CHAPTER 12CHAPTER 12

Cash Flows and Other Topics Cash Flows and Other Topics in Capital Budgetingin Capital Budgeting

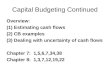

Time line for Solution Practice Problem 2Time line for Solution Practice Problem 2

Cash FlowsCash Flows

0 1$197,500

2$197,500

3$197,500

4$197,500

5$197,500

8$158,400+$41,400 =$199,800

6$158,400

7$158,400

TerminalCash flow

Annual Cash Flows

Initialoutlay$590,000

Automation ProjectAutomation Project:: Cost of equipment = Cost of equipment = $550,000$550,000.. Shipping & installation will be Shipping & installation will be $25,000$25,000.. $15,000$15,000 in net working capital required at setup. in net working capital required at setup. 8-year project life, 5-year class life.8-year project life, 5-year class life. Simplified straight line depreciation.Simplified straight line depreciation. Current operating expenses are Current operating expenses are $640,000$640,000 per yr. per yr. New operating expenses will be New operating expenses will be $400,000$400,000 per yr. per yr. Already paid consultant Already paid consultant $25,000$25,000 for analysis. for analysis. Salvage value after year 8 is Salvage value after year 8 is $40,000$40,000.. Cost of capital = Cost of capital = 14%,14%, marginal tax rate = marginal tax rate = 34%34%..

Problem 2Problem 2

Problem 2 Problem 2

Initial OutlayInitial Outlay::

(550,000)(550,000) Cost of new machineCost of new machine

+ (+ (25,00025,000)) Shipping & Shipping & installationinstallation

(575,000)(575,000) Depreciable assetDepreciable asset

+ (+ (15,000)15,000) NWC investmentNWC investment

(590,000)(590,000) Net Initial OutlayNet Initial Outlay

240,000 240,000 Cost decreaseCost decrease

((115,000115,000) ) Depreciation increaseDepreciation increase

125,000125,000 EBITEBIT

((42,50042,500)) Taxes (34%)Taxes (34%)

82,50082,500 EATEAT

115,000115,000 Depreciation reversalDepreciation reversal

197,500 = Annual Cash Flow 197,500 = Annual Cash Flow

For Years 1 - 5:For Years 1 - 5: Problem 2

CALCULATION OF ANNUAL CALCULATION OF ANNUAL DEPRECIATION FOR NEW MACHINE:DEPRECIATION FOR NEW MACHINE:

Depreciable asset/class life =$575,000/5 yrsDepreciable asset/class life =$575,000/5 yrs

= $115,000= $115,000

The machine is used only for 5 years. From The machine is used only for 5 years. From years 6-10, no depreciation; therefore years 6-10, no depreciation; therefore depreciation will be $0 for these last 5 years. depreciation will be $0 for these last 5 years.

240,000 240,000 Cost decreaseCost decrease

( 0)( 0) Depreciation increaseDepreciation increase

240,000240,000 EBITEBIT

(81,600)(81,600) Taxes (34%)Taxes (34%)

158,400158,400 EATEAT

00 Depreciation reversalDepreciation reversal

158,400 = Annual Cash Flow 158,400 = Annual Cash Flow

For Years 6 - 8:For Years 6 - 8:Problem 2

Terminal Cash FlowTerminal Cash Flow::

40,000 Salvage value40,000 Salvage value

(13,600) Tax on capital gain(13,600) Tax on capital gain

15,000 15,000 Recapture of NWC Recapture of NWC

41,400 Terminal Cash Flow41,400 Terminal Cash Flow

Problem 2

CALCULATION OF TERMINAL CASH FLOWCALCULATION OF TERMINAL CASH FLOW

Annual depreciation of new machine=$115,000 Annual depreciation of new machine=$115,000

(from slide 7)(from slide 7)

Book valueBook value = Depreciable asset – Total = Depreciable asset – Total amount depreciated amount depreciated

= $575,000 - $115,000(5yrs)= $575,000 - $115,000(5yrs)

= $0= $0

Capital gain Capital gain = Salvage value-Book Value= Salvage value-Book Value

= $40,000-$0 = $40,000= $40,000-$0 = $40,000

Tax on capital gain Tax on capital gain = 34% x $40,000= 34% x $40,000

= $13,600 (refer slide 8)= $13,600 (refer slide 8)

Problem 2 SolutionProblem 2 Solution

NPV and IRR:NPV and IRR: CF(year 0) CF(year 0) = -$590,000 (slide 4)= -$590,000 (slide 4) CF(years 1 - 5) CF(years 1 - 5) =$197,500 (slide 5)=$197,500 (slide 5) CF(years 6 - 7) CF(years 6 - 7) = $158,400 (slide 7)= $158,400 (slide 7) CF(year 8) CF(year 8) = $158,400 + $41,400 = $158,400 + $41,400

= $199,800 (slides 7 + 8)= $199,800 (slides 7 + 8) Discount rate = 14%.Discount rate = 14%. IRR = 28.13% IRR = 28.13% NPV = $293,543NPV = $293,543.. We would We would acceptaccept the project. the project.

FINDING NPV-FINDING NPV-11stst method (annuity + individual CF) method (annuity + individual CF)

NPVNPV = -$590,000 = -$590,000 (year 0) (year 0)

+ $197,500 (PVIFA 14%, years 1-5)+ $197,500 (PVIFA 14%, years 1-5) (years 1-5)(years 1-5)

+ $158,400 (PVIF 14%, 6+ $158,400 (PVIF 14%, 6thth yr) yr) (year 6)(year 6)

+ $158,400 (PVIF 14%, 7+ $158,400 (PVIF 14%, 7thth yr) yr) (year 7) (year 7)

+ $199,800 (PVIF 14%, 8+ $199,800 (PVIF 14%, 8thth yr) yr) (year 8)(year 8)

= -$590,000 = -$590,000

+ $197,500(3.4331)+ $197,500(3.4331)

+ $158,400 ( (0.4556)+ $158,400 ( (0.4556)

+ $158,400 ( (0.3996)+ $158,400 ( (0.3996)

+ $199,800 (0.3506)+ $199,800 (0.3506)

= -$590,000 +$678,037 +$72,167 +$63,297 +$70,050= -$590,000 +$678,037 +$72,167 +$63,297 +$70,050

= -$590,000 +$883,551 = = -$590,000 +$883,551 = $293,551$293,551

Accept the project since NPV is positive.Accept the project since NPV is positive.

FINDING NPV-FINDING NPV-22ndnd method (annuities) method (annuities)

NPVNPV = -$590,000 = -$590,000 (year 0) (year 0)

+ $197,500 (PVIFA + $197,500 (PVIFA 14%, 5years14%, 5years)) (years 1-5)(years 1-5)

+ $158,400 (PVIFA + $158,400 (PVIFA 14%, 2 years,6&7) 14%, 2 years,6&7)

(PVIF 14%, 5)(PVIF 14%, 5) (annuities years 6-7)(bring back to (annuities years 6-7)(bring back to time 0). time 0). Refer Refer to TVM ppt, slides 68-71 for to TVM ppt, slides 68-71 for understanding.understanding.

+ $199,800 (PVIF + $199,800 (PVIF 14%,1014%,10thth year year) ) (year 8)(year 8)

= -$590,000 = -$590,000

+ $197,500(3.4331)+ $197,500(3.4331)

+ $158,400 (1.6467)(0.5194)+ $158,400 (1.6467)(0.5194)

+ $199,800 (0.3506)+ $199,800 (0.3506)

= -$590,000 +$678,037 +$135,479 +$70,050= -$590,000 +$678,037 +$135,479 +$70,050

= -$590,000 +$883,556 = -$590,000 +$883,556 = $293,566 = $293,566

Accept the project since NPV is positive.Accept the project since NPV is positive.

Recommended