Country Profile 2005

Bangladesh This Country Profile is a reference work, analysing the country’s history, politics, infrastructure and economy. It is revised and updated annually. The Economist Intelligence Unit’s Country Reports analyse current trends and provide a two-year forecast.

The full publishing schedule for Country Profiles is now available on our website at http://www.eiu.com/schedule The Economist Intelligence Unit 15 Regent St, London SW1Y 4LR United Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For over 50 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where its latest analysis is updated daily; through printed subscription products ranging from newsletters to annual reference works; through research reports; and by organising seminars and presentations. The firm is a member of The Economist Group.

London The Economist Intelligence Unit 15 Regent St London SW1Y 4LR United Kingdom Tel: (44.20) 7830 1007 Fax: (44.20) 7830 1023 E-mail: [email protected]

New York The Economist Intelligence Unit The Economist Building 111 West 57th Street New York NY 10019, US Tel: (1.212) 554 0600 Fax: (1.212) 586 0248 E-mail: [email protected]

Hong Kong The Economist Intelligence Unit 60/F, Central Plaza 18 Harbour Road Wanchai Hong Kong Tel: (852) 2585 3888 Fax: (852) 2802 7638 E-mail: [email protected]

Website: www.eiu.com

Electronic delivery This publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, on-line databases and as direct feeds to corporate intranets. For further information, please contact your nearest Economist Intelligence Unit office

Copyright © 2005 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However, the Economist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-8145

Symbols for tables “n/a” means not available; “–” means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Bangladesh 1

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Contents

Bangladesh

3 Basic data

4 Politics 4 Political background 5 Recent political developments 8 Constitution, institutions and administration 10 Political forces 12 International relations and defence

15 Resources and infrastructure 15 Population 16 Education 17 Health 17 Natural resources and the environment 18 Transport, communications and the Internet 22 Energy provision

24 The economy 24 Economic structure 26 Economic policy 30 Economic performance 31 Regional trends

32 Economic sectors 32 Agriculture 35 Mining and semi-processing 35 Manufacturing 37 Construction 37 Financial services 40 Other services

40 The external sector 40 Trade in goods 41 Invisibles and the current account 42 Capital flows and foreign debt 43 Foreign reserves and the exchange rate

44 Regional overview 44 Membership of organisations

45 Appendices 45 Sources of information 46 Reference tables 46 Population 46 Energy reserves and production of natural gas 47 Transport 47 Gross domestic product

2 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

48 Gross domestic product by expenditure 48 Gross domestic product by sector 49 Central government finances 49 Money supply 50 Interest rates 50 Prices 50 Index of nominal wages 50 Agricultural crop production 51 Production and value of non-energy minerals 51 Production and value of selected manufactured items 52 Stockmarket indicators 52 Main exports 52 Main imports 53 Main trading partners 53 Balance of payments, IMF series 54 External debt, World Bank series 54 Remittances from Bangladeshis working abroad 55 Net official development assistance 55 Foreign reserves 55 Exchange rates

Bangladesh 3

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Bangladesh

Basic data

147,570 sq km

135.2m (2003/04 fiscal year)

Population in ‘000 (2001 census)

Dhaka (capital) 9,913 Chittagong 3,203 Khulna 1,227 Rajshahi 647

Tropical monsoon

Hottest month, July, 23-35°C (average daily minimum and maximum); coldest month, January, 11-28°C; driest months, December and January, 5 mm average monthly rainfall; wettest month, July, 567 mm average monthly rainfall

Bengali; Urdu and Hindi are minority languages and English is also used

Muslim (89.7% in 2001 census); Hindu (9.2%); Buddhist (0.7%); Christian (0.3%); others (0.2%)

Imperial system. Local measures include: 1 tola=11.66 g; 1 seer=80 tolas=932 g; 1 maund=40 seers=37.29 kg

Numbers are commonly expressed in crores and lakhs; 1 crore=10m, written 1,00,00,000; 1 lakh=100,000, written 1,00,000

Taka (Tk)=100 paisa. Annual average exchange rate in 2004: Tk59.5:US$1; exchange rate on November 8th 2005: Tk65.75:US$1

July 1st-June 30th

6 hours ahead of GMT

January 1st (New Year’s Day), 21st (Eid-ul-Adha); February 10th (Elam Hejir New Year); March 17th (Birthday of Bagabethu Sheikh Mujibur Rahman), 26th (Independence Day); April 14th (Bangla Naba Barsha), 29th (Buddha Purnima); May 1st (Labour Day); September 2nd (Shab-e Barat), October 11th (Durga Puja); November 3rd (End of Ramadan), 7th (National Revolution Day); December 16th (Victory Day); plus religious holidays that depend on lunar sightings and optional holidays for different religious groups.

Land area

Climate

Weather in Dhaka

Languages

Measures

Fiscal year

Time

Population

Main towns

Religion

Currency

Public holidays in 2005

4 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Politics

Bangladesh has a parliamentary democracy based on universal suffrage. The executive branch of government consists of a cabinet led by the prime minister. The Awami League (AL), led by Sheikh Hasina Wajed, ruled for five years until July 2001, when an interim caretaker government was established. The general election held in October that year was won by a four-party alliance led by the Bangladesh Nationalist Party (BNP) under the prime minister, Khaleda Zia, which is still in government. The BNP dominates the alliance, with a large parliamentary majority in its own right. The Jamaat-e-Islami (Jamaat), an Islamist party, is its largest coalition partner; the Islami Oikyo Jote (IOJ) and the Manjur faction of the Jatiya Party (JP) complete the government. A caretaker government will be appointed in October 2006 to supervise the next election, which must then be held within 90 days. Bangladesh had a presidential form of government before the constitution was amended in 1991, but the presidency is now a largely ceremonial position appointed by parliament.

Political background

The eastern part of Bengal became part of Pakistan with the end of British rule in India in 1947. From the beginning, East Pakistan had an uneasy relationship with the more powerful and richer West Pakistan. Despite some concessions from the West Pakistan government, such as the approval of Bengali as a joint official language with Urdu, and the division of Pakistan into two parts (East and West) with equal parliamentary representation, a secessionist movement led by Sheikh Mujibur Rahman and the AL gained increasing support. In 1970 Sheikh Mujib led the AL to parliamentary victory in East Pakistan and demanded a loose federation of the two parts of Pakistan, in which a central authority would be responsible only for foreign affairs, the currency and defence. On March 26th 1971 separatist forces declared independence, and a full-scale civil war broke out. This was eventually won by the Bengali freedom fighters, after the Indian military intervened on their behalf, on December 16th 1971.

Sheikh Mujib led the AL to an electoral victory in 1973, but the economic and political situation began to deteriorate rapidly. Sheikh Mujib declared a state of emergency in late 1974 and in early 1975 he became president, assuming dictatorial powers through one-party rule. He and several of his family members were assassinated in August 1975. A series of further coups ensued, but by 1977 General Ziaur Rahman had consolidated his power and assumed the presidency.

General Zia’s period in power was characterised by improvements in public order and economic management. In June 1978 he won the presidential election, and in the following year his newly formed party, the BNP, won two-thirds of the seats in parliament. However, in May 1981 General Zia was assassinated by a group of army officers. In March 1982 the army chief, General

Independence from Pakistan

The early years

General Zia is ousted by the army

Bangladesh 5

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Hossain Mohammad Ershad, took power in a bloodless coup, replacing Justice Abdus Sattar, who had briefly succeeded General Zia after his assassination.

General Ershad attempted to hold parliamentary and presidential elections to legitimise his position, but the principal opposition parties refused to participate, arguing that any election would be unfair under martial law. In March 1985 he banned political activities and staged a presidential election, in which he declared himself the winner, despite a dismal voter turnout. His autocratic rule provoked violent riots, and in 1987 the main opposition groups began a campaign to force him out. Three years of violence followed, during which General Ershad proclaimed a state of emergency and arrested opposition activists. In December 1990 General Ershad relinquished power to a neutral caretaker government, which organised a free and fair election in February 1991. General Ershad and many of his cronies faced charges of corruption and illegal possession of arms. He was sentenced to 13 years’ imprisonment in 1991, but was released in January 1997 in recognition of his Jatiya Party’s support for the newly elected AL government.

The 1991 election was won by the BNP, led by Khaleda Zia, General Zia’s widow. In parliament, there was initially a shaky truce between the AL and the BNP government. However, after alleged irregularities by the BNP during a February 1994 by-election all opposition parties boycotted parliament, demanding that the government resign and a general election be held. Although the BNP government dissolved parliament in late 1995, the opposition boycotted the general election in February 1996 because Mrs Zia had refused to step down before the election. The BNP claimed victory in a low-turnout election, but as violence escalated it was forced to transfer power to a caretaker government.

In the June 1996 election, supervised by a caretaker government, the AL, led by Sheikh Mujib’s daughter, Sheikh Hasina Wajed, won a majority of the seats in parliament and formed a government with support from the Jatiya Party led by General Ershad. The AL government repealed the Indemnity Ordinance, passed in 1975 to protect the assassins of Sheikh Mujib. A trial of some of the accused began in January 1997. In November 1998, 15 former soldiers were sentenced to death, although most of them had already fled the country in the meantime.

Recent political developments

The AL government made an arrangement with India to share the water of the Ganges river; it ended a 20-year insurgency by concluding a peace treaty with tribal rebels in the Chittagong Hill Tracts, repaired the devastation of the 1998 floods, and oversaw moderately high rates of economic growth. However, the AL government failed to resolve crippling power shortages and to prevent an alarming deterioration in law and order. Intense political antagonism between the AL and the BNP continued throughout the Hasina administration. Emulating previous AL tactics to undermine political stability, the BNP boycotted parliament and elections under AL rule. The government of

The AL steps down peacefully

The re-establishment of democracy

The AL government

General Ershad’s rule

6 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Sheikh Hasina completed its five-year term in July 2001 before agreeing to make way for a caretaker government. This orderly transfer of power was a milestone in the maturation of democracy in Bangladesh.

The four-party alliance led by the BNP won a landslide victory in the general election held on October 1st 2001. The alliance captured 219 seats, with the BNP alone taking 195 seats in the 300-member parliament. The AL won 58 seats, compared with 146 seats in the previous election held in June 1996. The BNP-led alliance won 46.9% of the votes cast, and the AL received 40.1%. Jamaat, an Islamist party and a partner in the BNP-led coalition, won 17 parliamentary seats. The JP won 14 seats, making it the second-largest opposition party.

During the first four years in office the four-party alliance oversaw steady economic growth of 5-6% a year, and some progress was made in areas such as poverty reduction and social development. However, the alliance failed to deliver on two key election promises—curbing corruption and improving law and order. Corruption remains a serious problem, and the law and order situation has, if anything, worsened under its tenure. The perpetrators of the assassination of the AL politician, Shah A M S Kibria, and of the August 2004 bomb attack on an AL rally, in which 21 people were killed, are still at large. Moreover, the highly co-ordinated attacks in August 2005, in which more than 350 bombs went off in 63 of Bangladesh’s 64 districts, seem to have vindicated fears of “Talibanisation” and of Bangladesh becoming a base for international terrorism. In February 2005 the government banned two Islamic organisations—the Jamiat-ul-Mujahideen (JMB) and Jagrata Muslim Janata Bangladesh (JMJB)—but had previously denied that there were any militants operating in the country. Thus, the BNP has faced criticism for not having cracked down on religious extremism earlier. The government’s position to adopt a firm stance against religious extremism has been complicated by its reliance on the support of two Muslim parties, the Jamaat and the IOJ, to remain in government.

Despite problems during the 2001 election campaign, monitors from domestic and international delegations said that polling on election day was generally free, fair and peaceful. They called on the AL to accept the result of the election, which was a substantial defeat for the party. However, Sheikh Hasina claimed that the election had been rigged and said that the non-partisan caretaker government, which had administered Bangladesh in the run-up to the general election, had conspired with the Election Commission to oust the AL. In June 2002 the research wing of the AL published a book on the "rigged election". The AL still refuses to accept the legitimacy of the government.

The mutual personal antipathy between the two leaders, Mrs Zia and Sheikh Hasina, has polarised the political scene to such an extent that it prevents the smooth operation of governance. For instance, the AL has chosen to oppose various government policies and the current BNP government itself by boycotting parliament and calling general strikes—the same tactics that the BNP used when it was in opposition. Without the semblance of opposition

The AL refuses to recognise the election as legitimate

Politics remain highly polarised

The BNP government

The BNP returns to power in a landslide victory

Bangladesh 7

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

engagement in the formal political process, the BNP-led government has struggled to fulfil one of its main campaign pledges, the restoration law and order, and to implement economic reforms. The expansion of power-generating capacity—an indispensable prerequisite for faster economic growth—has been minimal. Nevertheless, the government has made some progress. It has closed a politically sensitive textile mill, drawn up prudent budgets, and floated the taka at the end of May 2003. The country has enjoyed relative macroeconomic stability with stable inflation and economic growth of around 5% in recent years. The government has also sustained good relations with multilateral and bilateral donors. Although a bomb attack on an AL rally in August 2004, which killed several party leaders, led to a further deterioration of law and order, the BNP government is likely to see out its full term in office. The next election is due by early 2007.

Important recent events

October 1st 2001

The four-party alliance led by the Bangladesh Nationalist Party (BNP) wins a majority of more than two-thirds in parliament. The claim by the Awami League (AL) of election-rigging is rejected by impartial domestic and international observers.

January 9th 2003

The government promulgates the Joint Drive Indemnity Ordinance as Operation Clean Heart is wound down, protecting the armed forces from legal actions relating to abuses alleged to have been committed during the anti-crime crackdown. Parliament later passes the Joint Drive Indemnity Act.

June 25th 2003

The AL begins an indefinite boycott of parliament and does not attend the passage of the budget for fiscal year 2003/04 (July-June), preferring to agitate on the streets instead.

February-April 2004

The AL calls a series of hartals (general strikes) in an attempt to force the government from power by April 30th 2004. The deadline expires without any change in government.

July-August 2004

The country is hit by one of the worst floods in decades, which inundate two-thirds of the country. The floods leave 600 people dead, with 30m homeless and an estimated 20m people requiring food aid.

August 21st 2004

A grenade attack on an opposition AL rally in the capital, Dhaka, kills at least 19 people. The opposition leader, Sheikh Hasina, narrowly escapes, but several senior party members die in the attack. The perpetrators remain at large.

January 27th 2005

The prominent AL politician and former finance minister, Shah A M S Kibria, is killed in a grenade attack at a political rally. The AL calls a general strike in protest.

8 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

August 17th 2005

Some 350 small bombs detonate within about an hour of each other in 63 out of Bangladesh’s 64 districts. The highly co-ordinated terrorist onslaught kills two and injures more than 100. The Jamaat-ul-Mujahidin Bangladesh (JMB), a banned Islamist extremist organisation, has been linked to the attacks.

October 2005

The government launches the biggest-ever free rice distribution programme amid food shortages, following severe flooding in 2004 and a poor harvest in 2005.

Constitution, institutions and administration

Bangladesh has a parliamentary system of government based on universal adult suffrage. Before the 12th amendment (1991) of the constitution, a presidential form of government was in place. Under the current system, the prime minister is vested with executive power and the president (elected by parliament) can act only on the advice of the prime minister. The president appoints the Council of Ministers (cabinet) on the advice of the prime minister. The Jatiya Sangshad (parliament) is a unicameral legislature with 300 directly elected seats. It has a term of five years. Laws are passed by a simple majority, but constitutional amendments require a two-thirds majority. According to the constitution, the state religion is Islam, but other religions may be practised. The 13th amendment (1996) of the constitution provides for the organisation of general elections by caretaker non-party technocratic governments. The 14th amendment of the constitution—passed in May 2004—reserves 45 seats for women.

Bangladesh is divided into 64 districts, each with its own district council. Beneath the districts are 460 subdistricts and 4,488 union councils, which are currently the lowest tier of government in Bangladesh. In late 2003 the government formed 40,392 village governments (gram sarkar) as a fourth layer of government. Gram sarkars are non-elected bodies at the grassroots level and were introduced by a former president, General Zia, in the late 1970s. When he was president, General Ershad introduced upazila (local councils) in the mid-1980s, as an elected local government body. The village governments are aimed at local development by local people. Although the constitution provides for elected bodies at all tiers of local government, only the third tier—union councils and municipalities (mostly subdistrict and district administrative centres)—is elected; all others are administratively controlled. Bangladesh has six administrative divisions—Dhaka, Chittagong, Khulna, Barisal, Rajshahi and Sylhet—and four major municipal corporations—Dhaka, Chittagong, Rajshahi and Khulna. The mayors of the municipal corporations are directly elected and wield considerable political power.

A candidate can contest a maximum of five constituencies in a parliamentary election, allowing political leaders to ensure their election to the legislature. A by-election is called if a candidate wins in more than one constituency. Although both major political parties are currently led by women, they tend

Parliament is elected by universal suffrage

The local government system

Candidates may run for multiple constituencies

Bangladesh 9

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

not to nominate women candidates for general seats. Only 35 female candidates ran in the 2001 general election, out of a total of 1,933 candidates.

The 13th amendment

The caretaker government

The 13th amendment to the constitution, passed on March 26th 1996, provides for a non-partisan caretaker government to hold free and fair parliamentary elections. The caretaker government is responsible for giving the Election Commission "all possible aid and assistance that may be required for holding the general election of members of parliament peacefully, fairly and impartially". The caretaker government takes office within 15 days of the dissolution of parliament and must hold a general election within 90 days of the dissolution. The caretaker government is led by a chief adviser, who runs the government with not more than ten other advisers, appointed by the president on the advice of the chief adviser. The chief adviser enjoys the status and privileges of a prime minister, but does not have the power to make any policy that goes beyond his remit of ensuring the smooth conduct of the election. He and his advisers are collectively responsible to the president—unlike the prime minister—and carry on the routine functions of government. The supreme command of the military forces is vested in the president for the duration of the caretaker government. Bangladesh has had two caretaker governments: the first supervised the June 1996 general election, and the second oversaw the eighth parliamentary election held in October 2001.

The Supreme Court is the highest court and its judges are appointed by the president. There is a nationwide system of criminal and civil courts, and there are metropolitan magistrates in the major cities. In addition, money-loan courts and bankruptcy courts deal with financial matters. The legal framework is archaic, and court procedures are often cumbersome. The judiciary is not fully independent of the executive. It has, however, been playing a more active role: in 1999 and 2000 the Supreme Court reprimanded the then prime minister, Sheikh Hasina, for making misleading statements about the judiciary and demanded that the executive branch consult with the chief justice in appointing High Court judges. The government is working on separating the judiciary from the executive branch under an order passed by the Supreme Court in December 1999. Successive governments have delayed carrying out the law. The Supreme Court in October 2005 turned down a government petition seeking another four-month extension—the 22nd since 1999—to separate the judiciary from the executive.

Citizens are equal before the law and free from arbitrary arrest and discrimination. However, detention without trial is allowed in a state of emergency under the Special Powers Act (SPA) 1974. In April 2002 the BNP-led government secured the passage of the Law and Order Disruption Crimes (Summary Trial) Act 2002. The Summary Trial Act provides for expeditious trials of those charged with offences ranging from traffic disruption to terrorism. Opposition activists claim that the government may use this law for political ends.

The judiciary

Emergency laws allow for detention without trial

10 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Political forces

The main political parties are the AL and the BNP. The AL, which spearheaded the war of independence under Sheikh Mujib, is now led by his daughter, Sheikh Hasina. The AL governed Bangladesh between June 1996 and July 2001, after 21 years in opposition. During this time it moved away from its previous commitments to nationalisation and economic self-sufficiency to support market-oriented economic policies. Despite the new party line, the AL contains politicians who strongly oppose leaving the economy to the private sector.

The BNP, founded by a former president, General Zia, in 1978, is led by his widow and the current prime minister, Mrs Zia. The BNP espouses Bangladeshi nationalism with anti-Indian and pro-Islamic nuances; however, these nuances have not been evident in its policymaking since coming to power in October 2001. Relations with India have remained stable. The BNP, with close links to business, is committed to fostering a market economy and liberal democracy, and encourages private-sector-led economic growth.

Differences between the AL and the BNP in terms of official economic policy had largely disappeared by the late 1990s. The AL plays up its leadership during the war of liberation in 1971, whereas the BNP appeals more broadly to nationalists, drawing support from both sides of the liberation war. Despite the lack of a clear ideological distinction between the parties, the bitter personal animosity between Mrs Zia and Sheikh Hasina sets the two parties apart.

Other active parties include the Jatiya Party (JP). The JP’s main faction is led by the deposed former president, General Ershad. It has experienced several damaging splits since 1997 because of its alternating support for the AL and the BNP. A splinter element of the JP is a partner in the BNP-led coalition government.

Social tensions seem to have worsened over the last decade. Economic deprivation and a sense of powerlessness, exacerbated by lawlessness in parts of the country, provide a conducive environment for ethnic, class and religious differences to be exploited by political activists. However, social tensions are contained by political elites in the capital, Dhaka, in whose interest it is to preserve the status quo. Although there are Islamist parties in government, they are minor parties in the coalition.

The Jamaat-e-Islami (Jamaat), which co-operated with Pakistani occupation forces during the liberation war in 1971, is now a partner in the BNP-led coalition government. It is a fundamentalist party that espouses an Islamic state. The BNP, which alone controls 195 out of the 300 seats in parliament, is well-placed to resist any extreme demands from its coalition partners. The Islami Oikyo Jote (IOJ), the fourth member of the BNP-led government, also seeks to implement Islamic doctrine, but draws more support from traditional religious groups. There are several leftist parties, for example, the Bangladesh Communist Party, which have entered a variety of shifting alliances over the years.

The Awami League

The Bangladesh Nationalist Party

The Jatiya Party

Social tensions seem to be worsening

The Islamist parties

Bangladesh 11

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

General election results (no. of parliamentary seats)

1996

1979 1986 1988 1991 Feba Jun 2001

Awami League (AL) 39 76 - 96 - 146 58

Bangladesh Nationalist Party (BNP) 207 - - 139 272 116 195b

Jatiya Party (JP)c - 153 251 35 - 31 14

Jamaat-e-Islami (Jamaat) - 10 - 18 - 3 17b

Others 54 61 49 12 - 4 16

a Boycotted by opposition parties; not all seats were filled as violence disrupted the election. b In 2001 the BNP-led alliance, comprising the BNP, a faction of the JP, Jamaat and the Islami Oikyo Jote, won 219 seats. c A grouping dominated by the JP faction led by General Ershadin 2001.

Sources: Election Commission; press reports.

With the passing of the People’s Representation Order 2001 (PRO 2001) in August 2001 the Election Commission (EC), a constitutional body responsible for holding elections, gained considerable autonomy to carry out its responsibilities. Under PRO 2001 the EC has wide powers to monitor elections.

Students play an active role in politics, both within the political parties and more generally. This stems from the important role they played in the liberation war. In 1990 the All-Party Students’ Union was instrumental in forging the alliance between the quarrelling opposition parties that ultimately toppled the government of General Ershad. However, the active role of students in national politics has come under fire in recent years, because violent elements, including non-students, are perceived to be dominating student politics.

The army has played a prominent role in Bangladeshi politics, starting with the war of liberation in 1971, but especially following the military coup in mid-1975. After the fall of General Ershad in 1990, however, the army withdrew from politics. In the run-up to the general election in June 1996 the chief-of-staff, Abu Saleh Mohammad, led a failed military revolt against the caretaker government. Since then the army has refrained from seeking a direct role in politics, and the government has steered the army towards playing a role in UN peacekeeping operations. However, the military continues to play an important role in the background. Many leading politicians in both major parties are former soldiers, and in the event of an extremely serious breakdown in law and order military intervention cannot be ruled out.

The civil service, which was instrumental in sustaining military or pseudo-military rule in 1975-90—a linkage that impeded the institutional development of the civil service—remains divided, politicised and corrupt. One reason for holding general elections under neutral caretaker governments is that many civil servants back one of the political parties in the hope of being awarded lucrative postings and other benefits.

In the run-up to the general election in October 2001 the caretaker government transferred more than 1,100 government officials from their posts, believing them to be partisan. Since winning the election the BNP-led government has devoted much effort to replacing officials across the country. Partly because

The Election Commission

Student politics

The role of the army

The civil service

Governments devote much effort to replacing bureaucrats

12 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

politicians lack credibility, the bureaucracy in Bangladesh has greater influence over policymaking than in comparable countries. The civil service, organised into more than two dozen cadre services, also suffers from serious conflicts between specialists and generalists.

Main political figures

Khaleda Zia

The leader of the Bangladesh Nationalist Party (BNP) and prime minister since October 2001, Mrs Zia was previously prime minister in 1991-96. The wife of a former president, General Ziaur Rahman, who was assassinated by a group of rebel military officers, she assumed the leadership of the BNP in 1981.

Sheikh Hasina Wajed

The leader of the Awami League (AL) and prime minister in 1996-2001, Sheikh Hasina is a daughter of Bangladesh’s founder, Sheikh Mujibur Rahman. She became the leader of the AL in 1981. Under her leadership, the AL returned to power in 1996 after 21 years in opposition and completed its five-year term of office on July 15th 2001.

General Hossain Mohammad Ershad

The leader of the main faction of the Jatiya Party (JP) and a former president. He overthrew the government of Justice Abdus Sattar in a bloodless military coup in 1982 and ruled as an autocrat until 1990.

Matiur Rahman Nizami

Mr Nizami leads Jamaat-e-Islami, Bangladesh’s largest Islamist party and a member of the BNP-led coalition government. A cabinet reshuffle in May 2003 saw Mr Nizami moved from the Ministry of Agriculture to become industry minister. Jamaat remains controversial because of its pro-Pakistani role in 1971.

Iajuddin Ahmed

Mr Ahmed was sworn in as president in September 2002. The previous incumbent, A Q M Badrudozza Chowdhury, had been forced to resign in June 2002 after just six months in office, following a disagreement with the BNP government.

Mohammad Saifur Rahman

Mr Rahman, the finance and planning minister, is one of the BNP’s veteran ministers. He has presented 11 national budgets as a finance minister and has played an important role in shaping Bangladesh’s monetary, fiscal and trade policies.

International relations and defence

Bangladesh became a member of the UN in 1974 and has been elected to the UN Security Council twice, in 1978 and 2000. It is a member of the South Asian Association for Regional Co-operation (SAARC) and the Non-Aligned Movement (NAM). It is also a member of the Organisation of the Islamic Conference (OIC), the Commonwealth of Nations and the World Trade Organisation (WTO). In addition to its leading role in regional and international organisations of developing countries, Bangladesh is a major contributor to UN peacekeeping missions.

Membership of international bodies

Bangladesh 13

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Relations with India have been strained since the BNP-led coalition took office in 2001. Various issues of contention between Bangladesh and India remain unresolved, including the sale of natural gas to India, Bangladeshi immigration into India, and the sharing of water from the Ganges river. Moreover, India is concerned that Bangladesh has become a haven for various insurgent groups fighting Indian rule in the north-east and that Bangladesh might turn away from its secular, tolerant traditions towards Islamic extremism. Domestic opposition within Bangladesh to rapprochement with India has remained high, but there is an increasing realisation of the potential benefits of improved relations, particularly as regards trade. Differences in the ethnic and religious composition of the two countries’ populations have been a source of tension. India has alleged large-scale illegal immigration from Bangladesh, but Bangladesh has countered that many of those identified by India as illegal immigrants are Bengali-speaking Indian Muslims. The dialogue between Bangladesh and India has continued under India's new Congress-led government. India’s prime minister, Manmohan Singh, has pledged to resolve all outstanding issues with Bangladesh through sustained co-operation and consultation.

Relations with Pakistan have improved since the establishment of diplomatic relations in 1974 on the basis of mutual recognition. The relationship is, however, strained by Pakistan’s refusal to take back around 500,000 Urdu-speaking people, known as Biharis (a large proportion of whom migrated to Pakistan from the Indian state of Bihar), who claim Pakistani citizenship. Relations with Myanmar have been under pressure since 1992, when around 250,000 Rohingyas—Muslims from the Arakan region of Myanmar—fled to Bangladesh in the vicinity of Chittagong, alleging persecution by the Burmese authorities. Most Rohingyas had returned by 1995, but about 20,000 still remain in camps around Cox’s Bazar, a beach resort 152 km south of Chittagong. Mrs Zia visited Myanmar in March 2003 and reached an agreement on the establishment of direct road links between the two countries’ capitals, Dhaka and Yangon. In 2003 a total of 3,200 Rohingya were repatriated to Myanmar. Médecins Sans Frontières, an international medical aid agency, reports that many of the repatriated refugees have since returned to Bangladesh.

Bangladesh and China signed an accord on mutual recognition in 1975. In July 2004 Bangladesh and China agreed to establish road links between the two countries through Myanmar to facilitate trade integration. The road links will connect the two countries through China’s south-western Yunnan province. On a visit to Bangladesh in April 2005 the Chinese prime minister, Wen Jiabao, called for a further strengthening of economic and political ties and referred to Bangladesh as “a time-tested friend” of China.

Japan has been Bangladesh’s largest bilateral donor in recent years, especially in providing assistance for infrastructural development. Trade relations have been less strong—Japan’s share of Bangladesh’s imports fell from 13% in 1990 to 6.7% in 2003. Meanwhile, Japanese trade with other South Asian countries has

Japan is the largest bilateral donor

Relations with China improve

Relations with India have been strained under the BNP

Relations with Pakistan and Myanmar are strained

14 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

flourished. Japanese direct investment into Bangladesh is weak compared with other South Asian countries.

Relations with the US have improved over the past two decades, with nearly all of Bangladesh’s heads of state paying official visits to the US. The US is one of Bangladesh’s biggest bilateral donors. The participation of Bangladeshi troops in the 1991 Gulf war coalition and Bangladesh’s support for the US war on terror since the September 11th 2001 terrorist attacks on the US have strengthened the relationship. However, the government has admitted that Islamist extremist groups operate within Bangladesh, and the government may in future take a harder line against them, despite the presence of Islamist parties in the ruling coalition.

In mid-2000 Bangladesh and the US began holding joint military exercises, to improve “interoperability” between their forces, presumably as a form of contingency planning. In recent years there has been substantial US direct investment into Bangladesh, almost all destined for natural gas exploration and power generation. The US is the largest importer of Bangladesh’s flagship export, clothing. Bangladesh’s market position in the US has, however, come under stress since the US granted concessionary market access to some Sub-Saharan African countries in 2000. In September 2004 Bangladesh and the US signed an agreement on the avoidance of double taxation in order to facilitate bilateral investment and trade.

The armed forces totalled 125,500 in 2004. Expenditure on defence has hovered at around 2% of GDP in recent years. The inclusion of Bangladeshi troops in UN peacekeeping forces around the world has given the army an international role and a new source of income, both for itself and the government. In October 2005 some 9,000 Bangladeshi nationals were serving in 12 UN peacekeeping missions, along with other staff from the air force and the navy, making the country the biggest contributor to UN in terms of troop numbers.

In 2000 the army began recruiting women for all officer ranks except for combat roles. Previously, recruitment of female officers had been restricted to the army medical corps. Almost one-third of Bangladesh’s army medical officers are female.

Defence forces Army 110,000

Navy 9,000Air force 6,500Total 125,500Paramilitary 63,200

Source: The International Institute for Strategic Studies, The Military Balance, 2005/06.

Bangladesh supports the US campaign against terrorism

Defence expenditure is capped

The army recruits women

Bangladesh 15

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Resources and infrastructure

Population

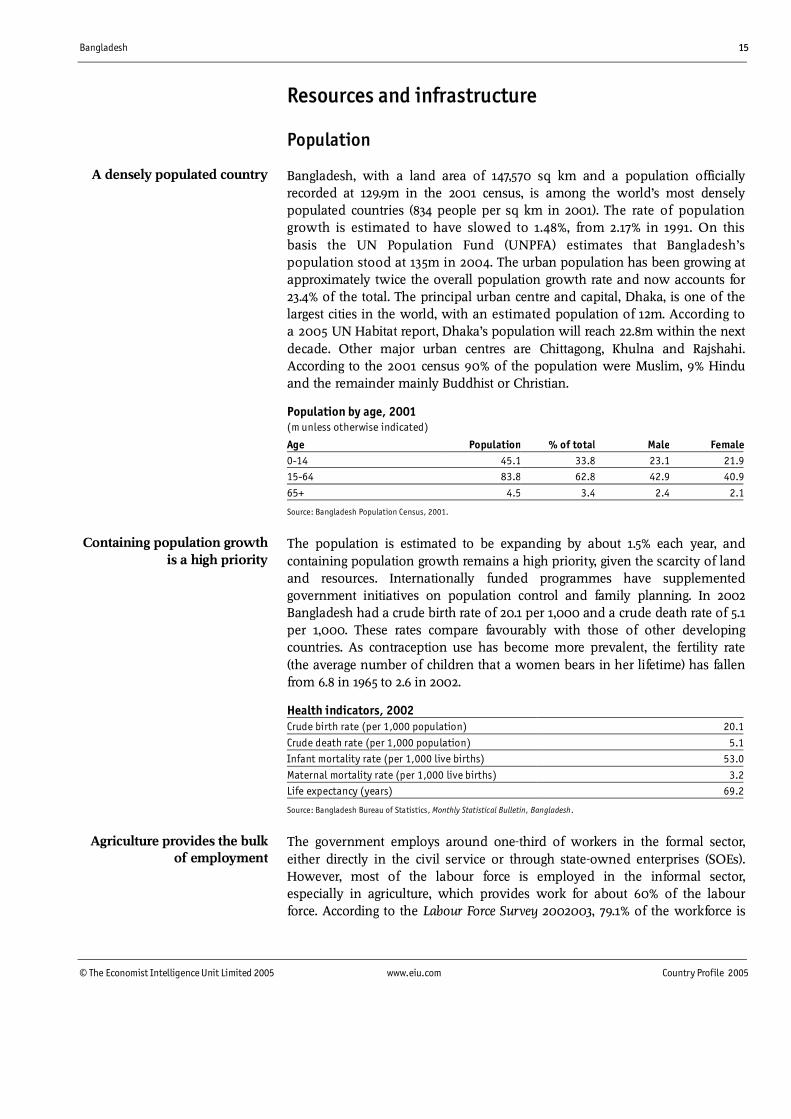

Bangladesh, with a land area of 147,570 sq km and a population officially recorded at 129.9m in the 2001 census, is among the world’s most densely populated countries (834 people per sq km in 2001). The rate of population growth is estimated to have slowed to 1.48%, from 2.17% in 1991. On this basis the UN Population Fund (UNPFA) estimates that Bangladesh’s population stood at 135m in 2004. The urban population has been growing at approximately twice the overall population growth rate and now accounts for 23.4% of the total. The principal urban centre and capital, Dhaka, is one of the largest cities in the world, with an estimated population of 12m. According to a 2005 UN Habitat report, Dhaka’s population will reach 22.8m within the next decade. Other major urban centres are Chittagong, Khulna and Rajshahi. According to the 2001 census 90% of the population were Muslim, 9% Hindu and the remainder mainly Buddhist or Christian.

Population by age, 2001 (m unless otherwise indicated)

Age Population % of total Male Female0-14 45.1 33.8 23.1 21.915-64 83.8 62.8 42.9 40.9

65+ 4.5 3.4 2.4 2.1

Source: Bangladesh Population Census, 2001.

The population is estimated to be expanding by about 1.5% each year, and containing population growth remains a high priority, given the scarcity of land and resources. Internationally funded programmes have supplemented government initiatives on population control and family planning. In 2002 Bangladesh had a crude birth rate of 20.1 per 1,000 and a crude death rate of 5.1 per 1,000. These rates compare favourably with those of other developing countries. As contraception use has become more prevalent, the fertility rate (the average number of children that a women bears in her lifetime) has fallen from 6.8 in 1965 to 2.6 in 2002.

Health indicators, 2002 Crude birth rate (per 1,000 population) 20.1

Crude death rate (per 1,000 population) 5.1Infant mortality rate (per 1,000 live births) 53.0

Maternal mortality rate (per 1,000 live births) 3.2Life expectancy (years) 69.2

Source: Bangladesh Bureau of Statistics, Monthly Statistical Bulletin, Bangladesh.

The government employs around one-third of workers in the formal sector, either directly in the civil service or through state-owned enterprises (SOEs). However, most of the labour force is employed in the informal sector, especially in agriculture, which provides work for about 60% of the labour force. According to the Labour Force Survey 2002003, 79.1% of the workforce is

A densely populated country

Containing population growth is a high priority

Agriculture provides the bulk of employment

16 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

employed in the informal sector. Of these, only 9.8% are employed in the manufacturing sector, according to the survey.

The number of Bangladeshis working abroad and remittances from those employed abroad have been increasing since the mid-1980s. Whereas only 70,000 skilled and unskilled persons obtained employment abroad in 1985/86, more than 250,000 Bangladeshis now do so each year, bringing the total number working abroad in 2005 to around 3m. Annual remittances from those abroad amounted to US$3.8bn in 2004/05, according to statistics released by the Bangladesh Bank (BB, the central bank). The importance of remittance inflows to the economy is likely to be far greater than reflected in official data, as large sums of money are thought to enter the country through unofficial channels.

The Middle East accounts for the bulk of job opportunities for Bangladeshis overseas. In recent years about 65% of total remittances originated from the Middle East, with more than one-third coming from Saudi Arabia. Other major transfer inflows came from countries with large Bangladeshi expatriate communities, such as the US and the UK. Substantial inflows of remittances are crucial to Bangladesh’s macroeconomic stability, as they have traditionally offset a large proportion of the country’s trade deficit and its services and income account deficit.

Education

The literacy rate among adults (those over 15 years of age) increased to 47.5% in 2001, from 31.5% in 1985. Notwithstanding major strides in primary and secondary education since the 1980s, low adult literacy continues to act as a break on faster economic development. Large disparities remain between the urban and rural populations and between males and females, but the gaps are narrowing. The government is the main provider of primary education, while private schools predominate in secondary education. Primary education was made universal, compulsory and free in 1993. Boys are entitled to five years of free schooling and girls to ten years (because families are less willing to pay to educate their daughters).

As a result of increased budgetary allocations, the employment of female teachers, stipends for female students and a food-for-education programme, the level of enrolment in primary schools increased sharply in the 1990s. The number of primary school children increased from 12m in 1990 to 17.7m in 2001, and the proportion of female students rose from 44.7% to 49.1% over the same period. However, fewer than half of all children complete five years of primary education. The poor quality of elementary education is attributable to badly trained or absentee teachers, large classes, and a shortage of books.

Secondary education is provided largely by the private sector. In 2004 there were 16,171 secondary schools with 7.9m students, about half of whom were female. At the higher level, many vocational and technical colleges and institutes are not well attended. Universities receive generous government subsidies but generally produce poor-quality graduates at high cost.

Many Bangladeshis seek work overseas

The literacy rate is improving

Few children complete five years of primary education

Provision of secondary education is largely private

Bangladesh 17

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Health

Medical facilities are extremely scarce. In 2001 there were 32,022 hospital beds, 32,498 registered doctors, 18,135 registered nurses and 15,794 midwives in the public sector, which provides more than 90% of health services. Only 12% of births were attended by skilled health personnel in the second half of the 1990s.

Annual spending on healthcare and family planning remained at around 1% of real GDP in the early 2000s, although there have been some modest increases in public spending. Access to medical services is more limited in Bangladesh than in neighbouring countries. Government health services are poor, and only about 12% of serious cases are referred to public health facilities. Poor-quality and poorly regulated private clinics have proliferated in both urban and rural areas. Non-governmental organisations (NGOs), such as the Bangladesh Rural Advancement Committee (BRAC), have also been providing health services.

Bangladeshis suffer from some of the highest malnutrition levels in the world. Major problems include childhood protein-energy deficiency, maternal under-nutrition, as evidenced by low weight, short stature and anaemia in expectant and nursing mothers, and micronutrient deficiencies, particularly in vitamin A, iron and iodine, which affect all ages. However, the prevalence of child malnutrition has gone down substantially over the last decade. The proportion of children aged 6-71 months classified as underweight has declined nationally from 72%in 1985/86 to 51% in 2000.

Natural resources and the environment

The land is mostly flat, although there are some hilly areas in the north-eastern and south-eastern regions. Much of the land is intersected by the numerous waterways of the Ganges (known locally as the Padma) delta and the Brahmaputra river (known locally as the Jamuna). The annual flooding of the land provides rich alluvial soils. The monsoon climate results in annual average rainfall that is among the world’s heaviest, exceeding 2,540 mm and falling mainly between July and October. Every year there is massive flooding during the monsoon season, and soil erosion and changes to river channels pose constant problems. Natural disasters are a fact of life, as many Bangladeshis live in precarious dwellings close to rivers and the coast. The low-lying areas at the mouth of the Ganges delta are at risk of tidal surges and cyclones.

Most of Bangladesh’s soil is rich and fertile. In 2003 forests covered 1.97m ha, or 13% of the total land area, according to the government. However, much of the land officially classified as forest is given over to plantations. About 67% of the total land area is cultivable, and around 75% of the planted crop area is devoted to rice crops. A large and growing proportion of the cropped area is subject to multiple cropping. Weather conditions, improved seed varieties and irrigation facilities permit two or three rice crops each year in the 70% of cultivable land that is not subject to serious flooding. In the remaining low lands, only one or

Natural disasters are a fact of life

Health services are poor

Spending on healthcare is flat

Malnutrition is a common problem

18 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

two crops each year are planted. Bangladesh has little additional land that can be brought under crop production.

The quality of drinking water

Arsenic poisoning in rural areas

Groundwater, the primary source of drinking water for much of the rural population in Bangladesh, is contaminated with arsenic, affecting more than 21m people in 61 of the 64 districts in Bangladesh. Recent reports suggest that the intensity of arsenic contamination in groundwater is extremely high—far above World Health Organisation (WHO) safety standards—in 45 south-western subdistricts (out of 460 subdistricts in Bangladesh). At least 200,000 people are suffering from arsenic-linked diseases. The exact source of the arsenic pollution is a controversial subject, but many experts and practitioners believe that it is geological: arsenic seeps into groundwater under naturally occurring aquifer conditions. Although evidence of arsenic contamination in groundwater had begun to surface in the 1980s, the issue—in terms of being a likely environmental disaster—only began to receive broad public attention from the mid-1990s.

Bangladesh is poor in non-energy minerals. Known resources include natural gas, limestone, glass sand and certain heavy minerals such as trace deposits of uranium and thorium. There are five major coal deposits in the country, but much of the coal lies too deep for commercial exploitation. The largest coal mines are Khalashpir (Rangpur), which has reserves estimated at 685m tonnes; Jamalgonj (Joypurhat), with reserves of 1.1bn tonnes; and Barapukuria (Dinajpur), with reserves of 389m tonnes. In 1995 deposits of high-quality bituminous coal were found at Dighipara (Dinajpur), which probably contains the largest coal reserves in the country. In 2005 the government entered into negotiations with multinational companies, including Tata of India and a UK-based concern, Asian Energy, to develop and exploit coal deposits in Dinajpur division.

Transport, communications and the Internet

Poor transport facilities and infrastructure are a major hindrance to economic development. A 2005 Investment Climate Assessment by the World Bank identified poor quality and poorly managed infrastructure as the major deficiencies in Bangladesh’s investment climate, together with security and law and order. Road connectivity between the country’s major urban centres is poor and unreliable. The road network in Dhaka, the capital, is also poor—there are only two flyovers in the whole city—making it one of the most congested cities in the world. The government is investing in the infrastructure with the support of multilaterals, but the challenges remain huge, given the intense population pressure in the decades ahead. There is concern that the government is devoting an excessive proportion of the budget to transport, specifically on projects that often have the potential for corruption or inefficiency. That said, some progress has been made in recent years, and

Non-energy mineral reserves are scarce

Transport infrastructure is a major problem

Bangladesh 19

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Bangladesh’s transport road infrastructure has improved. The road network now connects every district and subdistrict administrative centre, even those in remote areas.

Bangladesh had 2,706 km of railways in 2003, operated by Bangladesh Railways, a state-owned enterprise with monopoly rights, compared with 2,884 km in the early 1980s and 2,874 km in the early 1970s. Over the years the length of railways has declined and the standard of service has deteriorated, whereas the volume of freight and the number of passengers transported by road has increased.

The passenger railway service has been in decline since the country’s independence in 1971, owing to poor service and the phenomenal growth of road networks. Bus services, largely private, have emerged as a challenge to the railways by connecting remote places and providing better services.

Bangladesh had a road network that extended about 20,799 km in 2001, compared with 14,104 km in 1991. There are 3,086 km of national highways (about 15% of total road length), 1,751 km of regional highways (8%), with feeder roads accounting for the remaining 15,962 km. In addition, local governments maintain more than 16,000 km of rural roads, but only 8,546 km of these are tarred. In many parts of Bangladesh animal-driven carts still provide the main means of land-based transport for shorter distances. Despite the problems of road transport, more than 65% of all freight and more than 70% of all passengers are transported by road. Both the rail and road network tend to suffer severe damage in years of major floods, as was the case in 1998 and in 2004.

Waterways have become less important as a means of transport because of the declining navigability of some rivers and the poor performance of the largely state-operated system. There are about 8,300 km of navigable inland waterways, although this drops to 3,800 km in the dry season. The waterway network is particularly important as a transport link to some of the most remote parts of the country. Badly needed improvements to waterways include more dredging programmes, better boat safety regulations and the privatisation of some of the ferry and cargo routes. In 2005 hundreds of people were killed in several ferry accidents, bringing the number of fatalities in such accidents to at least 3,000 since 1997, according to official statistics.

There are two major seaports, at Chittagong and Mongla, and smaller inland ports at Dhaka, Narayanganj, Chandpur, Barisal and Khulna. Chittagong is the largest of the seaports, handling around 89% of seaborne merchandise imports and 85% of merchandise exports in 2001/02. The operational efficiency of the port is poor. Waiting times for ships for berths increased from 0.74 days in 1996 to 2.25 days in 2000. Chittagong is well connected to inland road, rail, river and air routes. Container handling at Chittagong port increased rapidly from 150,000 twenty-foot equivalent units (TEUs) in 1992/93 to 490,386 TEUs in 2000/01. The quantity of cargo handled also increased from 1.4m tonnes to 4.6m tonnes during the same period (the tonnage of imports passing through

The railways

Bus services

The road network

Waterways

Unions oppose plans to build private container terminals

20 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

all ports is more than eight times that of exports). The port authorities are building additional berth facilities for increased container services and a new container yard. The labour unions are, however, strongly opposed to private-sector plans to build two modern container terminals, one at Patenga in Chittagong and the other at Pangaon in Dhaka. At present, the competitiveness of Bangladeshi exports is severely constrained by the poor quality of service at the country’s main ports.

Bangladesh Shipping Corporation (BSC), a loss-making state-owned company, has handled around 7-9% of Bangladesh’s seaborne merchandise trade in recent years compared with an 18% share of imports and a 14% share of exports in the early 1990s. Private international shipping companies handle the rest of Bangladesh’s merchandise trade.

The national air carrier, Bangladesh Biman, has hitherto had a monopoly on international routes, but the government announced in June 2003 that domestic private airlines would be given the right to ply international routes too, following a review of air-service agreements with other countries. In January 2004 GMG Airlines, a domestic private carrier, was granted an operating licence for international flights, including the routes from Dhaka to the Sri Lankan capital, Colombo, via Chennai in southern India; from Dhaka to the capital of the Maldives, Male, via Colombo; and from Chittagong to Chiang Mai in northern Thailand. In September 2004 GMG Airlines started operating flights between Chittagong and Calcutta, in India. GMG, which began its domestic flight operations in 1998, now operates 32 daily flights to various destinations within Bangladesh. The national carrier Biman currently serves 29 overseas and eight domestic destinations, including direct flights from Dhaka to New York and Tokyo.

In 2004/05 Biman carried more than 1.5m passengers and around 30,000 tonnes of cargo. The carrier made a loss of Tk3bn (US$50) in 2004/05. Plans to commercialise Biman (initiated in 2000), to turn it into a profit-oriented business by forming a strategic partnership with a foreign company, remain stalled. The government blames uncertainties in the aviation industry since the terrorist attacks on the US in September 2001 for the lack of progress. The carrier faces many challenges. On international routes is coming up against increasing competition from private international airlines, and domestically the only private domestic carrier, GMG, has successfully extended its operations. Biman’s employees’ unions yield considerable power. For example, strike action led to major flight disruptions in September 2005. Rising fuel costs in recent years have added to the financial pressure. In October 2005 the state-owned Bangladesh Petroleum Cooperation (BPC) threatened to stop supplying fuel to the cash-strapped carrier, which owes BPC about US$80m.

Bangladesh has 16 operational airports, three of which are open to international flights. The main international airport is Zia International in Dhaka; the other two international airports are in Chittagong and Sylhet. There were 14 international airlines serving Dhaka’s Zia International Airport as of October 2005. These include five carriers from the Gulf, three from the South Asia

Biman is recovering from bad purchasing decisions

International air connectivity has improved

The state-owned shipping company is losing ground

Private airlines will fly international routes

Bangladesh 21

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

region (Pakistan, India and Bhutan), and another three from South-east Asia (Malaysia, Singapore and Thailand). British Airways continues to be the only European carrier to serve the Bangladeshi capital. Eastern China Airlines started operating direct flights between Dhaka and Kunming in China in May 2005. In mid-June the Indian flag carrier, Air India, resumed its flight operations to Dhaka, ending a 12-year suspension of direct flights between the two countries.

Bangladesh, where only 1.56 of every 100 people had access to telecommunications services in 2003, has the lowest teledensity in South Asia and one of the lowest in the world. The number of telephones increased from 220,000 in 1991 to around 1m in 2003. Fixed telephone lines are run by the state telecoms monopoly, Bangladesh Telegraph and Telephone Board (BTTB), and two private companies, Sheba Telecom and the Bangladesh Rural Telecom Authority (BRTA). Bangladesh has 0.55 fixed-line telephones per 100 inhabitants, whereas the number of mobile phones per 100 people stands at 1.01. The number of mobile phones—provided by four operators in foreign joint ventures—stood at about 2.3m in 2003.

A phased programme to install digital telephone exchanges at all subdistrict levels is under way. In recent years V-SAT (very small aperture terminal, a data-transmission system using satellites) and data network systems have been established, enabling Internet communication and other modes of data communication for both domestic and international use. The government has also begun projects to set up a high-technology industrial park and an information-technology village to encourage both domestic and international investment in the computer software sector.

The main telecoms operator is the state-owned BTTB. Private firms operate mobile-phone services, rural telephone exchanges, Internet and e-mail services, and paging and operator-assisted services. There are four private mobile-phone companies in Bangladesh: Bangladesh Telecom (Citycell); Grameen Phone (owned by Grameen Bank, a local bank); Telecom Malaysia International (owned by the Malaysian state-owned Telekom Malaysia); and Sheba Telecom (owned by Orascom, an Egyptian-based mobile-phone company). Grameen Phone is the market leader in mobile telephony, with a market share of more than 70%. There are also two private companies specialising in rural areas—the Bangladesh Rural Telecom Authority (BRTA, a former state-owned enterprise) and Rural Telecommunications (a subsidiary of Sheba Telecom). Bangladesh has 60 Internet service providers, with around 243,000 users at the end of 2003.

Postal services are extremely poor and archaic. In 2003/04 Bangladesh had only 9,860 post offices, of which 794 were in urban centres and 9,066 in rural areas. Only 164 postal stations, mostly in urban areas, provided guaranteed express post. Bangladesh had agreements for international express mail service (EMS) with 49 countries, and for international money order service with 13 countries. In August 2000 the postal department introduced e-mail services in some selected urban centres.

Postal services are archaic

The government is promoting the software sector

Private involvement in telecoms is growing

Low telephone density

22 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

There is a thriving local press with over 100 daily newspapers, about a dozen of which are published in English. The press has considerable freedom, although reporting restrictions have been imposed during periods of political unrest. Until recently Bangladesh Radio and Bangladesh Television were state monopolies, controlled directly by the government. In mid-2000 parliament passed a law providing for the autonomy of the state-owned media, but critics say that the act falls short of granting real autonomy, as the government still appoints the board members, and the broadcasters depend on the government for financial support. In 2004 the government signalled that it may allow more private satellite television channels to go on air. Currently there are three private television channels in Bangladesh: ATN Bangla, Channel i and NTV. International television channels are permitted to operate in Bangladesh through satellite channels; there are no foreign-owned broadcasters.

Energy provision

Electricity generation per head is among the lowest in the world, at about 154 kwh per year. There is huge unmet commercial demand for energy, and the lack of reliable sources of electricity has deterred foreign investment and held back economic growth. Current dependable generating capacity is estimated to be 3,950 mw. The shortfall of generating capacity is estimated to be around 2,500 mw in the next five years, according to the Asian Development Bank. Around 85% of households have no electricity, and only about 60% of the electricity generated is actually paid for. Moreover, system losses are high, at 30% of electricity generated in 2004. Electricity is mostly generated from gas—about 94%—and the remainder comes from hydroelectricity.

The power crisis is likely to persist, despite the addition of new generating capacity since 1997. Peak-hour demand runs at around 3,600 mw. Bangladesh’s Power System Master Plan envisages a doubling of generating capacity by 2010 to meet the increase in electricity demand. Load-shedding (the deliberate switching off of electricity supply to a service area as part of a planned rotation), especially in the summer, is quite common. Factories are often forced to run fewer shifts or to opt for their own expensive generators, driving up the cost of production. In 1996 the government created two new agencies—the Power Grid Company of Bangladesh (PGCB) and the Dhaka Electricity Supply Company (DESCO)—separating power transmission from power generation.

The government issued the Private Sector Power Generation Policy of Bangladesh in 1996 to attract more foreign investment to meet the rising power demand. Among the first so-called Independent Power Projects (IPPs) were a 360-mw gas-fired plant at Haripur, which began operation in October 2001, and a 450-mw gas-fired plant at Meghnaghat, which began operation in November 2002. In May 2005 a US-based company, Global Vulcan Energy International, announced plans to build several power plants with a total generating capacity of 1,800 mw. In 2005 India’s Tata Group proposed a 1,000-mw coal-fired power plant.

The local press is thriving and has considerable freedom

Electricity provision is extremely poor and unreliable

The power crisis is likely to persist

Private-sector power plants are coming online

Bangladesh 23

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

Power capacity and production (mw)

1999/2000 2000/01 2001/02 2002/03 2003/04Installed capacity 3,711 4,005 4,230 4,710 4,710Dependable capacity 2,665 3,033 3,300 3,600 3,700

Highest production 2,665 3,033 3,218 3,458 3,622

Source: Bangladesh Economic Survey, 2004.

Bangladesh has abundant reserves of natural gas. The stock of gas reserves, according to data from the Ministry of Finance, is estimated at 28.4trn cu ft of gas, of which 20.5trn cu ft is considered recoverable. Gas reserves are thought to be sufficient to meet domestic demand for the next 30 to 50 years. However, the precise extent of gas reserves is a matter of considerable dispute. Estimates by the Oil and Gas Journal put the country’s proven natural gas reserves at 10.6trn cu ft, while the state-owned Petrobangla puts them at 15.3trn cu ft. The US Geological Survey has estimated that Bangladesh has an additional 32.1trn cu ft of “undiscovered reserves.” Demand continues to rise, even though a large proportion of the population does not have access to gas. Petrobangla, the state-owned oil and gas corporation, forecasts that demand for gas will increase to 529.9bn cu ft/year by 2006/07. Delays in the construction of the Ashuganj-Manhardi gas pipeline, originally planned to come into operation in June 2004, forced the government to ration gas supplies in October 2005. Completion of the pipeline has been rescheduled for June 2006. About 50% of the gas produced is used for power generation, followed by fertiliser production, house-hold cooking and other industrial and commercial uses. The Bibiyana gas field, with a capacity of 200m cu ft per day, will begin operation in 2006. The Moulvibazar gas field, with a capacity of 70m cu ft/day, is due to become operational in 2010.

To encourage gas exploration, the government opened the gas sector to foreign investment in the mid-1990s and divided the country into 23 blocks. After two rounds of bidding the government signed eight production-sharing contracts (PSCs) with international oil companies covering gas exploration in 12 blocks. A US company, Rexwood Oakland, has discovered gas at the Sangu gas field in the Bay of Bengal and has supplied gas to the national grid since 1998. Another US company, Occidental, has discovered gas in two gas fields: Bibiana and Moulovi Bazar in Sylhet. In 2004 an Irish exploration and production company, Tullow Oil, discovered gas in Block 9, situated close to Dhaka. In August 2005 the government extended the PSC of a UK-based company, Cairn Energy, for Block 16 in the Bay of Bengal until May 2008.

The bidding process has, however, drawn criticism at home and abroad, and several PSCs, believed to have been hurriedly concluded by the Awami League (AL) government that stepped down in July 2001, have been shelved for further scrutiny. Critics charge that the bidding process has not been transparent, that Petrobangla is corrupt, and that Bangladesh should not export gas until it has secured a sufficiently high level of reserves to support domestic use in the future.

Foreign investment in exploration is encouraged

The bidding process is criticised

Natural gas reserves are plentiful

24 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Gas exports

Pressure for exports to India mounts

The government has come under increasing pressure in recent years to allow gas exports to India. Foreign investors involved in gas exploration in Bangladesh are finding the domestic market too small to recoup their investments. In addition to pressure from the international oil companies, the World Bank and the Asian Development Bank (ADB) have argued that revenue from gas exports would improve Bangladesh’s fragile foreign-exchange position and increase foreign direct investment. The World Bank and the ADB maintain that current recoverable gas reserves would be sufficient to meet Bangladesh’s domestic gas demand for 35-40 years at the current rate of consumption. If gas consumption grows by 8-10% each year, proven gas reserves would be adequate for 15-20 years for the country, according to the banks. The banks also rule out options such as using gas resources for domestic power generation or fertiliser production as a means of generating foreign exchange, and assess pipeline exports to India as the best option. India is expected to have a market of around 250m-300m cu ft/day within five to six years. Until the last general election, held in October 2001, both the Awami League (AL) and the Bangladesh Nationalist Party (BNP) were committed to gas exports only after it had been established that Bangladesh had at least 50 years of reserves for domestic use. Since its decisive election victory the BNP, a pro-business party, seems to have leaned away from a strong commitment to this condition and set up two committees to examine technical and economic aspects of the issue. The results of the committees’ deliberations have failed to provide clear grounds for a decision either way, and it is apparent that the decision is ultimately a political one. Supporters of gas exports will have to overcome the influence of the nationalists, who want to retain this natural resource for domestic use and who are especially opposed to allowing India to make use of it.

The economy

Economic structure Main economic indicators, fiscal year 2004/05 (Jul-Jun)a Real GDP growth (at constant 1995/96 market prices; %) 5.4

Consumer price inflation (av; %)b 3.2Current-account balance (US$ m)c -226.1Exchange rate (av; US$) 61.5

Population (m)d 135.2Foreign debt (year-end; US$ bn) 20.4

Foreign-exchange reserves (US$ bn)e 2.9

a Actual. b Calendar year 2004. c Estimate. d 2003/04 fiscal year estimate. e August 2005.

Source: Economist Intelligence Unit.

Bangladesh’s economy depends heavily on the agricultural sector, which accounts directly for 20% of GDP and provides employment for more than half of the labour force. Moreover, many other industries depend on the purchasing power of the millions of people employed in agriculture. However, the country

Agriculture plays a central role

Bangladesh 25

© The Economist Intelligence Unit Limited 2005 www.eiu.com Country Profile 2005

is one of the most densely populated in the world, and there is little room to expand the area used for crop cultivation. Rice production, which accounts for 70% of the sector’s value added, has risen by about 150% since the mid-1970s, driven largely by productivity increases, although the area under cultivation has risen by a mere 5%. Bangladesh has virtually achieved food self-sufficiency and has diversified the crop base (wheat is now the largest crop after rice). However, unpredictable climate conditions—flooding and droughts—regularly undermine production plans and targets, disrupting the economy and necessitating food imports.

Bangladesh imports most of its required intermediate inputs for the manufacturing process. This is particularly true for the garment sector. Moreover, the agricultural sector relies heavily on imported fertiliser. This strong reliance on imports limits the value added in the domestic production process, exposes firms to fluctuations in exchange rates and the price of raw materials, and has adverse consequences for the balance of payments. Although natural gas production is increasing, Bangladesh still runs a heavy fuel import bill. The government is attempting to diversify the economy and the export base by promoting industries such as information technology and agricultural processing, but these programmes have had limited success.

Comparative economic indicators, 2004 Bangladesh a India a Pakistan b Sri Lanka b Vietnam b

GDP (US$ bn) 56.0 c 672.0 d 96.0 c 20.0 45.0

GDP per head (US$) 402 c 622 d 626 c 975 548

GDP per head at PPP (US$) 1,728 c 3,139 d 2,211 c 3,385 2,737

Consumer price inflation (av; %) 3.2 3.8 7.4 7.6 7.8

Current-account balance (US$ bn) -0.2 1.1 -0.9 -0.6 -1.1

% of GDP -0.4 0.2 -0.8 -3.0 -2.5

Exports of goods fob (US$ bn) 8.2 80.2 13.4 5.7 25.8

Imports of goods fob (US$ bn) -11.1 -97.5 -17.9 -7.1 -28.3

External debt (US$ bn) 20.4 118.9 41.8 a 10.9 17.7

Debt-service ratio, paid (%) 7.8 9.6 20.7 9.3 3.1

a Estimates. b Actual. c Fiscal year (July-June). d Fiscal year (April-March).

Source: Economist Intelligence Unit, CountryData.

The manufacturing sector accounts for around 16% of GDP. Industrial activities are mostly centred in Bangladesh’s two largest cities, Dhaka and Chittagong. The government has set up export-processing zones (EPZs) in both cities and some other parts of the country to attract foreign investors, and offers generous tax concessions to firms that locate to these cities. Large enterprises—those that employ more than ten workers—account for around 70% of the real value of total industrial output.

On the expenditure side, private consumption accounts for around 76% of GDP, a large proportion of which is spent on basic goods such as food. Investment accounts for only 24% of GDP. Bangladesh’s net imports of goods and services are equivalent to a deficit of around 5% of GDP each year, which is financed by remittances from Bangladeshis working abroad and external financial assistance, mainly from international institutions and other countries.

The economy is dependent on imports

Industry is centred in the two main cities

Private consumption drives GDP

26 Bangladesh

Country Profile 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

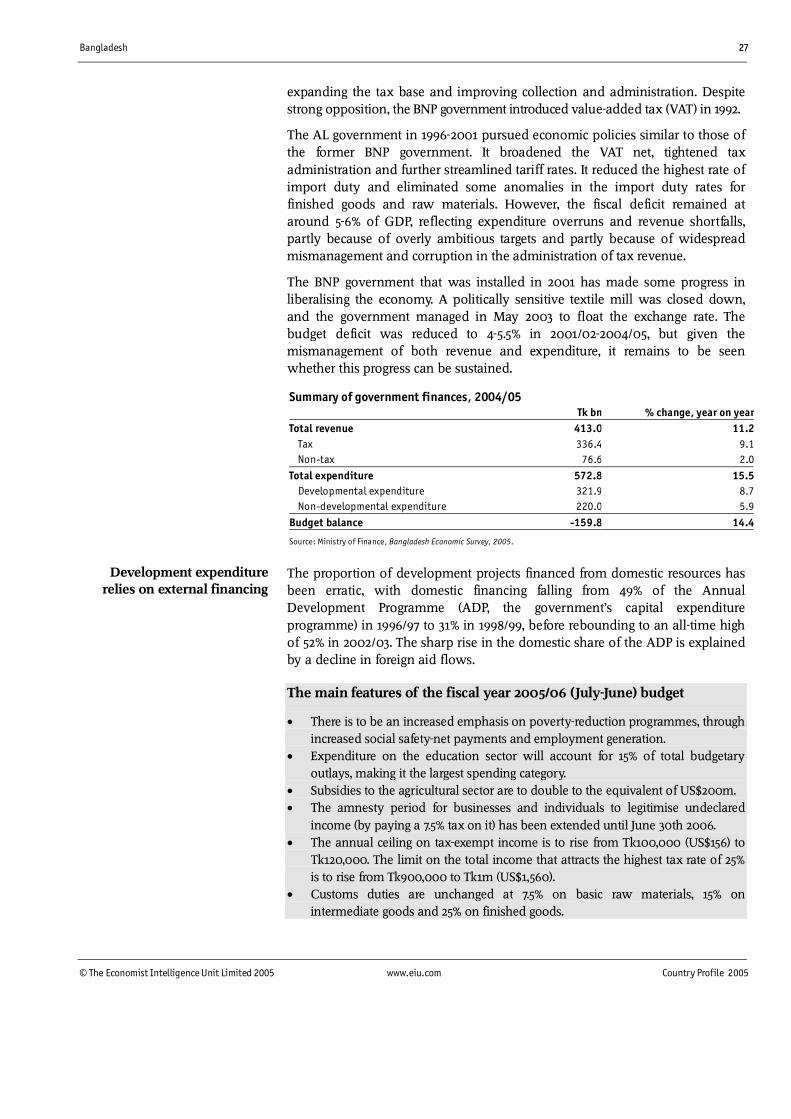

Economic policy

One basic problem for policymakers in Bangladesh is how to raise the rate of economic growth in a country where a substantial proportion of the population lives below the subsistence level. Although the incidence of poverty is high, it is declining. According to the Household Income and Expenditure Survey 2000, released in June 2002, 44.3% of the population lived below the poverty line in 2000, compared with 58.8% in 1991. The poverty line is defined as being able to afford to buy food providing a daily intake of 2,122 calories. While the percentage of the total population living in poverty has declined in the last decade, the absolute number of people living in poverty has changed little because of continued population growth. In absolute numbers, Bangladesh has the third-highest number of poor people in the world (after India and China), according to the World Bank.