CD Equisearch Pvt Ltd Nov 15, 2017

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

S

Aarti Industries Ltd

No. of shares (m) 82.12

Mkt cap (Rs crs/$m) 7319/1117.0

Current price (Rs/$) 891/13.6

Price target (Rs/$) 1034/15.8

52 W H/L (Rs.) 1040/653

Book Value (Rs/$) 175/2.7

Beta 0.7

Daily volume NSE (avg. monthly) 31630

P/BV (FY18e/19e) 4.6/3.9

EV/EBITDA (FY18e/19e) 12.5/10.9

P/E (FY18e/19e) 22.2/19.0

EPS growth (FY17/18e/19e) 24.7/4.6/17.0

OPM (FY17/18e/19e) 22.0/20.6/20.3

ROE (FY17/18e/19e) 25.3/22.4/22.1

ROCE(FY17/18e/19e) 15.4/13.8/13.9

D/E ratio (FY17/18e/19e) 1.1/1.1/1.0

BSE Code 524208

NSE Code AARTIIND

Bloomberg ARTO IN

Reuters ARTI.BO

Shareholding pattern %

Promoters 53.7

MFs / Banks / FIs 12.7

Foreign Portfolio Investors 4.0 .3 Govt. Holding 0.0

Public & Others 29.7

Total 100.0

As on Sep 30, 2017

Recommendation

ACCUMULATE

Analyst

KISHAN GUPTA, CFA, FRM

Phone: + 91 (33) 4488 0043

E- mail: [email protected]

Consolidated (Rs crs)

FY16

FY17 FY18e FY19e

Income from operations (gross) 3006.59 3163.46 3722.39 4333.40

Other Income 5.94 1.96 1.50 1.75

EBITDA (other income included) 578.20 655.46 710.74 812.44

Profit after MI 256.43 315.14 329.59 385.78

EPS(Rs) 30.78 38.38 40.13 46.98

EPS growth (%) 36.0 24.7 4.6 17.0

Company Brief

AIL is one of India's leading manufacturers of chemicals and pharmaceutical

intermediates: dyestuff; pigment; agro chemicals; speciality chemicals; active

pharmaceutical ingredient (API); intermediates of API

Quarterly Highlights

� Underpinned by higher capacity utilization, launch of some intermediates

and increased supplies from the caffeine plant, Aarti's pharmaceuticals

business in Q2 reported the highest revenue growth in at least six

quarters. Thanks to increased benefits of operating leverage, EBIT

margins soared to the highest level in at least ten quarters - 13.9% Vs

11.9% in Q2FY17 Vs 12..8% in Q1FY18. Despite miraculous jump in home

& personal care chemicals business in H1 (+51.3%). losses barely trimmed.

� After restart of acid plant post maintenance shutdown and draw down of

accumulated inventories, its speciality chemicals reported 10.3%

sequential growth in revenues (20.8% y-o-y). Increase in prices of finished

products explains most of the 13.2% growth in sales in H1 for the volumes

grew by an abysmal 3-4%, partly evidenced by 7.4% growth in NCB

production. Overall operating profits slid 2.3% in H1 and post tax

earnings declined by 10.7%.

� Given large long foreign currency exposure arising out of exports, rupee

appreciation continues to post no measly challenges. After spending Rs

245 crs as capex in H1, it is on course to meet its annual target of Rs 450-

500 crs ($68.7-76.3m). Most of its ongoing expansion projects including the

acid concentration plant in Vapi and API and pharmaceutical intermediate

de-bottlenecking and expansions at Vapi and Tarapur would get over by

FY19.

� The stock currently trades at 22.2x FY18e EPS of Rs 40.13 and 19x FY19e

EPS of Rs 46.98. Beneficial client engagement - larger revenue share from

older clients - and backward integration for intermediates does instill

wider economic moat and so does enriching global market share (25-40%

across products) in benzene products. Despite massive ongoing capex, its

return on capital has shown only faint signs of degradation in last few

years. Rebound in its speciality chemicals dispatches partly instigated by

resurrection in agrochemical industry and ramp up of nitro toluene

capacity next fiscal would help earnings surge by some 17%. On balance

we maintain "accumulate" rating on the stock with revised target of Rs

1034 (previous target: Rs 900) based on 22x FY19e earnings.

2

2

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

[

Outlook & Recommendation

Global specialty chemicals update

According to MarketsandMarkets, a global market research and consulting firm, the global specialty chemicals market is

expected to grow at a CAGR of 5.42% between 2015 and 2020 to reach $470bn. The report states that 'speciality coatings and

surfactants' has been the largest functions for the speciality chemicals market (27.2% market share in 2014) with increasing

demand for speciality chemicals such as construction chemicals, pesticides, oilfield chemicals, mining chemicals from Asia -

Pacific region and sturdy growth in end-user industries such as construction, automotive, and electronics. The firm expects

growth to surge partly driven by turnaround in these key markets and also higher need for speciality chemicals for these

functions. But the construction sector is expected to rule the roost for the construction chemicals are estimated to witness the

highest growth (8.63% CAGR) from 2015 to 2020, mainly on account of growing construction sector in major emerging

economies like India, China, Brazil and South Korea.

IHS Markit reckons that the center of gravity of the global chemical industry is shifting towards the Middle East - due to

availability of cheap petrochemical feedstocks - and Asia - high economic growth and cheap labour buttressing the shift - due

to tearing down of trade barriers, spread of process technology, rising standards of living in many developing countries and

fast growth in many industrialized Asian economies. As a result, North American, European and Japanese speciality chemical

manufacturers have either set up facilities in Asia or elsewhere or increased outsourcing from Chinese and Indian

manufacturers. Low per capita consumption of speciality chemicals in these fledgling regions - compared to that of the

advanced regions - presents irresistible market potential.

IHS Market posits that global volume consumption would grow by 3-3.5% annually during 2016 and 2021 with consumption in

North America, Western Europe and Japan combined to grow by about 2% annually, while emerging markets would grow at a

brisker pace. Despite economic setbacks, China would lead the pack with 6-7% annual growth during the forecast period.

Driven by Make In India initiative of the Government of India, Chemtech Foundation expects India to garner 6% of global

speciality chemicals markets by 2020 from 3% now. Indian Speciality Chemical Manufacturers' Association (ISCMA) expects

the Indian speciality chemicals industry in the range of $80-100bn by 2023, implying 6-7% annual growth for tightening

environmental norms (eg. REACH regulations) in developed countries and slowdown in China have opened up new vistas for

exports. Globally, India is emerging a strong market for agrochemicals, dyes and pigments and flavors and fragrances.

Source: IBEF

Though Research and Markets expects global speciality chemicals industry to grow by 6.3% CAGR from 2015 to 2022, volatile

material prices and environmental regulations regarding the usage of specialty chemicals have dragged market growth. It

reckons that growing concerns regarding environment due to production, usage and wastage of these chemicals is expected to

impact demand, most pertinently in food processing and manufacturing industry where governments continue to regulate

usage of these chemicals. Yet diminishing arable land, rising population and growing need for higher crop yields hold

potential for demand of pesticides.

3

3

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Capex

After being delayed by few months, Aarti's Greenfield nitro-toluene facility in Jhagadia finally commissioned in Q2, enabling

it to cross sell toulene derivatives to its existing customers in agrochemicals, optical brighteners, pigments and

pharmaceuticals. To prop up its asset accumulation binge (Rs 450-500 crs expected annually), it amassed land parcels for Rs

60 crs last fiscal. To expand its chloro benzene range of chemicals and introduce a new range of chlorinated compounds, its

chlorination capacity is being ramped up by 65ktpa this year. To further its quest for technological excellence, Aarti

announced plans to open up a R&D center, a scale up facility consisting of a kilo-lab, an innovation center and labs for process

safety, effluent treatment etc in Jhagadia . This Rs 75 crs ($11.4m) facility would enable development of value added products

in end user applications in agrochemicals, fuel additives, pharmaceuticals, polymers and rubber chemicals.

Despite gargantuan capital investments in last few years, shortening payback periods for some projects such as second phase

of PDA expansion (450 tpm to 1000 tpm ) and new ethylation unit in Dahej would not be in formidable as most of these newly

commissioned projects would take 2-3 years to reach 80-90% utilization. Its Dahej unit operated at sub10% utilization last

fiscal for the unit's production was aimed at getting qualifications. Beset by sluggishness in oil& gas sector, its calcium

chloride facilities (one commissioned in Jhagadia in Q1FY17) also ran in rough seas, which prompted it to explore other

overseas markets. Overall PDA capacities are also expected to run at no more than 50% in the current fiscal.

Financials & Valuation

Both local and overseas considerations dominate Aarti's mega expansion plans - be it commissioning of calcium chloride

facility and ethylation unit last fiscal to commencement of nitro toluene plant in September to expanding chlorination

capacity to commissioning acid concentration plant in Vapi. Burgeoning middle class population and low per capita

consumption of chemicals (one-tenth of world average) would invigorate Indian speciality chemical industry - some industry

reports expect industry to touch $70 bn by FY20 from $40bn in FY14, implying annual growth of 9.8%. Stricter environmental

regulations in West and China coupled with increased outsourcing from China and India of intermediates and high-end

performance products support the buoyancy in demand.

Indian pharmaceutical manufacturers also stand to benefit from tighter pollution norms compliance and stricter regulatory

processes for pharmaceutical intermediates in China. Off-patented generics markets in advanced countries have become a

lucrative market due to thin competition. Apart from expanding in to chlorobenzene and foraying in other chemistries, plans

abound to foray in oncology drugs.

4

4

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Yet risks in terms of stricter regulations interrupting operations or rupee appreciation impacting revenue recognition

/margins is not worthy of abject neglect; Aarti felt Rs 8-10 crs currency loss in last two quarters because of rupee

strengthening. With implementation of Phase 3 of EU's REACH (Registration, Evaluation, Authorization and Restriction of

Chemicals) from June 2018, chemical supplies to EU would entice greater scrutiny, a no less arduous task for scantily

regulated Indian chemical companies. Though bagging mega supply orders - like the Rs 4000 crs ($610.5m) agrochemical

intermediary supply contract with a global agriculture company - does help prequalify for similar orders in future, it does not

guarantee a propitious deal for stakeholders not least due to long gestation period of such deals and significant inbuilt

uncertainty in supply schedules.

The stock currently trades at 22.2x FY18e EPS of Rs 40.13 and 19x FY19e EPS of Rs 46.98. Aarti's margin faces risk of reeling

under the twin effects of rising crude oil prices (margins capped in absolute terms) and strengthening of Indian rupee. It

wobbly Home & Personal Care Chemicals have barely revived - continues to bleed - despite posting over 50% growth in

revenues in H1. Still rebound in its speciality chemicals dispatches partly instigated by resurrection in agrochemical industry

and ramp up of nitro toluene capacity next fiscal would help earnings surge by some 17%. Strong operating cash flows would

doubtlessly contain built up ever pinching financial leverage. On balance we maintain "accumulate" rating on the stock with

revised target of Rs 1034 (previous target: Rs 900) based on 22x FY19e earnings. For more info refer to our March report.

5

5

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Cross Sectional Analysis

Company

Equity (Rs crs)

CMP (Rs crs)

Mcap (Rs crs)

Inc. from ops.

(Rs crs)

Profit (Rs crs)

OPM (%)

NPM (%)

Int. coverage

ROE (%)

Mcap / IO P/BV P/E

Aarti Inds. 41 891 7318 3210 289 18.7 9.0 3.9 21.5 2.3 5.1 25.3

Atul Ltd 30 2446 7256 2798 224 14.6 8.0 24.7 12.1 2.6 3.7 32.3

Deepak Nitrite 26 215 2806 1290 69 13.6 5.4 3.4 11.0 2.2 3.7 37.0

Sudarshan Chem 14 370 2561 1292 77 12.8 6.0 5.1 19.0 2.0 5.9 33.2

calculations on ttm basis; Aarti income from operations approximated Companies not truly comparable due to product dissimilarity

Partly distressed by GST enforcement, Sudarshan Chemical revenues flat lined in first half of current fiscal with revenues of its

flagship pigments business rose by 4.4% while that of agro chemicals plunged by 25.4%; though not exactly comparable due to sales

reporting in Q2 net of GST. Pigments EBIT margins recovered somewhat in Q2 - 16.1% Vs 14.6% in Q1- but was still down over 200

bps in H1. PBT as a result tumbled by 16.4% (yoy) in H1. To augment its global position in the pigments market, subsidiaries in

Mexico and China have been set up. Risks of mass scale dumping by China looms large as the Indian pigment industry struggles

due to surplus capacities in China. Also Sudarshan continues to face challenges in procuring key intermediates from China.

After a tormenting Q1, Atul's performance and other chemicals business did show stark improvement in revenues and margins -

EBIT margins rose to 12.7% in Q2 from 7.6% in Q1 (though not exactly comparable due to sales in Q2 reported net of GST) but not

by enough to preclude nearly one-third fall in segment EBIT. Perceptible stress in both life science chemicals and performance and

other chemicals explains 35.8% drop in post tax earnings in H1. In its bulk chemicals business, plans are afoot to boost capacity

utilization of its new caustic chlorine plant - subject to external demand - and launch chlorine derivative products. Sensing

increased demand for its polymers, higher capacities are planned for specialty resins, sulphone intermediates and other

upstream/downstream products. For aromatics, building capacities for fragrance intermediate and downstream and launching new

products from its newly established kilo lab facility are also on the anvil.

Greater traction in Deepak Nitrite's performance products business last quarter - revenues up 23% (yoy) helped this business to turn

in to black; though not exactly comparable due to sales report net of GST in Q2. Buttressed by higher crude oil prices, its basic

chemicals business continued its good run for it has posted 30.2% growth in its EBIT in H1(23.6% in Q2) . To quicken

commissioning of its all engrossing phenol & acetone project by fourth quarter of current fiscal, Deepk Phenolics (DPL), wholly

owned subsidiary of Deepak Nitrite, is pulling out all stops to recruit commissioning and operational teams to speedup seed

marketing initiatives to finalize construction work. As per last reporting, the company has already invested Rs 865 crs and more

than Rs 1075 crs have been committed for project implementation.

6

6

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Financials

Quarterly Results -Standalone Figures in Rs crs

Q2FY18 Q2FY17 % chg. H1FY18 H1FY17 % chg.

Income from operations (Gross) 887.89 710.25 25.0 1679.70 1445.65 16.2

Other Income 0.11 0.18 -38.9 0.20 0.54 -63.0

Total Income (gross) 888.00 710.43 25.0 1679.90 1446.19 16.2

Total Expenditure 727.61 559.31 30.1 1381.03 1140.07 21.1

EBIDTA (other income included) 160.39 151.12 6.1 298.87 306.12 -2.4

Interest 31.38 28.98 8.3 60.62 55.96 8.3

Depreciation 33.00 27.64 19.4 64.69 54.44 18.8

PBT 96.01 94.50 1.6 173.56 195.72 -11.3

Tax 17.50 18.50 -5.4 32.00 37.21 -14.0

PAT 78.51 76.00 3.3 141.56 158.51 -10.7

Extraordinary Item - - - - - -

Adjusted Net Profit 78.51 76.00 3.3 141.56 158.51 -10.7 EPS (F.V. 5) 9.56 9.12 4.8 17.24 19.02 -9.4

Segment Results Figures in Rs crs

Q2FY18 Q2FY17 % chg. H1FY18 H1FY17 % chg.

Segment Revenue (Gross)

Speciality Chemicals 690.98 572.13 20.8 1317.16 1163.35 13.2

Pharmaceuticals 136.86 101.45 34.9 242.93 203.24 19.5

Home & Personal Care Chemicals 60.05 36.67 63.8 119.61 79.06 51.3

Total 887.89 710.25 25.0 1679.70 1445.65 16.2

Segment EBIT

Speciality Chemicals 128.64 129.23 -0.5 241.57 262.25 -7.9

Pharmaceuticals 19.04 12.07 57.7 32.65 23.82 37.1

Home & Personal Care Chemicals -0.76 -1.02 -25.5 -0.18 -0.90 -80.0

Total 146.92 140.28 4.7 274.04 285.17 -3.9

Interest 31.38 28.98 8.3 60.62 55.96 8.3

Other Unallocable Exp. (net of income) 19.53 16.80 16.3 39.86 33.49 19.0

PBT 96.01 94.50 1.6 173.56 195.72 -11.3

7

7

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Financials

Income Statement - Consolidated Figures in Rs crs

FY16 FY17 FY18e FY19e

Income from operations (Gross) 3006.59 3163.46 3722.39 4333.40

Growth (%) -3.7 5.2 17.7 16.4

Other Income 5.94 1.96 1.50 1.75

Total Income (gross) 3012.53 3165.42 3723.89 4335.15

Total Expenditure 2434.33 2509.96 3013.15 3522.71

EBITDA (other income included) 578.20 655.46 710.74 812.44

Interest 116.98 117.34 133.23 147.98

EBDT 461.22 538.12 577.51 664.46

Depreciation 98.50 122.52 147.44 169.60

Tax 94.63 88.06 88.16 96.00

Net profit 268.09 327.54 341.90 398.85

Minority interest 11.22 11.76 12.32 13.08

Net profit after MI 256.87 315.78 329.59 385.78

Extraordinary item 0.44 0.64 - -

Adjusted Net Profit 256.43 315.14 329.59 385.78

EPS (Rs.) 30.78 38.38 40.13 46.98

Segment Results Figures in Rs crs

FY16 FY17 FY18e FY19e

Segment Revenue

Speciality Chemicals 2430.36 2569.29 2975.77 3449.22

Pharmaceuticals 425.76 426.07 511.28 613.54

Home & Personal Care Chemicals 150.47 168.10 235.34 270.64

Total (gross) 3006.59 3163.46 3722.39 4333.40 Segment EBIT

Speciality Chemicals 503.64 565.75 589.88 668.82

Pharmaceuticals 38.80 48.13 68.88 88.96

Home & Personal Care Chemicals -0.24 0.77 -1.00 1.00

Sub Total 542.20 614.65 657.76 758.78

Interest 116.98 117.34 133.23 147.98

Other Unallocable Exp. (net of income) 62.50 81.72 94.45 115.95

PBT 362.72 415.59 430.07 494.86

8

8

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Consolidated Balance Sheet Figures in Rs crs

FY16 FY17 FY18e FY19e

SOURCES OF FUNDS

Share Capital 41.66 41.06 41.06 41.06

Reserves 1095.64 1321.41 1614.42 1911.24

Total Shareholders Funds 1137.30 1362.47 1655.48 1952.30

Minority Interest 52.09 63.85 76.16 89.24

Long term debt 526.76 596.44 758.73 728.58

Total Liabilities 1716.15 2022.76 2490.37 2770.12

APPLICATION OF FUNDS

Gross Block 2081.44 2654.61 3149.61 3589.61

Less: Accumulated Depreciation 835.48 957.59 1105.03 1274.64

Net Block 1245.96 1697.02 2044.58 2314.97

Capital Work in Progress 313.01 269.52 225.48 214.52

Investments 41.26 46.96 44.98 44.98

Current Assets, Loans & Advances

Inventory 495.19 571.41 605.69 696.55

Sundry Debtors 523.40 524.67 592.88 640.31

Cash and Bank 28.99 28.50 33.55 31.37

Other Assets 186.41 192.61 217.77 248.32

Total CA & LA 1233.99 1317.19 1449.90 1616.54

Current liabilities 1102.59 1292.57 1262.04 1410.57

Provisions 20.50 27.83 32.57 38.23

Total Current Liabilities 1123.09 1320.40 1294.60 1448.79

Net Current Assets 110.91 -3.21 155.29 167.75

Net Deferred Tax (net of liability) -127.06 -155.44 -179.16 -204.46

Other Assets (Net of liabilities) 132.08 167.91 199.21 232.36

Total Assets 1716.15 2022.76 2490.37 2770.12

9

9

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Cash Flow Statement Figures in Rs crs

FY17 FY18e FY19e

Net Income (a) 327.54 341.90 398.85

Non cash exp. & others (b) 149.85 170.91 194.65

Depreciation 122.52 147.44 169.60

Profit / loss on sale of assets / inv -0.80 0.00 0.00

Dividend income 0.00 0.00 0.00

Lease income -0.25 -0.25 -0.25

Deferred tax & others 28.38 23.72 25.30

(Increase) / decrease in NWC (c) -123.43 -300.04 -200.24

Inventory -76.22 -34.28 -90.85

Other assets (net of liabilities) -47.21 -265.76 -109.39

Operating cash flow (a+b+c) 353.96 212.77 393.27

Capex -530.22 -450.96 -429.04

Investments 0.60 0.00 0.00

Dividend income 0.00 0.00 0.00

Lease income 0.25 0.25 0.25

Investing cash flow (d) -529.04 -450.71 -428.79

Net borrowings 272.24 277.59 122.29

Dividends & others -1.64 -34.59 -88.96

Equity issuances -96.00 0.00 0.00

Financing cash flow (e) 174.60 243.00 33.33

Net change (a+b+c+d+e) -0.48 5.06 -2.19

10

10

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

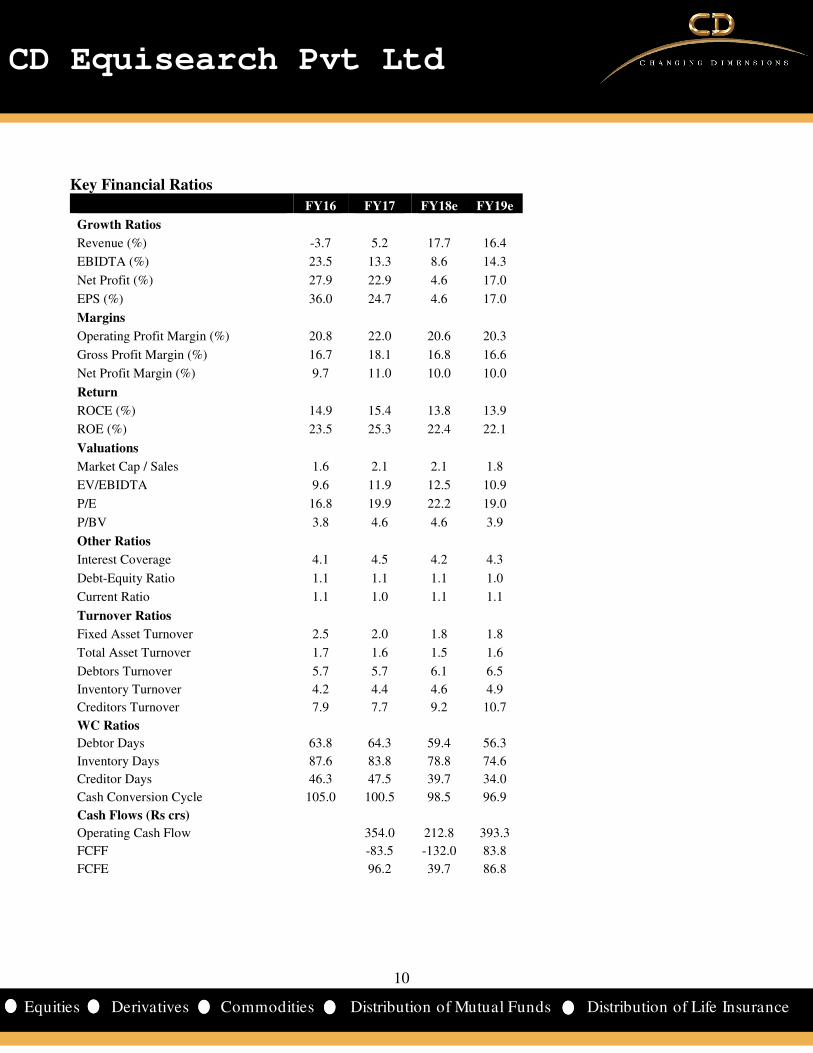

Key Financial Ratios

FY16 FY17 FY18e FY19e

Growth Ratios

Revenue (%) -3.7 5.2 17.7 16.4

EBIDTA (%) 23.5 13.3 8.6 14.3

Net Profit (%) 27.9 22.9 4.6 17.0

EPS (%) 36.0 24.7 4.6 17.0

Margins

Operating Profit Margin (%) 20.8 22.0 20.6 20.3

Gross Profit Margin (%) 16.7 18.1 16.8 16.6

Net Profit Margin (%) 9.7 11.0 10.0 10.0

Return

ROCE (%) 14.9 15.4 13.8 13.9

ROE (%) 23.5 25.3 22.4 22.1

Valuations

Market Cap / Sales 1.6 2.1 2.1 1.8

EV/EBIDTA 9.6 11.9 12.5 10.9

P/E 16.8 19.9 22.2 19.0

P/BV 3.8 4.6 4.6 3.9

Other Ratios

Interest Coverage 4.1 4.5 4.2 4.3

Debt-Equity Ratio 1.1 1.1 1.1 1.0

Current Ratio 1.1 1.0 1.1 1.1

Turnover Ratios

Fixed Asset Turnover 2.5 2.0 1.8 1.8

Total Asset Turnover 1.7 1.6 1.5 1.6

Debtors Turnover 5.7 5.7 6.1 6.5

Inventory Turnover 4.2 4.4 4.6 4.9

Creditors Turnover 7.9 7.7 9.2 10.7

WC Ratios

Debtor Days 63.8 64.3 59.4 56.3

Inventory Days 87.6 83.8 78.8 74.6

Creditor Days 46.3 47.5 39.7 34.0

Cash Conversion Cycle 105.0 100.5 98.5 96.9

Cash Flows (Rs crs)

Operating Cash Flow 354.0 212.8 393.3

FCFF -83.5 -132.0 83.8

FCFE 96.2 39.7 86.8

11

11

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Cumulative Financial Data Figures in Rs crs FY08-10 FY11-13 FY14-16 FY17-19e

Income from operations (net) 3640 5223 8295 10409

Operating profit 573 808 1440 2173

EBIT 462 627 1179 1738

PBT 282 403 807 1340

Profit after MI & associate profit 195 315 612 1031 OPM (%) 15.7 15.5 17.4 20.9

NPM (%) 5.4 5.5 7.2 10.3

Interest coverage 2.6 2.8 3.2 4.4

ROE (%) 17.6 17.1 21.5 22.7

ROCE (%) 14.1 12.6 14.7 14.4

Debt-equity ratio* 0.9 1.1 1.1 1.0

Fixed asset turnover 3.4 3.2 2.9 1.9

Debtors turnover 6.2 5.1 5.8 6.0

Inventory turnover 4.9 4.0 4.8 4.6

Creditors turnover 8.8 8.1 8.6 9.1

Debtors days 59.3 71.9 62.9 61.2

Inventory days 73.9 90.2 76.5 79.2

Creditor days 41.6 45.3 42.5 40.2

Cash conversion cycle 91.6 116.7 96.8 100.2

FY08-10 implies three years ending fiscal 10; *as on terminal year

Despite nerve-wracking fall in crude oil prices, Aarti managed to report nearly 60% growth in income from operations in FY14-

16 period (43% in previous three year period). Thanks to its pricing formula for speciality chemicals - which caps absolute

margins per tonne of chemicals sold - OPMs expanded strikingly during this period (see table). Yet growing stress from

slowdown in off take of speciality chemicals - volume growth at 8% last fiscal plunged to the lowest level in at least three years;

further down 3-4% in H1- portend near term strain in its speciality chemicals earnings - estimated to rise by a meager 4.3% in the

current fiscal. Its NCB production as a result is also expected to grow at the weakest pace in FY17-19 period when compared to

that in FY11-13 and FY14-16 periods.

Yet stabilization of newly commissioned nitro-toluene capacity and newly found vigor in its pharmaceutical business (due to

higher capacity utilization and launch of new intermediates) would prop up earnings next fiscal - cumulative post tax earnings

in FY17-19 period would surge by 68% (see table). Sub-optimal utilization of ethylene plant at Dahej and nitro toluene plant

coupled with prodigious capital asset addition plans (Rs 450-500 crs /$68.7-76.3m annually) would further stymie asset turnover

ratios; would marginally suppress return on capital due to vigorous ramp up in utilization of newly commissioned projects.

Cash conversion cycle though would more or less flat line in the ensuing period.

.

12

12

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Financial Summary – US dollar denominated

million $ FY16 FY17 FY18e FY19e

Equity capital 6.3 6.3 6.3 6.3

Shareholders funds 171.5 208.6 243.6 288.2

Total debt 194.7 241.2 281.1 299.7

Net fixed assets (incl CWIP) 235.0 303.3 346.5 386.1

Investments 6.2 7.2 6.9 6.9

Net current assets 16.7 -2.0 14.7 15.8

Total assets 258.7 310.4 371.1 413.0

Revenues (Gross) 459.3 471.5 568.2 661.4

EBITDA 88.2 97.6 108.5 124.0

EBDT 70.4 80.1 88.1 101.4

PBT 55.3 61.8 65.6 75.5

Profit after MI 39.2 47.0 50.3 58.9

EPS($) 0.47 0.57 0.61 0.72

Book value ($) 2.06 2.54 2.97 3.51

Operating cash flow 54.6 32.5 60.0

Investing cash flow -81.6 -68.8 -65.4

Financing cash flow 26.9 37.1 5.1

income statement figures translated at average rates; balance sheet and cash flow at year end rates; projections at current rates(Rs 65.52/$). All dollar denominated figures are adjusted for extraordinary items.

13

13

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Disclosure& Disclaimer CD Equisearch Private Limited (hereinafter referred to as ‘CD Equi’) is a Member registered with National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited (Formerly known as MCX Stock Exchange Limited). CD Equi

is also registered as Depository Participant with CDSL and AMFI registered Mutual Fund Advisor. The associates of CD Equi are engaged in

activities relating to NBFC-ND - Financing and Investment, Commodity Broking, Real Estate, etc.

CD Equi is registered under SEBI (Research Analysts) Regulations, 2014 with SEBI Registration no INH300002274. Further, CD Equi hereby

declares that –

• No disciplinary action has been taken against CD Equi by any of the regulatory authorities.

• CD Equi/its associates/research analysts do not have any financial interest/beneficial interest of more than one percent/material conflict of

interest in the subject company(s) (kindly disclose if otherwise).

• CD Equi/its associates/research analysts have not received any compensation from the subject company(s) during the past twelve months.

• CD Equi/its research analysts has not served as an officer, director or employee of company covered by analysts and has not been engaged

in market making activity of the company covered by analysts.

This document is solely for the personal information of the recipient and must not be singularly used as the basis of any investment decision.

Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations

as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document

(including the merits and risks involved) and should consult their own advisors to determine the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading

volume, as opposed to focusing on a company's fundamentals and as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed

to be true but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general guidance

only. CD Equi or any of its affiliates/group companies shall not be in any way responsible for any loss or damage that may arise to any person from

any inadvertent error in the information contained in this report. CD Equi has not independently verified all the information contained within this

document. Accordingly, we cannot testify nor make any representation or warranty, express or implied, to the accuracy, contents or data contained

within this document.

While, CD Equi endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory compliance or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information and its contents, information or data may not be reproduced, redistributed or

passed on, directly or indirectly. Neither, CD Equi nor its directors, employees or affiliates shall be liable for any loss or damage that may arise

from or in connection with the use of this information.

CD Equisearch Private Limited (CIN: U67120WB1995PTC071521)

Registered Office: 37, Shakespeare Sarani, 3rd Floor, Kolkata – 700 017; Phone: +91(33) 4488 0000; Fax: +91(33) 2289 2557 Corporate Office: 10,

Vasawani Mansion, 5th Floor, Dinshaw Wachha Road, Churchgate, Mumbai – 400 020. Phone: +91(22) 2283 0652/0653; Fax: +91(22) 2283, 2276

Website: www.cdequi.com; Email: [email protected]

buy: >20% accumulate: >10% to ≤20% hold: ≥-10% to ≤10% reduce: ≥-20% to <-10% sell: <-20%

Exchange Rates Used- Indicative

Rs/$ FY14 FY15 FY16 FY17

Average 60.5 61.15 65.46 67.09

Year end 60.1 62.59 66.33 64.84

All $ values mentioned in the write-up translated at the average rate of the respective quarter/ year as applicable. Projections converted at current

exchange rate. Cumulative dollar figure is the sum of respective yearly dollar value.

Recommended