2009 Manitoba

Transportation

Report

Prepared For: Manitoba Infrastructure and Transportation

Transport Institute, University of Manitoba

This report has been financially supported by the Manitoba Department of

Infrastructure and Transportation. The views expressed do not necessarily represent

those of the Department. The Department provides no warranties as to the validity or

accuracy of the information presented herein.

Introduction

The worldwide recession has had a profound impact on all business segments, with every

sector of the economy being affected. The impact on transportation has been significant with the

idling of hundreds of container vessels, abundant capacity in truck fleets, and a significant drop

in rail car loadings. We are only at the beginning of the turnaround with indications of a

strengthening economy appearing weekly.

Major issues being addressed in Canada’s premier conferences in 2009 include Rail Service,

Near-Sourcing, Supply on Demand, and China’s comeback. The need for detailed information

on all aspects of transportation flowing in and through the province of Manitoba has not

diminished but become ever more important for policy and decision makers in the province.

The Manitoba Transportation Report has been developed to fill this need for detailed

transportation information and trends. This report is produced for Manitoba Infrastructure and

Transportation. The target audience is the Minister of Infrastructure and Transportation,

executive officers in the department responsible for policy development and the many policy

analysts that support the department’s activities.

Data presented in this report is the latest available Statistics Canada, Manitoba Bureau of

Statistics, and industry data. This year’s report has been reformatted to better reflect the nature

of the information being presented. Due to the varying release dates of statistics, it is difficult to

present data in a consistent time-frame while still utilizing the most recent data available. In this

edition, all statistics and figures are current to at least 2007, while some further present data

collected in 2008 and 2009. A particular problem in data gathering over the past year has been

the lack of weight data reported by Statistics Canada. UMTI has developed a methodology to

estimate the weights based on historical weight to value relationships. We have been working

with Statistics Canada to reestablish the reporting of weight data in Statistics Canada reporting

systems.

Table of Contents

1. The Economic Impact of Transportation in Manitoba - $3.23 Billion in 2007 ............................ 1

2. Transportation and Warehousing and the Regional Canadian Economy ............................... 18

3. The State of the Macro Economy ................................................................................................... 40

Manitoba Economic Situation ................................................................................................... 46

Economic Indicators ................................................................................................................... 47

Monetary and Energy Indicators .............................................................................................. 59

4. Trade .................................................................................................................................................. 68

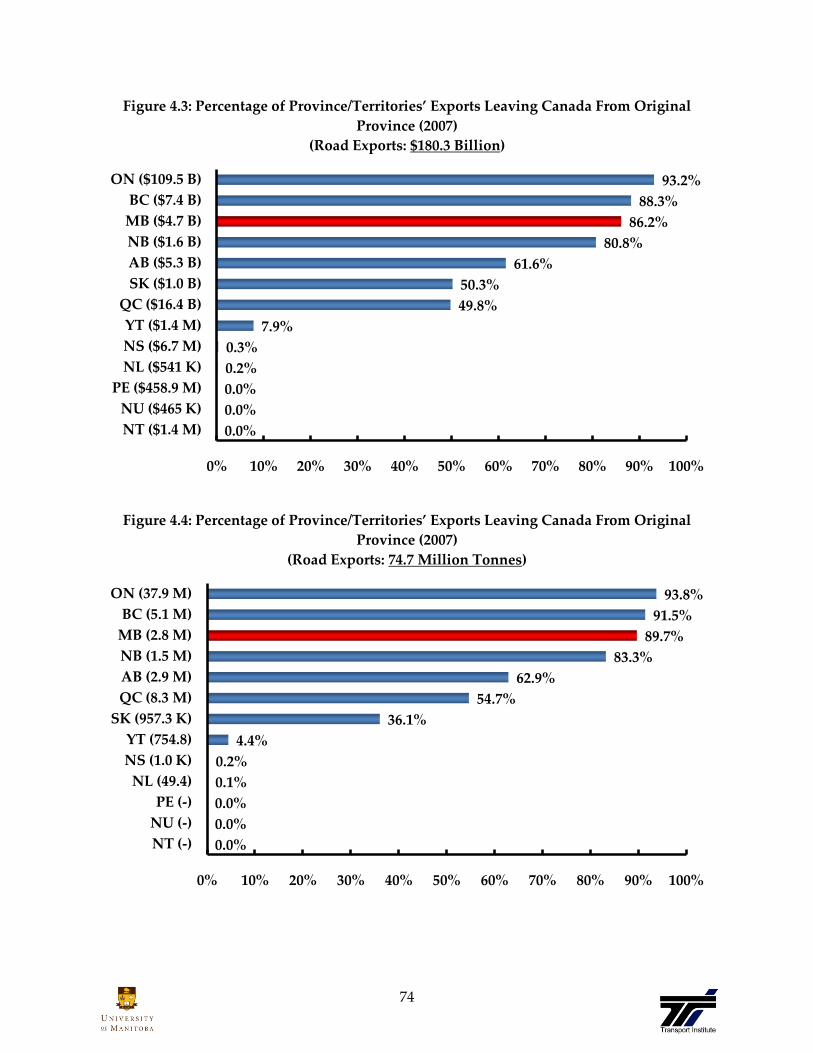

Domestic Trade & Infrastructure Utilization .......................................................................... 71

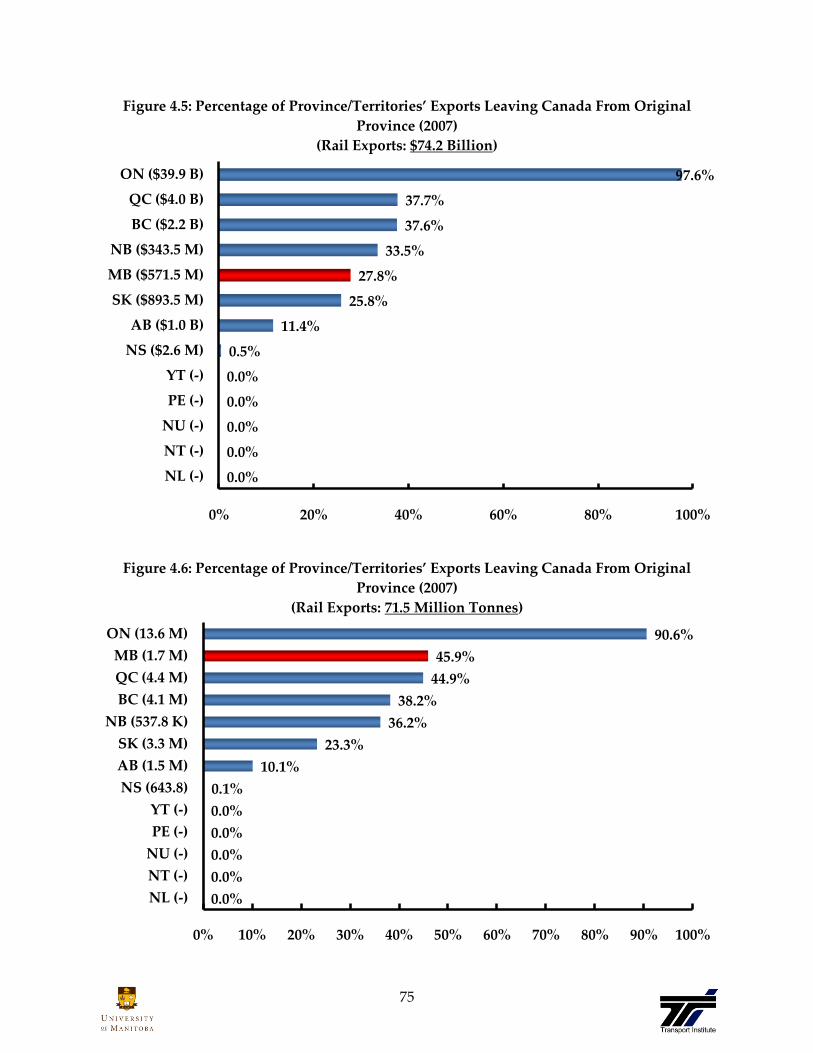

Export Routing and Usage of Transportation Infrastructure ......................................... 71

Usage of Manitoba’s Transportation Infrastructure ........................................................ 77

Manitoban Export Border Crossings ................................................................................. 95

Canadian Export Border Crossings ................................................................................... 99

Manitoban Import Border Crossings ............................................................................... 101

Canadian Import Border Crossings ................................................................................. 105

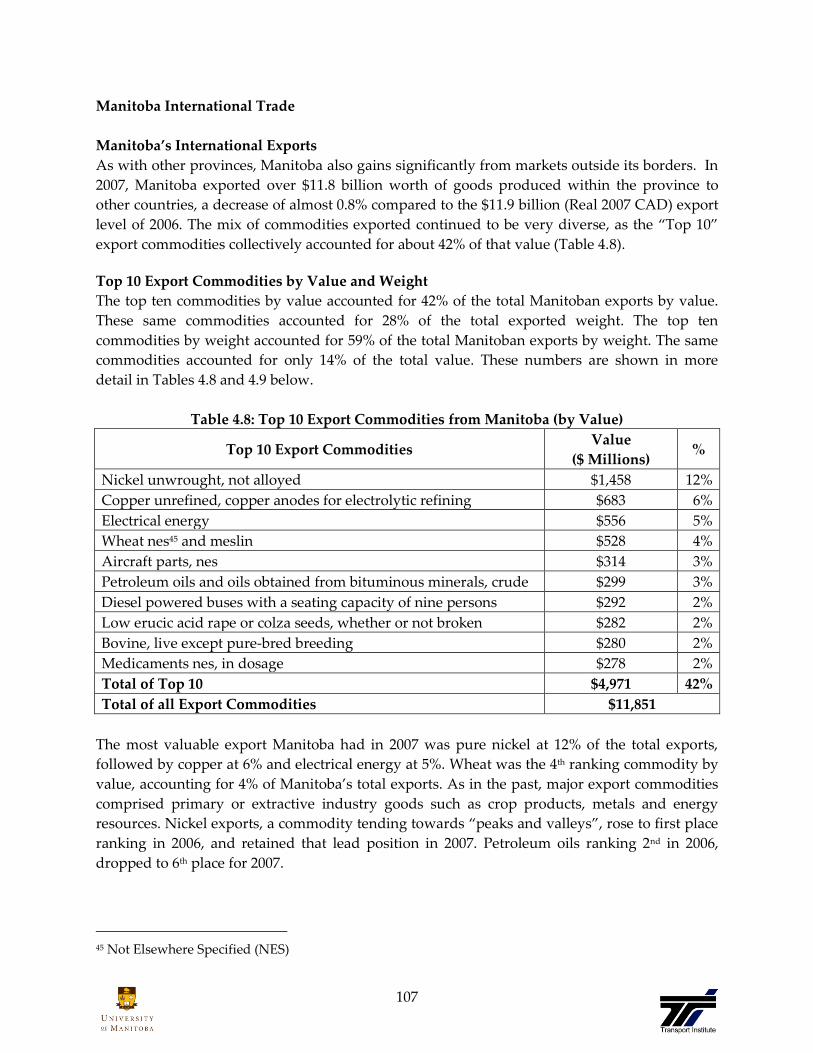

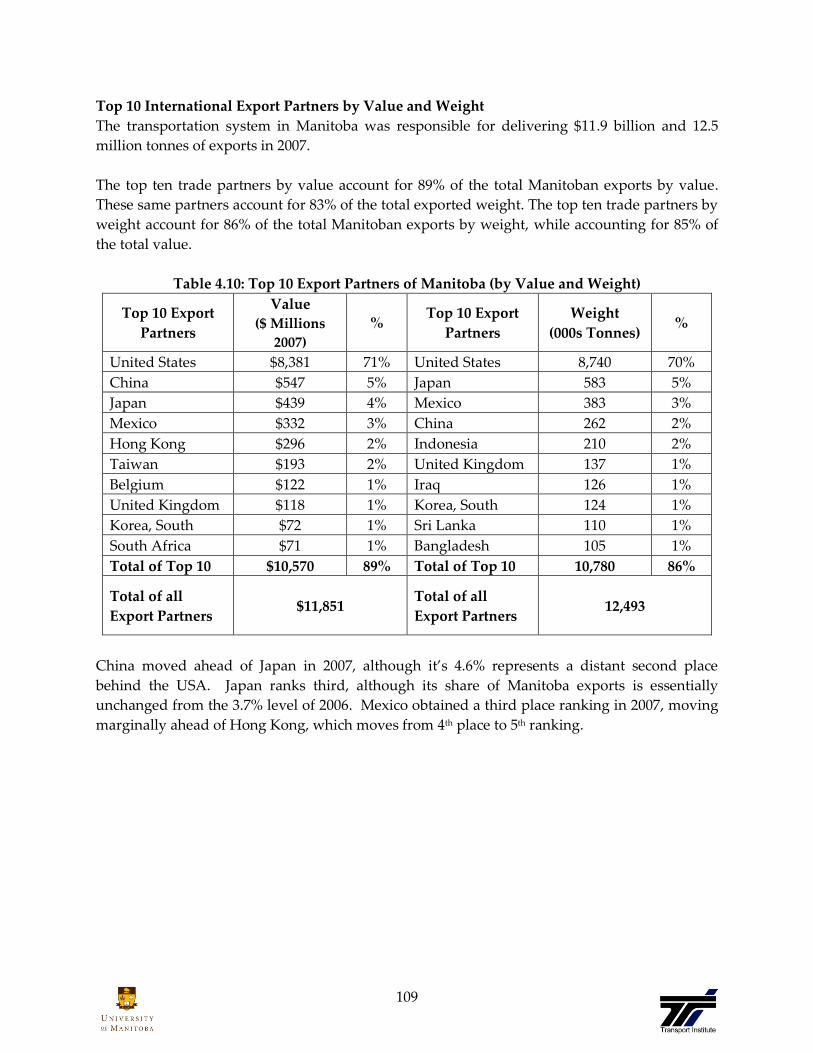

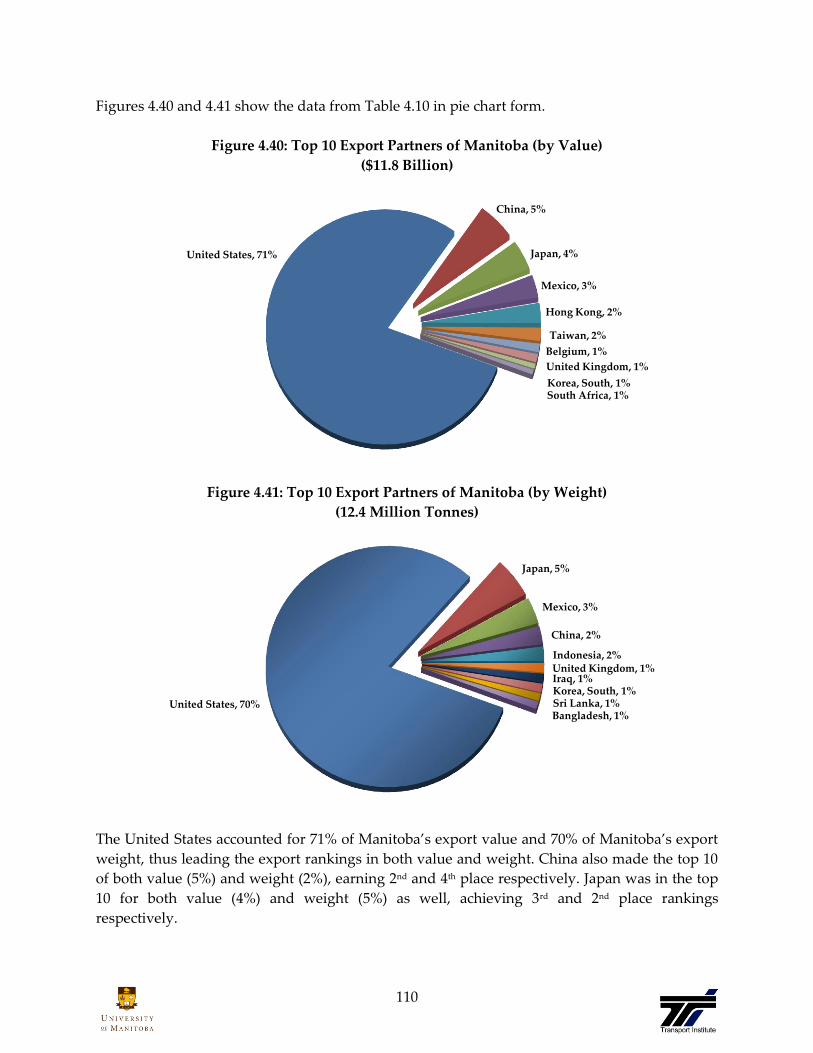

Manitoba International Trade ................................................................................................. 107

Manitoba’s International Exports ........................................................................................... 107

Manitoba’s International Imports .................................................................................... 113

NASCO Trade ............................................................................................................................ 119

Exports ........................................................................................................................................ 119

Imports ................................................................................................................................. 127

5. International Markets .................................................................................................................... 135

Advanced Markets .................................................................................................................... 135

European Union .................................................................................................................. 137

Japan ..................................................................................................................................... 145

United Kingdom ................................................................................................................. 151

United States ....................................................................................................................... 158

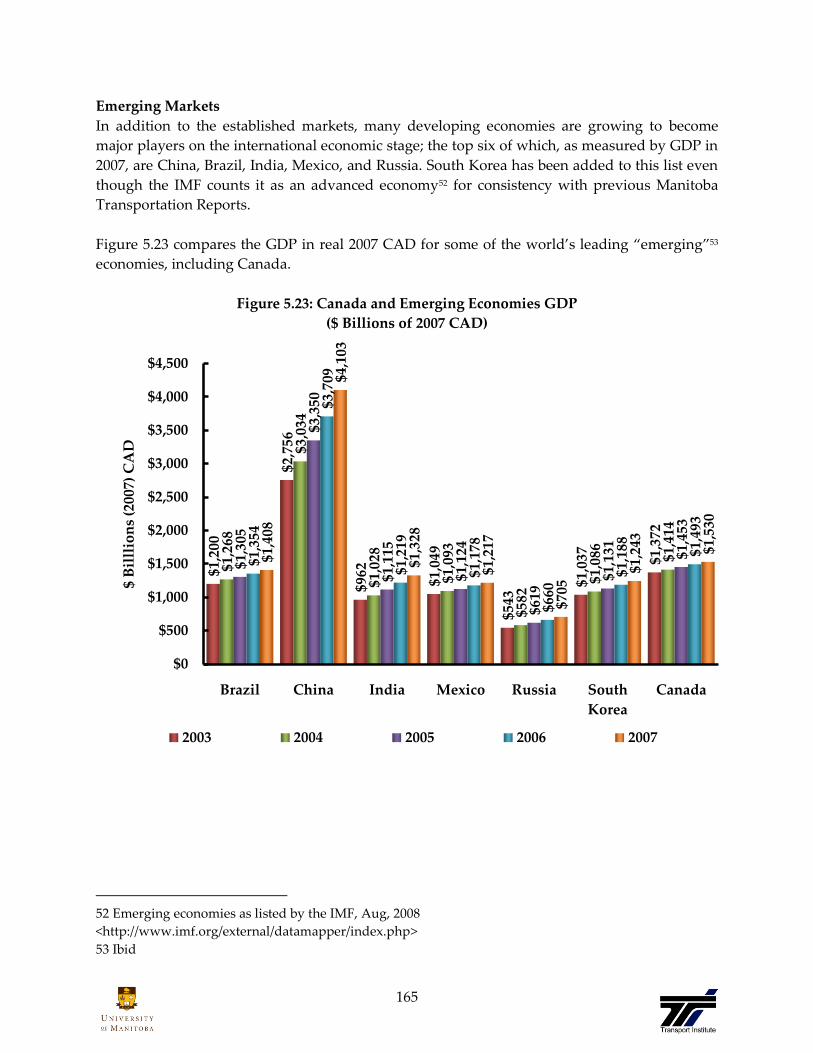

Emerging Markets ..................................................................................................................... 165

Brazil ..................................................................................................................................... 167

China .................................................................................................................................... 174

India ...................................................................................................................................... 180

Mexico .................................................................................................................................. 186

Russia ................................................................................................................................... 192

South Korea ......................................................................................................................... 198

Canadian International Trade ................................................................................................. 204

Exports ................................................................................................................................. 204

Imports ................................................................................................................................. 219

Glossary ................................................................................................................................................... 235

List of Figures ......................................................................................................................................... 239

List of Tables ........................................................................................................................................... 245

1

1. The Economic Impact of Transportation in Manitoba1 - $3.23 Billion in 20072

The activities of various sectors of an economy are intertwined with those of other sectors in an

economy such that the economic impact is magnified or multiplied throughout the overall

economy. Measurement of such effects is undertaken through economic impact models which

attempt to quantify the intersectoral relationships. There are numerous designs of such models,

which vary primarily in the scope of the ‚net‛ which defines the direct impacts of the sector

under investigation.

For this study of transportation in Manitoba, the definition applied is the commercial carriage of

goods and people. This definition is advantageous to producing sound measures of the impact.

It limits criticism of overstatement of the effects by limiting the sectors considered to those

directly performing commercial transportation. It excludes allied sectors such as service

industries (example hotels), repair shops, or equipment manufacturers. When included these

allied sectors open the measured economic impact to criticism since the multiplicative effects of

activities from the direct industry include the impacts on these allied sectors. Overall this more

restrictive definition of the sector minimizes the validity of any criticism of double counting.

The Manitoba Bureau of Statistics regularly updates the parameters of the Input/Output model

which proxies the activities of and interactions among the various sectors of the economy. It is

these interactions which provide the iterative process of the model. While making the model a

more accurate reflection of the economy, these revisions compromise the validity of

comparisons made to previous reports3.

The robustness of economic impact results is dependent on the quality of information acquired

about the direct (or economic impact ‚driver‛) sector, and the quality of the input output matrix

used to derive the indirect and direct effects. Manitoba is a relatively small economy with few

firms in many sectors. The consequence is general weakness of direct and input output data.

Two approaches are available to acquire data for the direct sector. Data can be acquired from

third party data providers or the sector can be directly surveyed. In both cases, estimates of the

economic drivers of the entire population are developed from the survey.

1 Annual data updates along with changes in multipliers, may yield results that are not comparable

among annual reports. 2 The dollar related information in this section is in current dollars. 3 An example of this is found when comparing the 2006 Economic Impact of Transportation between the

2008 and 2009 editions of the Manitoba Transportation Report. In the 2008 edition, this figure was

reported as $3.34 Billion.

2

This analysis uses data acquired from third party data providers, principally Statistics Canada.

This approach reduces costs, allows the creation of historical results and assures greater

consistency of that historical information. The modes included in the analysis are:

For Hire Trucking

Rail

Aviation

Couriers and Local Messengers,4 and

Urban and Interurban Bus

Based upon the ‚driver‛ data provided, the Manitoba Bureau of Statistics generates the indirect

and induced effects using multipliers created by its analysis of intersectoral relationships.

Figure 1.1 summarizes the estimated growth in total GDP for Manitoba that is derived solely

from transportation activities5. Total GDP measured on this basis rose from $2.8 billion in 2003

to $3.23 billion in 2007. Overall annual contribution to GDP has remained fairly stable since

rising to $3.2 billion in 2005.

Figure 1.1: Trend in Total GDP from Transportation in Manitoba

($ Billion)

This total includes the leverage effect of direct activity in transportation on other sectors.

4 Couriers and local messengers include the major international courier companies such as FedEx. 5 These transportation activities comprise aviation, trucking, rail, courier, and bus (urban and other) in

Manitoba.

2.802.89

3.20 3.21 3.23

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

2003 2004 2005 2006 2007

3

The total economic impact of transportation is defined as the sum of direct economic activity,

indirect economic activity and induced economic activity. Direct economic activity is measured

by the economic drivers of employment, employment income, and expenditures and

contribution to provincial gross domestic product for the transportation sector. Indirect

activities are those that occur in firms that supply inputs to the direct sector. Induced effects are

the trickle down affects of the expenditures by both the direct and related indirect sector as they

multiply through other sectors of the economy. These are largely driven by consumption

spending. The indirect and induced effects are a measure of the leverage derived from the

direct effect. The higher the amount of leverage, the greater the additional economic activity

spawned from the original source. The total economic impact of the sector can be measured

when the direct and the leverage effects are combined.

Figure 1.2 shows the economic impact of the total Manitoba transportation GDP as a ratio of

direct, indirect, and induced effects.

Figure 1.2: Trend in Total GDP by Leverage Component from Transportation in Manitoba

($ Billion)

$1.00 Direct GDP = $1.95 Total GDP

Leverage Factor = .95

Overall, one dollar of GDP from direct transportation activities results in an additional $0.95

generated through activities in other sectors. In basic terms, the Leverage Factor is determined

by summing the indirect and induced effects and representing that sum as a percentage of the

direct expenditure or effect.

1.43 1.47 1.64 1.64 1.65

0.64 0.660.72 0.72 0.73

0.74 0.76

0.83 0.84 0.84

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

2003 2004 2005 2006 2007

Direct Indirect Induced

2.80 2.89

3.20 3.21 3.23

4

Since 2003, total employment attributable to transportation in Manitoba6 increased from about

47,390 to 50,745 FTEs (Figure 1.3).

Figure 1.3: Trend in Total Transportation Employment in Manitoba

(FTEs)

The level of employment in trucking was a major influence in total FTEs associated with

transportation. As shown in Figure 1.4 and Figure 1.5, trucking represents a major and

increasing share of transportation employment in the province. Although appearing to

stabilize, the number of jobs related to trucking has topped 28,000 in 2007.

6 Statistics Canada made significant adjustments to employment to the 2003 employment data for couriers in 2005.

47,39049,105

52,19550,795 50,745

0

10,000

20,000

30,000

40,000

50,000

60,000

2003 2004 2005 2006 2007

5

Figure 1.4: Trend in Total Employment from Trucking in Manitoba7

Figure 1.5: Trend in Total Employment from Aviation, Couriers, Rail, and Bus

in Manitoba

7 As noted, 2009 figures may appear differently than those reported in previous editions of the Manitoba

Transportation Report, due to economic model updates released by the Manitoba Bureau of Statistics.

20,920

23,495

27,675 27,895 28,280

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2003 2004 2005 2006 2007

9,0758,510

7,1606,680 6,575

4,2303,755 3,760 3,725 3,755

8,100 7,940

8,425

7,500 7,275

5,0655,405 5,175

4,995 4,860

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2003 2004 2005 2006 2007Aviation Couriers Rail Bus

6

As shown in Figure 1.5, non-trucking sectors have generally declined in employment since 2003.

Aviation-related jobs decreased by 2,500 from 2003 to 2007, while bus related jobs declined by

205 FTEs. Rail and courier-related jobs declined by 825 and 475, respectively.

Figure 1.6 shows the total employment by year broken down between direct, indirect, and

induced effects. For each direct job in transportation an additional .93 jobs are created.

Figure 1.6: Trend in Employment by Leverage Component from Transportation

in Manitoba

Number of Employees

1 Direct Job in 2007 = 1.93 Total Jobs

Leverage Factor = .93

24,285 25,205 26,970 26,275 26,255

10,940 11,31511,930 11,640 11,645

12,16512,585

13,295 12,880 12,845

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

2003 2004 2005 2006 2007

Direct Indirect Induced

50,745

47,39049,105

52,195 50,795

7

Total labour income in Manitoba due to the transportation sector rose from $1.68 billion in 2003

to $1.83 billion in 2007 (Figure 1.7).

Figure 1.7: Trend in Total Labour Income from Transportation in Manitoba

($ Billion)

1.681.74

1.86 1.82 1.83

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

2003 2004 2005 2006 2007

8

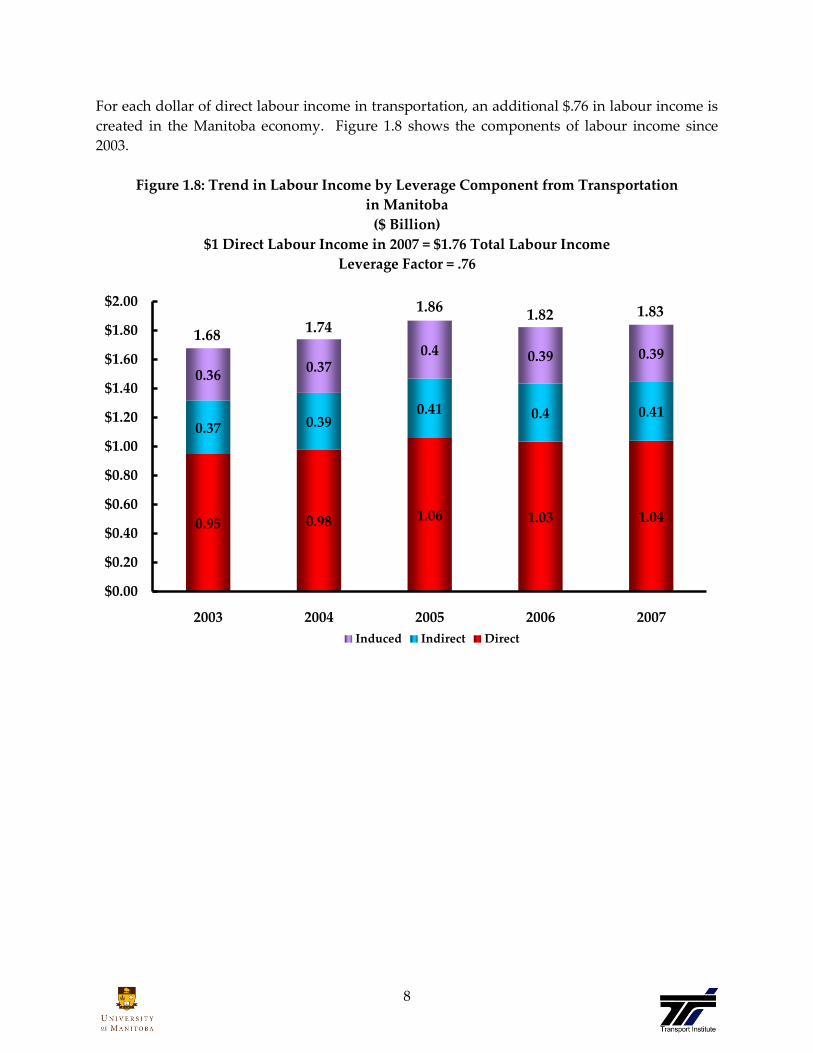

For each dollar of direct labour income in transportation, an additional $.76 in labour income is

created in the Manitoba economy. Figure 1.8 shows the components of labour income since

2003.

Figure 1.8: Trend in Labour Income by Leverage Component from Transportation

in Manitoba

($ Billion)

$1 Direct Labour Income in 2007 = $1.76 Total Labour Income

Leverage Factor = .76

0.95 0.98 1.06 1.03 1.04

0.37 0.390.41 0.4 0.41

0.360.37

0.4 0.39 0.39

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

2003 2004 2005 2006 2007

Induced Indirect Direct

1.83

1.681.74

1.861.82

9

Amongst the modes, trucking is the largest transportation sector in Manitoba, contributing

about $1.3 billion to GDP in 2007, as shown in Figure 1.9. This is followed by rail at $0.97 billion

and aviation, which generates $0.54 billion.

Figure 1.9: Total Contribution to Manitoba GDP by Transportation Mode: 2007

($3.23 Billion)

Trucking, $1.29

Rail, $0.97

Bus, $0.20

Aviation, $0.54

Couriers, $0.22

10

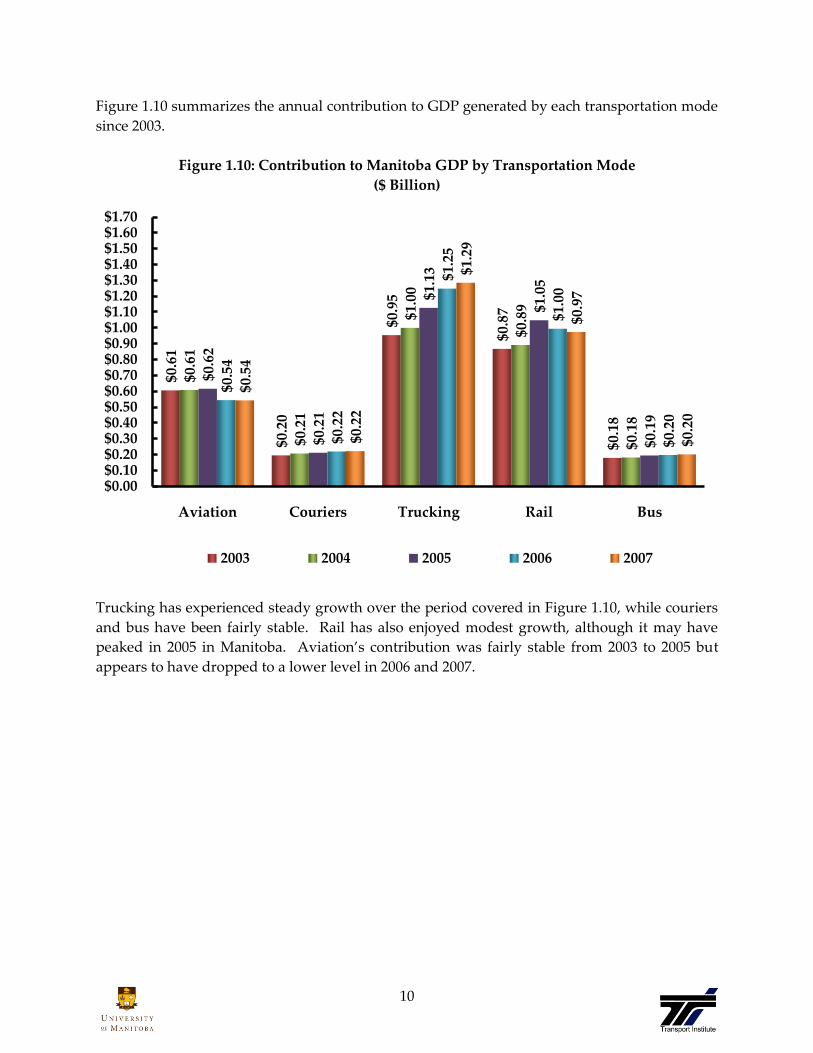

Figure 1.10 summarizes the annual contribution to GDP generated by each transportation mode

since 2003.

Figure 1.10: Contribution to Manitoba GDP by Transportation Mode

($ Billion)

Trucking has experienced steady growth over the period covered in Figure 1.10, while couriers

and bus have been fairly stable. Rail has also enjoyed modest growth, although it may have

peaked in 2005 in Manitoba. Aviation’s contribution was fairly stable from 2003 to 2005 but

appears to have dropped to a lower level in 2006 and 2007.

$0.6

1

$0.2

0

$0.9

5

$0.8

7

$0.1

8

$0.6

1

$0.2

1

$1.0

0

$0.8

9

$0.1

8

$0.6

2

$0.2

1

$1.1

3

$1.0

5

$0.1

9

$0.5

4

$0.2

2

$1.2

5

$1.0

0

$0.2

0

$0.5

4

$0.2

2

$1.2

9

$0.9

7

$0.2

0

$0.00$0.10$0.20$0.30$0.40$0.50$0.60$0.70$0.80$0.90$1.00$1.10$1.20$1.30$1.40$1.50$1.60$1.70

Aviation Couriers Trucking Rail Bus

2003 2004 2005 2006 2007

11

Figure 1.11 shows the comparative leverage of each of the modes in terms of contribution to

GDP. Per dollar of GDP generated directly, bus generates the highest level of leverage

throughout the economy at 1.69, followed by aviation at 1.52. Couriers and trucking had lower

leverage effects, at 1.09 and 1.04, respectively. Rail’s leverage for GDP was the lowest of the 5

modes, at 0.56.

Figure 1.11: Leverage Ratios for Manitoba Total GDP by Transportation Mode

1.69

1.52

1.091.04

0.56

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Bus Aviation Couriers Trucking Rail

12

As presented in Figure 1.12 total employment created by the trucking sector is greater than that

created by all the other sectors combined.

Figure 1.12: Contribution to Manitoba Total Employment by Transportation Mode: 2007

Total: 50,745 FTEs

Trucking, 28,280

Rail, 7,275

Bus, 4,860

Aviation, 6,575

Couriers, 3,755

13

Total employment generated by each of the modes from 2003 to 2007 are presented in Figure

1.13. Employment related to trucking had increased from 20,920 to 28,280, an increase of 7,360

FTEs. Aviation-generated employment declined from 9,075 to 6,575, or a loss of 2,500 FTEs.

Rail declined from 8,100 to 7,275. Employment associated with the Bus sector rose slightly from

its 2003 level to a recent high of 5,405, after which it fell to 4,860 FTEs by 2007. Courier sector-

related employment decreased from 4,230 in 2003 to 3,755 in 2004 and has remained fairly stable

since 2004-2007.

Figure 1.13: Total Employment by Transportation Mode

(FTEs)

9,07

5

4,23

0

20,9

20

8,10

0

5,06

58,51

0

3,75

5

23,4

95

7,94

0

5,40

5

7,16

0

3,76

0

27,6

75

8,42

5

5,17

5

6,68

0

3,72

5

27,8

95

7,50

0

4,99

5

6,57

5

3,75

5

28,2

80

7,27

5

4,86

0

0

5,000

10,000

15,000

20,000

25,000

30,000

Aviation Couriers Trucking Rail Bus

2003 2004 2005 2006 2007

14

With respect to leverage in creating jobs throughout the economy, each aviation direct job

generates an additional 1.5 jobs (Figure 1.14). This is followed by trucking at 0.92 FTEs, rail at

.86, bus at .81, and finally courier at .62 FTEs generated for each direct FTE.

Figure 1.14: Leverage Ratios for Manitoba Employment by Transportation Mode

1.49

0.920.86

0.81

0.62

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Aviation Trucking Rail Bus Couriers

15

Considering labour income, trucking is also the largest modal contributor to the economy. As

shown in Figure 1.15, the trucking industry overall produced $.86 billion in labour income in

2007. This was followed by rail at $.45 billion, aviation at $.26 billion, bus at $151 million and

couriers at $112 million.

Figure 1.15: Contribution to Manitoba Total Labour Income by Transportation Mode: 2007

$1.83 Billion

Trucking, $0.86

Rail, $0.45

Bus, $0.15

Aviation, $0.26

Couriers, $0.11

16

Labour income generated by each of the transportation sectors from 2003 to 2007 is presented in

Figure 1.16. Labour income generated from trucking increased from $.58 billion to $.86 billion.

Aviation decreased from $.41 billion to $.26 billion. Rail started at $.46 billion, peaked in 2005,

and dropped back to $.45 billion in 2007. Labour income associated with couriers was

essentially stable, while employment associated with the bus sector rose fractionally.

Figure 1.16: Total Labour Income by Transportation Mode

($ Billion)

$0.4

1

$0.1

0

$0.5

8

$0.4

6

$0.1

3

$0.3

7

$0.1

1

$0.6

7

$0.4

5

$0.1

4

$0.3

0

$0.1

1

$0.7

9

$0.5

2

$0.1

4

$0.2

6

$0.1

1

$0.8

4

$0.4

7

$0.1

5

$0.2

6

$0.1

1

$0.8

6

$0.4

5

$0.1

5

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

Aviation Couriers Trucking Rail Bus

2003 2004 2005 2006 2007

17

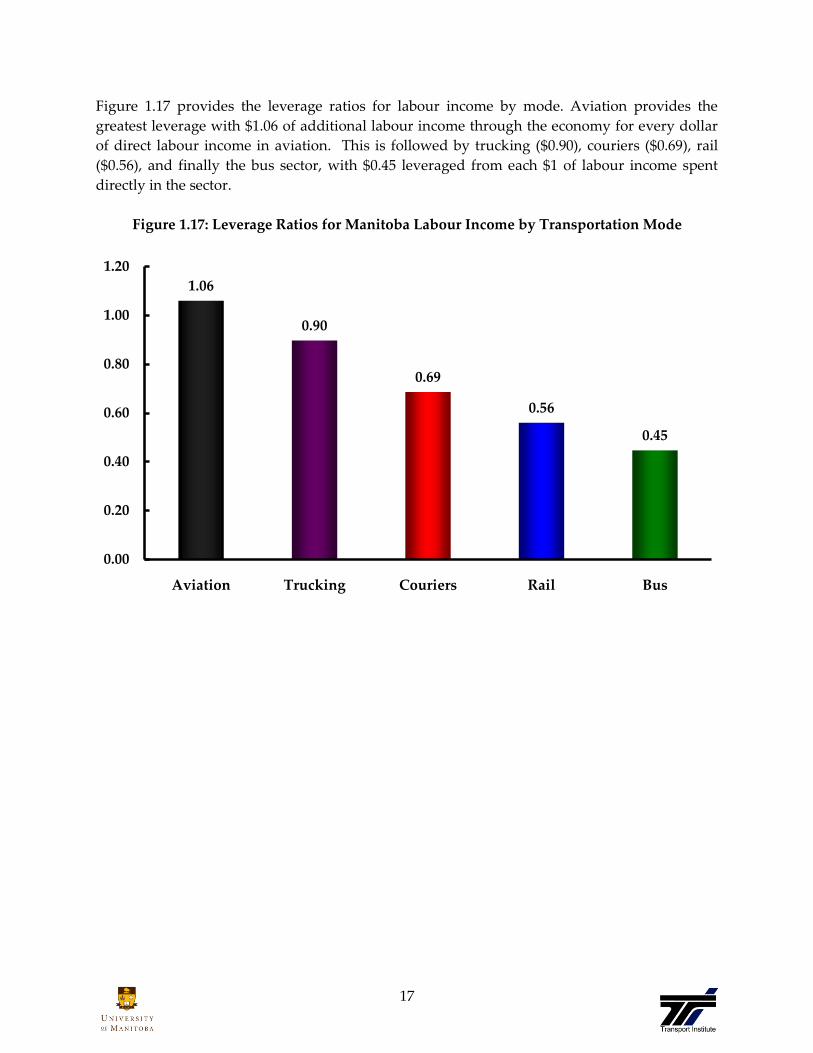

Figure 1.17 provides the leverage ratios for labour income by mode. Aviation provides the

greatest leverage with $1.06 of additional labour income through the economy for every dollar

of direct labour income in aviation. This is followed by trucking ($0.90), couriers ($0.69), rail

($0.56), and finally the bus sector, with $0.45 leveraged from each $1 of labour income spent

directly in the sector.

Figure 1.17: Leverage Ratios for Manitoba Labour Income by Transportation Mode

1.06

0.90

0.69

0.56

0.45

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Aviation Trucking Couriers Rail Bus

18

2. Transportation and Warehousing and the Regional Canadian Economy

Canada comprises the second largest national land mass on the globe, with likely the lowest

population density among industrialized nations. This, coupled with our dependence on

international trade, incorporates a significant spatial element to virtually all aspects of our

economy.

Figure 2.1 shows per capita gross domestic product8 from Transportation and Warehousing in

western Canada versus eastern Canada. GDP related to transportation has increased steadily

from 2003 to 2007 in both eastern and western Canada. Transportation and Warehousing on a

per capita basis is much higher in western Canada however, maintaining a value of $2,444 in

2007 compared to $1,391 in eastern Canada.

Figure 2.1: Per Capita Direct GDP from Transportation and Warehousing by Region9

Figure 2.2 displays the importance of transportation and warehousing in western Canada

relative to eastern Canada. The ratio of gross domestic product per capita from Transportation

8 Gross domestic product (GDP) figures are in 2002 dollars. Previous versions of the MTR used 1997

dollars for determining GDP figures, however these tables from Statistics Canada are no longer in

circulation, as such, some figures in this section may not be comparable to previous versions of the MTR

report. 9 Western Canada includes Manitoba, Saskatchewan, Alberta, British Columbia, Yukon Territory,

Northwest Territories and Nunavut.

$1,584$1,628

$1,674 $1,704 $1,715

$2,162$2,219

$2,327$2,411 $2,444

$1,334 $1,372 $1,389 $1,393 $1,391

$1,000

$1,400

$1,800

$2,200

$2,600

2003 2004 2005 2006 2007

Canada Western Canada Eastern Canada

19

and Warehousing grew steadily from 2003 to 2007. From 2006 to 2007, only a minimal increase

in the ratio of GDP was experienced. The ratio of GDP per capita from Transportation and

Warehousing has grown by 8% from 2003 to 2007. This rate of increase is an indicator that

Transportation and Warehousing is ever increasingly important in western Canada relative to

eastern Canada.

Figure 2.2: Ratio of Per Capita Contribution from Transportation and Warehousing to Direct

GDP: Western Canada Compared to Eastern Canada

162.1% 161.7%

167.6%

173.1%

175.7%

150%

155%

160%

165%

170%

175%

180%

2003 2004 2005 2006 2007

20

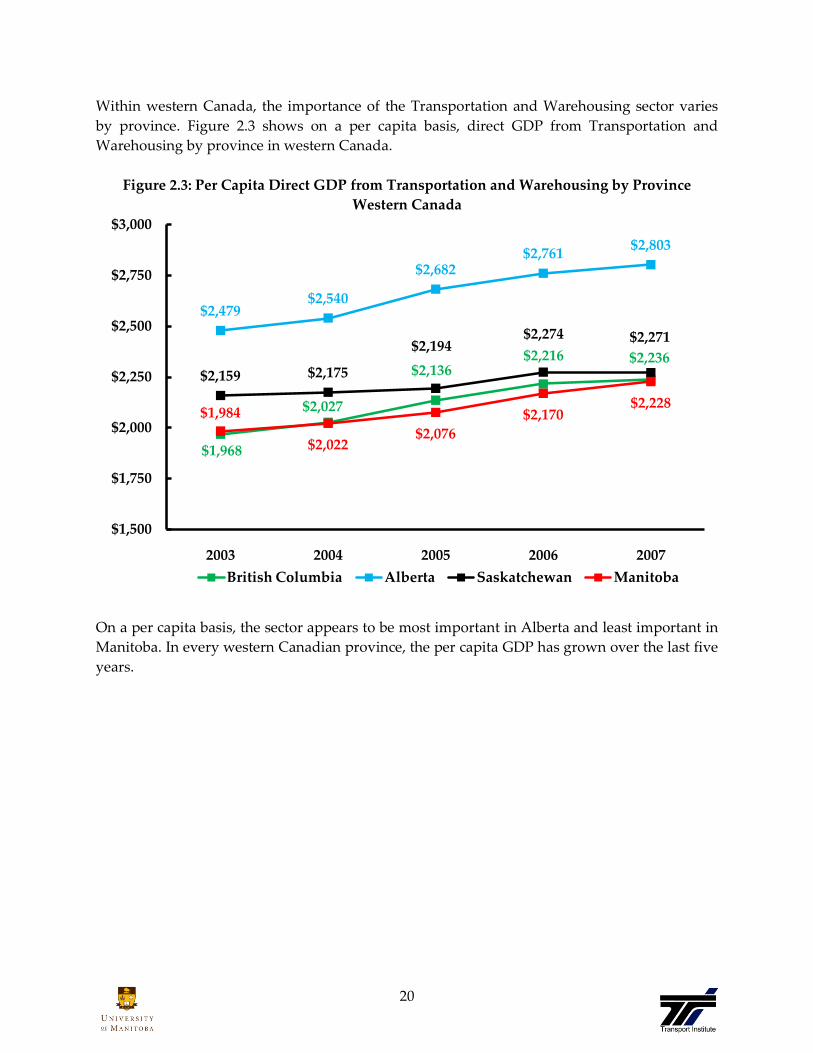

Within western Canada, the importance of the Transportation and Warehousing sector varies

by province. Figure 2.3 shows on a per capita basis, direct GDP from Transportation and

Warehousing by province in western Canada.

Figure 2.3: Per Capita Direct GDP from Transportation and Warehousing by Province

Western Canada

On a per capita basis, the sector appears to be most important in Alberta and least important in

Manitoba. In every western Canadian province, the per capita GDP has grown over the last five

years.

$1,968

$2,027

$2,136$2,216 $2,236

$2,479$2,540

$2,682$2,761

$2,803

$2,159 $2,175

$2,194$2,274 $2,271

$1,984

$2,022$2,076

$2,170$2,228

$1,500

$1,750

$2,000

$2,250

$2,500

$2,750

$3,000

2003 2004 2005 2006 2007

British Columbia Alberta Saskatchewan Manitoba

21

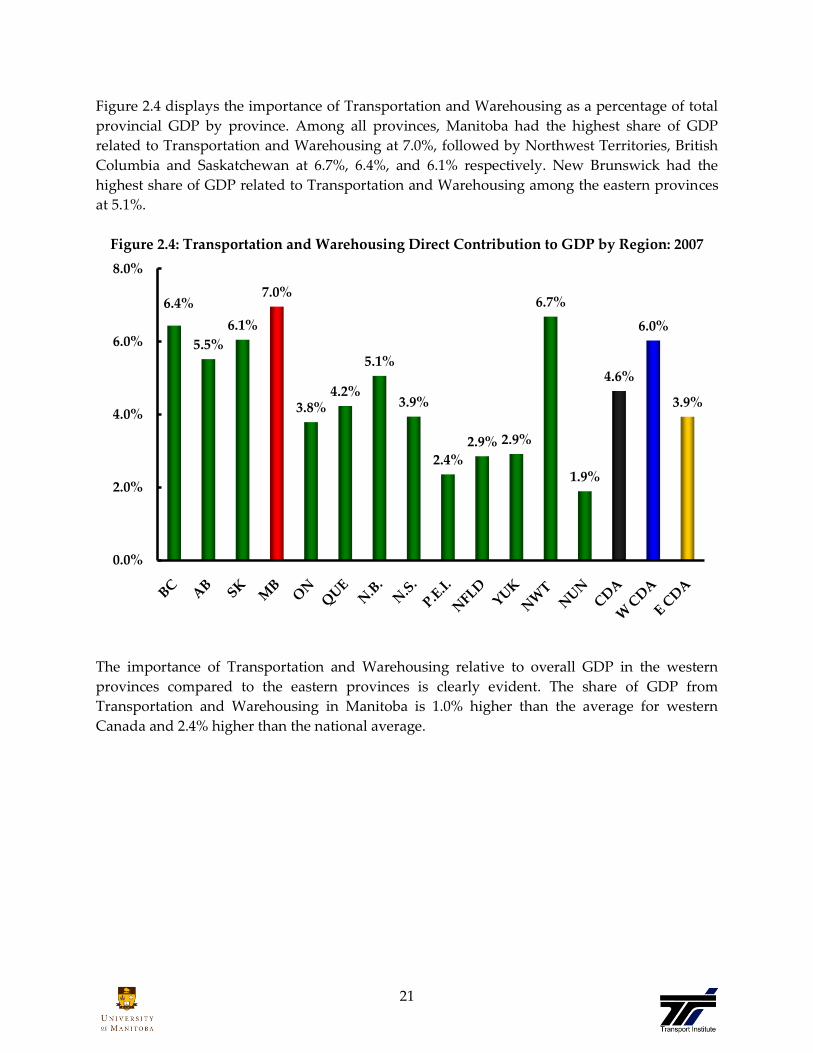

Figure 2.4 displays the importance of Transportation and Warehousing as a percentage of total

provincial GDP by province. Among all provinces, Manitoba had the highest share of GDP

related to Transportation and Warehousing at 7.0%, followed by Northwest Territories, British

Columbia and Saskatchewan at 6.7%, 6.4%, and 6.1% respectively. New Brunswick had the

highest share of GDP related to Transportation and Warehousing among the eastern provinces

at 5.1%.

Figure 2.4: Transportation and Warehousing Direct Contribution to GDP by Region: 2007

The importance of Transportation and Warehousing relative to overall GDP in the western

provinces compared to the eastern provinces is clearly evident. The share of GDP from

Transportation and Warehousing in Manitoba is 1.0% higher than the average for western

Canada and 2.4% higher than the national average.

6.4%

5.5%

6.1%

7.0%

3.8%4.2%

5.1%

3.9%

2.4%

2.9% 2.9%

6.7%

1.9%

4.6%

6.0%

3.9%

0.0%

2.0%

4.0%

6.0%

8.0%

22

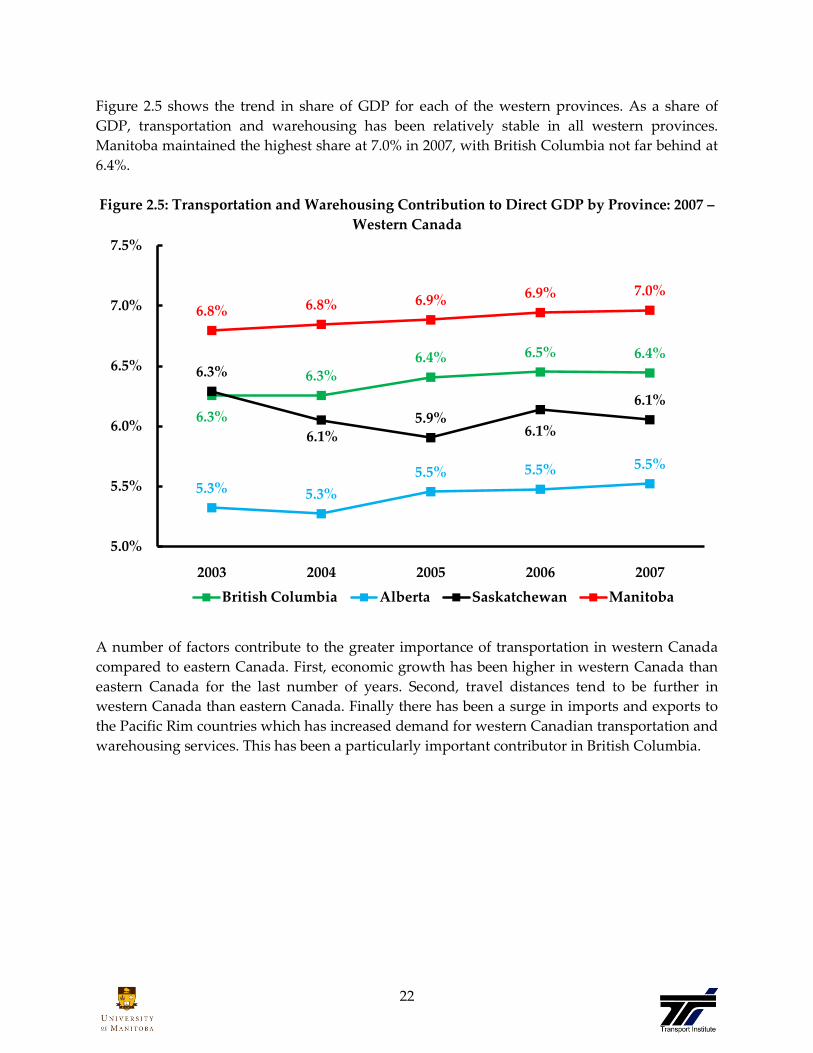

Figure 2.5 shows the trend in share of GDP for each of the western provinces. As a share of

GDP, transportation and warehousing has been relatively stable in all western provinces.

Manitoba maintained the highest share at 7.0% in 2007, with British Columbia not far behind at

6.4%.

Figure 2.5: Transportation and Warehousing Contribution to Direct GDP by Province: 2007 –

Western Canada

A number of factors contribute to the greater importance of transportation in western Canada

compared to eastern Canada. First, economic growth has been higher in western Canada than

eastern Canada for the last number of years. Second, travel distances tend to be further in

western Canada than eastern Canada. Finally there has been a surge in imports and exports to

the Pacific Rim countries which has increased demand for western Canadian transportation and

warehousing services. This has been a particularly important contributor in British Columbia.

6.3%

6.3%6.4% 6.5% 6.4%

5.3% 5.3%

5.5% 5.5% 5.5%

6.3%

6.1%5.9%

6.1%

6.1%

6.8% 6.8% 6.9% 6.9% 7.0%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

2003 2004 2005 2006 2007

British Columbia Alberta Saskatchewan Manitoba

23

Figure 2.6 displays employment in Transportation and Warehousing per thousand population.

Figure 2.6: Direct Employment in Transportation and Warehousing per 1,000 Population by

Region

In western Canada, employment in Transportation and Warehousing has consistently been 22

employees per 1000 persons from 2003 to 2007. In eastern Canada, employment has also been

consistent, averaging 18 employees per 1000 persons from 2003-2007.

19.3 19.4 19.5 19.6 19.8

22.5 22.4 22.322.7 22.9

18.0 18.1 18.2 18.3 18.4

15

17

19

21

23

25

2003 2004 2005 2006 2007

Canada Western Canada Eastern Canada

24

Figure 2.7 shows the ratio of per capita Transportation and Warehousing employment for

western Canada compared to eastern Canada. The ratio of Transportation and Warehousing

employment per capita has remained relatively stable from 2003 to 2007, declining slightly, then

increasing back to previous levels. The ratio of 124.4% in 2007 is only 0.4% lower than the 2003

ratio of 124.8%.

Figure 2.7: Ratio of Per Capita Direct Transportation and Warehousing Employment: Western

Canada Compared to Eastern Canada

124.8%124.0%

122.8%

124.2% 124.4%

110%

115%

120%

125%

130%

2003 2004 2005 2006 2007

25

Figure 2.8 displays direct employment in Transportation and Warehousing per thousand

persons in western Canada.

Transportation and Warehousing employment per thousand persons is highest in Manitoba at

24.3, closely followed by Alberta at 24.2. Manitoba’s Transportation and Warehousing

employment experienced a small drop from 2003 to 2005, and has since recovered slightly,

however this has allowed Alberta to close the gap. British Columbia’s Transportation and

Warehousing employment per thousand persons averaged 21.5 from 2003 to 2007, while

Saskatchewan averaged 19.8.

Figure 2.8: Direct Employment in Transportation and Warehousing per 1,000 Population by

Province: Western Canada

21.5 21.4 21.321.8 21.7

23.0 23.2 23.6 23.724.2

20.1 19.919.4 19.7 19.9

25.525.1

23.8 24.2 24.3

15

20

25

30

2003 2004 2005 2006 2007

British Columbia Alberta Saskatchewan Manitoba

26

Figure 2.9 shows the share of total employment from Transportation and Warehousing for each

region. Among all provinces, the share of jobs related to Transportation and Warehousing was

most important in Manitoba10 at 5.5% followed by New Brunswick at 5.4%. The share of jobs

related to Transportation and Warehousing was more important in western Canada which had

a value of 5.1% compared to 4.4% for eastern Canada and 4.6% nationally.

Figure 2.9: Transportation and Warehousing Contribution to Direct Employment by

Region: 2007

10 While the ratio is higher in both the Northwest Territories and the Yukon, the size of the population

and number of jobs are small.

5.1%

5.0%

4.8% 5.

5%

4.3% 4.5%

5.4%

4.5%

3.3%

4.8%

5.8%

10.5

%

5.2%

4.6% 5.

1%

4.4%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

27

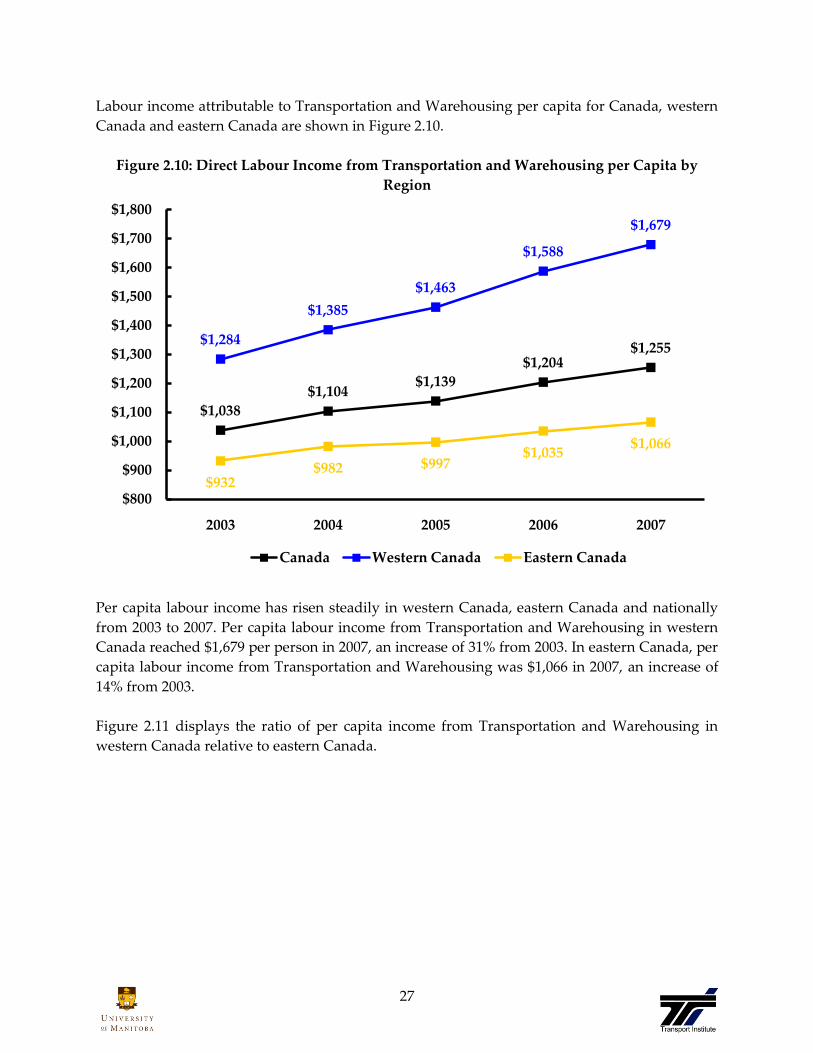

Labour income attributable to Transportation and Warehousing per capita for Canada, western

Canada and eastern Canada are shown in Figure 2.10.

Figure 2.10: Direct Labour Income from Transportation and Warehousing per Capita by

Region

Per capita labour income has risen steadily in western Canada, eastern Canada and nationally

from 2003 to 2007. Per capita labour income from Transportation and Warehousing in western

Canada reached $1,679 per person in 2007, an increase of 31% from 2003. In eastern Canada, per

capita labour income from Transportation and Warehousing was $1,066 in 2007, an increase of

14% from 2003.

Figure 2.11 displays the ratio of per capita income from Transportation and Warehousing in

western Canada relative to eastern Canada.

$1,038

$1,104$1,139

$1,204$1,255

$1,284

$1,385

$1,463

$1,588

$1,679

$932$982 $997

$1,035$1,066

$800

$900

$1,000

$1,100

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

$1,800

2003 2004 2005 2006 2007

Canada Western Canada Eastern Canada

28

Figure 2.11: Ratio of Direct Per Capita Income Contribution from Transportation and

Warehousing to GDP: Western Canada Compared to Eastern Canada

The ratio has risen steadily from 2003 to 2007 averaging annual growth of approximately 4.9%.

From 2003 to 2007, the ratio has increased by almost 20%. This indicates that in relative terms,

the Transportation and Warehousing industry is becoming an increasingly more important

sector in western Canada than eastern Canada.

137.8%

141.1%

146.8%

153.4%

157.5%

125%

130%

135%

140%

145%

150%

155%

160%

2003 2004 2005 2006 2007

29

Labour income per capita has grown in all western provinces over the past five years as shown

in Figure 2.12. During the previous five years (2003-2007), the per capita direct labour incomes

of each of the western Canadian provinces experienced annual increases. In 2007, Alberta

experienced the highest growth levels among western provinces as labour income per capita

from Transportation and Warehousing reached $2,053 in 2007, an increase of 51% from 2003.

Figure 2.12: Direct Labour Income from Transportation and Warehousing per Capita by

Province: Western Canada

$1,294

$1,364$1,388

$1,484$1,549

$1,361

$1,542

$1,712

$1,908

$2,053

$991 $1,018$1,080

$1,125$1,192$1,258

$1,308 $1,330$1,393

$1,436

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

2003 2004 2005 2006 2007

British Columbia Alberta Saskatchewan Manitoba

30

Figure 2.13 displays the share of labour income generated by Transportation and Warehousing

for each province and territory.

Figure 2.13: Transportation and Warehousing Direct Contribution to Labour Income by

Region: 2007

At 7.1%, Transportation and Warehousing’s share of labour income was highest in Manitoba

and Northwest Territories, followed by British Columbia at 6.7%. Nationally, 5.3% of labour

income was the result of Transportation and Warehousing. In western Canada the share was

6.4%, while in eastern Canada it was 4.7%.

6.7%

6.1% 5.9%

7.1%

4.5%

5.1% 5.3%

4.7%

2.9%

5.0%

4.4%

7.1%

3.5%

5.3%

6.4%

4.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

31

In 2007, Transportation and Warehousing was the fourth most important sector of the Manitoba

economy, contributing $2.7 billion to the provincial GDP11(worth approximately $38.3 billion).

Transportation and Warehousing only trailed the finance and insurance, manufacturing, and

health care and social assistance sectors in terms of direct GDP contribution to the Manitoba

economy. Transportation and Warehousing moved ahead of Public Administration into fourth

place in terms of contribution to GDP, a move up from its fifth place ranking in 2006.

Transportation is a derived demand and as such has a direct relationship with key sectors

(shown by the blue bars in Figure 2.14) such as manufacturing, retail trade, and construction.

When these sectors are included with Transportation and Warehousing, the GDP totals almost

$18 billion.

Figure 2.14: Direct GDP of Sectors of the Manitoba Economy: 2007

11 The GDP measured by Statistics Canada in this section is the direct contribution of Transportation and

Warehousing and directly related sectors. It excludes indirect and induced effects discussed in Section

1.

$7.0

$5.0

$3.1 $2.7 $2.6 $2.6$2.3 $2.0 $1.9 $1.7 $1.6

$1.2 $1.1 $1.0 $0.8 $0.7 $0.7 $0.4

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$ B

illi

on

s

32

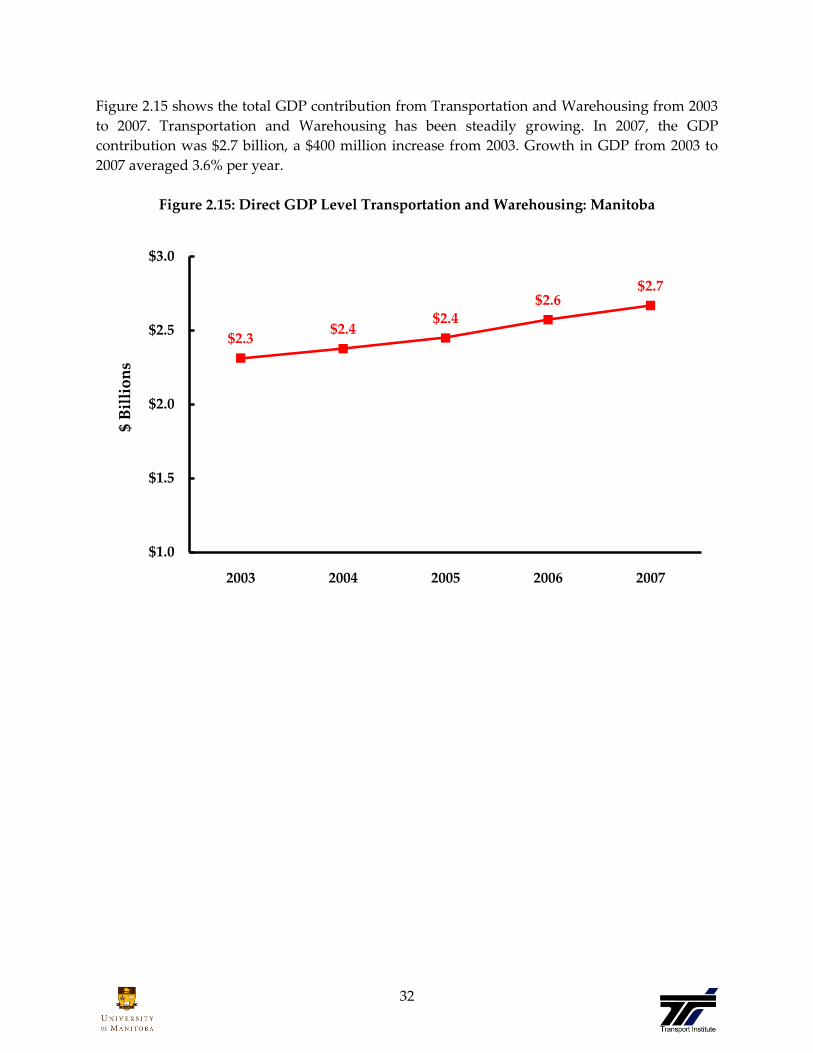

Figure 2.15 shows the total GDP contribution from Transportation and Warehousing from 2003

to 2007. Transportation and Warehousing has been steadily growing. In 2007, the GDP

contribution was $2.7 billion, a $400 million increase from 2003. Growth in GDP from 2003 to

2007 averaged 3.6% per year.

Figure 2.15: Direct GDP Level Transportation and Warehousing: Manitoba

$2.3$2.4

$2.4$2.6

$2.7

$1.0

$1.5

$2.0

$2.5

$3.0

2003 2004 2005 2006 2007

$ B

illi

on

s

33

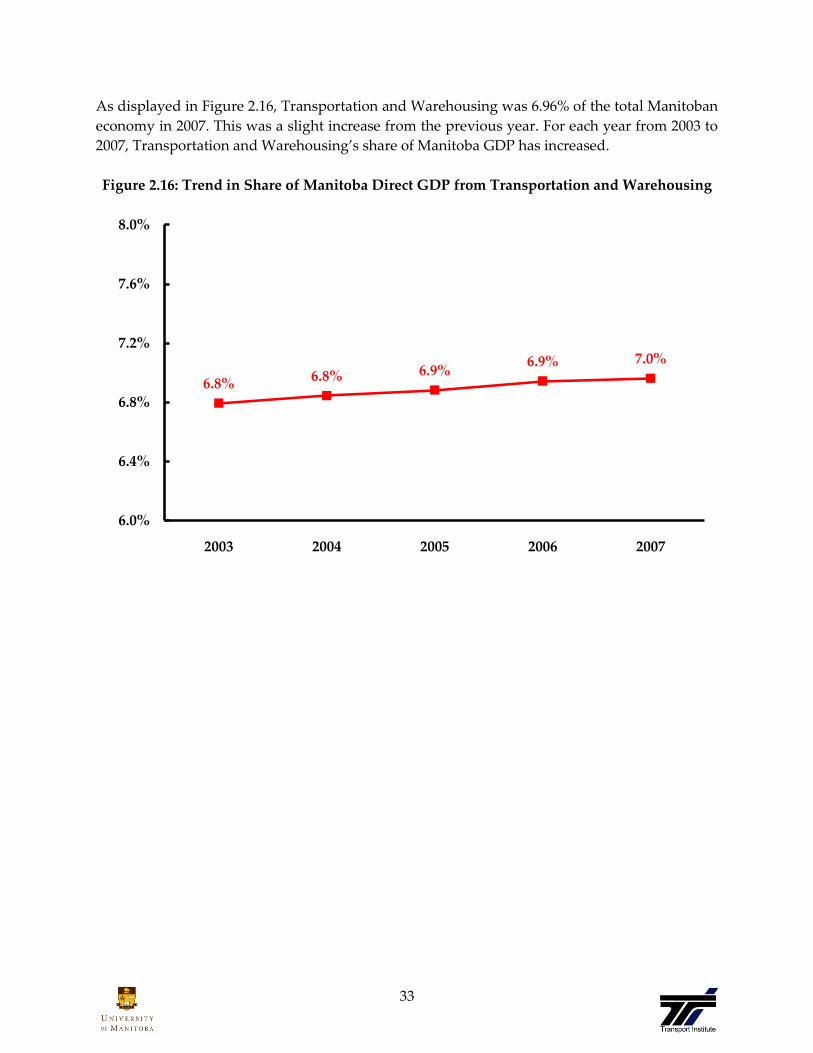

As displayed in Figure 2.16, Transportation and Warehousing was 6.96% of the total Manitoban

economy in 2007. This was a slight increase from the previous year. For each year from 2003 to

2007, Transportation and Warehousing’s share of Manitoba GDP has increased.

Figure 2.16: Trend in Share of Manitoba Direct GDP from Transportation and Warehousing

6.8%6.8% 6.9%

6.9% 7.0%

6.0%

6.4%

6.8%

7.2%

7.6%

8.0%

2003 2004 2005 2006 2007

34

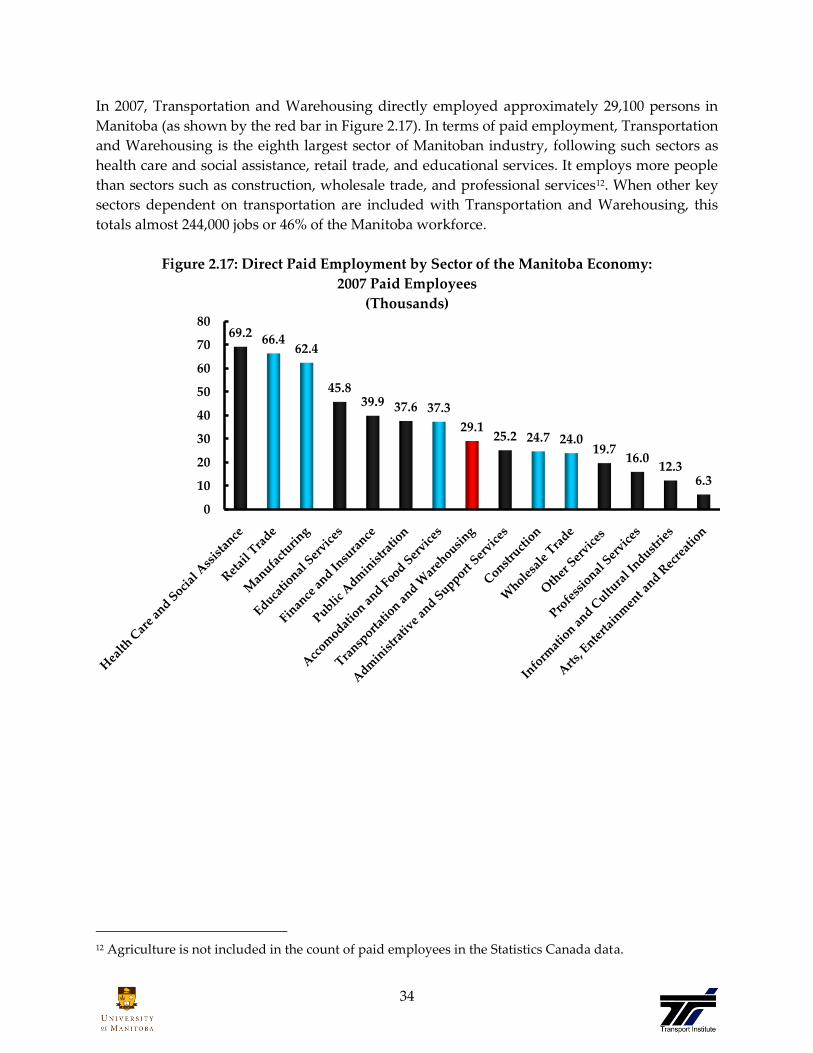

In 2007, Transportation and Warehousing directly employed approximately 29,100 persons in

Manitoba (as shown by the red bar in Figure 2.17). In terms of paid employment, Transportation

and Warehousing is the eighth largest sector of Manitoban industry, following such sectors as

health care and social assistance, retail trade, and educational services. It employs more people

than sectors such as construction, wholesale trade, and professional services12. When other key

sectors dependent on transportation are included with Transportation and Warehousing, this

totals almost 244,000 jobs or 46% of the Manitoba workforce.

Figure 2.17: Direct Paid Employment by Sector of the Manitoba Economy:

2007 Paid Employees

(Thousands)

12 Agriculture is not included in the count of paid employees in the Statistics Canada data.

69.2 66.462.4

45.839.9 37.6 37.3

29.125.2 24.7 24.0

19.716.0

12.36.3

0

10

20

30

40

50

60

70

80

35

Figure 2.18 displays the annual paid employment of Transportation and Warehousing workers

in Manitoba.

Figure 2.18: Trend in Transportation and Warehousing’s Direct Total Employment

Paid Employees

(Thousands)

Employment in the Transportation and Warehousing sector experienced a sizeable decrease

from 2003 to 2005 of approximately 1,800 paid employees. This figure has slightly recovered in

recent years, with employment reaching 29,100 in 2007.

29.8

29.5

28.0

28.6

29.1

27

27.5

28

28.5

29

29.5

30

30.5

31

2003 2004 2005 2006 2007

000

Pai

d E

mp

loy

ees

36

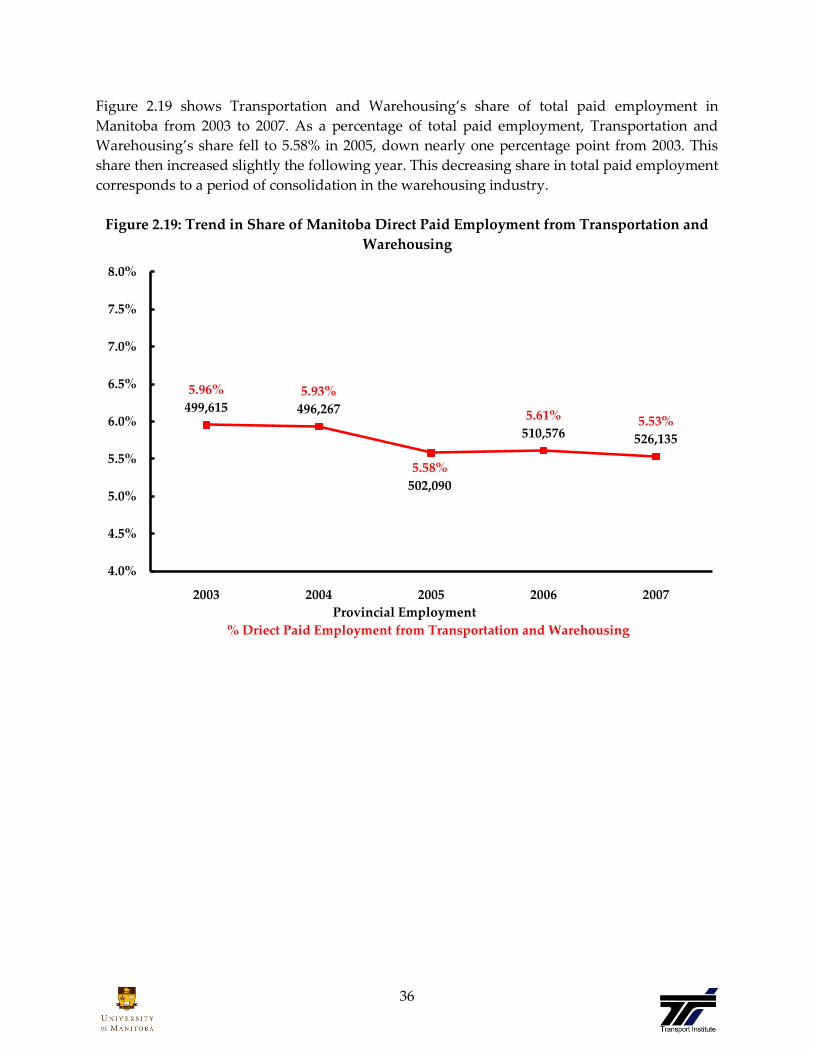

Figure 2.19 shows Transportation and Warehousing’s share of total paid employment in

Manitoba from 2003 to 2007. As a percentage of total paid employment, Transportation and

Warehousing’s share fell to 5.58% in 2005, down nearly one percentage point from 2003. This

share then increased slightly the following year. This decreasing share in total paid employment

corresponds to a period of consolidation in the warehousing industry.

Figure 2.19: Trend in Share of Manitoba Direct Paid Employment from Transportation and

Warehousing

5.96%

499,6155.93%

496,267

5.58%

502,090

5.61%

510,5765.53%

526,135

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

2003 2004 2005 2006 2007

Provincial Employment

% Driect Paid Employment from Transportation and Warehousing

37

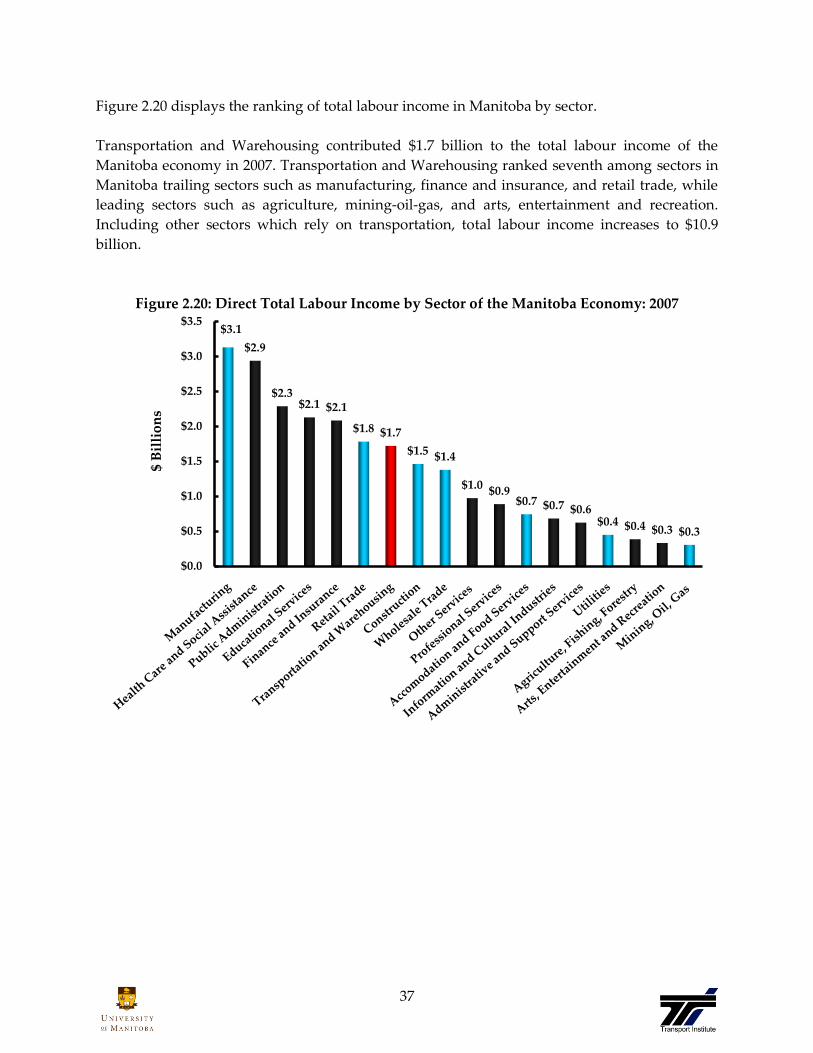

Figure 2.20 displays the ranking of total labour income in Manitoba by sector.

Transportation and Warehousing contributed $1.7 billion to the total labour income of the

Manitoba economy in 2007. Transportation and Warehousing ranked seventh among sectors in

Manitoba trailing sectors such as manufacturing, finance and insurance, and retail trade, while

leading sectors such as agriculture, mining-oil-gas, and arts, entertainment and recreation.

Including other sectors which rely on transportation, total labour income increases to $10.9

billion.

Figure 2.20: Direct Total Labour Income by Sector of the Manitoba Economy: 2007

$3.1

$2.9

$2.3$2.1 $2.1

$1.8 $1.7

$1.5 $1.4

$1.0 $0.9$0.7 $0.7 $0.6

$0.4 $0.4 $0.3 $0.3

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$ B

illi

on

s

38

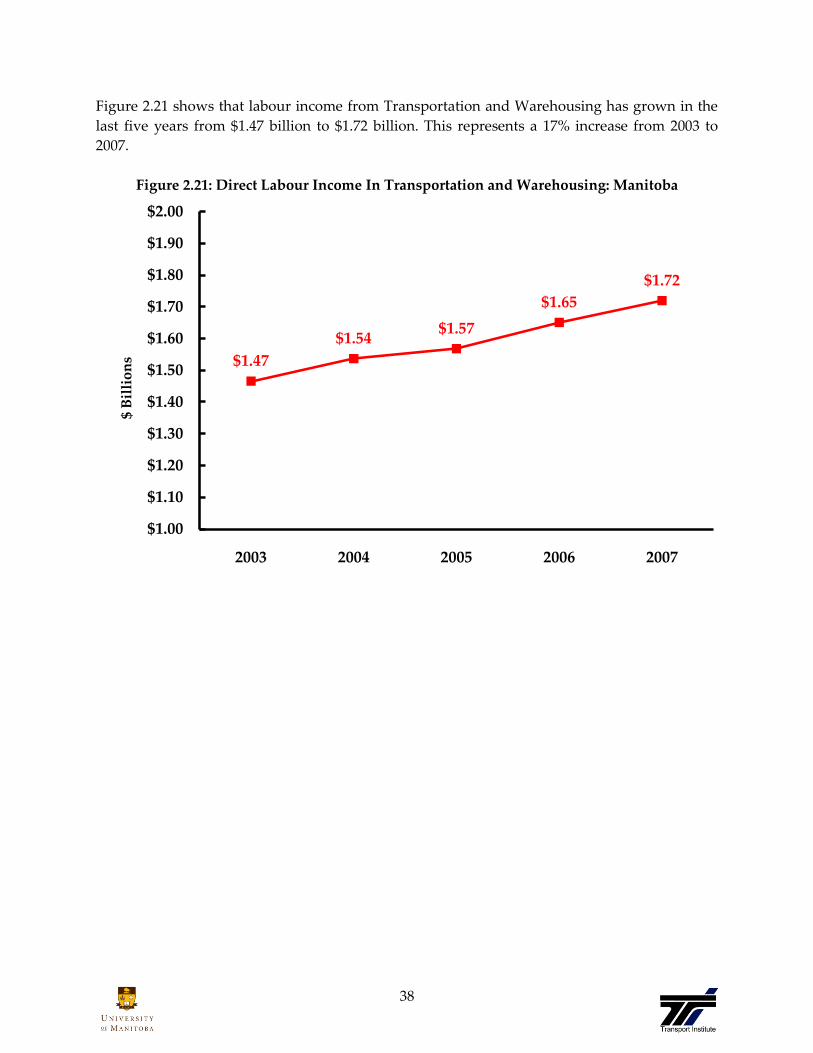

Figure 2.21 shows that labour income from Transportation and Warehousing has grown in the

last five years from $1.47 billion to $1.72 billion. This represents a 17% increase from 2003 to

2007.

Figure 2.21: Direct Labour Income In Transportation and Warehousing: Manitoba

$1.47

$1.54$1.57

$1.65

$1.72

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50

$1.60

$1.70

$1.80

$1.90

$2.00

2003 2004 2005 2006 2007

$ B

illi

on

s

39

In spite of the growth shown in Figure 2.21, as a share of total labour income in Manitoba,

Transportation and Warehousing has declined from 7.55% in 2003 to 7.09% in 2007 as shown in

Figure 2.22.

Figure 2.22: Trend in Share of Manitoba Labour Income from Transportation and

Warehousing

This decline reflects the fact that although wages have increased for the Transportation and

Warehousing sector, wages from all other industries have collectively increased by a larger

amount.

7.55% 7.50%7.34% 7.30%

7.09%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2003 2004 2005 2006 2007

40

3. The State of the Macro Economy

The macroeconomic perspective presents the performance, structure and behavior of the

national or the regional economies as a whole. This review of the macro economy will cover the

global, the Canadian and the Manitoba economies.

Most of the recent data and reports indicate that the global economy is in a severe global

economic downturn. In January of 2009, the World Economic Situation and Prospects 2009

prepared by the United Nations suggested that ‚the world economy is mired in the worst

financial crisis since the Great Depression. What first appeared as a sub-prime mortgage crack

in the United States housing market during the summer of 2007 began widening during 2008

into deeper fissures across the global financial landscape and ended with the collapse of major

banking institutions, precipitous falls on stock markets across the world and a credit freeze.‛13

It most likely began with the developed economies and then spread to the developing

economies which as mentioned in the UN report, ‚developing economies would be hurt more

through a deeper recession in the developed economies, a steeper fall in commodity prices and

a sharper reversal of capital inflows.‛14

The Global Growth Slowdown

For the past four years the average annual global real GDP growth was greater than 4.5 percent,

but recent data has shown that global growth has slowed in the major industrial countries with

the United States economy in an outright ‚recession‛. The slowdown in global growth kicked

in by the summer of 2007 and continued through the second half of 2008. Any recovery during

2009 will only be gradual.15 According to the United Nations baseline forecast, World Gross

Product (WGP) is expected to slow to 1.0 per cent rate of growth in 2009, a sharp deceleration

from the 2.5 per cent growth estimated for 2008 and well below the more robust growth of

previous years. The baseline forecast assumes that it will take six to nine months for financial

markets in developed countries to return to normalcy, assuming central banks in the United

States, Europe, and Japan provide further monetary stimulus from the end of 2008 and on into

2009.16

13 United Nations. World Economic Situation and Prospects 2009 - Global Outlook 2009. New York:

United Nations, 2009. 14 Ibid 15 Peterson Institute for International Economics. Global Economic Prospects 2008/2009: Hoping for a

Global Slowdown and a US Rescission, (April 2008). 16 United Nations. World Economic Situation and Prospects 2009 - Global Outlook 2009. New York:

United Nations, 2009.

41

Is the United States in Recession?

Based on the definition of recession, the United States is not in a ‚classical recession‛. A

recession has been traditionally defined as two consecutive quarters of economic contraction.

However, the definition by U.S National Bureau of Economic Research (NBER) is broader. It

defines a recession as ‚a significant decline in economic activity spread across the economy,

lasting more than a few months, normally visible in real GDP, real income, employment,

industrial production and wholesale-retail sales.‛ Many economists believe that the United

States is in recession, and the definition should be redefined. However, whether the United

States is in recession or not, the consequences for the global economy have begun. ‚Various

overseas economies are struggling in the global recession, largely due to less demand for their

products in the U.S. and other western nations. Reuters has reported that factory production in

China, Russia, and India has fallen dramatically in recent months. Factories in India are also

said to be cutting jobs, while Russia’s manufacturing drop is worse than it experienced during

the 1998 financial crisis. Also, South Korea is expecting its weakest growth since the beginning

of the decade, while Singapore’s economy could shrink up to two percent in 2009‛.17

‚Yet with the official announcement on December 1st 2008 that America had entered recession

last December, the traditional explanation for recessions is wearing awfully thin. Though it may

end up as one of the longest recessions, if not the longest, of the post-war era, the current

episode still seems to have more in common with the mild downturns of 1990-91 and 2001 than

the more wrenching affairs that came before. Although the recession has not yet been much

deeper than its predecessors, it almost certainly will be by the time it is over. Many economists

expect the recession to continue until mid-2009, which would be longer than those of 1973-75

and 1981-82. Moreover, employment is likely to keep falling after the official end of the

recession.‛18

According to the UN report, World Economic Situation and Prospects 2009, the ‚most developed

economies entered into recession during the second half of 2008, and the economic slowdown

has spread to developing countries and the economies in transition. In a more pessimistic

scenario, both the fire sale of financial assets and the credit crunch would last longer, while

monetary stimulus would prove ineffective in the short run and fiscal stimulus would turn out

to be too little, too late. This would then lead to worldwide recession in 2009, with global output

falling by 0.4 per cent, and postpone recovery to, at best, the following year. In a more

optimistic scenario, a large-scale fiscal stimulus coordinated among major economies would

stave off the worst of the crisis, yet, for the reasons indicated, it would not prevent a significant

slowdown of the global economy in 2009.‛19

17 U.S. recession impacting global economy. <http://www.nasdaq.com/newscontent/20090102/U.S.-

recession-impacting-global-economy.aspx?storyid=18953475> 18 The Economist. A thoroughly modern recession. The current recession fits the pattern of recent ones –

but is likely to last longer. Washington, DC (Dec. 4th 2008).

<http://www.theelectroniceconomist.com/world/unitedstates/displaystory.cfm?story_id=12725124> 19 United Nations. World Economic Situation and Prospects 2009 - Global Outlook 2009. New York:

United Nations, 2009.

42

What Has Caused the Recession?

‚This is another staunchly debated topic, but the general consensus is that it was primarily

caused by the actions taken to control the money supply in the economy. The Federal Reserve

is responsible for maintaining an ideal balance between money supply, interest rates, and

inflation. When the Fed loses balance in this equation, the economy can spiral out of control,

forcing it to correct itself. This is precisely what we have seen in 2007, where the Fed’s

monetary policy of injecting tremendous amounts of money supply into the money market has

kept interest rates lower while inflation continues to rise. This coupled with relaxed policies in

lending practices making it easy to borrow money; the economic activity became unsustainable

resulting in the economy coming to a near halt. It is also said that recession can be caused by

factors that stunt short term growth in the economy, such as spiking oil prices or war.‛20

The Credit Crunch

‚The main message is not to think of the credit problems over the past year as a one-time event,

that once resolved will immediately place the economy back into high growth mode. Relatively

short-lived shocks can have longer lasting effects. The credit problems of today can act as a

financial accelerator whereby a shock is amplified or becomes long lasting by restricting firms

through swings in their balance sheets and spending intentions.‛21

‚The steps to 2007/08 credit crunch:

U.S. mortgage lenders sell many inappropriate mortgages to customers with low income

and poor credit.

There was an incentive to sell mortgages even though they were too expensive and

highly likely to default.

To sell more profitable subprime mortgages, mortgage companies borrowed to be able

to lend mortgages.

These mortgage debts were bought by financial intermediaries. The idea was to spread

the risk, but it actually just spread the problem.

The rating agencies gave these risky subprime mortgages a low risk rating. Therefore,

the financial system denied the extent of risk in their balance sheets.

Many of these mortgages had an introductory period of 1-2 years of very low interest

rates. At the end of this period, interest rates increased.

In 2007, the United States had to increase interest rates because of inflation. This made

mortgage payments, more expensive. Furthermore, many home owners who had taken

out mortgages two years earlier now faced ballooning mortgage payments as their

introductory period ended.

This caused a rise in mortgage defaults, as many new homeowners could not afford

mortgage payments. These defaults also signaled the end of the United States housing

boom.

20 <http://recession.org/definition> 21 TD Economics. TD Quarterly Economic Forecast 2008

43

The number of defaults caused many medium sized United States mortgage companies

to go bankrupt.

The result was that worldwide, it became very difficult to raise funds and borrow

money as the markets ‚dried up‛.

This affected many firms who had been exposed to the subprime lending. It also affected

a wide variety of firms who now have difficulty borrowing money.

The slowdown in borrowing has contributed to a slowing economy with the recession in

the United States.‛22

Decline of the American Dollar

‚The decline in the value of the dollar appears to have had a positive impact. Real imports have

declined and real export growth had accelerated. Moreover, the current account deficit has

begun to improve.‛23 A contrasting option stated that although ‚many think that a declining

currency will fix America’s export problem, they are wrong. The weak currency will not face

the fact that America is consuming far more than Americans produce. It actually could make

the economy much worse. A declining dollar decreases the net-worth of every citizen who

holds it and threatens America’s status as the world’s reserve currency. Once the status as

reserve currency is gone, America will no longer be able to afford the outstanding national and

current account deficits. America’s trade imbalance solution is not a declining dollar.‛24

Fuel Prices

‚The immediate cause of rising oil prices is the weak dollar. Oil-producing countries are

requiring more dollars to purchase the same barrel of oil because the dollar is worth less today

than it was years ago. Rapidly rising oil prices have a number of direct and indirect negative

influences on the U.S. economy. In direct terms, consumers will spend $90 million more on

discretionary spending.‛25

The high oil prices did not just stress American consumers, as reported in North American

Economic Outlook (prepared by MFC Global Investment Management in fall 2008) ‚In contrast,

Canada is a net energy exporter, making the rise in energy prices a boon for a large sector in

Canada’s economy.‛26

22 Credit Crunch Explained <http://www.mortgageguideuk.co.uk/blog/debt/credit-crunch-explained/> 23 Deloitte Research. Global Economic Outlook 2008 24 Economy In Crisis. Low Dollar: Not The Solution to Trade Deficit. 2007

< http://www.economyincrisis.org/articles/show/1159> 25Martin Frost. 2008 <http://www.politico.com/news/stories/0608/10940.html> 26 North American Economic Outlook Fall 2008 MFC Global Investment Management

44

Oil has witnessed a significant fall since July 2008 (almost $150 per/barrel). In early

December’08, oil was trading around $40 US a barrel. By the end of the month the price has

declined to $35 US a barrel.27 ‚On Dec.9, 2008, the U.S. Energy Information Administration

predicted that global demand for oil would fall through 2009, marking the longest contraction

in demand since the oil crisis of the 1970s.‛28 ‚International research firm CapGemini issued a

report on Nov. 24 2008, warning that low oil prices could mean trouble. The report suggested:

Low oil prices will render expensive projects no longer financially viable. This includes

the development of the Alberta oil sands

Cheap oil makes the development of renewable energy sources too expensive to be

worth the investment‛29

In its most recent world energy outlook, the International Energy Agency predicted that global

demand for energy would increase annually by 1.6 per cent until 2030, (about a 45 per cent total

increase from today’s demand). The agency notes that while there’s enough oil underground to

meet the demand, the supply in existing oil fields is declining too quickly to support the

demand. That means a lot more money will have to be devoted to oil exploration and

extraction. Merrill Lynch recently predicted that oil could fall as low as $25 per barrel, if the

recession is as deep or as long as some forecasters fear. That will spell trouble for oil-producing

provinces like Alberta and Newfoundland and Labrador. ‚If oil prices continue at below $60

US per barrel, we could be facing a deficit of several hundred million dollars next year and

could potentially be facing deficits in the years to come.‛ 30

Global Economics Imbalance

A July 2008 report produced by the Global Economic Research Division of the Scotiabank

Group suggested that ‚there is a significant risk that prolonged weak and unbalanced global

growth will heighten friction over trade and foreign direct investment, the principal sources of

global locomotion over the past two decades.‛31 A Deloitte Research study has examined how

the economic imbalance between the United States and China contributed to the housing bubble

in the North America. The bursting of the housing bubble is having important consequences for

the global economy. Among other things it was due to the imbalance that the global economy is

headed towards a recession in 2009.

27The Wall Street Journal. Oil Prices Slide Near Four-Year Low, 2008 28 Cheaper crude: who wins, who doesn’t

<http://www.cbc.ca/consumer/story/2008/12/09/f-oildecline.html> 29 Ibid 30 Ibid 31 Scotiabank. Global Economic Research Scotiabank Group, (July 2008)

45

Inflation

‚Inflation is one of the manifestations of the global crisis, and arises from changes in the

relationship between the volume of commodities and of money in the economy.‛32 Inflation is

driven by record high oil and food prices. Additional factors putting pressure on inflation

included excess capacity utilization and higher wages. In addition, many countries faced the

dilemma of choosing between controlling inflation or stimulating the economy through looser

monetary and fiscal policies. In the baseline outlook for 2009, inflation is expected to slow as

aggregate demand will continue to weak.33

Canada/America Economic Relationship

The Canadian economy’s competitiveness is directly linked to the strength of the relationship

with its closest and largest trading partner, the United States. Weaker American growth and

tighter credit limits have resulted in Canada’s economy falling into a recession. Economic

forecasts have projected zero growth during 2009. Even the most optimistic economic forecasts

predict that in general, Canadians will became poorer in 2009, and as many as 200,000 workers

will lose their jobs as the economic recession deepens.

Strong Domestic Demand and the Weaker Export Market

Canada is a developed nation that is highly dependent on international trade. The U.S.

economic downturn and slowdown has slowed the global economy and has reduced both the

demand and prices of Canadian commodities. The largest drag to real economic growth is a

continued weakness in the Canadian export sector, which accounts for approximately 40% of

the real economy.

Employment Growth

The sharp American slowdown constitutes further economic risks for Canada. The number of

Canadians who lost their jobs in December 2008 was more severe than analysts has expected.

As the recession deepens the Canadian unemployment rate is likely to increase.

32 Vasily Koltashov. 2008. Institute of Globalization and Social Movement. The Crisis of the global

economy. Moscow <http://www.metamute.org/en/the_crisis_of_the_global_economy> 33 United Nations. World Economic Situation and Prospects 2008 - Global Outlook 2008. New York:

United Nations, 2008.

46

Manitoba Economic Situation

Manitoba’s major industries include manufacturing, transportation, agriculture, hydro-

electricity, minerals, finance, and trade. It has recorded the most stable provincial economy in

Canada over the last decade. The Government of Manitoba’s most recent speech from the

throne outlined the provincial response to the growing global financial crisis by committing to

balance this year’s budget, while continuing to reduce personal, corporate, and small business

taxes. Initiatives to boost skills training and an investment of $4.7 billion in provincial

infrastructure over four years have been implemented in an effort to strengthen and grow the

economy and better position the province once stability returns to the world economy.

Although provincial growth is forecasted to slow across Canada, Manitoba’s economy is

forecasted to grow in 2009. Indicators suggest that Manitoba is well positioned to weather the

impacts of a global economic slowdown.

According to Statistics Canada, Manitoba is one of only three provinces that have generated 15

consecutive years of positive employment growth. Among these, Manitoba’s employment

growth has been the most consistent. Manitoba is also unique among provinces with 18

consecutive years of private investment growth. Manitoba’s geographic location has been an

important element in developing a diverse economy. Its economic stability is also rooted in its

relatively large service sector. The service sector tends to be more stable through the business

cycle relative to the goods-producing sector. In the last four years, no service industry in

Manitoba has posted any real decline.34

34 Manitoba Finance: Budget Paper A. The Economy (2008)

47

Economic Indicators

The economic performance indicators listed in this section capture a set of trends in the

economies of Canada and Manitoba between 2004 and 2008. Together, the indicators provide a

context for understanding why and when developments in the transportation sector have

occurred.

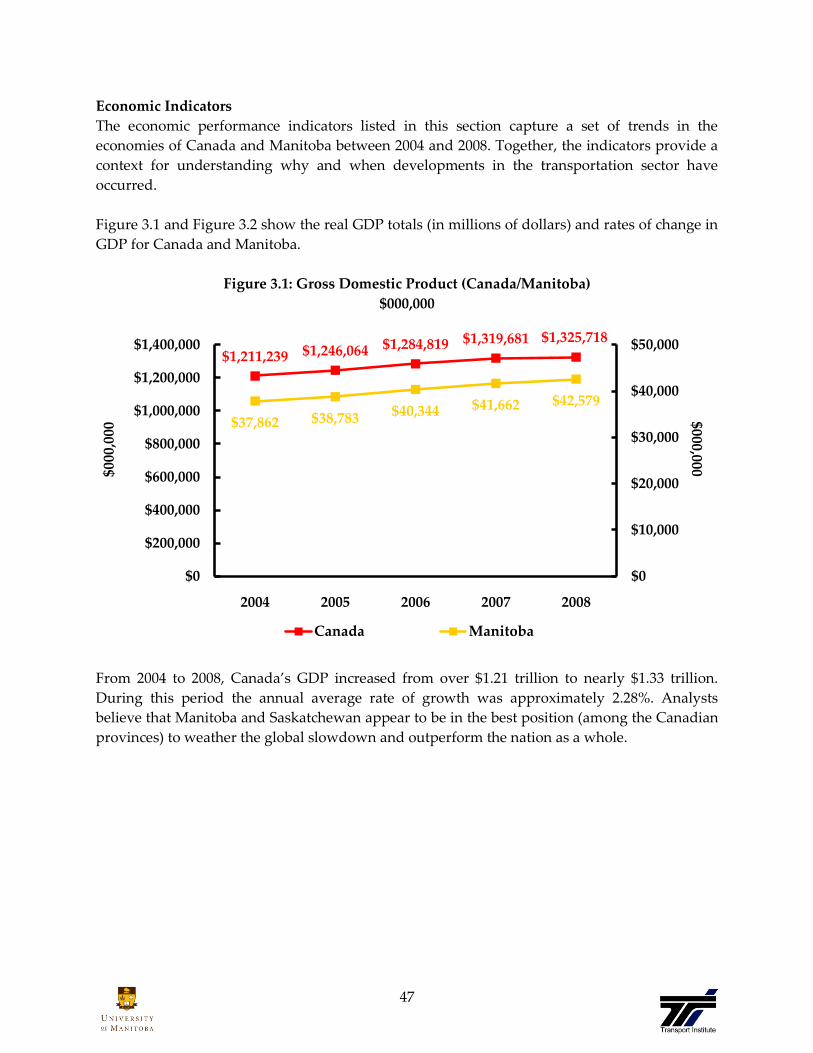

Figure 3.1 and Figure 3.2 show the real GDP totals (in millions of dollars) and rates of change in

GDP for Canada and Manitoba.

Figure 3.1: Gross Domestic Product (Canada/Manitoba)

$000,000

From 2004 to 2008, Canada’s GDP increased from over $1.21 trillion to nearly $1.33 trillion.

During this period the annual average rate of growth was approximately 2.28%. Analysts

believe that Manitoba and Saskatchewan appear to be in the best position (among the Canadian

provinces) to weather the global slowdown and outperform the nation as a whole.

$1,211,239 $1,246,064 $1,284,819 $1,319,681 $1,325,718

$37,862 $38,783 $40,344 $41,662 $42,579

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

2004 2005 2006 2007 2008

$000,000$0

00,0

00

Canada Manitoba

48

Figure 3.2 displays annual changes in the GDP growth rate. During the years of 2004 to 2007

national level of growth has fluctuated while the provincial growth has maintained a steady

overall increase, and in 2008 the rate of growth has dropped.

Figure 3.2: Change in GDP (Canada/Manitoba)

Economic indicators released in early 2008 confirm that the U.S. economy is indeed slowing.

Serious economic weakness in the U.S. has a negative impact on the Canadian economy as a

weaker export sector has spilled over into the non-export components of the Canadian

economy.35 Canadian GDP growth has seen a significant decline from 2007 to 2008, from 2.7% to

0.5%. Meanwhile Manitoba’s economic performance in the last three years has been

exceptionally strong. The GDP growth of Manitoba for the years of 2006 to 2008 has

outperformed the national average. Manitoba real GDP grew by 3.3% in 2007 above the

Canadian growth of 2.7%, and grew 2.2% in 2008 above Canadian growth 0.5%. In 2009,

Manitoba’s economy is expected to grow by 1.9%, above the Canadian growth of 0.8%.36

35 Manitoba Finance: Budget Paper A. The Economy (2008) 36 Manitoba Economic Highlights, 2008

3.1%2.9%

3.1%

2.7%

0.5%

2.2%2.4%

4.0%

3.3%

2.2%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2004 2005 2006 2007 2008

% C

han

ge

Canada Manitoba

49

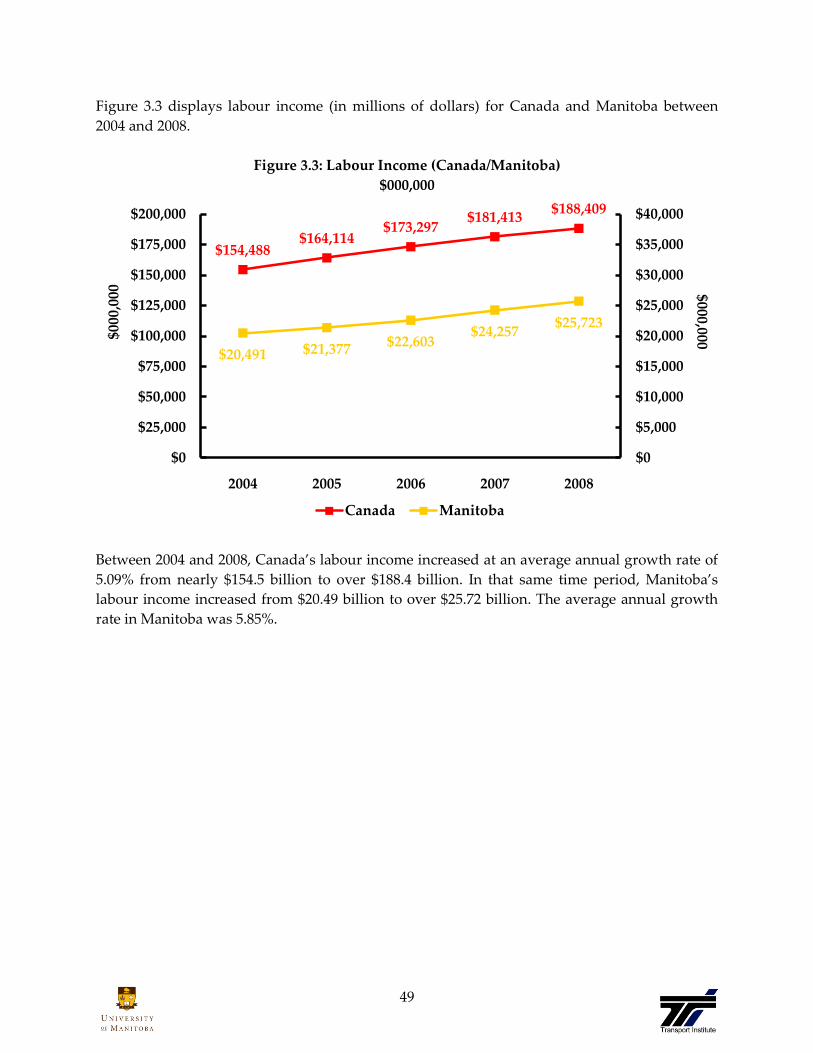

Figure 3.3 displays labour income (in millions of dollars) for Canada and Manitoba between

2004 and 2008.

Figure 3.3: Labour Income (Canada/Manitoba)

$000,000

Between 2004 and 2008, Canada’s labour income increased at an average annual growth rate of

5.09% from nearly $154.5 billion to over $188.4 billion. In that same time period, Manitoba’s

labour income increased from $20.49 billion to over $25.72 billion. The average annual growth

rate in Manitoba was 5.85%.

$154,488$164,114

$173,297$181,413

$188,409

$20,491 $21,377$22,603

$24,257$25,723

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$0

$25,000

$50,000

$75,000

$100,000

$125,000

$150,000

$175,000

$200,000

2004 2005 2006 2007 2008

$000,000$000

,000

Canada Manitoba

50

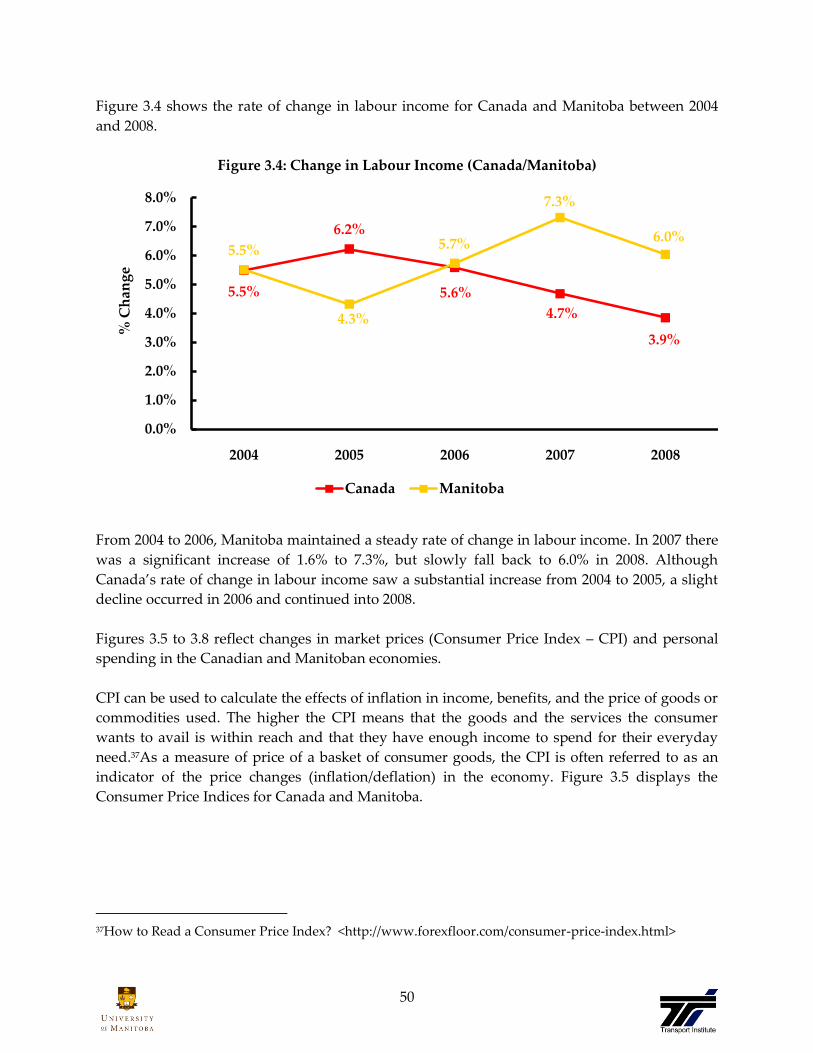

Figure 3.4 shows the rate of change in labour income for Canada and Manitoba between 2004

and 2008.

Figure 3.4: Change in Labour Income (Canada/Manitoba)

From 2004 to 2006, Manitoba maintained a steady rate of change in labour income. In 2007 there

was a significant increase of 1.6% to 7.3%, but slowly fall back to 6.0% in 2008. Although

Canada’s rate of change in labour income saw a substantial increase from 2004 to 2005, a slight

decline occurred in 2006 and continued into 2008.

Figures 3.5 to 3.8 reflect changes in market prices (Consumer Price Index – CPI) and personal

spending in the Canadian and Manitoban economies.

CPI can be used to calculate the effects of inflation in income, benefits, and the price of goods or

commodities used. The higher the CPI means that the goods and the services the consumer

wants to avail is within reach and that they have enough income to spend for their everyday

need.37As a measure of price of a basket of consumer goods, the CPI is often referred to as an

indicator of the price changes (inflation/deflation) in the economy. Figure 3.5 displays the

Consumer Price Indices for Canada and Manitoba.

37How to Read a Consumer Price Index? <http://www.forexfloor.com/consumer-price-index.html>

5.5%

6.2%

5.6%

4.7%

3.9%

5.5%

4.3%

5.7%

7.3%

6.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2004 2005 2006 2007 2008

% C

han

ge

Canada Manitoba

51

Figure 3.5: Consumer Price Index (Canada/Manitoba)

Between 2004 and 2008, the CPI for the Canadian economy increased from 124.6 to 135.8.

During this period the average annual growth rate was 2.18%. The CPI for Manitoba also

increased in the same time period from 127.8 to 139.6, with the average annual rate 2.23% per

year.

124.6127.3

129.9132.7

135.8127.8

131.2133.7

136.5139.6

100

110

120

130

140

2004 2005 2006 2007 2008

Ind

ex P

oin

ts

Canada Manitoba

52

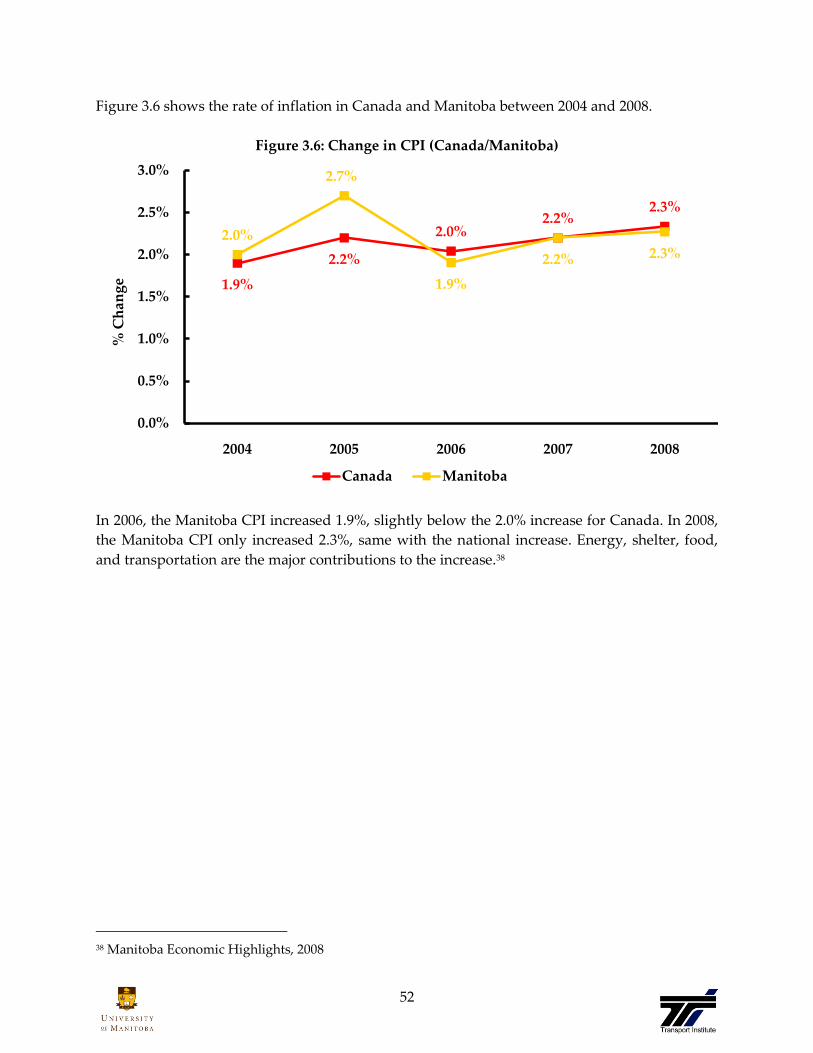

Figure 3.6 shows the rate of inflation in Canada and Manitoba between 2004 and 2008.

Figure 3.6: Change in CPI (Canada/Manitoba)

In 2006, the Manitoba CPI increased 1.9%, slightly below the 2.0% increase for Canada. In 2008,

the Manitoba CPI only increased 2.3%, same with the national increase. Energy, shelter, food,

and transportation are the major contributions to the increase.38

38 Manitoba Economic Highlights, 2008

1.9%

2.2%

2.0%2.2%

2.3%

2.0%

2.7%

1.9%

2.2% 2.3%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2004 2005 2006 2007 2008

% C

han

ge

Canada Manitoba

53

Figure 3.7 displays the changing value of personal expenditures in the Canadian and Manitoba

economies. Personal expenditures represent the portion of GDP that is contributed by the

consumption of consumer goods and services. These goods and services are meant to reflect

household expenditures.

Figure 3.7: Personal Expenditures (Canada/Manitoba)

$000,000

Canada’s personal expenditures increased to over $811 billion in 2008, an increase of over $23

billion from 2007. Between the years of 2004 to 2008 the average annual growth rate was 3.86%.

Manitoba’s personal expenditures increased to nearly $27.4 billion in 2008 from $23.6 billion in

2004 representing an annual average growth rate of 3.85%. Consumer spending will remain

firm as long as commodity prices don’t ‚fall through the floor‛.39

39 MFC Global Investment Management. North American Economic Outlook. (Fall 2008)

$697,566$723,181

$754,179$788,224 $811,690

$23,571$24,273

$25,063$26,311

$27,419

$10,000

$15,000

$20,000

$25,000

$30,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

2004 2005 2006 2007 2008

$000,000$0

00,0

00

Canada Manitoba

54

Figure 3.8 shows the trends in personal expenditures for Canada and Manitoba between 2004

and 2008.

Figure 3.8: Change in Personal Expenditures (Canada/Manitoba)

Canada’s rate of change in personal expenditures has slightly increased from 3.3% to 3.0% from

year of 2004 to 2008. During this same period Manitoba’s rate of change in personal

expenditures increased to 4.2% in 2008 from 3.1% in 2004. Robust income growth and a

booming labour market created a backdrop for strong domestic demand in Canada over the

past four years. It was largely expected that this wouldn’t last and that consumer spending

would slow from an unsustainable pace of 4-5%. Due to a national decrease in job creation,

income growth is expected to slow from 5.09% in 2008 to 2.5% in 2009, which will act as a

headwind to consumer spending.40

40TD Economics. TD Quarterly Economic Forecast. (2008)

3.3%3.7%

4.3%

4.5%

3.0%3.1% 3.0%3.3%

5.0%

4.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2004 2005 2006 2007 2008

% C

han

ge

Canada Manitoba

55

Figure 3.9 presents the number of housing starts in Canada and Manitoba between 2004 and

2008. The housing sector leads the Canadian and Manitoban economies.

Figure 3.9: Housing Starts (Canada/Manitoba)

000’s

In 2008 the number of Canadian housing starts declined to 845.300 from 911,000 in 2007 (a

change of approximately -0.7%). Despite fluctuations in the level of national housing starts

between the year of 2004 to 2008, Canada has a negative average annual growth rate of -2.38%.

The Manitoba housing market strengthened further in 2007 as housing starts achieved a two-

decade high and resale activity accelerated. Housing starts for Manitoba increased from 17,500

to 22,300 during the period of 2004 and 2008, resulting in an average annual growth rate of

6.25%.

930.7896.3 916.5

911.0845.3

17.518.8

20.2

23.0 22.3

0

5

10

15

20

25

0

200

400

600

800

1000

2004 2005 2006 2007 2008

000's000'

s

Canada Manitoba

56

Figure 3.10 shows the rate of change in housing starts in Canada and Manitoba between 2004

and 2008.

Figure 3.10: Change in Housing Starts (Canada/Manitoba)

Growth in Canada’s housing starts diminished with a negative growth rates of -3.7% in 2005,

the Canadian market recovered slightly with an of 2.3% in 2006, but recovered another negative

growth rate of -0.6% in 2007, in 2008 it dropped to -7.2% . Compared to Canadian housing

starts, Manitoban housing starts appear to be stable. From 2004 to 2007 the Manitoban level of

growth has increased annually from 5.4% to 13.9%. In 2008 the growth rate of housing starts in

Manitoba has declined to -3.0%.

6.0%

-3.7%

2.3%

-0.6%-7.2%

5.4%

7.4% 7.4%

13.9%

-3.0%

-10.0%

0.0%

10.0%

20.0%

2004 2005 2006 2007 2008

% C

han

ge

Canada Manitoba

57

Figure 3.11 displays the unemployment rate in Canada and Manitoba between 2004 and 2008.

Figure 3.11: Unemployment Rate (Canada/Manitoba)

Between year of 2004 to 2008, the national unemployment rate declined from 7.2% (2004) to 6.1

% (2008), an average annual rate of growth was -4.03%. In 2007 the Manitoba unemployment

rate experienced a 0.1% increase from 2006 4.4% prior to this, the province had experienced an

annual 2 year decline of approximately 0.5%. Overall, between 2004 and 2008 the

unemployment rate in Manitoba has fallen from 5.3% to 4.2%.

7.2%6.8%

6.3% 6.0% 6.1%

5.3%4.8%

4.3% 4.4% 4.2%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

2004 2005 2006 2007 2008

% o

f L

abo

ur

Fo

rce

Canada Manitoba

58

Figure 3.12 displays the change in the unemployment rate in Canada and Manitoba between

2004 and 2008. A negative number indicates a decrease in the unemployment rate, resulting

from an increase in employment.

Figure 3.12: Change in Unemployment Rate (Canada/Manitoba)

Canada has experienced a declining unemployment rate since 2004, decreasing by -0.4% in 2004

and further reducing to -0.5% in 2006. This was followed in 2007 with another decrease of -0.3%,

increased to 0.01% in year of 2008. According to a Statistics Canada report the unemployment

rate is at its lowest level in 33 years, with over 400,000 new jobs created since the end of 2006.

The Manitoban unemployment rate has fluctuated both positively and negatively between

years of 2004 to 2008.

-0.4%

-0.5% -0.5%

-0.3%

-0.02%

0.3%

-0.4% -0.5%

0.1%0.1%

-1.00%

-0.50%

0.00%

0.50%

1.00%

2004 2005 2006 2007 2008

% o

f L

abo

ur

Fo

rce

Canada Manitoba

59

Monetary and Energy Indicators