Are you in the right room?

•You should be here if▫You think accounting is fun▫You can see how accounting will be

relevant to your future career▫You think you may want to be an

accountant▫You have successfully passed ADA or have

been granted credit for this course because of your prior studies.

04/19/23Prepared by Scott Copeland, UniSA 2007

1

WELCOME TO FINANCIAL ACCOUNTING 1

Time to lift the curtain on the second act in your accounting education

19/04/23Prepared by Scott Copeland, UniSA

2005

2

ADMINISTRATIVE MATTERS•Assumed Knowledge•Materials Required

▫Course Information/Study Guide▫Text and Practice Set▫Course Website

•Course Expectations▫Course Structure▫Tutorial Preparation▫Items of Assessment

•Course Coordinator

19/04/23Prepared by Scott Copeland, UniSA 2005

3

ASSUMED KNOWLEDGE•Accounting, Decisions And Accountability

is presumed knowledge for this course •The condensed nature of the delivery of

this course places a lot of responsibility on you. I am here to plant the seed, you must make it grow.

•FA 1 is designed to build on your ADA knowledge and will require more effort from you.

19/04/23Prepared by Scott Copeland, UniSA 2005

4

Resources and Expectations

•Course Information/Study Guide▫Text Books

Hoggett, John, Edwards, Lew and Medlin, John 2006, Accounting in Australia, 6th edition, Brisbane: John Wiley and Sons. http://

www.johnwiley.com.au/highered/accounting/aia6e/home/aia_home.html

Sportzone QuickBooks Practice Set 2006/7 -Value Pack, shrink-wrapped with CD for QuickBooks. http://www.pearsoned.com.au/Catalogue/TitleDetails.aspx?isbn=9780733990939

Accounting Handbook www.aasb.com.au

19/04/23Prepared by Scott Copeland, UniSA 2005

5

Resources and Expectations

•Course Website http://www.unisanet.unisa.edu.au/subjectinfo/subject.asp?SUBJECT=12262

▫Topic Folders Lecture Notes Case Studies Solutions

19/04/23Prepared by Scott Copeland, UniSA 2005

6

Course Expectations:Teaching arrangements

•Lectures/Seminars – 2.5 hours for 8 nights (2 visits)▫Time to go over the theory▫Demonstration of problems▫Lectures add to learning, they do not drive it

•Tutorials 2.5 hours per fortnight▫Your chance to seek assistance▫Small portion allocated to Practice Set▫You benefit more if you come prepared

19/04/23Prepared by Scott Copeland, UniSA 2005

7

Resources and Expectations

• Assessment▫ Assignment

Major Focus on Topic 2 Research should go “beyond the text

book” Designed to give you early feedback on

the practice set

19/04/23Prepared by Scott Copeland, UniSA 2005

8

Resources and Expectations•Practice Set

▫Not designed as training in QuickBooks▫Gives exposure to manual and

computerised systems to allow comparison▫Do a little bit each week

•Exam▫Must achieve 50% ▫Details provided closer to the date▫Past papers or specific guidance supplied

19/04/23Prepared by Scott Copeland, UniSA 2005

9

Working as a team

•Your assignments are due individually, however,▫ I expect that you will work closely with your tutor▫And may compare your work with other students.▫This is OK.

•BUT▫ It is your responsibility to ensure your work is

easily distinguishable from everyone else's and is properly referenced.

▫Plagiarism will not be tolerated and will be pursued.

19/04/23Prepared by Scott Copeland, UniSA 2005

10

Visits• These are designed to give you the key

information about the course.• We will cover a lot of information

quickly, but we will go through it clearly.• Visit 1 will cover the following topics

Specialised Journal and Ledgers Assets, Acquisition, Depreciation and

Disposal The key elements of inventories,

receivables and bank reconciliations

19/04/23Prepared by Scott Copeland, UniSA 2005

11

Visits Continued

•Visit 2 will cover ▫Liabilities and Completing the Accounting

Cycle ▫Preparation for the exam.

•Remember▫Lectures add to learning, they do not drive

it

19/04/23Prepared by Scott Copeland, UniSA 2005

12

Tutorials•You must make the most of these sessions

▫Do not let the tutor do the work for you▫They are not the one who will be doing the

exam•Accounting is a subject where practice

will help•It does not rely on rote learning equations•Your tutor is part of your team, make use

of them.

19/04/23Prepared by Scott Copeland, UniSA 2005

13

Tonight in FA 1

•Establish a new accounting system▫Review the role of a chart of accounts▫Using the general journal

•Review the role of adjusting entries•Identify the need for reversing entries•Highlight the resources and expectations

in this course

19/04/23Prepared by Scott Copeland, UniSA 2005

14

Where does it all begin?

•FA 1 is designed to pick up the threads exposed in ADA.

•These will be woven into a new and more comprehensive accounting system.

•To do this we must go back and review.•Our first port of call … the general

journal.

19/04/23Prepared by Scott Copeland, UniSA 2005

15

Using the General Journal

•Later in this course we will see the GJ used in a new way.

•The old rules still apply▫All debits listed first▫Followed by credits slightly indented▫A date must be entered for each

transaction▫A narration is required

19/04/23Prepared by Scott Copeland, UniSA 2005

16

The Opening Entry

•This is the first “transaction” you will complete in FA 1

•Entering data from a “chart of accounts” into the new system

•An example of a chart of accounts is on the next slide

19/04/23Prepared by Scott Copeland, UniSA 2005

17

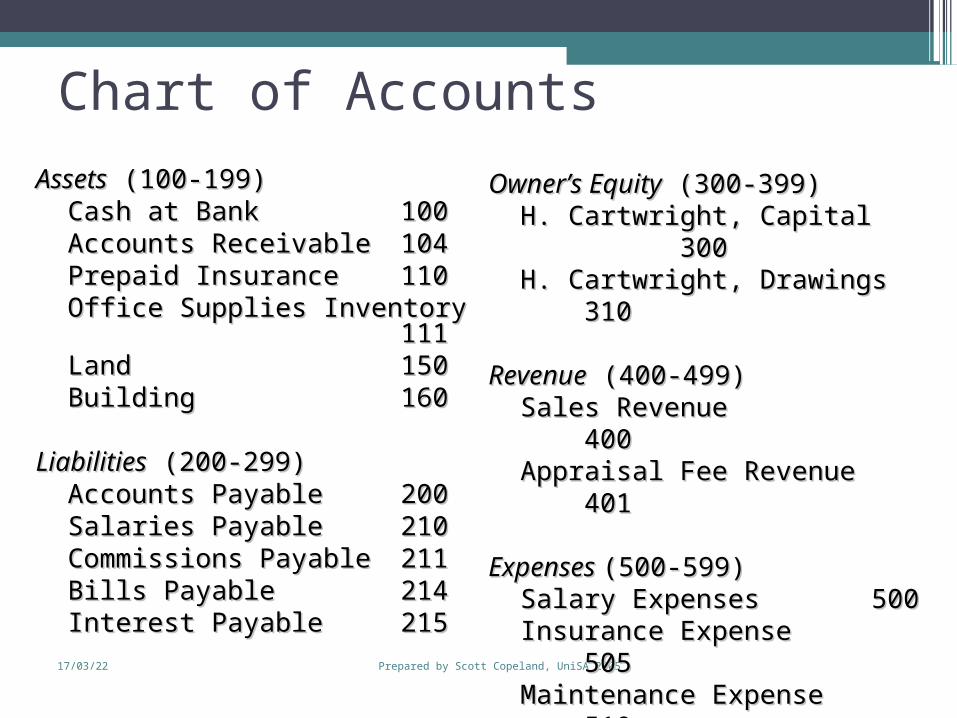

Chart of Accounts

Prepared by Scott Copeland, UniSA 2005

1819/04/23

AssetsAssets (100-199) (100-199) Cash at BankCash at Bank 100100 Accounts ReceivableAccounts Receivable 104104 Prepaid InsurancePrepaid Insurance 110110 Office Supplies InventoryOffice Supplies Inventory 111111 LandLand 150150 BuildingBuilding 160160

LiabilitiesLiabilities (200-299) (200-299) Accounts PayableAccounts Payable 200200 Salaries PayableSalaries Payable 210210 Commissions PayableCommissions Payable 211211 Bills PayableBills Payable 214214 Interest PayableInterest Payable 215215

Owner’s EquityOwner’s Equity (300-399) (300-399) H. Cartwright, Capital H. Cartwright, Capital

300300 H. Cartwright, DrawingsH. Cartwright, Drawings 310310

RevenueRevenue (400-499) (400-499) Sales RevenueSales Revenue

400400 Appraisal Fee RevenueAppraisal Fee Revenue

401401

Expenses Expenses (500-599)(500-599) Salary ExpensesSalary Expenses 500500 Insurance ExpenseInsurance Expense 505505 Maintenance ExpenseMaintenance Expense

510510 Materials expenseMaterials expense 515515 etc.etc.

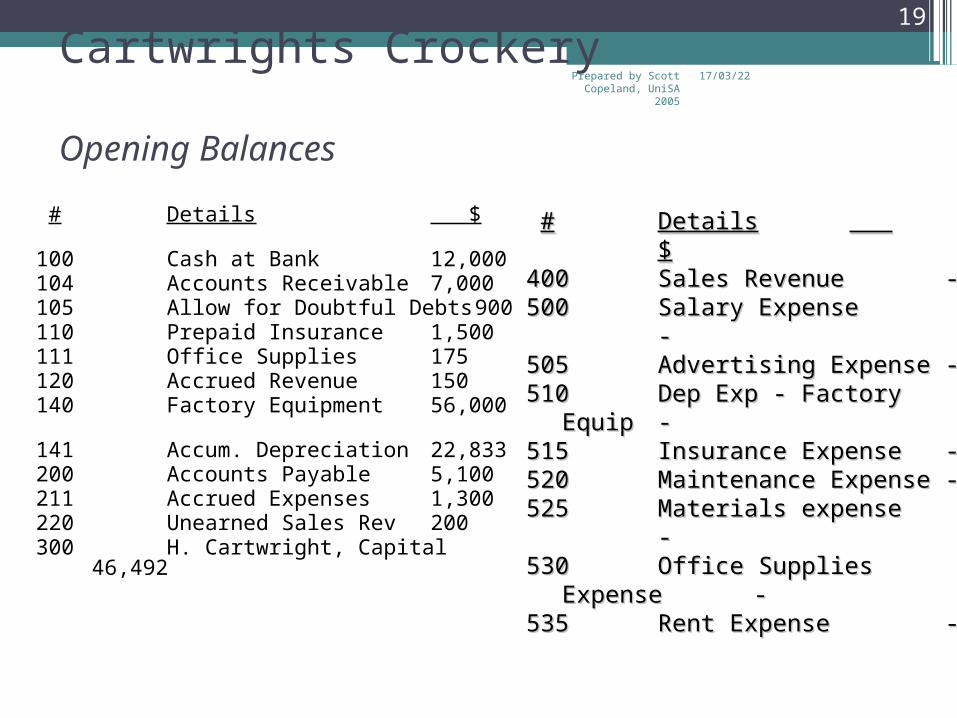

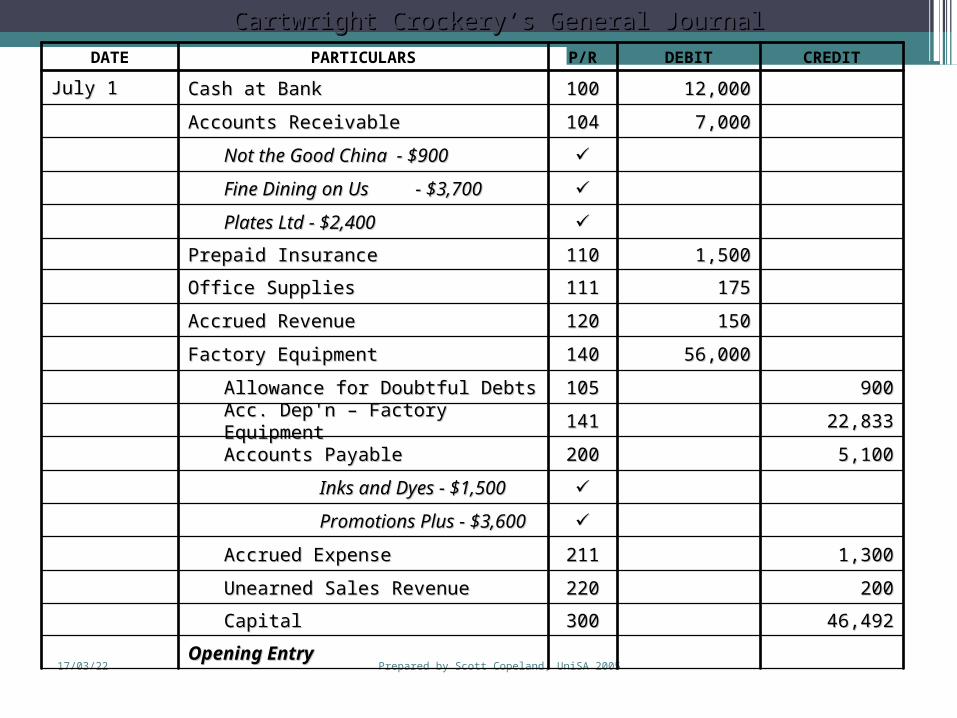

Cartwrights Crockery

Opening Balances

# Details $

100 Cash at Bank 12,000104 Accounts Receivable 7,000105 Allow for Doubtful Debts 900110 Prepaid Insurance 1,500111 Office Supplies 175120 Accrued Revenue 150140 Factory Equipment 56,000

141 Accum. Depreciation 22,833200 Accounts Payable 5,100211 Accrued Expenses 1,300220 Unearned Sales Rev 200300 H. Cartwright, Capital 46,492

19/04/23Prepared by Scott Copeland, UniSA 2005

19

## DetailsDetails $$400400 Sales RevenueSales Revenue --500500 Salary ExpenseSalary Expense --505505 Advertising ExpenseAdvertising Expense --510510 Dep Exp - Factory EquipDep Exp - Factory Equip

--515515 Insurance ExpenseInsurance Expense --520520 Maintenance ExpenseMaintenance Expense --525525 Materials expenseMaterials expense

--530530 Office Supplies ExpenseOffice Supplies Expense

--535535 Rent ExpenseRent Expense --

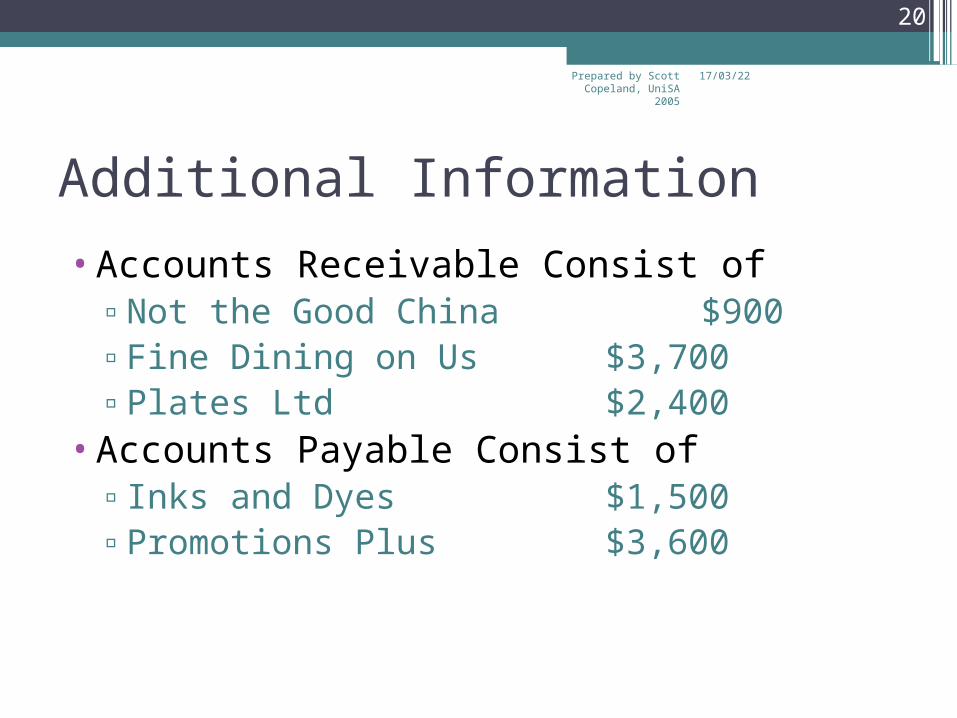

Additional Information

•Accounts Receivable Consist of▫Not the Good China $900▫Fine Dining on Us $3,700▫Plates Ltd $2,400

•Accounts Payable Consist of▫Inks and Dyes $1,500▫Promotions Plus $3,600

19/04/23Prepared by Scott Copeland, UniSA 2005

20

Prepared by Scott Copeland, UniSA 2005

2119/04/23

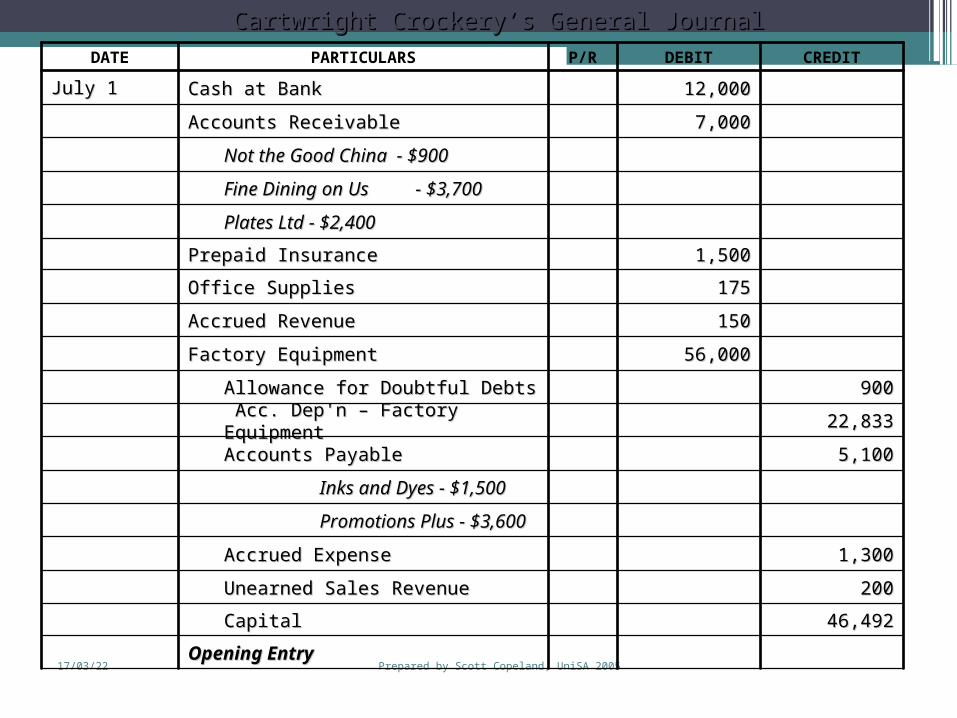

46,49246,492

Opening EntryOpening Entry

CapitalCapital

200200Unearned Sales RevenueUnearned Sales Revenue

1,3001,300Accrued ExpenseAccrued Expense

Promotions Plus - Promotions Plus - $3,600$3,600

Inks and Dyes - $1,500Inks and Dyes - $1,500

5,1005,100Accounts PayableAccounts Payable

22,83322,833 Acc. Dep'n Acc. Dep'n –– Factory Equipment Factory Equipment

900900Allowance for Doubtful DebtsAllowance for Doubtful Debts

CREDITDEBITP/RPARTICULARSDATE

12,00012,000Cash at BankCash at BankJuly 1July 1

7,0007,000Accounts Receivable Accounts Receivable

56,00056,000Factory EquipmentFactory Equipment

150150Accrued RevenueAccrued Revenue

175175Office SuppliesOffice Supplies

1,5001,500Prepaid InsurancePrepaid Insurance

Plates Ltd - $2,400Plates Ltd - $2,400

Fine Dining on UsFine Dining on Us - $3,700- $3,700

Not the Good China - $900Not the Good China - $900

Cartwright Crockery’s General JournalCartwright Crockery’s General Journal

Important Points

•All debits listed first•Subsidiary accounts

▫information still required▫cannot be included in the main columns

this would lead to double counting•A narration is required•Posting references only entered after

posting has been done.

19/04/23Prepared by Scott Copeland, UniSA 2005

22

What to do next?

•Post all entries to the relevant general and subsidiary ledgers

•Enter relevant posting notations into the General Journal

19/04/23Prepared by Scott Copeland, UniSA 2005

23

Prepared by Scott Copeland, UniSA 2005

2419/04/23

46,49246,492

Opening EntryOpening Entry

CapitalCapital

200200Unearned Sales RevenueUnearned Sales Revenue

1,3001,300Accrued ExpenseAccrued Expense

Promotions Plus - Promotions Plus - $3,600$3,600

Inks and Dyes - $1,500Inks and Dyes - $1,500

5,1005,100Accounts PayableAccounts Payable

22,83322,833Acc. Dep'n Acc. Dep'n –– Factory Equipment Factory Equipment

900900Allowance for Doubtful DebtsAllowance for Doubtful Debts

56,00056,000Factory EquipmentFactory Equipment

150150Accrued RevenueAccrued Revenue

175175Office SuppliesOffice Supplies

1,5001,500Prepaid InsurancePrepaid Insurance

Plates Ltd - $2,400Plates Ltd - $2,400

Fine Dining on UsFine Dining on Us - $3,700- $3,700

Not the Good China - $900Not the Good China - $900

7,0007,000Accounts Receivable Accounts Receivable

CREDITDEBITP/RPARTICULARSDATE

12,00012,000

300300

220220

211211

200200

141141

105105

140140

120120

111111

110110

104104

100100Cash at BankCash at BankJuly 1July 1

Cartwright Crockery’s General JournalCartwright Crockery’s General Journal

Ready to Go ?

•Not quite yet – lets review the opening balances

•Most are straight forward•What is the impact of accrual accounting

▫Prepaid insurance, accrued revenue, accrued expenses and unearned sales revenue

•All have been subject to adjusting entries

19/04/23Prepared by Scott Copeland, UniSA 2005

25

Why Adjust?

•To accurately reflect the performance and position of an entity in an accrual accounting system

•Adjustments are necessary to deal with deferrals and accruals▫Deferrals include items which have been

prepaid. Accruals include expenses incurred but not yet paid & revenue earned not received

19/04/23Prepared by Scott Copeland, UniSA 2005

26

What is the impact?

•On the business operations▫No affect

•On the accounting system▫See the following slides

19/04/23Prepared by Scott Copeland, UniSA 2005

27

19/04/23Prepared by Scott Copeland, UniSA 2005

28

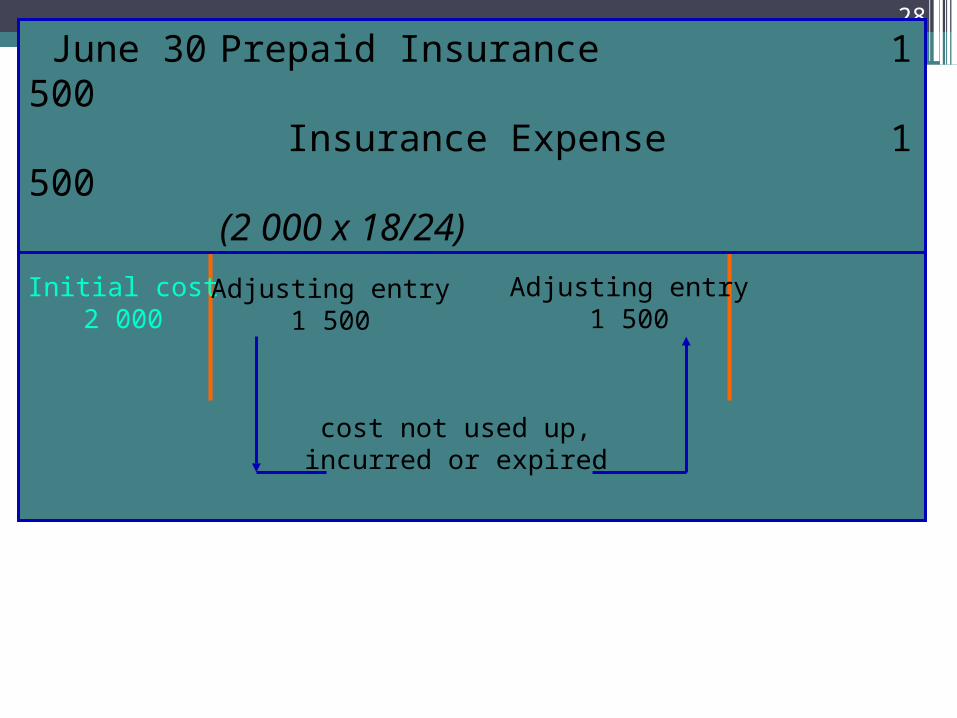

Insurance Expense

Initial cost2 000

Prepaid Insurance

Adjusting entry1 500

Adjusting entry1 500

cost not used up,incurred or expired

June 30 Prepaid Insurance 1 500 Insurance Expense 1 500(2 000 x 18/24)

19/04/23Prepared by Scott Copeland, UniSA 2005

29

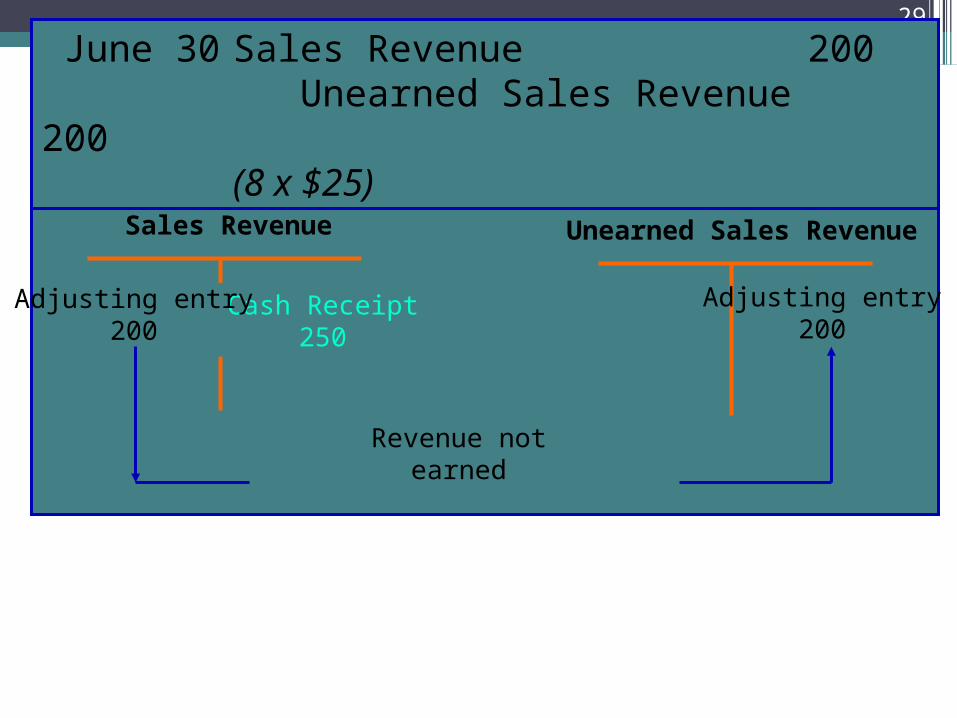

Sales Revenue

Cash Receipt250

Unearned Sales Revenue

Adjusting entry200

Adjusting entry200

Revenue notearned

June 30 Sales Revenue 200 Unearned Sales Revenue 200(8 x $25)

19/04/23Prepared by Scott Copeland, UniSA 2005

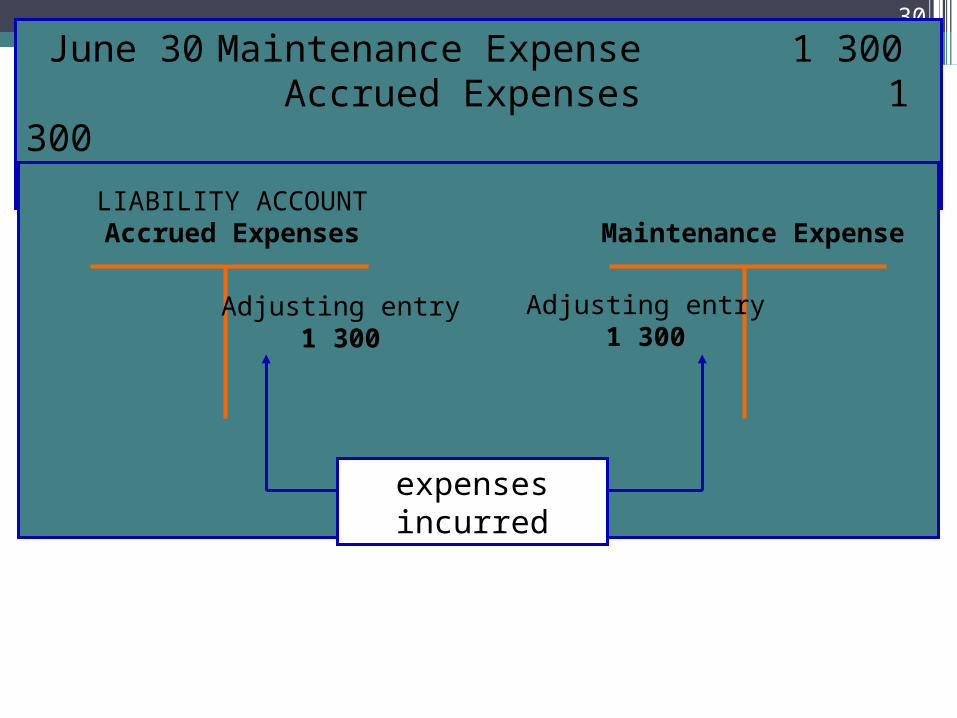

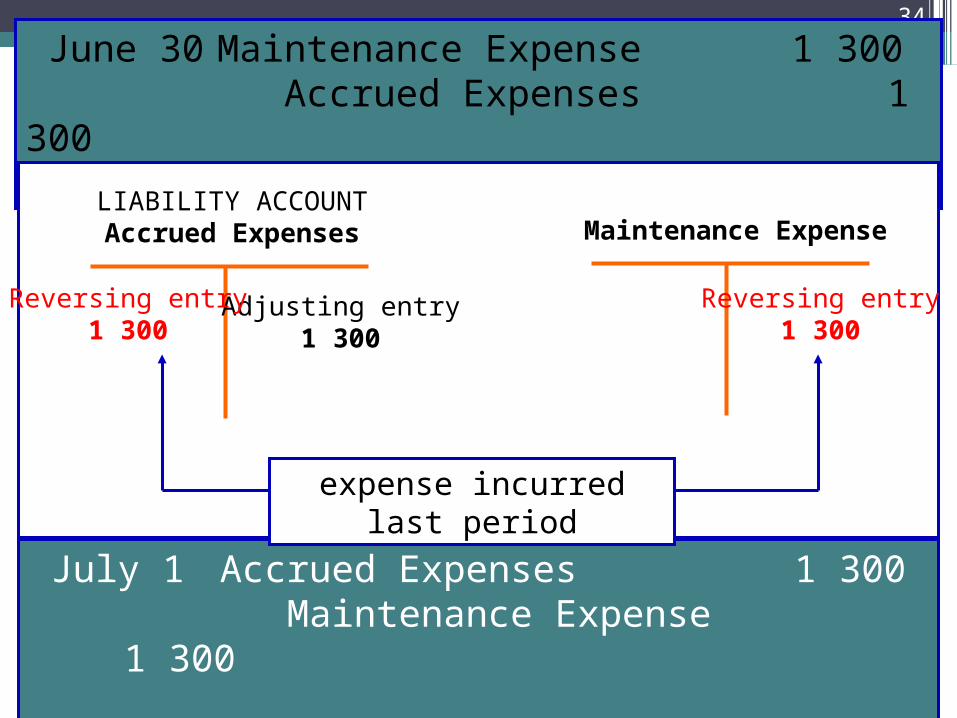

30 June 30 Maintenance Expense 1 300

Accrued Expenses 1 300

LIABILITY ACCOUNTAccrued Expenses Maintenance Expense

expenses incurred

Adjusting entry1 300

Adjusting entry1 300

19/04/23Prepared by Scott Copeland, UniSA 2005

31

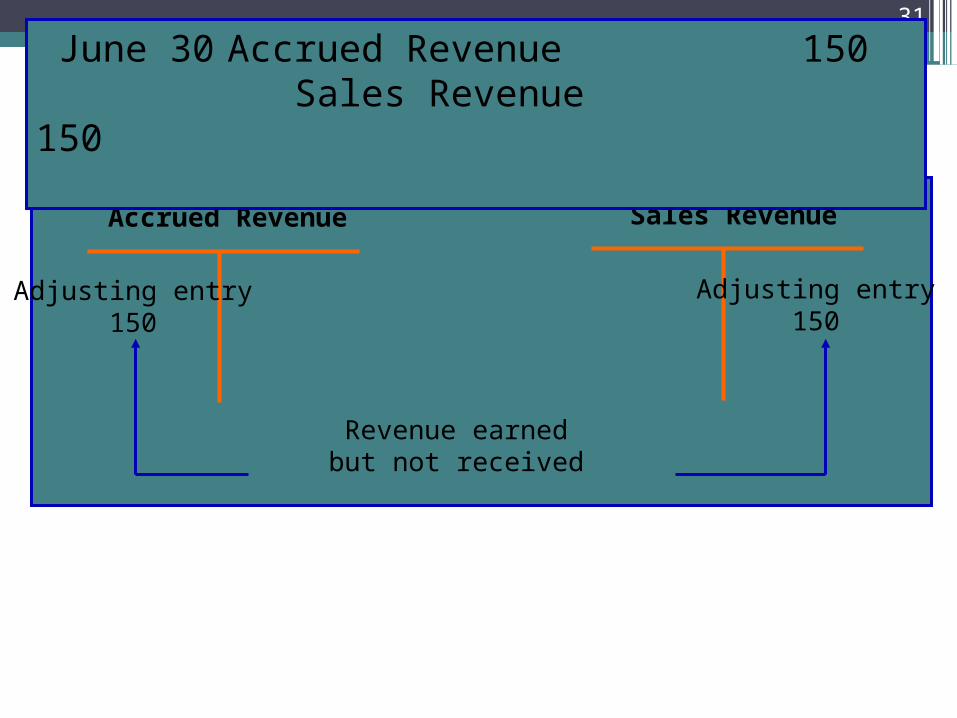

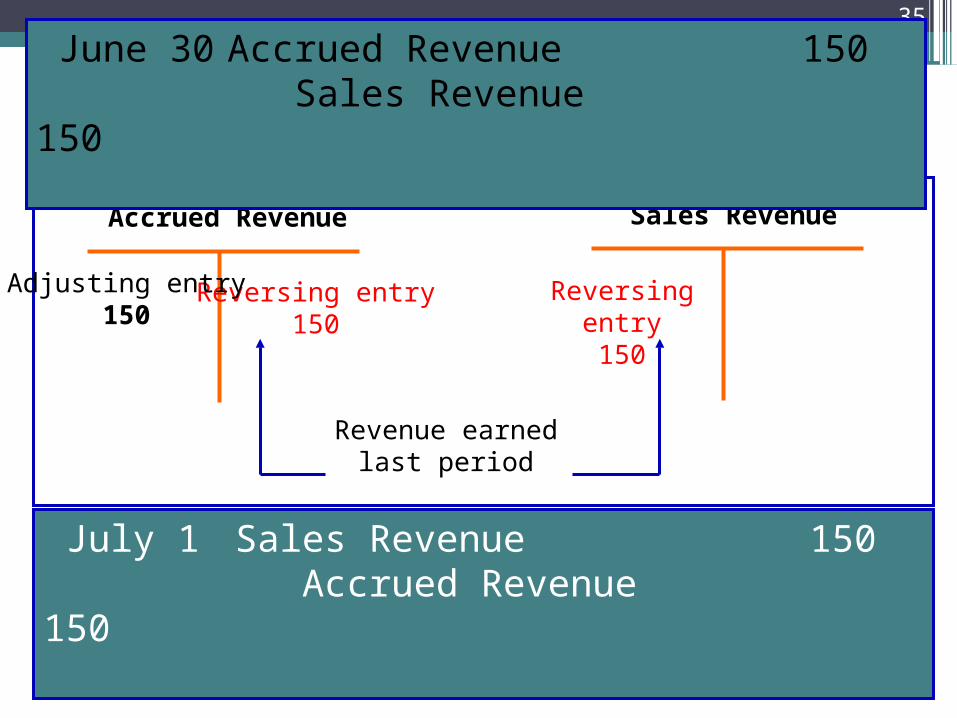

Accrued Revenue Sales Revenue

Adjusting entry150

Adjusting entry150

Revenue earnedbut not received

June 30 Accrued Revenue 150 Sales Revenue 150

Why do we need to know this?

•Adjusting entries are required for accounting reports

•But they are only book entries•An entity’s operations continue unaffected•Closing entries (to be covered in Topic

11) reset Revenue and Expense items•Reversing entries are required

19/04/23Prepared by Scott Copeland, UniSA 2005

32

What are Reversing Entries?

•An entry to counteract the effects of an adjusting entry

•Can be done for almost any adjusting entry but is most beneficial for accruals

•Accruals must be reversed in this course, reversal of prepayments is optional

19/04/23Prepared by Scott Copeland, UniSA 2005

33

19/04/23Prepared by Scott Copeland, UniSA 2005

34 June 30 Maintenance Expense 1 300

Accrued Expenses 1 300

LIABILITY ACCOUNTAccrued Expenses Maintenance Expense

Adjusting entry1 300

July 1 Accrued Expenses 1 300 Maintenance Expense 1 300

expense incurred last period

Reversing entry1 300

Reversing entry1 300

19/04/23Prepared by Scott Copeland, UniSA 2005

35

Accrued Revenue Sales Revenue

Reversing entry150

Reversing entry150

Revenue earnedlast period

June 30 Accrued Revenue 150 Sales Revenue 150

July 1 Sales Revenue 150 Accrued Revenue 150

Adjusting entry150

Why are these entries necessary?•To return the accounting system to the

position prior to adjustments•So that subsequent entries can be

processed “normally”•Allows for separation of duties and

greater efficiency

19/04/23Prepared by Scott Copeland, UniSA 2005

36

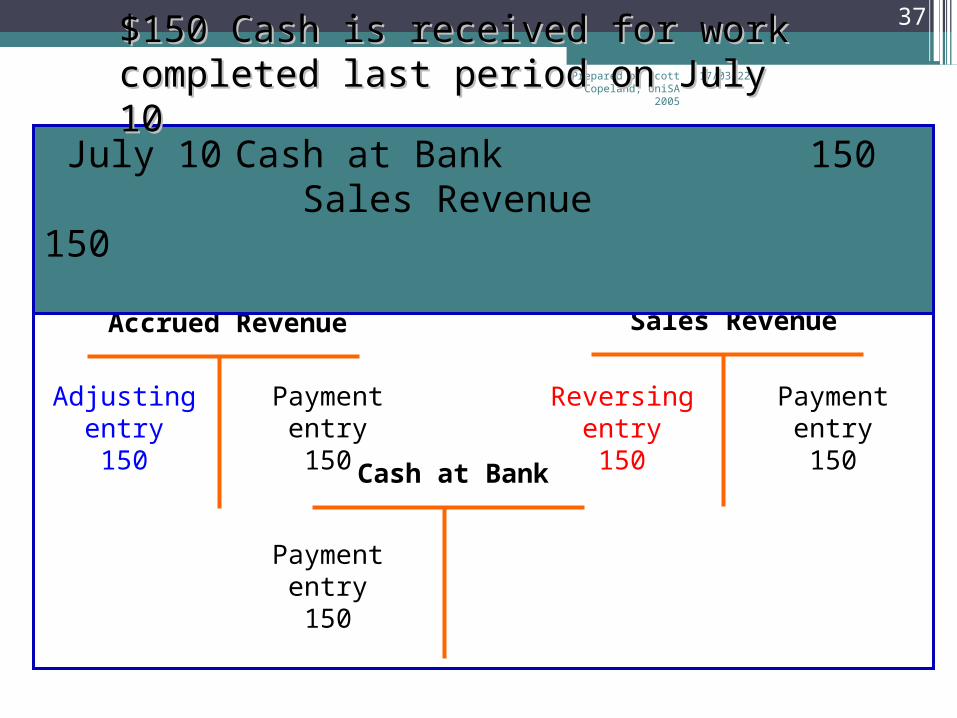

19/04/23Prepared by Scott Copeland, UniSA 2005

37

Accrued Revenue Sales Revenue

Reversing entry150

July 10 Cash at Bank 150 Sales Revenue 150

Cash at Bank

$150 Cash is received for work $150 Cash is received for work completed last period on July 10completed last period on July 10

Payment entry150

Payment entry150

Payment entry150

Adjusting entry150

19/04/23Prepared by Scott Copeland, UniSA 2005

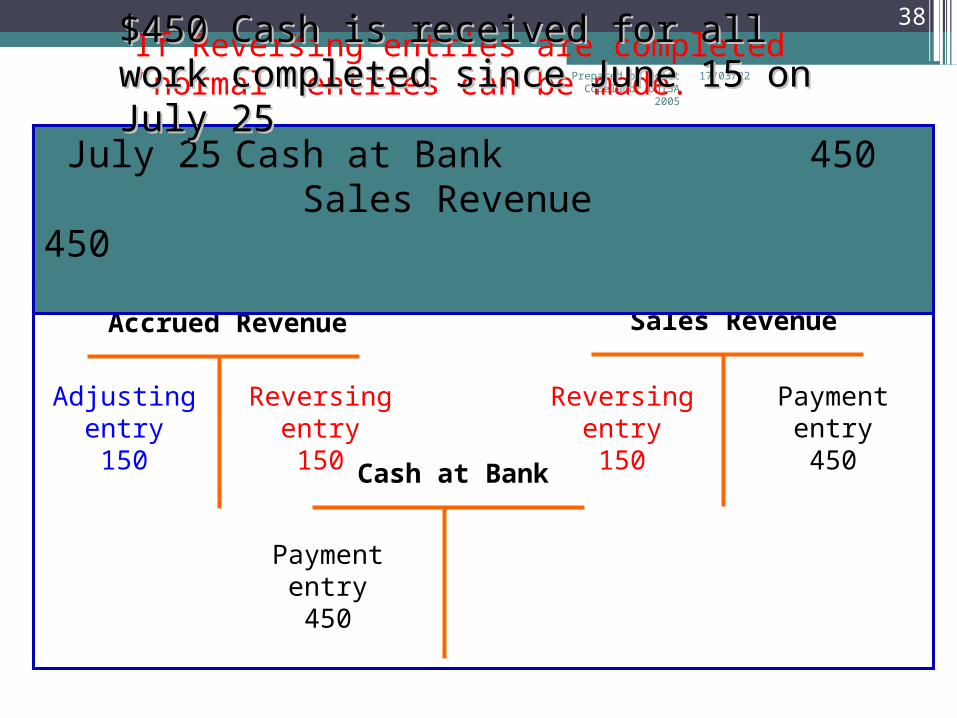

38

Accrued Revenue Sales Revenue

Reversing entry150

July 25 Cash at Bank 450 Sales Revenue 450

Cash at Bank

If Reversing entries are completed “normal” entries can be made.

$450 Cash is received for all work $450 Cash is received for all work completed since June 15 on July 25completed since June 15 on July 25

Payment entry450

Payment entry450

Reversing entry150

Adjusting entry150

19/04/23Prepared by Scott Copeland, UniSA 2005

39

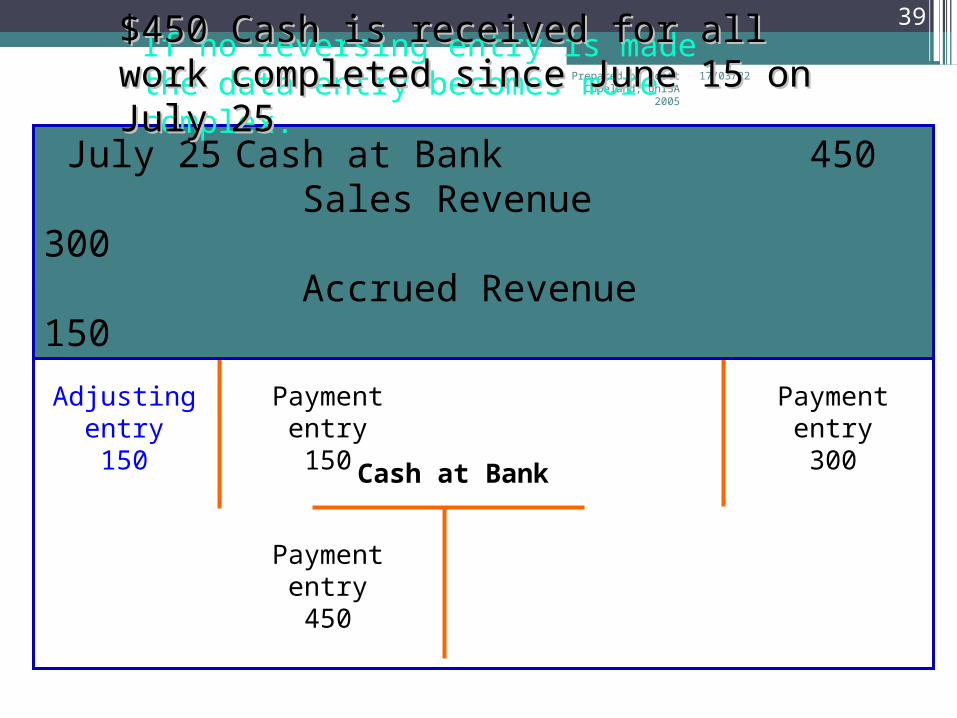

Accrued Revenue Sales Revenue

July 25 Cash at Bank 450 Sales Revenue 300 Accrued Revenue 150

Cash at Bank

If no reversing entry is made the data entry becomes more complex.

$450 Cash is received for all work $450 Cash is received for all work completed since June 15 on July 25completed since June 15 on July 25

Payment entry300

Payment entry450

Payment entry150

Adjusting entry150

Next

•What guides accountants in their work?

•The Conceptual Framework Revisited

•What has been the impact of International Standards?

19/04/23Prepared by Scott Copeland, UniSA 2005

40

TOPIC 2THE CONCEPTUAL FRAMEWORK’S RELEVANCE AND IMPACT

19/04/23Prepared by Scott Copeland, UniSA

2005

41

The Conceptual Framework

•The road map to accounting in Australia•The contents of the Conceptual

Framework are deemed to represent best practice

•It should be followed by accountants in the preparation and presentation of financial statements

•Non-mandatory

19/04/23Prepared by Scott Copeland, UniSA 2005

42

The Conceptual Framework

•Where did it come from?•Developed jointly by AASB and AARF•GOAL: Define the nature, subject,

purpose and broad content of general-purpose financial reporting

•MEANS: Statements of Accounting Concepts (SACs)

19/04/23Prepared by Scott Copeland, UniSA 2005

43

Why have a Conceptual Framework?•Benefits of conceptual framework:

▫accounting standards more consistent▫increased international comparability▫the Boards should be more accountable for

their decisions▫enhanced process of communication

between the Boards and constituents▫more economical Accounting Standard

development

19/04/23Prepared by Scott Copeland, UniSA 2005

44

Statements of Accounting Concepts•SAC 1 — Definition of the Reporting

Entity•SAC 2 — Objective of General Purpose

Financial Reports•AASB Framework

▫Qualitative Characteristics of Financial Information

▫Definition and Recognition of the Elements

19/04/23Prepared by Scott Copeland, UniSA 2005

45

Statements of Accounting Concepts•Initial plan was to develop more•Next SAC was to be on measurement•Agreement could not be reached so SAC

development stalled•Now replaced with IASB Framework•Remember from ADA, accounting only

exists because of general acceptance of the basic principles

19/04/23Prepared by Scott Copeland, UniSA 2005

46

SAC 1 — Definition of the Reporting Entity•Defines general-purpose financial reports

(GPFRs)▫reports intended to meet the information

needs common to users who are unable to command the preparation of reports tailored to their specific needs

▫GPFRs to be produced by entities who have users who cannot command the preparation of specific information

19/04/23Prepared by Scott Copeland, UniSA 2005

47

SAC 2 — Objective of GPFRs

•Objective of GPFRs is to provide relevant and reliable information to assist users to make and evaluate decisions about the allocation of scarce resources and to allow management and governing bodies to discharge their accountability

•Defines users of GPFRs

19/04/23Prepared by Scott Copeland, UniSA 2005

48

AASB Framework — Qualitative Characteristics of Financial Information•Identifies the characteristics of financial

information necessary to allow users to make and evaluate decisions about the allocation of scarce resources

•Primary qualitative characteristics:▫relevance▫reliability

19/04/23Prepared by Scott Copeland, UniSA 2005

49

AASB Framework — Qualitative Characteristics of Financial Information•Relevance

▫if information influences decisions about the allocation of scarce resources

•Reliability▫faithfully represents the entity’s

transactions and events▫free from bias▫free from undue error

19/04/23Prepared by Scott Copeland, UniSA 2005

50

AASB Framework — Qualitative Characteristics of Financial Information•Other considerations include

▫Understandability▫Materiality▫Comparability▫Substance over form▫Constraints

Timeliness Cost and Benefit

19/04/23Prepared by Scott Copeland, UniSA 2005

51

AASB Framework - Definition and Recognition of the Elements•Defines:

▫assets▫liabilities▫equity▫income▫expenses

•See your handout for full definitions

19/04/23Prepared by Scott Copeland, UniSA 2005

52

Definition of Equity

•Equity is defined as:▫the residual interest in the assets of the

entity after deduction of its liabilities•Directly a function of the definition given

to assets and liabilities•This is also true of Expenses and Income

19/04/23Prepared by Scott Copeland, UniSA 2005

53

Recognition of Elements•If an item fits one of the definitions above

it is not automatically recognised in the financial statements

•Recognition only occurs if▫it is probable that any future economic

benefit associated with the item will flow to or from the entity; and

▫it has a cost or other value that can be measured reliably

para 83 (a) and (b)

19/04/23Prepared by Scott Copeland, UniSA 2005

54

Recognition of Elements

•Other considerations▫Materiality (paras 29 and 30)▫Interrelationship of elements

recognition of one element will require recognition of another “balancing” element

▫Measurement Basis Including - Historic cost, Current Cost,

Realisable (settlement) value, Present Value

19/04/23Prepared by Scott Copeland, UniSA 2005

55

Accounting Standards

•If the Conceptual Framework is the road map

•The Standards are the specific directions•AASB standards can be found at

http://www.aasb.com.au/pronouncements/standards_index.htm

19/04/23Prepared by Scott Copeland, UniSA 2005

56

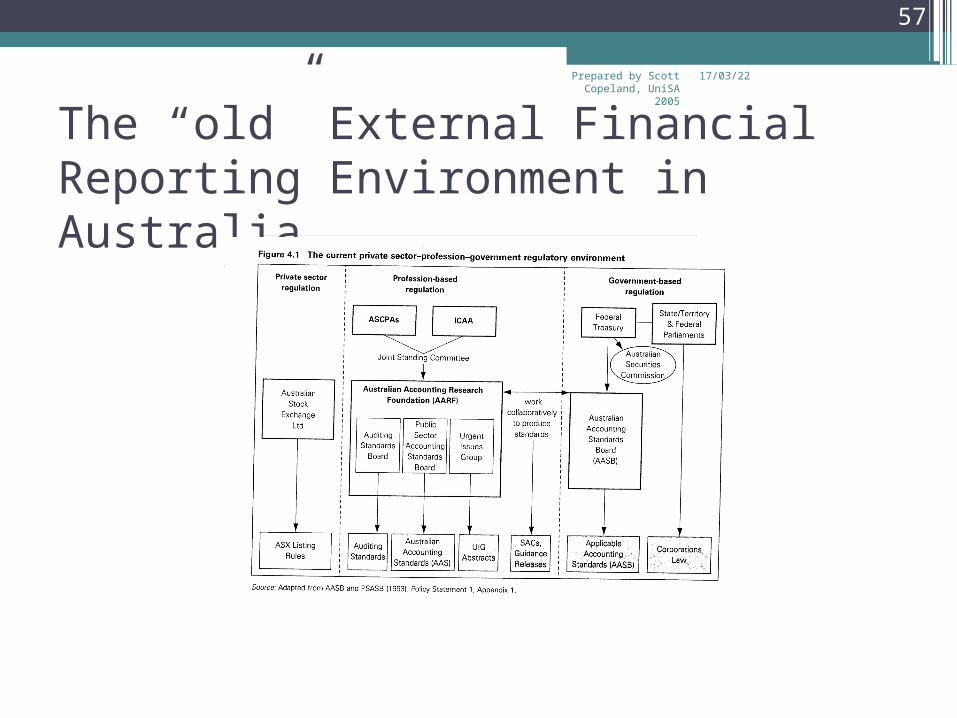

The “old” External Financial Reporting Environment in Australia

19/04/23Prepared by Scott Copeland, UniSA 2005

57

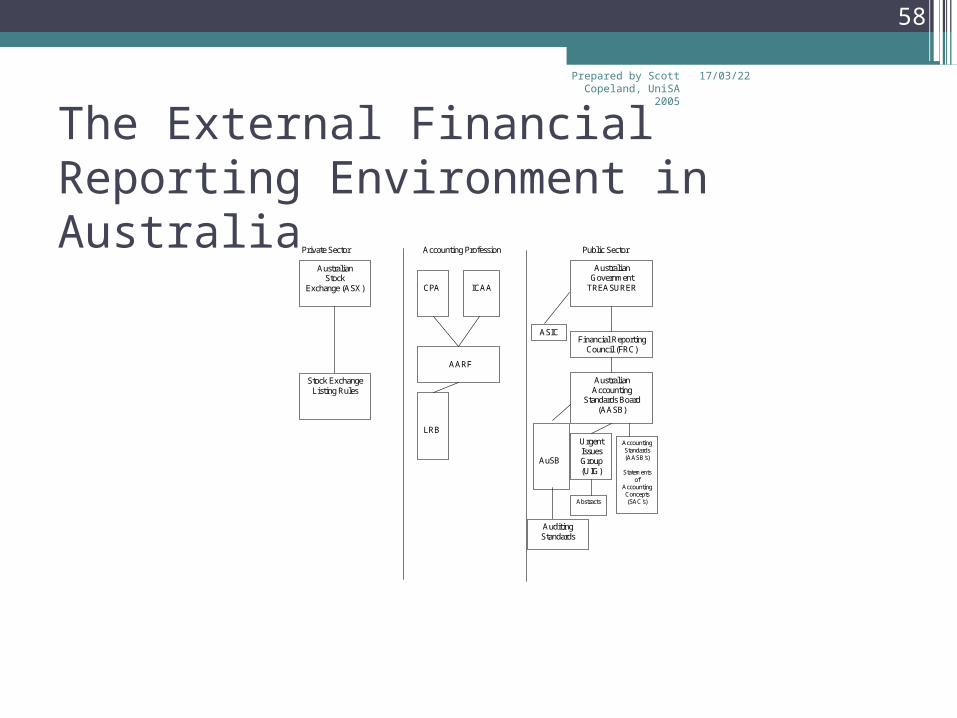

The External Financial Reporting Environment in Australia

Private Sector

Accounting Profession

Public Sector

Australian Stock

Exchange (ASX)

Stock Exchange Listing Rules

CPA

ICAA

AARF

LRB

AuSB

Auditing Standards

Australian Government

TREASURER

Financial Reporting Council (FRC)

Australian Accounting

Standards Board (AASB)

Urgent Issues Group (UIG)

Abstracts

Accounting Standards (AASB's)

Statements

of Accounting Concepts (SAC's)

ASIC

19/04/23Prepared by Scott Copeland, UniSA 2005

58

Development of an Accounting Standard•Initiated from a variety of sources•Much greater government involvement

now through FRC.•Created by AASB backed by Corporations

Act, therefore legally enforceable•Outcomes is AASB Standards

19/04/23Prepared by Scott Copeland, UniSA 2005

59

The Major Players•The Financial Reporting Council (FRC)•The Australian Securities and Investments

Commission (ASIC)•The Australian Accounting Standards

Board (AASB)•International Accounting Standards Board

(IASB)•International Financial Reporting

Interpretations Committee (IFRIC)•The Urgent Issues Group (UIG)•The Australian Accounting Research

Foundation (AARF)•The Australian Stock Exchange (ASX)

19/04/23Prepared by Scott Copeland, UniSA 2005

60

International Harmonisation and Convergence•FRC’s decision to harmonise•Major reason was to maintain capital

inflow into Australia (political decision?)•This meant aligning Australia’s standards

with those produced by International Accounting Standards Committee (IASC)

19/04/23Prepared by Scott Copeland, UniSA 2005

61

International Harmonisation and Convergence•January 2005 saw convergence•This means adopting international

standards to replace current AASBs•These are IASs and IFRSs•Have been rebadged as AASBs to comply

with Corporations Law•Applies to financial years beginning after

January 2005

19/04/23Prepared by Scott Copeland, UniSA 2005

62

International Harmonisation and Convergence•The Impacts

▫Changes to conceptual framework Definition of Revenue – Income and Gains SACs 1 and 2 + AASB Framework

▫Designed for “for profit” entities▫More scope for management choice in

many international standards▫Some additional guidance has been

required for Australia specific issues Aus notes and extractive industries standard

19/04/23Prepared by Scott Copeland, UniSA 2005

63

What do you have to find?

•More details and examples of what has changed

•How standards are developed •Who is involved in the development of

standards•Whether standards really help or if the

conceptual framework is enough

19/04/23Prepared by Scott Copeland, UniSA 2005

64

Tomorrow Night

•Specialised Journals•Control Accounts

▫Subsidiary ledgers•How to make the Practice Set Work for

you.•A reintroduction to assets

19/04/23Prepared by Scott Copeland, UniSA 2005

65

Recommended