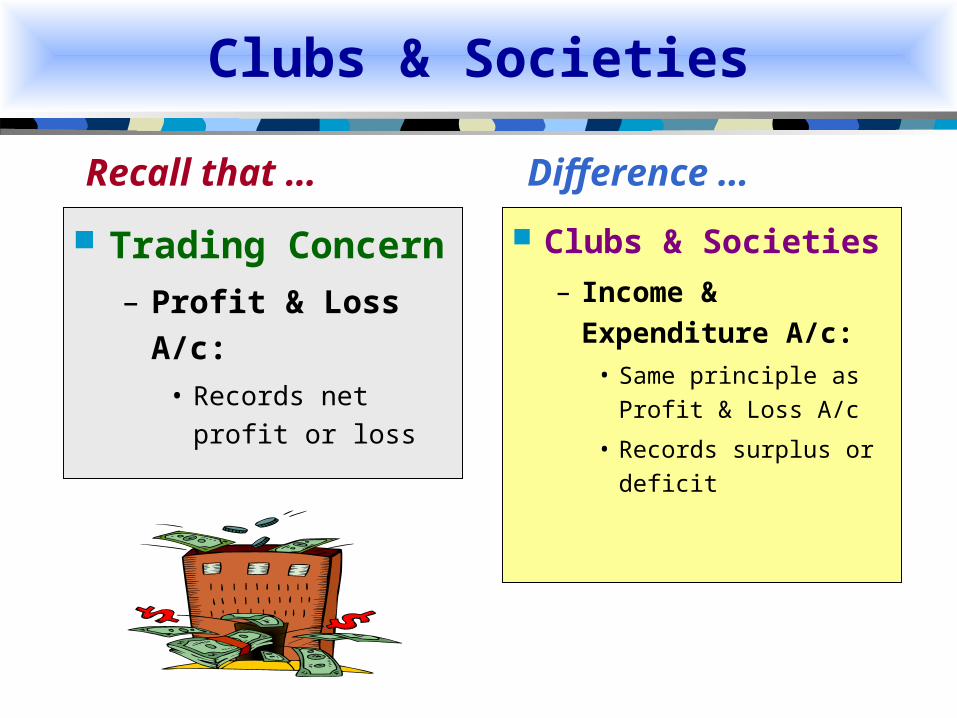

Clubs & Societies

Trading Concern– Profit & Loss A/c:

• Records net profit or loss

Clubs & Societies– Income &

Expenditure A/c:• Same principle as

Profit & Loss A/c

• Records surplus or deficit

Difference …Recall that …

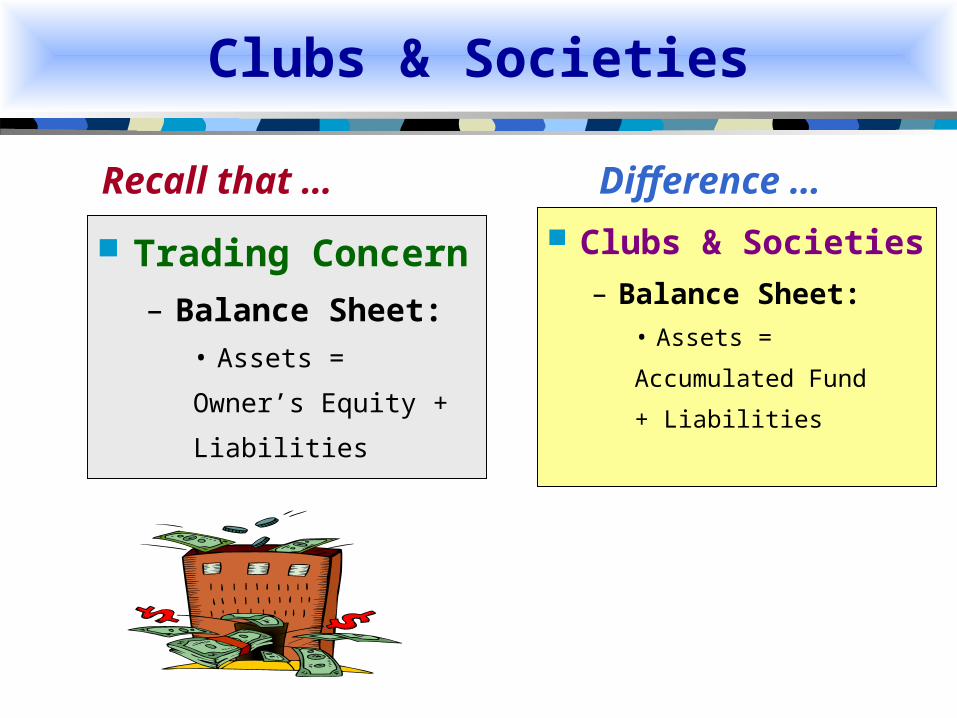

Clubs & Societies

Trading Concern– Balance Sheet:

• Assets =

Owner’s Equity +

Liabilities

Clubs & Societies– Balance Sheet:

• Assets =

Accumulated Fund

+ Liabilities

Difference …Recall that …

Clubs & Societies

1. Distinguish between trading & non-trading concerns – profit motive?

2. Different accounts used: Receipts & Payments A/c

Bar Trading A/c

Income & Expenditure A/c

Accumulated Fund

Clubs & Societies

What have we learnt today?

End of Lesson 1: 2 periods (70 min)

Clubs & Societies

Do you know ?

What are the differences between

the Receipts & Payments A/c

and

the Income & Expenditure A/c ?

Differences…

Receipts & Payments A/c

1. Summary of total

receipts and payments

of cash and cheques.

Equivalent to a

summarised form of a

Cash Book of a trading

concern.

Income & Expenditure A/c

1. Summary of the

operating expenses

and revenue items.

Equivalent to a Profit and

Loss Account of a trading

concern.

Receipts & Payments A/c

2. Contains both capital

and revenue

expenditure as well

as capital and

revenue receipts.

Income & Expenditure A/c

2. Contains only revenue

expenditure and

revenue receipt items

only.

Differences…Differences…

Receipts & Payments A/c

3. Includes those revenue

and capital items that

are actually paid for

and received.

Items which may refer to

preceding or succeeding

periods are also

included.

Income & Expenditure A/c

3. Includes only revenue

items incurred or earned

during the current

accounting period.

Excludes prepaid

expenses, unearned revenue.

Includes accrued

expenses, accrued revenue.

Differences…

Receipts & Payments A/c

4. Final balance is the

balance of cash in

hand, or cash at bank.

Is a current asset in the

Balance Sheet.

Overdraft is a current

liability.

Income & Expenditure A/c

4. Final balance shows

either a surplus or a

deficit for the period.

Surplus is added to the

accumulated fund in the

Balance Sheet.

Deficit is deducted

from accumulated fund.

Differences…

Presentation …

Receipts and Payments Account

Debit all receipts(both capital& revenuereceipts)

Credit all payments(both capital &

revenueexpenditure)

Income and Expenditure Account

Debit all currentyear revenueexpenditure

Credit all currentyear revenue

receipts

Prepare

the Receipts and Payments Account

for Weekend Football Club.

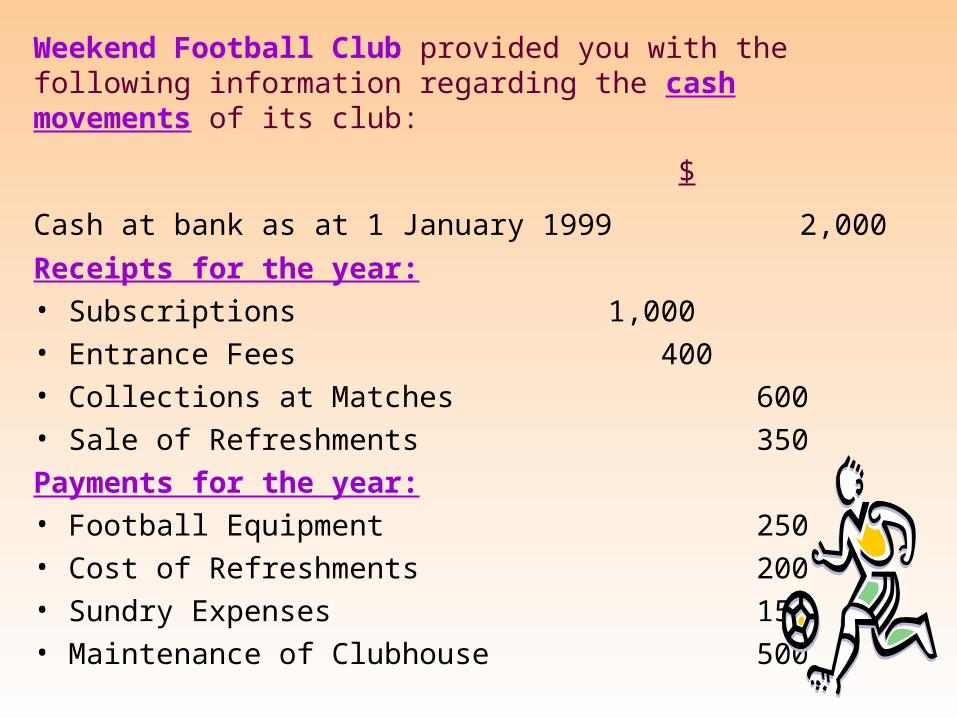

Weekend Football Club provided you with the following information regarding the cash movements of its club:

$

Cash at bank as at 1 January 1999 2,000

Receipts for the year: • Subscriptions 1,000• Entrance Fees 400• Collections at Matches 600• Sale of Refreshments 350

Payments for the year:• Football Equipment 250• Cost of Refreshments 200• Sundry Expenses 150• Maintenance of Clubhouse 500

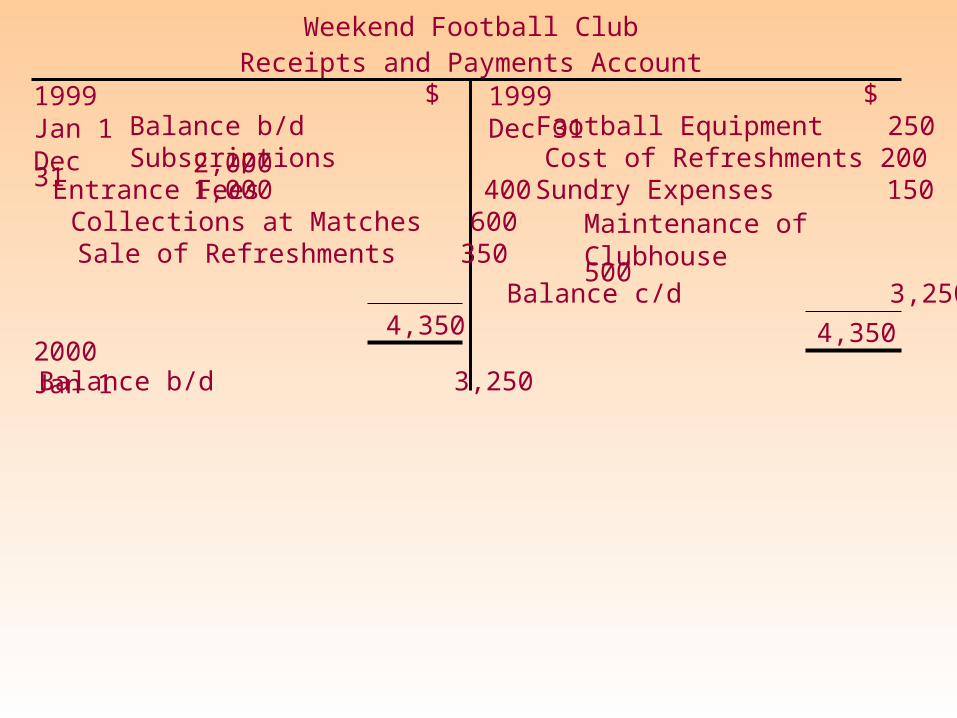

Weekend Football ClubReceipts and Payments Account

1999Jan 1Dec 31

Balance b/d 2,000

$ $

Subscriptions 1,000Entrance Fees 400

Sale of Refreshments 350Collections at Matches 600

Football Equipment 250Cost of Refreshments 200

1999Dec 31

Sundry Expenses 150Maintenance of Clubhouse 500 Balance c/d 3,250

4,350 4,3502000Jan 1 Balance b/d 3,250

Weekend Football ClubReceipts and Payments Account

1999Jan 1Dec 31

Balance b/d 2,000

$ $

Subscriptions 1,000Entrance Fees 400

Sale of Refreshments 350Collections at Matches 600

Football Equipment 250Cost of Refreshments 200

1999Dec 31

Sundry Expenses 150Maintenance of Clubhouse 500 Balance c/d 3,250

4,350 4,3502000Jan 1 Balance b/d 3,250

Can you prepare the Income and Expenditure Account

for the year ended 31 December 1999?

Weekend Football ClubReceipts and Payments Account

1999Jan 1Dec 31

Balance b/d 2,000

$ $

Subscriptions 1,000Entrance Fees 400

Sale of Refreshments 350Collections at Matches 600

Football Equipment 250Cost of Refreshments 200

1999Dec 31

Sundry Expenses 150Maintenance of Clubhouse 500 Balance c/d 3,250

4,350 4,3502000Jan 1 Balance b/d 3,250

Weekend Football ClubIncome and Expenditure Account for the year ended 31

December 1999Expenditure $ Income $

Weekend Football ClubReceipts and Payments Account

1999Jan 1Dec 31

Balance b/d 2,000

$ $

Subscriptions 1,000Entrance Fees 400

Sale of Refreshments 350Collections at Matches 600

Football Equipment 250Cost of Refreshments 200

1999Dec 31

Sundry Expenses 150Maintenance of Clubhouse 500 Balance c/d 3,250

4,350 4,3502000Jan 1 Balance b/d 3,250

Weekend Football ClubIncome and Expenditure Account for the year ended 31

December 1999Expenditure $ Income $

Cost of Refreshments 200Sundry Expenses 150Maintenance of Clubhouse 500

Subscriptions 1,000Entrance Fees 400Collections at Matches 600Sale of Refreshments 350Surplus 1,500

2,350 2,350

End of lesson 2:

1 period (35 min)

Trading Account

• Clubs and societies are not formed with a view to make profit.

• Clubs may operate a restaurant or bar selling refreshment and food to members.

• A Trading Account is prepared to determine the profit or loss.

• Records of stock of refreshment, refreshment debtors and creditors will be needed.

• Adjustments to find out the exact amount of sales, purchases and other expenses will be required to prepare the Trading Account.

Preparing the

Refreshment Trading Account

for Weekend Golf Club…

Weekend Golf Club provided the following information:

Receipts and Payments Account for the year ended 31 June 2000

$ $

Sale of refreshment 8,000

Additional Information:

Refreshment debtors 4,000

Refreshment creditors 900 3,000

Cost of refreshment 5,000

Wages for the preparationof refreshments 3,000

Refreshment creditors 1,000

31 June 20001 July 1999

Refreshment stock 2,000 3,500$

Refreshment debtors 500 6,500

$

Accrued wages for the preparation of refreshments 700 1,000

Step 1: Calculate Credit Sales of Refreshments

Weekend Golf Club provided the following information:

Receipts and Payments Account for the year ended 31 June 2000

$ $

Sale of refreshment 8,000

Additional Information:

Refreshment debtors 4,000

Refreshment creditors 900 3,000

Cost of refreshment 5,000

Wages for the preparationof refreshments 3,000

Refreshment creditors 1,000

31 June 20001 July 1999

Refreshment stock 2,000 3,500$

Refreshment debtors 500 6,500

$

Accrued wages for the preparation of refreshments 700 1,000

Step 1: Calculate Credit Sales of Refreshments

Refreshment Debtors’ Account$ $1999

Jul 12000 Jun 30Balance b/d 500 Cash or Bank 4,000

Balance c/d 6,500

10,50010,500

Balance c/d 6,5002000 Jul 1

Sales 10,000

Credit sales $10,000 is the balancing figure.

Step 2: Calculate Total Sales of Refreshments

Step 2: Calculate Total Sales of Refreshments

$

Credit Sales of Refreshments10,000Cash Sales of Refreshments 8,000

Total Sales of Refreshments 18,000

$18,000 is transferred to the Trading Account

Step 3: Calculate Credit Purchases of Refreshments

Weekend Golf Club provided the following information:

Receipts and Payments Account for the year ended 31 June 2000

$ $

Sale of refreshment 8,000

Additional Information:

Refreshment debtors 4,000

Refreshment creditors 900 3,000

Cost of refreshment 5,000

Wages for the preparationof refreshments 3,000

Refreshment creditors 1,000

31 June 20001 July 1999

Refreshment stock 2,000 3,500$

Refreshment debtors 500 6,500

$

Accrued wages for the preparation of refreshments 700 1,000

Step 3: Calculate Credit Purchases of Refreshments

Refreshment Creditors’ Account$ $1999

Jul 12000 Jun 30 Balance b/d 900Cash or Bank 1,000

Balance c/d 3,000

4,000 4,000

Balance c/d 3,0002000 Jul 1

Purchases 3,100

Credit purchases $3,100 is the balancing figure.

Step 4: Calculate Total Purchases of Refreshments

$

Credit Purchases of Refreshments 3,100Cash Purchases of Refreshments 5,000

Total Purchases of Refreshments 8,100

$8,100 is transferred to the Trading Account

Step 5: Calculate wages for the preparation of refreshment

Weekend Golf Club provided the following information:

Receipts and Payments Account for the year ended 31 June 2000

$ $

Sale of refreshment 8,000

Additional Information:

Refreshment debtors 4,000

Refreshment creditors 900 3,000

Cost of refreshment 5,000

Wages for the preparationof refreshments 3,000

Refreshment creditors 1,000

31 June 20001 July 1999

Refreshment stock 2,000 3,500$

Refreshment debtors 500 6,500

$

Accrued wages for the preparation of refreshments 700 1,000

Step 5: Calculate wages for the preparation of refreshment

Wages Account

$ $1999Jul 1

2000 Jun 30 Balance b/d 700Cash or Bank 3,000

Balance c/d 1,000

4,000 4,000

Balance c/d 1,0002000 Jul 1

Trading A/c 3,100

Wages $3,100 incurred for the year is the balancing figure.

Step 6: Prepare the Refreshment Trading Account

Weekend Golf Club

$ $Opening Stock 2,000

Refreshment Trading Account for the year ended 30 June 2000

Less Closing Stock (3,500)

Cost of Sales 6,600

Add Purchases 8,10010,100

Gross Profit 11,400

Sales 18,000

18,000Gross Profit 11,400

18,000Wages for preparation of refreshment 3,100Net Profit 8,300

11,40011,400

Step 7: Transferring refreshment net profitto the Income and Expenditure Account

Weekend Golf Club

Income and Expenditure Account for the year ended 30 June 2000

Debit all currentyear revenueexpenditure

Credit all currentyear revenue

receipts

Step 7: Transferring refreshment net profitto the Income and Expenditure Account

Weekend Golf Club

Income and Expenditure Account for the year ended 30 June 2000

Net Profit from Refreshments 8,300

$$

End of lesson 3: 2 periods (70 min)

• Most records of clubs are kept using the single- entry system.

• Balance day adjustments are needed to get the necessary data to prepare the accounts.

Balance Day Adjustments

Adjustments are usually made to the following:

• Subscription Account – to find exact subscription for the year.

• Trading Account – to find sales, purchases, expenses incurred for the year.

• Other revenue generating activities – to find net gain or loss from the event.

• Disposal of new assets and acquisition of new assets – to record a gain or loss on disposal.

Balance Day Adjustments

Adjustments are usually made to the following:

• Subscription Account – to find exact subscription for the year.

• Trading Account – to find sales, purchases, expenses incurred for the year.

• Other revenue generating activities – to find net gain or loss from the event.

• Disposal of new assets and acquisition of new assets – to record a gain or loss on disposal.

Balance Day Adjustments

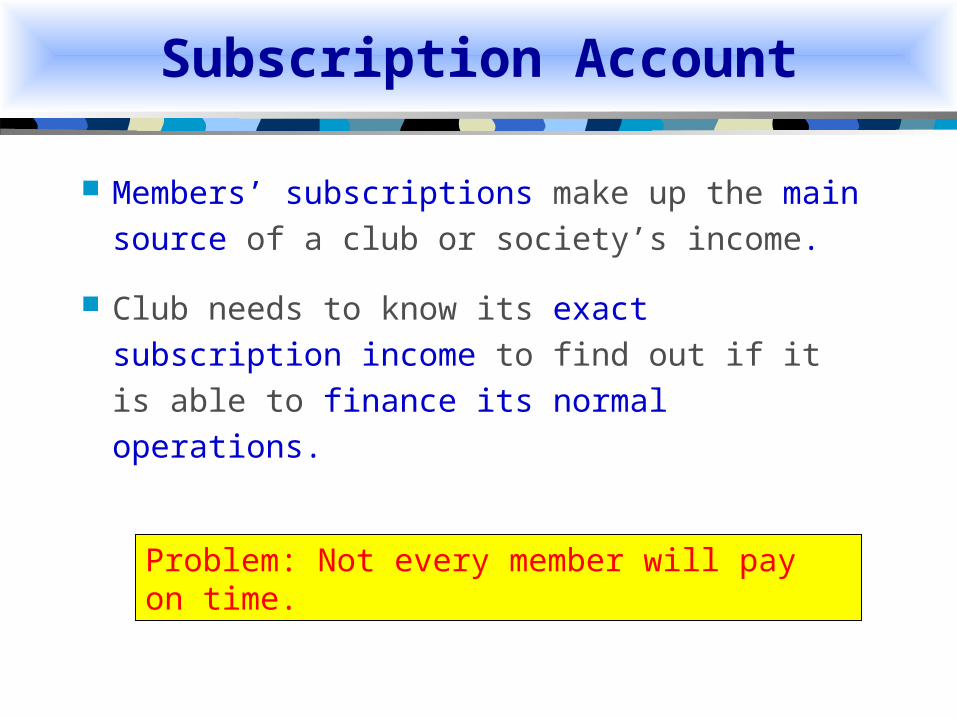

Subscription Account

Members’ subscriptions make up the main source of a club or society’s income.

Club needs to know its exact subscription income to find out if it is able to finance its normal operations.

Problem: Not every member will pay on time.

Subscription Account

Subscription is a revenue receipt and

recorded in the Subscription Account.

Subscription owed by members is known as

subscription due or subscription in arrears.

Subscription paid by members in the current

financial year for the next financial year is

known as subscription in advance.

Subscription Account

When an arrears or advance payment happens,

adjustments in the preparation of the Subscription Account have to be made

so that only the amount of revenue earned during the current year

is included in the current year’s Income and Expenditure Account

according to the matching principle.

Subscriptions Account CrDr

Subscription in arrears b/d(not collected during the

previous year)

$ $

Income & ExpenditureAccount (exact amount of

Subscription revenuefor the current year)

Subscription received inadvance b/d (collected in

the previous year)

Total cash received assubscription during the

current year

Subscription in arrears c/d(not yet received for the

current year)

Subscription in advance c/d(collected for subsequent year)

Weekdays Country Club has the following in the books:

Receipts and Payments Account for the year ended 31 Jun 2000$ $

Subscription 5,500

Additional information:1 Jul 1999 31 Jun 2000

Subscription in advance 600 900

Subscription in arrears 1,500 850$$

Question:

What would the Subscription Account look like?

Subscriptions Account

$ $Balance b/d 1,500

1999Jul 1

1999Jul 1 Balance b/d 600

2000Jun 30

2000Jun 30 Bank

5,500Income andExpenditure A/c Balance c/d 850Balance c/d 900 6,9506,950

4,550

In this example, the subscription for the

current year is thebalancing figure.

2000Jul 1 Balance b/d 850

2000Jul 1 Balance b/d 900

Subscriptions Account

$ $Balance b/d 1,500

1999Jul 1

1999Jul 1 Balance b/d 600

2000Jun 30

2000Jun 30 Bank

5,500Income andExpenditure A/c Balance c/d 850Balance c/d 900 6,9506,950

4,550

Income and Expenditure Account for the year ended 30 June 2000

$ $

2000Jul 1 Balance b/d 850

2000Jul 1 Balance b/d 900

Subscriptions Account

$ $Balance b/d 1,500

1999Jul 1

1999Jul 1 Balance b/d 600

2000Jun 30

2000Jun 30 Bank

5,500Income andExpenditure A/c Balance c/d 850Balance c/d 900 6,9506,950

4,550

Income and Expenditure Account for the year ended 30 June 2000

$ $

Subscription 4,550

2000Jul 1

2000Jul 1Balance b/d 850 Balance b/d 900

Subscriptions Account

$ $Balance b/d 1,500

1999Jul 1

1999Jul 1 Balance b/d 600

2000Jun 30

2000Jun 30 Bank

5,500Income andExpenditure A/c Balance c/d 850Balance c/d 900 6,9506,950

4,550

Balance Sheet as at 30 June 2000$ $

Current Assets Current Liabilities

2000Jul 1

2000Jul 1Balance b/d 850 Balance b/d 900

Subscriptions Account

$ $Balance b/d 1,500

1999Jul 1

1999Jul 1 Balance b/d 600

2000Jun 30

2000Jun 30 Bank

5,500Income andExpenditure A/c Balance c/d 850Balance c/d 900 6,9506,950

4,550

Balance Sheet as at 30 June 2000$ $

Current Assets Current Liabilities

Subscription in advance 900Subscription in arrears 850

Adjustments are usually made to the following:

• Subscription Account – to find exact subscription for the year.

• Trading Account – to find sales, purchases, expenses incurred for the year.

• Other revenue generating activities – to find net gain or loss from the event.

• Disposal of new assets and acquisition of new assets – to record a gain or loss on disposal.

Balance Day Adjustments

Adjustments are usually made to the following:

• Subscription Account – to find exact subscription for the year.

• Trading Account – to find sales, purchases, expenses incurred for the year.

• Other revenue generating activities – to find net gain or loss from the event.

• Disposal of new assets and acquisition of new assets – to record a gain or loss on disposal.

Balance Day Adjustments

Other Revenue Generating Activities

Examples are charging for the use of club facilities or holding dances and socials.

Expenses incurred from these activities must be deducted from the related revenue obtained to show a GAIN or LOSS.

The net proceeds from such activities are part of the current operating revenue and recorded in the Income and Expenditure Account.

Example:

Everyday Dance Club held a dance competition

for its members. Registration fees collected was

$330. Prizes and refreshments for the

competitors amounted to $200. What is the gain

or loss from this event?

Income and Expenditure Account for the year ended 31 Jun 2000 $$

Everyday Dance Club

Gain from dance competition ($330-$200) 130

Adjustments are usually made to the following:

• Subscription Account – to find exact subscription for the year.

• Trading Account – to find sales, purchases, expenses incurred for the year.

• Other revenue generating activities – to find net gain or loss from the event.

• Disposal of new assets and acquisition of new assets – to record a gain or loss on disposal.

Balance Day Adjustments

Disposal of Old Asset and Acquisition of New Asset

Whenever a non-trading organisation disposes an asset, it can make a “gain” or “loss” due to previous under-provision or over-provision of depreciation.

“Gain” or “loss” is usually treated as a revenue item.

“Gain” or “loss” is normally not capitalised.

“Gain” or “loss” is recorded in the Income and Expenditure Account.

Weekdays Football Club has the following in the books:

Receipts and Payments Account for the year ended 31 Jun 2000$ $

Sale of surplusfootball equipment(book value $200) 150

Additional information:1 Jul 1999 31 Jun 2000

Football equipment at valuation 500 550

$$

Questions: - Is there a GAIN or LOSS on disposal?

-What is the DEPRECIATION for the year?

New footballequipment 300

Weekdays Football Club has the following in the books:

Receipts and Payments Account for the year ended 31 Jun 2000$ $

Sale of surplusfootball equipment(book value $200) 150

Additional information:1 Jul 1999 31 Jun 2000

Football equipment at valuation 500 550

$$

Questions: - Is there a GAIN or LOSS on disposal?

New footballequipment 300

Sale of surplus football equipment $150

Book value of equipment sold $200

Loss on sale of football equipment $50Income and Expenditure Account for the year ended 31

Jun 2000$ $

Is there a GAIN or LOSS on

disposal?

Weekdays Football Club

Loss on sale of footballEquipment ($150-$200)50

Weekdays Football Club has the following in the books:

Receipts and Payments Account for the year ended 31 Jun 2000$ $

Sale of surplusfootball equipment(book value $200) 150

Additional information:1 Jul 1999 31 Jun 2000

Football equipment at valuation 500 550

$$

Questions: -What is the DEPRECIATION for the

year?

New footballequipment 300

2 methods to arrive at the answer ….

What is the DEPRECIATION for the

year?

Method 1:

Balance as at 1 Jul 1999500Add Purchases 300

800Less Sale of equipment (200)

600

Depreciation = $600 - $550 = $50

2 methods to arrive at the answer ….

What is the DEPRECIATION for the

year?

Method 2:

Football Equipment Account

$ $

Balance b/d 500

Purchases 300 Disposal 200

Balance c/d 550

800 800

Depreciation 50

Remember to show your working for calculating

depreciation whatever method you use ….

Income and Expenditure Account for the year ended 31 Jun 2000$ $

What is the DEPRECIATION for the

year?

Weekdays Football Club

Loss on sale of footballequipment 50

Depreciation of footballequipment 50

End of lesson 4: 2 periods (70 min)

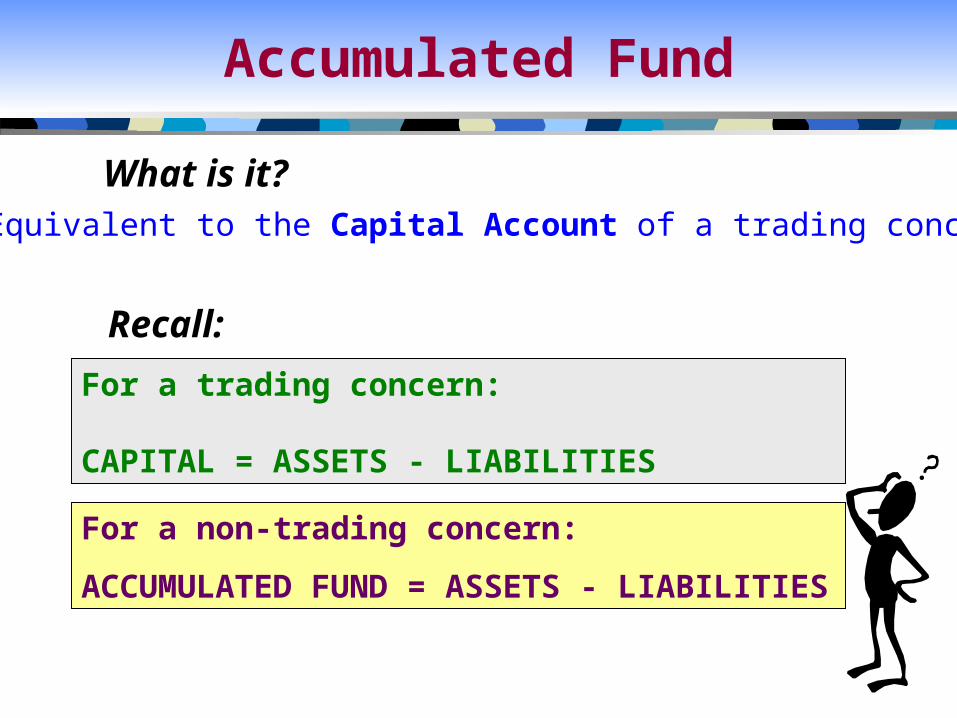

What is it?

Accumulated Fund

Equivalent to the Capital Account of a trading concern.

Recall:

For a trading concern:

CAPITAL = ASSETS - LIABILITIES

For a non-trading concern:

ACCUMULATED FUND = ASSETS - LIABILITIES

Accumulated Fund

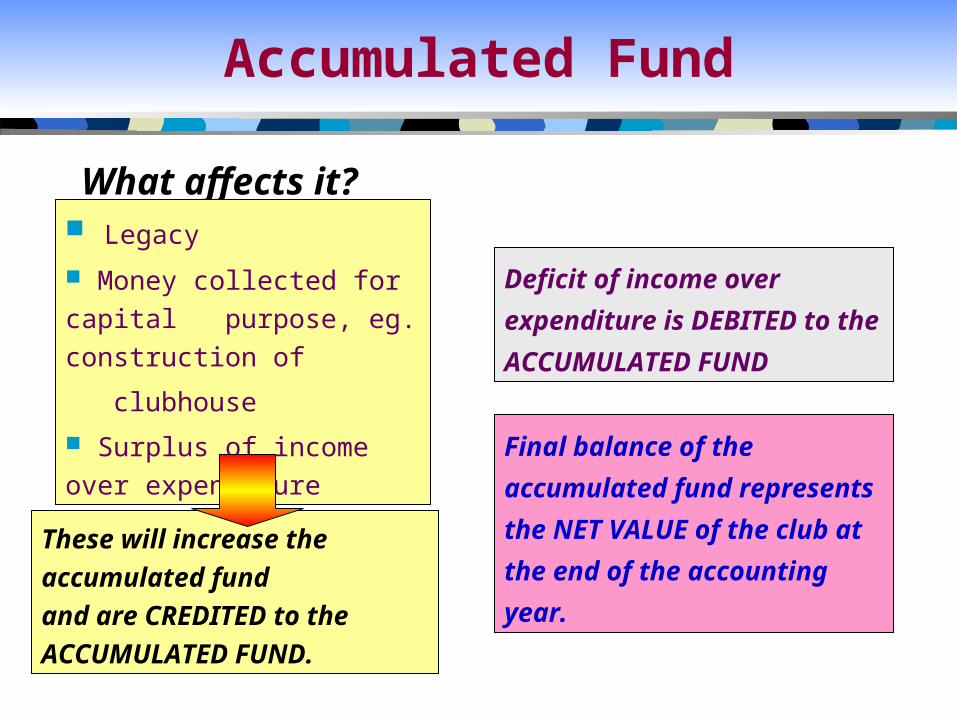

What affects it? Legacy

Money collected for capital purpose, eg. construction of

clubhouse

Surplus of income over expenditure

These will increase the accumulated fundand are CREDITED to the ACCUMULATED FUND.

Deficit of income over

expenditure is DEBITED

to the ACCUMULATED

FUND

Final balance of the

accumulated fund

represents the NET

VALUE of the club at the

end of the accounting

year.

Weekend Rollarblading Club has the following in its books:

Receipts and Payments Account$ $2000

Jan 12000Dec 31Balance b/d 2,000

Dec 31 Locker fees 500 Subscription:• 1999 100• 2000 300• 2001 150

Rent 1,500Extensionto clubhouse 1,900Sundry exp 120

On 1 Jan 2000, the club had the following assets:Rollarblading equipment $600

Clubhouse $12,000

Additional information:

• Rent paid included $500 for accrued rent from the previous year.• As at 31 Dec 2000, accrued locker fees was $210.

What information would I

need

to calculate the

Accumulated Fund as at 1

Jan 2000?

Weekend Rollarblading Club has the following in its books:

Receipts and Payments Account$ $2000

Jan 12000Dec 31Balance b/d 2,000

Dec 31 Locker fees 500 Subscription:• 1999 100• 2000 300• 2001 150

Rent 1,500Extensionto clubhouse 1,900Sundry exp 120

On 1 Jan 2000, the club had the following assets:Rollarblading equipment $600

Clubhouse $12,000

Additional information:

• Rent paid included $500 for accrued rent from the previous year.• As at 31 Dec 2000, accrued locker fees was $210.

Calculation of Accumulated Fund as at 1 Jan 2000:

Assets $

Cash at Bank2,000Subscription in arrears

100Rollarblading equipment 600Clubhouse 12,000

14,700Less: LiabilitiesAccrued rent (500)

Accumulated fund as at1 Jan 2000 14,200

Receipts and Payments A/c as at 1 Jan 2000

Presentation …

Balance Sheet as at 31 December 2000

Weekend Rollarblading Club

$Accumulated Fund

Balance as at 1/1/2000 14,200

Add Surplus XXX

Balance as at 31/12/2000 XXX

End of lesson 5: 1 period (35 min)

Recommended