Cancer Molecular Diagnostics: On the Critical Path to

Personalized Medicine

Dr. Sudeep Basu, Senior Analyst

Drug Discovery & Clinical Diagnostics

July 24, 2008

2

Presentation Focus Points

� Industry Participants

� Hot Topics

� Market Challenges

� Growth Drivers and Restraints

� Market Coverage and Definitions

� Revenue Forecast

3

Market Coverage and Definitions

Forecast Period: 2008 – 2014

Base Year: 2007

Region: United States

U.S. Cancer Molecular Diagnostics Markets

• U.S. Breast Cancer Molecular Diagnostics Market

• U.S. Prostate Cancer Molecular Diagnostics Market

• U.S. Colorectal Cancer Molecular Diagnostics Market

• U.S. Other Cancers Molecular Diagnostics Market

• U.S. Cancer Companion Diagnostics Market

4

Industry Participants

5

Market Challenges, Growth Drivers and Restraints

2004 – 2007:

• Growth of Cancer Molecular Diagnostics

• New Entrants, M&A

• First Commercial Launch of FDA Approved IVDMIA: MammaPrint

2008 – 2014:

• What applications/new opportunities will drive the U.S. cancer molecular

diagnostics market?

• What is the main barrier to the U.S. cancer molecular diagnostics market?

• Will the U.S. cancer molecular diagnostics market continue to grow?

• How will the market play out in the future with regards to M&A ?

• What is the timeline for new market entrances?

• How will the regulatory environment affect the market?

6

Role of Venture Capital

• Venture Backed Start-Ups in Cancer Molecular Diagnostics

• Major Concerns of the VC Firms

• Listing of Key VC Firms Investing in Cancer Molecular Diagnostic

• Key Pointers for VC Funding for Cancer Molecular Diagnostics

• Price point considerations

• High cost low volumes vs. low cost high volume models

• FDA regulations

• Therapeutic implications in cancer molecular diagnostic

7

FDA Regulation in Cancer Molecular Diagnostics

2008 – 2014:

• FDA Draft Guidelines on IVDMIA

• CLIA vs. IVD Routes for Test Commercialization

• Case Study Based Discussion of the Models

• Effect of Regulation on M&A

• Strategic Recommendations

8

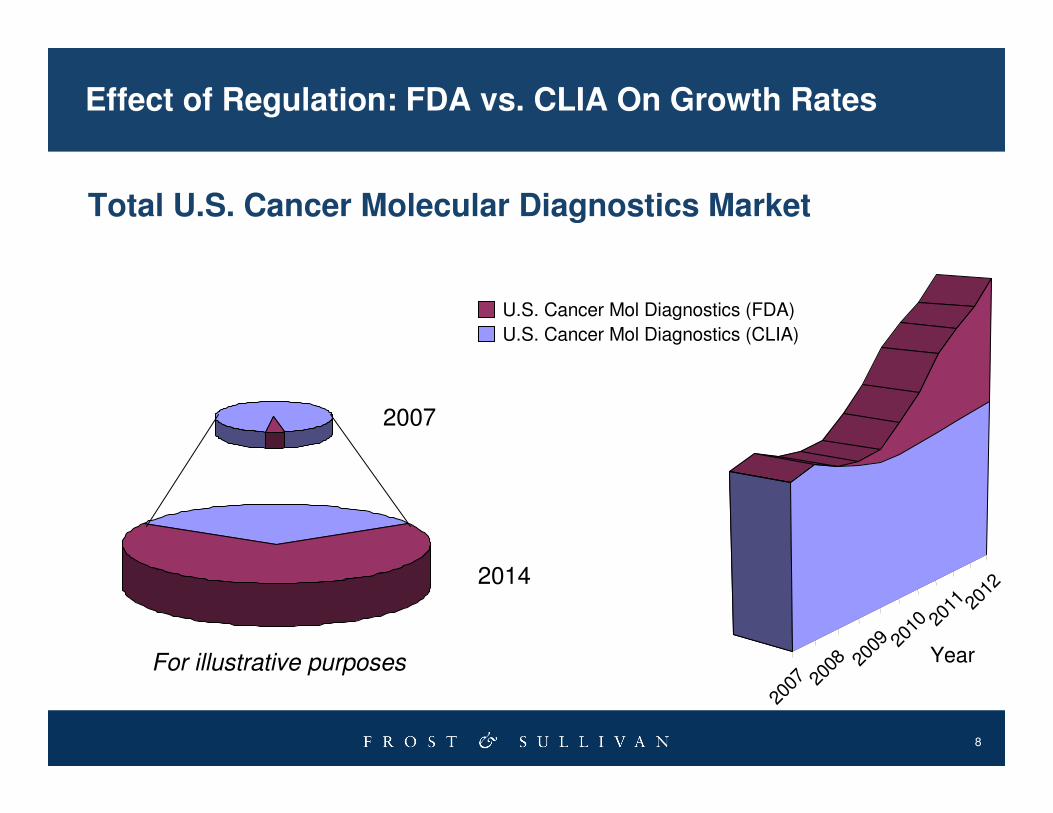

Effect of Regulation: FDA vs. CLIA On Growth Rates

U.S. Cancer Mol Diagnostics (FDA)

U.S. Cancer Mol Diagnostics (CLIA)

2007 20

08 2009 20

10 2011 20

12

Year

Total U.S. Cancer Molecular Diagnostics Market

For illustrative purposes

2007

2014

9

Biomarkers and Companion Diagnostics

BIOMARKER

DISCOVERY

FDA’s CONCEPT

PAPER

WILL THE FDA MOVE ON K- RAS ?

COMPANION--

DIAGNOSTICS

IS EUROPE (EMEA) AHEAD OF THE U.S. (FDA) ?

10

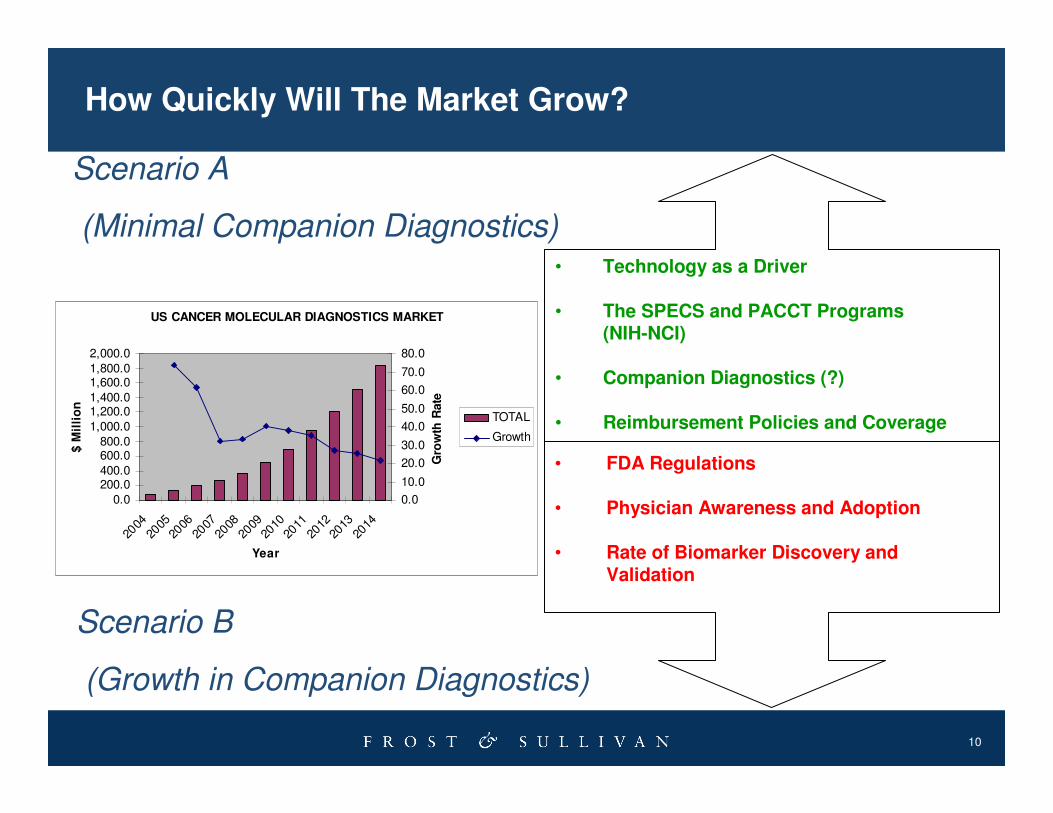

How Quickly Will The Market Grow?

• FDA Regulations

• Physician Awareness and Adoption

• Rate of Biomarker Discovery and Validation

• Technology as a Driver

• The SPECS and PACCT Programs(NIH-NCI)

• Companion Diagnostics (?)

• Reimbursement Policies and Coverage

Scenario A

(Minimal Companion Diagnostics)

Scenario B

(Growth in Companion Diagnostics)

US CANCER MOLECULAR DIAGNOSTICS MARKET

0.0

200.0400.0

600.0800.0

1,000.0

1,200.01,400.0

1,600.01,800.0

2,000.0

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Year

$ M

illi

on

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Gro

wth

Rate

TOTAL

Growth

11

How Will The M&A Landscape Change ?

• 2008 – 2014:

• Noteworthy Deals

• Who Are The Acquirers?

•

• Who Are The Target Companies?

• How Will Platform Technology Companies Enter The Space?

• Will Pharma Integrate Diagnostics?

• How Will Consolidation Effect The Market?

12

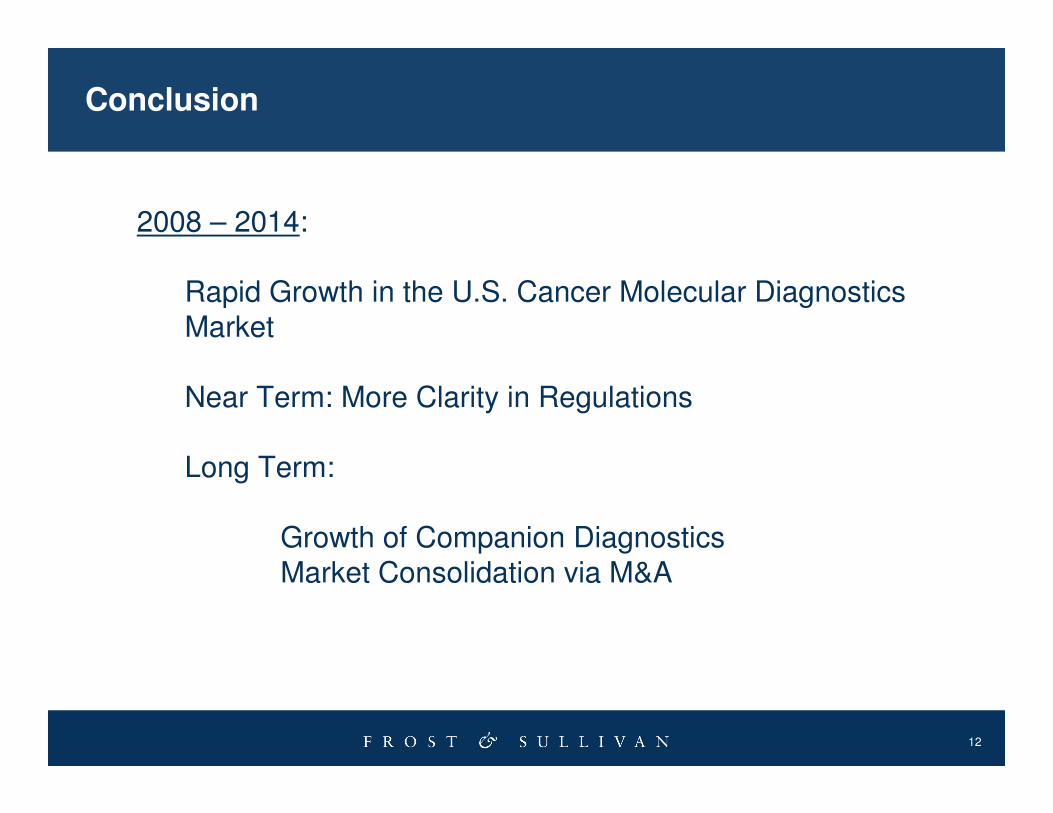

Conclusion

2008 – 2014:

Rapid Growth in the U.S. Cancer Molecular Diagnostics

Market

Near Term: More Clarity in Regulations

Long Term:

Growth of Companion Diagnostics

Market Consolidation via M&A

13

Personalized Medicine

Clinical Diagnostics and Drug Discovery Technologies:The Next Generation of Growth Opportunities

laboratoryautomation

multiplexassays

compoundscreening

innovativeresearch tools

workflowsystems

cancer

infectiousdisease

geneticdisorders

drugmetabolism

diseaseprognostics

expressionprofiling

genotyping

cytogenetics

epigenetics

sequencing

M O L E C U L A R D I A G N O S T I C S

P H A R M A C O G E N O M I C S

C O M P A N I O N D I A G N O S T I C S

P O I N T OF C A R E D I A G N O S T I C S

G E N O M I C S & P R O T E O M I C S

Personalized Medicine

Clinical Diagnostics and Drug Discovery Technologies:The Next Generation of Growth Opportunities

Personalized Medicine

Clinical Diagnostics and Drug Discovery Technologies:The Next Generation of Growth Opportunities

laboratoryautomation

multiplexassays

compoundscreening

innovativeresearch tools

workflowsystems

cancer

infectiousdisease

geneticdisorders

drugmetabolism

diseaseprognostics

expressionprofiling

genotyping

cytogenetics

epigenetics

sequencing

M O L E C U L A R D I A G N O S T I C S

P H A R M A C O G E N O M I C S

C O M P A N I O N D I A G N O S T I C S

P O I N T OF C A R E D I A G N O S T I C S

G E N O M I C S & P R O T E O M I C S

laboratoryautomation

multiplexassays

compoundscreening

innovativeresearch tools

workflowsystems

cancer

infectiousdisease

geneticdisorders

drugmetabolism

diseaseprognostics

expressionprofiling

genotyping

cytogenetics

epigenetics

sequencing

laboratoryautomation

multiplexassays

compoundscreening

innovativeresearch tools

workflowsystems

laboratoryautomation

multiplexassays

compoundscreening

innovativeresearch tools

workflowsystems

cancer

infectiousdisease

geneticdisorders

drugmetabolism

diseaseprognostics

cancer

infectiousdisease

geneticdisorders

drugmetabolism

diseaseprognostics

expressionprofiling

genotyping

cytogenetics

epigenetics

sequencing

expressionprofiling

genotyping

cytogenetics

epigenetics

sequencing

M O L E C U L A R D I A G N O S T I C S

P H A R M A C O G E N O M I C S

C O M P A N I O N D I A G N O S T I C S

P O I N T OF C A R E D I A G N O S T I C S

G E N O M I C S & P R O T E O M I C S

M O L E C U L A R D I A G N O S T I C S

P H A R M A C O G E N O M I C S

C O M P A N I O N D I A G N O S T I C S

P O I N T OF C A R E D I A G N O S T I C S

G E N O M I C S & P R O T E O M I C S

Industry Coverage

PREVIOUS NEXT

Strategic and

in-depth

analysis of the

personalized

medicine

microcosm

markets and a

holistic

perspective of

how they fit in

the overall

clinical

diagnostics and

drug discovery

technologies

markets.

14

Industry Expertise

PREVIOUS NEXT

StrategicExpert Analysis

ComprehensiveSupply-side Analysis

RobustEnd-user Analysis

Through Detailed Market Intelligence

and Inquiry Time with Analysts,

Our Team of Industry Experts Will Help You

•Identify High-Growth Segments in Molecular Diagnostics

•Establish Investment Criteria for Pharmacogenomics

•Predict IVDMIA Regulations’ Impact on New Diagnostic Tests

•Determine how the Drug—DiagnosticsCo-Development Model will Evolve

•Understand the Role of Reimbursementin Personalized Medicine

•Evaluate the Influence that Partnershipsand M&A Activity will have on the

Competitive Landscape

•Examine the ways Platform TechnologyProviders Position Themselves Relative to

Biomarker and Diagnostic Development

15

Total Rapid Microbiology Tests Market:

Percent of Revenues by Market Segment (U.S.), 2007

Manufacturing

Tests

18.8%

Rapid Clinical

Tests

Rapid

Bioterroism

Tests

15.2%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Re

ven

ue

s (

$ b

illio

ns

)

EsotericTesting

Rapid growth expected for esoteric testing. It is expected to reach $10.6 billion by 2014 from $5.1 billion in 2007 at a CAGR of 11.0%

2007

2014

Total Esoteric Testing Market:Revenue Forecasts (U.S.), 2007-2014

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Re

ven

ue

s (

$ b

illio

ns

)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Re

ven

ue

s (

$ b

illio

ns

)

EsotericTesting

Rapid growth expected for esoteric testing. It is expected to reach $10.6 billion by 2014 from $5.1 billion in 2007 at a CAGR of 11.0%

EsotericTesting

Rapid growth expected for esoteric testing. It is expected to reach $10.6 billion by 2014 from $5.1 billion in 2007 at a CAGR of 11.0%

2007

2014

2007

2014

Total Esoteric Testing Market:Revenue Forecasts (U.S.), 2007-2014

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Total qRT-PCR Markets:Revenue Forecasts (U.S.), 2002-2012

Year

Reven

ues

($ M

illio

n)

Gro

wth

Rate

(%)

Revenues

Growth

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Total qRT-PCR Markets:Revenue Forecasts (U.S.), 2002-2012

Year

Reven

ues

($ M

illio

n)

Gro

wth

Rate

(%)

Revenues

Growth

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Market Engineering Research

PREVIOUS NEXT

Measurement-based strategies developed

through our exclusive market engineering

methodology – presents an accurate picture of

the current and future marketplace, opportunities

for growth, challenges, and market drivers.

“We have relied on Frost & Sullivan’s strategic research studies for

reliable insights into several competitive markets. Their ability to identify

and analyze industry-specific trends gives their clients not only a clear

indication of where markets are going, but why they are going there.”

- Gen-Probe

• Cancer Molecular Diagnostics Markets

• Pharmacogenomics Markets

• Epigenetics and MicroRNA Markets

• Established Infectious Disease Molecular Diagnostics Markets

• Emerging Infectious Disease Molecular Diagnostics Markets

• Genetic Testing and Genomic Profiling Markets

• Rapid Microbiology Testing Markets

• Nucleic Acid Isolation and Purification Markets

16

Customer Research

PREVIOUS NEXT

Specialized Insight into:

• Researcher and Physician Utilization

• Laboratory and Hospital

Implementation

• Reimbursement Policies

• Regulations

• Healthcare Privacy Laws

17

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

18

For Additional Information

For Additional Information

Stephanie Ochoa

Corporate Communications

North American Analyst Briefing Coordinator

(210) 247-2421

Chris Olsen

Director of Business Development

Healthcare

(650) 475-4502

Mona Patel

Research Director

Healthcare & Life Sciences

(650) 475-4506

Recommended