Atlas Pipeline Partners, L.P.

Pinnacle MLP Conference

March 28, 2013

Tulsa, OK

THE WORDS “BELIEVES, ANTICIPATES, EXPECTS”, “PRO FORMA” AND SIMILAR EXPRESSIONS ARE

INTENDED TO IDENTIFY FORWARD LOOKING STATEMENTS.

SUCH STATEMENTS ARE SUBJECT TO CERTAIN RISKS AND UNCERTAINTIES, WHICH COULD CAUSE

ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE PROJECTED IN THE FORWARD LOOKING

STATEMENTS.

FACTORS THAT COULD CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY FROM THE FORWARD-

LOOKING STATEMENTS INCLUDE THOSE FACTORS LISTED ABOVE, FINANCIAL PERFORMANCE,

REGULATORY CHANGES, CHANGES IN LOCAL OR NATIONAL ECONOMIC CONDITIONS AND OTHER

RISKS DETAILED FROM TIME TO TIME IN THE PARTNERSHIP’S PERIODIC REPORTS FILED WITH THE

SEC, INCLUDING QUARTERLY REPORTS ON FORM 10-Q, CURRENT REPORTS ON FORM 8-K AND

ANNUAL REPORTS ON FORM 10-K; PARTICULARLY THE SECTION TITLED RISK FACTORS. READERS ARE

CAUTIONED NOT TO PLACE UNDUE RELIANCE ON THESE FORWARD LOOKING STATEMENTS, WHICH

SPEAK ONLY AS OF THE DATE HEREOF.

THE PARTNERSHIP UNDERTAKES NO OBLIGATIONS TO PUBLICLY RELEASE THE RESULTS OF ANY

REVISIONS TO FORWARD LOOKING STATEMENTS, WHICH MAY BE MADE TO REFLECT EVENTS OR

CIRCUMSTANCES AFTER THE DATE HEREOF OR TO REFLECT THE OCCURRENCE OF UNANTICIPATED

EVENTS.

2

Atlas Pipeline Partners, L.P. (NYSE: APL)

3

Assets located in enviable basins,

including Permian, Woodford Shale, and

Mississippian Lime with access to other

basins through newly-acquired treating

business

Units currently yielding approximately 6.7%

to unitholders based on annualized recent

distribution of $0.58 per unit for 4Q 2012*

Strong margin protection of cash flow

through risk management program

Strong balance sheet versus midstream

industry peers enables opportunistic

pursuit of organic and external growth

As of 2Q 2013, overall processing

capacity will have doubled company-wide

to almost 1.3 Bcf/d** over past 2 years

Growth-Oriented Midstream Gathering

& Processing MLP with 13 Processing

Plants and over 10,100 miles of

gathering pipelines

20% interest in WestTX LPG NGL

pipeline (operated by Chevron)

Recently purchased Cardinal

Midstream (named Arkoma) for $600

million to add a fourth major gathering

and processing system as well as a

treating business located in other

enviable basins, which could create

incremental midstream opportunities

Completed significant expansions at

WestOK and Velma and major

expansions to come in 2013-2014 at

WestTX and Arkoma

* Market data as of 3/26/2013 ** On a gross basis as compared to 2Q 2011

Disciplined Approach to Managing our Business - Conservative Financially and Aggressive Operationally

APL and The Atlas Family Know how to Create MLP Value

4

Atlas was the #1 MLP (ATLS) and #1 Midstream MLP (APL) in the U.S. over the past 3 years

5

Diversified Asset Base in Oil / NGL-Rich Areas Provides Significant Exposure to Increasing Drilling Activity

6

Gas Processor Processing Capacity

(mmcf/d)

Gas Processor Processing

Plants

Enogex Products LLC 1,120 ATLAS PIPELINE PARTNERS 9

ATLAS PIPELINE PARTNERS 838 DCP Midstream 9

DCP Midstream 757 Enogex Products LLC 8

Enbridge G & P 450 Copano/Scissortail Energy LLC 6

ONEOK Partners, LP 448 ONEOK Partners, LP 6

Devon Gas Services LP 400 Enbridge G & P 3

MarkWest Energy Partners, LP 225 Mustang Gas Products, LLC 3

Copano/Scissortail Energy LLC 208 Superior Pipeline Company 3

TOTAL IN OKLAHOMA 5,314 mmcf/d TOTAL IN OKLAHOMA 70 plants

APL is one of the Largest Natural Gas Processors in OK

Source: EIA and company research; Data as of 4Q 2012 Pictured: APL’s new Arkoma assets

APL Becomes a Major Player in the Mid-Continent over the past 3 years

41

192

877

266 277 345

2010 2011 2012

Growth in OK Investment

Total APL Employees

Total OK Investment ($mm)

Strategic Focus & Business Initiatives

Capital

Discipline

De-risk the

Business

Maintain and

Preserve

Balance Sheet

Strategically

Grow our Asset

Base

Targeting 20-25%+ IRR on growth capital

Utilize credit profile and liquidity to fund highly accretive projects at attractive rates of return

Major organic expansions completed or in progress across all systems, most of which are above rate-of-return

target

Physically and Financially

Reduced gross-margin risk by shifting from keep-whole to percentage of proceeds and fee-based contracts

Fee-based NGL transportation pipeline and long-term, fee-based gathering and processing contributes fixed-fee

cash flow with no direct commodity price exposure

Implement sound fiscal prudence – liquidity, leverage, capital, and distribution coverage

Deploying capital with low-cost revolving credit financing to spur organic expansion prior to realizing cash flows

Future expansions and potential acquisitions will be appropriately funded to maintain balance sheet strength

Recent purchase of Cardinal Midstream (now the Arkoma system) funded with over 50% equity

Organically and Opportunistically

Focusing on organic growth expansions and M&A opportunities in liquids-rich or strategic areas with accretive

returns

Recent $600 purchase of Arkoma system adds heft and potential synergies in Woodford shale to compliment

Velma’s footprint

7

Partnership produced strong 2012 results as the result of record gathered volumes

Company-wide organic capital expansions plus addition of Cardinal Midstream (now the Arkoma System) in 2012/13 expect to contribute significantly to EBITDA growth in 2013 and beyond

2011 2012 Growth

Adjusted EBITDA

$181 mm $220 mm 22%

Distributable Cash Flow

$130 mm $146 mm 12%

Distribution $1.96/unit $2.27/unit 16%

Processed Volumes (avg)

549 mmcfd 923 mmcfd 68%

8

Operational and Financial Goals for 2013 Successful 2012

Plants are all at or near capacity and experiencing stronger than expected drilling activity behind all systems

Execute previously announced organic expansions at Velma (Complete), WestOK (Complete),WestTX (2Q’13) and Arkoma (1Q’14)

Committed to maintaining strong balance sheet and liquidity position as Partnership completes current capital program and pursues further growth opportunities - recent $600mm acquisition of Cardinal Midstream funded with over 50% equity

Systematically grow distribution in conjunction with cash flows from announced accretive projects while targeting above average annualized coverage of 1.15x as compared to midstream MLP space

Adjusted EBITDA Growth ($ mm)

Projects & M&A to Contribute Significantly in 2013

175 181

220

340

0

50

100

150

200

250

300

350

2010 2011 2012 2013*

Distributable Cash Flow (DCF) Growth ($ mm)

Transformation of Balance Sheet Drives DCF

87

130146

220

0

50

100

150

200

250

2010 2011 2012 2013*

Processing Capacity Growth (mmcfd)

Significant Increase in Processing Capacity

583 613

1,093

1,293

0

200

400

600

800

1,000

1,200

1,400

1,600

2010 2011 2012 2013**

Strong Results Pave Way for Future Success

* Based upon median of previously announced guidance / ** Based upon expected timing of expansions

Operational Overview

9

WestOK Update

Geographical Area: Anadarko Basin / Mississippi Lime

Miles of Pipeline: Approx. 5,400

Processing Capacity: 458,000 mcfd

Number of Rigs Running: 39

Average Processed Volume (mcfd)

Overview

Recently added 200 mmcfd expansion quickly filing up with continued robust activity in Mississippi Lime

SandRidge, Chesapeake, Shell, Range and Devon active with sizeable acreage positions

DCP Southern Hills NGL takeaway pipeline to allow for increased liquids production in 2Q 2013

APL connected 139 wells in 4Q 2012, 12% more than previous quarter

211,533230,717 228,865

247,868263,654

275,567 279,305

315,753

380,113

412,682

150,000175,000200,000225,000250,000275,000300,000325,000350,000375,000400,000425,000

3Q2010 4Q2010 1Q2011 2Q2011 3Q2011 4Q2011 1Q2012 2Q2012 3Q2012 4Q2012

WestOK System

System Notes

10

I & II

Geographical Area: Woodford Shale/Ardmore Basin

Miles of Pipeline: Approx. 1,200

Processing Capacity: 160,000 mcfd

Number of Rigs Running: 12

Velma Update

Average Processed Volume (mcfd)

Overview

Recent 4Q volumes temporally affected by field operations - system processing over 140 mmcfd as of mid-February 2013

Addition of 60 mmcfd expansion in July 2012 all fixed fee and expected to be economically full by 3Q 2013

Major producers include ExxonMobil / XTO Energy, Range, Chesapeake, Continental, and Newfield in Velma’s area of operations

System located 50 miles to the west of Arkoma system and potential future synergies exist for producers in the Woodford

84,25587,732 85,158

96,625

104,930 105,115

122,904129,070

133,166

106,577

50,000

60,000

70,000

80,000

90,000

100,000

110,000

120,000

130,000

140,000

3Q2010 4Q2010 1Q2011 2Q2011 3Q2011 4Q2011 1Q2012 2Q2012 3Q2012 4Q2012

System Notes

Velma System

11

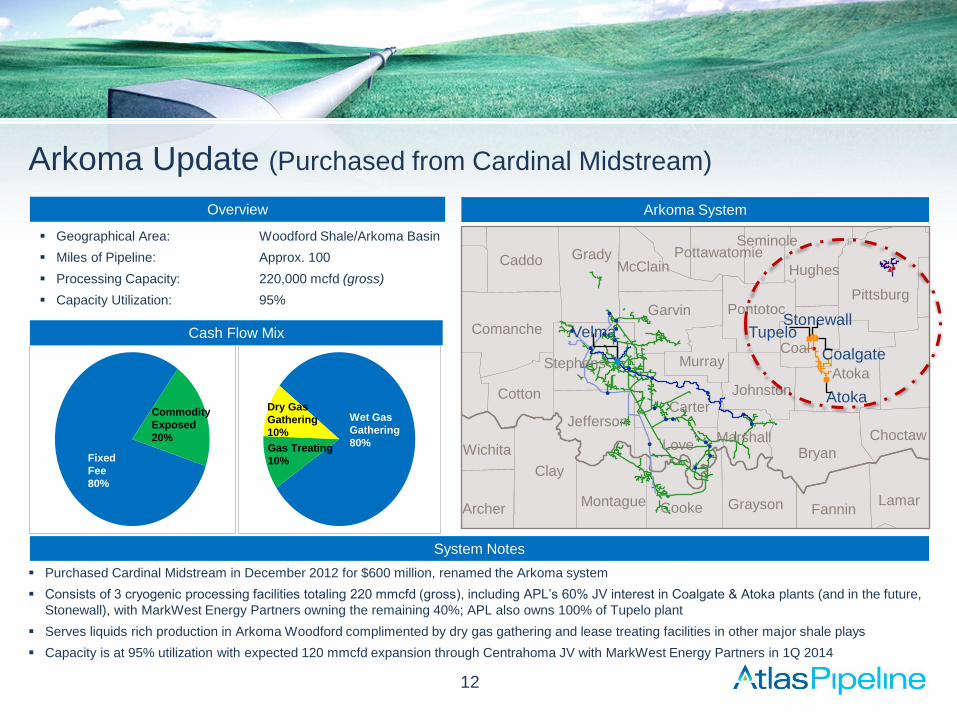

(V-100 & V-60)

Geographical Area: Woodford Shale/Arkoma Basin

Miles of Pipeline: Approx. 100

Processing Capacity: 220,000 mcfd (gross)

Capacity Utilization: 95%

Arkoma Update (Purchased from Cardinal Midstream)

Cash Flow Mix

Overview

Purchased Cardinal Midstream in December 2012 for $600 million, renamed the Arkoma system

Consists of 3 cryogenic processing facilities totaling 220 mmcfd (gross), including APL’s 60% JV interest in Coalgate & Atoka plants (and in the future,

Stonewall), with MarkWest Energy Partners owning the remaining 40%; APL also owns 100% of Tupelo plant

Serves liquids rich production in Arkoma Woodford complimented by dry gas gathering and lease treating facilities in other major shale plays

Capacity is at 95% utilization with expected 120 mmcfd expansion through Centrahoma JV with MarkWest Energy Partners in 1Q 2014

System Notes

Arkoma System

12

Fixed

Fee

80%

Wet Gas

Gathering

80%

Commodity

Exposed

20%

Dry Gas

Gathering

10%

Gas Treating

10%

Atoka

Coalgate

Stonewall Tupelo

Atoka

Bryan

Caddo

Carter

Choctaw

Coal

Comanche

Cotton

Garvin

Grady Hughes

Jefferson

Johnston

Love

McClain

Marshall

Murray

Pittsburg Pontotoc

Pottawatomie Seminole

Stephens

Archer

Clay

Cooke Fannin Grayson Lamar Montague

Wichita

Velma

Geographical Area: Permian Basin

Miles of Pipeline: Approx. 3,300

Current Processing Capacity: 255,000 mcfd

Number of Rigs Running: 66

WestTX Update

170,988169,413172,817

193,714198,068

220,506230,504

236,213

255,709271,592

125,000

150,000

175,000

200,000

225,000

250,000

275,000

3Q2010 4Q2010 1Q2011 2Q2011 3Q2011 4Q2011 1Q2012 2Q2012 3Q2012 4Q2012

WestTX System

Average Processed Volume (mcfd)

Overview

System Notes

200 mmcfd Driver facility being accelerated to facilitate growing production

DCP Sand Hills NGL takeaway pipeline to provide further NGL takeaway for Driver facility to move increasing NGLs coming on system

Pioneer just finished best ever horizontal Permian well on acreage dedicated to APL

Pioneer has over 900,000 acres in Permian and just secured JV partner to accelerate production which is expected to benefit APL

13

& CONSOLIDATOR

West Texas LPG NGL Pipeline

Geographical Area: Permian Basin, Barnett Shale

Miles of Pipeline: Approx. 2,200

Transportation Capacity: 230,000 bbls/day

Delivery to: Mont Belvieu

Average Volume (bbls/day)

Overview

Pipeline is operated by majority (80%) owner Chevron Corporation

Common carrier Y-grade NGL transportation pipeline begins in New Mexico and West Texas and transports liquids to Mont Belvieu

Pipeline is connected to Enterprise Products Partners, L.P. Rockies MAPL system for further NGL supply

Pipeline provides stable, fixed fee cash flow with no direct primary commodity exposure

System Notes

West Texas LPG

100%

Consolidator Plant

Benedum Plant

14

230,913 227,822 236,614 242,318 243,708256,579 262,094

0

50,000

100,000

150,000

200,000

250,000

2Q 2011 3Q 2011 4Q 2011 1Q 2012 2Q 2012 3Q 2012 4Q 2012

Financial & Investment Overview

15

Financial Objectives

16

APL is committed to operating from a position of strength

Target <4.0x Bank

Leverage Through

Capital Program and

Commodity Cycle

Structure Balance

Sheet to Maintain Financial Flexibility

Maintain at Least

$100 MM of Liquidity

Maintain Significant

Margin Protection

and Increase Tenor

into Further Periods

Improve Credit Rating

Sustain and Grow

with Senior Secured

Leverage Below 1.5x

($ in millions except as noted) 4Q 2012 3Q 2012 % Variance

Throughput Volume (Mcfd)

Velma 111,572 136,939 -18.5%

WestOK 436,694 403,304 8.3%

WestTEX 298,252 288,607 3.3%

Processed Volume (Mcfd)

Velma 106,577 133,166 -20.0%

WestOK 412,682 380,113 8.6%

WestTX 271,592 255,709 6.2%

Realized WAVG NGL Price ($/gal) $0.90 $0.87 3.4%

Average NYMEX Price ($/Mcf) $3.18 $2.60 22.3%

Total Revenue $354.5 $293.9 20.6%

Adjusted EBITDA $64.1 $55.9 14.7%

Distributable Cash Flow $40.4 $37.6 7.4%

Distribution to LP Unitholders $0.58 $0.57 1.8%

Distribution Coverage* 1.1x 1.1x N/A

Maintenance Capex $5.8 $4.7 23.4%

Growth / Acquisition Capex $722.3 $91.2 692.0%

Total Bank Leverage (TTM EBITDA) 4.0x 3.4x N/A

Total Debt $1,179.9 $786.6 50.0%

Senior Secured Debt $293.1 $80.1 265.9%

Total Liquidity $310.3 $520.1 -40.3%

4th Quarter Update Summary Quarterly Performance Comparison

Continued strong volume growth with sequentially better

natural gas and NGL pricing versus 3Q 2012

Distribution now at $0.58/unit – 2012 yearly payout 16%

higher than 2011

Purchased Cardinal Midstream (now named Arkoma) in

December 2012 for $600 million

Velma volume impacted temporarily in 4Q by 3rd party field

operations but now resolved

Approximately 90% completed in $600 million of expansion

capital to fund organic projects

Installation of Driver facility at WestTX being accelerated

due to robust activities in the Permian

UPDATE: In 1Q 2013, APL made a tender offer for its

8.75% 2018 notes to be replaced with a new issuance at

5.875% as well as a reduction of the majority of revolver

balance

17

* Pro forma for a full quarter of Arkoma cash flow

4Q 2012 Beat Expectations as Volume and Price Increase vs last Quarter

DCF

$1.60

DCF$1.88

DCF

$2.00

DCF

$2.24

DCF

$2.80 DCF

$2.69DCF

$2.64 DCF

$2.44

DCF$2.80

DCF$2.88

$0.89

$1.08 $1.10

$1.25$1.27

$1.17

$1.03

$0.80$0.87

$0.90

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

$2.20

$2.40

$2.60

$2.80

$3.00

3Q 2010 4Q 2010 1Q 2011 2Q 2011 3Q 2011 4Q 2011 1Q 2012 2Q 2012 3Q 2012 4Q 2012

Weig

hte

d A

vg

. N

GL

pri

ce (

$/g

al)

Ru

n-r

ate

Dis

trib

uta

ble

Cash

Flo

w P

er

Un

it

EBITDA, DCF, & Distribution

continue to increase despite

weak commodity price

environment

Partnership continues to build

business on fundamental volume

growth and execute on

remaining expansions its

systems

Distribution increase was 9th in

past 10 quarters as EBITDA for

year ($220mm) at high end of

guidance ($200-225)

With addition of Arkoma assets,

APL will be even less exposed to

NGL price volatility as new

assets are 80% fixed fee cash

flows

Realized NGL price vs. Run-Rate Distributable Cash Flow/Unit

Note: Run-rate DCF is measured as current quarter distributable cash flow per unit multiplied by four;

Based on average current units outstanding at time of quarter

Weighted Average

NGL price/ per gallon (left axis)

18

Run-rate DCF per unit

(right axis)

APL Fixed-Fee More than Doubles in Past Two Years

Actively restructuring contracts to align with producers or reduce commodity exposure (fee-based or possible take-or-pay)

Continue to utilize risk management program to prevent margin deterioration (swaps and options where applicable)

Significant portion of POP and Keep-Whole contracts include a fixed-fee component, mitigating commodity sensitivity

Long-term NGL takeaway agreements in place to mitigate downstream risk; Converting to Mont Belvieu pricing allows for current

pricing upgrade and reduces basis risk for hedging activities

Recent purchase of Arkoma system (purchased from Cardinal Midstream) in December 2012 is approximately 80% fixed fee cash

flow

Current Contract Mix*+

Percent of

Proceeds

51%

Fixed

Fee

17% Keep-

Whole

32%

Percent of

Proceeds

54%

Fixed

Fee

33%

Keep-

Whole

13%

Pre-Elk City & LMM Sale (Sept 2010)*

* Based on gross margin, not volume

+ As of 2/15/2013 and pro forma for Cardinal acquisition 19

Margin Well Protected for 2013, Increasing for 2014

Total Risk Management Margin Coverage* Executing on Risk

Management

Strategy to hedge up

to 80% of value for

the next 12 months

78% margin

coverage for 2013,

56% for 2014, and

24% for 2015

Continuing to add to

positions at attractive

prices and terms

Opportunistically

adding protection in

contango markets

Note: Hedges are at the corporate level and are not asset specific

* Excludes ethane; Data as of 2/15/2013

72%75%

82% 84%

60%

53%58%

56%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1Q 2013 2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014 3Q 2014 4Q 2014

Perc

en

t H

ed

ged

(%

) Average

for 2013: 78%

20

Average

for 2014: 56%

Key Investment Highlights

Diversified

asset base

Stable long-

term contracts

and

relationships

Strong Balance

Sheet

Proven

Management

Team

Gathering & Processing MLP with diversified assets in Oklahoma, Texas and Kansas

Robust growth of drilling programs in attractive NGL-rich areas in Partnership’s footprint

Significant service provider in attractive operating areas: Permian Basin, specifically the Spraberry &

Wolfberry Trends; Woodford Shale, and Mississippian Limestone & Carbonate formations

Over 84% of total processed volume and fixed fee margin tied to contracts that mature 2015+

Agreement with Pioneer through 2022 under which Pioneer has dedicated all production in an eight

county area in the Permian Basin to the WestTX system

Restructuring contracts to align producer and processor interests and reduce commodity exposure

Best-in-class balance sheet to capitalize on significant, announced growth opportunities

High levels of liquidity and no near term debt maturities

Recently executed on two new long term debt issuances and reduced revolver borrowings to position

balance sheet to fund future organic capex and M&A opportunities

Experienced executive and operations teams

Senior management team averages over 26 years of experience in the oil and natural gas industry

Long-term strategic E&P partners with proven capital and aggressive well drilling schedules

21

Appendix

22

Reconciliation to Non-GAAP Measures

23 Note: Figures in thousands of dollars ($ 000) except per unit data

Reconciliation to Non-GAAP Measures LTM

31-Dec-12 30-Sep-12 30-Jun-12 31-Mar-12 31-Dec-11 31-Dec-12

Reconciliation of net income (loss) to other non-GAAP measures:

Net income (loss) (6,907)$ (6,356)$ 74,851$ 6,471$ (5,254)$ 68,059$

Income attributable to non-controlling interests (1,902) (1,511) (1,061) (1,536) (1,708) (6,010)

Depreciation and amortization 24,314 23,161 21,712 20,842 19,936 90,029

Interest expense, net of ineffective interest rate swaps 14,091 9,692 9,269 8,708 7,078 41,760

Income tax expense (benefit) 176 - - - - 176

EBITDA 29,772$ 24,986$ 104,771$ 34,485$ 20,052$ 194,014$

Adjust for gain (loss) on sale of assets - - - - (598) -

Premium expense for purchased derivatives 5,168 4,855 3,984 3,752 2,905 17,759

Adjust for cash flow from equity investment (288) 378 (117) 904 (191) 877

Non-cash (gain) loss on derivatives 8,285 22,477 (64,741) 10,696 27,015 (23,283)

Acquisition costs and other adjustments 21,159 3,268 5,163 1,250 56 30,840

Adjusted EBITDA 64,096$ 55,964$ 49,060$ 51,087$ 49,239$ 220,207$

Interest expense (14,091) (9,692) (9,269) (8,708) (7,078) (41,760)

Amortization of deferred financing costs 1,316 1,061 1,130 1,165 1,126 4,672

Premium expense for purchased derivatives (5,168) (4,855) (3,984) (3,752) (2,905) (17,759)

Other - (131) (161) (34) 457 (326)

Maintenance capital expenditures (5,779) (4,732) (4,000) (4,510) (4,796) (19,021)

Distributable Cash Flow 40,374$ 37,615$ 32,776$ 35,248$ 36,043$ 146,013$

Weighted Average Units Outstanding 56,288 53,736 53,646 53,620 53,617 54,323

Weighted Average Annualized DCF per Unit 2.87$ 2.80$ 2.44$ 2.63$ 2.69$ 2.69

Three Months Ended

Recommended

![[Pipeline] Inspecting Pipeline Installation](https://img.dokumen.tips/doc/110x75/55cf8d045503462b1391543e/pipeline-inspecting-pipeline-installation.jpg)