EEI 2013 FINANCIAL REVIEW 33

Business StrategiesRegulated Electric revenue increased 4.7%, despite a minimal 0.1% in-crease in nationwide electric output. Competitive Energy revenue had a modest 1.5% increase, while its asset total was virtually unchanged.

2013 Revenue by SegmentRegulated Electric revenue in-

creased by $10.9 billion, or 4.7%, to $245.4 billion from $234.5 billion in 2012. The segment’s share of to-tal industry revenue grew to 66.2% from 66.0% in 2012, totals that are now well above the 52.1% level of 2005.

Business Segmentation—RevenuesU.S. INVESTOR-OWNED ELECTRIC UTILITIES

($ Millions) 2013 2012r Difference

Regulated Electric Competitive EnergyNatural Gas Distribution Natural Gas PipelineNatural Gas and Oil Exploration & ProductionOther

Eliminations/Reconciling Items

Total Revenues

% Change

Note: Difference and Percent Change columns may reflect rounding. Totals may reflect rounding.

Source: Based on segment reporting from SEC filings of 57 U.S. Investor-Owned Electric Utilities

245,441 234,504 10,938 4.7% 68,171 67,187 984 1.5% 36,269 32,328 3,942 12.2% 6,175 6,658 (483) (7.3%) 941 1,750 (809) (46.2%) 13,641 12,773 869 6.8% (14,151) (15,303) 1,152 (7.5%) 356,488 339,896 16,592 4.9%

r = revised

Business Segmentation

The industry’s regulated business segments, Regulated Electric and Natural Gas Distribution, showed the largest revenue gains in both dol-lar and percentage terms in 2013, and were the only categories with as-set growth. Continuing a multi-year trend, the industry’s regulated asset base grew and accounted for a larger share of total industry assets. Regu-lated Electric assets grew to a 66.4% share of total assets, providing most of the industry’s asset growth.

Natural Gas Distribution revenue had significant gains for the second straight year, rising by $3.9 billion, or 12.2%, from $32.3 billion in 2012 to $36.3 billion in 2013. This followed a 15.6% increase the year before. Annual revenue here has his-torically fluctuated due to significant swings in natural gas prices.

Total regulated revenue—the sum of the Regulated Electric and Natu-ral Gas Distribution segments— increased by $14.9 billion, or 5.6%, to $281.7 billion in 2013. The year-to-year change for this metric has

BUSINESS STRATEGIES

34 EEI 2013 FINANCIAL REVIEW

growth in recent years and the fact that several companies sold off non-core businesses during the period.

Regulated ElectricRegulated Electric segment op-

erations include the generation, transmission and distribution of regulated electricity for residential, commercial and industrial custom-ers. Regulated Electric revenue gains were widespread across the industry, summing to the overall $10.9 bil-lion, or 4.7%, increase. Forty-six of 54 companies (85%) had higher revenues for this segment, with five companies (9%) reporting double-digit percentage growth. The seg-ment’s overall increase was support-ed by a continued record-high level of capital expenditures and a gener-ally constructive regulatory environ-ment at the state level. An offsetting factor was the 9% decline in cooling- degree days, although they were 11%

Source: EEI Finance Department and company annual reports

Revenue Breakdown 2013U.S. INVESTOR-OWNED ELECTRIC UTILITIES

RegulatedElectric66.2%

Natural Gas Distribution

9.8%Natural Gas

Pipeline 1.7%

18.4%

Competitive Energy

Natural Gas and Oil Exploration & Production

0.3%

Other 3.7%

Revenue Breakdown 2012U.S. INVESTOR-OWNED ELECTRIC UTILITIES

RegulatedElectric66.0%

Natural Gas Distribution

9.1%Natural Gas

Pipeline 1.9%

18.9%

Competitive Energy

Natural Gas and Oil Exploration & Production

0.5%

Other 3.6%

2013 Assets by SegmentRegulated Electric assets increased

from 65.5% of total industry assets at December 31, 2012 to 66.4% at December 31, 2013, rising by $23.5 billion, or 2.7%, over the year-end 2012 level. Competitive Energy as-sets were nearly unchanged, with a $39 million decrease from the prior year. Natural Gas Distribution assets grew by $6.5 billion, or 6.4%, while the two smaller natural-gas-related categories, Pipeline and Exploration & Production, experienced declines of 0.4% and 27.6%, respectively.

Total regulated assets (Regulated Electric plus Natural Gas Distribu-tion) accounted for 74.3% of total industry assets at year-end 2013, up from 73.1% on December 31, 2012. This aggregate measure has grown steadily from 61.6% at year-end 2002, underscoring the indus-try’s significant regulated rate base

varied in recent years, falling by $13.0 billion in 2012 (-4.7%) and $2.1 billion (-0.8%) in 2011, ris-ing $4.1 billion (+1.5%) in 2010, declining $20.6 billion (-6.9%) in 2009 and increasing $22.5 billion (+7.7%) in 2008 and $14.4 billion (+5.2%) in 2007. Despite the year-to-year dollar fluctuations, regulated operations have steadily grown as a percentage of total industry revenue in recent years. Total regulated reve-nue accounted for 76.0% of total in-dustry revenue in 2013, extending a steady upward trend from 65.3% in 2005. The Business Segmentation— Revenues table presents the industry’s revenue breakdown by business seg-ment. Eliminations and reconciling items were added back to total rev-enue to arrive at the denominator for the segment percentage calcula-tions shown in the graphs Revenue Breakdown 2013 and 2012.

Business Segmentation—AssetsU.S. INVESTOR-OWNED ELECTRIC UTILITIES

r = revised

Note: Difference and Percent Change columns may reflect rounding. Totals may reflect rounding.

Source: Based on segment reporting from SEC filings of 55 U.S. Investor-Owned Electric Utilities

($ Millions) 12/31/13 12/31/12r Difference % Change

Regulated Electric 902,569 879,092 23,476 2.7%

Competitive Energy 202,921 202,960 (39) 0.0%

Natural Gas Distribution 107,964 101,455 6,510 6.4%

Natural Gas Pipeline 36,269 36,420 (151) (0.4%)

Natural Gas and Oil Exploration

& Production 2,653 3,666 (1,013) (27.6%)

Other 105,907 118,153 (12,246) (10.4%)

Eliminations/Reconciling Items (66,058) (78,482) 12,423 (15.8%)

Total Assets 1,292,225 1,263,265 28,960 2.3%

BUSINESS STRATEGIES

EEI 2013 FINANCIAL REVIEW 35

growth in recent years and the fact that several companies sold off non-core businesses during the period.

Regulated ElectricRegulated Electric segment op-

erations include the generation, transmission and distribution of regulated electricity for residential, commercial and industrial custom-ers. Regulated Electric revenue gains were widespread across the industry, summing to the overall $10.9 bil-lion, or 4.7%, increase. Forty-six of 54 companies (85%) had higher revenues for this segment, with five companies (9%) reporting double-digit percentage growth. The seg-ment’s overall increase was support-ed by a continued record-high level of capital expenditures and a gener-ally constructive regulatory environ-ment at the state level. An offsetting factor was the 9% decline in cooling- degree days, although they were 11%

Source: EEI Finance Department and company annual reports

Revenue Breakdown 2013U.S. INVESTOR-OWNED ELECTRIC UTILITIES

RegulatedElectric66.2%

Natural Gas Distribution

9.8%Natural Gas

Pipeline 1.7%

18.4%

Competitive Energy

Natural Gas and Oil Exploration & Production

0.3%

Other 3.7%

Revenue Breakdown 2012U.S. INVESTOR-OWNED ELECTRIC UTILITIES

RegulatedElectric66.0%

Natural Gas Distribution

9.1%Natural Gas

Pipeline 1.9%

18.9%

Competitive Energy

Natural Gas and Oil Exploration & Production

0.5%

Other 3.6%

prices and a slow economic recov-ery, as well as plant divestitures and merchant operations sales. The seg-ment’s 2012 revenue was the low-est annual total for this category to date, based on data covering the last decade. The highest annual revenue over the last decade was $113.2 bil-lion in 2008. Competitive Energy covers the generation and/or sale of electricity in competitive markets, including both wholesale and retail transactions. Wholesale buyers are typically electric utilities seeking to supplement generation capacity, along with regional power pools and large industrial customers. Competi-tive Energy also includes the trading and marketing of natural gas. Of the 29 companies that have Competitive Energy operations, approximately half (14 companies, or 48%) grew these assets during 2013, while 59% had revenue gains.

higher than normal. The industry is less impacted by heating degree days, which rose by 19%.

The 2013 revenue increase fol-lows declines in the preceding two years, at 2.8% in 2012 and 0.6% in 2011. These were caused by a slug-gish U.S. economy and the impact of continued low natural gas prices on the fuel component of rates. In 2010, favorable weather drove a 2.4% revenue increase. U.S. electric output decreased by 1.8% in 2012 and 0.6% in 2011 after growing by 3.7% in 2010, and falling 3.7% in 2009 and 0.9% in 2008. Year-to-year output declines have historically been rare events for an industry that typically experiences low-single-digit percent annual demand growth. Energy efficiency and demand-side management programs continue to be factors behind the flat growth.

During 2013, 60% of companies increased regulated assets as a percent of total assets (or maintained a 100% regulated structure). OGE Energy had the largest increase, raising its regulated percentage from 72.8% at year-end 2012 to 84.2% at year-end 2013. The rise reflects a lower asset total for its natural gas pipeline seg-ment. The company reduced its pri-mary business segments from three to two over the last year, the result of its newly formed master limited partnership with CenterPoint Energy and ArcLight Capital Partners.

Competitive EnergyCompetitive Energy segment rev-

enue increased by 1.5% in 2013, gaining $984 million to $68.2 bil-lion from $67.2 billion in 2012. This follows a sharp decline of $22.4 billion, or 26.0%, in 2012 that was due to continued weak electricity

BUSINESS STRATEGIES

36 EEI 2013 FINANCIAL REVIEW

The Natural Gas Pipeline and Natural Gas E&P segments had de-clines in both revenues and assets in 2013. Natural Gas Pipeline assets fell by $151 million, or 0.4%, while its revenues were $483 million, or 7.3%, lower. Natural Gas E&P assets decreased by $1.0 billion, or 27.6%, along with a $809 million, or 46.2%, decline in revenues.

Over the longer term, the Pipeline and E&P segments have accounted for a declining share of total indus-try assets. This is due to a combina-tion of growth in the other business segments and divestitures within these two. Natural Gas Pipeline and Natural Gas E&P fell from 3.7% and 2.1% shares of total assets on December 31, 2003 to 2.7% and 0.2% on December 31, 2013, with their combined total assets down by $11.8 billion, or 23%, over this ten-year time frame.

In comparison, 94%, 62%, 75% and 91% of companies had year-to-year revenue declines in 2012, 2011, 2010 and 2009 respectively, while 89% experienced gains in 2008.

Natural Gas Distribution includes the delivery of natural gas to homes, businesses and industrial customers throughout the United States, while the Natural Gas Pipeline business concentrates on the transmission and storage of natural gas for local distribution companies, marketers and traders, electric power generators and natural gas producers. Added together, Natural Gas Distribution, Natural Gas Pipeline and Explora-tion & Production (E&P) activities produced $43.4 billion of the indus-try’s revenue in 2013, up from $40.7 billion in 2012. In percentage terms, the revenue contribution from natu-ral gas activities increased to 11.8% in 2013 from 11.5% in 2012.

Natural Gas DistributionNatural Gas Distribution revenue

increased by $3.9 billion, or 12.2%, in 2013, reversing a declining trend in each of the previous four years. The higher revenues correlate with a 19% increase in heating degree days in 2013. On the other hand, natu-ral gas prices continued to be de-pressed, spending much of the year under $4/mmBTU. The 2013 rise in revenue follows declines of $6.2 billion, or 15.6% in 2012, $701 mil-lion, or 1.7%, in 2011, $1.5 billion, or 3.6%, in 2010 and a much larger decline of $9.8 billion, or 19.1%, in 2009 due to sharply falling gas prices and the impact of the eco-nomic downturn. Natural gas pric-es peaked above $12/mmBTU in 2008, a year marked by very high price volatility. Overall, 28 of the 32 companies (88%) that report gas distribution revenue showed year-to-year revenue increases in 2013.

Source: EEI Finance Department and company annual reports

Asset BreakdownAs of December 31, 2013

U.S. INVESTOR-OWNED ELECTRIC UTILITIES

RegulatedElectric66.4%

Natural Gas Distribution

7.9%

Natural Gas Pipeline 2.7%

14.9%

Competitive Energy

Natural Gas and Oil Exploration & Production

0.2%

Other 7.8%

Asset BreakdownAs of December 31, 2012

U.S. INVESTOR-OWNED ELECTRIC UTILITIES

RegulatedElectric65.5%

Natural Gas Distribution

7.6%

Natural Gas Pipeline 2.7%

15.1%

Competitive Energy

Natural Gas and Oil Exploration & Production

0.3%

Other 8.8%

BUSINESS STRATEGIES

EEI 2013 FINANCIAL REVIEW 37

2013 Year-End List of Companies by Category

Early in each calendar year we update our list of investor-owned electric utility holding companies by business category based on the previ-ous year-end’s business segmentation data presented in 10Ks and supple-mented by discussions with parent companies. Our categories are as follows: Regulated (80% of holding company assets are regulated); Mostly Regulated (50%-79% of holding company assets are regulated); Diversified (less than 50% of hold-ing company assets are regulated).

We use assets rather than revenue for determining categories because we think assets provide a clearer picture of strategic trends. Fluctu-ating natural gas and power prices can impact revenue so greatly that some companies’ strategic approach to business segmentation is distorted by reliance on revenue data alone.

List of Companies by Category at December 31, 2013

AlleteAlliant EnergyAmeren American Electric PowerAvista Black HillsCleco CMS EnergyConsolidated EdisonDPL DTE EnergyDuke EnergyEdison International

El Paso ElectricEmpire District ElectricEntergyGreat Plains EnergyIberdrola USAIDACORP Integrys Energy Group IPALCO EnterprisesNortheast UtilitiesNorthWestern EnergyOGE EnergyOtter Tail PowerPepco Holdings

PG&EPinnacle West CapitalPNM ResourcesPortland General Electric Puget EnergySouthernTECO EnergyUIL HoldingsUnitil UNS EnergyWestar EnergyWisconsin EnergyXcel Energy

Regulated (39)

CenterPoint EnergyDominion ResourcesExelonFirstEnergyMGE Energy

MidAmerican Energy Holdings NextEra EnergyNiSourcePPL

Public Service Enterprise GroupSCANASempra EnergyVectren

Mostly Regulated (13)

Energy Future Holdings Hawaiian Electric MDU ResourcesDiversified (3)

Comparing the list of companies from year to year reveals company migrations between categories and indicates the general trend in indus-try business models. We also base our quarterly category financial data during the year on this list.

The overall trend toward a more regulated industry continued in 2013. The Regulated group totaled 39 companies at year-end, represent-ing 71% of the industry’s compa-nies, up from 67% last year. OGE Energy, Otter Tail Power and Pepco Holdings migrated from the Mostly Regulated to the Regulated category. OGE’s regulated asset percentage grew from 72.8% at year-end 2012 to 84.2% at year-end 2013, reflect-ing a lower asset total for its natural gas pipeline segment. The company reduced its primary business seg-ments from three to two over the last year, the result of its newly formed master limited partnership with

CenterPoint Energy and ArcLight Capital Partners. Otter Tail’s increase from 76.5% to 80.9% relates to a decline in its Corporate asset divi-sion, which is categorized as Other for our purposes. Pepco reshuffled its segments over the prior year, re-moving its Other Non-Regulated Category. This was driven by the company’s termination of its inter-ests in its cross-border energy lease investments during 2013.

The Diversified category added Hawaiian Electric from the Mostly Regulated Category, as the compa-ny continues to straddle to 50.0% threshold of regulated assets. Hawai-ian’s regulated percentage fell from 50.3% to 49.2% over the last year, after making an opposite jump in categories the previous year.

The total number of companies in the EEI universe fell from 58 at year-end 2012 to 55 at year-end 2013, the result of merger activity. The buyouts of CH Energy (acquired by Fortis Inc. in 2013), NV Energy (acquired by MidAmerican Energy in 2013) and Central Vermont Power (acquired by Gaz Metro LP in 2012) caused the decrease. At the close of 2013, there were 39 Regulated, 13 Mostly Regulated and 3 Diversified companies (see List of Companies by Category at December 31, 2013).

BUSINESS STRATEGIES

38 EEI 2013 FINANCIAL REVIEW

Ameren Divests Merchant Generation to Dynegy

The year’s first major transaction, announced on March 14, took the form of Ameren’s move to exit the competitive generation business by selling its coal-fired merchant gen-eration fleet, comprised of five plants in Illinois, and a related energy mar-keting business to independent pow-er producer Dynegy. Ameren said the sale was motivated by its desire to focus the company exclusively on rate-regulated electric, natural gas and transmission operations, clarify-ing both its strategic direction and source of value to shareholders. The company said it expects the transac-tion will reduce business risk, im-prove the predictability of future earnings and cash flows, strengthen its credit profile and support its divi-dend. The divestiture was valued at approximately $900 million, includ-ing removal of $825 million of debt from Ameren’s consolidated balance sheet and an estimated $180 mil-lion of tax benefits expected to be substantially realized in 2015, par-tially offset by about $75 million in transaction-related costs and pen-sion liabilities retained by Ameren. Ameren received no cash proceeds as a result of the transaction. Ame-ren also announced plans for $8.1 billion in infrastructure investment from 2013 to 2017, largely in de-livery and transmission in Illinois and Missouri.

Seeking to boost its exposure to a power and capacity market recovery in the Midwest, Dynegy said the ac-quisition would build scale in a key market with assets similar to its cur-rent Illinois-based coal fleet while cre-ating operating synergies estimated

single state utilities with good organ-ic growth potential as profitable ad-ditions to larger holding companies.

There were four whole company deals announced during the year: i) Ameren’s divestiture of merchant coal assets to Dynegy in a “back-to-basics” move; ii) MidAmerican’s acquisition of Nevada’s NV Energy; iii) a pure merchant power play in NRG’s bid for Edison Mission En-ergy; and iv) Canadian utility Fortis’ proposed purchase of Arizona’s UNS Energy. In each of the two deals tar-geting a regulated utility, the buyer wanted the utility just as it was, for its solid earnings and growth poten-tial, and with no plans for financial engineering, re-strategizing or cost cutting to wring out value. The year also produced a failed deal. In De-cember, Entergy and ITC Holdings abandoned plans to divest Entergy’s transmission assets to ITC after a two-year struggle marked by resis-tance from FERC, state regulators and other stakeholders.

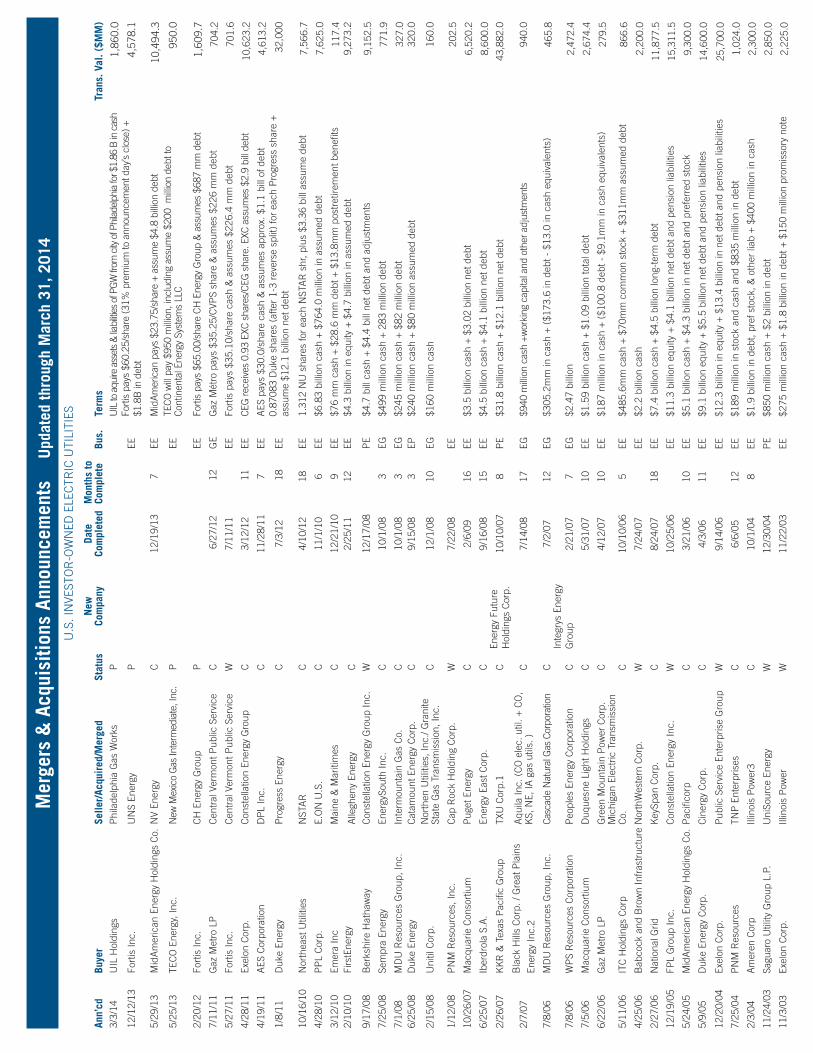

Mergers and Acquisitions

There were no proposed combina-tions of multi-state diversified utili-ties announced in 2013, an area of M&A that was quiet for the second year in a row as many of the head-winds from 2012 persisted, including weak power demand, uncertain U.S. economic growth, challenging state regulatory navigation and low natu-ral gas prices with associated weak stock prices of utility holding com-panies with merchant generation. The most recent large deals were First Energy’s successful bid for Allegh-eny (closed in February 2011), the Exelon/Constellation merger (closed in March 2012), the “merger of equals” involving New England utili-ties NSTAR and Northeast Utilities (completed in April 2012) and the Duke/Progress merger (completed in July 2012). However, utility M&A was alive and relatively well in 2013, emphasizing movement of merchant assets and the appeal of high-quality

0

5

10

15

20

25

30

Source: EEI Finance Department

Status of Mergers & Acquisitions 1995–2013

U.S. INVESTOR-OWNED ELECTRIC UTILITIES

2010 2011 2012 20131995 1996 1997 1998 1999 2000 2001

Completed (98 total)

Announced (122 total)

Withdrawn (27 total)

(Number of Mergers & Acquisitions)

20062002 2003 2004 2005 2007 2008 2009

BUSINESS STRATEGIES

EEI 2013 FINANCIAL REVIEW 39

in Nevada. MidAmerican agreed to purchase all outstanding shares of NV Energy’s common stock for $23.75 per share in cash, for an enter-prise value of approximately $10 bil-lion. NV Energy shares jumped 23% on the announcement from their May 29 closing price of $19.28. In the weeks preceding the announce-ment, the shares had fallen, along with many interest rate sensitive dividend-paying stocks, about 11% off their late-April high of $21.63, evidently placing their value at an at-tractive level for MidAmerican.

MidAmerican cited NV Energy’s solid commitment to the state of Nevada and its performance as a high-quality energy business as mo-tivations for the deal, along with its similar corporate values, out-standing assets and superb manage-ment team. Analysts noted that NV Energy generates positive free cash flow, which supports a growing divi-dend, is benefitting from an improved regulatory environment in the state, and sits geographically alongside MidAmerican’s presence in nearby Utah, Idaho, Oregon and northern California. Analysts also cited NV Energy’s commitment to renewable energy and its growing solar genera-tion as an attraction, with Nevada’s renewable portfolio standard as one of the most aggressive in the nation, requiring that at least 25 percent of the company’s retail energy sales be derived from renewable energy resources by 2025.

NV Energy cited as deal drivers MidAmerican’s stability, expertise in renewable generation and ability to provide low-cost capital for NV Energy’s renewable energy growth

at $60 million annually by 2015. It will also benefit from acquiring an established retail business (Ameren Energy Marketing) with significant scale that supports its merchant goal and gas plants. Dynegy noted that its existing coal generation fleet and the acquired plants are compliant with the EPA’s Mercury and Air Toxic Standards, which should leave the combined portfolio well positioned to benefit from tightening supply as noncompliant or uneconomic gener-ation retires. Dynegy also noted the financial terms ensured that little if any capital support would be needed for the acquired plants, thereby pre-serving capital allocation flexibility. The company said targeted syner-gies along with forward natural gas prices and its view on forward power and capacity prices should make

the acquisition accretive to adjusted EBITDA in 2014 and to free cash flow by 2015.

The transaction was completed on December 2, 2013. In addition, in October 2013 Ameren entered into an agreement to sell three merchant gas-fired plants, which were not part of the Dynegy transaction, to pri-vate equity buyer Rockland Capi-tal. With that sale, which closed in early February 2014, Ameren com-pleted its exit from the merchant generation business.

MidAmerican Acquires NV EnergyOn May 30, Berkshire Hathaway

subsidiary MidAmerican Energy Holdings announced it had reached an agreement to acquire NV Energy, which serves approximately 1.3 mil-lion electric and natural gas customers

Status of Announced Mergers & Acquisitions1995–2013

U.S. INVESTOR-OWNED ELECTRIC UTILITIES

Year

1995199619971998199920002001200220032004200520062007200820092010201120122013

Totals

21

139

10236511136612242

98

Completed

813111026952233746–4513

122

Announced

333–214311–212––1––

27

Withdrawn

Source: EEI Finance Department

BUSINESS STRATEGIES

40 EEI 2013 FINANCIAL REVIEW

to provide NRG with a lower cost of capital for acquisition of generation assets, benefitting from investors’ hunt for yield in a very low interest rate environment. The subsidiary owns generation assets with long-term contracts and passes through cash flow to investors in the form of steady dividends. The structure’s dividend can grow as assets are added to the NRG Yield portfolio. By year-end 2013, the NRG Yield shares had appreciated 80% from their July IPO price of $22 per share. The EME portfolio contains 2,600 net MW of fully-contracted generation; 1,600 MW are under long-term contracts with credit-worthy counterparties, with a weighted average remaining contract life of 14 years. NRG noted that the contracted portfolio is com-posed of 1,100 net MW of wind ca-pacity and a 500 MW gas-fired fa-cility which came online during the summer of 2013.

NRG also said the acquisition would enhance its core generation platform, balancing the geographic distribution and dispatch-level di-versity of its conventional generation fleet by adding 1,200 MW of con-tracted gas assets in California and 4,300 MW of coal-fired capacity in PJM West.

The companies hoped to close the transaction in early 2014, following approval by the Federal Energy Reg-ulatory Commission (FERC), the U.S. Department of Justice and the Federal Trade Commission under the Hart-Scott-Rodino Act, and the Public Utility Commission of Texas. EME will also submit notice of the acquisition to the California Public Utilities Commission.

1,700 MW of wind capacity, 1,600 MW of natural gas-fired ca-pacity, 4,300 MW of coal-fired capacity and 400 MW of oil and waste coal generation. NRG cited three primary reasons for the deal: i) it increases NRG’s generation port-folio by nearly 8,000 MW, providing fuel diversity, geographic diversity and opportunities for economies of scale; ii) it significantly expands the pipeline of assets available to drive growth at NRG Yield Co. (NYSE: NYLD), with 1,600 MW of long-term, fully-contracted wind and natural gas assets; and iii) it builds off the platform and best practices developed in association with NRG’s acquisition in 2012 of GenOn En-ergy, which created the largest com-petitive power provider in the U.S.

As an indication of the broad secular trends reshaping the electric generation business, the companies and Wall Street analysts stressed the renewable generation component of the combination. The deal would make NRG the nation’s third-largest domestic renewable energy gen-erator, with over 2,900 net MW of wind and solar capacity in operation or under construction, while broad-ening the scale and geographic diver-sity of NRG’s renewable generation portfolio with the addition of 1,700 net MW of wind capacity, including 1,150 net MW outside the compa-ny’s concentration in the Texas and southwest U.S. region.

Another key benefit cited by the company and analysts is the sup-port the acquisition can provide to NRG Yield, a majority-owned sub-sidiary which NRG partially spun off through a July 2013 initial pub-lic offering. NRG Yield was set up

strategy. NV Energy will remain a Nevada company, operate as a sepa-rate corporate subsidiary of MidAm-erican under its current name and will continue to be headquartered in Las Vegas. The merger closed on December 19, 2013, sooner than the companies’ initial early 2014 estimate, after receiving state and federal regulatory approvals or clearances from the Public Utilities Commission of Nevada (PUCN), the Federal Energy Regulatory Commission (FERC), and the U.S. Department of Justice. The compa-nies said Nevada approval came fol-lowing a multi-party agreement in the state and a one-time bill credit to customers of NV Energy totaling $20 million.

NRG Bids for Edison Mission Energy

The year’s second merchant deal occurred on October 18 when in-dependent power producers NRG Energy and Edison Mission Energy (EME) agreed that NRG would ac-quire EME for $2.6 billion (or $1.6 billion net of approximately $1 bil-lion retained cash within EME) for 12.7 million shares of NRG com-mon stock, valued at approximately $350 million, and with the balance to be paid in cash. The terms im-ply a transaction enterprise value of approximately $2.8 billion after including $1.3 billion of adjusted non-recourse debt assumed in con-nection with the purchase. Santa Anna, California-based EME, a for-mer merchant power subsidiary of Edison International, filed Chapter 11 bankruptcy in December 2012.

EME’s generation portfolio con-sists of nearly 8,000 net MW locat-ed throughout the U.S., including

BUSINESS STRATEGIES

EEI 2013 FINANCIAL REVIEW 41

UNS acquisition is expected to be accretive to earnings in the first full year after closing, excluding one-time transaction costs. Fortis cited several specific reasons for its interest in UNS, including a 10-year com-pound annual growth rate in net in-come of 7.7% and in assets of 3.1%; increased geographic and regulatory diversification; a supportive regula-tory environment in Arizona, with rate design that allows pass-through of costs related to fuel, purchased power, environmental compliance, renewable resources, energy effi-ciency and distributed generation; and a favorable local economy that can support growth. UNS previous-ly projected that capital investment will total approximately US$2.3 bil-lion over the period 2013 through 2018, creating rate base growth at approximately 7% annually through 2018. Fortis said UNS Energy will remain a standalone utility in the Fortis model; its headquarters and management team will remain in Tucson, Arizona and UNS custom-ers will not pay for costs related to the transaction.

UNS said Fortis’ financial strength will improve access to capital to fund the ongoing diversification of UNS’ generating fleet, including growth in solar generation, as well as other infrastructure investments. Upon closing, Fortis plans to invest $200 million in UNS Energy to strength-en its balance sheet and help fund the planned purchase of a natural gas-fired plant, a transaction that will reduce UNS subsidiary Tuscon Electric Power’s reliance on coal-fired generation.

Fortis cited as motivation for the deal UNS’ strong management team with proven regulatory exper-tise and high-quality regulated util-ity assets located in a region of the U.S. experiencing above-average economic growth, saying the acqui-sition is consistent with its strategy of investing in high-quality regu-lated Canadian and U.S. utilities. Fortis acquired New York’s Hudson Valley utility CH Energy in a deal announced in 2012, closing a year later in June 2013. Fortis’ 2011 bid for Central Vermont Public Service (CVPS) was terminated when CVPS accepted what it deemed a more at-tractive offer from another Canadian utility (Gaz Metro). Fortis said the

Fortis Seeks to Acquire UNS Energy

The year’s whole-company activ-ity concluded with Canadian util-ity Fortis’ December 11 offer to ac-quire Arizona regulated utility UNS Energy for $60.25 per share in cash, resulting in an aggregate value of ap-proximately $4.3 billion, including assumption of approximately $1.8 billion of debt. UNS shares closed at $45.84 the day before the announce-ment, resulting in about a 31% pre-mium to the pre-offer price. UNS Energy has approximately $1.5 bil-lion in revenue and total assets of ap-proximately $4.3 billion and serves 654,000 electricity and gas custom-ers, primarily in Arizona.

Merger Impacts 1995–2013U.S. INVESTOR-OWNED ELECTRIC UTILITIES

Number of Companies Declined by 50% since Dec.’95

Source: EEI Finance Department

Note: Based on completed mergers in the EEI Index groupof electric utilities.

Date No. of Utilities Change

12/31/95 98 N/A12/31/96 98 – 12/31/97 91 (7.14%)12/31/98 86 (5.49%)12/31/99 83 (8.79%)12/31/00 71 (14.46%)12/31/01 69 (2.82%)12/31/02 65 (5.80%)12/31/03 65 – 12/31/04 65 – 12/31/05 65 – 12/31/06 64 (1.54%)12/31/07 61 (4.69%)12/31/08 59 (3.28%)12/31/09 58 (1.69%)12/31/10 56 (3.45%)12/31/11 55 (1.79%)12/31/12 51 (7.27%)12/31/13 49 (3.92%)

Mer

gers

& A

cqui

sitio

ns A

nnou

ncem

ents

U

pdat

ed th

roug

h M

arch

31,

201

4U

.S. I

NVE

STO

R-O

WN

ED E

LEC

TRIC

UTI

LITI

ES

Ann’

cdBu

yer

Selle

r/Ac

quir

ed/M

erge

dSt

atus

New

Co

mpa

nyDa

teCo

mpl

eted

Mon

ths

to

Com

plet

eBu

s.Te

rms

Tran

s. V

al. (

$MM

)3/

3/14

UIL

Hol

ding

sP

hila

delp

hia

Gas

Wor

ksP

UIL

to a

quire

ass

ets

& lia

biliti

es o

f PG

W fr

om c

ity o

f Phi

lade

lphi

a fo

r $1.

86 B

in c

ash

1,86

0.0

12/1

2/13

Fort

is In

c.U

NS

Ener

gyP

EEFo

rtis

pays

$60

.25/

shar

e (3

1% p

rem

ium

to a

nnou

ncem

ent d

ay’s

clo

se) +

$1

.8B

in d

ebt

4,57

8.1

5/29

/13

Mid

Am

eric

an E

nerg

y H

oldi

ngs

Co.

NV

Ener

gyC

12/1

9/13

7EE

Mid

Am

eric

an p

ays

$23.

75/s

hare

+ a

ssum

e $4

.8 b

illio

n de

bt10

,494

.3

5/25

/13

TEC

O E

nerg

y, In

c.N

ew M

exic

o G

as In

term

edia

te, I

nc.

PEE

TEC

O w

ill p

ay $

950

mill

ion,

incl

udin

g as

sum

e $2

00 m

illio

n de

bt to

C

ontin

enta

l Ene

rgy

Syst

ems

LLC

950.

0

2/20

/12

Fort

is In

c.C

H E

nerg

y G

roup

PEE

Forti

s pa

ys $

65.0

0/sh

are

CH

Ene

rgy

Gro

up &

ass

umes

$68

7 m

m d

ebt

1,60

9.7

7/11

/11

Gaz

Met

ro L

PC

entr

al V

erm

ont P

ublic

Ser

vice

C

6/2

7/12

12

GE

Gaz

Mét

ro p

ays

$35.

25/C

VPS

shar

e &

ass

umes

$22

6 m

m d

ebt

704.

2

5/27

/11

Fort

is In

c.C

entr

al V

erm

ont P

ublic

Ser

vice

W

7/11

/11

EE

Fort

is p

ays

$35.

10/s

hare

cas

h &

ass

umes

$22

6.4

mm

deb

t70

1.6

4/28

/11

Exel

on C

orp.

Con

stel

latio

n En

ergy

Gro

up

C

3/12

/12

11

EEC

EG re

ceiv

es 0

.93

EXC

sha

res/

CEG

sha

re. E

XC a

ssum

es $

2.9

bill

debt

10,6

23.2

4/19

/11

AES

Cor

pora

tion

DP

L In

c.C

11

/28/

117

EEA

ES p

ays

$30.

0/sh

are

cash

& a

ssum

es a

ppro

x. $

1.1

bill

of d

ebt

4,61

3.2

1/8/

11D

uke

Ener

gyP

rogr

ess

Ener

gyC

7/

3/12

1

8EE

0.87

083

Duk

e sh

ares

(af

ter

1-3

reve

rse

split

) fo

r ea

ch P

rogr

ess

shar

e +

as

sum

e $1

2.1

billi

on n

et d

ebt

32,0

00

10/1

6/10

Nor

thea

st U

tiliti

esN

STA

RC

4/10

/12

18EE

1.31

2 N

U s

hare

s fo

r ea

ch N

STA

R s

hr, p

lus

$3.3

6 bi

ll as

sum

e de

bt

7,56

6.7

4/28

/10

PP

L C

orp.

E.O

N U

.S.

C11

/1/1

06

EE$6

.83

billi

on c

ash

+ $

764.

0 m

illio

n in

ass

umed

deb

t7,

625.

0

3/12

/10

Emer

a In

cM

aine

& M

ariti

mes

C12

/21/

109

EE$7

6 m

m c

ash

+ $

28.6

mm

deb

t + $

13.8

mm

pos

tret

irem

ent b

enefi

ts11

7.4

2/10

/10

Firs

tEne

rgy

Alle

ghen

y En

ergy

C

2/25

/11

12EE

$4.3

bill

ion

in e

quity

+ $

4.7

billi

on in

ass

umed

deb

t9,

273.

2

9/17

/08

Ber

kshi

re H

atha

way

Con

stel

latio

n En

ergy

Gro

up In

c.

W12

/17/

08

PE

$4.7

bill

cas

h +

$4.

4 bi

ll ne

t deb

t and

adj

ustm

ents

9,15

2.5

7/25

/08

Sem

pra

Ener

gyEn

ergy

Sout

h In

c.

C10

/1/0

83

EG$4

99 m

illio

n ca

sh +

283

mill

ion

debt

771.

9

7/1/

08M

DU

Res

ourc

es G

roup

, Inc

.In

term

ount

ain

Gas

Co.

C

10/1

/08

3EG

$245

mill

ion

cash

+ $

82 m

illio

n de

bt32

7.0

6/25

/08

Duk

e En

ergy

Cat

amou

nt E

nerg

y C

orp.

C

9/15

/08

3EP

$240

mill

ion

cash

+ $

80 m

illio

n as

sum

ed d

ebt

320.

0

2/15

/08

Uni

til C

orp.

N

orth

en U

tiliti

es, I

nc./

Gra

nite

St

ate

Gas

Tra

nsm

issi

on, I

nc.

C12

/1/0

810

EG$1

60 m

illio

n ca

sh16

0.0

1/12

/08

PN

M R

esou

rces

, Inc

.C

ap R

ock

Hol

ding

Cor

p.W

7/22

/08

EE

202.

5

10/2

6/07

Mac

quar

ie C

onso

rtiu

mP

uget

Ene

rgy

C2/

6/09

16EE

$3.5

bill

ion

cash

+ $

3.02

bill

ion

net d

ebt

6,52

0.2

6/25

/07

Iber

drol

a S.

A.

Ener

gy E

ast C

orp.

C9/

16/0

815

EE$4

.5 b

illio

n ca

sh +

$4.

1 bi

llion

net

deb

t 8,

600.

0

2/26

/07

KK

R &

Tex

as P

acifi

c G

roup

TXU

Cor

p.1

CEn

ergy

Fut

ure

H

oldi

ngs

Cor

p.10

/10/

078

PE

$31.

8 bi

llion

cas

h +

$12

.1 b

illio

n ne

t deb

t43

,882

.0

2/7/

07B

lack

Hill

s C

orp.

/ G

reat

Pla

ins

Ener

gy In

c.2

Aqu

ila In

c. (

CO

ele

c. u

til. +

CO

, K

S, N

E, IA

gas

util

s. )

C7/

14/0

817

EG$9

40 m

illio

n ca

sh +

wor

king

cap

ital a

nd o

ther

adj

ustm

ents

940.

0

7/8/

06M

DU

Res

ourc

es G

roup

, Inc

.C

asca

de N

atur

al G

as C

orpo

ratio

nC

7/2/

0712

EG$3

05.2

mm

in c

ash

+ (

$173

.6 in

deb

t - $

13.0

in c

ash

equi

vale

nts)

465.

8

7/8/

06W

PS

Res

ourc

es C

orpo

ratio

nP

eopl

es E

nerg

y C

orpo

ratio

nC

Inte

grys

Ene

rgy

Gro

up2/

21/0

77

EG$2

.47

billi

on2,

472.

4

7/5/

06M

acqu

arie

Con

sort

ium

Duq

uesn

e Li

ght H

oldi

ngs

C5/

31/0

710

EE$1

.59

billi

on c

ash

+ $

1.09

bill

ion

tota

l deb

t2,

674.

4

6/22

/06

Gaz

Met

ro L

PG

reen

Mou

ntai

n P

ower

Cor

p.C

4/12

/07

10EE

$187

mill

ion

in c

ash

+ (

$100

.8 d

ebt -

$9.

1mm

in c

ash

equi

vale

nts)

279.

5

5/11

/06

ITC

Hol

ding

s C

orp

Mic

higa

n El

ectr

ic T

rans

mis

sion

C

o.C

10/1

0/06

5EE

$485

.6m

m c

ash

+ $

70m

m c

omm

on s

tock

+ $

311m

m a

ssum

ed d

ebt

866.

6

4/25

/06

Bab

cock

and

Bro

wn

Infr

astr

uctu

reN

orth

Wes

tern

Cor

p.W

7/24

/07

EE$2

.2 b

illio

n ca

sh2,

200.

0

2/27

/06

Nat

iona

l Grid

Key

Span

Cor

p.C

8/24

/07

18EE

$7.4

bill

ion

cash

+ $

4.5

billi

on lo

ng-t

erm

deb

t11

,877

.5

12/1

9/05

FPL

Gro

up In

c.C

onst

ella

tion

Ener

gy In

c.W

10/2

5/06

EE$1

1.3

billi

on e

quity

+ $

4.1

billi

on n

et d

ebt a

nd p

ensi

on li

abili

ties

15,3

11.5

5/24

/05

Mid

Am

eric

an E

nerg

y H

oldi

ngs

Co.

Pac

ifico

rpC

3/21

/06

10EE

$5.1

bill

ion

cash

+ $

4.3

billi

on in

net

deb

t and

pre

ferr

ed s

tock

9,30

0.0

5/9/

05D

uke

Ener

gy C

orp.

Cin

ergy

Cor

p.C

4/3/

0611

EE$9

.1 b

illio

n eq

uity

+ $

5.5

billi

on n

et d

ebt a

nd p

ensi

on li

abili

ties

14,6

00.0

12/2

0/04

Exel

on C

orp.

Pub

lic S

ervi

ce E

nter

pris

e G

roup

W

9/14

/06

EE$1

2.3

billi

on in

equ

ity +

$13

.4 b

illio

n in

net

deb

t and

pen

sion

liab

ilitie

s25

,700

.0

7/25

/04

PN

M R

esou

rces

TNP

Ent

erpr

ises

C6/

6/05

12EE

$189

mill

ion

in s

tock

and

cas

h an

d $8

35 m

illio

n in

deb

t1,

024.

0

2/3/

04A

mer

en C

orp

Illin

ois

Pow

er3

C10

/1/0

48

EE$1

.9 b

illio

n in

deb

t, pr

ef s

tock

, & o

ther

liab

+ $

400

mill

ion

in c

ash

2,30

0.0

11/2

4/03

Sagu

aro

Util

ity G

roup

L.P

.U

niSo

urce

Ene

rgy

W12

/30/

04P

E$8

50 m

illio

n ca

sh +

$2

billi

on in

deb

t2,

850.

0

11/3

/03

Exel

on C

orp.

Illin

ois

Pow

erW

11/2

2/03

EE$2

75 m

illio

n ca

sh +

$1.

8 bi

llion

in d

ebt +

$15

0 m

illio

n pr

omis

sory

not

e

2,22

5.0

4/30

/02

Aqu

ila In

cC

ogen

trix

Ene

rgy

Inc

W8/

2/02

EIP

P$4

15 m

illio

n ca

sh +

$1.

125

billi

on in

ass

umed

deb

t1,

540.

0

4/29

/02

Am

eren

Cor

pC

ILC

OR

P4

C1/

31/0

39

EE$5

41 m

illio

n ca

sh +

$78

1 in

ass

umed

deb

t + $

41 m

illio

n in

pre

f sto

ck1,

400.

0

10/8

/01

Nor

thw

est N

atur

al G

asP

ortla

nd G

ener

alW

5/16

/02

GE

$1.5

5 bi

llion

cas

h +

$25

0mm

in s

tock

1,80

0.0

9/20

/01

Duk

e En

ergy

Wes

tcoa

st E

nerg

yC

3/14

/02

6EG

Equi

ty +

cas

h va

lued

at $

27.9

0 pe

r W

estc

oast

sha

re8,

500.

0

9/10

/01

Dom

inio

n R

esou

rces

Loui

s D

reyf

us N

atur

al G

as

C11

/1/0

12

EG$8

90m

m c

ash

+ $

900m

m s

tock

+$5

05m

m d

ebt

2,29

5.0

2/20

/01

Ener

gy E

ast

RG

S En

ergy

C6/

28/0

216

EE$1

.4 b

ill. c

ash

& e

quity

+ $

1.0

bill.

net

deb

t2,

400.

0

2/12

/01

PEP

CO

Con

ectiv

C8/

1/02

18EE

$2.2

bill

cas

h &

equ

ity +

$2.

8 bi

ll. n

et d

ebt

5,00

0.0

11/9

/00

PN

MW

este

rn R

esou

rces

5W

1/8/

02EE

Stoc

k tr

ansf

er4,

442.

0

10/2

/00

Nor

thW

este

rnM

onta

na P

ower

6C

2/15

/02

16EE

$1.1

bill

ion

in c

ash

1,10

0.0

9/5/

00N

atio

nal G

rid G

roup

N

iaga

ra M

ohaw

kC

1/31

/02

16EE

$19

per

shar

e8,

900.

0

8/8/

00Fi

rstE

nerg

yG

PU

Inc.

C11

/7/0

115

EE$3

5.60

per

sha

re12

,000

.0

7/31

/00

FPL

Gro

upEn

terg

yW

4/2/

01EE

1/1

- FP

L, 0

.585

/1 -

ETR

27,0

00.0

7/17

/00

AES

Cor

pora

tion

IPA

LCO

C3/

27/0

18

IPP

E$2

5 pe

r sh

are

3,0

40.0

6/30

/00

NS

Pow

erB

ango

r H

ydro

CEm

era

10/1

0/01

16EE

$26.

50 p

er s

hare

206.

0

5/30

/00

WP

S R

esou

rces

Wis

cons

in F

uel a

nd L

ight

C4/

2/01

11EG

1.73

sha

res

of W

PSR

55.0

2/28

/00

Pow

erG

en p

lcLG

&E

C12

/11/

0010

EE$2

4.85

per

sha

re5,

400.

0

11/1

0/99

Ener

gy E

ast

Ber

kshi

re E

nerg

y R

esou

rces

C9/

1/00

10EG

$38

per

shar

e13

6.0

11/8

/99

Sier

ra P

acifi

c R

esou

rces

Por

tland

Gen

eral

W4/

26/0

1EE

$2.1

bill

ion

3,10

0.0

11/4

/99

Key

Span

East

ern

Ente

rpris

esC

11/9

/00

12EG

$64

per

shar

e2,

500.

0

10/2

5/99

Ber

kshi

re H

atha

way

Mid

Am

eric

an E

nerg

yC

3/14

/00

5P

E$3

5.05

per

sha

re9,

000.

0

10/1

3/99

Con

solid

ated

Edi

son

Nor

thea

st U

tiliti

esW

3/15

/01

EE$2

5 pe

r sh

are

7,50

0.0

10/5

/99

DTE

Ene

rgy

MC

N E

nerg

yC

5/31

/01

19EG

$28.

50 p

er s

hare

4,60

0.0

9/23

/99

Pec

o En

ergy

Co.

Uni

com

Cor

p.C

Exel

on10

/23/

0013

EE0.

95/1

- U

CM

, 1/1

- P

E31

,800

.0

9/9/

99A

llegh

eny

Ener

gyW

est V

irgin

ia P

ower

C1/

4/00

4EE

$75

mill

ion

75.0

8/23

/99

Car

olin

a P

ower

& L

ight

Flor

ida

Pro

gres

sC

Pro

gres

s En

ergy

11

/30/

0015

EE$5

4 pe

r sh

are

8,00

0.0

6/30

/99

Ener

gy E

ast

CTG

Res

ourc

esC

9/1/

0015

EG$4

1 pe

r sh

are

575.

0

6/28

/99

Wis

cons

in E

nerg

y C

orp.

Wic

or In

c.C

4/26

/00

10EG

$31.

50 p

er s

hare

1,27

5.0

6/15

/99

Ener

gy E

ast

CM

P G

roup

, Inc

.C

9/1/

0015

EE$2

9.50

per

sha

re

1,22

8.0

6/15

/99

Nor

thea

st U

tiliti

esYa

nkee

Gas

C3/

1/00

9EG

$45

per

shar

e67

9.0

6/14

/99

Dyn

egy

Illin

ova

C2/

2/00

7IP

PE

0.69

/1 -

DYN

, 1/1

- IL

N2,

000.

0

6/14

/99

Indi

ana

Ener

gySi

gCor

pC

Vect

ren

3/31

/00

9G

E1.

33/1

- S

IG, 1

/1-

IEI

1,90

0.0

6/7/

99N

isou

rce

Inc.

Col

umbi

a En

ergy

C11

/1/0

017

EG$7

4/sh

are

6,20

0.0

5/25

/99

S.W

. Acq

uisi

tion

Cor

p.TN

P C

orpo

ratio

nC

4/7/

0011

PE

$74

per

shar

e10

0.0

5/17

/99

OG

E En

ergy

Tran

sok

LLC

C7/

1/99

2EG

$701

mill

ion

701.

0

5/11

/99

Util

icor

p U

nite

dEm

pire

Dis

tric

t Ele

ctric

W1/

3/01

EE$2

9.50

per

sha

re in

cas

h or

sto

ck76

5.0

4/23

/99

Ener

gy E

ast

Con

nect

icut

Ene

rgy

C2/

9/00

9EG

$42

per

shar

e, 5

0% c

ash

and

1.43

-1.8

2/1

- C

NE

617.

0

3/25

/99

Nor

ther

n St

ates

Pow

erN

ew C

entu

ry E

nerg

ies

CXc

el E

nerg

y8/

17/0

017

EE1.

55/1

- N

CE,

1/1

- N

SP6,

000.

0

3/5/

99U

tilic

orp

Uni

ted

St. J

osep

h P

ower

& L

ight

Co.

C12

/29/

0021

EE$2

3 pe

r sh

are

277.

0

2/22

/99

Dom

inio

n R

esou

rces

Con

solid

ated

Nat

ural

Gas

Co.

C1/

28/0

011

EG$6

6.60

per

sha

re6,

400.

0

2/17

/99

SCA

NA

Cor

pP

SC O

f Nor

th C

arol

ina

C2/

10/0

012

EG$3

3 pe

r sh

are

or 1

.02-

1.45

sha

res

of S

CG

9,00

0.0

2/1/

99N

atio

nal G

rid U

SA/N

EES

East

ern

Util

ities

Ass

ocia

tes

C4/

19/0

014

EE$3

1 pe

r sh

are

in c

ash

634.

0

2/1/

99Se

mpr

a En

ergy

KN

Ene

rgy

W6/

1/99

EG$2

5 pe

r sh

are

6.0

1 TX

U (

now

Ene

rgy

Futu

re H

oldi

ngs

Cor

p.)

was

acq

uire

d by

the

Texa

s En

ergy

Fut

ure

Hol

ding

s Li

mite

d P

artn

ersh

ip (

TEF)

on

10/1

0/20

07.

TE

F w

as fo

rmed

by

a gr

oup

of in

vest

ors

led

by K

ohlb

erg

Kra

vis

Rob

erts

and

Tex

as P

acifi

c G

roup

to fa

cilit

ate

the

mer

ger.

2 A

mer

en p

urch

ased

Illin

ois

Pow

er fr

om D

yneg

y C

orpo

ratio

n. D

yneg

y C

orp

acqu

ired

Illin

ois

Pow

er in

Feb

ruar

y 20

00.

3 A

mer

en p

urch

ased

CIL

CO

RP

from

AES

Cor

pora

tion.

AES

Cor

p ac

quire

d C

ILC

OR

P in

O

ctob

er 1

999.

4 P

NM

pur

chas

ed W

este

rn R

esou

rces

’ ele

ctric

ope

ratio

ns in

clud

ing

gene

ratio

n,

tran

smis

sion

, and

dis

trib

utio

n.

5 N

orth

Wes

tern

Cor

pora

tion

purc

hase

d M

onta

na P

ower

’s e

lect

ric a

nd n

atur

al g

as tr

ansm

issi

on

and

dist

ribut

ion

asse

ts.

NA

= A

cqui

red

com

pany

priv

atel

y he

ld o

r no

dat

a av

aila

ble

Sour

ce: E

EI F

inan

ce D

epar

tmen

t and

SN

L Fi

nanc

ial

C =

Com

plet

edW

= W

ithdr

awn

PN

= P

endi

ngE

= E

lect

ricG

= G

as

O =

Oil

IPP

= In

depe

nden

t

Pow

er P

rodu

cer

P =

Priv

atiz

ed

Mer

gers

& A

cqui

sitio

ns A

nnou

ncem

ents

U

pdat

ed th

roug

h M

arch

31,

201

4U

.S. I

NVE

STO

R-O

WN

ED E

LEC

TRIC

UTI

LITI

ES

Ann’

cdBu

yer

Selle

r/Ac

quir

ed/M

erge

dSt

atus

New

Co

mpa

nyDa

teCo

mpl

eted

Mon

ths

to

Com

plet

eBu

s.Te

rms

Tran

s. V

al. (

$MM

)3/

3/14

UIL

Hol

ding

sP

hila

delp

hia

Gas

Wor

ksP

UIL

to a

quire

ass

ets

& lia

biliti

es o

f PG

W fr

om c

ity o

f Phi

lade

lphi

a fo

r $1.

86 B

in c

ash

1,86

0.0

12/1

2/13

Fort

is In

c.U

NS

Ener

gyP

EEFo

rtis

pays

$60

.25/

shar

e (3

1% p

rem

ium

to a

nnou

ncem

ent d

ay’s

clo

se) +

$1

.8B

in d

ebt

4,57

8.1

5/29

/13

Mid

Am

eric

an E

nerg

y H

oldi

ngs

Co.

NV

Ener

gyC

12/1

9/13

7EE

Mid

Am

eric

an p

ays

$23.

75/s

hare

+ a

ssum

e $4

.8 b

illio

n de

bt10

,494

.3

5/25

/13

TEC

O E

nerg

y, In

c.N

ew M

exic

o G

as In

term

edia

te, I

nc.

PEE

TEC

O w

ill p

ay $

950

mill

ion,

incl

udin

g as

sum

e $2

00 m

illio

n de

bt to

C

ontin

enta

l Ene

rgy

Syst

ems

LLC

950.

0

2/20

/12

Fort

is In

c.C

H E

nerg

y G

roup

PEE

Forti

s pa

ys $

65.0

0/sh

are

CH

Ene

rgy

Gro

up &

ass

umes

$68

7 m

m d

ebt

1,60

9.7

7/11

/11

Gaz

Met

ro L

PC

entr

al V

erm

ont P

ublic

Ser

vice

C

6/2

7/12

12

GE

Gaz

Mét

ro p

ays

$35.

25/C

VPS

shar

e &

ass

umes

$22

6 m

m d

ebt

704.

2

5/27

/11

Fort

is In

c.C

entr

al V

erm

ont P

ublic

Ser

vice

W

7/11

/11

EE

Fort

is p

ays

$35.

10/s

hare

cas

h &

ass

umes

$22

6.4

mm

deb

t70

1.6

4/28

/11

Exel

on C

orp.

Con

stel

latio

n En

ergy

Gro

up

C

3/12

/12

11

EEC

EG re

ceiv

es 0

.93

EXC

sha

res/

CEG

sha

re. E

XC a

ssum

es $

2.9

bill

debt

10,6

23.2

4/19

/11

AES

Cor

pora

tion

DP

L In

c.C

11

/28/

117

EEA

ES p

ays

$30.

0/sh

are

cash

& a

ssum

es a

ppro

x. $

1.1

bill

of d

ebt

4,61

3.2

1/8/

11D

uke

Ener

gyP

rogr

ess

Ener

gyC

7/

3/12

1

8EE

0.87

083

Duk

e sh

ares

(af

ter

1-3

reve

rse

split

) fo

r ea

ch P

rogr

ess

shar

e +

as

sum

e $1

2.1

billi

on n

et d

ebt

32,0

00

10/1

6/10

Nor

thea

st U

tiliti

esN

STA

RC

4/10

/12

18EE

1.31

2 N

U s

hare

s fo

r ea

ch N

STA

R s

hr, p

lus

$3.3

6 bi

ll as

sum

e de

bt

7,56

6.7

4/28

/10

PP

L C

orp.

E.O

N U

.S.

C11

/1/1

06

EE$6

.83

billi

on c

ash

+ $

764.

0 m

illio

n in

ass

umed

deb

t7,

625.

0

3/12

/10

Emer

a In

cM

aine

& M

ariti

mes

C12

/21/

109

EE$7

6 m

m c

ash

+ $

28.6

mm

deb

t + $

13.8

mm

pos

tret

irem

ent b

enefi

ts11

7.4

2/10

/10

Firs

tEne

rgy

Alle

ghen

y En

ergy

C

2/25

/11

12EE

$4.3

bill

ion

in e

quity

+ $

4.7

billi

on in

ass

umed

deb

t9,

273.

2

9/17

/08

Ber

kshi

re H

atha

way

Con

stel

latio

n En

ergy

Gro

up In

c.

W12

/17/

08

PE

$4.7

bill

cas

h +

$4.

4 bi

ll ne

t deb

t and

adj

ustm

ents

9,15

2.5

7/25

/08

Sem

pra

Ener

gyEn

ergy

Sout

h In

c.

C10

/1/0

83

EG$4

99 m

illio

n ca

sh +

283

mill

ion

debt

771.

9

7/1/

08M

DU

Res

ourc

es G

roup

, Inc

.In

term

ount

ain

Gas

Co.

C

10/1

/08

3EG

$245

mill

ion

cash

+ $

82 m

illio

n de

bt32

7.0

6/25

/08

Duk

e En

ergy

Cat

amou

nt E

nerg

y C

orp.

C

9/15

/08

3EP

$240

mill

ion

cash

+ $

80 m

illio

n as

sum

ed d

ebt

320.

0

2/15

/08

Uni

til C

orp.

N

orth

en U

tiliti

es, I

nc./

Gra

nite

St

ate

Gas

Tra

nsm

issi

on, I

nc.

C12

/1/0

810

EG$1

60 m

illio

n ca

sh16

0.0

1/12

/08

PN

M R

esou

rces

, Inc

.C

ap R

ock

Hol

ding

Cor

p.W

7/22

/08

EE

202.

5

10/2

6/07

Mac

quar

ie C

onso

rtiu

mP

uget

Ene

rgy

C2/

6/09

16EE

$3.5

bill

ion

cash

+ $

3.02

bill

ion

net d

ebt

6,52

0.2

6/25

/07

Iber

drol

a S.

A.

Ener

gy E

ast C

orp.

C9/

16/0

815

EE$4

.5 b

illio

n ca

sh +

$4.

1 bi

llion

net

deb

t 8,

600.

0

2/26

/07

KK

R &

Tex

as P

acifi

c G

roup

TXU

Cor

p.1

CEn

ergy

Fut

ure

H

oldi

ngs

Cor

p.10

/10/

078

PE

$31.

8 bi

llion

cas

h +

$12

.1 b

illio

n ne

t deb

t43

,882

.0

2/7/

07B

lack

Hill

s C

orp.

/ G

reat

Pla

ins

Ener

gy In

c.2

Aqu

ila In

c. (

CO

ele

c. u

til. +

CO

, K

S, N

E, IA

gas

util

s. )

C7/

14/0

817

EG$9

40 m

illio

n ca

sh +

wor

king

cap

ital a

nd o

ther

adj

ustm

ents

940.

0

7/8/

06M

DU

Res

ourc

es G

roup

, Inc

.C

asca

de N

atur

al G

as C

orpo

ratio

nC

7/2/

0712

EG$3

05.2

mm

in c

ash

+ (

$173

.6 in

deb

t - $

13.0

in c

ash

equi

vale

nts)

465.

8

7/8/

06W

PS

Res

ourc

es C

orpo

ratio

nP

eopl

es E

nerg

y C

orpo

ratio

nC

Inte

grys

Ene

rgy

Gro

up2/

21/0

77

EG$2

.47

billi

on2,

472.

4

7/5/

06M

acqu

arie

Con

sort

ium

Duq

uesn

e Li

ght H

oldi

ngs

C5/

31/0

710

EE$1

.59

billi

on c

ash

+ $

1.09

bill

ion

tota

l deb

t2,

674.

4

6/22

/06

Gaz

Met

ro L

PG

reen

Mou

ntai

n P

ower

Cor

p.C

4/12

/07

10EE

$187

mill

ion

in c

ash

+ (

$100

.8 d

ebt -

$9.

1mm

in c

ash

equi

vale

nts)

279.

5

5/11

/06

ITC

Hol

ding

s C

orp

Mic

higa

n El

ectr

ic T

rans

mis

sion

C

o.C

10/1

0/06

5EE

$485

.6m

m c

ash

+ $

70m

m c

omm

on s

tock

+ $

311m

m a

ssum

ed d

ebt

866.

6

4/25

/06

Bab

cock

and

Bro

wn

Infr

astr

uctu

reN

orth

Wes

tern

Cor

p.W

7/24

/07

EE$2

.2 b

illio

n ca

sh2,

200.

0

2/27

/06

Nat

iona

l Grid

Key

Span

Cor

p.C

8/24

/07

18EE

$7.4

bill

ion

cash

+ $

4.5

billi

on lo

ng-t

erm

deb

t11

,877

.5

12/1

9/05

FPL

Gro

up In

c.C

onst

ella

tion

Ener

gy In

c.W

10/2

5/06

EE$1

1.3

billi

on e

quity

+ $

4.1

billi

on n

et d

ebt a

nd p

ensi

on li

abili

ties

15,3

11.5

5/24

/05

Mid

Am

eric

an E

nerg

y H

oldi

ngs

Co.

Pac

ifico

rpC

3/21

/06

10EE

$5.1

bill

ion

cash

+ $

4.3

billi

on in

net

deb

t and

pre

ferr

ed s

tock

9,30

0.0

5/9/

05D

uke

Ener

gy C

orp.

Cin

ergy

Cor

p.C

4/3/

0611

EE$9

.1 b

illio

n eq

uity

+ $

5.5

billi

on n

et d

ebt a

nd p

ensi

on li

abili

ties

14,6

00.0

12/2

0/04

Exel

on C

orp.

Pub

lic S

ervi

ce E

nter

pris

e G

roup

W

9/14

/06

EE$1

2.3

billi

on in

equ

ity +

$13

.4 b

illio

n in

net

deb

t and

pen

sion

liab

ilitie

s25

,700

.0

7/25

/04

PN

M R

esou

rces

TNP

Ent

erpr

ises

C6/

6/05

12EE

$189

mill

ion

in s

tock

and

cas

h an

d $8

35 m

illio

n in

deb

t1,

024.

0

2/3/

04A

mer

en C

orp

Illin

ois

Pow

er3

C10

/1/0

48

EE$1

.9 b

illio

n in

deb

t, pr

ef s

tock

, & o

ther

liab

+ $

400

mill

ion

in c

ash

2,30

0.0

11/2

4/03

Sagu

aro

Util

ity G

roup

L.P

.U

niSo

urce

Ene

rgy

W12

/30/

04P

E$8

50 m

illio

n ca

sh +

$2

billi

on in

deb

t2,

850.

0

11/3

/03

Exel

on C

orp.

Illin

ois

Pow

erW

11/2

2/03

EE$2

75 m

illio

n ca

sh +

$1.

8 bi

llion

in d

ebt +

$15

0 m

illio

n pr

omis

sory

not

e

2,22

5.0

4/30

/02

Aqu

ila In

cC

ogen

trix

Ene

rgy

Inc

W8/

2/02

EIP

P$4

15 m

illio

n ca

sh +

$1.

125

billi

on in

ass

umed

deb

t1,

540.

0

4/29

/02

Am

eren

Cor

pC

ILC

OR

P4

C1/

31/0

39

EE$5

41 m

illio

n ca

sh +

$78

1 in

ass

umed

deb

t + $

41 m

illio

n in

pre

f sto

ck1,

400.

0

10/8

/01

Nor

thw

est N

atur

al G

asP

ortla

nd G

ener

alW

5/16

/02

GE

$1.5

5 bi

llion

cas

h +

$25

0mm

in s

tock

1,80

0.0

9/20

/01

Duk

e En

ergy

Wes

tcoa

st E

nerg

yC

3/14

/02

6EG

Equi

ty +

cas

h va

lued

at $

27.9

0 pe

r W

estc

oast

sha

re8,

500.

0

9/10

/01

Dom

inio

n R

esou

rces

Loui

s D

reyf

us N

atur

al G

as

C11

/1/0

12

EG$8

90m

m c

ash

+ $

900m

m s

tock

+$5

05m

m d

ebt

2,29

5.0

2/20

/01

Ener

gy E

ast

RG

S En

ergy

C6/

28/0

216

EE$1

.4 b

ill. c

ash

& e

quity

+ $

1.0

bill.

net

deb

t2,

400.

0

2/12

/01

PEP

CO

Con

ectiv

C8/

1/02

18EE

$2.2

bill

cas

h &

equ

ity +

$2.

8 bi

ll. n

et d

ebt

5,00

0.0

11/9

/00

PN

MW

este

rn R

esou

rces

5W

1/8/

02EE

Stoc

k tr

ansf

er4,

442.

0

10/2

/00

Nor

thW

este

rnM

onta

na P

ower

6C

2/15

/02

16EE

$1.1

bill

ion

in c

ash

1,10

0.0

9/5/

00N

atio

nal G

rid G

roup

N

iaga

ra M

ohaw

kC

1/31

/02

16EE

$19

per

shar

e8,

900.

0

8/8/

00Fi

rstE

nerg

yG

PU

Inc.

C11

/7/0

115

EE$3

5.60

per

sha

re12

,000

.0

7/31

/00

FPL

Gro

upEn

terg

yW

4/2/

01EE

1/1

- FP

L, 0

.585

/1 -

ETR

27,0

00.0

7/17

/00

AES

Cor

pora

tion

IPA

LCO

C3/

27/0

18

IPP

E$2

5 pe

r sh

are

3,0

40.0

6/30

/00

NS

Pow

erB

ango

r H

ydro

CEm

era

10/1

0/01

16EE

$26.

50 p

er s

hare

206.

0

5/30

/00

WP

S R

esou

rces

Wis

cons

in F

uel a

nd L

ight

C4/

2/01

11EG

1.73

sha

res

of W

PSR

55.0

2/28

/00

Pow

erG

en p

lcLG

&E

C12

/11/

0010

EE$2

4.85

per

sha

re5,

400.

0

11/1

0/99

Ener

gy E

ast

Ber

kshi

re E

nerg

y R

esou

rces

C9/

1/00

10EG

$38

per

shar

e13

6.0

11/8

/99

Sier

ra P

acifi

c R

esou

rces

Por

tland

Gen

eral

W4/

26/0

1EE

$2.1

bill

ion

3,10

0.0

11/4

/99

Key

Span

East

ern

Ente

rpris

esC

11/9

/00

12EG

$64

per

shar

e2,

500.

0

10/2

5/99