4/6/2015

1

Chapter 10: Futures Arbitrage Strategies

� I. Short-Term Interest Rate Arbitrage

� 1. Cash and Carry/Implied Repo

� Cash and carry transaction means to buy asset and sell futures

� Use repurchase agreement/repo to obtain funding

� A repurchase agreement is the sale of securities together with an agreement for the seller to buy back the securities at a later date.

� Repo Rate: financing rate (overnight vs. term repo)

� The repurchase price should be greater than the original sale price, the difference effectively representing interest, is called the repo rate.

� Implied Repo Rate

� The financing rate that produces no arbitrage profit

� Cost of carry pricing model: f= S + θ� π = f – S - θ = 0

= f – S(1+r)T = 0� r = (f / S)1/T– 1 � r is the equilibrium rate� Arbitrage will be profitable if

implied repo rate (r) > actual repo rate (R)That is, f is over-priced

2. Eurodollar Arbitrage� Eurodollar Futures as a synthetic loan: Buyer of Eurodollar futures agrees to “lend” (e.g., buy $1,000,000 Eurodollar TD), while seller agrees to “borrow”

4/6/2015

2

� Using Eurodollar futures with spot to earn an arbitrage profit.

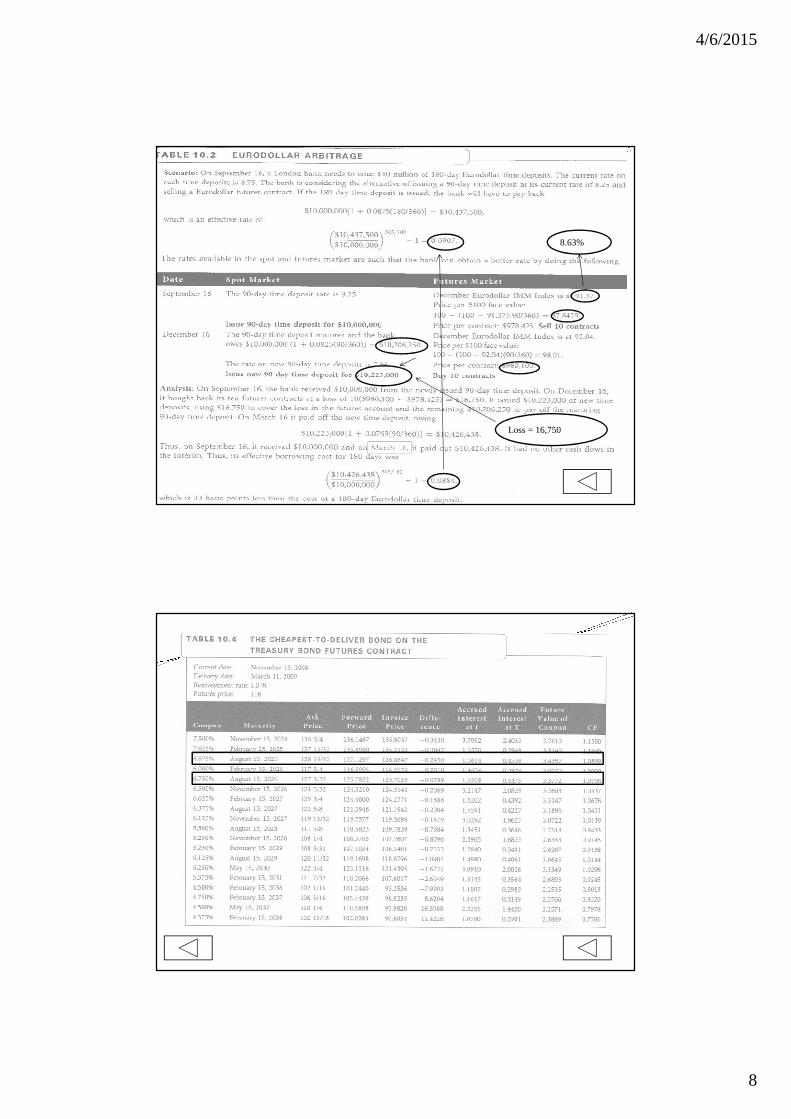

� Sept. 16� 90-day Eurodollar discount@ 8.25% � 180-day Eurodollar discount@ 8.75% � December Eurodollar Futures: IMM=91.37 � yield 8.63%� Repo rate (R) = 8.25%

� Is Arbitrage profitable?� S: 180-day Eurodollar price S=100-(8.75)(180/360) = 95.625� f: f = 100 – (8.63)(90/360) = 97.8425 (price/contract=978,425)� r = (f/S)1/T -1 = (97.8425/95.625)1/(90/365) – 1 = 9.7445%� Since r > R, arbitrage is profitable

� Arbitrage examples� Long Eurodollar, short Eurodollar futures� Table 10.2, p. 332

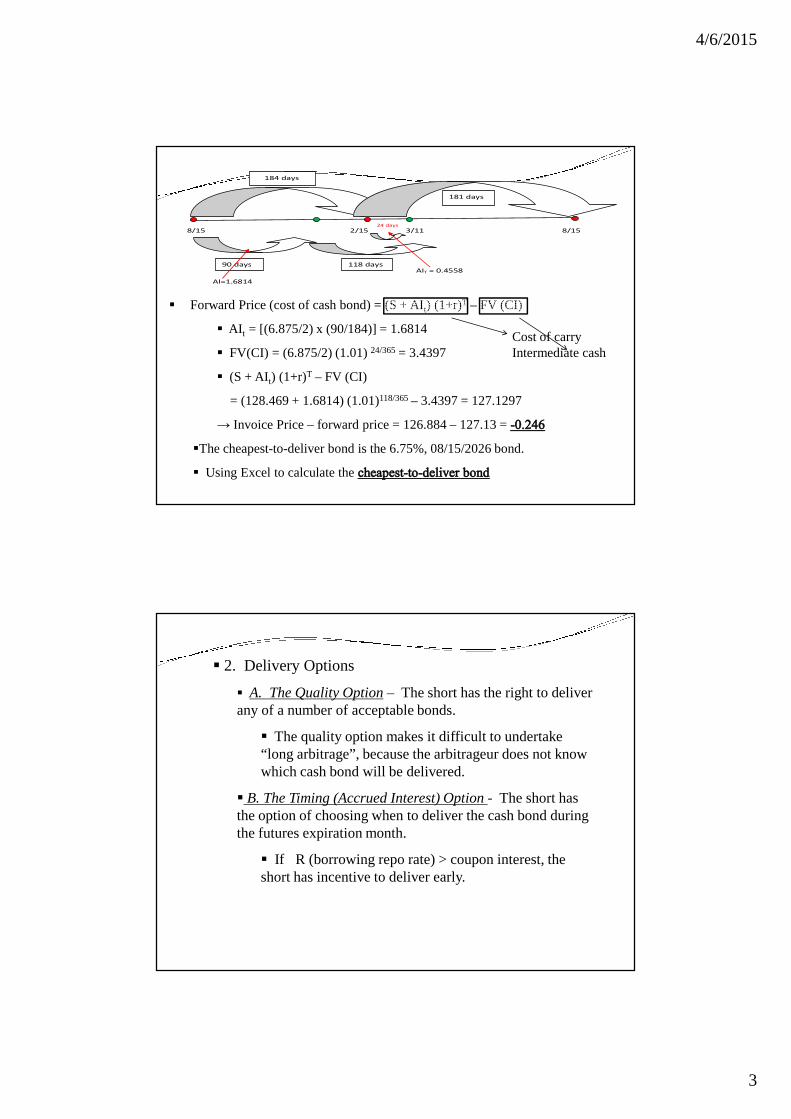

II. T-Bond Arbitrage – Short futures, long bond

1. Determine Cheapest-to-Deliver (CTD) Bond

� The bond that maximizes (invoice price – forward price )

� shows these calculations for all deliverable bonds. Example: 3rd bond (6.875%, 08/15, 2025). On 11/13, f=116, delivery date =3/11, reinvestment rate =1%

(Accrued Interest: AIt=1.6814) (AIT=0.4558)

� Invoice Price = f • (CF) + AIT

= 116 x ( ) + [(6.875/2) x (24/181)] = 126.4284+0.4558 =

4/6/2015

3

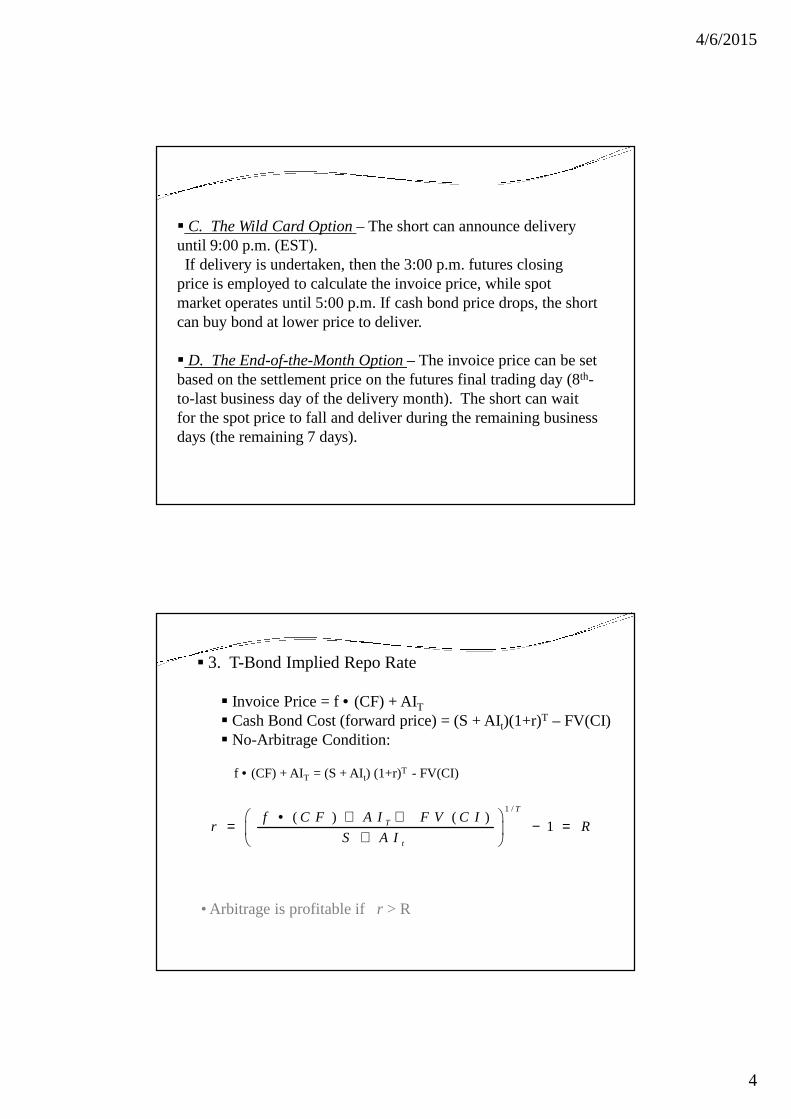

� Forward Price (cost of cash bond) = (S + AIt) (1+r)T – FV (CI)

� AI t = [(6.875/2) x (90/184)] = 1.6814

� FV(CI) = (6.875/2) (1.01) 24/365= 3.4397

� (S + AIt) (1+r)T – FV (CI)

= (128.469 + 1.6814) (1.01)118/365– 3.4397 = 127.1297

→ Invoice Price – forward price = 126.884 – 127.13 =

�The cheapest-to-deliver bond is the 6.75%, 08/15/2026 bond.

� Using Excel to calculate the

Cost of carryIntermediate cash

184 days

181 days

8/15 2/15 3/11 8/15

90 days 118 days

24 days

AI=1.6814

AIT = 0.4558

� 2. Delivery Options

� A. The Quality Option – The short has the right to deliver any of a number of acceptable bonds.

� The quality option makes it difficult to undertake “long arbitrage”, because the arbitrageur does not know which cash bond will be delivered.

� B. The Timing (Accrued Interest) Option - The short has the option of choosing when to deliver the cash bond during the futures expiration month.

� If R (borrowing repo rate) > coupon interest, the short has incentive to deliver early.

4/6/2015

4

� C. The Wild Card Option – The short can announce delivery until 9:00 p.m. (EST).If delivery is undertaken, then the 3:00 p.m. futures closing

price is employed to calculate the invoice price, while spot market operates until 5:00 p.m. If cash bond price drops, the short can buy bond at lower price to deliver.

� D. The End-of-the-Month Option – The invoice price can be set based on the settlement price on the futures final trading day (8th-to-last business day of the delivery month). The short can wait for the spot price to fall and deliver during the remaining business days (the remaining 7 days).

� 3. T-Bond Implied Repo Rate

� Invoice Price = f • (CF) + AIT� Cash Bond Cost (forward price) = (S + AIt)(1+r)T – FV(CI)� No-Arbitrage Condition:

f • (CF) + AIT = (S + AIt) (1+r)T - FV(CI)

• Arbitrage is profitable if r > R

1 /( ) ( )

1T

T

t

f C F A I F V C Ir R

S A I

• + += − = +

4/6/2015

5

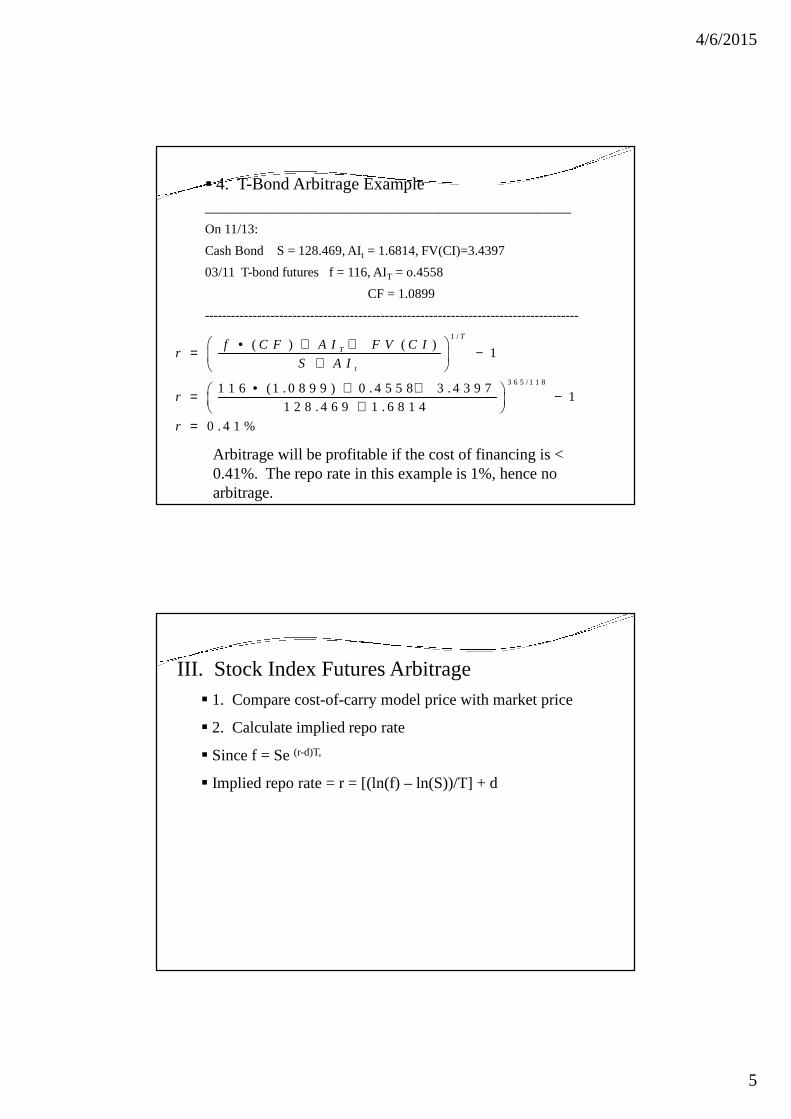

� 4. T-Bond Arbitrage Example_______________________________________________________

On 11/13:

Cash Bond S = 128.469, AIt = 1.6814, FV(CI)=3.4397

03/11 T-bond futures f = 116, AIT = o.4558

CF = 1.0899

-------------------------------------------------------------------------------------

1 /

3 6 5 /1 1 8

( ) ( )1

1 1 6 (1 . 0 8 9 9 ) 0 . 4 5 5 8 3 . 4 3 9 71

1 2 8 . 4 6 9 1 . 6 8 1 4

0 . 4 1 %

T

T

t

f C F A I F V C Ir

S A I

r

r

• + += − +

• + + = − +

=

Arbitrage will be profitable if the cost of financing is < 0.41%. The repo rate in this example is 1%, hence no arbitrage.

III. Stock Index Futures Arbitrage� 1. Compare cost-of-carry model price with market price

� 2. Calculate implied repo rate

� Since f = Se (r-d)T,

� Implied repo rate = r = [(ln(f) – ln(S))/T] + d

4/6/2015

6

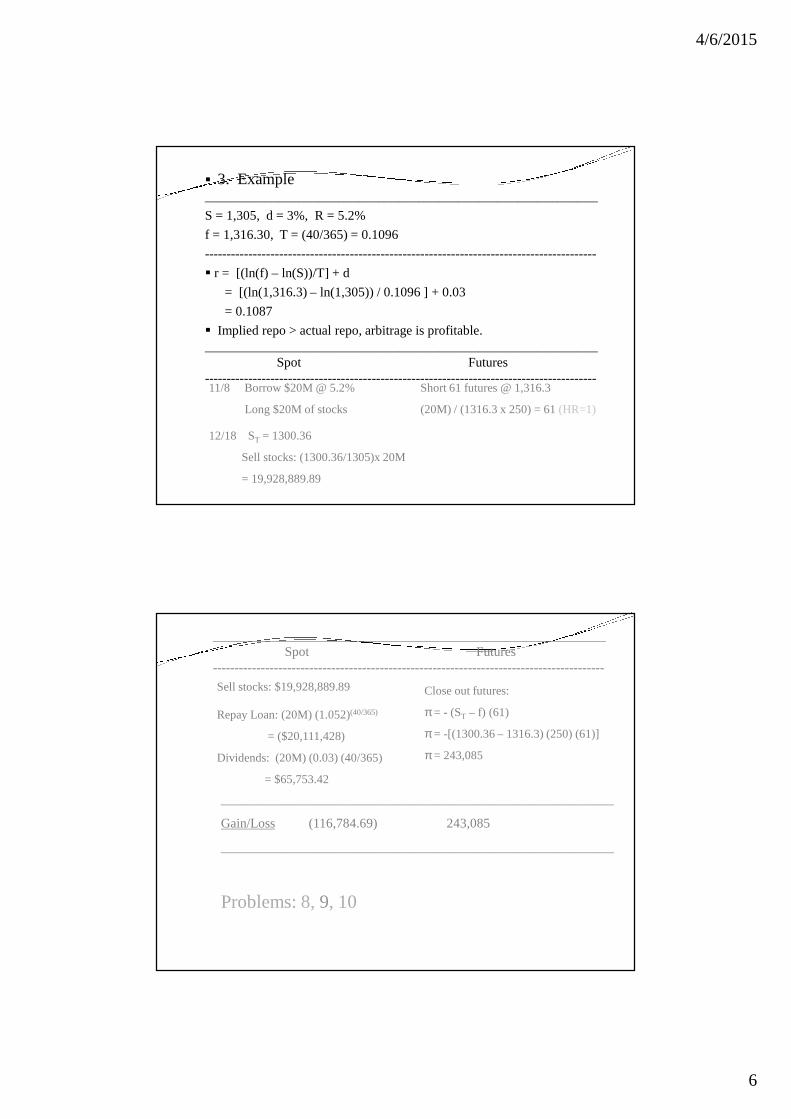

� 3. Example___________________________________________________________

S = 1,305, d = 3%, R = 5.2%

f = 1,316.30, T = (40/365) = 0.1096

-----------------------------------------------------------------------------------------

� r = [(ln(f) – ln(S))/T] + d

= [(ln(1,316.3) – ln(1,305)) / 0.1096 ] + 0.03

= 0.1087

� Implied repo > actual repo, arbitrage is profitable.___________________________________________________________

Spot Futures-----------------------------------------------------------------------------------------11/8 Borrow $20M @ 5.2%

Long $20M of stocks

Short 61 futures @ 1,316.3

(20M) / (1316.3 x 250) = 61 (HR=1)

12/18 ST = 1300.36

Sell stocks: (1300.36/1305)x 20M

= 19,928,889.89

___________________________________________________________Spot Futures

-----------------------------------------------------------------------------------------

Repay Loan: (20M) (1.052)(40/365)

= ($20,111,428)

Dividends: (20M) (0.03) (40/365)

= $65,753.42

Sell stocks: $19,928,889.89 Close out futures:

π = - (ST – f) (61)

π = -[(1300.36 – 1316.3) (250) (61)]

π = 243,085

___________________________________________________________

Gain/Loss (116,784.69) 243,085

___________________________________________________________

Problems: 8, 9, 10

4/6/2015

7

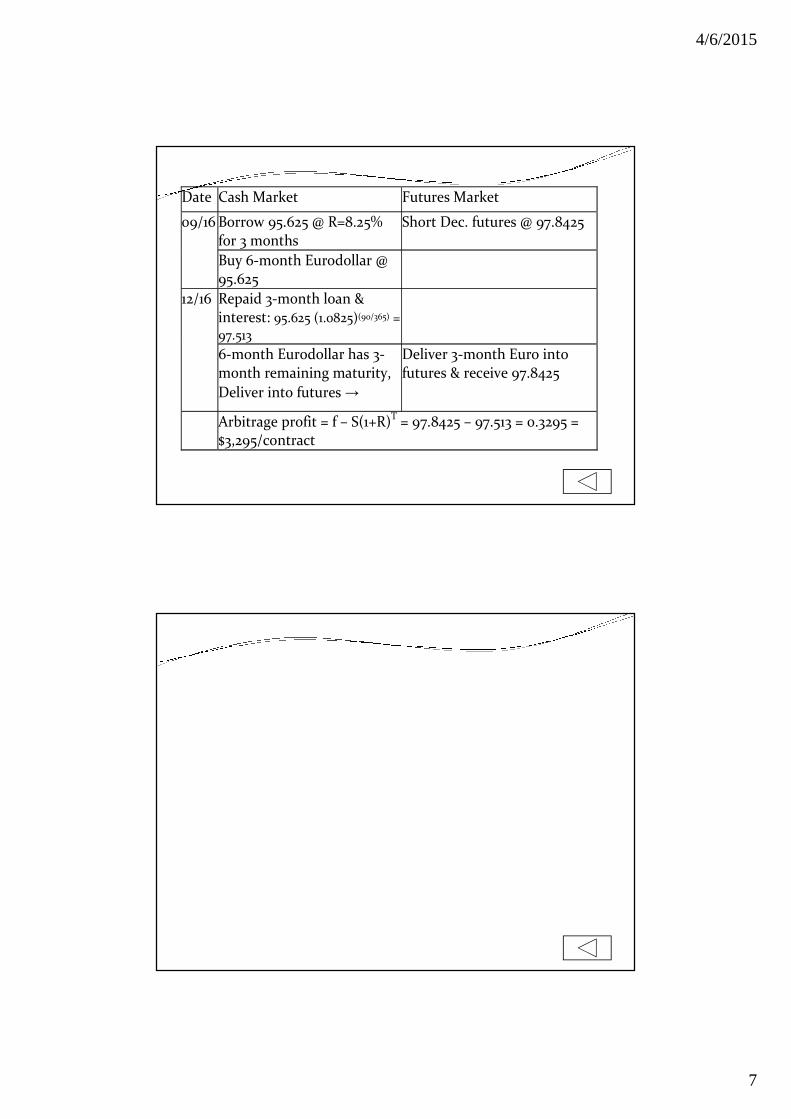

Date Cash Market Futures Market

Borrow 95.625 @ R=8.25% for 3 months

Short Dec. futures @ 97.8425 09/16

Buy 6-month Eurodollar @ 95.625

Repaid 3-month loan & interest: 95.625 (1.0825)(90/365) = 97.513

12/16

6-month Eurodollar has 3-month remaining maturity,

Deliver into futures →

Deliver 3-month Euro into futures & receive 97.8425

Arbitrage profit = f – S(1+R)T = 97.8425 – 97.513 = 0.3295 = $3,295/contract

4/6/2015

8

Loss = 16,750

8.63%

Recommended