Basics

Inputs

$69.81 69

71.65% 7

Riskfree Rate- Annual (r) 4.95% 5

Exercise Price (X) $70.00 70

Time To Maturity - Years (T) 0.5777 6

Outputs

BLACK SCHOLES OPTION PRICING

Stock Price Now (S0)

Standard Dev - Annual (s)

d1

d2

N(d1)

N(d2)

Call Price (C0)

-d1

-d2

N(-d1)

N(-d2)

Put Price (P0)

1d Ts

20ln / / 2 /S X r T Ts s

0 0 1 2rTC S N d Xe N d

0 0 1 2rTP S N d Xe N d

Continuous Dividend

Inputs

Option Type FALSE

$69.81 69

71.65% 7

Riskfree Rate- Annual (r) 4.95% 5

Exercise Price (X) $70.00 70

Time To Maturity - Years (T) 0.5777 6

Dividend Yield (d) 1.00% 1

Outputs

BLACK SCHOLES OPTION PRICING

Stock Price Now (S0)

Standard Dev - Annual (s)

d1

d2

N(d1)

N(d2)

Call Price (C0)

-d1

-d2

N(-d1)

$0 $20 $40 $60 $80 $100 $120 $140$0

$10

$20

$30

$40

$50

$60

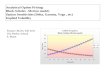

Dynamic Chart of Black Scholes Option Pricing

Stock Price Now

Op

tio

n P

ric

e

Call Put

20ln / / 2 /S X r d T Ts s

0 0 1 2dT rTC S e N d Xe N d

Option Type

Data Table: Sensitivity of Option Price to Stock Price NowInput Values for Stock Price Now (P)

Output Formula:Option PriceIntrinsic Value

Greeks

Inputs Call Greeks

$69.81 69

71.65% 7

Riskfree Rate- Annual (r) 4.95% 5

N(-d2)

Put Price (P0)

BLACK SCHOLES OPTION PRICING

Stock Price Now (S0)

Standard Dev - Annual (s)

$0 $20 $40 $60 $80 $100 $120 $1400.00

2.00

4.00

6.00

8.00

10.00

12.00

Greeks by Stock Price Now

Stock Price Now

Gre

ek

Va

lue

0 0 1 2dT rTP S e N d Xe N d

Delta

Theta

Gamma

Vega

Rho

Greeks

Exercise Price (X) $70.00 70 Put Greeks

Time To Maturity - Years (T) 0.5777 6

Dividend Yield (d) 1.00% 1

Outputs FALSE

d1

d2

$0 $20 $40 $60 $80 $100 $120 $1400.00

2.00

4.00

6.00

8.00

10.00

12.00

Greeks by Stock Price Now

Stock Price Now

Gre

ek

Va

lue

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.00.00

2.00

4.00

6.00

8.00

10.00

12.00

Greeks by Time To Maturity

Time To Maturity

Gre

ek

Va

lue

Delta

Theta

Gamma

Vega

Rho

Greeks

1dTDelta e N d

1

0

1 1where = normal evaluated at

dTN d eGamma

S T

N d density d

s

0 10 1 2

1 1

2

where = normal evaluated at

dTdT rTS N d e

Theta dS N d e rXe N dT

N d density d

s

Call Greeks

Put Greeks

Delta (¶Call / ¶Stock Price)Theta (-¶Call / ¶Time To Mat)

Gamma (¶2Call / ¶Stock Price2)Vega (¶Call / ¶Std Dev)Rho (¶Call / ¶Riskfree Rate)

Delta (¶Put / ¶Stock Price)Theta (-¶Put / ¶Time To Mat)

Gamma (¶2Put / ¶Stock Price2)Vega (¶Put / ¶Std Dev)Rho (¶Put / ¶Riskfree Rate)

2rTRho XTe N d

1dTDelta e N d

1

0

1 1where = normal evaluated at

dTN d eGamma

S T

N d density d

s

0 1

1 1where = normal evaluated at

dTVega S T N d e

N d density d

Call Gamma

Call Vega

2rTRho XTe N d

0 10 1 2

1 1

2

where = normal evaluated at

dTdT rTS N d e

Theta dS N d e rXe N dT

N d density d

s

Data Table: Sensitivity of the Selected Greek to Stock Price NowInput Values for Stock Price Now

Output Formula:Selected Greek

Time To MaturityData Table: Sensitivity of the Selected Greek to Time To Maturity Index

Input Values for Time To Maturity IndexOutput Formula:Selected Greek

Implied Volatility

InputsOption Type: 1=Call, 2=Put 1 1 1 1 1 2 2 2 2 2

$1,513 $1,513 $1,513 $1,513 $1,513 $1,513 $1,513 $1,513 $1,513 $1,51321.66% 17.31% 14.77% 16.01% 13.81% 15.66% 14.73% 14.02% 11.25% 6.31%

Riskfree Rate- Annual (r) 4.62% 4.62% 4.62% 4.62% 4.62% 4.62% 4.62% 4.62% 4.62% 4.62%Exercise Price (X) $1,450 $1,500 $1,520 $1,540 $1,600 $1,450 $1,500 $1,520 $1,540 $1,600Time To Maturity - Years (T) 0.2416 0.2416 0.2416 0.2416 0.2416 0.2416 0.2416 0.2416 0.2416 0.2416Dividend Yield (d) 1.62% 1.62% 1.62% 1.62% 1.62% 1.62% 1.62% 1.62% 1.62% 1.62%Observed Option Price $105.60 $63.40 $45.50 $40.00 $14.50 $17.70 $32.40 $39.50 $42.00 $76.50

Outputs

SolverDifference (observed - model)

BLACK SCHOLES OPTION PRICING

Stock Price Now (S0)Standard Dev - Annual (s)

d1

d2

N(d1)

N(d2)

Model Call Price (C0)

-d1

-d2

N(-d1)

N(-d2)

Model Put Price (P0)

GraphImplied Volatility from CallsImplied Volatility from Puts

Exotic Options

Continuous Dividend Black Scholes Inputs Additional Exotic Option Inputs

$69.81 69 $70.00 70

71.65% 7 70.1% 7

Riskfree Rate- Annual (r) 4.95% 5 0.20 12

Exercise Price (X) $70.00 70 2.0% 2

Time To Maturity - Years (T) 0.5777 6 Time to Chooser Decision (tc) 0.20 2

BLACK SCHOLES OPTION PRICING

Stock Price Now (S0) Asset 2 Stock Price Now (S2)

Standard Dev - Annual (s) Asset 2 Standard Dev (s2)

Corr(Asset 1, Asset 2) (r)

Asset 2 Dividend Yield (d2)

$1,425 $1,450 $1,475 $1,500 $1,525 $1,550 $1,575 $1,600 $1,6253%

5%

7%

9%

11%

13%

15%

17%

19%

21%

23%

"Scowl" Pattern of Implied Volatilities

CallsPuts

Exercise Price

Imp

lied

Vo

lati

lity

Dividend Yield (d) 1.00% 1 Cash Payoff (Z) $60.00 60

Gap Amount (g) $4.00 4

$70.00 70

Continuous Dividend Black Scholes Outputs $75.00 75

11

Supershare Lower Bound (XL)

Supershare Upper Bound (XH)d1

d2

N(d1)N(d2)Call Price (C0)

-d1

-d2

N(-d1)N(-d2)Put Price (P0)

$0 $20 $40 $60 $80 $100 $120 $1400.00

2.00

4.00

6.00

8.00

10.00

12.00

Exotic Options by Stock Price Now

Stock Price NowE

xo

tic

Op

tio

n V

alu

e

Exchange Option

Min of Two Assets

Max of Two Assets

Chooser

Cash-Or-Nothing Call

Cash-Or-Nothing Put

Asset-Or-Nothing Call

Asset-Or-Nothing Put

Exotic Options

Gap Call

Gap Put

Supershare

2 22 22s s rss

22 0 2

1

ln 0.5S S d d Tw

T

Exotic Options

Exchange Option

Minimum of Two AssetsMaximum of Two Assets

Chooser

Binary Options(Digital Options): Cash-or-Nothing Call Cash-or-Nothing Put Asset-or-Nothing Call Asset-or-Nothing Put Gap Call Gap Put

w1

w2

w3

wL

wH

2 1w w T

22 1 0 2

d T dTExchange S e N w S e N w

0 Min of two assets S Exchange

0 Max of two assets S Exchange

2- - rTCash Or Nothing Call Ze N d

2- - rTCash Or Nothing Put Ze N d

0 2- - dTAsset Or Nothing Call e S N d

0 2- - dTAsset Or Nothing Put e S N d

20

3

ln 0.5S X r d T tcw

tc

ss

3 0 3rT dTChooser Call Xe N w tc S e N ws

Supershare

Data Table: Sensitivity of the Selected Exotic Option to Stock Price Now

20ln 0.5L

L

S X r d Tw

T

s

s

20ln 0.5H

H

S X r d Tw

T

s

s

2

0d T

L HL

S eSupershare N w N w

X

0 1 2 dT rTGap Call e S N d X g e N d

2 0 1 rT dTGap Put X g e N d e S N d

0 2- - dTAsset Or Nothing Put e S N d

Input Values for Stock Price NowOutput Formula:Selected Exotic Option

Recommended