i

ii

Affidavit

I, ERI NAGAI, hereby declare

1. that I am the sole author of the present Master’s Thesis, "The Value of Resources", 92 pages, bound, and that I have not used any source or tool other than those referenced or any other illicit aid or tool, and

2. that I have not prior to this date submitted this Master’s Thesis as an examination paper in any form in Austria or abroad.

Vienna, 09.06.2011 Signature

iv

v

Acknowledgements

I send my heartfelt appreciation to my supervisor Dr. Johann Fellner for all his kind

support and attention. I also wish to send my BIG thank you to my family for their

endless love and patience. Special thank you to little Marceau, for his smiles of hope.

To my friends, for their love and encouragements. And to C, for celebrating and

believing in me.

vi

vii

Table of Contents

Table of Contents .....................................................................................................vii

List of Abbreviations................................................................................................. ix

I. INTRODUCTION .................................................................................................. 1

1. Background and Motivation ............................................................................. 1

2. Research Aims and Questions........................................................................... 2

II. CURRENT STATUS AND LEGAL FRAMEWORK CONCERNING THE

TREATMENT OF ELECTRONIC APPLIANCES ............................................... 4

1. Sustainability ...................................................................................................... 4

2. Hazardous Substances and Material Recovery ............................................... 6

3. European Union ................................................................................................. 7

3.1. The Waste Electrical and Electronic Equipment (WEEE) Directive..... 8

3.2. The Restriction on the use of certain Hazardous Substances in

electrical and electronic equipment (RoHS) Directive ................................... 9

3.3. The Ecodesign Directives and the REACH Regulations ....................... 10

4. Japan ................................................................................................................. 11

5. Basel Convention on the Control of Transboundary Movements of

Hazardous Wastes and Their Disposal .............................................................. 13

6. Material Declaration Drivers and Programs................................................. 14

III. RESEARCH METHODOLOGY..................................................................... 17

1. Target Products ................................................................................................ 17

2. Methodology ..................................................................................................... 17

3. Data Collection and Analysis .......................................................................... 18

3.1. Challenges in Data Collection .................................................................. 18

3.2. Material Categorization............................................................................ 19

3.3. Composite Materials and Printed Circuit Board (PCB) ....................... 20

3.4. Price Data................................................................................................... 21

IV. RESULTS ........................................................................................................... 22

1. Refrigerator-Freezers ...................................................................................... 22

2. Washing Machines ........................................................................................... 27

3. Televisions and Monitors................................................................................. 31

3.1. CRT Displays ............................................................................................. 31

3.2. Flat Panel Displays .................................................................................... 35

viii

4. Computers......................................................................................................... 40

4.1. Desktops ..................................................................................................... 40

4.2. Laptops ....................................................................................................... 44

5. Mobile Phones................................................................................................... 47

V. DISCUSSIONS .................................................................................................... 55

VI. CONCLUSION .................................................................................................. 61

Bibliography ............................................................................................................. 63

List of Figures ........................................................................................................... 70

Appendix ................................................................................................................... 72

ix

List of Abbreviations

COP Conference of the Parties

CPU Central Processing Unit

CRT Cathode Ray Tube

EEE Electrical and Electronic Equipment

EuP Energy-Using Products

E-waste Electronic Waste (also WEEE)

FPD Flat Panel Display

LCD Liquid Crystal Display

LDCs Least Developed Countries

PCB Printed Circuit Board

RoHS Restriction of the Use of Certain Hazardous Substances in Electrical

and Electronic Equipment (European Union directive)

WEEE Waste Electrical and Electronic Equipment (also e-waste)

x

xi

Abstract

The electronics industry is a constantly and rapidly evolving industry, and

even the material composition within the same category of appliances is continuously

evolving with new technology, customer preferences, legislative changes, and

nowadays, health and environmental concerns. This paper follows the changes in the

material composition and the relative value of those materials for seven categories of

electronic appliances: refrigerators, washing machines, CRT displays, flat panel

displays, desktop computers, laptop computers, and mobile phones.

The results showed that the relative value of resources contained in an

electronic product, compared to its market price, is very low for all products studied.

This indicates that despite growing concern today, even a large-scale increase in

resource prices, including precious metals, is unlikely to lead to any significant

increase in market prices of electronic products. The study also indicated that the

smaller and more high-tech an appliance becomes, the less valuable and more

difficult it tends to become for resource recovery at the end of its lifecycle.

xii

1

I. INTRODUCTION

1. Background and Motivation

At the backbone of every economy are resources. Over the history of

mankind we have continuously been learning to extract and modify natural resources

to meet our diverse needs. Different resources have been sought after and considered

valuable at different times. Substances like lead and mercury used to be in extensive

use, but their applications have been phasing out since their toxic effects on

organisms have become wide-known. Plastic material, invented in the late 19th

century, is today an absolutely indispensable material in a wide range of industrial

products. Then there are also some resources, such as gold, silver, and copper, which

have always been valuable to men. The application and the associated value of

material resources are constantly evolving and changing along with the development

and the needs of our society.

In earlier times, the manufactured products or tools used by men were not so

complicated in their composition or structure. Perhaps only a few materials were

combined to form one product. Also the assembly process and the research and

design behind the product were not always particularly sophisticated or complicated.

Such simplicity began to change with the ever-progressing knowledge, skills, and

technology, and eventually began the manufacturing of complicated and high-tech

electrical and electronic equipments. These evolved from relatively-basic in structure,

design, and ability to highly-complicated and multi-tasking in just over a few

decades as the society pursued after smaller, lighter, faster, “more able” products.

The fastest changing products are inevitably in the IT-sector, namely phones

(particularly mobile) and computers, but even household appliances have seen

noticeable transformations.

In its earlier days, the electronics industry single-mindedly explored higher

performance. Consumers continuously demanded improved efficiency and

convenience at lower costs. Today’s newest challenge, however, is the need for

reconsideration of material composition and design while maintaining the same level

of performance quality, as the environmental concerns stemming from the electronics

industry heighten and the call for a proper disposal of end-of-life electric and

2

electronic equipments intensifies. As the electronics manufacturing industry adapts

its appliances’ design and composite materials in response to such multidimensional

technical, social, and environmental demands, what happens to the “value” of

resources contained in these products? How exactly has the use of resources and the

relative values of those resources in electric and electrical appliances changed and

developed over time?

2. Research Aims and Questions

The aim of this paper is to conduct an analysis on the development of

“relative value” of materials over time in consumer electrical/electronic equipments

and household electronic appliances. With technological advancements the efficiency

of our products is continuously increasing, combining less resource more efficiently

for higher performance. At the same time, the absolute quantity of resources being

mined and consumed has been expanding at a remarkable rate as well, keeping up

with the increasing speed of economic developments and consequently people’s

pursuit of greater material wealth. This increased demand for resources can have an

influence on their prices, particularly on those supplies that are high in value and/or

relatively limited in supply, which in turn may influence the pricing of manufactured

goods that rely on those materials as ingredients.

What happens to the value of resources, as electronic products evolve from simple

combinations of a few metals to a complex assembly of numerous parts, and the

utility value of the produced appliances become increasingly more dependent on

research and development, i.e. human intelligence and skills, rather than primarily

on the cost of the resources contained?

Do the used resources decrease or increase in relative value within the products over

time?

Does the increased efficiency and fierce market competitions work together to keep

the price under control, thus holding the relative value of resources more or less

constant?

3

As products’ composite materials diversify, are there grounds to be concerned for the

dwindling availability and the price hikes of the so-called “scarce” or “precious”

metals, or are their contribution to the composition minimal enough to not make a

serious impact on the end-pricing?

Are there any materials that are consistently important and irreplaceable?

These are some of the questions that could begin to be addressed by tracking

the changing value of materials within our electrical and electronic appliances.

4

II. CURRENT STATUS AND LEGAL FRAMEWORK CONCERNING THE

TREATMENT OF ELECTRONIC APPLIANCES

The research presented in this paper belongs in the wider investigation of the

development of resource use and the environmental and economic implications of

sustainable resource management. In order to think about these larger questions in

the context of value and importance of resources, it becomes vital to understand the

basic overall trend in the use of resources and how the relative values of these

resources have been evolving through time.

Generally the research on resources focuses on critical materials and

hazardous materials, and so far there has not been a significant amount of studies

being conducted on the general trends and changes on the material composition of

electronic equipments as such and the accompanying investigation into the value of

resources contained in them. Especially driven by growing legislative changes

related to the use of certain substances and the treatment of waste equipments, much

of the studies related to material compositions of electrical and electronic products

have focused on the reduction and treatment of hazardous substances for

environmental reasons and the product design and its recycling potential for high-

value recoverable materials for economic reasons.

1. Sustainability

In recent times there have been growing concerns over the negative impacts

caused by industry and its products on both society and the environment. The

concept of sustainability has therefore gained increasing attention, and with it, our

responsibility to live in a more sustainable manner. It has been understood for a

while now that the current scale of resource use is not well-managed and therefore

unsustainable in the long-term. The society today is faced with a rapid and

accelerating population growth, a general augmentation in wealth, and an incredible

rise in the consumption of energy, materials, and other resources. At the ongoing rate

of consumption, particularly in developed countries and emerging markets, access to

a fair share of resources are endangered for future generations, and the potential for

resource exhaustion may be a realistic concern. Furthermore, with expanding

5

scientific acknowledgement that critical global environmental problems such as

climate change is heavily influenced by human activities, there is a clear and urgent

need to address how our modern society consumes and often wastes valuable

resources.

One of the most discussed areas under the issue of sustainable resource use is

the electronics sector – the way in which we manufacture, use, and dispose of the

electrical and electronic equipments (EEE). The electronics industry has continued to

show a remarkable growth, and many electronic devices have become absolutely

indispensable to the modern way of life. Nevertheless, despite such a close

integration into our lifestyle, a functioning and sustainable operation of material

management has not yet been fully implemented in this sector. In fact, much of the

EEE boast a rather unsustainable cycle of consumption, as they are often replaced

long before the intended lifetime due to increased performance, reduced cost, and

innovative designs for each upcoming generation of product. This unsustainable

pattern of consumption is further underlined by a fierce competition within the

industry and the availability of a wide variety of products.

The electronics companies have been coming under heavy attacks from

environmental organizations, given their unsustainable material consumption due to

increasingly shortening product lifecycles, the use of hazardous materials and

processes, and the generation of waste both during production and at end-of-life. The

industry has also been criticized for their frequent choice of disposal for end-of-life

appliances, effectively dumping them in developing countries where regulations

against toxic substances have not been established yet. The improper dumping and

landfilling of harmful substances may cause serious damages to ecosystems and

compromise the health of living organisms including humans. Wealthy, developed

societies have been enjoying the convenience offered by modern technology without

the willingness to take responsibility for the massive amount of waste generated as

the byproduct of the benefits. These issues are bound to intensify as the developing

nations catch up with developed nations on resource consumption patterns. Faced

with the increased attention on the handling of the waste stream and the emphasis on

producer responsibility, the environmental performance of end-of-life processing has

become important, and appropriate legislative adaptations have been taking place in

order to tackle this issue (Hester and Harrison, 2009).

6

As an example, in the EU, the European Commission proposed a “Strategy

on the Sustainable Use of Natural Resources used in Europe” on 21 December, 2005,

focusing on reducing the environmental impacts stemming from resource use in the

context of growing economy. Reducing the environmental impacts associated with

resource use is believed to be a decisive factor for the EU to achieve its sustainable

development goals. Other initiatives addressing sustainability are also being

implemented on local, regional, and global scales. A strategic, efficient, and well-

controlled use of resources is today understood to be crucial for a strong and sound

development of any economy.

2. Hazardous Substances and Material Recovery

One of the key focuses in the study of material composition is the question of

hazardous materials. The recycling of home appliances and other electronic devices

has become a legal requirement in some countries in an attempt to keep them out of

the waste stream and ultimately the environment. The objective is to avoid damages

on the health of ecosystems by preventing hazardous and toxic substances from

leeching into the environment.

Another important aspect is the concept of resource recovery, or recycling:

the process in which certain materials contained in waste products are collected and

separated for reuse. Resource recovery, if successfully carried out, can not only be

environmentally friendly but also be cost-effective, as it reduces the amount of waste,

saves space in landfills, and conserves natural resources. Reclamation specifically in

metal compounds and elements from products, buildings, and various waste is called

urban mining. The precious metals that are particularly sought after in urban mining

include e.g. gold, silver, platinum, and iridium, which can be found in various

everyday consumer electronics from phones to cameras to televisions. With growing

concerns about metal resource scarcity and recently increasing mineral prices, much

research has been conducted over the effectiveness of the metal recovery processes,

the economic advantages, and the potential benefits reaped by the reuse.

For example, over the years the use of gold has expanded beyond their

traditional role in jewelry and investment. Nowadays gold is also an integral

component in industrial applications, especially in electronic devices. According to

7

Hagelüken and Corti (2010), well over 300 tons of gold are used in electronics

annually, therefore offering an important recycling potential for the secondary supply

of gold from end-of-life electronic equipments. Electronic equipments may also

contain other precious metals, such as silver, palladium, and to smaller extent,

platinum and ruthenium.

Keeping hazardous substances ‘out’ and keeping valuable resources ‘in’:

these are the drivers of the legislative changes concerning resource use and

management in the electronics industry.

3. European Union

Realizing that societies as a whole, and in particular the electronics industry,

must find a lifestyle built on responsible and sustainable way of production and

consumption, the European Commission has introduced a series of legislation based

on Producer Responsibility principle over the last several years. This principle calls

for a creation of link between the production and disposal phase of a product and

addresses all concerned actors, i.e. manufacturers, distributors, consumers, and

operators, in the proper management of the life cycle of EEE. Producer

Responsibility principle stands as an extension of the traditional ‘polluter pays’

principle. Therefore, the responsibility for the proper disposal of end-of-life

equipments is shouldered by the original producer.

The producer responsibility principle calls for:

• Attaining the objectives for a more efficient resource use and reduction of

the amount of waste being sent to landfill

• The redirection of the end-of-life products for reuse and recycling

• The abolishment of the use of certain hazardous materials and minimizing

energy consumption throughout product lifecycle

Therefore, the legislations based on producer responsibility encourage producers to

design, manufacture, and market products that:

8

• Reduce or eliminate the use of hazardous materials

• Incorporate greater amounts of recycled materials

• Makes end-of-life treatment easier

• Minimize waste

• Can be re-used

• Are more resource-efficient throughout their lifecycle

As the presence and essentiality of the electrical and electronic devices grow

in our lives, the manufacturers are faced with a greater responsibility for a

sustainable management of their industry. It is growingly required by legislation and

expected by consumers (Hester and Harrison, 2009).

Of the numerous EU directives and regulations intended to incorporate

producer responsibility principle, the major legislations pertaining to the electrical

and electronics industry include: the WEEE, RoHS and Energy using Products

Directives, and the REACH Regulations.

3.1. The Waste Electrical and Electronic Equipment (WEEE) Directive

The Waste Electrical and Electronic Equipment (WEEE) Directive

(2002/96/EC) came into force on 1 July, 2006. The Directive is an important

cornerstone of the EU’s environmental policy on electronic waste, and it addresses a

highly complex waste flow of obsolete, or end-of-the-life, equipments in terms of:

• The variety of products

• The association of different materials and components

• The contents in hazardous substances

• The growth patterns of this waste stream

The aim of this European Community Directive is to set collection, recycling,

and recovery targets for all types of electrical goods, ultimately aiming to create a

closed loop economy. It also encourages product design modifications that make

WEEE easier to be dismantled, recycled, and recovered (Hagelüken and Corti, 2010;

Hester and Harrison, 2009; Huisman et al., 2007). This is an innovative approach that

9

challenges the widespread style of production by the manufacturers of EEE and its

component, which traditionally regarded performance in use as the highest priority in

design (DEFRA, 2004). The WEEE covered under the Directive are divided into the

following ten categories:

1. Large household appliances

2. Small household appliances

3. IT and telecommunications equipment

4. Consumer equipment

5. Lighting equipment

6. Electrical and electronic tools

7. Toys, leisure, and sports equipment

8. Medical devices

9. Monitoring and control instruments

10. Automatic dispensers

The Directive further seeks to minimize and control toxic substances from

escaping into the environment by placing regulations on both ends of the product’s

lifetime, at manufacturing and disposal phases. A selective treatment of collected

WEEE is mandated in order to remove hazardous materials and components from the

waste stream, with some of the items requiring special treatments. This is further

explained in the closely linked RoHS Directive (Hester and Harrison, 2009; Huisman

et al., 2007).

3.2. The Restriction on the use of certain Hazardous Substances in electrical and

electronic equipment (RoHS) Directive

The Restriction on the use of certain Hazardous Substances in electrical and

electronic equipment (RoHS) (2002/95/EC) is the complementary Directive to the

WEEE Directive. The RoHS Directive seeks to reduce the environmental impact of

electrical and electronic appliances by restricting the use of the following six

hazardous substances during the manufacturing process:

10

• Lead (Pb)

• Mercury (Hg)

• Cadmium (Cd)

• Hexavalent chromium (Cr6+)

• Polybrominated biphenyls (PBB)

• Polybrominated diphenyl ether (PBDE)

Any new electrical and electronic products that contain any of these six

restricted substances are banned from being sold on the EU market. In summary, the

WEEE Directive and the RoHS Directive together regulate not only the application

of hazardous substances within the equipments but also streamline the disposal

process at their end-of-life (Bhuie et al., 2004; Hester and Harrison, 2009). Such a

change will still take some time to show up in the end-of-life waste of products with

a long-lifetime, such as televisions and refrigerators, but for products with a shorter

lifetime, such as computers and mobile phones, the impact on the waste stream

should start appearing shortly (Hester and Harrison, 2009).

3.3. The Ecodesign Directives and the REACH Regulations

The Ecodesign Directive for Energy-using Products (2005/32/EC) became an

EU law in August 2005 and has been transposed by Member States into national law

during the following two years. Ecodesign is a new concept that promotes the

reduction of energy consumption by energy-using products (EuP) such as household

electrical appliance. The Directive establishes a framework whereby manufacturers

of EuP are mandated to improve energy efficiency of their products throughout their

lifecycle and to reduce their overall negative environmental impacts. The framework

directive is intended to apply to all EuP that are placed on the market, and its scope

also includes individual external parts that are intended to be incorporated by end-

users into products placed on the market.

The Ecodesign Directive is intended to instigate significant changes on the

design phase of a wide variety of EEE. The main objective of the legislation is to

enhance energy efficiency throughout a product’s lifecycle, from the extraction of

the raw material through to recycling and disposal. It effectively targets

11

improvements in the initial design phase because this should be the key stage where

the product’s resource need and energy efficiency are determined. Furthermore,

information regarding the product’s environmental performance and energy

efficiency must be made transparent ideally on the product itself, thereby providing

consumers the means to assess the products prior to purchase. Although the Directive

is primarily aimed at the reduction of energy use, it takes into consideration related

environmental parameters such as general resource use, waste, and recyclability. In

2009 the Directive was revised to extend its scope to include energy-related products,

i.e. all goods having an effect on energy consumption during their use, such as

windows and insulation materials (EUROPA, 2011; Hester and Harrison, 2009).

Focusing on the research of hazardous substances is REACH, the Regulation

on Registration, Evaluation, Authorisation and Restriction of Chemicals (EC

1907/2006), that entered into force on 1 June, 2007. The main of goals of REACH

are to ensure an improved protection of human health and the environment through

early and clear identification of the potential risks posed by chemical substances and

to enhance innovation and competitiveness of the EU chemicals industry. It obliges

the chemical industry to perform proper risk management and to provide appropriate

safety information to the users. The regulation also promotes the progressive

substitution of the most harmful substances for which suitable alternatives have been

identified (EUROPA, 2011).

4. Japan

In Japan, the Law for the Recycling of Specified Kinds of Home Appliances1,

more commonly known as Home Appliance Recycling Law (HARL), came into

effect in April 2001. The law is a part of a series of measures put forth by the

government with the aim of establishing a recycle-based society. Its goal is to create

an appropriate waste treatment flow and promote the efficient use of resources in

order to achieve a more closed-loop-material society. The following four target

appliances were designated in the original legislation for their large product volume

and number of sales:

1*%&'+($ #"!)

12

• Air conditioners

• Refrigerators

• Televisions

• Washing machines

The law places responsibility principally on the manufacturers and retailers to

collect and recycle their own appliances, although the actual financial burden of

recycling and transport is placed on the consumers. First, the consumer is to take

back the home appliance to be discarded to the retailer and pay a collection/transfer

fee and a recycling fee. Then the retailer transports the waste home appliance to a

designated collection site, and finally, the collection site transfers the collected

appliances to the recycling facility to be recycled. Before this law was enacted, these

products were either returned to the retailer or simply collected as bulky items, and in

both cases eventually shredded and landfilled with only a minor recovery of reusable

metals. The HARL was a first piece of legislation of its kind in Japan that put into

practice the concept of Extended Producers Responsibility, requiring the producers to

carry full responsibility for their manufactured goods all the way to the very final

stage of their lifecycle (Matsuto et al., 2004; Murakami et al., 2006).

Although at the time of enactment there were concerns for the increase in

illegal dumping of appliances as a possible side effect of the law, so far this take-

back system has been working smoothly overall without any noticeable increase in

illegal dumping. The number of recovered appliances has been steadily increasing

since the implementation of the law (Murakami et al., 2006; Nakamura and Kondo

2006).

Some key differences between the European approach and the Japanese

approach can be observed. In the European legislations the front-end payment

scheme is often employed, which encourages cost-internalization (i.e. recycling costs

are included in the market price of the product and hidden from consumers) or

advance recovery fees (recovery fees are identified on the receipt at the time of

purchase). In contrast under the Japanese HARL, the fees for the collection, transport,

and recycling of the appliances are paid by the consumer at the time of drop-off

(INFORM, 2003; Matsuto et al., 2004). Another noteworthy distinction between the

recycling laws in Japan and the EU is the different emphasis on targets to be

13

achieved. Whereas the EU’s WEEE Directive sets collection targets, the HARL

emphasizes recycling goals, requiring the following recycling rates for each type of

appliance (INFORM, 2003):

• Air conditioners: 60 percent

• Refrigerators: 50 percent

• Televisions: 55 percent

• Washing machines: 50 percent

On 2 December, 2008, an amendment to the HARL was adapted, adding

liquid-crystal/plasma television sets and clothing dryers to target appliances. The

amendment also raised the required recycling rates for three of the four appliances

included in the original law. The new regulation has been in enforcement since 1

April, 2009 (Japan for Sustainability, 2009).

5. Basel Convention on the Control of Transboundary Movements of Hazardous

Wastes and Their Disposal

The international legal framework that includes the treatment of electronic

waste (e-waste) in its scope is the Basel Convention on the Control of Transboundary

Movements of Hazardous Wastes and Their Disposal, adopted on 22 March, 1989

and entered into force on 5 May, 1992. Generally known simply as the Basel

Convention, it is a comprehensive international treaty to control the movements of

hazardous waste between nations and most specifically to prevent its flow from

developed to least developed countries (LDCs). The Basel Convention emphasizes

environmentally sound management of hazardous waste, and its specific objectives

include:

• The reduction of transboundary movements of hazardous and other wastes

• The prevention and minimization of the generation of hazardous wastes

• The promotion of the transfer and use of cleaner technologies

14

The Basel Convention is the only existing global international legal

instrument that addresses the comprehensive dimensions of the issue of hazardous

and other wastes and lays down the grounds for a structured control system for their

proper treatment and disposal (Mobile Phone Working Group, 2008). Recognizing

the increasing significance of e-waste in the global waste stream and the high cost

and toxicity resulting from their disposal, the eighth meeting of the Conference of the

Parties (COP8) to the Convention, held in December 2006, focused on the creation of

progressive solutions for the effective management of e-waste (Davis, 2006).

6. Material Declaration Drivers and Programs

One of the essential factors that determines the product’s overall resource

consumption, safety, environmental performance, and recyclability is its

comprehensive material composition. Knowledge of the composition may be a

prerequisite in selecting the most appropriate technology for recycling and in the

regulation/restriction of the use of hazardous materials in industrial production.

Public calls for improved material content specifications and transparency

have finally started gaining momentum in recent years. Going further than

legislations that were aimed at controlling the use of hazardous substances and

streamlining waste management, regulatory, technical, and market pressures are

pushing the EEE manufacturers to clearly identify and publish the information

regarding the chemical and material content of their manufactured products.

One of the causes of the lack of transparency in the material composition of

electronic appliances is that quite often a product is not completely manufactured in-

house. Different components may be made by different suppliers, and the details of

these external components do not necessarily get communicated throughout the

supply chain. There are growing movements in the electronics industry to implement

a harmonized material declaration system in order to facilitate the flow of

information within and from the industry (O’Connell and Brady, 2002).

A material declaration is a disclosure of the material content of a product. It

could either be a “positive” declaration, listing the types and quantities of substances

that a product contains, or a “negative” declaration, stating the hazardous and

regulated substances that the product does not contain. Currently material declaration

15

is not required by law but only done on a voluntary basis, and no single unified

declaration mechanism exists on a global scale. Each association within the industry

has developed separate standards and declaration programs on its own. Below is a

description of some of the declaration systems in use today:

EIA (Electronic Industries Alliance)2 Material Declaration Guide: developed in

2001, this provides a guideline on sharing material content information between

suppliers and final manufacturers. Its three primary purposes are: to identify

materials that are relevant in electrical and electronic equipments, to determine the

disclosure threshold level for each material, and to establish a set format for

disclosure (O’Connell and Brady, 2002).

IPC (Association Connecting Electronics Industries) Materials Declaration: IPC has

a series of standards, most relevantly IPC-1751A and IPC-1752A, that establishes

and improves a standard reporting format for information exchange between

participants in the supply chain (IPC, 2011).

Joint Industry Guide – Material Composition Declaration for Electrotechnical

Products: Launched together by the Consumer Electronics Association (CEA),

DIGITALEUROPE, and the Japanese Green Procurement Survey Standardization

Initiative (JGPSSI) and revised in 2011, this guide is meant to facilitate the flow of

material content information in electrotechnical products across the global supply

chain. It incorporates the most up-to-date regulatory and market requirements and

also covers the latest substances considered under the EU’s REACH regulation (CEA,

2011).

Having different standards and formats is likely to hinder the promotion of an

industry-wide smooth exchange of data, especially considering the dynamism that

characterizes the electronics industry. Unfortunately, the likelihood of the realization

of a global materials declaration system is very low. Aside from the many different

2 The EIA ceased operations on 28 February, 2011. The former sectors of EIA are the Electronic

Components Association (ECA), JEDEC, Government Electronics and Information Technology

Association (GEIA), now part of TechAmerica, Telecommunications Industry Association (TIA), and

Consumer Electronics Association (CEA).

16

declaration standards currently available, individual companies have their own

proprietary systems, a factor that complicates the situation even further. As material

declaration in the supply chain is not legally mandated or controlled but only

voluntary, it is up to the manufacture and the supplier to agree on which standard

they will employ (Castorina, 2011; O’Connell and Brady, 2002).

The transparency of the products’ material composition has been improving

also at the level accessible by consumers, especially concerning potentially

hazardous substances, increasingly on a voluntary basis. For example, Nokia states

on its website that it has created a full material declaration together with its suppliers

so that it can respond to any concerns that may arise about the substances used in its

products. Nokia also provides the so-called Nokia Substance List online, which

identifies substances whose use has been voluntarily banned or restricted by the

company (Nokia, 2011b). Motorola has also published some data concerning the use

of lead and other toxic substances in their phones (Motorola, 2007).

Even if the outlook of a global materials declaration standard is not promising,

the general movement toward an increased transparency and accessibility of material

composition data of EEE is a favorable development from the perspectives of better

resource management, environmental protection, consumer safety, and researches

concerning technology and materials. In the long-term, even without a global

harmonization of the mechanisms, some form of a verifiable material declaration

may become an industry requirement.

17

III. RESEARCH METHODOLOGY

1. Target Products

The following categories of consumer electrical and electrical appliances

were selected for the purpose of this study, primarily based on their widespread use

and data availability for both material composition and market prices:

• Freezer-Refrigerators

• Washing Machines

• Televisions and Monitors (CRT & Flat Panel Display)

• Personal Computers (Desktop & Laptop)

• Mobile Phones

2. Methodology

First, data was collected on the material composition for each category of

appliances. These were aggregated and used to estimate the average material

composition for the years in which they were manufactured. At the same time, the

historical global market price of each raw material contained in the target appliance,

at the given time of its manufacturing, was obtained.

Then, based on the average material composition, the theoretical “raw

material price” of the appliance, strictly expressed as the sum of the market prices of

the raw materials for the given year or time period, was determined for each

appliance. Meanwhile, the actual historical market prices of the appliances were also

collected, and eventually the average selling price of the appliance was determined

for relevant years.

Additional interest was in finding out about how much the material cost

contributed to the final market price of a product. The relative value of the raw

materials contained was determined as a function of the two prices – in a comparison

between the raw material price and the actual market price. This was repeated for all

five types of appliances through time to see if any significant changes and trends

could be observed.

18

The relative value of the raw materials was expected to decrease over time, as

the composition of the electronic appliances became more complex; the number of

materials used in each appliance increased; and the role of skilled labor, technical

knowledge, and innovation in design and manufacturing became relatively more

important than the ingredient cost from the materials contained.

3. Data Collection and Analysis

3.1. Challenges in Data Collection

Breaking down the manufactured electrical and electronic equipments into

their components and determining the detailed material composition is quite a

complicated task. Some studies comment on the difficulty of doing such an analysis,

primarily highlighting the challenges involved in the analytical process, which

inevitably leads to a lack of enough appropriate data.

First, substantial differences in composition exist between different types of

electric and electrical appliances and even within individual types of appliances. For

example within the personal computer industry, compositions of desktop and laptop

computers are noticeably different, as they are designed for uses in different manners

and settings, despite both performing ultimately the same functions (Chancerel and

Rotter, 2009).

Furthermore, the material composition of appliances is generally not constant

over time, making it extremely difficult to determine the typical composition of an

appliance at any given time (Bhuie et al., 2004; Hester and Harrison, 2009).

Chancerel and Rotter (2009) state that due to the continuous changes in the design

and function, the mechanical and material properties of electronic appliances are

highly variable and difficult to track down. As discussed earlier, these fluctuations in

the raw material content are driven by both technological progress and new

legislative regulations. A good example of technological advancement is a switch

from CRT-based televisions and monitors to flat panel displays in the television and

computer industry (Hester and Harrison, 2009). An example of a change prompted

by legislative regulations is the elimination of lead as a result of the EU’s RoHS

Directive. Traditionally lead-based solder, which is mainly used to attach metallic

19

components to each other and to printed wire assemblies, is now being replaced by

lead-free solder (Bhuie et al., 2004).

In addition, some products such as mobile phones and computers contain a

large number of materials closely interlinked (some substances being vital but

miniscule in amounts), which also poses significant challenges when it comes to

taking them apart. As will be explained later, many studies and recycling facilities

simply categorized some components with complex structures as “composite

materials” and do not break them down any further.

Finally, the choice of a variety of methods that can be employed in the

analysis of material composition means that the results from different studies may

give slightly different figures, making the exact trends in composition unclear. This

is particularly true for the said composite materials, with different studies opting to

treat them differently according to their needs. In sum, the sheer heterogeneity

present within the EEE components makes the data assembly and analysis a highly

complicated process (Chancerel and Rotter, 2009; Doctori Blass et al., 2008).

As an important side note, the competition factor must also be considered.

Doctori Blass et al. (2008) point out that the rapid evolution of material composition

in mobile phones is compelled by fierce competition within the industry, and

therefore the companies are not willing to make the product composition details

readily available for any given year or model. In fact, this attitude is not exclusive to

the mobile phone industry. The companies and manufacturers of any appliances are

generally unwilling to disclose detailed information on the material components and

structure of their products, unless they are obligated to do so under legal

requirements and/or wish to demonstrate their environmental initiatives and to show

their compliance with the safety standards. For this reason, much of the data

concerning the material composition of EEE were obtained not directly from

manufacturers but from waste treatment and recycling centers.

3.2. Material Categorization

In the process of identifying and categorizing the relevant materials found in

the appliances, various similar materials were combined and assigned to the same

20

category, to the extent that it did not have any significant impact on the consideration

of the overall average material composition.

• Iron and steel were combined under “Ferrous Materials.”

• All plastic-materials, e.g. Polypropylene, PS&HIPS 3 , ABS 4 , PVC 5 ,

Polyurethane, and other assorted plastics, were combined under the

category “Plastics.”

• Silicon (Si) and Silica (SiO2) were combined under “Silicon.”

• Brass was calculated as consisting of two-thirds copper and one-third zinc

• Glass and ceramics were combined into one category “Glass/Ceramics,” as

they are generally used interchangeably for the same function6.

• Similarly, for mobiles phones, Platinum (Pt) and Tantalum (Ta) were

combined under “Platinum (Pt) or Tantalum (Ta),” as they can be used

interchangeably from a functional perspective7.

• The category “Other Metals” was used as the umbrella category for metals

that were only contained in trace amounts and did not have a significant

enough presence in the overall consideration of material content analysis

or when a more detailed breakdown was not available.

3.3. Composite Materials and Printed Circuit Board (PCB)

In some studies the material composition was broken down only into parts,

such as electronic components and chipboards, and not further down into the

individual elements of those parts. A relatively high fraction of studies also used the

category “composite materials.” Composite materials can refer to any complex

assemblies containing interconnected metals and plastics, which are not

mechanically separable into homogeneous material fractions. These include electrical

parts with interconnected materials, such as printed circuit board (PCB), motors, and

CD drivers (Chancerel and Rotter, 2009).

3 polystyrene & high-impact polystyrene 4 acrylonitrile butadiene styrene 5 polyvinyl chloride 6 Most studies consulted also considered them in one category “glass or ceramics.” 7 although ideally, from a resource value point of view, they should be separated

21

In cases where sufficient information could not be obtained, these composite

materials were classified as “other” along with minor miscellaneous materials.

However, when the components of the breakdown could be identified as PCB or

other similar electronic parts, the average material content of a PC motherboard,

provided by Brady et al. (2003), was applied for the analysis. According to Brady et

al. (2003), for most compounds, only minor differences were observed between the

material content of one appliance’s circuit board to the other. Therefore, in this study,

the material breakdown from of an average computer PCB from Brady et al. (2003)

was assumed to be constant for all types of circuit boards and applied not only to

computers but to other types of appliances equally. This method was employed

particularly for the reconstruction of data provided by Townsend et al. (2004) and

also for data from several other studies.

3.4. Price Data

Many of the historical price data was obtained from The value of a dollar :

prices and incomes in the United States, 1860-2009 by Derks (2004). For

refrigerators/freezers and washing machines, most of the price data were taken

originally from the ratings reports published in Consumer Reports magazine, as

compiled and reported by Horie (2004) and Bole (2006), respectively. All historical

prices were adjusted for inflation to the 2011 level and converted to USD. Most of

the historical raw material prices were taken from the data provided by the United

States Geological Survey (USGS).

22

IV. RESULTS

1. Refrigerator-Freezers

Various types of refrigerator-freezers were considered for the study. Here, the

results for the typical Japanese refrigerator-freezers and western (primarily based on

American) refrigerator-freezers are presented. These were analyzed separately due to

the consistent differences in their weight and material composition.

Weight and Material Composition

While the main material constituent of the American (and also European)

refrigerator-freezers is ferrous metals, at an average of about 65%, the Japanese

counterparts contain less ferrous metals and about the same amount of plastics, both

around 40-50%. The American appliances were also much larger and heavier,

averaging around 120kg, whereas the Japanese ones averaged around 70kg. The

difference is most likely due to the difference in the size and spaciousness of

households in the US and Japan. The Japanese manufacturers use much more plastic

and less ferrous metals in order to keep their appliances smaller and lighter to fulfill

the Japanese consumers’ preferences and make them suitable for the Japanese

kitchens, typically limited in space.

From the late 1940s to 1970s, especially in the US, the average refrigerator-

freezers overall became more multi-functional and larger in size, keeping up with the

advancing technology and consumer demand for more storage space. However, the

development in the functions and the average size of refrigerator-freezers seems to

have peaked and settled down around the 1980s, and since then, trends show that

both the size/weight and the material composition have remained more or less

constant (Street, 2011). The results from this study, covering the time period 1982-

1998 over the two categories, confirmed this pattern. Figure 1 shows the weight and

material composition of US refrigerator-freezers from 1990 to 1998. Figure 2 shows

the weight and material composition of Japanese refrigerator-freezers from1982-

1998. In neither Japanese nor American refrigerator/freezers, no major differences in

weight or material composition were observed over time during this period.

23

This is also in agreement with the findings and assumptions of Horie (2004),

who states that there have been no major shifts in the material composition of

refrigerator-freezers for decades. The only exception is the change in refrigerant

following the banning of the ozone-depleting substances by the Montreal Protocol,

which entered into force in 1989, but the change in both the material composition

and the total weight was found to be negligible in the comparison of appliances

before and after the implementation of the Protocol.

Figure 1. US Freezer-Refrigerator Weight & Material Composition [kg]

Figure 2. Japanese Freezer-Refrigerator Weight & Material Composition [kg]

[kg]

[kg]

24

Prices and Values

In terms of market prices, Dale et al. (2009) conducted a study on the

changing efficiency levels and price trends of major appliances including

refrigerators and washing machines. It was found that although the analysts of the

Department of Energy had predicted the appliance prices to increase in response to

efficiency gains by the market, the actual trends actually revealed that between 1970

and 2000, refrigerator and washing machine prices in the market declined while

appliance efficiencies increased. The process of technological change is assumed to

be responsible for this contradiction, in which overall production costs, especially for

high-efficiency appliances, are decreasing over time. This trend of the inflation-

adjusted prices decreasing through time was found in all four appliance types tested

in the study8. In the time period covered in this study, the prices did not show any

decreasing trend but rather stayed more or less constant in both categories. The

developments in market price, material price, and weight for both Japanese and

American machines are shown in Figure 9 and Figure 10. In both figures material

prices have been multiplied by a factor of 10 in order to make it visible on the figure

and to make the comparison easier. Hypothetical dashed lines have been used to fill

in the gap where no data were available.

As for material prices, Figure 3 and Figure 4 show that the total value of

materials in both the American and Japanese appliances shows a declining tendency.

This can most likely be explained by the role played by plastics. The American

appliances contain on average about 20% plastics, and the Japanese appliances are up

to 56% made of plastics. The main ingredients of plastics are oil and natural gas, and

consequently their prices are largely influenced by the price movements of oil and

gas. The oil and gas prices were generally on a decreasing trend during the period in

the 80s and 90s, which thus reduced the cost of plastics production. The prices of the

other materials have remained relatively unchanged during this period.

8 The other two appliances were room air conditioners and central air conditioners.

25

Normally, a constant size and material composition coupled with decreasing

market prices would suggest an increasing trend in the relative value of materials –

the percentage that the total value of the raw materials occupy in the overall value, i.e.

the market price, of the appliance. However, in this case, because the total material

prices also decreased along with the market prices, the result seen was a decrease in

the relative value of materials, as shown in Figure 5 and Figure 7.

Figure 3. Material Value [USD] of US Freezer-Refrigerators

Figure 4. Material Value [USD] of Japanese Freezer-Refrigerators

26

When visualized in the context, however, it becomes clear that the changes in

the price of raw materials are quite insignificant. Figure 6 and Figure 8 display the

relative value of materials on a 100% scale. For both the US and Japanese appliances,

the percentage value of raw materials, which fluctuates between about 3% and 6%

(as indicated in Figure 5 and Figure 7), is a mere fraction of the final market value

placed on the appliances.

Figure 5. Material Value of US Freezer-

Refrigerator as a % of Market Price

Figure 6. Material Value of US Freezer-

Refrigerators on a 100% Scale

Figure 7. Material Value of Japanese

Freezer-Refrigerator as a % of Market Price

Figure 8. Material Value of Japanese

Freezer-Refrigerator on a 100% Scale

27

2. Washing Machines

Weight and Material Composition

Washing machine data were collected for the machines manufactured

between 1978 and 2004. Figure 11 shows the weight and the material composition of

washing machines, and the trends shown widely agrees with the observations made

in the study by Bole (2006). In his life-cycle study on washing machines, Bole found

that material composition data for washing machines over time strongly indicates

Figure 10. Development in Market Price, Material Price [USD], and Weight

[kg] of Japanese Freezer-Refrigerators over time

Figure 9. Development in Market Price, Material Price [USD], and Weight [kg]

of US Freezer-Refrigerators over time

[kg]

[kg]

28

that lighter materials, such as aluminum and polymers, are increasingly being

favored over heavier materials, mainly ferrous metals. While an average washing

machine manufactured in the late 1980s weighed about 84kg and contained over

80% steel and cast iron and 6% plastics, average washing machines from the 1990s

and early 2000s contain about 50% ferrous materials and more than twice the amount

of plastics on average. These shifts in material use can also be confirmed in the

material composition changes shown in Figure 11. The use of the other main

materials, i.e. aluminum, copper, and glass/ceramics, remained relatively stable.

In his study Bole (2006) also noted a growing tendency towards lighter-

weight machines. A decreasing trend in the overall weight of the machines over time

can also be seen in this study, however, only on a rather small scale. Comparing the

1978 breakdown data to those of later years, it can be assumed that the weight-factor

provided by ferrous metals in the earlier days was presumably replaced by the use of

concrete. Although the 1978 machine contained no concrete, the later machines

contain up to almost 30% concrete in weight. The average weight of the machine

during this time period remained at around 80kg.

Figure 11. Washing Machine Weight & Material Composition [kg]

[kg]

29

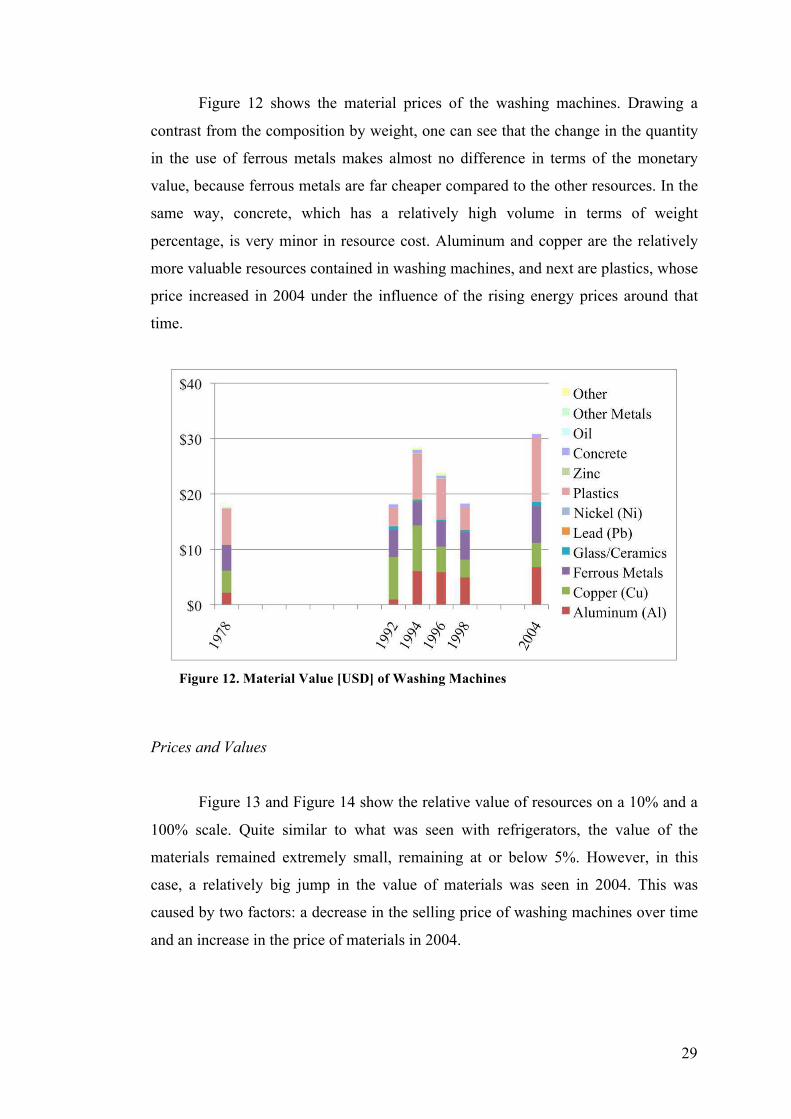

Figure 12 shows the material prices of the washing machines. Drawing a

contrast from the composition by weight, one can see that the change in the quantity

in the use of ferrous metals makes almost no difference in terms of the monetary

value, because ferrous metals are far cheaper compared to the other resources. In the

same way, concrete, which has a relatively high volume in terms of weight

percentage, is very minor in resource cost. Aluminum and copper are the relatively

more valuable resources contained in washing machines, and next are plastics, whose

price increased in 2004 under the influence of the rising energy prices around that

time.

Prices and Values

Figure 13 and Figure 14 show the relative value of resources on a 10% and a

100% scale. Quite similar to what was seen with refrigerators, the value of the

materials remained extremely small, remaining at or below 5%. However, in this

case, a relatively big jump in the value of materials was seen in 2004. This was

caused by two factors: a decrease in the selling price of washing machines over time

and an increase in the price of materials in 2004.

Figure 12. Material Value [USD] of Washing Machines

30

Figure 15 shows the development in market price, material price, and weight

of washing machines. Material prices have been multiplied by a factor of 10, and

hypothetical dashed lines have been used to fill in the gap where no data were

available. It is interesting to see that the market price of the machines continuously

decreased through time and was at the relative lowest in 2004, despite the total cost

of resources being highest that year. A couple possible explanations may exist for

this event. First, in the pursuit of manufacturing lighter machines, the cheaper

materials (i.e. ferrous metals, concrete) are being replaced by materials that are

relative more costly and/or have unstable prices, namely plastics and also aluminums.

Secondly, as discussed earlier in the freezer-refrigerator section, Dale et al. (2009)

has shown that major appliances are decreasing in market prices while increasing in

efficiency. Again, technological advancement and the resulting reduction in

production costs can be considered to be responsible for this trend. Ultimately,

however, even taking into consideration the increase in 2004, Figure 13 and Figure

14 show that the relative overall value of the resources still remains very low.

Figure 14. Material Value of Washing

Machines on a 100% Scale

Figure 13. Material Value of Washing Machines

as a % of Market Price

31

Another point that should be noted in terms of metals used and the material

values contained within for washing machines, as well as possibly for refrigerators,

is the fact that these machines do not require a high processing power and therefore

even today contain only a relatively small amount of complicated electronics. Unlike

computers and mobile phones, which contain high-tech and high-value circuit boards,

washing machines and refrigerators are mostly composed of low-cost laminates

containing fewer valuable materials (Hester and Harrison, 2009). This means that

presumably, what makes up the bulk of the actual market price of these appliances

are not the raw materials themselves but rather the technologies and the

manufacturing processes, and therefore, even relatively large changes in the prices of

resources should not lead to significant changes in the market value.

3. Televisions and Monitors

3.1. CRT Displays

Cathode Ray Tube (CRT) televisions and monitors can obviously vary

largely in sizes. In order to keep the comparison simple, for this study CRT data

collection was controlled to a more or less limited range, between 15 and 21 inches,

with the exception of 1982, for which only data from a 9-inch display could be found.

Figure 15. Development in Market Price, Material Price [USD], and Weight [kg]

of Washing Machines over time

[kg]

32

1986 is 16 inches, 1988 is 15 inches, and all data from the 1990s are for a 21-inch

display.

Weight and Material Composition

Figure 16 shows the weight and material compositions of CRT displays. Even

though the size of the display increased from 1986 to 1998, the total weight of the

product slightly declined. This could be due to a relatively less use of heavier ferrous

metals or perhaps simply a change in the preferred style and design, such as the outer

frame and the addition/removal of leg stands. Even among the CRT monitors and

televisions sold today, some degrees of weight variance can be observed within the

same sized displays, depending on the design.9 As for the material composition, there

seems to be a declining tendency in the amount of ferrous metals, which again may

account for the decline in the overall weight. The amount of tin contained also

showed a declining tendency. The relative share of plastics remained stable with

perhaps a very slight increasing tendency. One observation worth mentioning is that

although these data are from the pre-RoHS Directive days, it appears that the use of

lead was decreasing already.

10

9 The same can be said about the flat panel displays. 10 The small size of the CRT in 1982 is due to the fact that only data from a 9-inch display could be

found, while the others are between 15 and 21 inches.

Figure 16. CRT Displays Weight & Material Composition [kg]

[kg]

33

Prices and Values

Figure 17 shows the value of the materials. Several interesting observations

can be made about the material price data for CRT. First of all, one notices a

relatively large share of tin in the value, especially in 1986. This is partly due to the

CRT from 1986 containing a relatively higher amount of tin at 1.8% compared to

later years (less than 1% after 1994), but also because the price of tin was much

higher in 1986 and then continued to decline throughout the 90s. Although

glass/ceramics and plastics together account for the majority of the percentage

weight in composition, neither are very expensive materials and therefore are much

less important when considering the material value of the products. What gives the

largest price value to CRT monitors is actually a material that is only contained in an

infinitely small amount – averaging at about 0.006% and not even visible in the

material composition graphs of Figure 16: gold. Gold is a precious metal that is

consistently tremendously high in value, and even when it is contained in such a

miniscule amount, it can make up the majority of the monetary resource value of a

product. It can also be said that CRT displays do not contain any other precious

metals very high in value, with the exception of silver, but the price of silver is on

average 50-60 times less than the price of gold.

11

11 Note that for 1982 a 9-inch display has considered (while the others are between 15 and 21 inches).

Figure 17. Material Value [USD] of CRT Displays

34

The total material price shows a much stronger decreasing tendency than the

average weight, especially between 1994 and 1998. This can be attributed to the

generally decreasing trend shown by some of the price-relevant resources, namely

copper, glass/ceramics, and gold, during the latter half of the 90s.

12

As for the total resource value as a percentage of the market price, Figure 18

and Figure 19 show that there is an overall increasing trend from the 80s to the 90s,

then stabilizing, perhaps slightly decreasing, in the 90s. This can be explained by the

fact that along with the overall decrease in the value of resources during that time,

the average market price of CRT displays also went down. The stable decline in the

market price of CRT may be the result of the emerging competition from the new

technology offered in the form of flat-panel displays. Once again, however, although

slightly higher than the figures for washing machines and refrigerators, the overall

value of resource prices for CRT remained quite low, no more than 7% and

averaging at about 6%. The overall development in market price, material price, and

weight of CRT displays is shown in Figure 20.

12 Note that for 1982 a 9-inch display has considered (while the others are between 15 and 21 inches).

Figure 18. Material Value of CRT Displays

as a % of Market Price

Figure 19. Material Value of CRT Displays

on a 100% Scale

35

13

3.2. Flat Panel Displays

In order to keep the comparison consistent, data from 20-inch flat panel

displays were used for all three years 1997, 1999, and 2003. Screens larger than this

size (22 inch and above) did not appear widely on the market until around 2000 and

did not become commercially viable for most people until a few years later.

Weight and Material Composition

First of all, the biggest and the most obvious difference between a CRT

display and a flat panel display in their appearance and structure, as the name of the

latter suggests, is in its horizontal dimension. Its thinness, and consequently the

lightness in weight, is the single biggest advantage of flat panels over CRTs. This

advancement in technology means that although they ultimately serve the same

function – to transmit images – there are substantial differences between flat panel

displays (FPDs) and CRTs in terms of their material composition and therefore,

possibly, implications to the relative value of resources.

Flat panel displays were still relatively new on the market in the late 1990s

and continued to undergo major developments well into the late 2000s. This was

primarily reflected in the rapidly decreasing prices, particularly for the large sized

13 Note that for 1982 a 9-inch display has considered (while the others are between 15 and 21 inches).

Figure 20. Development in Market Price, Material Price [USD], and Weight of CRT

Displays over time

[kg]

36

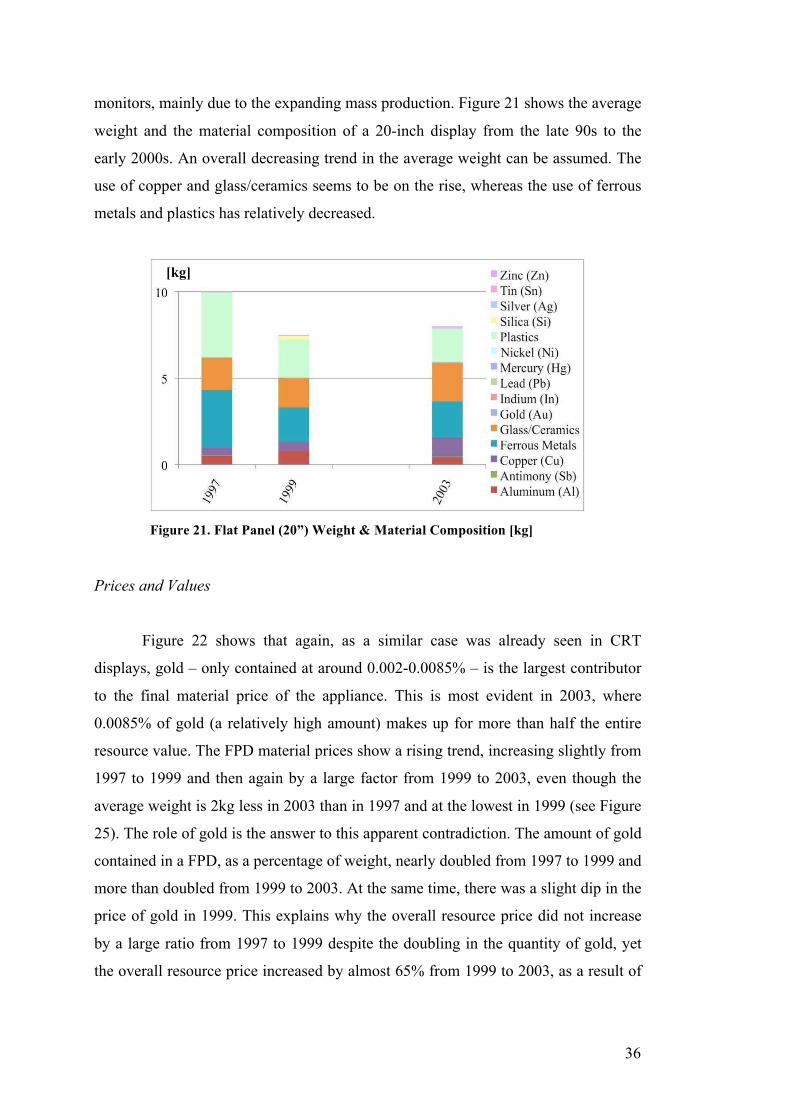

monitors, mainly due to the expanding mass production. Figure 21 shows the average

weight and the material composition of a 20-inch display from the late 90s to the

early 2000s. An overall decreasing trend in the average weight can be assumed. The

use of copper and glass/ceramics seems to be on the rise, whereas the use of ferrous

metals and plastics has relatively decreased.

Prices and Values

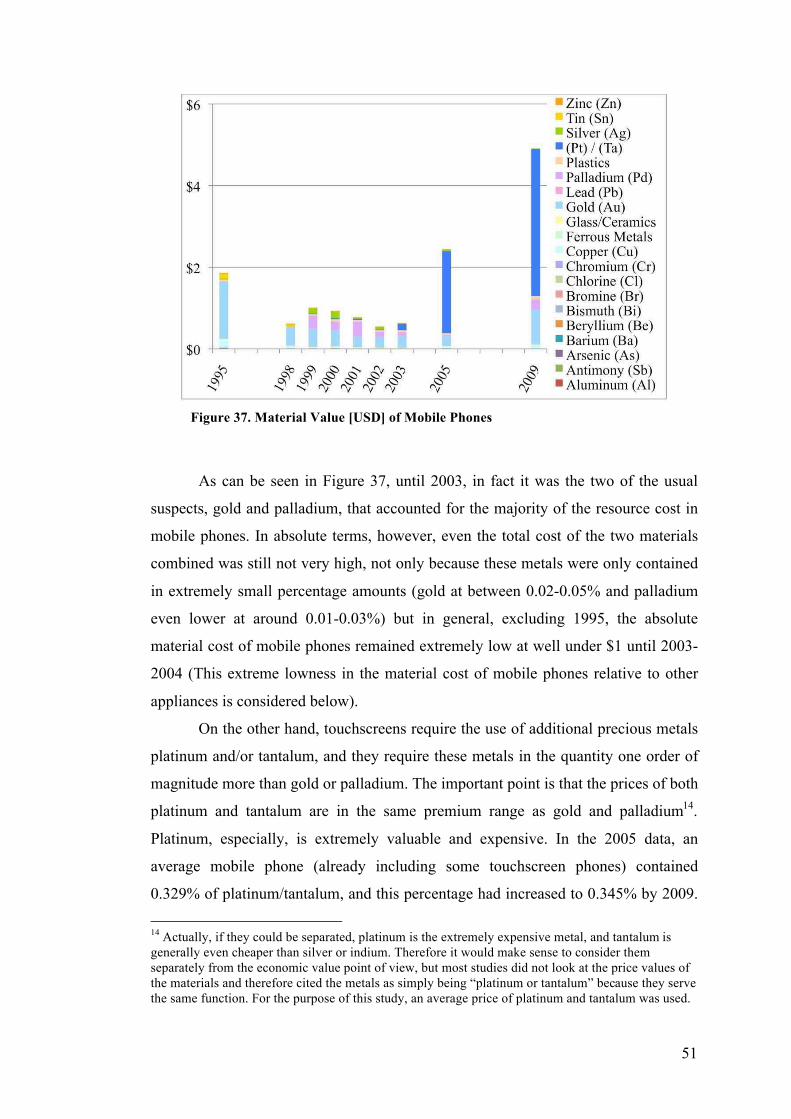

Figure 22 shows that again, as a similar case was already seen in CRT

displays, gold – only contained at around 0.002-0.0085% – is the largest contributor

to the final material price of the appliance. This is most evident in 2003, where

0.0085% of gold (a relatively high amount) makes up for more than half the entire

resource value. The FPD material prices show a rising trend, increasing slightly from

1997 to 1999 and then again by a large factor from 1999 to 2003, even though the

average weight is 2kg less in 2003 than in 1997 and at the lowest in 1999 (see Figure

25). The role of gold is the answer to this apparent contradiction. The amount of gold

contained in a FPD, as a percentage of weight, nearly doubled from 1997 to 1999 and

more than doubled from 1999 to 2003. At the same time, there was a slight dip in the

price of gold in 1999. This explains why the overall resource price did not increase

by a large ratio from 1997 to 1999 despite the doubling in the quantity of gold, yet

the overall resource price increased by almost 65% from 1999 to 2003, as a result of

Figure 21. Flat Panel (20”) Weight & Material Composition [kg]

[kg]

37

the increase in both the quantity and price of gold. This again highlights the

importance of gold as a valuable material and illustrates that due to its vastly high

cost, even a small change in the price and/or in the amount of gold used may cause a

visible shift in the material price.

The two other metals that show a similar presence in Figure 22, though on a

smaller scale, are silver and indium. Both of these are considered precious metals,

though not nearly as costly as gold. As it was already mentioned under the discussion

on CRT displays, silver is priced 50-60 times less than gold on average. The price of

indium used to be comparable to that of silver, but its value began rising in the 90s,

spiked in mid 2000s, and still remains high today. This is in direct response to the

rapidly increasing consumption of indium, most intensely in the FPD industry itself

but also in other industries e.g. the photovoltaic sector (Böni and Widmer, 2011).

The other major price constituents are plastics, copper, and aluminum. None of these

are particularly high in value, and especially plastics have a relatively low price, but

its sizable quantity makes a contribution to the overall value. One thing to perhaps

keep in mind, as will be discussed later, is that the price of plastics is not stable and

therefore uncertain how cheap it will remain depending on the movements in the oil

and gas prices.

Figure 22. Material Value [USD] of 20” Flat Panel Displays

38

Figure 23 and Figure 24 show the relative resource values on a 10% and a

100% scale. A relatively big increase in the resource value percentage in 2003 is

caused by a combination of a decrease in the market price (see Figure 25) and an

increase in the price of materials, similar to what was seen in the 2004 data of

washing machines.

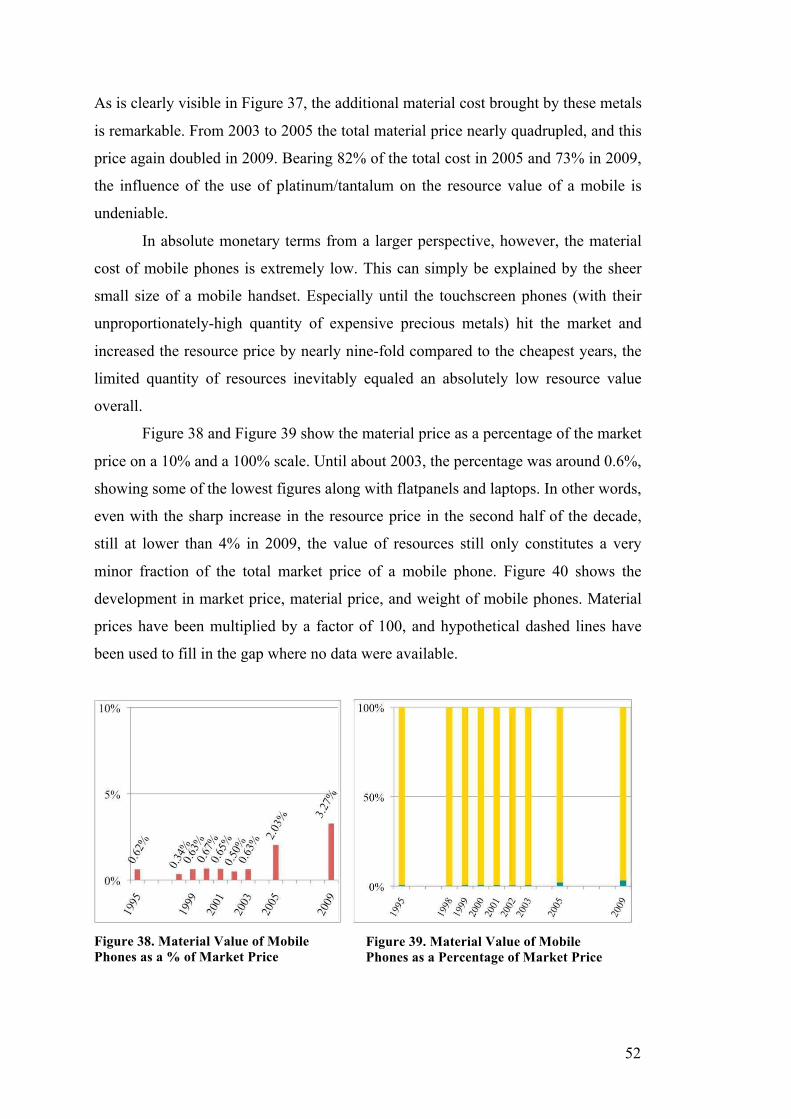

What becomes evident in Figure 23 and Figure 24, however, is the

surprisingly miniscule share of the resources in the overall value of FPDs, far lower

than what has been seen with washing machines, refrigerators, or CRTs. This may be

shocking at a first glance, given the technology, presumably more advanced than

CRT displays, involved in the manufacturing of FPDs. However, factors such as the

cost of research & development and the leading manufacturing processes are simply

not reflected in the value strictly based on materials. As far as the resources are

concerned, although there are clear changes in the material composition between

CRT and FPD, the new technology for FPD did not necessarily require the use of

large amounts of expensive materials. From the perspective of resource use, the

technological changes from CRT to FPD primarily required a reshuffling of shares in

the three major materials: ferrous metals, glass/ceramics, and plastics, all of which,

seen from a larger perspective, happen to be quite close in prices and not very costly.

One crucial difference in the composition of CRT and FPD is in the use of the

precious metal indium, but its application appears to be small enough in quantity that

it does not have a significant impact on the overall resource costs.

Figure 23. Material Value of 20” Flat Panel

Displays as a % of Market Price

Figure 24. Material Value of Flat Panel

Displays on a 100% Scale

39

However, given that the flat counterpart is significantly lighter and requires

much less resources in absolute quantity than the traditional CRT displays, this

means that the total absolute value of resources will be far lower for flat panels than

for CRTs, despite the much higher market prices. Even given the rapidly shrinking

market prices of flat panels (see Figure 25), the percentage share of resource cost in

the overall cost still remained less than 2% in 2003. Figure 25 shows the

development in market price, material price, and weight of FPDs over time. Material

prices have been multiplied by a factor of 50, and hypothetical dashed lines have

been used to fill in the gap where no data were available.

Although this study only covers up to 2003, the FPD industry has continued

to develop rapidly, and as of 2011, the prices of FPDs including the largest screens

widely available to consumers (up to 60 inches) have mostly settled down in the

lowest possible price ranges. If an analysis were to be conducted for the relative

material value for these past several years, the percentage share of resource value

will most likely have seen an increase – particularly sharp increases for larger sized

screens – accompanying their rapid decrease in market prices. Larger screens

inevitably use a larger absolute quantity of materials, which should also increase the

relative value of resources. Even then, however, from the current observable trend, it

remains highly doubtful whether the relative value of resources will ever become

significant enough to matter in the consideration of the actual market price.

Figure 25. Development in Market Price, Material Price [USD], and Weight [kg] of

Flat Panel Displays over time

[kg]

40

4. Computers

4.1. Desktops

All desktop computer data used for this study include an average 17-inch

CRT monitor.

Weight and Material Composition

Figure 26 shows that the total weight of desktop computers, including both

the actual computer part and the monitor, declined in the 1990s and seems to have

more or less stabilized in the 2000s. As discussed earlier, the weight of CRT

monitors showed a decreasing tendency in the 1990s, thus the change in the weight

of the monitor part may account for the decrease in the overall weight of desktops. It

is also possible that the computer part itself went through changes in weight and

material composition; however, not enough data could be obtained for the detailed

material composition of the computer part alone.