BRINNER1

10.ppt

Business Investment

Lecture 10

BRINNER2

10.ppt

Business Investment

“Investment”: not “financial” in the everyday sense but purchases of plant & equipment, (or additions to inventories)

“I” is demand today, supply tomorrow; unique among GNP spending categories

The capacity created by I is flexible (through variation in shifts, maintenance schedules, etc) so purchase can be delayed in tough times

BRINNER3

10.ppt

Business Investment

-10%

-5%

0%

5%

10%

15%

20%

1983

1985

1987

1989

1991

1993

1995

1997

1999

Investment Growth Real GDP Growth

A key question for economists seeking to understand the business cycle was: “Why are the cycles in investment growth so much greater than those in output growth?”

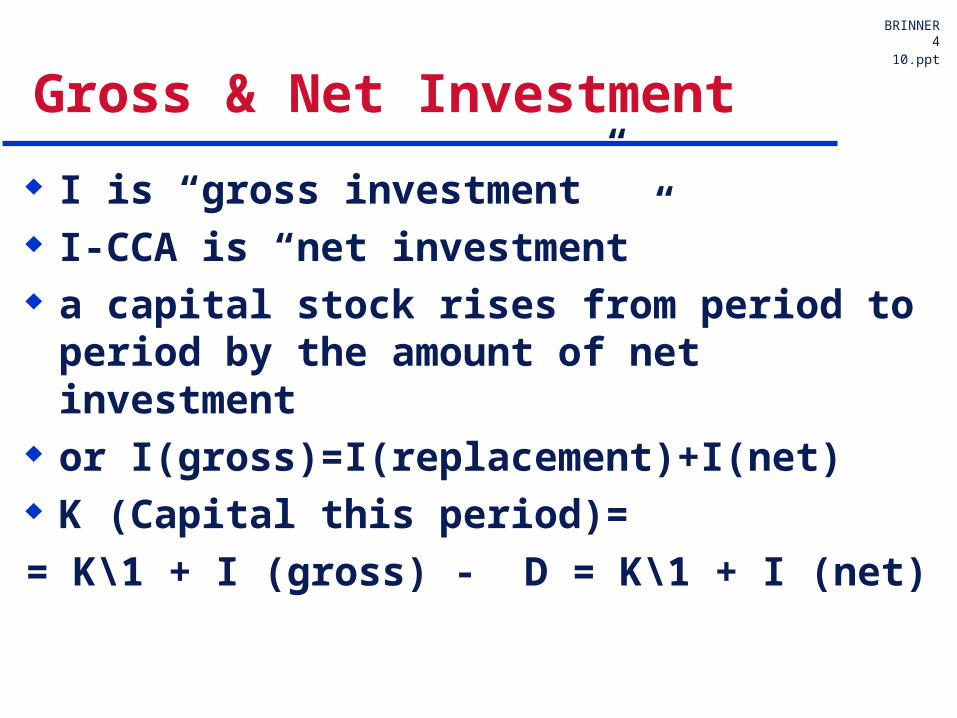

BRINNER4

10.ppt

Gross & Net Investment

I is “gross investment” I-CCA is “net investment” a capital stock rises from period to period by

the amount of net investment or I(gross)=I(replacement)+I(net) K (Capital this period)=

= K\1 + I (gross) - D = K\1 + I (net)

BRINNER5

10.ppt

The Optimal Level of Capital

Simple World: It takes· one $2500 machine· housed in a $2500 building· plus $3000 of labor · to make $5000 of output.· Machines last 10 years, buildings 25,

decaying linearly.· No substitution is possible.

BRINNER6

10.ppt

The Optimal Level of Capital

K / Y = ($2500+$2500) / $5000 = 1 Thus Optimal=Necessary K = 1 x Y If Y is constant at $5000, then so must be K K decays/depreciates each year by

· 10% x $2500 (equip)=$250· 4% x $2500 (building)=$100· thus I (replacement) must be $350 per year to

keep K stable at $5000, with $2500 of each type of K

BRINNER7

10.ppt

The Optimal Level of Capital

What if the producer wants to boost output (Y) by 3% to $5150?

K must rise to $5150, meaning I (net) must be $150 added to I(replacement) $350 implies I(gross) = $500

So investment in that year is 10% of output In fact, these are the numbers for the US

Machines & Factories Required to Produce Output

0

2000

4000

6000

8000

10000

12000

1959

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

$ B

illi

on

Real GDP Private Cap

Accelerator Data: Change in Output vs Levels of Gross & Net Investment

$(200)

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

1959

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

Change in Real GDP Gross Investment Net Investment

Recent shift to even higher investment relative to GDP is due to new technology opportunities

Note: Net Investmentroughly matches theUS change in GDP

BRINNER10

10.pptAccelerator Model Implications for the Business Cycle

Note how variations in Y get amplified in variations in I

A $150 change in Y required a $150 change in I Or, a 3% change in Y required a 40+% change

in I Realistically, the response to an output change

isn’t so sudden, and the base level of investment includes some net addition because output is trending up

BRINNER11

10.ppt

The Optimal Level of Capital I = I(gross)= I (replacement) + I(net)

• I (replacement)=dep. rate x K = c1 x K=c1 x Y• I (net) = c2 * [ Y - Y \1]

I = c1 * Y + c2 * [ Y - Y\1 ] Note that the level of investment is a function of the

change (the first derivative) in output; By extension, the growth of investment (the first

derivative) is a function of the acceleration (the second derivative) in output:

Hence the Accelerator Model of Investment

BRINNER12

10.ppt

The Optimal Level of Capital

In a more realistic model, production can temporarily rise without adding K by adding a shift or overtime or delaying maintenance, thus c1 is not rigidly fixed, and new capital- or labor saving technology can be introduced so c2 is also not rigidly fixed

The microeconomic basis of c2: the optimal capital-output ratio• relative prices and productivity for capital , output, and

labor determine this• the first basic extension is the Cobb-Douglas production

model

BRINNER13

10.ppt

The Optimal Level of Capital

Y= KbL(1-b)

dY/dK=marginal product of capital = bK(b-1)L(1-b)

» =b (1/K) KbL(b-1)

» =b (1/K) Y» =b Y/K = b * Average Product of Capital

marginal product of capital = b * average product of capital

BRINNER14

10.ppt

The Optimal Level of Capital

dY/dK=marginal product of capital = b * Y/K = b * Avg. Product of Capital The real price paid per unit of capital is Pk / Py In equilibrium, this price is its marginal product

• Thus Pk/Py = b * Y /K Solve for K to find the optimal K:

• K = b * Py/Pk * Y Or the optimal K/Y ratio = b* Py/Pk

• Just like the simple fixed coefficient model, except the ratio is now sensitive to the real price of capital

BRINNER15

10.ppt

The Optimal Level of Capital

The price paid per unit of capital is Pk / Py In equilibrium, this price is its marginal

product Pk/Py = b * Y /K What is b, that is how can it be interpreted

beyond “the exponent of capital”?

• b= (Pk * K) / (Py * Y)• = capital income / total income• hence the capital share of income

BRINNER16

10.ppt

The “Price or Cost” of Capital

The cost of funds (“r”)... ...minus price appreciation of the real

asset (“inflation”)... ...plus the cost of perfect maintenance =

the rate of depreciation (“d”)

So the cost, Pk/Py = r - inflation + d

BRINNER17

10.pptTransitions between Targeted Equilibrium Points

In practice, future K (K*) is targeted to hit the optimal level consistent with an expected future path of Y (Y*) given an expected cost of capital ( (Pk/Py)* )

K* = b Q* (Py/Pk)* Economists add lag structures to reflect

expectations

BRINNER18

10.ppt

Examples from a specific company The company manufactures equipment used to

facilitate construction:» Aerial work platforms (“AWP” in next slides for lifting people ; 2

types--”scissor lifts” and “boom lifts”» Material Handlers to lift bricks, wood, etc

The “output” driving the need for capital is thus construction spending

You will see that the cycle in this firm’s equipment sales are far greater than the cycle in construction

Construction is itself more volatile than GDP

BRINNER19

10.ppt

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1985

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

0

7,000

14,000

21,000

28,000

35,000

42,000

49,000

56,000

63,000

70,000

Total Booms Straight Booms Articulated Booms

Scissors Total Units

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

1985

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

Total Booms Straight Booms Articulated BoomsScissors Total Units

The cyclical volatility of scissors is similar to that of total booms, but slightly greater

Historical Patterns in Aerial Work Platform Demand Growth and Volatility of Industry Sales

• The boom and scissors markets are locked in tandem, with scissors remaining near 70%. (Total aerial work platform units are charted against the right scale, scissors and all others against the left scale)

• Articulated booms enjoy a persistent, stable market preference versus straight booms

AWP Unit Sales AWP Sales Growth

Yea

r O

ver

Yea

r G

row

th R

ate

Num

ber

of U

nits

by

Pro

duct

Lin

e

Total N

umber of U

nits

BRINNER20

10.ppt

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1985

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

-60%

-45%

-30%

-15%

0%

15%

30%

45%

60%

75%

Nonresidential ConstructionIndustrial Production (excluding computers)Gross Domestic ProductTotal Units

-60%

-40%

-20%

0%

20%

40%

60%

80%

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

Aerial Work PlatformsValue of Semiconductor ShipmentsSales of ElectronicsSales of Semiconductors - Worldwide

Perhaps the growth of this sector is best appreciated by comparing it to a widely-hailed, high-growth, and high-tech sector: semiconductors

Three alternate government indicators of semiconductor growth are charted above; none have grown as rapidly as aerial work platforms

Historical Patterns in Aerial Work Platform DemandGrowth Rates in Sales and Served Markets

• One of the primary served markets, nonresidential construction, is 3-4 times more volatile than the total US economy, as measured by either manufacturing production or GDP

• Offsetting this liability is the persistently stronger growth of the aerial work platform industry. Unit growth is charted against the right scale, 3 times the left scale used for the national indicators

Industry Growth RatesUnit Growth vs. National Indicators

Yea

r ov

er Y

ear

Gro

wth

Rat

eU

nit Grow

th Rate

Nat

iona

l Ind

icat

or G

row

th R

ate

BRINNER21

10.ppt

Historical Patterns in Aerial Work Platform DemandCyclical Forces Driving Sales around the Rising Penetration Trend

• Durable equipment sales are inherently the most cyclical markets in an economy• New equipment purchases serve two goals

» Replace worn-out or obsolete equipment to maintain existing total production capacity. In your markets, production capacity is required to match construction activity or manufacturing / commercial operations

Replacement demands are relatively steady, tending to approximate a percentage of the pre-existing fleet of equipment accumulated over a decade

However, even replacement budgets are cyclical, becoming more generous in prosperous markets and lean in soft markets

» Expand capacity to meet higher production levels These are highly cyclic sales, in that if construction is simply flat, no new equipment is

required for expansion In other words, the level of such sales tracks the growth in customer production

• Equipment sales lag served markets by approximately a year, reflecting two factors:» Businesses typically extrapolate from recent experience, expecting strong markets to continue

and weak to stay soft, rather than making independent forecasts» Capital budgets are created at the beginning of a year, then executed through the year

• This lag tends to produce cycles of excess or insufficient capacity, producing volatile orders to the equipment supplier

BRINNER22

10.ppt

A simple model of equipment sales in your industry, using construction as an example:The customer’s desired fleet is proportional to nonresidential construction: one AWP per $2million of construction

Fleet = 2000 x Construction

10% of the fleet must be replaced every year.Replacement Sales = 10% x Fleet (prior year)

thus = 10% x 2000 x Construction (prior year)

Additional Capacity-Expanding Sales match Changes in ConstructionExpansion Sales = 2000 x (Construction-Construction (prior year))

Total Sales = Replacement + Expansion Sales= 200 x Construction + 2000 x (Construction-Construction (prior year))

Historical Patterns in Aerial Work Platform Demand

Simplified Example to Highlight Source of VolatilityYear 1 2 3 4 5 6 7 8 9 10

Construction ($ Billion)$ Billion(Excluding Inflation) 100 105$ 110$ 121$ 133$ 133$ 127$ 127$ 133$ 140$ Growth Rate 5% 5% 5% 10% 10% 0% -5% 0% 5% 5%

Construction Equipment (units) Requirements

Existing Fleet2000 x

Construction 200,000 210,000 220,500 242,550 266,805 266,805 253,465 253,465 266,138 279,445 New Sales to meet 2 goals: Replacement 10% 19,048 20,000 21,000 22,050 24,255 26,681 26,681 25,346 25,346 26,614

Capacity Expansion

2000 x Construction

Increase 9,524 10,000 10,500 22,050 24,255 - (13,340) - 12,673 13,307 Total 28,571 30,000 31,500 44,100 48,510 26,681 13,340 25,346 38,020 39,921 Growth Rate 5% 5% 40% 10% -45% -50% 90% 50% 5%

Your actual industry cycles, although large, are muted by the year-to-year inertia in customer capital budgeting decisions and by he ongoing rising penetration of such equipment in construction and manufacturing.

As in this example, cycles in the fleet of units parallel cycles in the served construction market (as shown earlier).

Stable construction growthproduces matching equipment growth

Cycle in construction growthproduces amplified equipment cycle

BRINNER23

10.ppt

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

Historical

Fitted (without special 1999 allowance)

Unexplained Deviations

Historical Patterns in Aerial Work Platform Demand Cyclical Forces Driving Sales around the Rising Penetration Trend

Using your trade association data from 1985 through 1999, models reflecting this structure have been estimated for scissor and total boom sales

Additional factors are the trend gains in penetration in served markets and the potential sales gain in 1999 due to consolidation of the rental industry

With regard to lags in response, sales are driven by the level and change in construction spending in the current and prior two years

The estimates confirm a far greater sensitivity of lifts to manufacturing activity; boom sales are almost totally driven by nonresidential construction

% explained (R-squared) =98.3%Standard error = 847 Units

Potential Rental Consolidation Shift:1999 Actual - Estimate = 780 Units

% explained (R-squared) =97.4%Standard error = 2858 Units

Potential Rental Consolidation Shift:1999 Actual - Estimate = 3307 Units

Results in models without allowance for special 1999 gain

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

Hisorical

Fitted (without special 99 allowance)

Unexplained Deviations

Booms Scissors

Recommended

![Investment Ppt[1]](https://img.dokumen.tips/doc/110x75/5448b00db1af9f5e278b4587/investment-ppt1.jpg)