1

Define merchandise inventory Whose Inventory

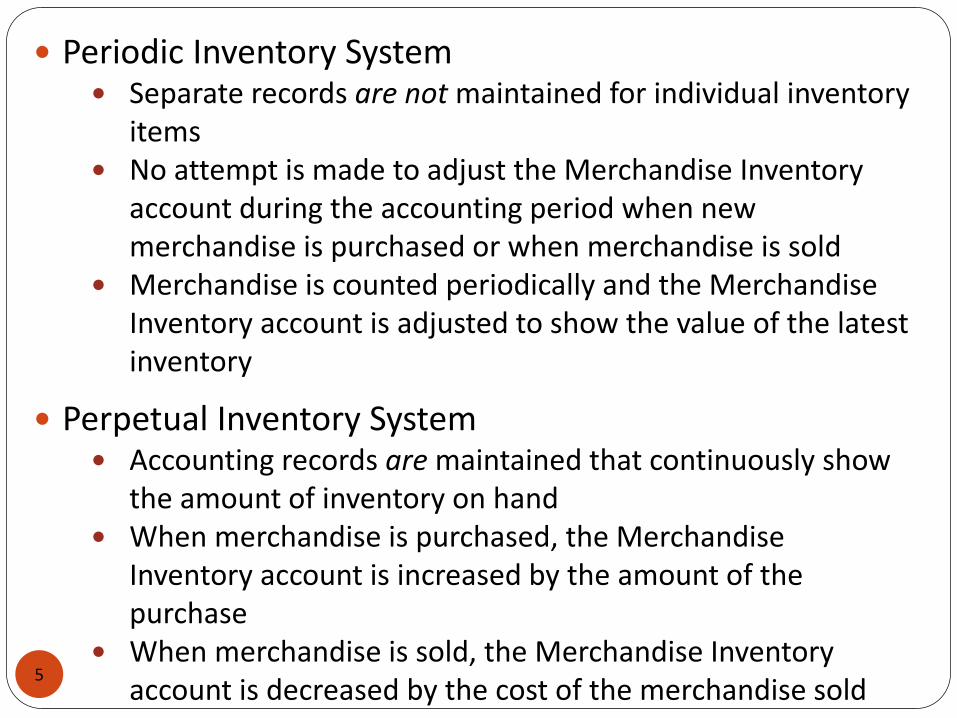

Periodic Inventory System

Perpetual Inventory System

Inventory valuation: Specific ID

FIFO

LIFO

Weighted Average

Gross Profit and Retail Methods

Valuation Effects of Inventory on Net Income

Ch. 15 Accounting for Merchandise Inventory

Merchandise Inventory

2

Consists of goods held for sale to customers in the normal course of business

In a supermarket, merchandise includes canned goods, meats, fruits, and fresh vegetables

Merchandise Inventory account

The only account that appears on both the balance sheet and the income statement

The ending inventory is reported on the balance sheet as a current asset

Income statement’s cost of goods sold includes both the beginning inventory and the ending inventory

An error in the ending inventory will cause an error on both the Balance Sheet and Income Statement

Whose Inventory ?

The title to the goods passes to the buyer as soon as the seller delivers the goods to the transportation company

Goods in transit are included in the inventory of the buyer, not the seller

3

Title does not pass to the buyer until the goods are actually delivered

Goods in transit should not be included in the buyer’s inventory, but would be included in the inventory of the seller

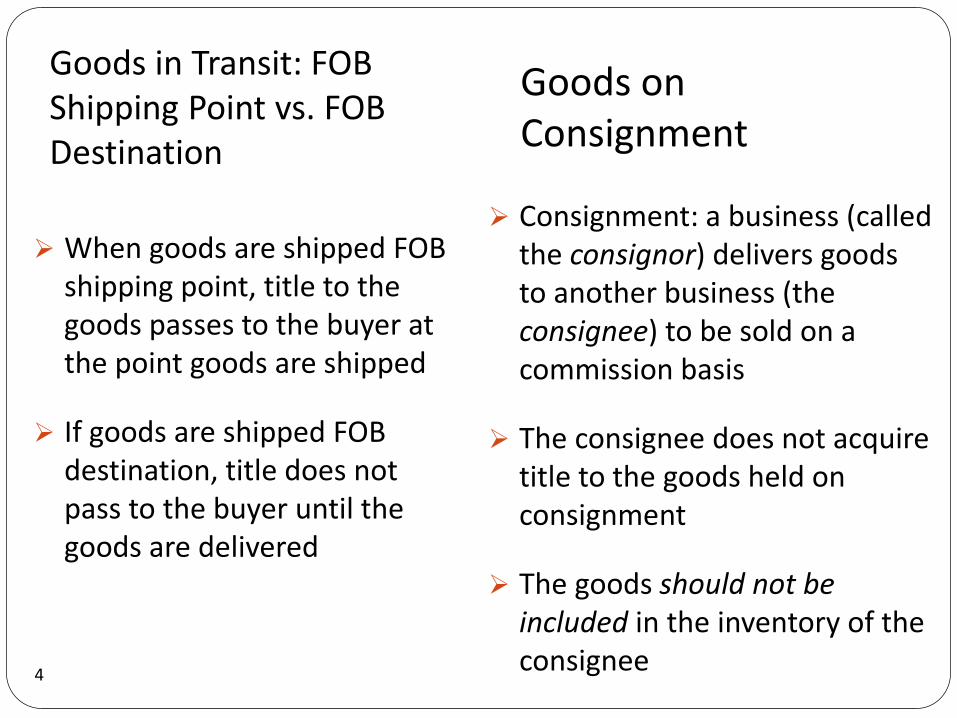

Goods in Transit: FOB Destination

Goods in Transit: FOB Shipping Point

Goods in Transit: FOB Shipping Point vs. FOB Destination

When goods are shipped FOB shipping point, title to the goods passes to the buyer at the point goods are shipped

If goods are shipped FOB destination, title does not pass to the buyer until the goods are delivered

4

Consignment: a business (called the consignor) delivers goods to another business (the consignee) to be sold on a commission basis

The consignee does not acquire title to the goods held on consignment

The goods should not be included in the inventory of the consignee

Goods on Consignment

Perpetual Inventory System Accounting records are maintained that continuously show

the amount of inventory on hand When merchandise is purchased, the Merchandise

Inventory account is increased by the amount of the purchase

When merchandise is sold, the Merchandise Inventory account is decreased by the cost of the merchandise sold

5

Periodic Inventory System Separate records are not maintained for individual inventory

items No attempt is made to adjust the Merchandise Inventory

account during the accounting period when new merchandise is purchased or when merchandise is sold

Merchandise is counted periodically and the Merchandise Inventory account is adjusted to show the value of the latest inventory

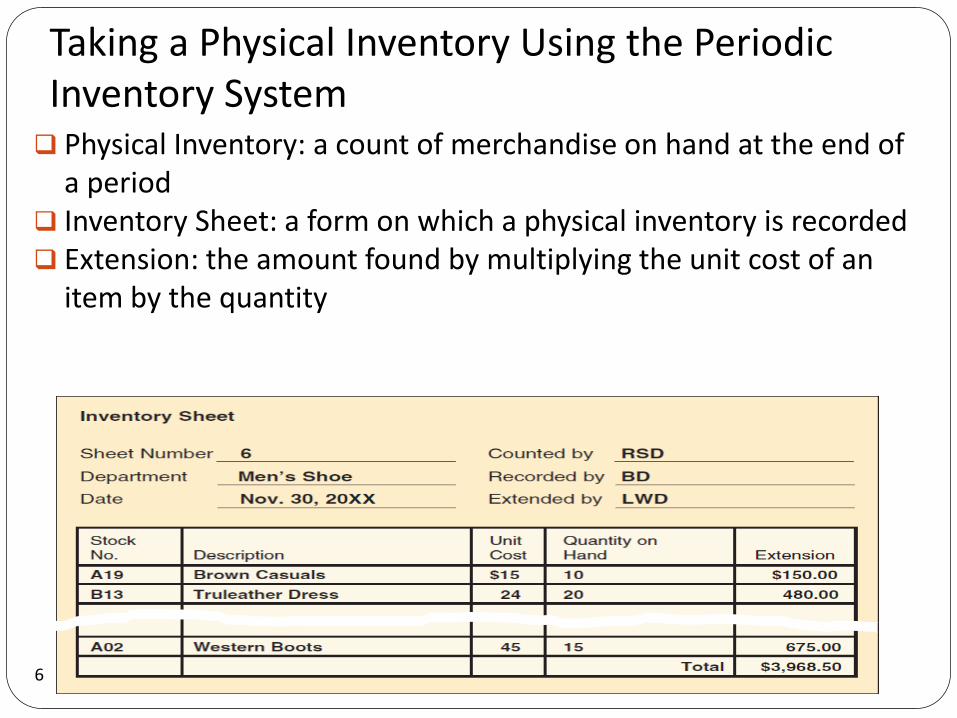

Taking a Physical Inventory Using the Periodic Inventory System Physical Inventory: a count of merchandise on hand at the end of

a period Inventory Sheet: a form on which a physical inventory is recorded Extension: the amount found by multiplying the unit cost of an

item by the quantity

6

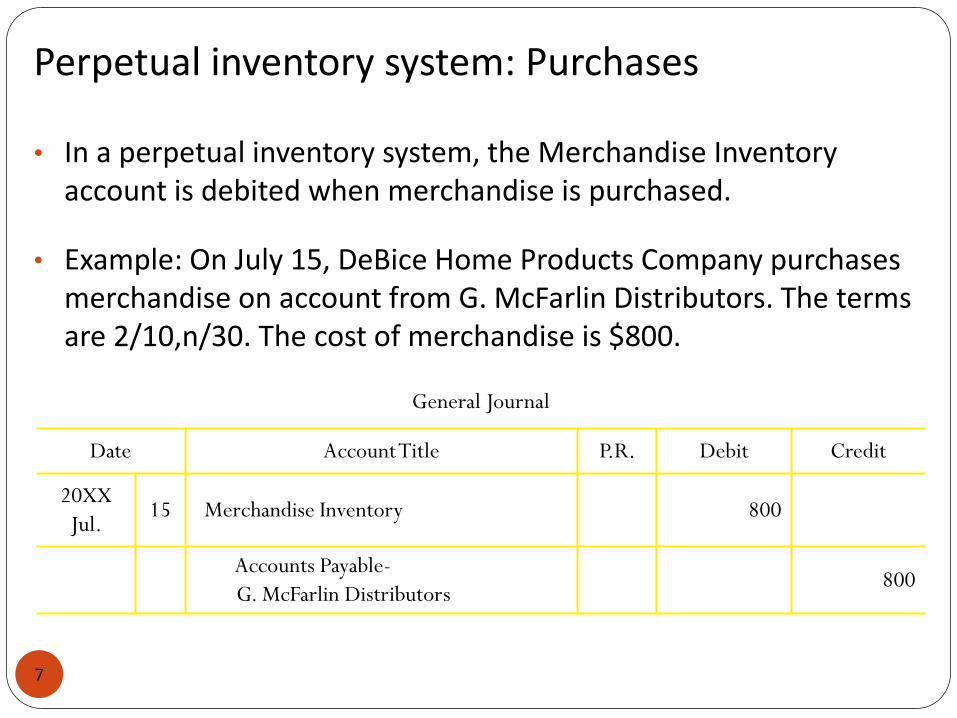

Perpetual inventory system: Purchases

• In a perpetual inventory system, the Merchandise Inventory account is debited when merchandise is purchased.

• Example: On July 15, DeBice Home Products Company purchases merchandise on account from G. McFarlin Distributors. The terms are 2/10,n/30. The cost of merchandise is $800.

7

General Journal

Date Account Title P.R. Debit Credit

20XX

Jul. 15 Merchandise Inventory 800

Accounts Payable-

G. McFarlin Distributors 800

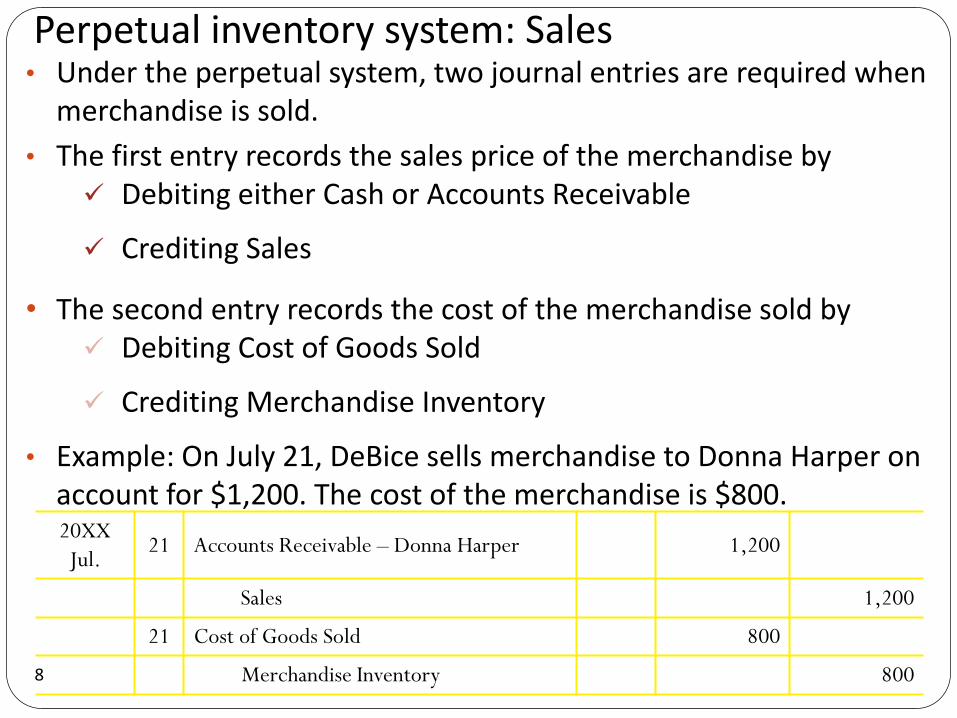

• Under the perpetual system, two journal entries are required when merchandise is sold.

• The first entry records the sales price of the merchandise by Debiting either Cash or Accounts Receivable

Crediting Sales

• The second entry records the cost of the merchandise sold by Debiting Cost of Goods Sold

Crediting Merchandise Inventory

• Example: On July 21, DeBice sells merchandise to Donna Harper on account for $1,200. The cost of the merchandise is $800.

8

Perpetual inventory system: Sales

20XX

Jul. 21 Accounts Receivable – Donna Harper 1,200

Sales 1,200

21 Cost of Goods Sold 800

Merchandise Inventory 800

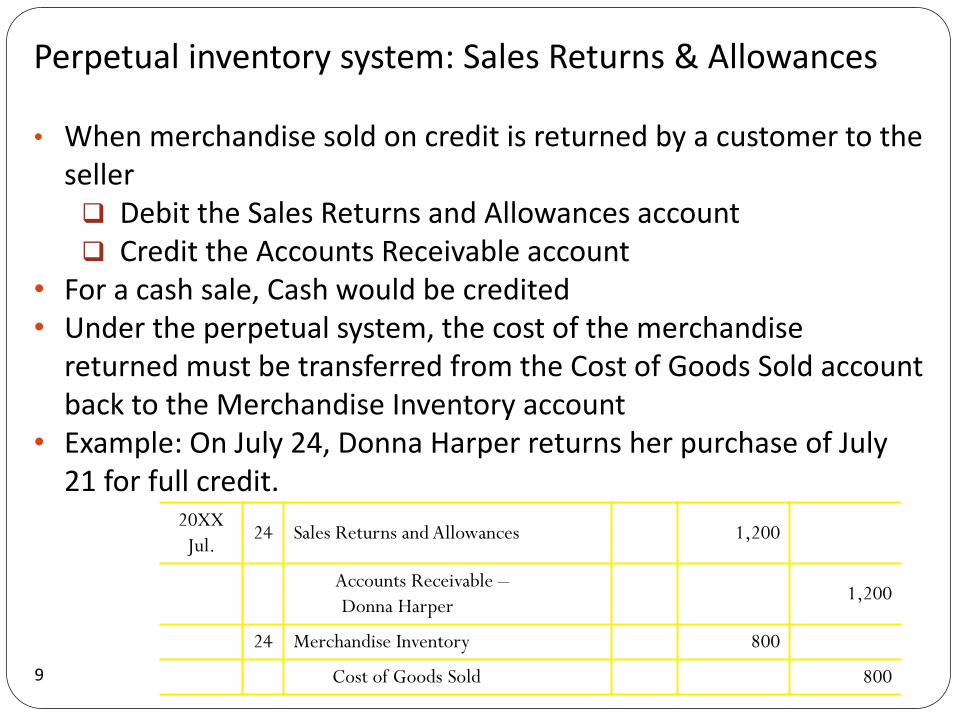

Perpetual inventory system: Sales Returns & Allowances

• When merchandise sold on credit is returned by a customer to the seller Debit the Sales Returns and Allowances account Credit the Accounts Receivable account

• For a cash sale, Cash would be credited • Under the perpetual system, the cost of the merchandise

returned must be transferred from the Cost of Goods Sold account back to the Merchandise Inventory account

• Example: On July 24, Donna Harper returns her purchase of July 21 for full credit.

9

20XX

Jul. 24 Sales Returns and Allowances 1,200

Accounts Receivable –

Donna Harper 1,200

24 Merchandise Inventory 800

Cost of Goods Sold 800

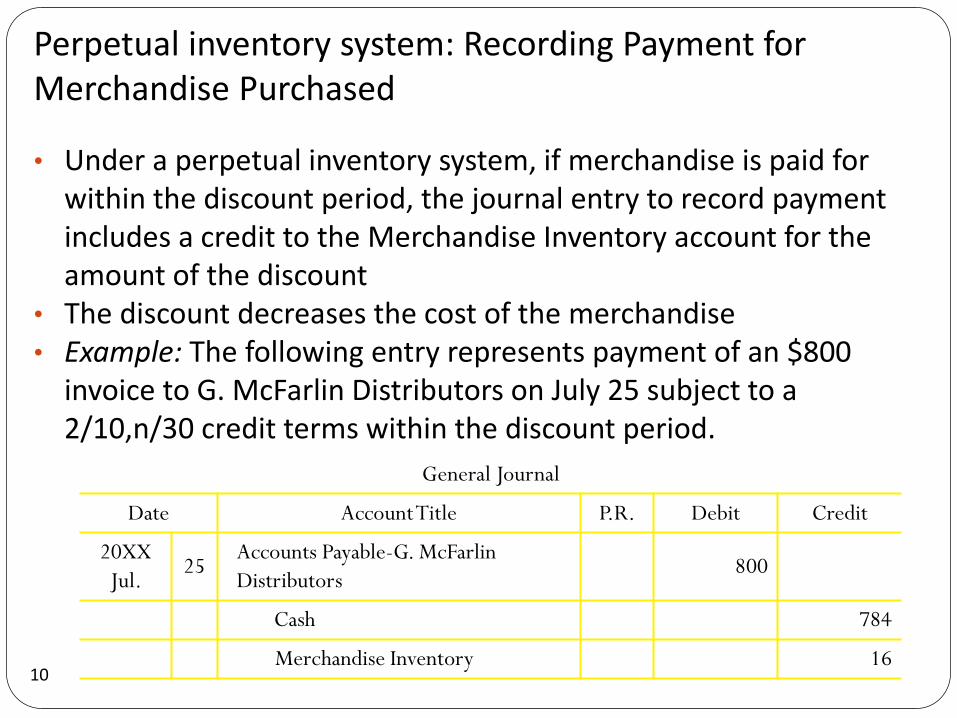

Perpetual inventory system: Recording Payment for Merchandise Purchased

• Under a perpetual inventory system, if merchandise is paid for within the discount period, the journal entry to record payment includes a credit to the Merchandise Inventory account for the amount of the discount

• The discount decreases the cost of the merchandise • Example: The following entry represents payment of an $800

invoice to G. McFarlin Distributors on July 25 subject to a 2/10,n/30 credit terms within the discount period.

10

General Journal

Date Account Title P.R. Debit Credit

20XX

Jul. 25

Accounts Payable-G. McFarlin

Distributors 800

Cash 784

Merchandise Inventory 16

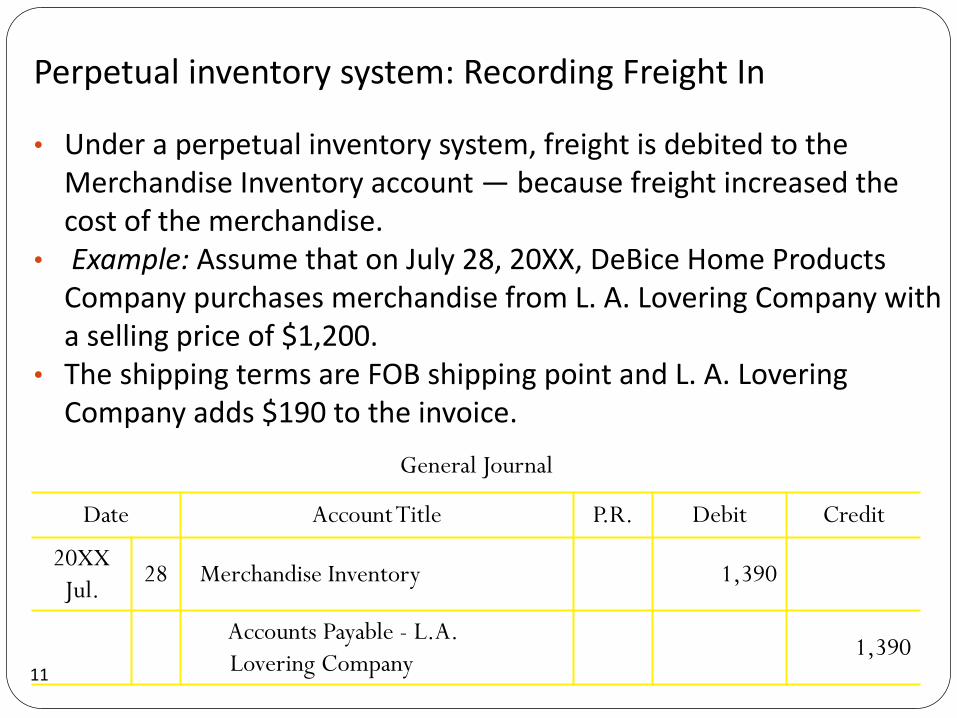

Perpetual inventory system: Recording Freight In

• Under a perpetual inventory system, freight is debited to the Merchandise Inventory account — because freight increased the cost of the merchandise.

• Example: Assume that on July 28, 20XX, DeBice Home Products Company purchases merchandise from L. A. Lovering Company with a selling price of $1,200.

• The shipping terms are FOB shipping point and L. A. Lovering Company adds $190 to the invoice.

11

General Journal

Date Account Title P.R. Debit Credit

20XX

Jul. 28 Merchandise Inventory 1,390

Accounts Payable - L.A.

Lovering Company 1,390

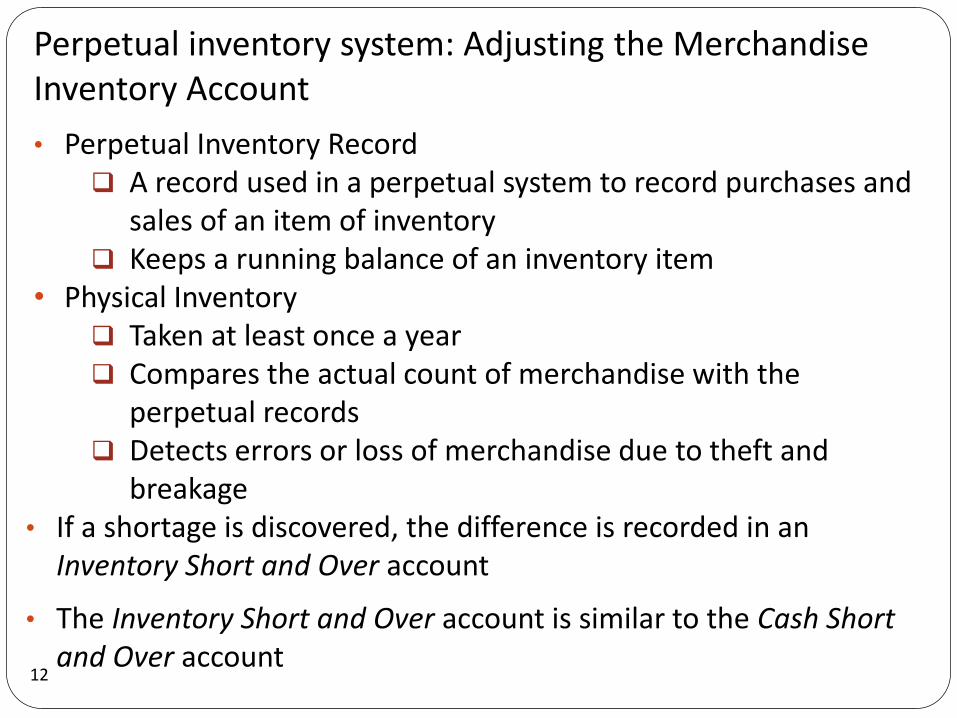

Perpetual inventory system: Adjusting the Merchandise Inventory Account

• Perpetual Inventory Record A record used in a perpetual system to record purchases and

sales of an item of inventory Keeps a running balance of an inventory item

• Physical Inventory Taken at least once a year Compares the actual count of merchandise with the

perpetual records Detects errors or loss of merchandise due to theft and

breakage

12

• If a shortage is discovered, the difference is recorded in an Inventory Short and Over account

• The Inventory Short and Over account is similar to the Cash Short and Over account

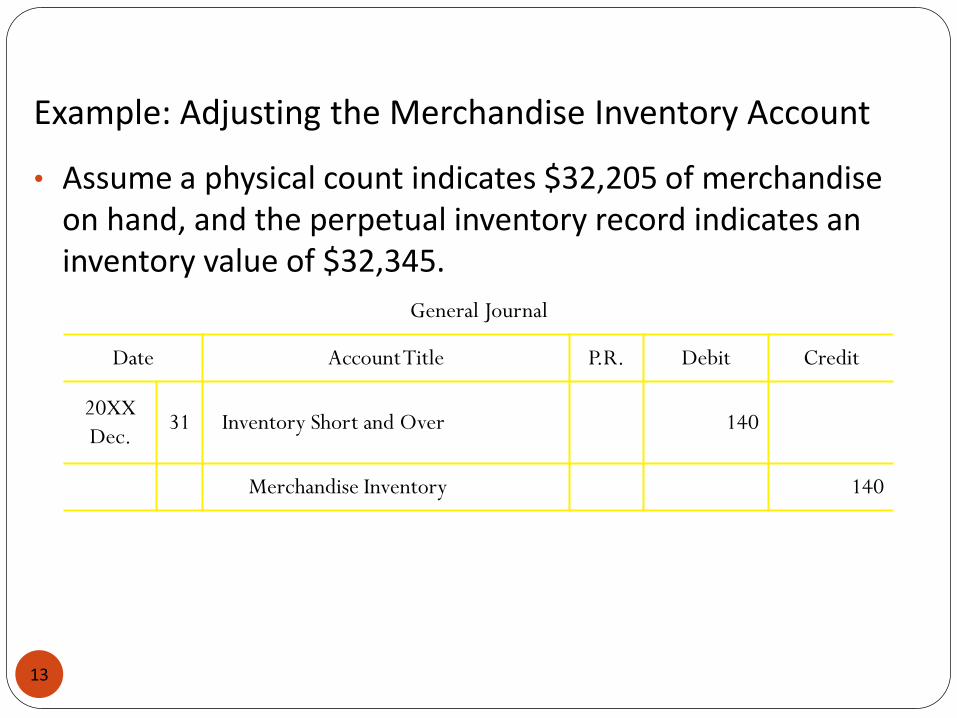

Example: Adjusting the Merchandise Inventory Account

13

• Assume a physical count indicates $32,205 of merchandise on hand, and the perpetual inventory record indicates an inventory value of $32,345.

General Journal

Date Account Title P.R. Debit Credit

20XX

Dec. 31 Inventory Short and Over 140

Merchandise Inventory 140

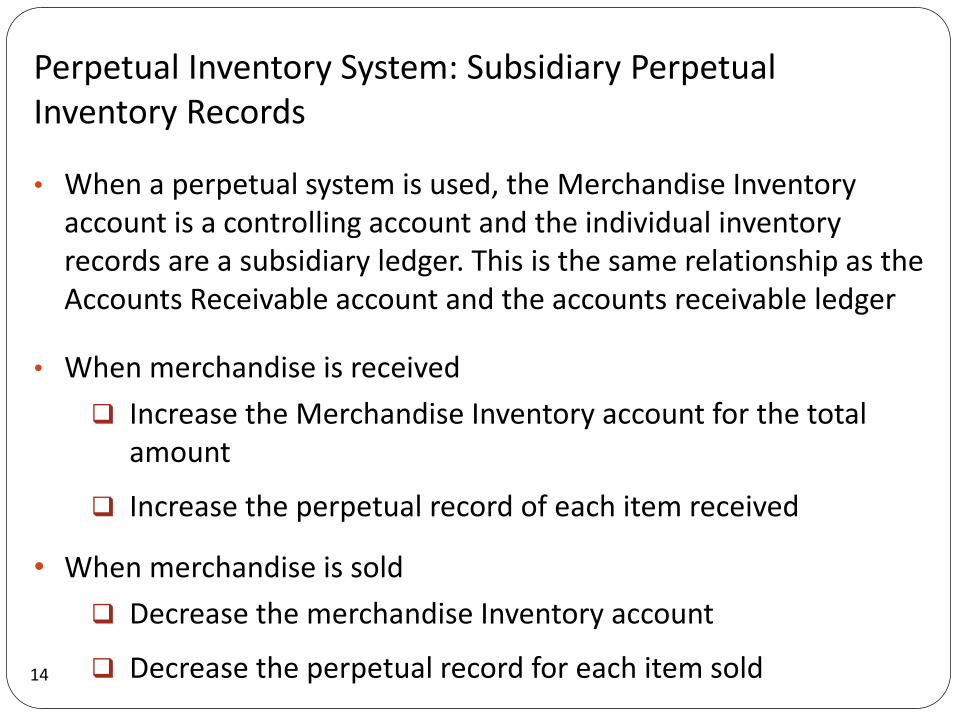

• When merchandise is received

Increase the Merchandise Inventory account for the total amount

Increase the perpetual record of each item received

• When merchandise is sold

Decrease the merchandise Inventory account

Decrease the perpetual record for each item sold

Perpetual Inventory System: Subsidiary Perpetual Inventory Records

• When a perpetual system is used, the Merchandise Inventory account is a controlling account and the individual inventory records are a subsidiary ledger. This is the same relationship as the Accounts Receivable account and the accounts receivable ledger

14

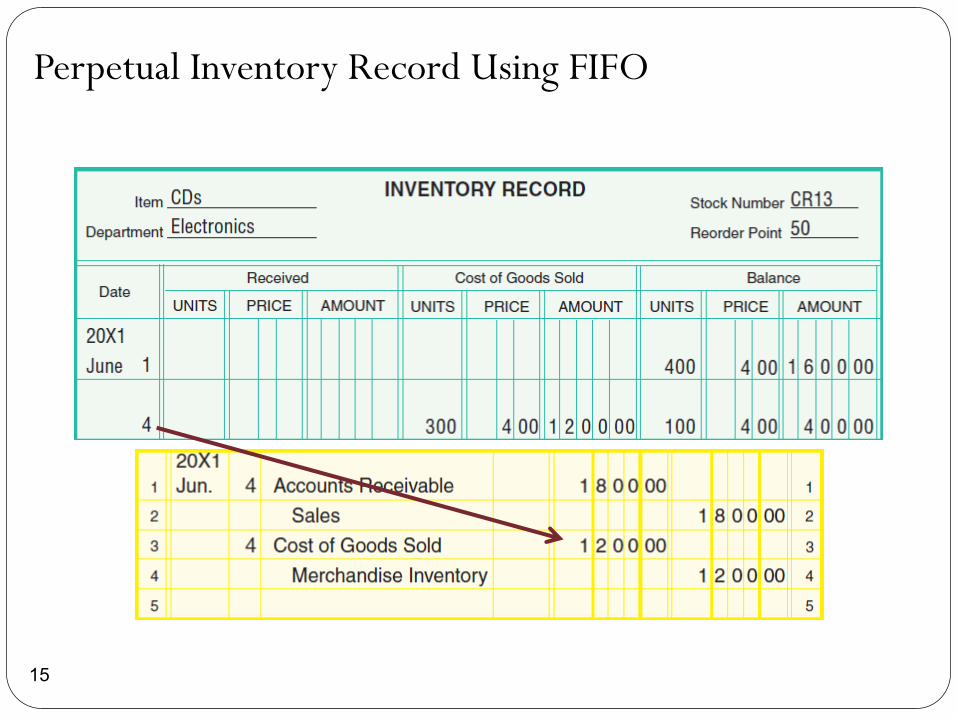

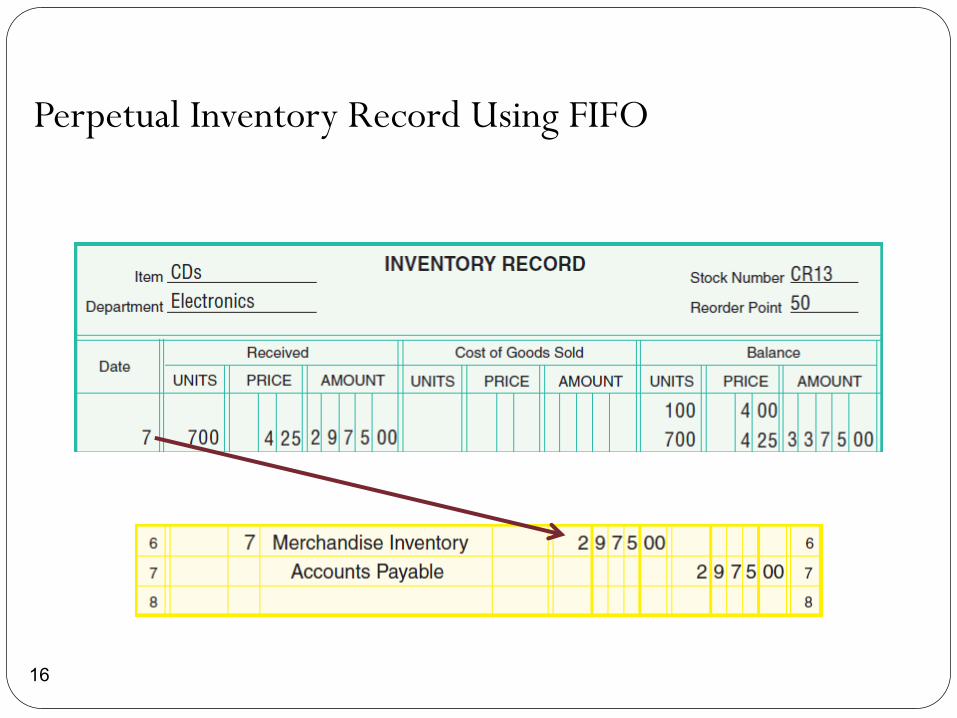

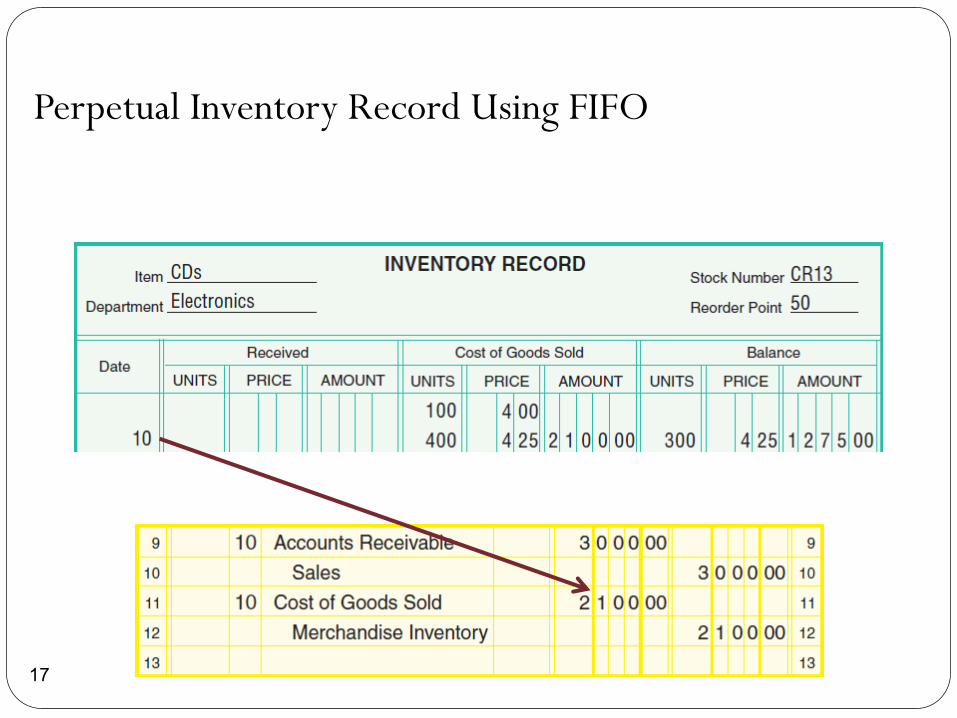

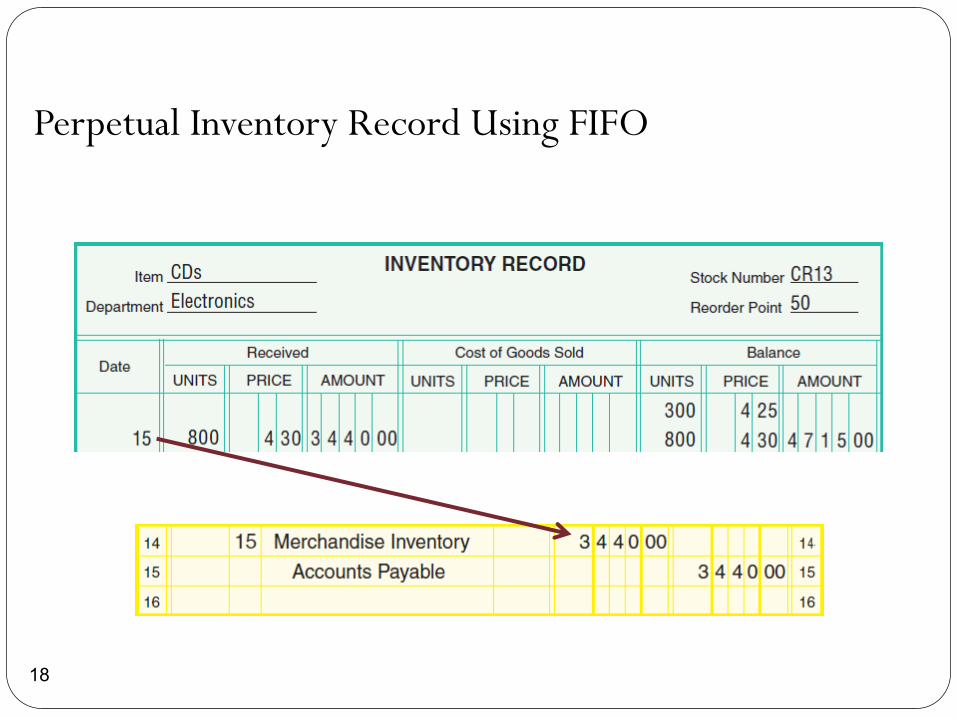

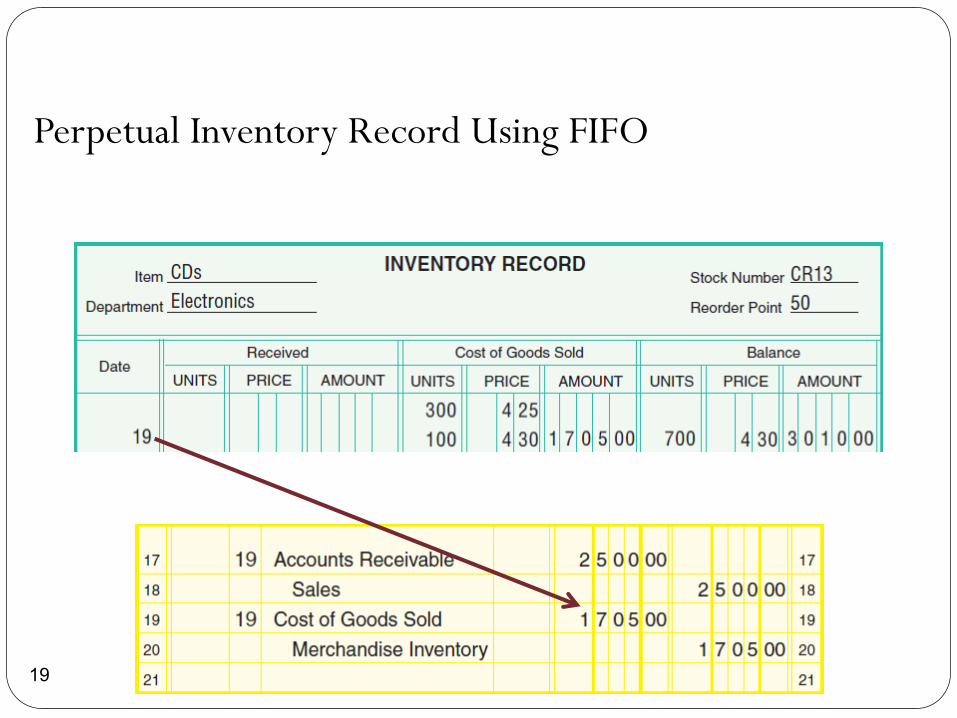

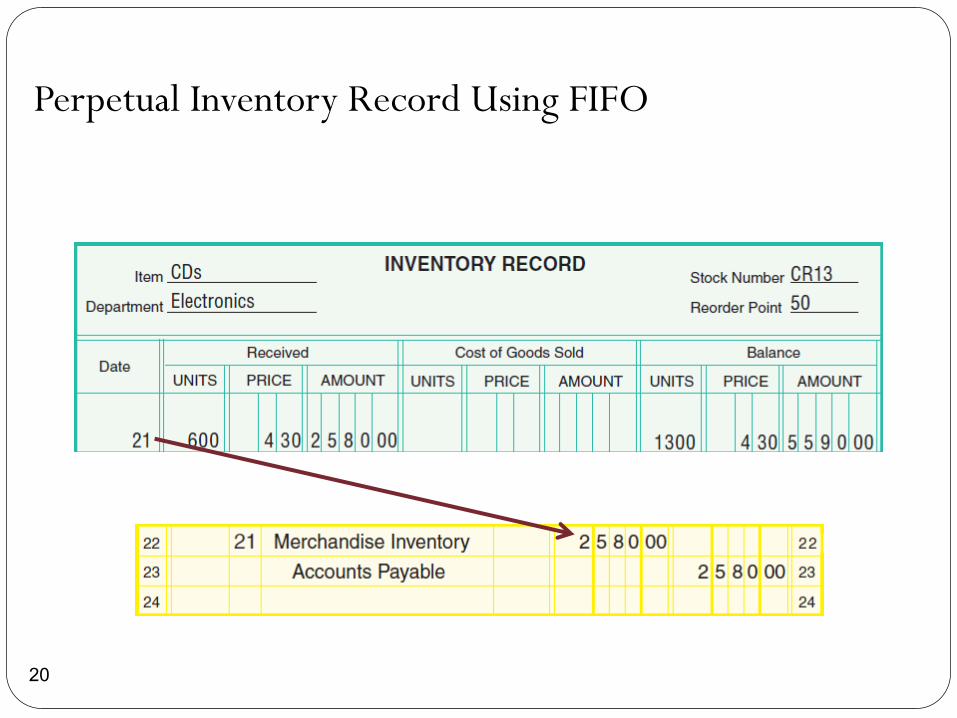

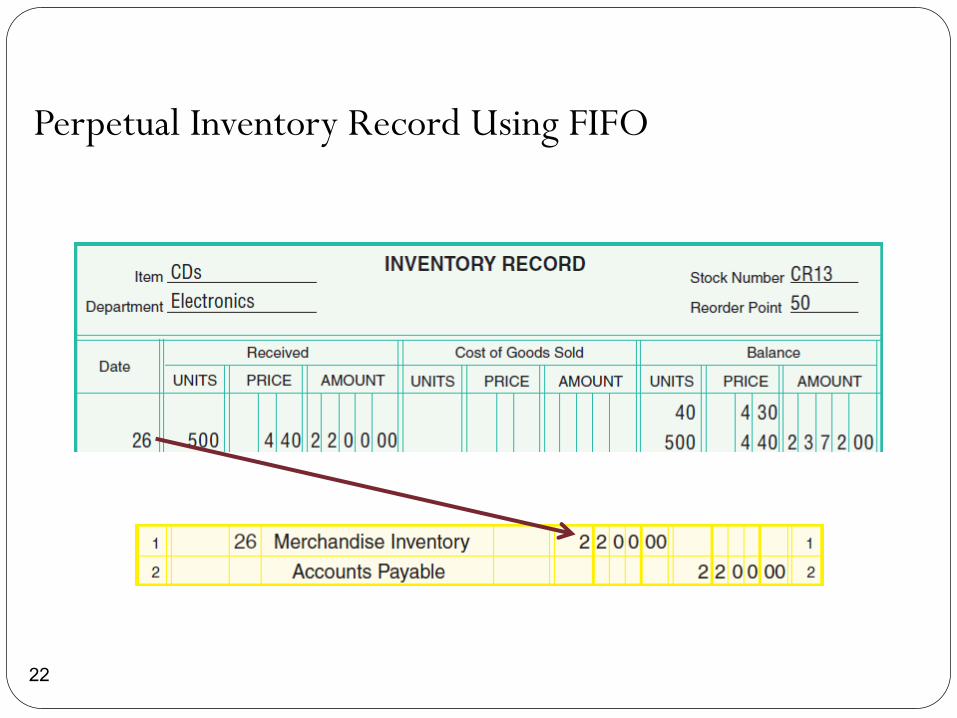

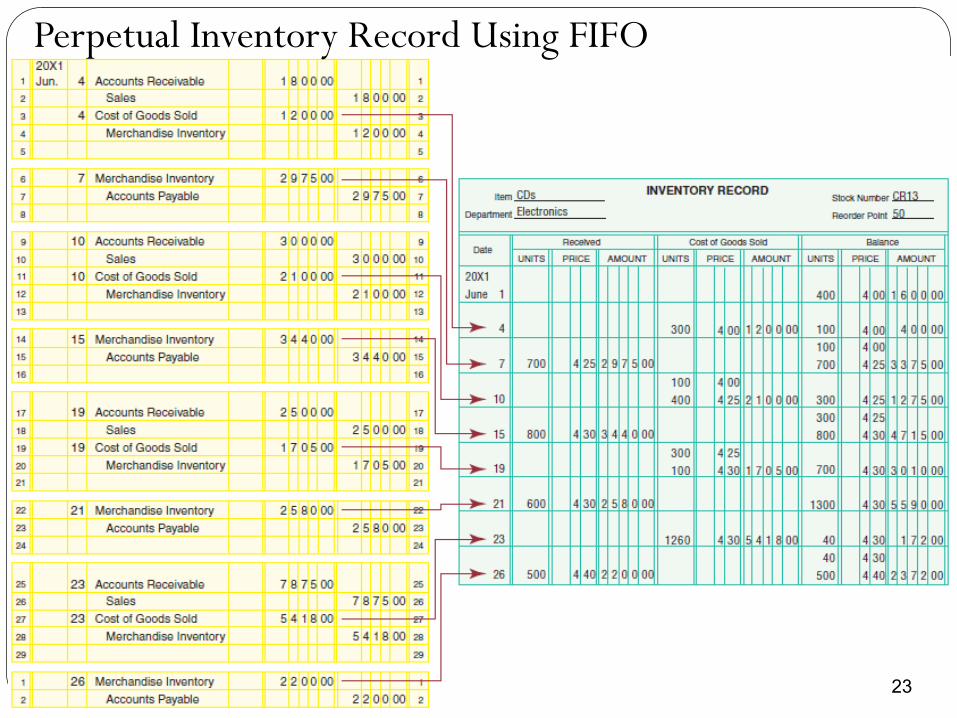

Perpetual Inventory Record Using FIFO

15

Perpetual Inventory Record Using FIFO

16

Perpetual Inventory Record Using FIFO

17

Perpetual Inventory Record Using FIFO

18

Perpetual Inventory Record Using FIFO

19

Perpetual Inventory Record Using FIFO

20

Perpetual Inventory Record Using FIFO

21

Perpetual Inventory Record Using FIFO

22

Perpetual Inventory Record Using FIFO

23

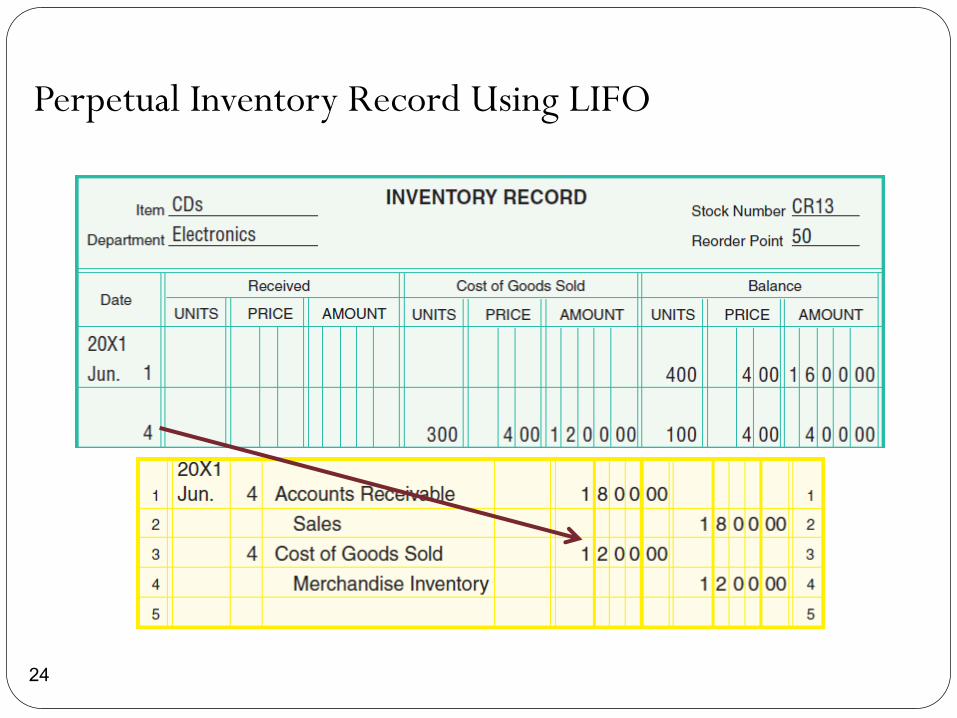

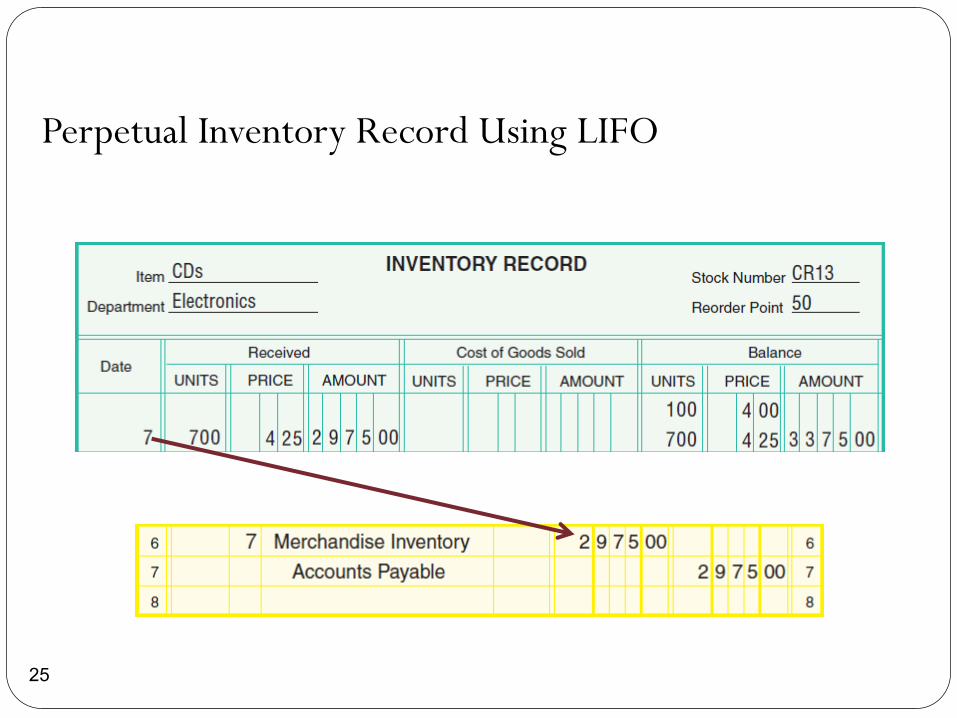

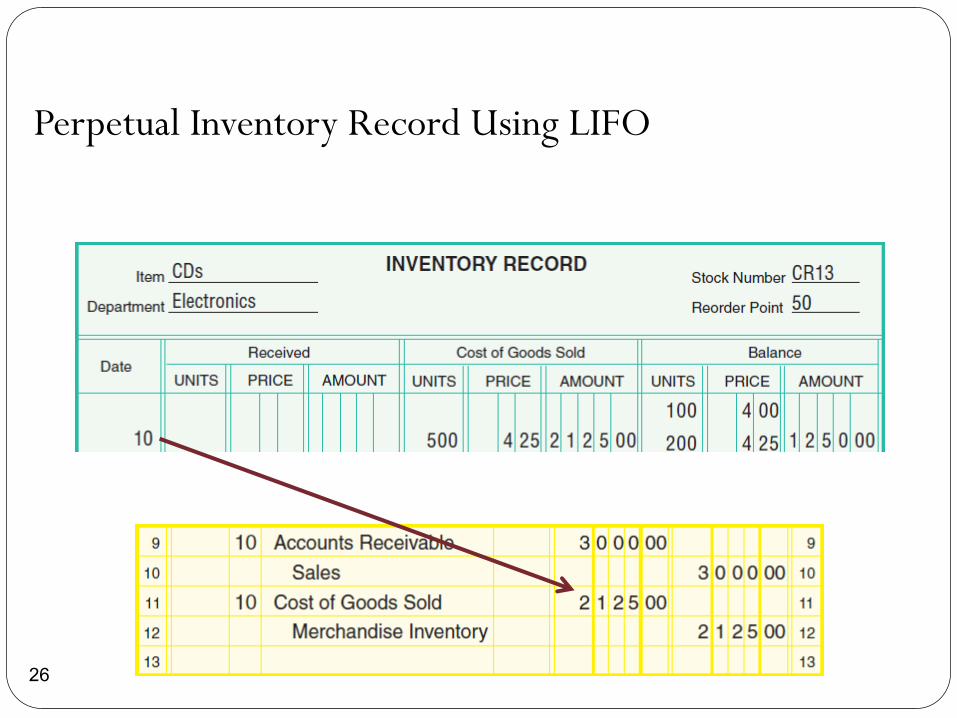

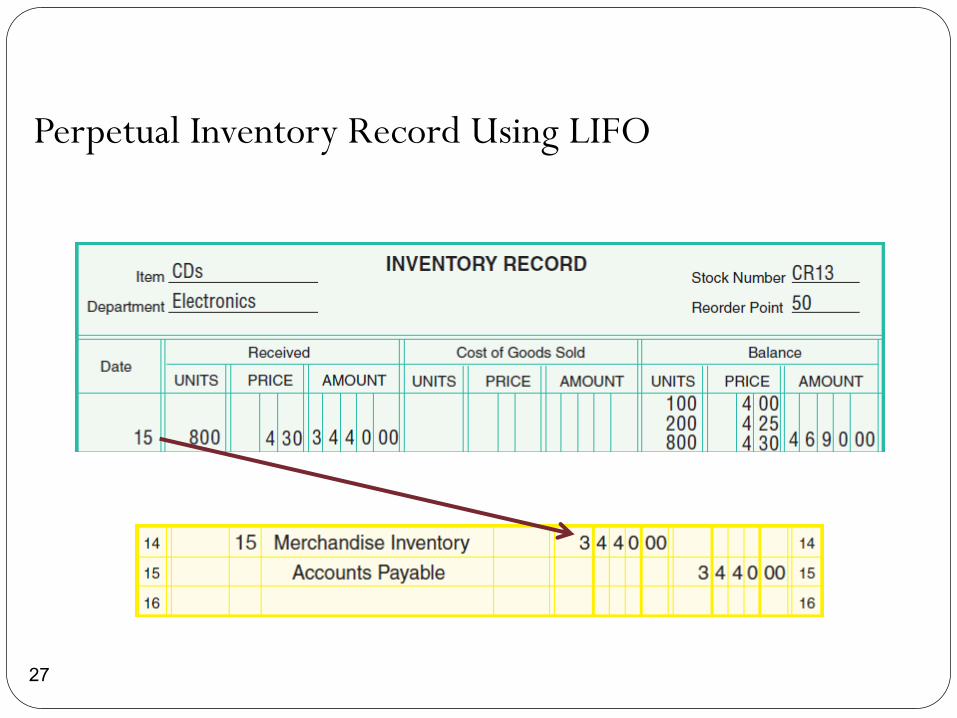

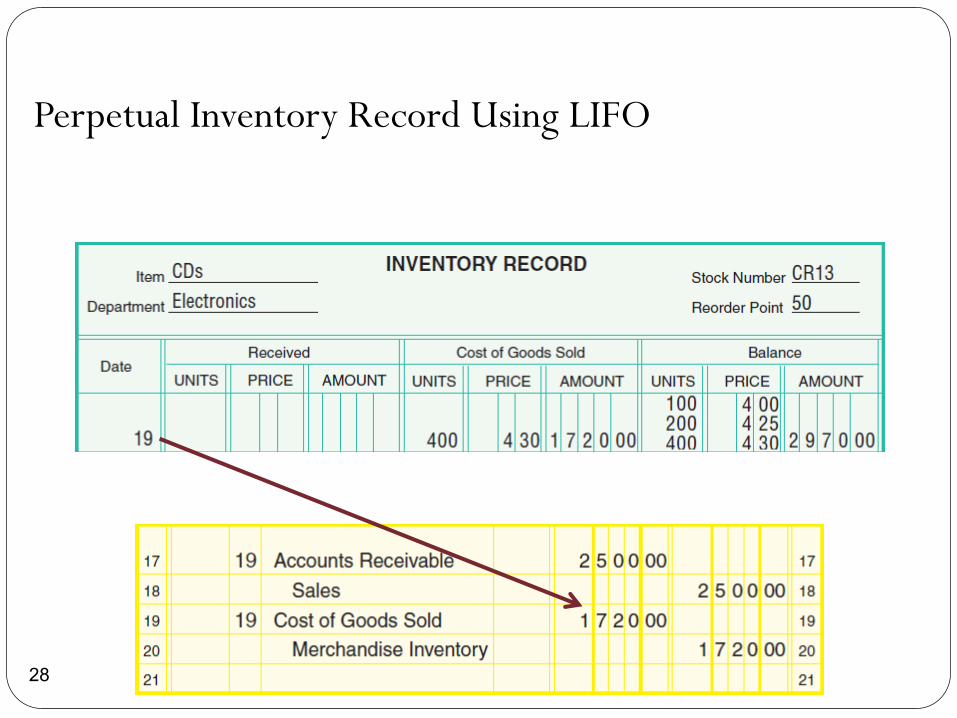

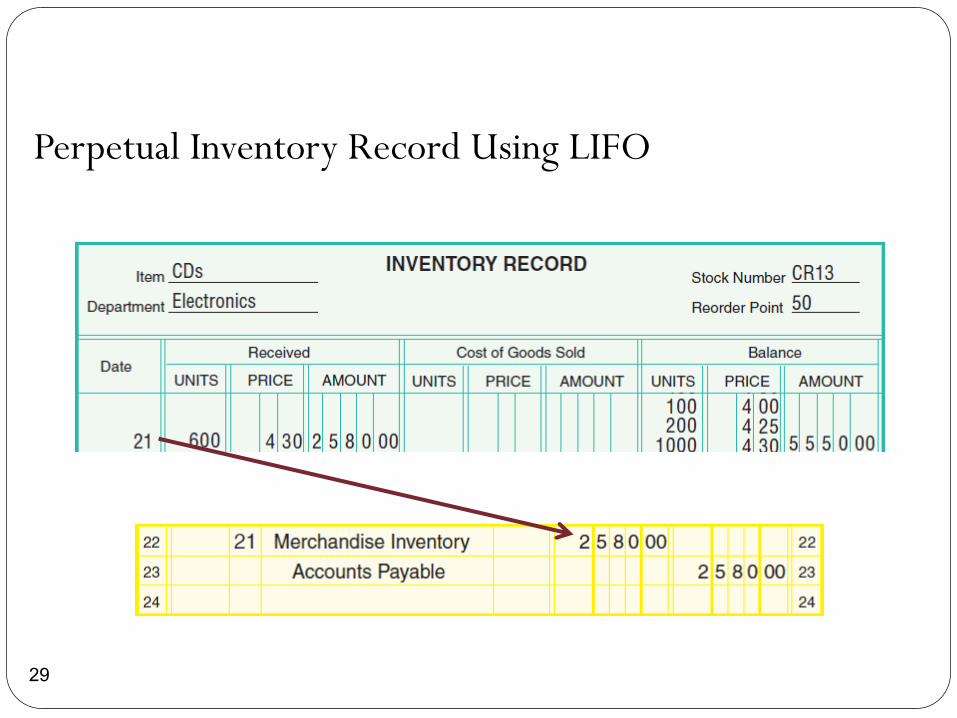

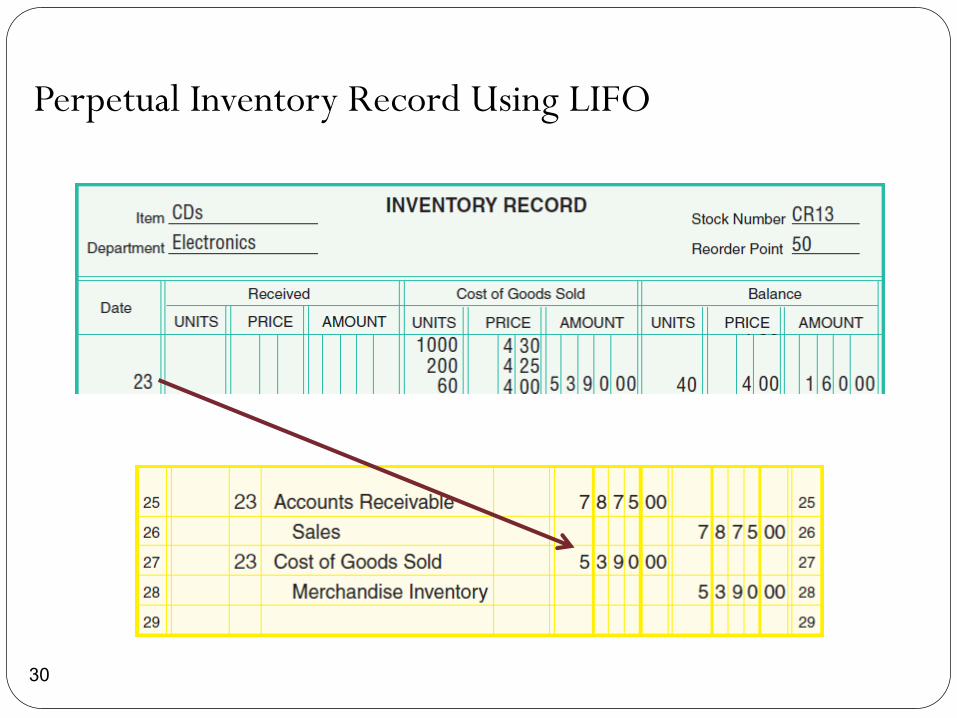

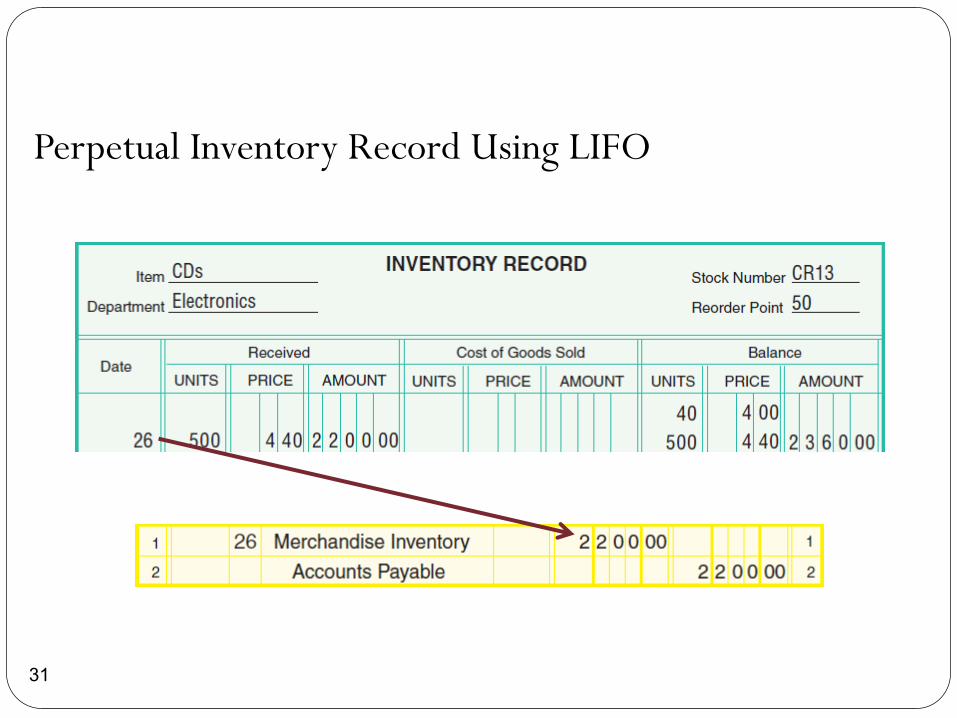

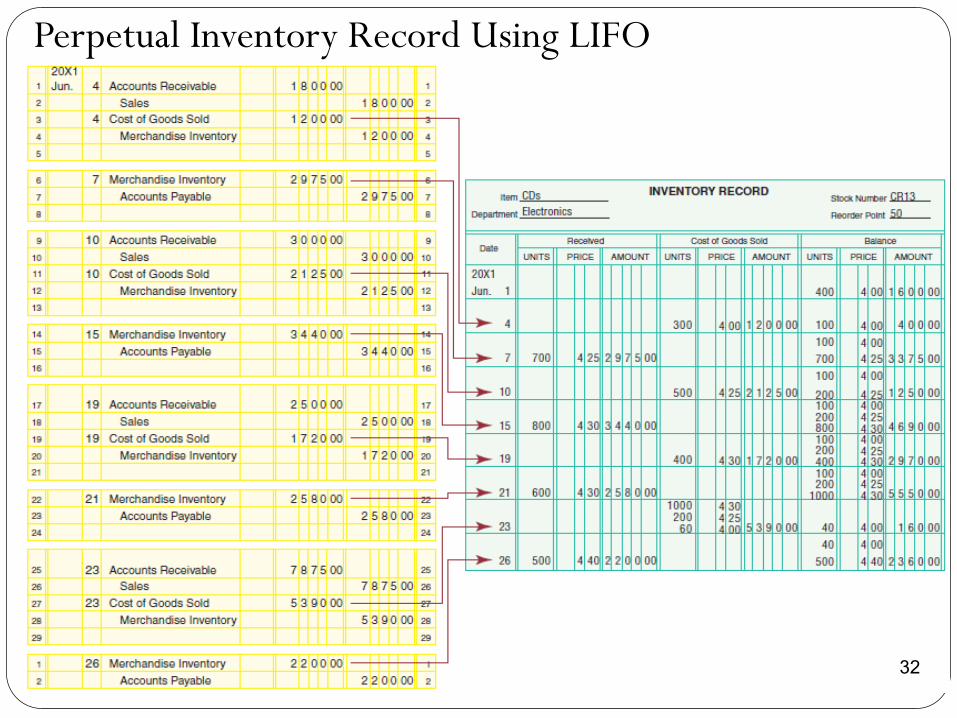

Perpetual Inventory Record Using LIFO

24

Perpetual Inventory Record Using LIFO

25

Perpetual Inventory Record Using LIFO

26

Perpetual Inventory Record Using LIFO

27

Perpetual Inventory Record Using LIFO

28

Perpetual Inventory Record Using LIFO

29

Perpetual Inventory Record Using LIFO

30

Perpetual Inventory Record Using LIFO

31

Perpetual Inventory Record Using LIFO

32

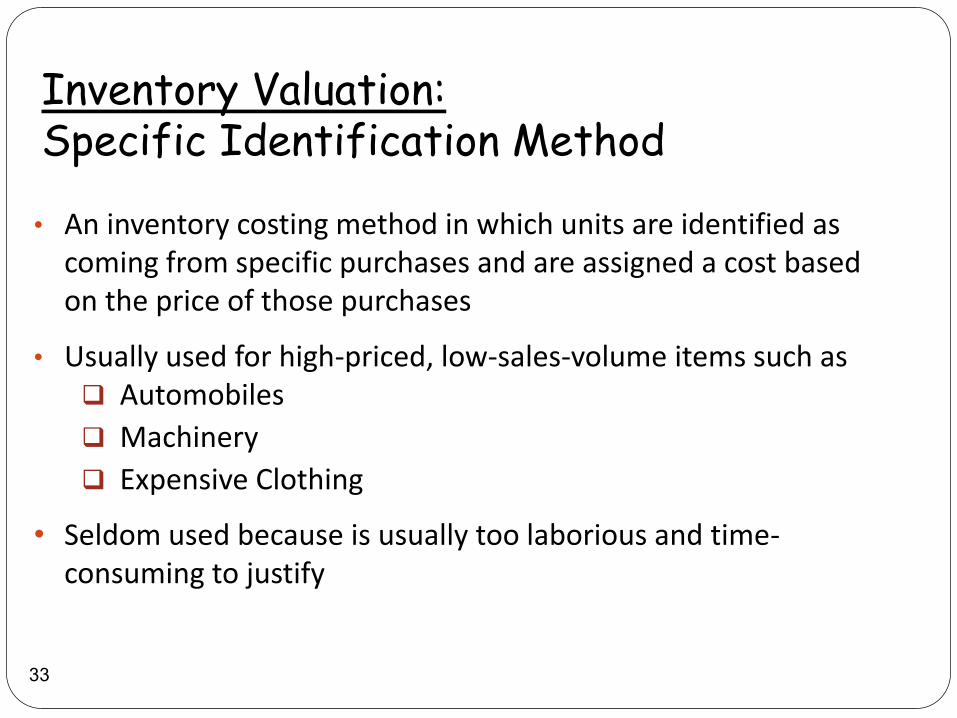

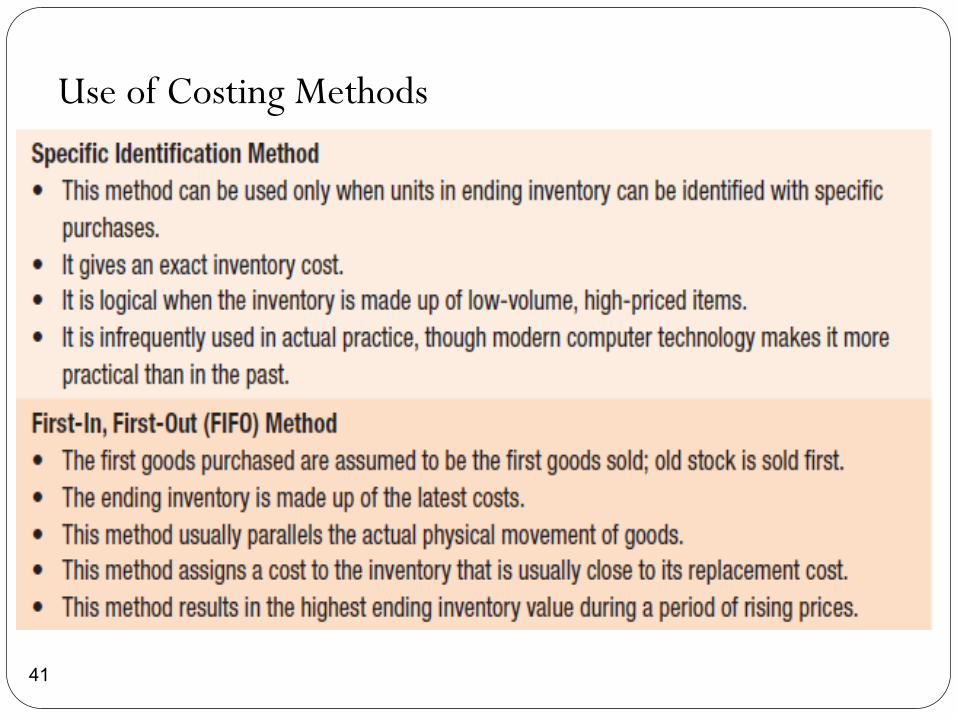

Inventory Valuation: Specific Identification Method

• An inventory costing method in which units are identified as coming from specific purchases and are assigned a cost based on the price of those purchases

• Usually used for high-priced, low-sales-volume items such as Automobiles

Machinery

Expensive Clothing

• Seldom used because is usually too laborious and time-consuming to justify

33

34

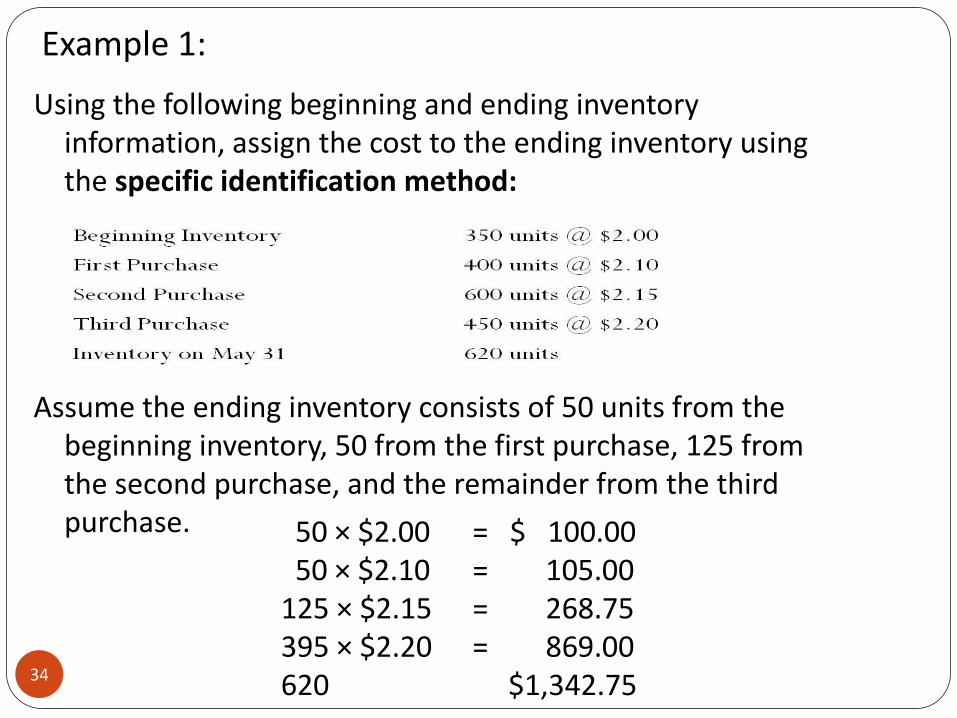

Using the following beginning and ending inventory information, assign the cost to the ending inventory using the specific identification method:

Assume the ending inventory consists of 50 units from the

beginning inventory, 50 from the first purchase, 125 from the second purchase, and the remainder from the third purchase.

Example 1:

50 × $2.00 = $ 100.00 50 × $2.10 = 105.00 125 × $2.15 = 268.75 395 × $2.20 = 869.00 620 $1,342.75

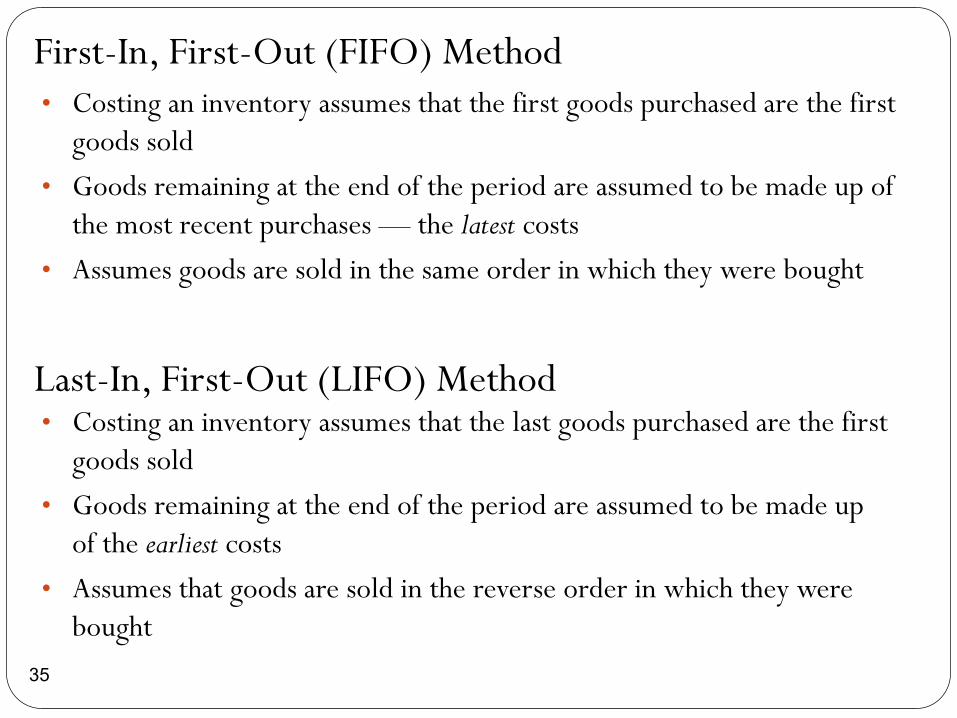

First-In, First-Out (FIFO) Method • Costing an inventory assumes that the first goods purchased are the first

goods sold

• Goods remaining at the end of the period are assumed to be made up of

the most recent purchases — the latest costs

• Assumes goods are sold in the same order in which they were bought

35

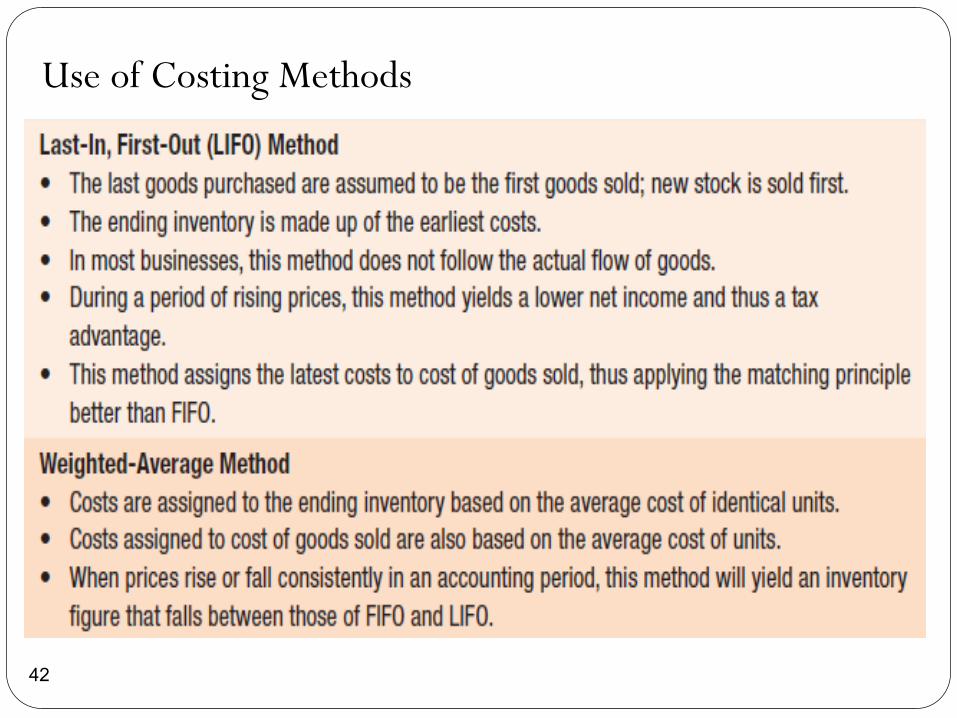

Last-In, First-Out (LIFO) Method • Costing an inventory assumes that the last goods purchased are the first

goods sold

• Goods remaining at the end of the period are assumed to be made up

of the earliest costs

• Assumes that goods are sold in the reverse order in which they were

bought

36

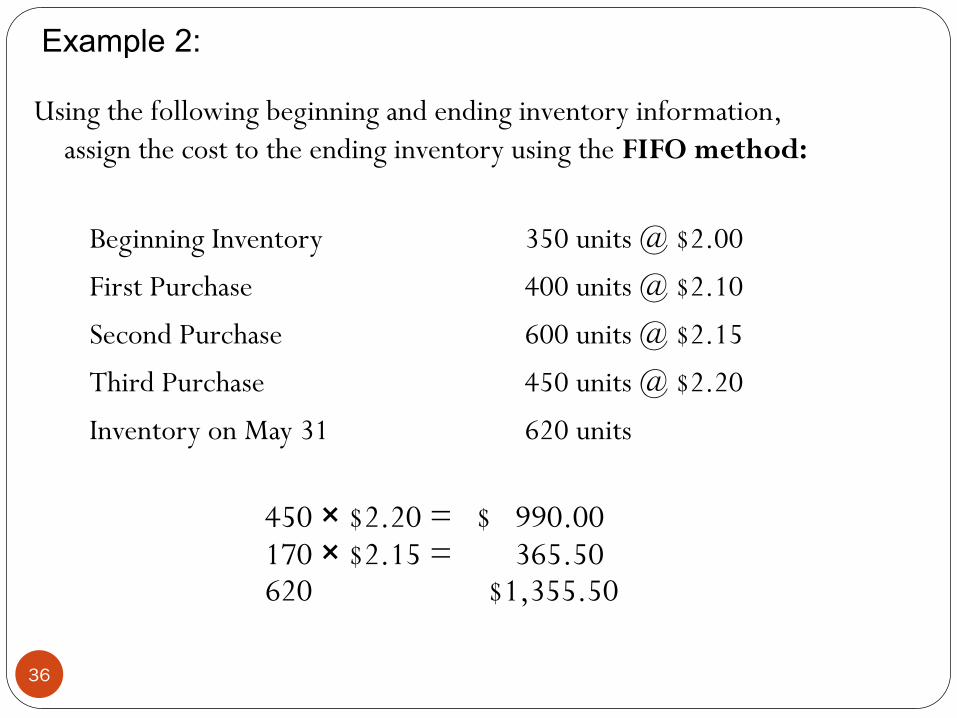

Using the following beginning and ending inventory information,

assign the cost to the ending inventory using the FIFO method:

Beginning Inventory 350 units @ $2.00

First Purchase 400 units @ $2.10

Second Purchase 600 units @ $2.15

Third Purchase 450 units @ $2.20

Inventory on May 31 620 units

450 × $2.20 = $ 990.00 170 × $2.15 = 365.50 620 $1,355.50

Example 2:

37

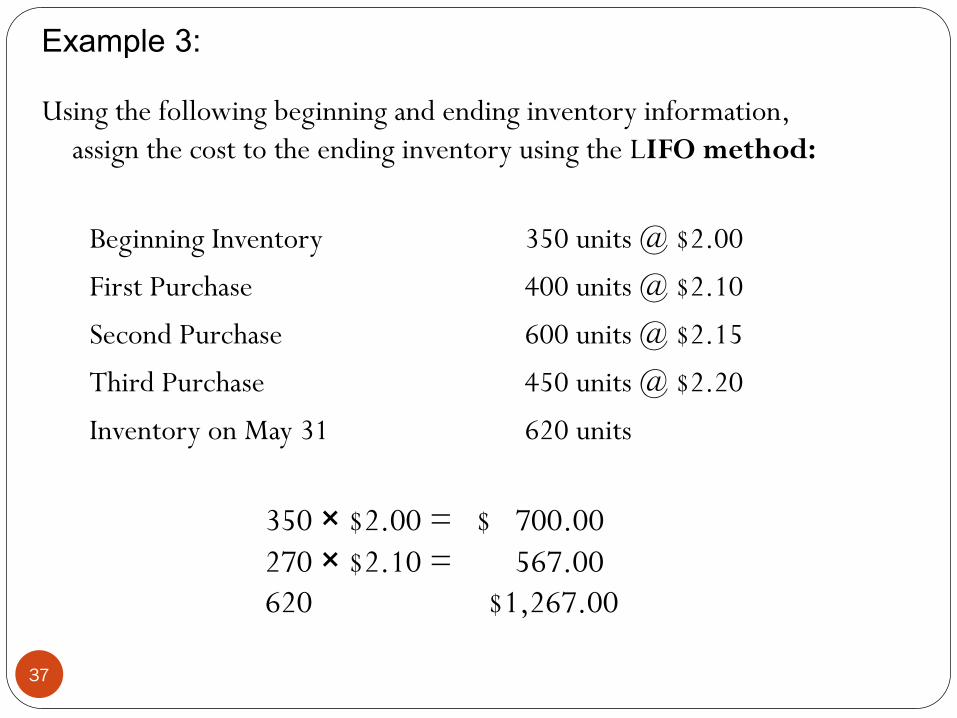

Using the following beginning and ending inventory information,

assign the cost to the ending inventory using the LIFO method:

Beginning Inventory 350 units @ $2.00

First Purchase 400 units @ $2.10

Second Purchase 600 units @ $2.15

Third Purchase 450 units @ $2.20

Inventory on May 31 620 units

350 × $2.00 = $ 700.00

270 × $2.10 = 567.00

620 $1,267.00

Example 3:

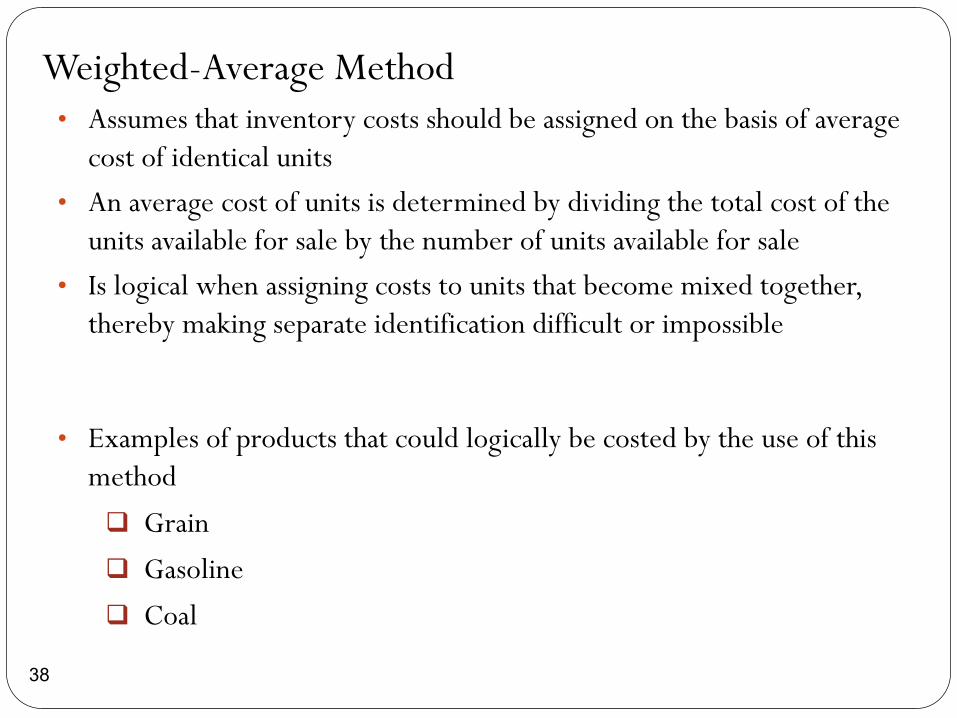

• Examples of products that could logically be costed by the use of this

method

Grain

Gasoline

Coal

Weighted-Average Method • Assumes that inventory costs should be assigned on the basis of average

cost of identical units

• An average cost of units is determined by dividing the total cost of the

units available for sale by the number of units available for sale

• Is logical when assigning costs to units that become mixed together,

thereby making separate identification difficult or impossible

38

39

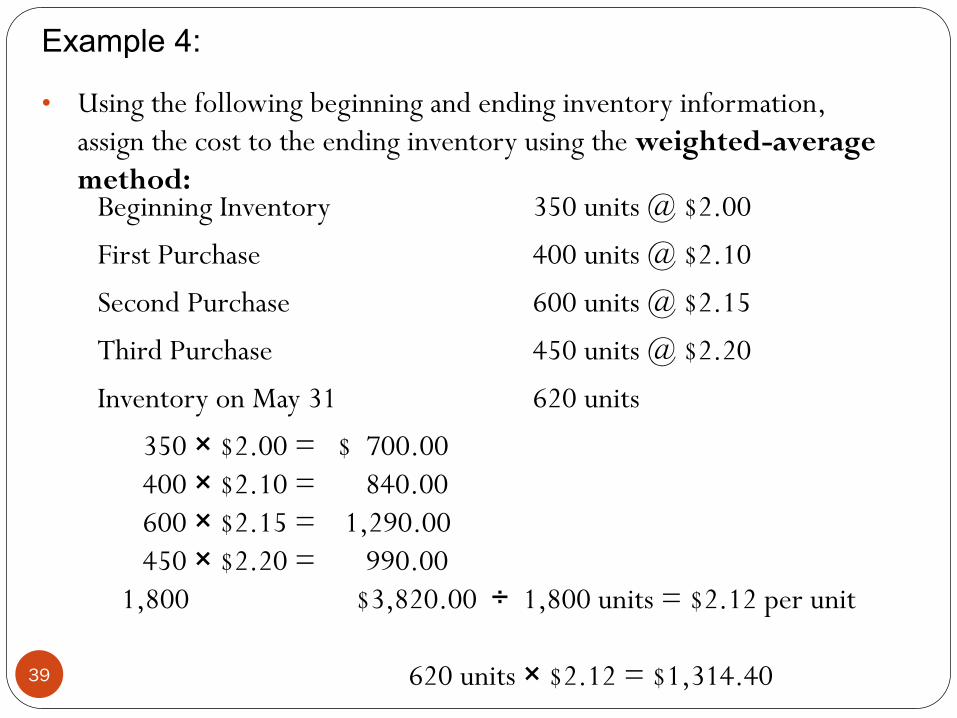

• Using the following beginning and ending inventory information,

assign the cost to the ending inventory using the weighted-average

method: Beginning Inventory 350 units @ $2.00

First Purchase 400 units @ $2.10

Second Purchase 600 units @ $2.15

Third Purchase 450 units @ $2.20

Inventory on May 31 620 units

350 × $2.00 = $ 700.00

400 × $2.10 = 840.00

600 × $2.15 = 1,290.00

450 × $2.20 = 990.00

1,800 $3,820.00 ÷ 1,800 units = $2.12 per unit

620 units × $2.12 = $1,314.40

Example 4:

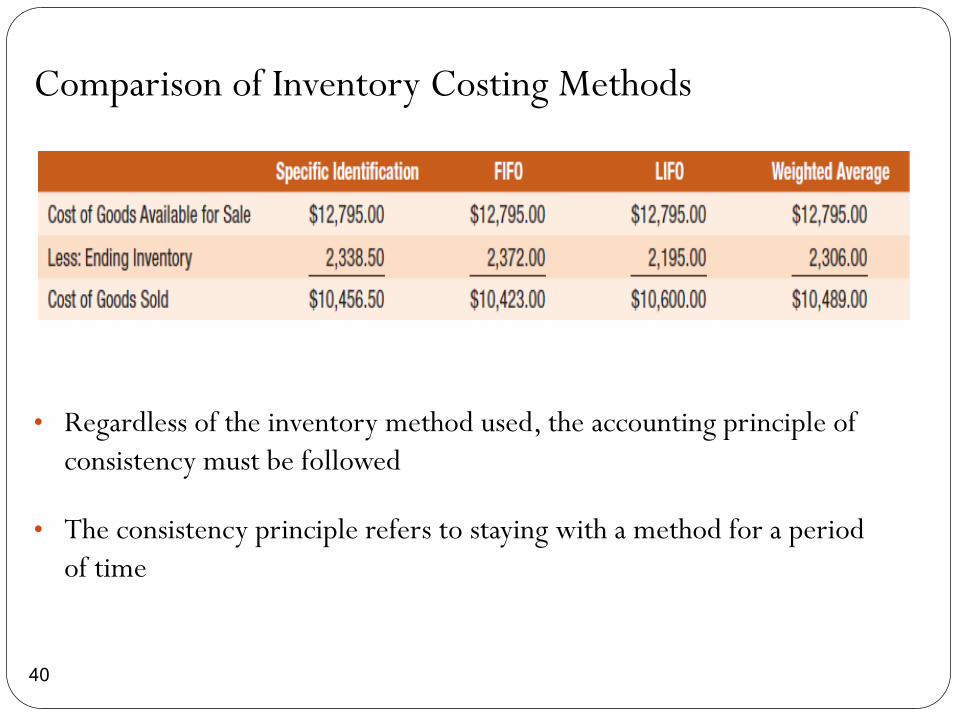

Comparison of Inventory Costing Methods

• Regardless of the inventory method used, the accounting principle of

consistency must be followed

• The consistency principle refers to staying with a method for a period

of time

40

Use of Costing Methods

41

Use of Costing Methods

42

Inventory Estimation: Gross Profit Method and Retail

Method

• Financial statements prepared for a period of time less than a fiscal year

• Require a business to determine an inventory at the

End of the month or

Quarter

• The amount of the inventory may be estimated using

Gross profit method or

Retail method

43

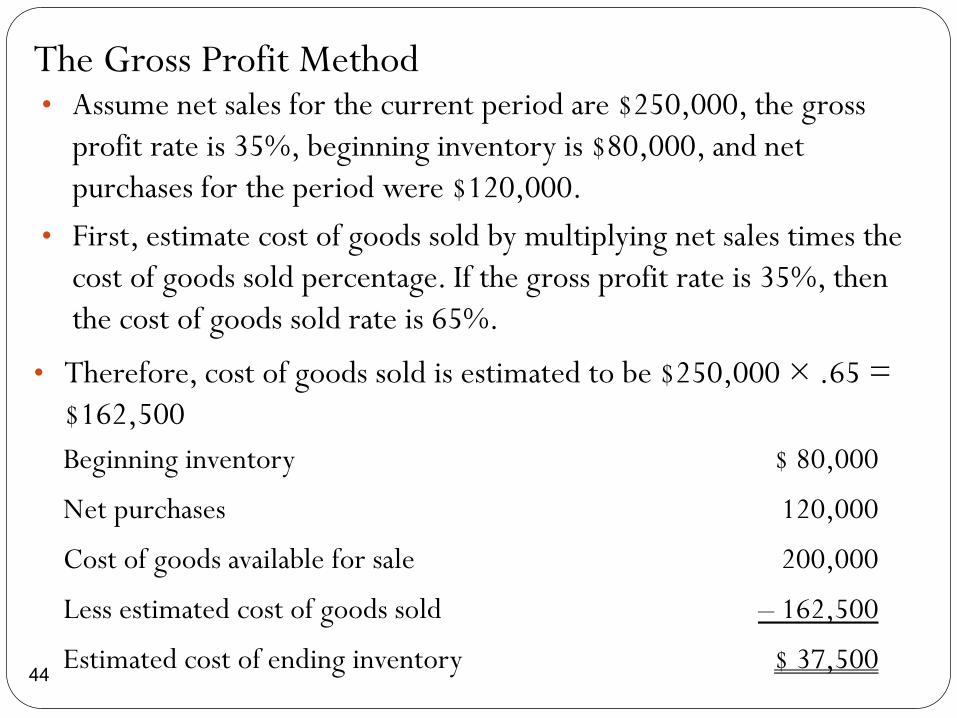

Beginning inventory $ 80,000

Net purchases 120,000

Cost of goods available for sale 200,000

Less estimated cost of goods sold – 162,500

Estimated cost of ending inventory $ 37,500

The Gross Profit Method

44

• Assume net sales for the current period are $250,000, the gross

profit rate is 35%, beginning inventory is $80,000, and net

purchases for the period were $120,000.

• First, estimate cost of goods sold by multiplying net sales times the

cost of goods sold percentage. If the gross profit rate is 35%, then

the cost of goods sold rate is 65%.

• Therefore, cost of goods sold is estimated to be $250,000 × .65 =

$162,500

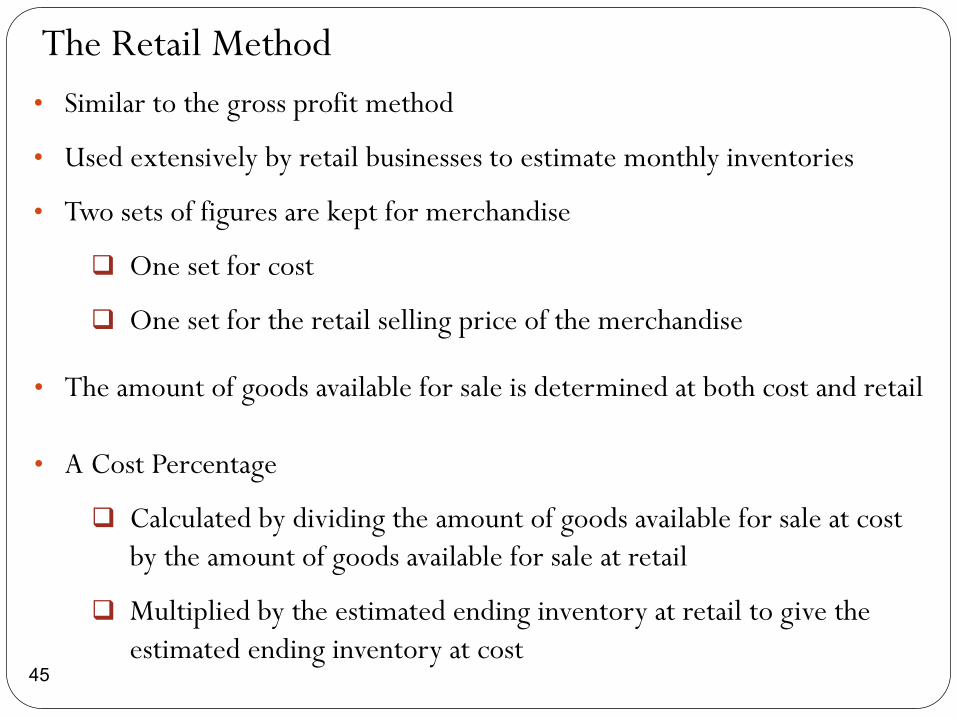

The Retail Method

• Similar to the gross profit method

• Used extensively by retail businesses to estimate monthly inventories

• Two sets of figures are kept for merchandise

One set for cost

One set for the retail selling price of the merchandise

45

• The amount of goods available for sale is determined at both cost and retail

• A Cost Percentage

Calculated by dividing the amount of goods available for sale at cost

by the amount of goods available for sale at retail

Multiplied by the estimated ending inventory at retail to give the

estimated ending inventory at cost

46

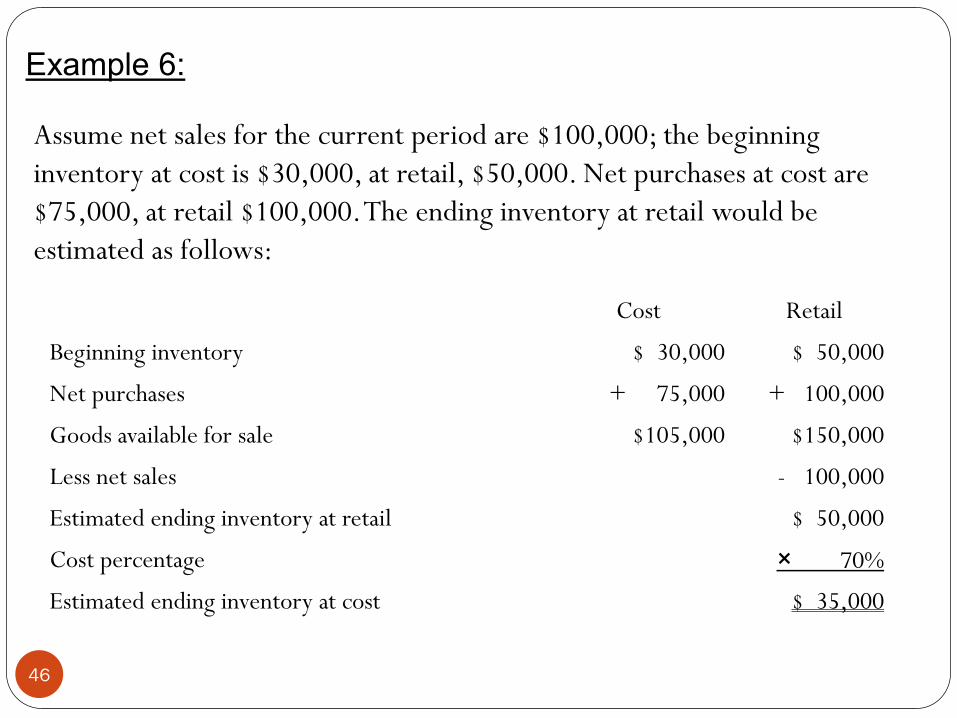

Assume net sales for the current period are $100,000; the beginning

inventory at cost is $30,000, at retail, $50,000. Net purchases at cost are

$75,000, at retail $100,000. The ending inventory at retail would be

estimated as follows:

Example 6:

Cost Retail

Beginning inventory $ 30,000 $ 50,000

Net purchases + 75,000 + 100,000

Goods available for sale $105,000 $150,000

Less net sales - 100,000

Estimated ending inventory at retail $ 50,000

Cost percentage × 70%

Estimated ending inventory at cost $ 35,000

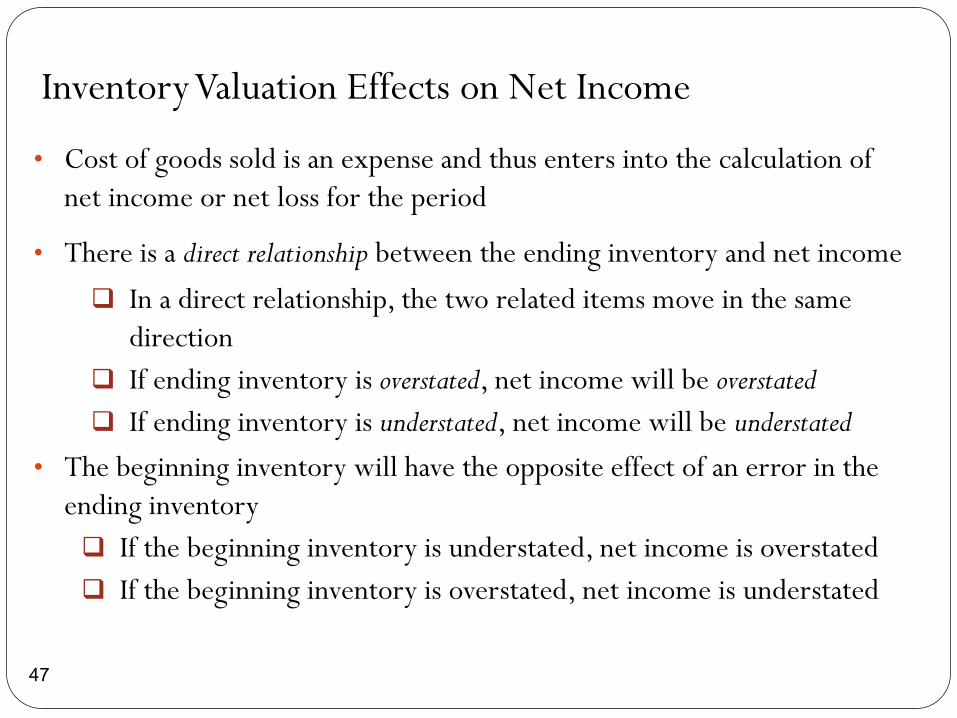

• Cost of goods sold is an expense and thus enters into the calculation of

net income or net loss for the period

• There is a direct relationship between the ending inventory and net income

In a direct relationship, the two related items move in the same

direction

If ending inventory is overstated, net income will be overstated

If ending inventory is understated, net income will be understated

• The beginning inventory will have the opposite effect of an error in the

ending inventory

If the beginning inventory is understated, net income is overstated

If the beginning inventory is overstated, net income is understated

47

Inventory Valuation Effects on Net Income

48

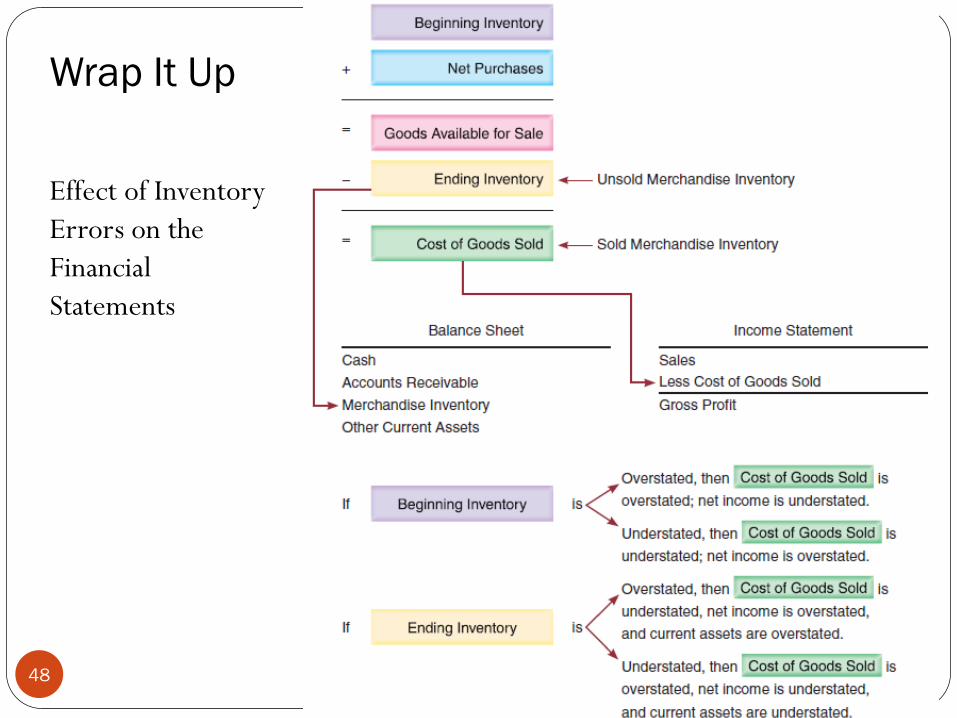

Effect of Inventory

Errors on the

Financial

Statements

Wrap It Up

Recommended