123

Presenting ...

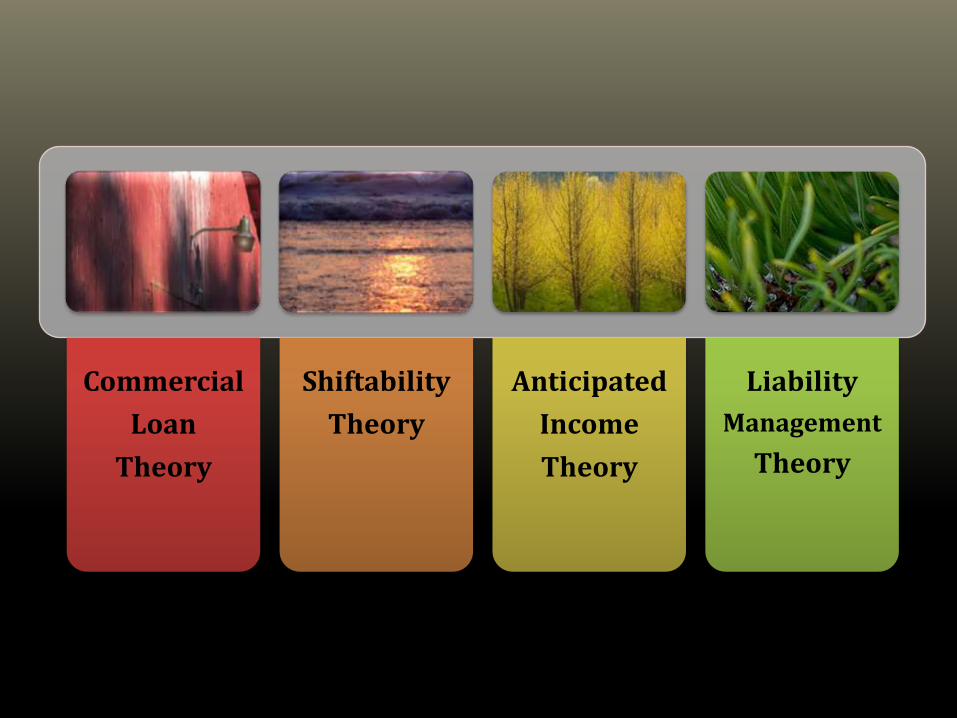

There are four important concepts of liquidity management through history

Commercial

Loan

Theory

Shiftability

Theory

Anticipated

Income

Theory

Liability

Management

Theory

Originated in England during the 18th century

The Theory States: A Commercial Bank must provide short term liquidating loans to meet

working capital requirements. Bank should refrain from long term loans

Banks have to meet the short term obligations for its depositors, borrowers and other customers

A new loan is not granted unless the previous loan was repaid; thus it created an imbalance between demand and supply

Banks should provide loans before the maturity of the previous bills

It has failed to take cognizance of the fact that bank can ensure liquidity of its assets only when these are readily convertible into cash without any loss.

During an economic depression prices of goods fall, goods can not move fast through normal channel and it gives no guarantee whether debtor will be able to repay the borrowed amount or not.

Originated in USA in 1918 by H. G. Moulton

The Theory States: According to this theory the problem of liquidity is not a problem but

shifting of assets without any material loss.

Moulton Says, “To attain minimum reserve, relying on maturing bills is not needed but maintaining quantity of assets which can be shifted to other banks whenever necessary”

In case of liquidity crisis, banks should maintain liquidity by possessing assets which can be shifted to the central bank.

Eligibility of shifting assets is a big question that has to ensure the soundness and acceptability of those assets.

Under an economic crisis, when whole industry suffer – shares and debentures fail to attract buyer and thus cost of shifting assets would be high

Even though blue chip securities lose their Shiftability character.

Developed in 1948 by Herbert V. Prochnow

The Theory States:Banks should increase in participating term loans.

According to this theory, bankers should plan the liquidation of term loans on the basis of anticipated earnings of the borrowers.

Borrowers need not to sale their assets or not to shift the term loans to other banks

All loans will become liquid only when borrowers havethe capacity to repay the sum

A continuous estimation is needed to assumethe future earning or net cash inflow of theborrowers for amortization of loan

Future earning of a person may diminish thanthat of current level of earnings.

Emerged in the year 1960

The Theory States:This is one of the most important liquidity theories which

has been practicing till now.

According to this theory banks need to acquire reserves from several different sources by creating additional liabilities against itself and to balance them properly.

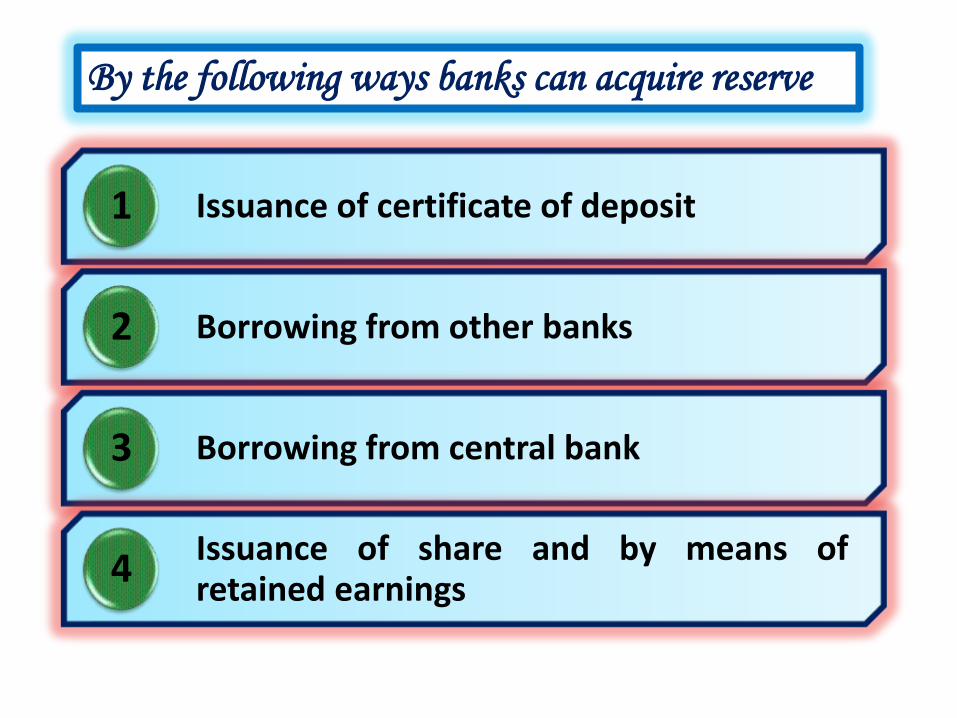

• Issuance of certificate of deposit1

• Borrowing from other banks2

• Borrowing from central bank3

• Issuance of share and by means ofretained earnings

4

By the following ways banks can acquire reserve

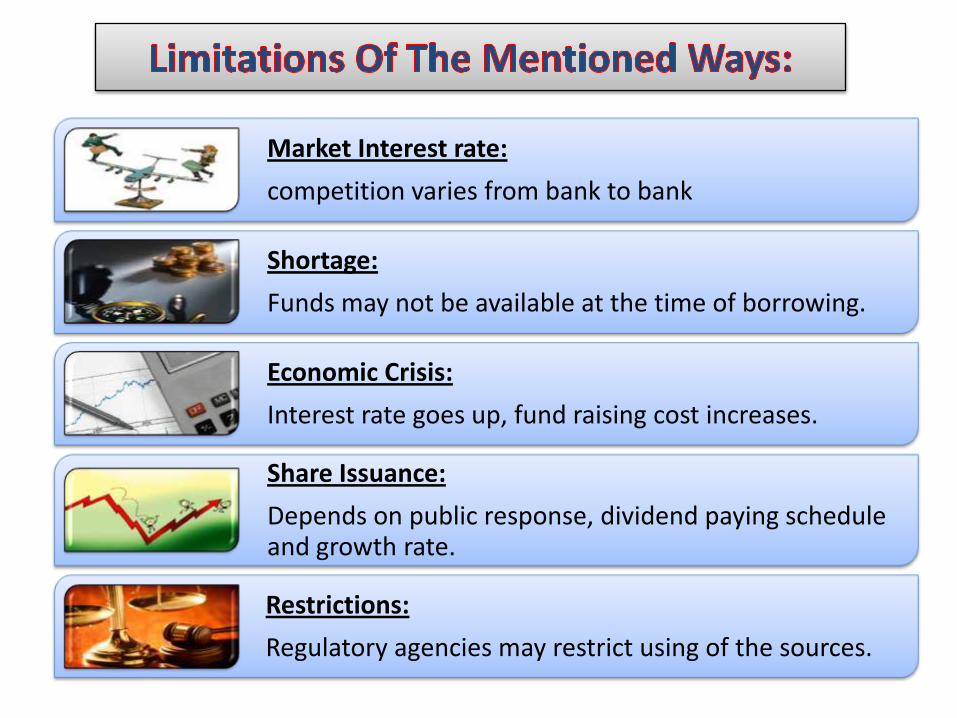

Market Interest rate:

competition varies from bank to bank

Shortage:

Funds may not be available at the time of borrowing.

Economic Crisis:

Interest rate goes up, fund raising cost increases.

Share Issuance:

Depends on public response, dividend paying schedule and growth rate.

Restrictions:

Regulatory agencies may restrict using of the sources.

The theory practicing currently makes a limited contribution.

Recommended