Bilingual Series-Strategic Management

Chapter 6

Corporate-Level Strategy

Corporate-Level Strategy

- - low costlow cost- differentiation- differentiation- integrated low cost/differentiation- integrated low cost/differentiation

- - focused low costfocused low cost- focused differentiation- focused differentiation

How to create competitive advantage in each How to create competitive advantage in each business in which the company competesbusiness in which the company competes

1. 1. Business-Level StrategyBusiness-Level Strategy (Competitive Strategy)(Competitive Strategy)

A Diversified CompanyA Diversified CompanyHas Two Levels of StrategyHas Two Levels of Strategy

How to create value for the corporation as a wholeHow to create value for the corporation as a whole

2. 2. Corporate-Level StrategyCorporate-Level Strategy (Companywide Strategy)(Companywide Strategy)

1. 1. What businesses should the What businesses should the corporation be in?corporation be in?

2. 2. How should the corporate office How should the corporate office manage the array of business units?manage the array of business units?

Corporate StrategyCorporate Strategy is what makes the corporate is what makes the corporate whole add up to more than the sum of its business whole add up to more than the sum of its business unit parts ( 2 + 2 => 5 )unit parts ( 2 + 2 => 5 )

Key Questions of Corporate StrategyKey Questions of Corporate Strategy

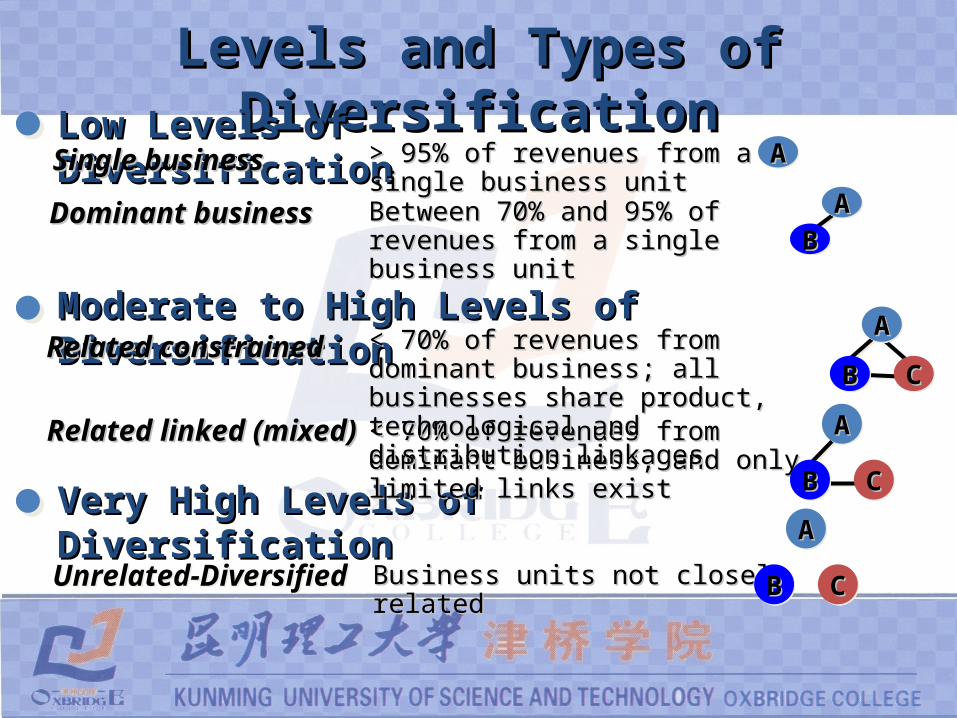

Levels and Types of DiversificationLevels and Types of DiversificationLow Levels of DiversificationLow Levels of Diversification

Moderate to High Levels of DiversificationModerate to High Levels of Diversification

Very High Levels of Very High Levels of DiversificationDiversification

Related linked (mixed)Related linked (mixed) < 70% < 70% of revenues from dominant of revenues from dominant business, and only limited links existbusiness, and only limited links exist

AAAA

BBBB CCCC

Single businessSingle business > 95% > 95% of revenues from a single of revenues from a single business unitbusiness unit

AAAA

Dominant businessDominant business Between 70% and 95% of Between 70% and 95% of revenues from a single revenues from a single business unitbusiness unit

BBBBAAAA

Unrelated-DiversifiedUnrelated-Diversified Business units not closely related Business units not closely related

AAAA

BBBB CCCC

< 70% < 70% of revenues from dominant of revenues from dominant business; all businesses share business; all businesses share product, technological and distribution product, technological and distribution linkageslinkages

Related constrainedRelated constrainedAAAA

BBBB CCCC

Motives, Incentives, and ResourcesMotives, Incentives, and Resourcesfor Diversificationfor Diversification

Motives to Enhance Strategic Motives to Enhance Strategic CompetitivenessCompetitiveness

Economies of ScopeEconomies of Scope

Market PowerMarket Power

Financial EconomiesFinancial Economies

ResourcesResources

ManagerialManagerialMotivesMotives

IncentivesIncentives

Incentives and Resources with Incentives and Resources with Neutral Effects of Strategic Neutral Effects of Strategic

CompetitivenessCompetitiveness

Anti-Trust RegulationAnti-Trust Regulation

Tax LawsTax Laws

Low PerformanceLow Performance

Uncertain Future Cash FlowsUncertain Future Cash Flows

Firm Risk ReductionFirm Risk Reduction

Tangible ResourcesTangible Resources

Intangible ResourcesIntangible Resources

ManagerialManagerialMotivesMotives

ResourcesResources

IncentivesIncentives

Motives, Incentives, and ResourcesMotives, Incentives, and Resourcesfor Diversificationfor Diversification

Managerial Motives Causing Managerial Motives Causing Value ReductionValue Reduction

Diversifying ManagerialDiversifying ManagerialEmployment RiskEmployment Risk

Increasing Managerial Increasing Managerial CompensationCompensation

ManagerialManagerialMotivesMotives

ResourcesResources

IncentivesIncentives

Motives, Incentives, and ResourcesMotives, Incentives, and Resourcesfor Diversificationfor Diversification

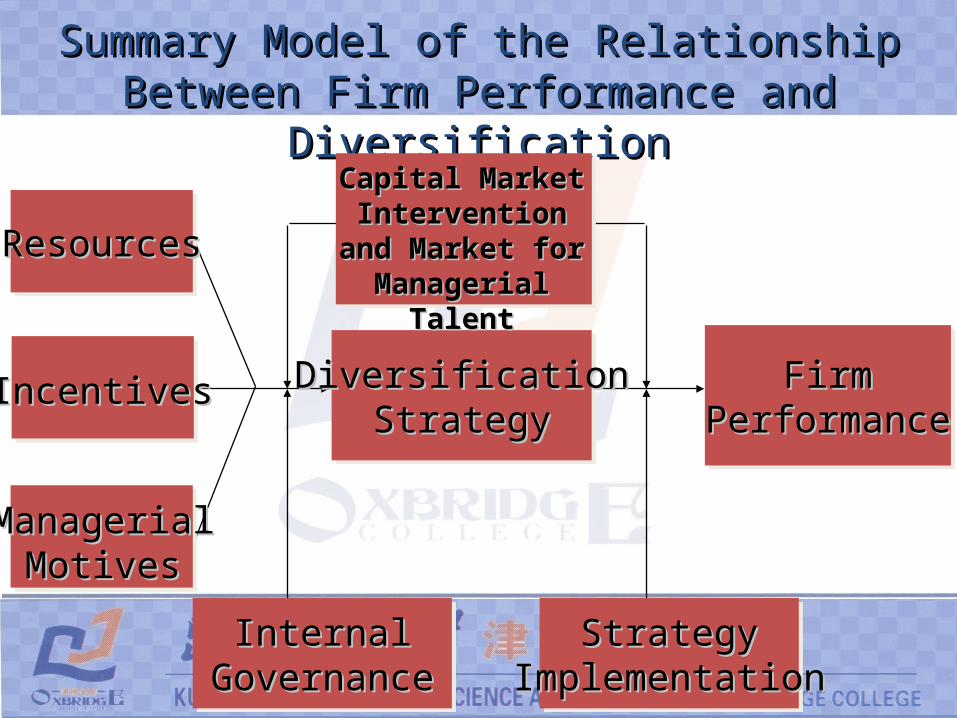

Summary Model of theSummary Model of theRelationship Between FirmRelationship Between Firm

Performance and DiversificationPerformance and Diversification

DiversificationDiversificationStrategyStrategy

ManagerialManagerialMotivesMotives

ResourcesResources

IncentivesIncentives

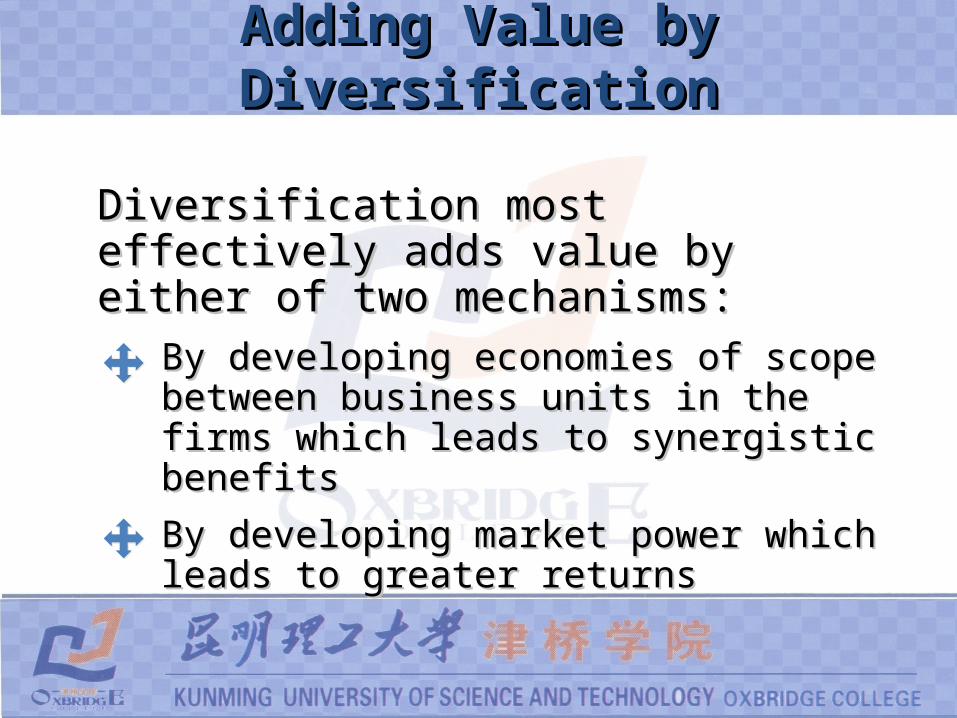

Adding Value by DiversificationAdding Value by Diversification

Diversification most effectively adds Diversification most effectively adds value by either of two mechanisms:value by either of two mechanisms:

By developing economies of scope By developing economies of scope between business units in the firms which between business units in the firms which leads to synergistic benefitsleads to synergistic benefits

By developing market power which leads By developing market power which leads to greater returnsto greater returns

Alternative Diversification StrategiesAlternative Diversification Strategies

Related Diversification Strategies

Unrelated Diversification Strategies

Sharing ActivitiesSharing Activities

Transferring Core CompetenciesTransferring Core Competencies

Efficient Internal Capital Market AllocationEfficient Internal Capital Market Allocation

RestructuringRestructuring

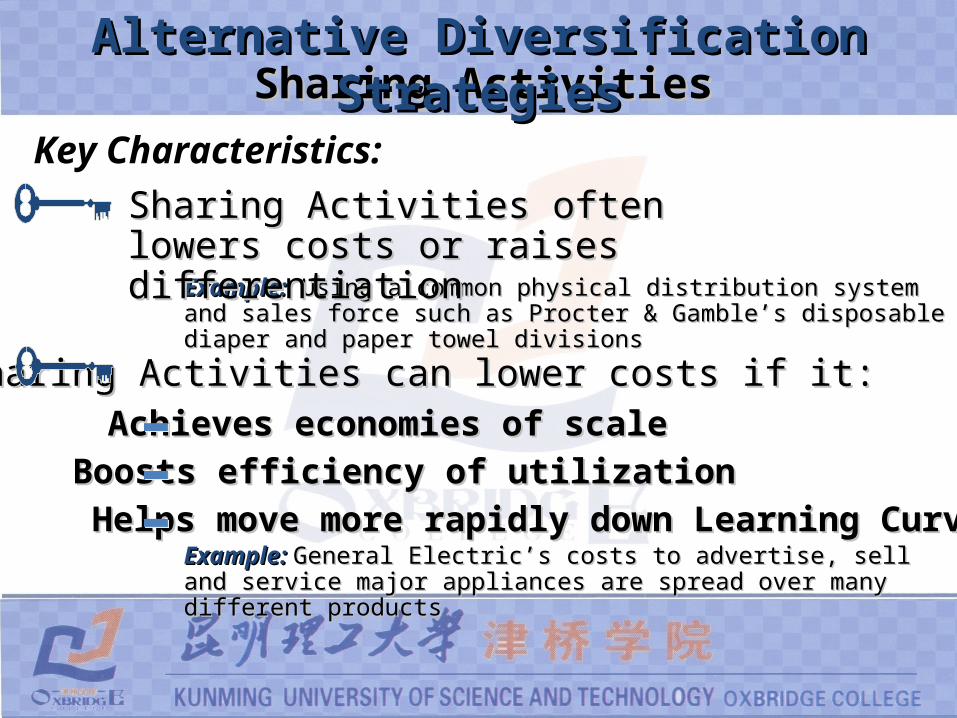

Key Characteristics:

Example:Example: Using a common physical distribution system and sales force Using a common physical distribution system and sales force such as Procter & Gamble’s disposable diaper and paper towel divisionssuch as Procter & Gamble’s disposable diaper and paper towel divisions

Example:Example: General Electric’s costs to advertise, sell and service major General Electric’s costs to advertise, sell and service major appliances are spread over many different productsappliances are spread over many different products

Sharing ActivitiesSharing ActivitiesAlternative Diversification StrategiesAlternative Diversification Strategies

Achieves economies of scaleAchieves economies of scale

Boosts efficiency of utilizationBoosts efficiency of utilization

Helps move more rapidly down Learning CurveHelps move more rapidly down Learning Curve

Sharing Activities often lowers costs or Sharing Activities often lowers costs or raises differentiationraises differentiation

Sharing Activities can lower costs if it:Sharing Activities can lower costs if it:

Example:Example: Procter & Gamble’s sharing of sales and physical Procter & Gamble’s sharing of sales and physical distribution for disposable diapers and paper towels is effective distribution for disposable diapers and paper towels is effective because these items are so bulky and costly to shipbecause these items are so bulky and costly to ship

Key Characteristics:

Sharing ActivitiesSharing ActivitiesAlternative Diversification StrategiesAlternative Diversification Strategies

Sharing Activities can enhance potential Sharing Activities can enhance potential for or reduce the cost of differentiationfor or reduce the cost of differentiation

Must involve activities that are crucial to Must involve activities that are crucial to competitive advantagecompetitive advantage

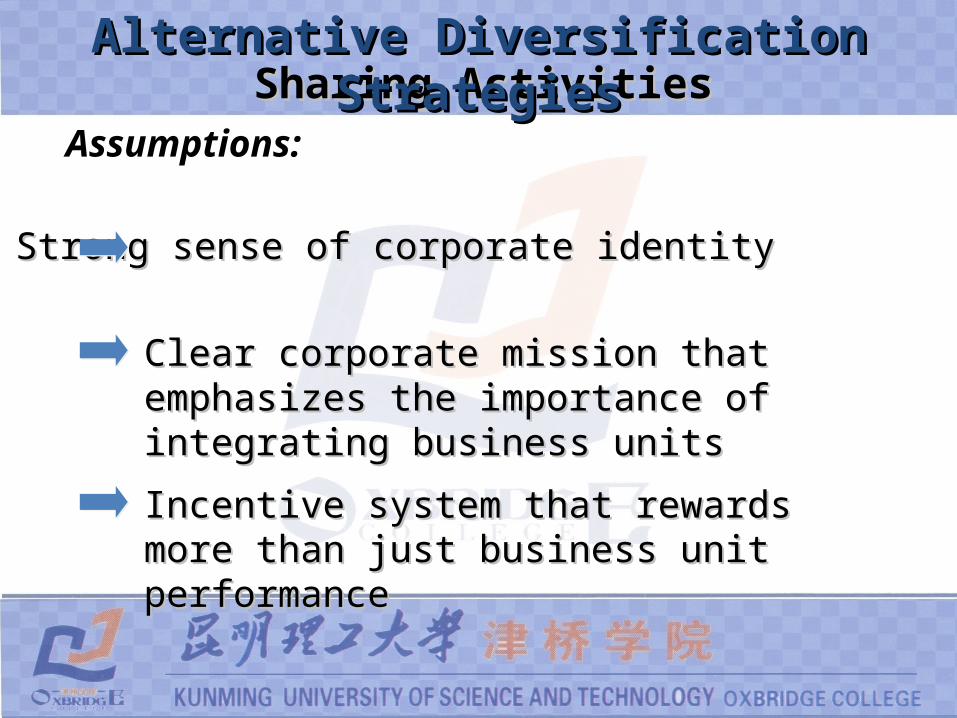

Assumptions:

Sharing ActivitiesSharing ActivitiesAlternative Diversification StrategiesAlternative Diversification Strategies

Strong sense of corporate identityStrong sense of corporate identity

Clear corporate mission that emphasizes the Clear corporate mission that emphasizes the importance of integrating business unitsimportance of integrating business units

Incentive system that rewards more than Incentive system that rewards more than just business unit performancejust business unit performance

Alternative Diversification StrategiesAlternative Diversification Strategies

Related Diversification Strategies

Unrelated Diversification Strategies

Sharing ActivitiesSharing Activities

Transferring Core CompetenciesTransferring Core Competencies

Efficient Internal Capital Market AllocationEfficient Internal Capital Market Allocation

RestructuringRestructuring

Key Characteristics:

Transferring Core CompetenciesTransferring Core CompetenciesAlternative Diversification StrategiesAlternative Diversification Strategies

Identify ability to transfer skills or Identify ability to transfer skills or expertise among similar value chainsexpertise among similar value chainsIdentify ability to transfer skills or Identify ability to transfer skills or expertise among similar value chainsexpertise among similar value chains

Exploit ability to Exploit ability to transfer activitiestransfer activities

Exploits Exploits InterrelationshipsInterrelationships among divisions among divisionsExploits Exploits InterrelationshipsInterrelationships among divisions among divisions

Start with Start with Value ChainValue Chain analysisanalysisStart with Start with Value ChainValue Chain analysisanalysis

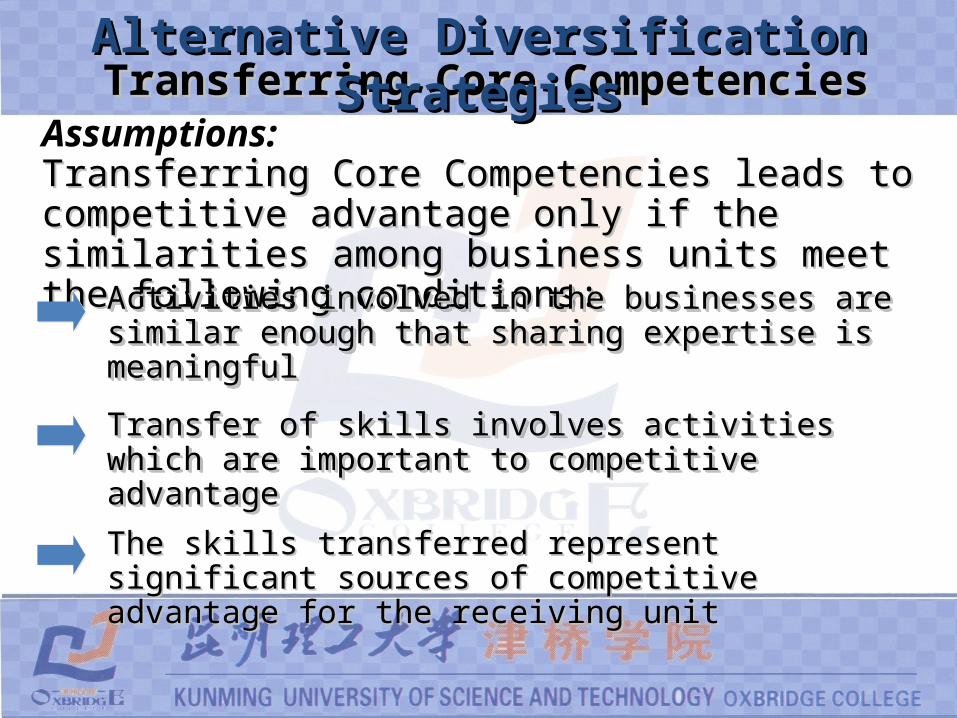

Assumptions:Transferring Core Competencies leads to competitive Transferring Core Competencies leads to competitive advantage only if the similarities among business advantage only if the similarities among business units meet the following conditions:units meet the following conditions:

Activities involved in the businesses are similar enough Activities involved in the businesses are similar enough that sharing expertise is meaningfulthat sharing expertise is meaningfulActivities involved in the businesses are similar enough Activities involved in the businesses are similar enough that sharing expertise is meaningfulthat sharing expertise is meaningful

Transfer of skills involves activities which are important to Transfer of skills involves activities which are important to competitive advantagecompetitive advantageTransfer of skills involves activities which are important to Transfer of skills involves activities which are important to competitive advantagecompetitive advantage

The skills transferred represent significant sources of The skills transferred represent significant sources of competitive advantage for the receiving unitcompetitive advantage for the receiving unit

Transferring Core CompetenciesTransferring Core CompetenciesAlternative Diversification StrategiesAlternative Diversification Strategies

Alternative Diversification StrategiesAlternative Diversification StrategiesRelated Diversification Strategies

Unrelated Diversification Strategies

Sharing ActivitiesSharing Activities

Transferring Core CompetenciesTransferring Core Competencies

Efficient Internal Capital Market AllocationEfficient Internal Capital Market Allocation

RestructuringRestructuring

Key Characteristics:Firms pursuing this strategy frequently diversify by Firms pursuing this strategy frequently diversify by acquisition:acquisition:

Efficient Internal Capital Market AllocationEfficient Internal Capital Market AllocationAlternative Diversification StrategiesAlternative Diversification Strategies

Acquire sound, attractive companiesAcquire sound, attractive companies

Acquiring corporation supplies needed capital Acquiring corporation supplies needed capital

Portfolio managers transfer resources from units Portfolio managers transfer resources from units that generate cash to those with high growth that generate cash to those with high growth potential and substantial cash needspotential and substantial cash needs

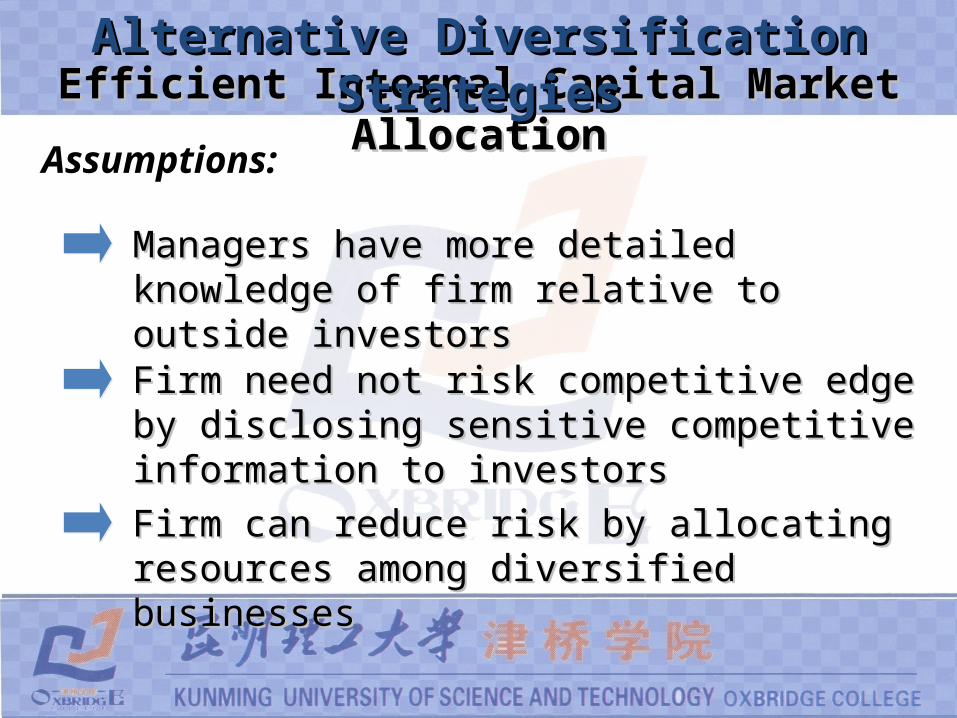

Assumptions:

Efficient Internal Capital Market AllocationEfficient Internal Capital Market AllocationAlternative Diversification StrategiesAlternative Diversification Strategies

Managers have more detailed knowledge of firm Managers have more detailed knowledge of firm relative to outside investorsrelative to outside investors

Firm need not risk competitive edge by disclosing Firm need not risk competitive edge by disclosing sensitive competitive information to investorssensitive competitive information to investors

Firm can reduce risk by allocating resources Firm can reduce risk by allocating resources among diversified businessesamong diversified businesses

Alternative Diversification StrategiesAlternative Diversification Strategies

Related Diversification Strategies

Unrelated Diversification Strategies

Sharing ActivitiesSharing Activities

Transferring Core CompetenciesTransferring Core Competencies

Efficient Internal Capital Market AllocationEfficient Internal Capital Market Allocation

RestructuringRestructuring

Key Characteristics:

RestructuringRestructuring

- - Changes sub-unit management teamChanges sub-unit management team

- - Shifts strategyShifts strategy

-- Infuses (Infuses (注入注入 ) ) firm with new technologyfirm with new technology

-- Divests (Divests (剥夺剥夺 ) ) part of firmpart of firm

-- Enhances discipline by changing control systemsEnhances discipline by changing control systems

Alternative Diversification StrategiesAlternative Diversification Strategies

Seek out undeveloped, sick or threatened organizations Seek out undeveloped, sick or threatened organizations or industriesor industries

Parent company (acquirer) intervenes and frequentlyParent company (acquirer) intervenes and frequently::

Frequently sell unit after making one-time changes since Frequently sell unit after making one-time changes since parent no longer adds value to ongoing operationsparent no longer adds value to ongoing operations

Assumptions:RestructuringRestructuring

Alternative Diversification StrategiesAlternative Diversification Strategies

Requires keen management insight in Requires keen management insight in selecting firms with depressed values or selecting firms with depressed values or unforeseen potentialunforeseen potential

Must do more than restructure companiesMust do more than restructure companies

Need to initiate restructuring of industries to Need to initiate restructuring of industries to create a more attractive environmentcreate a more attractive environment

Example: China Textiles IndustryExample: China Textiles Industry

Internal Incentives:

Incentives to DiversifyIncentives to Diversify

Relaxation of Anti-Trust regulation allows more related Relaxation of Anti-Trust regulation allows more related acquisitions than in the pastacquisitions than in the pastBefore 1986, higher taxes on dividends favored spending Before 1986, higher taxes on dividends favored spending retained earnings on acquisitionsretained earnings on acquisitionsAfter 1986, firms made fewer acquisitions with retained After 1986, firms made fewer acquisitions with retained earnings, shifting to the use of debt to take advantage of earnings, shifting to the use of debt to take advantage of tax deductible interest payments (after mid-90’s, situation tax deductible interest payments (after mid-90’s, situation changed again)changed again)

External Incentives:

Poor performance may lead some firms to diversify to Poor performance may lead some firms to diversify to attempt to achieve better returns attempt to achieve better returns

Per

form

ance

Per

form

ance

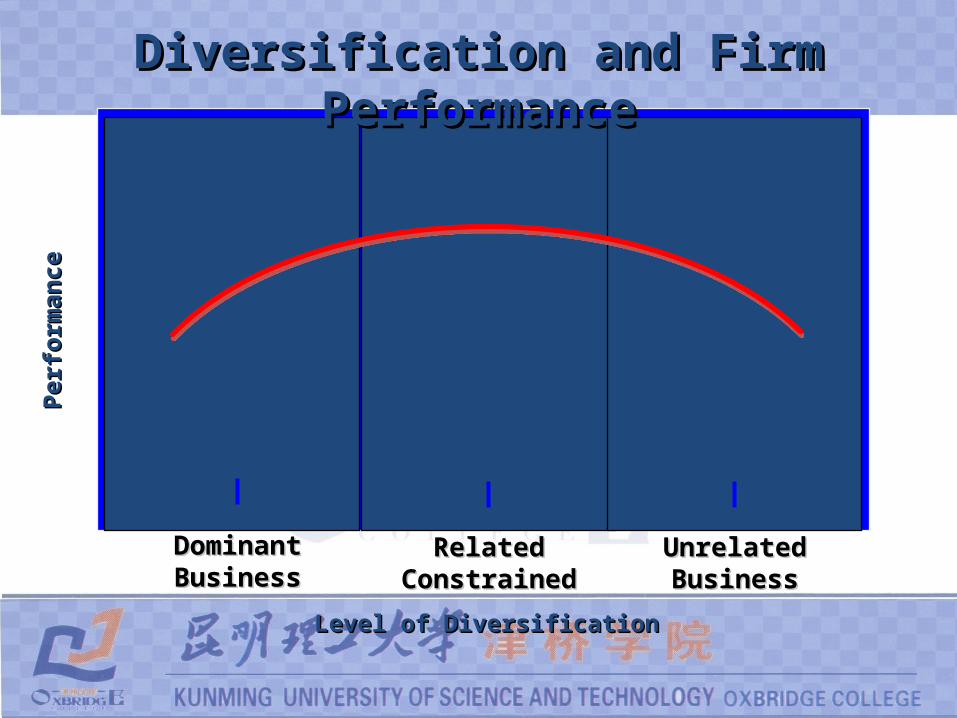

Level of DiversificationLevel of Diversification

Diversification and Firm PerformanceDiversification and Firm Performance

DominantDominantBusinessBusiness

UnrelatedUnrelatedBusinessBusiness

RelatedRelatedConstrainedConstrained

Incentives to DiversifyIncentives to DiversifyInternal Incentives:Internal Incentives:

Poor performance may lead some firms to diversify to Poor performance may lead some firms to diversify to attempt to achieve better returns attempt to achieve better returns

Firms may diversify to balance uncertain future cash flowsFirms may diversify to balance uncertain future cash flows

Firm may diversify into different businesses in order to Firm may diversify into different businesses in order to reduce riskreduce risk

Managers often have incentives to diversify in order to Managers often have incentives to diversify in order to increase their compensation and reduce employment risk, increase their compensation and reduce employment risk, although effective governance mechanisms may restrict although effective governance mechanisms may restrict such abusessuch abuses

Summary Model of the Relationship Between Summary Model of the Relationship Between Firm Performance and DiversificationFirm Performance and Diversification

ResourcesResources

DiversificationDiversificationStrategyStrategy

FirmFirmPerformancePerformance

InternalInternalGovernanceGovernance

StrategyStrategyImplementationImplementation

Capital Market Capital Market Intervention and Intervention and

Market for Market for Managerial TalentManagerial Talent

IncentivesIncentives

ManagerialManagerialMotivesMotives

Recommended