IATA Maintenance Cost Conference 2016 – © SGI Aviation

Aircraft retirements and part-outEffective use of existing trends and opportunities

in the market

15 September 2016

Bangkok

1IATA Maintenance Cost Conference 2016 – © SGI Aviation

Index

SGI Aviation

Introduction

Retirement

- Historical trends

- Retirements by age, type and region

- Storage and disassembly locations

Retirement drivers

- Economy and oil prices

- Introduction of new aircraft

- Components value and demand

Conclusion

2IATA Maintenance Cost Conference 2016 – © SGI Aviation

Group overview

Our locations and services

SGI SingaporeAircraft & Engine

technical services

Business jets

SGI AmsterdamAsset management

Aircraft & Engine technical services

Business jets

Consulting

Regulatory services

SGI AmericasTechnical services

Engine services

4SGI has offices located in

Amsterdam, Singapore,

Guernsey and New York.

45+Over 45 experts, located on

almost all continents

15Local experts in 15 countries

who speak the language &

know the culture

100+ More than 100 inspections

performed, including 45

aircraft redeliveries in 2015

150Over 150 engines

inspections, including

management of 20 shop visits

7,500More than 7,500 inspection

days performed in 2015

63% Lessors

& financiers

37% Airlines

150+Technical services

Engine management

Asset management

Consulting services

30+ aircraft under

management

Services

Client base

Management 2015 Engagements

45

60

35

41

Valuation

Annual

Redeliveries

Pre purchase

3IATA Maintenance Cost Conference 2016 – © SGI Aviation

Index

SGI Aviation

Introduction

Retirement

- Historical trends

- Retirements by age, type and region

- Storage and disassembly locations

Retirement drivers

- Economy and oil prices

- Introduction of new aircraft

- Components value and demand

Conclusion

4IATA Maintenance Cost Conference 2016 – © SGI Aviation

0

100

200

300

400

500

600

700

0

36000

24000

42000

12000

48000

6000

18000

30000

72000

114000

108000

102000

96000

90000

84000

120000

78000

66000

60000

54000

# of aircraft

FH

0

100

200

300

400

# of aircraft

FH

96000

90000

72000

66000

78000

60000

54000

84000

100000

24000

36000

120000

30000

42000

18000

6000

48000

Source: FAA AC120-14 and EASA AMC20-20, various Airbus & Boeing publications and Ascend Fleet Database (Aug, 2016).

Note: Retired aircraft have an assumed annual utilization of 3,000 FH.

Introduction

Technical life ≠ Economic life

In-service: 6%

Retired: 66%

DSG ESG

A320

737CL

DSO ESO

In-service: 47%

Retired: 96%

Retired

In-service Design Service Goal or Design Service

Objective (DSG/DSO) is the period of time

during which the principal structure will be

reasonably free from significant cracking

- This is established at design or certification

- The DSG/DSO is expressed in Flight Hours or

Flight Cycles

Limit of validity (LOV) is the period of time

up to which it has been demonstrated that

widespread fatigue is unlikely to occur in an

airplane’s structure

- This is by virtue of its design and required

maintenance actions

- The LOV is also expressed in Flight Hours or

Flight Cycles

Operation beyond the DSG/DSO requires an

extensive inspection program

Retired

In-service

5IATA Maintenance Cost Conference 2016 – © SGI Aviation

Index

SGI Aviation

Introduction

Retirement

- Historical trends

- Retirements by age, type and region

- Storage and disassembly locations

Retirement drivers

- Economy and oil prices

- Introduction of new aircraft

- Components value and demand

Conclusion

6IATA Maintenance Cost Conference 2016 – © SGI Aviation

6

8

10

12

14

5,000

25,000

20,000

15,000

10,000

0

30,000

1985

2000

1980

2005

2010

2015

1990

1995

Aircraft retirements and retirement age (1980-2015)

The number of commercial aircraft in service has increased from approximately 12,000 in 1980 to more than 27,000 by the end of

2015

From 1980 to 2015, more than 15,000 commercial aircraft have been retired world wide

- The compound annual growth rate was more than 4%

The average age of aircraft in service has been relatively stable in the last 15 years, albeit with a decreasing trend in the last 5

years;

As a result of the growing young world fleet, there will be increasing amount of aircraft removed from service and subsequently

retirements over the upcoming years;

Historical trends

The increasing world fleet will result in an increase of aircraft retirements over the next decades

Number of aircraft in service and average age (1980-2015)

668762

10

15

20

25

30

1,000

2,000

4,000

0

5,000

3,000

3,484

2,059

1990-

1994

2000-

2004

2,437

1995-

1999

1,405

1985-

1989

1980-

1984

4,719

2005-

2009

2010-

2015

Average retirement age

Aircraft retirements# of aircraft

Average age

Source: SGI Aviation analysis, internal databases and Ascend database

7IATA Maintenance Cost Conference 2016 – © SGI Aviation

Index

SGI Aviation

Introduction

Retirement

- Historical trends

- Retirements by age, type and region

- Storage and disassembly locations

Retirement drivers

- Economy and oil prices

- Introduction of new aircraft

- Components value and demand

Conclusion

8IATA Maintenance Cost Conference 2016 – © SGI Aviation

The average retirement age for commercial

aircraft over the last 36 years was 26.5 years;

More than half of the aircraft are retired between

the age of 20 and 30 years;

About 10% of the aircraft were retired before the

age of 15 during the analysed term;

Another some 10% of the aircraft went out of

service after the age of 37;

More than 50% of the aircraft are still in operation

at the age of 25 years;

Retirement age distribution (1/4)

More than 50% of the aircraft are still in operation at the age of 25 years

0

150

300

450

600

750

900

444642 485014121086 40383634323028262422201816

10 155 20 4535 4030

0%

25

25%

75%

50%

100%

52%

Aircraft retirement age distribution (1980-2015)

10%

90%

50%

% of retired fleet by ages (1980-2015)

Source: SGI Aviation analysis, internal databases and Ascend database

9IATA Maintenance Cost Conference 2016 – © SGI Aviation

Retirement age distribution (2/4)

Freighters tend to be retired later than passenger aircraft

0

50

100

150

10

15

20

25

20

14

20

12

20

10

20

00

20

02

19

96

19

94

20

08

19

88

19

90

19

84

20

06

19

86

19

98

19

82

19

80

19

92

20

04

Average age at conversion

Converted freighters

Converted freighters (1980-2015)

0

200

400

600

800

86 36 4414 2818 481210 3422 262016 424038323024 5046

Freighter

Passenger

Retirement age distribution by aircraft usage (1980-2015)

Total retirement:

- Passenger aircraft: 82%

- Freight aircraft: 17%

- 39% (1,046 aircraft) were converted freighters.

Significant differences between passenger and

freight aircraft retirement:

- Average retirement age: freighters (32.5),

passenger aircraft (25.1);

- Surviving rate at age 33: freighters (50%),

passenger aircraft (13%);

Freighter conversion:

- Average conversion age: 18

- 10 to 20 years of extended life

- Low utilisation

Source: SGI Aviation analysis, internal databases and Ascend database

10IATA Maintenance Cost Conference 2016 – © SGI Aviation

Retirement age distribution (3/4)

There are differences in retirement age of narrow body, wide body and small aircraft

Retirement age distribution of small aircraft (1980-2015)

0

100

200

300

40 4838 46444234 36326 8 10 12 14 16 18 20 2422 26 3028

Retirement share: 39%

Average retirement age: 25.6

Note: Aircraft with 100 seats or less are classified as small aircraft & aircraft with 100 to 200 seats are classified as narrow body aircraft

Source: SGI Aviation analysis, internal databases and Ascend database

0

100

200

300

400

500

4832 38 42403428 30 44 46368 106 1412 261816 2420 22

Retirement share: 47%

Average retirement age: 27.4

Retirement age distribution of narrow body aircraft (1980-2015)

11IATA Maintenance Cost Conference 2016 – © SGI Aviation

Retirement age distribution (3/4)

There are differences in retirement age of narrow body, wide body and small aircraft

Note: Wide body aircraft are classified as aircraft with 200 seats or more

Source: SGI Aviation analysis, internal databases and Ascend database

0

40

80

120

160

146 168 1210 2018 2422 2826 484642403836343230 44

Retirement age distribution of wide body aircraft (1980-2015)

Retirement share: 14%

Average retirement age: 25.5

0%

20%

40%

60%

80%

100%

4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50

% of retired fleet by ages and aircraft types (1980-2015)

Regional

WB

NB

12IATA Maintenance Cost Conference 2016 – © SGI Aviation

Manufacturer’s locations of retired aircraft (1980-2015)

Retired types of aircraft (1/2)

The aircraft types of which a medium portion has been retired will drive the retirement in the short-term future

Top 20 aircraft retired (till 31/12/2015)

Aircraft type # retired % retiredAverage

retirement age

727 1492 84% 31.4

737-100/-200 810 75% 30.3

An-24 760 69% 30.3

DC-9 725 78% 35.2

747 714 48% 27.1

737 CL 670 34% 22.7

Tu-154 648 78% 22.9

Yak-40 629 67% 25.9

MD-80 490 41% 24.0

707 456 63% 24.5

Tu-134 453 82% 25.4

L-410 Turbolet 453 61% 16.8

Il-18 440 83% 24.1

DC-8 430 78% 31.7

A300 276 49% 24.5

Viscount 273 62% 21.7

DC-10 268 71% 30.3

A320 266 6% 20.1

F.27 253 57% 32.2

L-1011 TriStar 221 89% 26.8

13IATA Maintenance Cost Conference 2016 – © SGI Aviation

Retirement rate by manufacturer’s locations (till 31/12/2015)

Retired types of aircraft (2/2)

America and Europe built aircraft with low retirement rate are projected to shape the long-term market

Top 20 aircraft delivered (till 31/12/2015)

Asia-Pacific

596 47%70%

28,674

Europe

16,520

6,134

USSR/CIS

23%

Americas

29%

Aircraft type # delivered # retired % retiredAv. retirement

age

737 NG 5478 54 1% 12.6

A320 4115 266 6% 20.1

737 CL 1979 670 34% 22.7

727 1775 1492 84% 31.4

747 1492 714 48% 27.1

A319 1382 23 2% 14.0

777 1355 20 1% 16.8

A330 1222 21 2% 16.9

A321 1210 18 1% 19.1

MD-80 1190 490 41% 24.0

Dash 8 1123 69 6% 17.9

An-24 1100 760 69% 30.3

737-100/-200 1078 810 75% 30.3

767 1064 160 15% 24.5

757 1039 101 10% 24.3

CRJ RJ 1021 146 14% 14.2

Yak-40 942 629 67% 25.9

DC-9 931 725 78% 35.2

Tu-154 834 648 78% 22.9

ATR 72 814 31 4% 19.6

% of aircraft retired

# of aircraft manufactured

Manufacturer’s location

Source: SGI Aviation analysis, internal databases, Ascend database

14IATA Maintenance Cost Conference 2016 – © SGI Aviation

Last operating country (1980-2015)

Retirement regions

The aircraft were largely on an US registration at the moment of decommissioning

Top 20 countries/regions of retired aircraft (1980-2015)

Country/Region # of RetiredAverage

Retirement Age

United States 5,555 26.6

USSR/CIS 3,620 24.9

United Kingdom 488 25.2

Indonesia 302 26.9

Canada 295 27.6

France 234 23.6

China 213 17.6

Mexico 194 33.7

Nigeria 190 29.1

Venezuela 173 31.8

Congo (Democratic Republic) 167 32.8

Ireland 164 25.2

South Africa 161 31.5

Brazil 161 30.2

Germany 151 23.7

Australia 144 24.9

Colombia 113 29.5

Spain 102 27.0

Philippines 99 30.8

Netherlands 93 22.5

15IATA Maintenance Cost Conference 2016 – © SGI Aviation

Index

Introduction

Retirement

- Historical trends

- Retirements by age, type and region

- Storage and disassembly locations

Retirement drivers

- Economy and oil prices

- Introduction of new aircraft

- Components value and demand

Conclusion

16IATA Maintenance Cost Conference 2016 – © SGI Aviation

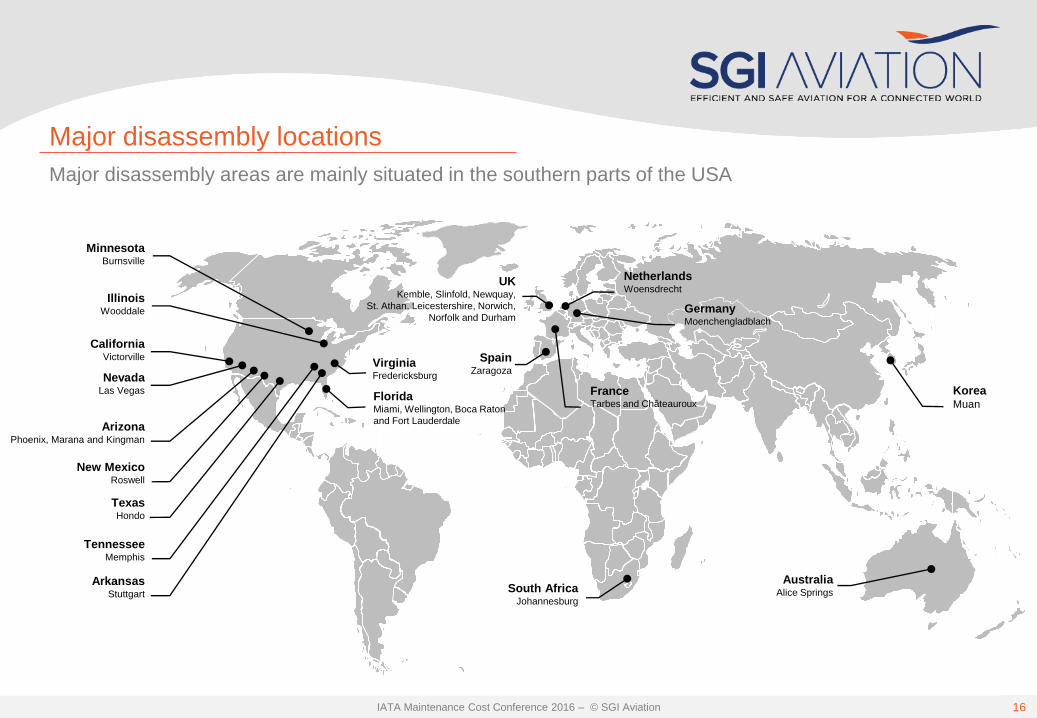

Major disassembly locations

Major disassembly areas are mainly situated in the southern parts of the USA

ArizonaPhoenix, Marana and Kingman

NevadaLas Vegas

CaliforniaVictorville

New MexicoRoswell

TexasHondo

MinnesotaBurnsville

IllinoisWooddale

ArkansasStuttgart

TennesseeMemphis

SpainZaragoza

AustraliaAlice Springs

KoreaMuan

NetherlandsWoensdrecht

UKKemble, Slinfold, Newquay,

St. Athan, Leicestershire, Norwich,

Norfolk and DurhamGermanyMoenchengladblach

FranceTarbes and Châteauroux

VirginiaFredericksburg

FloridaMiami, Wellington, Boca Raton

and Fort Lauderdale

South AfricaJohannesburg

17IATA Maintenance Cost Conference 2016 – © SGI Aviation

Top 20 storage airport locations

More than 33% of the stored aircraft are located in the USA

ArizonaKingman, Marana

Phoenix and Tucson

CaliforniaVictorville

New MexicoRoswell

TexasSan Angelo

CanadaCalgary

SpainTeruel

FranceTarbes and Toulouse

MissouriKansas City

VenezuelaCaracas

South AfricaJohannesburg

IranTehran

UAEFujairah

RussiaZhukovsky, Moscow (Vnukovo

and Domodedovo)

ArkansasBlytheville

18IATA Maintenance Cost Conference 2016 – © SGI Aviation

Index

SGI Aviation

Introduction

Retirement

- Historical trends

- Retirements by age, type and region

- Storage and disassembly locations

Retirement drivers

- Economy and oil prices

- Introduction of new aircraft

- Components value and demand

Conclusion

19IATA Maintenance Cost Conference 2016 – © SGI Aviation

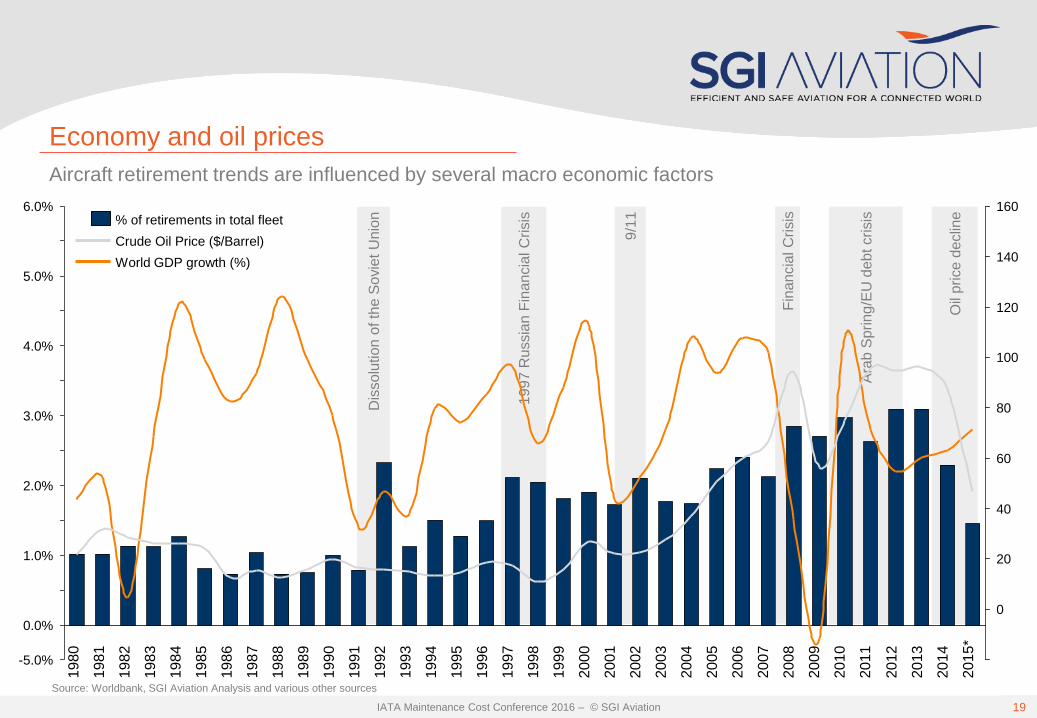

Fin

an

cia

l C

risis

Oil

price d

eclin

e

9/1

1

Dis

so

lution

of th

e S

ovie

t U

nio

n

199

7 R

ussia

n F

inan

cia

l C

risis

Ara

b S

prin

g/E

U d

eb

t crisis

Economy and oil prices

Aircraft retirement trends are influenced by several macro economic factors

World GDP growth (%)

% of retirements in total fleet

Crude Oil Price ($/Barrel)

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015*

Source: Worldbank, SGI Aviation Analysis and various other sources

80

40

5.0%

4.0%

3.0%

2.0%

140

60

120

0

1.0%

0.0%

6.0% 160

20

-5.0%

100

20IATA Maintenance Cost Conference 2016 – © SGI Aviation

Index

SGI Aviation

Introduction

Retirement

- Historical trends

- Retirements by age, type and region

- Storage and disassembly locations

Retirement drivers

- Economy and oil prices

- Introduction of new aircraft

- Components value and demand

Conclusion

21IATA Maintenance Cost Conference 2016 – © SGI Aviation

Introduction of new aircraft

Technical development is an important aircraft retirement driver

0

150

300

450

0%

20%

40%

60%

80%

100%

2005 201020001975 199519901980 19851970 2015*

A330

A300/A310

0

500

1,000

1,500

0%

20%

40%

60%

80%

100%

200019801975 20051985 2015*20101970 19951990

737NG

737CL

737-100/200

737 family in service rate & total retirement (till 31/12/2015)

A300 and A330 family in service rate & total retirement (till 31/12/2015)

22IATA Maintenance Cost Conference 2016 – © SGI Aviation

Index

SGI Aviation

Introduction

Retirement

- Historical trends

- Retirements by age, type and region

- Storage and disassembly locations

Retirement drivers

- Economy and oil prices

- Introduction of new aircraft

- Components value and demand

Conclusion

23IATA Maintenance Cost Conference 2016 – © SGI Aviation

Components value and demand

Supply and demand in the component market also influence the retirement curve

OTHERSNAVIGATION

FLIGHT

CONTROLS

ELECTRICAL

POWERAPU

LANDING

GEARS

AIRFRAMEENGINESTOTAL

Indicative breakdown of individual component values

Source: SGI Aviation proprietary databases

24IATA Maintenance Cost Conference 2016 – © SGI Aviation

Index

SGI Aviation

Introduction

Retirement

- Historical trends

- Retirements by age, type and region

- Storage and disassembly locations

Retirement drivers

- Economy and oil prices

- Introduction of new aircraft

- Components value and demand

Conclusion

25IATA Maintenance Cost Conference 2016 – © SGI Aviation

Over 15,000 aircraft retired in last 36 years

Average retirement age around 27 years

Freighter conversion adds about 10 to 20 years of life

Conclusion

World growth and price of oil is one of the main

drivers

Geopolitical events and regulatory restrictions also

heavily influence retirements

Parts value is heavily dependent on actual condition

Main value is in the engines

Airframe has limited value and some structural parts

are difficult to sell

26IATA Maintenance Cost Conference 2016 – © SGI Aviation

Questions?

Joost Groenenboom – Executive Director

T +31 20 880 4238 M +31 65 0736001

Email: [email protected] │Web: http://www.sgiaviation.com

Recommended